Month: July 2017

BT offers to spend up to £600M on rural broadband in the UK

BT has offered to spend up to £600M to connect the final 1M homes and businesses in rural areas of Britain to a broadband connection suitable for most needs. The telecom company said every home and business in the UK would have a broadband speed of at least 10 megabits per second (Mbits/s), fast enough to stream movies, video conference and browse the web.

Broadband endpoints will either be connected via the Openreach network through fiber-optic cables, a network of copper lines via xDSL, or through the fixed broadband wireless system, where connections use radio and, in some cases, satellite signals.

BT’s plan is for 99% of the UK population to be able to obtain a broadband service of at least 10 Mbit/s by 2020. That speed meets the needs of a typical household, according to UK regulatory authority Ofcom, but is less than the 2015 FCC broadband speed minimum of 25M bit/s (downstream).

About 93% of the UK population can already access a service of at least 24 Mbit/s, according to the UK government, but there has been concern about a growing “digital divide” as rural communities miss out on the broadband revolution.

The government said it was weighing BT’s proposal against a regulatory approach. “We warmly welcome BT’s offer and now will look at whether this or a regulatory approach works better for homes and businesses,” said Culture Secretary Karen Bradley in a weekend statement. “Whichever of the two approaches we go with in the end, the driving force behind our decision making will be making sure we get the best deal for consumers.”

Actual network construction is not due to finish until late 2021 or 2022, because of work on the rollout of fixed network technologies.

The UK government said rollout would take longer under a regulatory approach but highlighted the pricing implications of BT’s plan for rivals and broadband consumers.

“It is also proposed that BT would fund this investment and recover its costs through the charges for products providing access to its local access networks,” it said. “The approach to recovering these costs will be considered in Ofcom’s current wholesale local access review.”

Gavin Patterson, CEO of BT, said:“ We are pleased to make a voluntary offer to deliver the Government’s goal for universal broadband access at minimum speeds of 10Mbps. This would involve an estimated investment of £450m — £600m depending on the final technology solution.”

At the top end of this range, the investment would equal about 2.5% of BT’s revenues in its last fiscal year (to end-March 2017) and about 17% of overall capital expenditure across the Group.

BT said it would look to recover the cost of its investment by leasing the rural networks to its rivals. The offer will also be reflected in Ofcom’s current review of how to regulate the market for super fast, fiber-based networks of the future.

Capex soared by about £3.5 billion ($4.6 billion) at BT last year, largely because of spending on broadband roll outs. BT is planning several major investments in the coming years: it plans to extend all-fiber networks to around 2 million UK premises by 2020, and connect another 10 million homes and businesses to a xDSL technology called G.fast, which boosts connectivity speeds over last-mile copper loops. (See BT to Cover 2M Homes With FTTP in $8.7B Plan.)

Earlier this month, BT CEO Patterson said he was considering the viability of a much more ambitious fiber roll out that would benefit around 10 million premises by 2025. (See BT Rejigs Consumer Biz as Profits Hit by £225M Italy Payout.)

He has also indicated that BT will participate in an upcoming auction of airwaves that could be used to support new 5G services. Operators made crippling payments for spectrum licenses during previous auctions, although experts do not expect a 5G auction to generate a similar windfall.

References:

https://www.ft.com/content/a4ba67a4-73b0-11e7-aca6-c6bd07df1a3c

http://www.itproportal.com/news/bt-unveils-600m-scheme-to-bring-broadband-to-every-rural-uk-home/

TBR Analysis of Verizon’s 2nd Quarter Results + Earnings Call Remarks

Unlimited data boosts Verizon’s phone net additions though wireless margins continue to diminish

by Steve Vachon, TBR Analyst

In 2Q17 Verizon was able to report consolidated year-to-year revenue growth (+0.1%, on a historical, non-adjusted basis) for the first quarter since 1Q16, but this was mainly due to $693 million in revenue generated from acquisitions that have closed in the past year, including Fleetmatics, Telogis and, most recently, Yahoo, which closed on June 13, 2017.

Verizon’s core businesses continue to feel the weight of pricing pressures and market saturation within the mobility, video and business services markets. These trends are exemplified by wireless revenue remaining in decline (-1.9% year-to-year) despite the recent launch of unlimited data, competition from over the top (OTT) preventing Fios video subscriber additions and growth within Verizon’s new Business Markets unit being largely contingent on the XO Communications acquisition.

The launch of Verizon’s unlimited data plans in February boosted postpaid phone net additions, totaling 358,000 in 2Q17 compared to 86,000 in 2Q16, as more customers are shifting to unlimited data for its convenience and to support increasing mobile video usage. TBR believes the price point of Verizon’s unlimited plans is also benefiting subscriber growth while minimizing average revenue per user (ARPU) declines as they strike a happy medium, starting at a lower price point than AT&T’s Unlimited Plus program, competing on-par with multiline T-Mobile One Plus plans without yielding to the overly aggressive pricing of Sprint’s Unlimited Freedom promotions.

Maintaining sufficient LTE capacity is critical as the carrier is continuing to rely on its reputation of providing superior network coverage as its primary differentiator to attract unlimited data coverage. TBR believes Verizon is well-positioned to sustain its unlimited data strategy long term as currently only 50% of its spectrum is being used for LTE and the company can continue to add network capacity via small cells, deploying AWS-3 licenses and refarming 3G licenses for LTE. However, Verizon’s network distinctions are becoming less pronounced as competitors continue to densify their networks and move towards 1Gbps data speeds by implementing LTE-Advanced technologies, which will require Verizon to implement new differentiators to stand out in the unlimited data market.

Despite the success of Verizon’s unlimited data plans, wireless EBITDA margins fell for the third-consecutive quarter in 2Q17, declining 170 basis points year-to-year to 45.8%. Verizon’s diminishing wireless (profit) margins are in part due to the carrier’s shift to a non-subsidy device pricing model as decreased equipment subsidies are failing to offset service revenue declines stemming from lower-priced wireless plans offered under this model. Postpaid ARPU is also being limited by Verizon Plan features including Carryover Data and Safety Mode that are helping tiered data customers conserve data usage. Conversely, TBR anticipates the adoption of unlimited data plans will mainly have a stabilizing effect on postpaid phone ARPU over the next year as migrations from customers on less expensive plans will be offset by the cost savings heavy overage customers will realize by transitioning to unlimited data.

