Month: January 2019

AT&T Extends Fiber Footprint, Grows Wireless Network; Identifies 2019 Strategic Initiatives

AT&T’s fiber footprint continues to grow. On yesterdays 4Q2018 earnings call, AT&T CFO John Stephens said: “We now passed more than 1 million customer locations with fiber and are on our way to hit the 40 million locations later this year. This will extend our fiber network to 22 million locations when include business. Subscribers on our fiber network increased by more than 1 million last year, driving the number of total broadband customers in our fiber footprint to substantially more than 3 million, and the longer we have fiber in the market the higher our penetration rates go.,,This performance is helping drive broadband revenue growth.”

AT&T CEO Randal Stephenson added: “We also accelerated our fiber deployment and we now reach a 11 million customer locations in addition to 8 million business locations. As a result, our broadband business grew by over 6% in the quarter and it’s really important to note that this fiber deployment is foundational to our 5G network.”

During the Q&A session, Stephenson said: “we will finish the lion share of the fiber build by mid-year. We’ll be at 14 million locations passed with our fiber footprint. You’re seeing now the impact as we move our customers into the fiber footprint. You’re not seeing the overall broadband subscribers grow, but as people migrate to fiber you’re seeing a significant lift in ARPU. We had 6% broadband growth in the fourth quarter with no overall subscriber growth. We added about 250,000 fiber customers roughly.”

………………………………………………………………………………………………………………………………………………………………………………………………

In the communications segment, AT&T’s largest business, the carrier and media giant gained a net 134,000 phone subscribers who pay a monthly bill, falling far short of analysts’ estimates of 208,000, according to research firm FactSet. AT&T has 153 million total phone subscribers. Churn, or the rate of customer defections, was 1 percent during the fourth quarter, up from 0.89 percent the previous year.

Stephenson played up AT&T’s wireless network when he said: “In terms of our networks, our quality and performance are on a very strong trajectory. GWS named us the best network and the most comprehensive study that’s been conducted. We introduced the first standards based mobile 5G network in parts of 12 cities last month and our first net deployments finished the year well ahead of schedule.”

During the Q&A, he added: “I will say over time three to five year time horizon unequivocally 5G will serve as a fixed broadband replacement product. I am very convicted that that will be the case. We are obviously on a standards-based path. We want a standards-based path that is mobile (5G) first, but just like every other product evolution and mobility this will play out the same.”

“Will you have enough capacity with 5G to have a good broadband product that serves as a streaming service for all of your DIRECTV NOW, your Netflix, etc? I absolutely am convinced that we will have that capacity, particularly as we turn up millimeter wave spectrum. That’s where the capacity and the performance comes from and that’s where you’ll begin to see a broad – a true replacement opportunity for fixed line broadband. So I have little doubt that in the three to five year time horizon you’ll start to see substitution of wireless for fixed line broadband.”

With respect to AT&T’s 5G Evolution (which is really 4G+), Stephens said: “We also made significant strides in our (5G, but really 4G+) network of evolution in the fourth quarter. Randall told you about our network leadership (referred ti as “standards based 5G;” yet the IMT 2020 standard won’t be completed till late 2020 at the earliest) in 5G introduction. With the additional spectrum we’re adding, carrier aggregation and other network improvements, 5G evolution is producing better speeds for our customers today when compared to standard LTE. Our first net deployment is reaching critical mass and providing a tailwind for our results.”

During the Q&A session Stephens added: “We’re seeing the effects of 5G evolution be real and in customers hands today which is making a difference. We do have about 450,000 FirstNet qualified customers from about 5000 organizations or departments that have signed up for it. A significant amount of those early adopters were migrations, so maybe close to two thirds or 60% or so, but we are now getting a lot of new ads. And as this build out gets passed the existing 40% in the 50%, 60% and 70% so to speak as we continue make that progress, I think you’ll see us begin to grow that new customer share and numbers significantly.

