Meager Telco Capital Spending Entering New Era of Desynchronized Cycles; Dell’Oro & AT&T on CAPEX

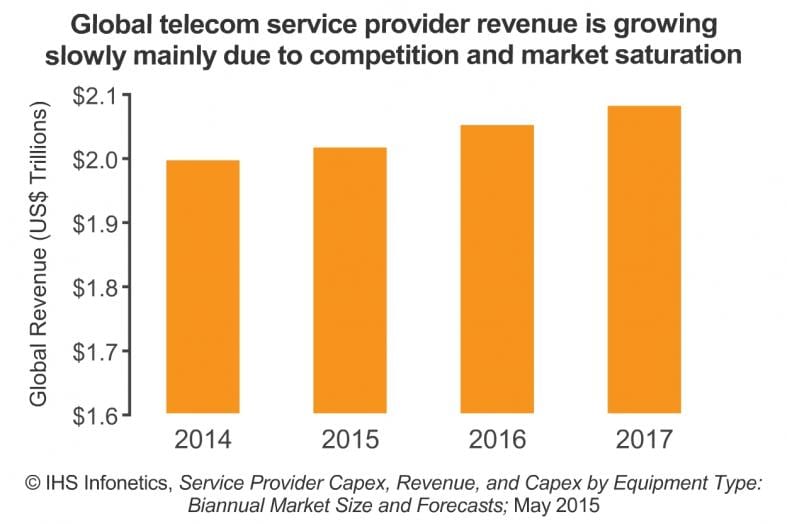

The latest IHS Infonetics Service Provider Capex, Revenue, and Capex by Equipment Type report notes that worldwide telecom service provider capital expenditures (CAPEX) grew 2.9% year-over-year in 2014, to US$352 billion.

CAPEX REPORT HIGHLIGHTS:

- In 2014, expenditures for every type of equipment except TDM voice slowly grew or stayed flat from the year prior.

- Europe posted 3.3% year-over-year growth in carrier CAPEX, mainly fueled by Deutsche Telekom and Vodafone.

- China more than offset spending declines in Japan and South Korea to drive Asia Pacific’s capex growth to 4.2 percent year-over-year in 2014.

- Meanwhile, a World Cup hangover slowed telecom spending in Latin America.

- IHS forecasts worldwide telecom capex to total a cumulative US$1.8 trillion in the 5 years from 2015 to 2019.

“We’re entering a new era of desynchronized cycles in telecom spending. Regions and economic powers have their own investment agendas and pace, and this will result in overall flat-to-low-single-digit capex growth through 2019 unless a major event occurs,” said Stéphane Téral, research director for mobile infrastructure and carrier economics at IHS.

CAPEX REPORT SYNOPSIS:

IHS Infonetics’ biannual service provider CAPEX report provides worldwide and regional market size, forecasts through 2019, analysis, and trends for revenue and capex by service provider type (incumbent, competitive, cable operators, independent wireless, satellite) and CAPEX by equipment type (broadband aggregation equipment; wireless infrastructure; IP routers and CES; optical equipment; IP and TDM voice infrastructure; video infrastructure; all other telecom/datacom network equipment; and CPE non-telecom/datacom network equipment).

To purchase the report, please visit: www.infonetics.com/contact.asp

RELATED RESEARCH

- Europe Exiting Optical Network Spending Slump

- Hotspot 2.0 and Virtualization Key to New Revenue for WiFi Carriers

- Carrier Voice-over-IP Market Off to Strong Start in 2015, Led by U.S.

- Mobile Operators Using EDGE, HSPA+ to Improve User Experience on Road to LTE

- Big Jump in Carrier WiFi Gear Expected as 802.11ac and Hotspot 2.0 Accelerate

From Dell’Oro Group’s Carrier Economics report: Dollar Strength to Wipe Out $20 B in Telecom Capex During 2015:

“We have not made any major changes to our constant currency Capex projections for 2015 and continue to expect the market will grow at a low-single-digit pace in 2015 driven primarily by China and Europe,” said Stefan Pongratz, Dell’Oro Group Carrier Analyst. “But in U.S. Dollar terms, assuming rates remain at current levels, the strengthening U.S. Dollar will unequivocally impact Telecom Capex, and we have revised our 2015 Capex in U.S. Dollar terms downward rather significantly to adjust for currency fluctuations,” continued Pongratz.

AT&T says by 2020, 75% of its network will be software-centric, with the use of network functions virtualization and software defined networking (SDN) technologies. Note however, that AT&T’s definition of SDN has nothing to do with the original definition which includes strict separation of data & control planes, centralized controller with a global view of the network (not just adjacent network elements), use of Open Flow API/protocol as the Southbound API from the control to data planes. AT&T is NOT a member of the Open Network Foundation that is specifying SDN architectures and protocols.

As part of AT&T’s ongoing Domain 2.0 effort, about 40% of its strategic IT applications have been migrated to the cloud, with an ongoing process of one application to be migrated a day. According to the company, that move has enabled greater operational efficiencies over applications running on dedicated hardware. In addition, about 400,000 processor cores are running the cloud IT apps and operating 50% more efficiently than on dedicated hardware, the company claims.

AT&T expects future networking deployments to further reduce capex over the next five years. “This is a big opportunity for change and will allow us to look at our network model in a different way,” said Susan Johnson, senior vice president of global supply chain at AT&T.