Highlights of Verizon’s Earnings Call Transcript:

Matthew D. Ellis – Verizon Communications, Inc.

We had a strong quarter of execution. First, we invested in our 4G network leadership position, resulting in a sweep of third-party network performance surveys for the first half of 2017, while prepositioning for 5G services. Second, we delivered solid wireless operational performance and financial results in a competitive environment with an increase in both postpaid and prepaid accounts. Third, we successfully completed the acquisition of Yahoo’s operating assets to scale our media business.

Network leadership is the central element of our strategy, and we are continually investing in our network to extend our leadership in 4G capacity growth with densification using small cells, which includes expanding our fiber capabilities. As we prepare for the network of the future, we announced the acquisition of Straight Path for $3.1 billion, which we expect will close by the end of first quarter 2018. Straight Path complements our spectrum portfolio and positions us to lead and further drive 5G technology and its ecosystem. We have begun the pre-commercial fixed wireless trials in eight out of the 11 markets and have our first batch of customers on this technology. As we have previously highlighted, we will have trial results later in the year, and I look forward to sharing them with you.

We had a strong quarter, adding and retaining wireless customers as the momentum from the launch of our unlimited plans was sustained throughout the quarter. We delivered a strong wireless operational performance that reflects customer demand for our high-quality network in a highly competitive market. Finally, we completed the acquisition of Yahoo’s operating assets and immediately began executing on integration plans that we’ve been working on for over a year. We are confident in the execution of our strategy, which we expect to drive profitable growth, generate strong cash flows, and return long-term value to our shareholders.

Total wireline revenue on a reported basis grew 1.2%, including the recently acquired XO operations. On an organic basis, wireline segment revenue decreased 2.8% compared to a decline of 3.2% last quarter. This shift in the wireline revenue trend towards fiber is growing. Organically, fiber based products grew more than 3%, which supports our plans to further invest in fiber. Our emphasis on delivering value to all business customers, from the very small to the large enterprise, was recognized recently in a leading third-party study. More importantly, we won the large enterprise business award for the second consecutive year in the same study.

Consumer markets revenue increased 0.6%, driven by Fios Internet activity. Consumer Fios revenue growth of 4.1% was consistent with the past several quarters. During the quarter, we launched Fios Gigabit Connection in certain markets, which offers symmetrical speeds of up to 1 gigabit per second. In Fios Internet, we added 49,000 customers. Fios Video results were pressured due to softer secular demand for traditional linear video, given growth in the over-the-top offerings, as well as competitive promotional activity. Fios Video losses were 15,000 in the quarter. For the second quarter, Enterprise Solutions revenue fell 4.1% on an organic basis, which was due to persistent trends in our legacy products and pricing compression in the marketplace. On a constant-currency basis, revenue was down 3.5%.

Partner Solutions revenue declined 6.8% on an organic basis, while the revenue mix towards fiber has been trending higher. Within business markets, fiber revenue is expanding, driven by Fios broadband demand, offset by continued pressure in legacy products. On an organic basis, revenue declined 4.9% and improved slightly sequentially.

On a comparable basis, the second quarter wireline EBITDA margin was 20.8%, compared to 13.3%, which included the work stoppage, last year. Sequentially, wireline EBITDA margin was down 120 basis points, primarily due to lower revenue from Enterprise Solutions and Partner Solutions and an increase in operating expense as a result of leasing data center space related to the sale to Equinix.

…………………………………………………….

Commentary from Fierce Wireless:

Whether Verizon can maintain its network edge in an era of unlimited data is unclear, however. Recent data from Ookla indicates that the networks of both Verizon and AT&T have suffered as traffic has ramped up in recent months, as T-Mobile recently pointed out. So Verizon must continue to move quickly to meet the ever-increasing demands of consumers as mobile data traffic soars.

“Subscriber trends recovered sharply this quarter; however, this is partly due to an aggressive push behind unlimited that we don’t think is sustainable for Verizon,” New Street Research analysts said in a note to investors. “They have the least capacity per sub of all the carriers, and their network performance is already deteriorating both in absolute terms and relative to peers. Verizon is also paying for improved subscriber trends with ARPU and service revenue pressure. The recovery in subs is also partly due to record low churn across the industry in general, which we suspect will reverse later in the year with the new iPhone launch.”

TBR: AT&T Improves Profitability Despite Declining Revenues & Price Pressures

Below is TBR’s commentary on AT&T’s 2Q17 earnings. Contact Steve Vachon at +1 (603) 929-1166 or [email protected] for additional commentary.

For content reuse and media usage guidelines, please see TBR terms of use.

AT&T is improving its value proposition as competition within the mobile and video markets intensify

AT&T’s consolidated revenue fell 1.7% year-to-year to $39.8 billion in 2Q17 due to declines across all of the company’s core businesses, with the exception of its International division. AT&T’s profitability improved in the quarter, however, as operating margins rose 220 basis points year-to-year to 18.4%, aided by the company’s emphasis on non-subsidized wireless device plans.

Pricing pressures, smartphone saturation and stronger competition from OTT providers are creating obstacles for AT&T to grow its mobility and video businesses, which is spurring the carrier to become more reliant on bundles combining both services to improve its value proposition. Though TBR believes AT&T trailed all of its Tier 1 competitors in postpaid phone net additions in 2Q17, the launch of its unlimited data plans helped to mitigate declines as the carrier’s postpaid phone losses improved in the quarter to -89,000, compared to -180,000 in 2Q16.

In June AT&T Unlimited Choice customers gained the option to add DirecTV Now to their accounts for $10 per month, a benefit previously offered only to Unlimited Plus customers. TBR believes the move will boost wireless and DirecTV subscriber additions, but will come at the expense of limiting postpaid phone ARPU as customers now have less incentive to select AT&T Unlimited Plus plans, which have a starting price point that is $30 more expensive than Unlimited Choice plans.