So we really do view that as a tailwind for the whole business as it improves existing customers quality, speed, throughput, but it also gives us visibility which we’ve been successful at, our teams had a good job with gaining new customers.”

![]()

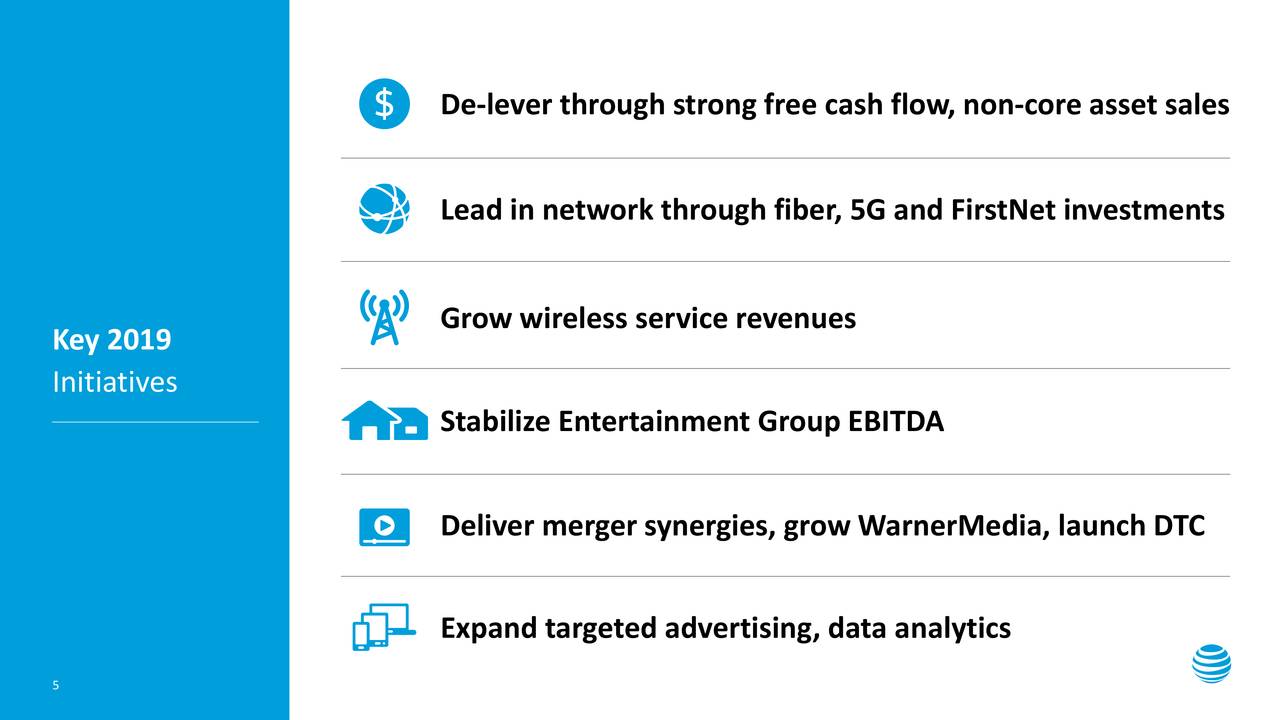

Here are AT&T’s strategic goals for 2019:

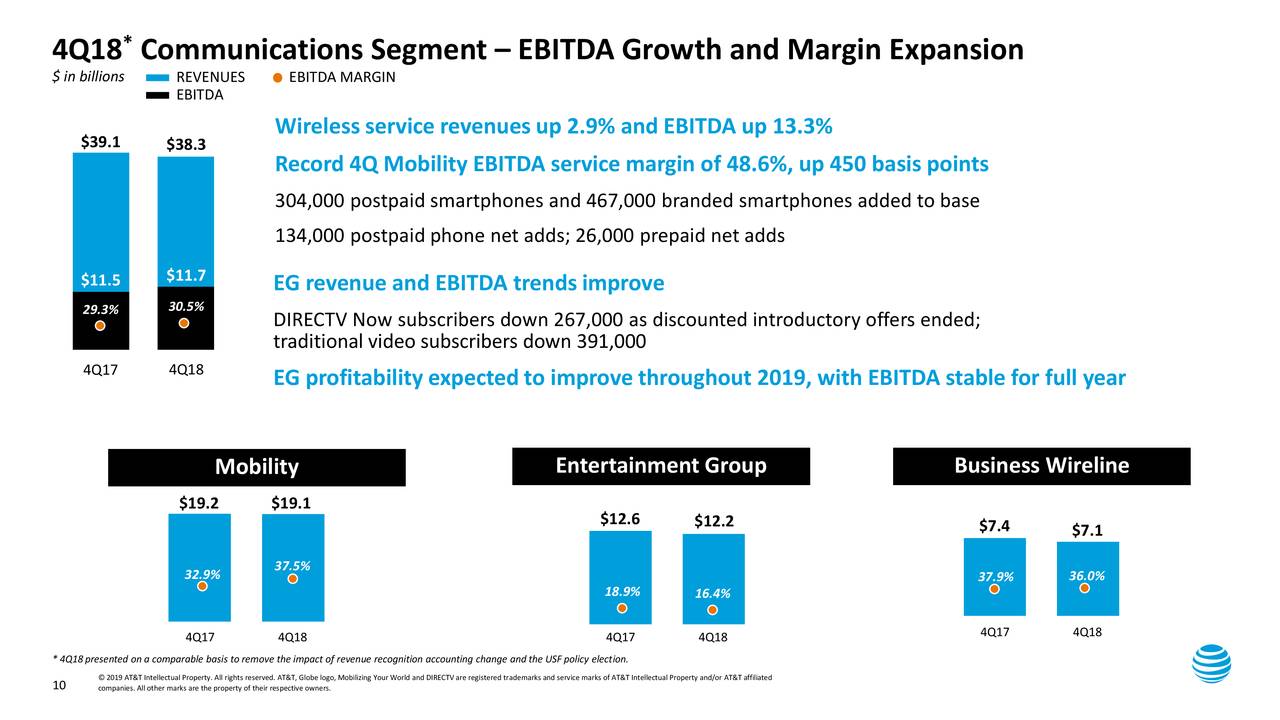

Here are the 4Q2018 Results of AT&T’s Communications business:

Analyst Opinions:

AT&T’s revenue of $47.99 billion missed estimates of $48.5 billion. AT&T also reported net additions of 134,000 phone subscribers, below analyst estimates of 308,000. The company also lost 403,000 satellite TV subscribers and 14 percent of its DirecTV Now streaming subscribers in the quarter.

Bank of America analyst David Barden said that, despite the quarter’s shortcomings, AT&T is moving in the right direction. “Within the wireless business, which accounts for 50% of total EBITDA, service revenue grew, net adds were positive, and EBITDA beat by a material amount as the handset upgrade rate was much lower than expected,” Barden wrote.

Raymond James analyst Frank Louthan said AT&T is prioritizing deleveraging its balance sheet in 2019 and should be able to hit its 2.5 times target by the end of the year. “We believe the video sub trends will be offset as marketing packages with mobility and FirstNet take hold and drive improved profitability per sub, but this could take time for investors to see the signs,” Louthan wrote.

Morgan Stanley analyst Simon Flannery said there were some encouraging signs for investors in the fourth quarter, but AT&T has limited near-term financial visibility as it digests its Time Warner acquisition.

IHS Markit 5G Smartphone Whitepaper; Analysts on Samsung’s Feb. 20 Galaxy 10 Launch?

IHS Markit 5G Smartphone Whitepaper:

In a new complimentary white paper, “Substance behind the Hype: 5G Smartphones Primed and Ready for Fast Rollout,” IHS Markit explores how the global 5G transition is poised to take place at a faster pace than for any previous wireless generation transition. “It is easy to paint the current momentum behind 5G as the usual pre-launch hype drummed up by vested stakeholders,” said Wayne Lam, principle analyst for IHS Markit and lead author of the white paper. “However, the mobile industry is fundamentally better prepared and more aligned with a common standard than at any previous technology transition.”

