Huawei widens lead in broadband CPE market; VDSL Vectoring to the Rescue!

Infonetics Research released excerpts from its 1st quarter 2013 (1Q13) Broadband CPE and Subscribers: PON, FTTH, Cable, and DSL market share, size and forecasts report, which tracks digital subscriber line (DSL), cable and fiber to the home (FTTH) customer premises equipment (CPE), residential gateways and broadband subscribers.

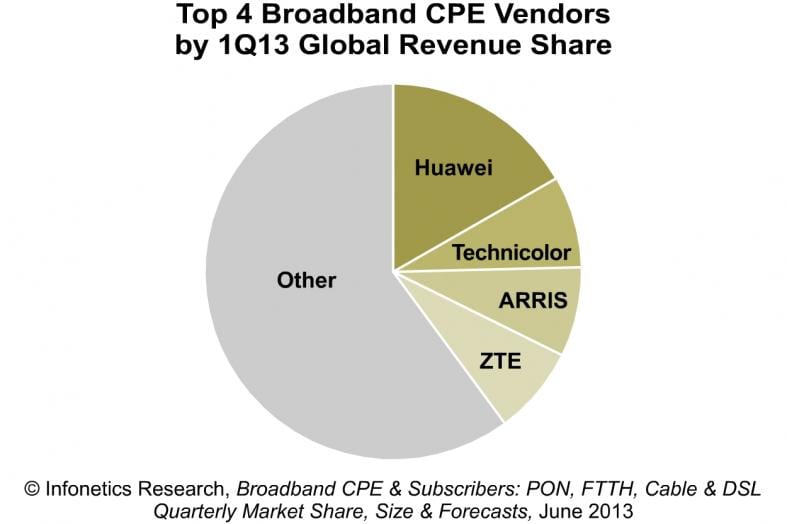

1Q13 BROADBAND CPE MARKET HIGHLIGHTS:

- Owing to the continued strong growth of FTTH and cable CPE, the global broadband CPE market hit $2.2 billion in 1Q13, an increase of 6% sequentially and 17% from the year-ago quarter .

- Though the overall DSL CPE market is slowing on an annual basis, VDSL CPE continues to enjoy strong growth (+30% YoY), particularly in North America and EMEA (Europe, Middle East, Africa ).

- Broadband CPE share leader Huawei pulled farther away from the pack in 1Q13, thanks to a 26% spike in revenue coming mostly from China , Singapore and Malaysia, where it is the primary supplier of GPON ONTs and ADSL CPE.

- Former #2 ZTE slipped to 4th place, leapfrogged by Technicolor and Arris .

- Pace’s share of the broadband CPE market continues to grow, and Infonetics expects it to challenge for a place in the top 3 this year.

- Headless video gateways are forecast by Infonetics to grow at a 117% compound annual growth rate (CAGR) from 2012 to 2017

“Better than expected sales of higher-end cable CPE, including headed and headless video gateways being sold in North America and Europe, helped the broadband CPE market put up another strong quarter,” notes Jeff Heynen, principal analyst for broadband access and pay TV at Infonetics Research. Heynen adds: “Operators across multiple verticals are in the middle of a long-term transition to higher-speed broadband technologies like FTTH, DOCSIS 3.0 and VDSL2 to keep up with subscriber demand for multiscreen video.”

REPORT SYNOPSIS:

Infonetics’ quarterly broadband CPE report provides worldwide and regional market size, vendor market share, forecasts through 2017, analysis and trends for ADSL and VDSL modems, gateways and IADs; standard and DOCSIS 3.0 cable modems, gateways and EMTAs; FTTH ONTs and gateways; residential gateways; PON and Ethernet FTTH ports; and broadband subscribers. Companies tracked: Alcatel-Lucent, Arris, AVM, Cisco (Linksys, Scientific Atlanta), Comtrend, D-Link, Dasan Networks, Fiberhome, Hitron, Huawei, Mitsubishi, Motorola, Netgear, OF Networks, Pace, Sagemcom, SMC Networks, Sumitomo, Telsey, Technicolor, TP-Link, Ubee Interactive, Zhone, ZTE, Zyxel and others.

To buy report, contact Infonetics at: http://www.infonetics.com/contact.asp

Reference: http://www.infonetics.com/newsletters/Broadband-Access-June-2013.html

Comments on VDSL:

After 10 years (1996-2006) of slow growth and unfilled potential, VDSL-based CPE grew 30 percent year-over-year in North America and EMEA. For network operators that have a large base of copper plant, VDSL2 has become a viable near-term option to deliver higher speed services and video.

Three major telcos, including AT&T, Deutsche Telekom and Telecom Italia, have outlined large-scale build out plans that will continue through the year 2016. AT&T’s Project VIP will extend U-Verse and IP DSLAM FTTN coverage by 8.5 million homes by 2015, while Deutsche Telekom will increase VDSL coverage to 65 percent by 2016. Telecom Italia will deploy fiber to the cabinet to 6.1 million homes in 100 cities by the end of 2014.

Unlike ADSL which uses ATM and AAL5 as a L2 framing, almost all VDSL/VDSL2 uses Ethernet MAC frames and Unnumbered Information (UI) Frames for Layer 2 (Data Link layer. Hence, we see an increase of more Ethernet compatible gear in the home, small office and telco central office (e.g. IP/Ethernet DSLAMs).

More importantly, VDSL got a new lease on life through the concept of “vectoring,” which was co-invented by IEEE ComSocSCV member George Ginis. Check out his excellent paper on that topic:

Vectored DSL to the Rescue

http://www.ospmag.com/issue/article/vectored-dsl-rescue

Congrats George!