AT&T is relying on the low price point and flexibility of DirecTV Now, which gained 152,000 customers in 2Q17, to help offset declines within its U-verse TV and DirecTV satellite businesses, which lost a combined 351,000 subscribers in the quarter. Though AT&T increased Video Entertainment revenue by 2.1% year-to-year in 2Q17, TBR believes sustaining revenue growth in the segment will be increasingly challenging as total video subscribers decrease and the company trades linear TV subscribers for lower ARPU DirecTV Now connections.

New features such as the inclusion of additional live local channels and upcoming 4K HDR and cloud DVR support provide added incentives to attract DirecTV Now customers, but addressing the platform’s streaming capacity is critical as recent service interruptions will drive some subscribers to switch to rivals such as SlingTV and Hulu Live.

AT&T deepens emphasis on the public sector and software-mediated network services to improve Business Solutions revenue

To improve Business Solutions revenue, which decreased 2.7% year-to-year in 2Q17 due primarily to lower legacy voice and data revenue, AT&T is targeting growth from government customers. In April AT&T announced it is consolidating its government and education operations, which generated about $15 billion in sales in 2016, into the new Global Public Sector division to improve cohesiveness and foster partnerships across agencies in different sectors. Additionally, AT&T will be able to provide first responders with more reliable connectivity through its collaboration with First Net, which has already attracted contracts from five states as of July.

AT&T will improve the profitability of Business Solutions long-term by adopting NFV and SDN technologies. Integrating open-source technologies and white box hardware will provide cost savings by enabling the carrier to become less dependent on more costly, proprietary infrastructure. Additionally, TBR expects the acquisition of Brocade’s Vyatta network operating system will enable AT&T to meet its goal of virtualizing 75% of its network by 2020.

In addition to cost savings, AT&T is creating revenue streams by introducing new software-mediated network services to its portfolio, including an upcoming SD-WAN service in collaboration with VeloCloud. However, AT&T will be disadvantaged by its relatively late entry into the SD-WAN market as competitors including Verizon and CenturyLink have already begun to cement leading positions within the segment.

…………………………………………………………………………………………………………

References:

http://edge.media-server.com/m/p/gz5k2iq4/lan/en (Recording of earnings call)

J.D. Power: SMB a Growth Opportunity; Telecom ARPU Falling in Every Region

J.D. Power Report Highlights:

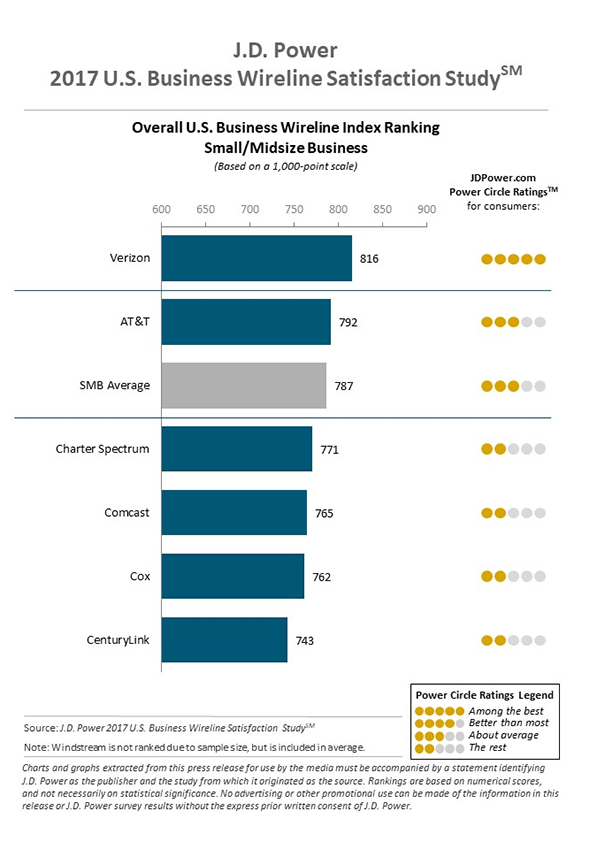

Enterprises with 500 or more employees are more likely to be satisfied with their telecom service, according to a report from J.D. Power, which sees the small- to medium-size business market as a growth opportunity for telcos. Medium-size businesses had an average satisfaction score of 787, J.D. Power said in a press release.

The J.D. Power report, which grades larger telecoms and cable companies, gives Verizon and AT&T the highest marks.

Verizon exceeded the average satisfaction level and topped the rankings for all three categories of businesses – small, mid-size and large. The company’s overall scores were 762, 816 and 821, respectively, for small, mid-size and large companies.

AT&T came in second place and exceeded the average score in the mid-size and large categories, with scores of 792 and 820, respectively. But Cox came in second among the smallest businesses, with a score of 744. AT&T followed at 730.

Cox was the only cableco to have a score above the average in any of the three categories. Among the telcos, CenturyLink also failed to have a score above the average in any category – a situation that company will want to address whenever its merger with Level 3 closes and the company becomes the most enterprise-focused of all the major service providers.

J.D. Power attributes the higher satisfaction level of the larger businesses to several factors, including higher satisfaction levels with communication, cost of service and customer service. Those companies with an account representative assigned to their business have notably higher overall satisfaction, researchers noted – and larger companies are more likely to have account representatives assigned to them.

Service providers in general have been emphasizing the business market in recent years and that emphasis seems to be yielding positive results. Scores for all the categories of companies were higher than for a similar study that J.D. Power conducted in 2015. Scores for 2015 were 783 for large companies, 747 for mid-size companies and 715 for small companies.

The business market has been a particularly strong focus for cable companies, which do not have wireless businesses but do have modern fiber network infrastructure. The J.D. Power results suggest cable companies still have a way to go in gaining business customers’ loyalty and trust, however.

The J.D. Power results suggest opportunities for service providers that can excel at serving SMBs – and tier two service providers such as Windstream and Frontier have been focusing on that market for a long time. So was TW Telecom (which was acquired by Level 3, which is in turn being acquired by Century Link) and XO Communications which was acquired by Verizon.

Tier two telcos were not included in the J.D. Power report.