Industry uncertainly adds friction to development and discourages firms from making big bets when the outcome is less than certain. While past wireless technology upgrades had competing standards vying for industry attention, there is no doubt about the air interface standard that will be used for 5G. “The 5G electronic ecosystem is significantly more mature, at this point, compared to the same time during the LTE transition,” Lam said. “Key 5G chipsets have been tested, proven and designed into devices, and the industry is now poised to deliver their first 5G smartphone in early 2019.”

“As telecom companies embark on the start of another wireless generation transition, they are doing so with a robust and coordinated ecosystem of carriers, handset makers and component suppliers,” Lam said. “By and large, the industry is finding itself with an unprecedented opportunity to execute a wireless transition in the best position possible.”

To download the complimentary “Substance behind the Hype: 5G Smartphones Primed and Ready for Fast Rollout” white paper from IHS Markit, visit https://cdn.ihs.com/www/pdf/0119/IHSMarkit-Whitepaper_5G-Smartphone_Jan2019.pdf.

Update: Global smartphone market ends 2018 on downturn

By Gerrit Schneemann, smartphones senior research analyst, IHS Markit; Wayne Lam, mobile devices and networks director, IHS Markit; and Jusy Hong, mobile handset devices director, IHS Markit

Global smartphone shipments recorded a negative year-over-year growth rate in the fourth quarter (Q4) of 2018, for a third consecutive quarter. According to IHS Markit preliminary smartphone data, global smartphone shipments reached 365.2 million units in Q4 2018, which is a 5.7 percent y/y decline. For the 2018 calendar year, shipments declined 2.4 percent compared to the previous year, from 1.44 billion units in 2017 to 1.41 billion units in 2018.

Following is an overview of the smartphone market leaders in 2018, based on unit shipments:

Samsung Electronics

Samsung Electronics maintained its shipment-volume lead, shipping 70.2 million units in Q4 2018. Samsung’s negative growth rate in 2018 continued, as shipments declined 5.5 percent compared to the same quarter of 2017. As a result, its market share fell to 19.2 percent in Q4 2018, which is flat compared to the previous year. Severe competition from Chinese rivals in many regions continued to impact Samsung’s business – and has led to Samsung changing its strategy for how new technologies are deployed in the company’s product range. For example, the first triple-camera Samsung device was a Galaxy A phone and, instead of a Galaxy S device, Samsung released the world’s first quad-camera smartphone – the Galaxy A9 — last year.

Overall Samsung smartphone shipment volume declined 8 percent, falling from 316 million units in 2017 to 290 million units in 2018. This is the first time Samsung shipped fewer than 300 million units in any year since 2014.

Huawei

Huawei shipped 60.5 million units in Q4 2018, rising 47.7 percent, year over year. The company continued its double-digit y/y growth for the fourth consecutive quarter, growing in most of regions, except North America where Huawei has little exposure. Fast growing markets for Huawei include Europe, Middle East and Africa. In 2018, Huawei was able to exceed Apple in unit-based shipments for three consecutive quarters, propelling the Chinese brand to second-ranked position in the market, unseating Apple from its perch. However, the network infrastructure side of Huawei has faced increased scrutiny from the United States and other governments around the world, due to potential security concerns in to roll out of 5G networks.

Apple

Apple shipped 64.3 million units in Q4 2018, down 16.9 percent from 77.3 million units in Q4 2017. The company’s performance faced significant challenges in China and in the overall global smartphone market in Q4 2018. Furthermore, Apple’s super-premium handset pricing seems to have stunted its unit growth potential in the quarter. Importantly, there is no quick fix for Apple to change fortunes in China or India. In China, local competition is fierce; while in India, Apple’s products are ill-equipped to fit into the country’s price-cautious market.