…………………………………………………………………………………………

Telecom ARPU Falling in Every Region

Closing Comment:

Perhaps, the negative growth in telecom is causing telcos to merge to acquire scale and to go into other businesses (like Orange investing in on-line banking instead of its core telecom business).

Fierce Telecom reported on July 24th:

CenturyLink, Frontier, Windstream suffer worst 3 quarters in history

CenturyLink, Frontier and Windstream have continued to see pressure over the past three quarters as shares at each of these companies dropped dramatically due to issues at each company.

“Shares in the wireline ILEC/RLEC space (CenturyLink, Frontier, Windstream) have endured the worst three consecutive quarters in industry history, with shares plummeting an average of -20% in 4Q16, -21% in 1Q17, and -24% in 2Q17 (we note another -5% in 3Q17 thus far), mostly from Frontier and Windstream as CenturyLink shares are being supported by the Level 3 acquisition,” Cowen said in a research note.

Overall, the three companies face the industry-wide challenge of balancing strategic service growth with ongoing legacy service declines and losing market share to cable operators.

Additionally, each of these companies has been dealing with specific headwinds in their businesses. Frontier has been challenged by integrating the properties it purchased from Verizon in California, Texas and Florida, while CenturyLink is dealing with a raft of lawsuits over alleged consumer fraud issues and Windstream is seeing declines in its legacy TDM-based wholesale business sector.

References:

http://www.jdpower.com/sites/default/files/2017108.pdf

AT&T: Latency sensitive, next-gen apps need Edge Computing & We’re All In!

AT&T strongly advocates the use of edge computing (EC) as a way to reinvent the telco network and cloud so as to make new services like augmented reality, virtual reality, and low latency “5G” applications practicable.

The company’s CTO wrote in a blog post that it is adding intelligence to its cell towers, central offices, and small cells that are at the “edge” of the cloud by outfitting them with high-end graphics processing chips and other general purpose computers. By doing so, it will reduce the distance that data has to travel to get processed, thereby reducing latency and boosting overall network performance.

“Edge computing fulfills the promise of the cloud to transcend the physical constraints of our mobile devices,” said Andre Fuetsch, president of AT&T Labs and CTO in a statement. “The capabilities of tomorrow’s “5G” are the missing link that will make edge computing possible.” That’s because many “5G” applications require low latency, especially for real time control of machinery and Internet connected devices (IoT).

AT&T said it will begin deploying edge computing out over the next few years starting with urban areas and expanding those over time. The company also said that MEC is an important element to the company’s network virtualization program. The company’s goal is to have 55 percent of its network virtualized by year-end with a longer term goal of having 75 percent of its network virtualized by 2020.

The above referenced AT&T blog post identified the challenge and solution for next-gen applications:

Here’s the challenge: Next-gen applications like autonomous cars and augmented reality/virtual reality (AR/VR) will demand massive amounts of near-real time computation.

For example, according to some third-party estimates, self-driving cars will generate as much as 3.6 terabytes of data per hour from the clusters of cameras and other sensors. Some functions like braking, turning and acceleration will likely always be managed by the computer systems in the cars themselves.

But what if we could offload some of the secondary systems to the cloud? These include things like updating and accessing detailed maps these cars will use to navigate.

Or consider AR/VR. The industry is moving to a model where those applications will come through your smartphone. But creating entirely virtual worlds or overlaying digital images and graphics on top of the real world in a convincing way also requires a lot of processing power. Even when phones can deliver that horsepower, the tradeoff is extremely short battery life.

Edge computing addresses those obstacles by moving the computation into the cloud in a way that feels seamless. It’s like having a wireless supercomputer follow you wherever you go.

………………………………………………………………………………………………………………………

AT&T said that it’s already deploying EC-capable services to enterprise customers today through AT&T FlexWareSM service. Customers can currently manage powerful network services through a standard tablet device. We expect to see more applications for EC in areas like public safety that will be enabled by the FirstNet wireless broadband network.

The company claims to be committed to deploying mobile 5G as soon as possible and are committed to edge computing. As AT&T rolls out EC over the next few years, dense urban areas will be their first targets, and they’ll expand from those over time.

In conclusion, AT&T stated “we’re all in- now (for edge computing)” as per these strong closing remarks:

AT&T Labs and AT&T Foundry innovation centers are at the heart of designing and testing edge computing. In February, the AT&T Foundry in Palo Alto, CA, released a white paper on the computing and networking challenges around AR/VR. We’ll put out a second white paper in the coming weeks. It will discuss how we can apply edge computing to enable mobile augmented and virtual reality technology in the ecosystem.

There’s no time to lose. We think edge computing will drive a wave of innovation unlike anything seen since the dawn of the internet itself. Stay tuned.

…………………………………………………………………………………………………………………………..

Other network operators have been touting multi-access edge computing (MEC) in conjunction with “5G” networks. Late last year, 5G Americas, a trade group representing several operators in North and South America (including AT&T), released a white paper about the growing interest in MEC and said that standards bodies like the 3GPP and ETSI are considering including MEC in the 5G standards development.

ETSI has formed the Multi-access Edge Computing Industry Specification Group (MEC ISG). Earlier this month, ETSI released its first package of standardized application programming interfaces (APIs) that will support MEC interoperability.

……………………………………………………………………….

References:

http://about.att.com/story/reinventing_the_cloud_through_edge_computing.html

https://www.wirelessweek.com/news/2017/07/t-turns-edge-computing-vr-other-5g-use-cases

Telecom Italia “5G” trial to blanket San Marino in 2018

According to the Financial Times (on line subscription required):

Telecom Italia plans to test its home grown “5G” technology in the micro-state of San Marino next year, making it the first country in the world to boast a nationwide 5G network. The state of San Marino, which has little more than 30,000 citizens, extends to only 61 sq km, making it the smallest republic in the world.

Telecom Italia Mobile (TIM) has signed a memorandum of understanding with the government of the tiny country to upgrade the existing 4G-LTE network in advance of a trial of “5G” services in 2018. It will double the number of mobile sites and will install a network of small cells in downtown San Marino, a Unesco heritage site, this year that will provide the backbone of the future commercial network. Investment in 5G network trials are taking place around the world with carriers in South Korea, China and the US among the most active in testing 5G technology. Giovanni Ferigo, head of technology for Telecom Italia Mobile, said San Marino’s 5G network would be the first in Europe “for sure.”

It was not revealed who created the specs for the Italian telco’s “5G” network or where Telecom Italia will procure the end point devices/handsets. One would assume that Ericsson is supplying TIM with the “5G” base stations, based on a MOU signed between the two companies in March of this year. TIM wrote in a press release on March 2, 2017:

TIM and Ericsson are committing to share skills, projects, laboratories and resources for designing, testing and building the technological components of the new 5G network needed to create a complete and open ecosystem around next-generation digital services.

In particular, the agreement will directly involve the research and innovation structures of the two companies, focusing on the design and testing of access infrastructure, the respective antenna systems and network virtualisation solutions, particularly through joint participation in Italian and European research projects and integration of service platforms for testing in the field of innovative Use Cases.

The 5G system will provide peak speeds of up to dozens of Gbps for UltraHD services and cloud computing solutions, a decrease in communication latency, reducing it to a few milliseconds, reliability for mission-critical services and service density with the ability to connect up to a hundred thousand terminals per cell. These characteristics mean that 5G will become the reference mobile network for next-generation digital services (such as virtual reality) and for the industrial Internet (robotics, manufacturing, health, environment, self-driving logistics).

The agreement is part of the “5G for Italy” initiative launched in 2016 by TIM and Ericsson for the establishment of an ecosystem of experimental industrial partners, confirming the commitment of the two companies to innovating technologies and networks in support of the socio-economic growth of the country.

…………………………………………………………………………………………..

Telecom Italia is also testing “5G” in Milano and Torino, but has more freedom in San Marino to experiment because of fewer restrictions on the use of airwaves than in Italy.

“We need to experiment as soon as possible,” Mr Ferigo said. The work done in San Marino would play a critical role in the future of 5G technology in Italy but was also crucial to the wider European sector as standards for the new network are refined.

“For 5G, our intention is a European leadership in standardization,” he said. The European Commission published a 5G action plan last year when it estimated that sectors such as healthcare, transport, cars and utilities would see economic benefits of €113bn by 2025 from the technology. However, the European Commission does not generate any telecom standards. For Europe, that’s ETSI which contributes to 3GPP and its members contribute to ITU-R WP 5D which is standardizing true 5G (as we’ve noted in numerous blog posts/articles).

Earlier this year, Telecom Italia Mobile (TIM) said LTE customers are expected to account for around 90% of its mobile broadband customers by 2019; That’s due to almost blanket LTE coverage of Italy with network speeds up to 75 Mbps and peaks of 500 Mbps in the main cities via the use of LTE Advanced Carrier Aggregation.

The above referenced FT “5G” article states:

Some countries have committed to the first 5G launches in 2019 but the wider telecoms industry is still struggling to define exactly what 5G technology is and some have argued that it is not yet clear how they can justify spending billions on the new network.

Mr Ferigo said the San Marino launch would be “very important” in defining the use case for 5G that would transform all sectors from healthcare to robotics to public transport. Telecom Italia has started working with companies including Maserati and Ducati on the use of better wireless technology but also the makers of parmesan cheese who want to better monitor the cows in their fields. Small territories have been used in the past for telecoms testing. The first 3G trial in the UK took place on the Isle of Man, while the remote Isle of Bute in Scotland was used to test “white space” technology.

Copyright The Financial Times Limited 2017. All rights reserved.

……………………………………………………………………………………….

References:

http://www.telecomitalia.com/tit/en/archivio/media/note-stampa/market/2017/PN-TIM-Turin-5G-Day.html

https://www.ericsson.com/assets/local/publications/white-papers/wp-5g.pdf

https://www.ericsson.com/en/news-and-events/press-center/media-kits/5g

Verizon trial validates NG-PON2 interoperability via its OpenOMCI specification; 5G backhaul spending

Verizon reported a successful trial of next-generation passive optical networking NG-PON2 technology using the carrier’s OpenOMCI specification. The OpenOMCI specification is aligned with ITU-T Recommendation G.989.3, but there are different versions from several carriers.

It’s important to note that this is Verizon’s own version of the OpenOMCI spec. Verizon, along with ADTRAN, Broadcom, Cortina Access, Ericsson/Calix and Intel, worked together to develop the OpenOMCI specification that led to the successful trial. The specification defines the OLT-to-ONT interface and is aligned with the ITU-T Recommendation G.989.3. Since the initial NG-PON2 trial by Verizon in December 2016 , these companies intend to make their hardware and software compliant and are actively contributing to the OpenOMCI specification.

AT&T also published an OpenOMCI specification just a few weeks ago, based on ITU-T G.988 Managed Entities. AT&T intends to deploy an XGS-PON architecture as part of the overall FTTP solution for its Lightspeed service, hence its OpenOMCI spec differs from Verizon’s FiOS-based one. XGS-PON is championed by Nokia (who is not part of Verizon’s vendor group) and also delivers 10Gbit/s to customers.

The trial at Verizon’s technology center in Waltham, MA involved optical network terminal management and provisioning.

By outlining the tools necessary to model a multi-wavelength PON, Verizon says the OpenOMCI specification optimises the number of managed entities and methods that can be used to implement a particular service function while disallowing vendor-proprietary objects and features that have provided a major obstacle for interoperability efforts until now. The OpenOMCI also includes specific managed entities that, in Verizon’s opinion, improve the stability of PON systems. With today’s PON deployments, telcos are obliged to use the same vendor for both optical line terminals (OLT) and optical network terminals (ONT) which prevents multi-vendor interoperability.

“The NG-PON2 interoperability effort is important, not only for Verizon but for NG-PON2 technology, and is based on lessons learned over the last 13 years of PON deployment and great partnerships,” said Vincent O’Byrne, PhD and director of technology at Verizon. “We see this work as removing a major roadblock and helping accelerate NG-PON2 deployment.”

O’Byrne told FierceTelecom that the OpenOMCI specification will help to ensure the company can deploy an array of OLTs and ONTs in its network. He said:

“Since October 2016 we have been working with the vendors on enabling interoperability to mix and match one vendor’s OLT with another vendor’s ONTs, which is an object we have had since we started deploying BPON in 2004. “We have been working with these vendors and have developed OpenOMCI communications between the OLT and the ONT and how that issue is handled for NG-PON2.”

Along with ONT management and provisioning, the trial investigated transmission convergence layer features that allow support of not only business and residential traffic but wireless transport services. These features are a unique addition to NG-PON2 compared to other PON systems.

“We continuously sought the various contributors’ feedback and constructive input,” said Denis Khotimsky , Distinguished Member of the Technical Staff and Verizon’s lead engineer for the trial. “NG-PON2 technology creates specific challenges for the management layer to handle, such as multi-wavelength operations, pluggable optics and multiple interface enhancements. The Verizon OpenOMCI specification meets those challenges.”

Representatives of several telcos interested in the NG-PON2 technology – including Deutsche Telekom, SK Telecom and Vodafone – participated in the trial as virtual observers, which gave them access to the specification, test plans and readouts.

Following the successful completion of the trial, Verizon shared its OpenOMCI specification with the industry for possible inclusion within the appropriate standards. A copy of Verizon OpenOMCI specification can be found here.

References:

http://www.telecompetitor.com/verizon-partners-demonstrate-key-ng-pon2-interoperability-milestone/

http://www.fiercetelecom.com/telecom/verizon-completes-openomci-interoperability-testing-for-ng-pon2

………………………………………………………

Addendum: On July 18th, Fierce Telecom reported: 5G backhaul spending to reach $2B by 2022, NG-PON2 to dominate

“The technology that will dominate 5G backhaul will be NG-PON2,” CIR stated. “By 2022, more than $890 million will be spent on this technology for 5G backhaul.”

The analyst firm noted that Verizon has selected NG-PON2 for 5G backhaul. Top vendors, including Cisco, Nokia, Huawei, Calix, Adtran, Ericsson and Alcatel-Lucent all have PON solutions for 5G backhaul.

NG-PON2 should remain the most popular technological choice, provided prices come down as expected, based on the development of less costly tunable components, CIR said. Most of the suppliers of those components will be based in China, the firm expects.

CIR also calculated that more than 170,000 fiber miles (280,000 kilometers) of cable is expected to be shipped for 5G backhaul applications in 2022, with major fiber and cable suppliers such as Corning already showing signs of specifically targeting 5G infrastructure with their products.

The firm also noted that the introduction of high-speed wireless may have the side effect of reducing the need for fiber to the premise/home (FTTP/FTTH).

There will be some short-term uncertainty until 5G standards are finally ratified, but CIR concluded that “5G is potentially a massive opportunity for the fiber optics industry, with this taken to include opportunities for the makers of modules and components as well as the fiber/cable manufacturers themselves.”

Microsoft White Spaces Plan would bring 2 million Americans online by 2022

Microsoft today announced a project to bring broadband internet access to rural parts of the U.S. using TV white spaces, unlicensed and unused spectrum. Microsoft President Brad Smith unveiled details about the initiative at a Tuesday event in Washington, D.C. as a way to bridge the digital divide between urban and rural areas.

Microsoft’s ambitious plan, dubbed the Rural Air-band Initiative, will begin in 12 states, where the company said it will invest in broadband connectivity alongside local telecom services. The company said that it does not intend to enter the telecom business itself or profit directly from the initiative. Instead, Microsoft said it will supply the upfront capital required to expand broadband coverage, then recoup that cost by sharing in the revenue with local operating partners.

The company is calling for a combination of private and public investments to get about 2 million rural Americans online in the next five years. Microsoft plans to partner with telecommunications companies that serve rural counties in 12 states: Wisconsin, Michigan, North Dakota, South Dakota, Kansas, Washington, Texas, Arizona, Georgia, Virginia, New York and Maine. It’s also asking for regulatory support from the Federal Communications Commission.

Mr. Smith will also urge President Donald Trump and his administration to ensure that unlicensed white space is available in all U.S. markets. “As a country, we should not settle for an outcome that leaves behind more than 23 million of our rural neighbors,” Smith wrote in a blog post.

“To the contrary, we can and should bring the benefits of broadband coverage to every corner of the nation,” he added. Smith said the TV white spaces provides powerful bandwidth to allow wireless signals to travel over hills and through buildings and trees.

“Today, 34 million Americans still lack broadband internet access, which is defined by the Federal Communications Commission as a 25 Mbps connection,” Smith posted. “Of these, 23.4 million live in rural parts of our country. People who live in these rural communities increasingly are unable to take advantage of the economic and educational opportunities enjoyed by their urban neighbors.” Smith said Microsoft wants to eliminate the rural broadband gap by July 4, 2022.

“Our goal is to serve as a catalyst for market investments by others in order to reach additional rural communities,” he stated in his blog post.

Microsoft company faces many hurdles with the technology. For one, few manufacturers are making devices compatible with white-spaces technology, and some devices that can be used with the technology cost more than $1,000 each. The National Association of Broadcasters, a trade group, said that only 800 devices that worked with white-spaces technology had been registered with regulators.

“White spaces has tremendous opportunity to help with broadband coverage in rural areas, but it’s hard to justify the cost to device makers who don’t see economies of scale in rural areas,” said Doug Brake, a senior analyst at the Information Technology & Innovation Foundation, a research organization that is sponsored by tech companies including Microsoft.

Mr. Smith said that he would demonstrate four devices that work with white-space technology at Tuesday’s event, adding that prices for such gadgets would fall below $200 by next year.

Another challenge is a battle with television broadcasters who have long argued that devices on the unused airwaves can interfere with the broadcasts run on neighboring channels. This week, the National Association of Broadcasters filed comments with the Federal Communications Commission arguing against Microsoft’s request for one nationwide channel to be set aside for white-spaces use.

“Microsoft has been making promises about white-spaces technology for well over a decade,” Patrick McFadden, an associate general counsel for the association, wrote in comments to the commission. “At what point do we finally conclude that the white spaces project is a bust?”

References:

https://www.microsoft.com/en-us/research/project/dynamic-spectrum-and-tv-white-spaces/

http://whitespaces.microsoftspectrum.com/

https://www.theverge.com/2017/7/11/15953310/microsoft-rural-airband-broadband-strategy

http://www.detroitnews.com/story/tech/2017/07/11/rural-broadband-microsoft/103618818/

https://www.microsoft.com/en-us/research/project/networking-over-white-spaces-knows/

China Orders Telecom Companies To Block VPN Access to Global Internet

China’s government has reportedly directed telecommunications companies to block their users from accessing a secure internet network.

The country’s authorities are specifically mandating that state-run wireless carriers — like China Telecom, China Unicom and China Mobile — forbid people from using virtual private networks (VPNs). China is giving the quasi-private companies until Feb. 1, 2018 to comply with its orders, according to Bloomberg.

The technological capability gives users the ability to navigate the web anonymously through an encrypted, secure connection.

VPNs enable Chinese citizens with the ability to circumvent the country’s firewall (also known as the Great Firewall of China), which technically prohibits people from accessing many online services and sites that are available on the global internet. Social media sites like Facebook and Twitter, for example, are not accessible due to the firewall, so many Chinese citizens use Sina Weibo, a similar platform that is based in China and adheres to government’s calls for targeted censorship.

China’s propensity towards censorship manifests itself quite often, in fact, including in late June when the popular Netflix original “BoJack Horseman” was blocked just days after debuting in the country. (RELATED: China Battles For Internet Hegemony After America Gives Up Control)

“In the past, any effort to cut off internal corporate VPNs has been enough to make a company think about closing or reducing operations in China. It’s that big a deal,” Jake Parker, vice president of the U.S.-China Business Council, told Bloomberg.

“VPNs are incredibly important for companies trying to access global services outside of China,” he said, adding that the order also seems to affect individuals across the country.

References:

https://en.wikipedia.org/wiki/Internet_censorship_in_China

http://www.cnbc.com/2017/07/10/china-bans-vpns-to-further-tighten-internet-controls-says-report.html

https://www.theguardian.com/world/2017/jul/11/china-moves-to-block-internet-vpns-from-2018

https://www.bloomberg.com/news/articles/2017-07-10/china-is-said-to-order-carriers-to-bar-personal-vpns-by-february

Overview & Schedule for ITU-R WP 5D: IMT 2020 True “5G” Standards

Overview of ITU-R Working Party 5D work (as per July 5, 2017 report):

Working Party 5D:

1. Is responsible for the overall system aspects of the terrestrial component of IMT, comprising IMT-2000, IMT-Advanced, and IMT for 2020 and beyond.

2. Has the prime responsibility within ITU-R for issues related to the terrestrial component of IMT, including technical, operational and spectrum related issues to meet the objectives of future IMT systems.

3. Is the lead group for the overall maintenance of existing and the development of new Reports/Recommendations on IMT.

4. Is responsible for studies related on aspects regarding the continued deployment of IMT‑2000 and IMT-Advanced including aspects such as convergence impacts regulatory and operational matters within the purview of Study Group 5.

5. Will continue to work closely with Working Parties 4B and 4C on issues related to the satellite component of IMT.

6. Will continue to work closely with other Working Parties on issues relevant for IMT systems.

……………………………………………………………………………………………….

Scopes for the various ITU-R WP 5D Working Groups:

WG GENERAL ASPECTS:

– To develop deliverables on services, forecasts, and also convergence of services of fixed and mobile networks which take account the needs of end users, and the demand for IMT capabilities and supported services. This includes aspects regarding the continued deployment of IMT, other general topics of IMT and overall objectives for the long-term development of IMT. To update the relevant IMT Recommendations/Reports.

– To ensure that the requirements and needs of the developing countries are reflected in the work and deliverables of WP 5D in the development of IMT. This includes coordination of work with ITU-D Sector on deployments of IMT systems and transition to IMT system.

WG TECHNOLOGY ASPECTS:

– To provide the technology related aspects of IMT through development of Recommendations and Reports. To update the relevant IMT‑2000 and IMT-Advanced Recommendations. To work on key elements of IMT technologies including requirements, evaluation, and evolution. To develop liaison with external research and standardization forums, and to coordinate the external and internal activities related to the IMT-2020 process.

– To manage the research topics website and its findings.

WG SPECTRUM ASPECTS:

– To undertake co-existence studies, develop spectrum plans, and channel/frequency arrangements for IMT. This includes spectrum sharing between IMT and other radio services/systems coordinating as appropriate with other Working Parties in ITU-R.

AD HOC WORK PLAN:

– To coordinate the work of WP 5D to facilitate efficient and timely progress of work items.

…………………………………………………………………………………………………………………………………

Meeting schedule

The following table shows the proposed meeting dates for Working Party 5D following on WRC‑15. Some adjustment of these dates might be required to accommodate availability of facilities at specific venues. Every effort will be made to keep these dates as listed. Please check the ITU website in case meeting details have changed. (http://www.itu.int/events/monthlyagenda.asp?lang=en)

|

GROUP |

No. |

FROM |

TO |

PLACE |

COMMENTS |

|

WP 5D |

23 |

23 February 16 |

2 March 16 |

China |

7 working day meeting |

|

WP 5D |

24 |

14 June 16 |

22 June 16 |

Geneva |

7 working day meeting |

|

WP 5D |

25 |

5 October 16 |

13 October 16 |

Geneva |

7 working day meeting |

|

WP 5D |

26 |

14 February 17 |

22 February 17 |

Geneva |

7 working day meeting |

|

WP 5D |

27 |

13 June 17 |

21 June 17 |

Canada |

7 working day meeting |

|

WP 5D |

28 |

3 October 17 |

11 October 17 |

Germany |

7 working day meeting, including a one-day workshop |

|

WP 5D |

29 |

31 January 18 |

7 February 18 |

[Korea] |

|

|

WP 5D |

30 |

13 June 18 |

20 June 18 |

[TBD] |

|

|

WP 5D |

31 |

9 October 18 |

16 October 18 |

[Japan] |

|

|

WP 5D Expert meeting |

31bis |

[11 February 19] |

[15 February 19] |

[TBD] |

If needed. Focus of meeting towards RA-19 and WRC-19 |

|

CPM19-2 |

– |

18 February 19 |

28 February 19 |

Geneva |

|

|

WP 5D |

32 |

9 July 19 |

17 July 19 |

[TBD] |

7 working day meeting |

|

RA-19 |

– |

21 October 19 |

25 October 19 |

Geneva |

|

|

WRC-19 |

– |

28 October 19 |

22 November 19 |

[Egypt] |

|

|

WP 5D |

33 |

[9 December] 19 |

[13 December] 19 |

[TBD] |

Focus meeting on evaluation (WG Technology Aspects) |

|

WP 5D |

34 |

19 February 20 |

26 February 20 |

[TBD] |

|

|

WP 5D |

35 |

24 June 20 |

1 July 20 |

[TBD] |

|

|

WP 5D |

36 |

7 October 20 |

14 October 20 |

[TBD] |

………………………………………………………………………………………………………………………………..

Work with involved organizations, including research entities:

The strategy for ITU-R WP 5D going forward is to gather information from the organizations involved in the global research and development and those that have an interest in the future development of IMT and to inform them of the framework and technical requirements in order to build consensus on a global level.

ITU-R WP 5D can play an essential role to promote and encourage these research activities towards common goals and to ensure that information from the WP 5D development on the vision, spectrum issues, envisioned new services and technical requirements are widespread among the research community. In the same manner, WP 5D encourages inputs from the external communities involved in these research and technology developments.

It is evident that continuing dialogue between the ITU and the entities taking part in research is a key to the continuing success of the industry in advancing and expanding the global wireless marketplace.

Working Party 5D, as is the case with all ITU organizations, works from input contributions submitted by members of the ITU. In order to facilitate receipt of information from external entities who may not be direct members of ITU, the Radiocommunication Bureau Secretariat may be considered as the point of interface, in accordance with Resolution ITU-R 9‑5.

The following major activities are foreseen to take place outside of the ITU, including WP 5D, in order to successfully complement the WP 5D work:

– research on new technologies to address the new elements and new capabilities of IMT‑2020;

– the ongoing development of specifications for IMT and subsequent enhancements.

………………………………………………………………………………………

Agreed overall deliverables/workplan of WP 5D

The following table provides the schedule of when approval of the planned major deliverables will be achieved following the procedures of WP 5D.

|

October 2017 |

TBD WP 5D #28 |

• Finalize revision of Recommendation ITU-R M.2012 • Liaison Reply to Task Group 5/1 |

|

February 2018 |

TBD WP 5D #29 |

• Finalize input to WP 1A on WRC-19 agenda item 1.15 • Finalize CPM text on WRC-19 agenda item 9.1, issue 9.1.1 • Finalize draft new Report ITU-R M.[IMT.MS/MSS.2GHz] |

|

June 2018 |

TBD WP 5D #30 |

• Finalize CPM text on WRC-19 agenda item 9.1, issue 9.1.8 (MTC) • Finalize draft new Report ITU-R M.[IMT.EXPERIENCES] • Finalize draft new Report ITU-R M.[IMT. MTC] • Further update/Finalize draft new Report/Recommendation ITU-R • Finalize input to WP 4A on WRC-19 agenda item 9.1, issue 9.1.2 |

|

October 2018 |

TBD WP 5D #31 |

• Finalize draft new Report ITU-R M.[IMT.1452-1492MHz] • Finalize draft new Report/Recommendation ITU-R M.[IMT.3300 MHz RLS] • Finalize draft new Recommendation ITU-R M.[MT.3300 MHz FSS] • Finalize draft new Report/Recommendation ITU-R M.[IMT.COEXISTENCE.AMS] • Finalize draft revision of Report ITU-R M.2373 • Finalize revision of Recommendation ITU-R M.1036 • Finalize draft new Report ITU-R M.[IMT.BY.INDUSTRIES] • Finalize revision of Recommendation ITU-R M.1457 |

|

July 2019 |

TBD WP 5D #32 |

• Finalize Doc. IMT-2020/YYY Input Submissions Summary • Finalize Addendum 4 to Circular Letter IMT‑2020 |

|

October 2019 |

TBD WP 5D #33 |

|

|

February 2020 |

TBD WP 5D #34 |

• Finalize Doc. IMT-2020/ZZZ Evaluation Reports Summary • Finalize Addendum 5 to Circular Letter IMT‑2020 |

|

June 2020 |

TBD WP 5D #35 |

• Draft new Report ITU-R M.[IMT-2020.OUTCOME] • Finalize Addendum 6 to Circular Letter IMT‑2020 |

|

October 2020 |

TBD WP 5D #36 |

• Finalize draft new Recommendation ITU-R M.[IMT‑2020.SPECS] • Finalize Addendum 7 to Circular Letter IMT‑2020 |

…………………………………………………………………………………………………………………………………

Detailed timeline and process for Technology related work stream towards IMT-2020:

Working Party 5D has developed a work plan, timeline, process and required deliverables for the future development of IMT, necessary to provide by 2020 timeframe, the expected ITU-R outcome of evolved IMT in support of the next generation of mobile broadband communications systems beyond IMT-Advanced.

Circular Letter(s) are expected to be issued at the appropriate time(s) to announce the invitation to submit formal proposals and other relevant information.

It has been agreed that the well-known process and deliverable formats utilized for both IMT-2000 and IMT-Advanced should be utilized also for IMT-2020 and considered as a “model” for the IMT‑2020 deliverables to leverage on the prior work.

…………………………………………………………………………………………………………………

Dates have been decided for RA-19 (21-25 October 2019) and WRC-19 (28 October – 22 November 2019).

The WP 5D #32 (July) is the main meeting for year 2019.

The WP 5D #33 is to be held in December with a focus on the evaluation process (WG Technology Aspects).

If needed there is an opportunity for expert meeting to focus on preparation towards WRC-19 (WG General Aspects and WG Spectrum Aspects) prior to the WP 5D #32 (July).

Click on above image to enlarge. Source: ITU-R WP5D report, 5 July 2017

………………………………………………………………………………………………

Reference:

Timeline for IMT 2020 (5G) Radio Access Recommendations + Evaluation Methodology