Xiaomi

The recent trend of high double-digit growth halted for Xiaomi in Q4 2018. The company shipped 24.8 million units, down 12.1 percent from 28.2 million units in Q4 2017.

Oppo and Vivo

Oppo and Vivo shipped 26.4 and 25.2 million units, respectively. Oppo shipments declined 3.6 percent, while Vivo shipments grew 7.2 percent.

Conclusions

Xiaomi, Oppo and Vivo were adversely affected by the continued negative growth of the smartphone market in China. On the other hand, Huawei strengthened its market leadership in China. Tension between the US and China stimulated a feeling of patriotism in China, leading smartphone users to choose Huawei over other brands. Moreover, Huawei boasts significant international business – which other brands are still working to establish – enabling the company to achieve tremendous success in the fourth quarter.

The combined market concentration on the top six companies continued to intensify in Q4 2018, accounting for 75 percent of global smartphone shipments. Most of the rest brands saw their shipments and market shares fall in the quarter.

Meanwhile, Nokia increased its shipments to 15 million units in 2018, up from 5 million units in the previous year. Finland-based HMD Global is operating its Nokia-branded smartphone business, by focusing on mid-range and low-end smartphones in Europe, Asia and Africa. The company will soon expand into North America.

Quarterly Global Smartphone Shipments (Millions of Units)

| Q4-18 | Q3-18 | Q4-17 | QoQ | YoY | |||||

| Rank | Shipments | M/S | Shipments | M/S | Shipments | M/S | |||

| 1 | Samsung |

70.2 |

19% |

70.9 |

20% |

74.3 |

19% |

-1% |

-6% |

| 2 | Apple |

64.3 |

18% |

46.9 |

13% |

77.3 |

20% |

37% |

-17% |

| 3 | Huawei |

60.5 |

17% |

52.0 |

15% |

41.0 |

11% |

16% |

48% |

| 4 | Oppo |

26.4 |

7% |

31.2 |

9% |

27.4 |

7% |

-15% |

-4% |

| 5 | vivo |

25.2 |

7% |

28.9 |

8% |

23.5 |

6% |

-13% |

7% |

| 6 | Xiaomi |

24.8 |

7% |

33.3 |

9% |

28.2 |

7% |

-26% |

-12% |

| 7 | LG |

11.1 |

3% |

11.6 |

3% |

13.9 |

4% |

-4% |

-20% |

| 8 | Motorola |

10.1 |

3% |

10.7 |

3% |

11.4 |

3% |

-6% |

-11% |

| 9 | TCL-Alcatel |

4.5 |

1% |

5.7 |

2% |

4.8 |

1% |

-21% |

-5% |

| 10 | Nokia |

4.2 |

1% |

4.5 |

1% |

4.4 |

1% |

-7% |

-5% |

| Others |

63.3 |

18% |

59.9 |

17% |

81.3 |

21% |

6% |

-22% |

|

| Total |

365.2 |

|

355.6 |

|

387.4 |

|

3% |

-6% |

|

Source: IHS Markit – Smartphone Intelligence Service

© 2019 IHS Markit

Global Smartphone Shipments (Millions of Units)

| Rank | Company | 2018 | 2017 | YoY |

| 1 | Samsung | 290 | 316 | -8% |

| 2 | Huawei | 206 | 153 | 35% |

| 3 | Apple | 205 | 216 | -5% |

| 4 | Xiaomi | 120 | 92 | 30% |

| 5 | Oppo | 115 | 118 | -2% |

| 6 | vivo | 104 | 95 | 9% |

| 7 | LG | 45 | 56 | -19% |

| 8 | Motorola | 39 | 38 | 3% |

| 9 | TCL-Alcatel | 17 | 21 | -18% |

| 10 | Nokia | 15 | 5 | 175% |

| Others | 254 | 334 | -24% | |

| Total | 1,410 | 1,444 | -2% |

Source: IHS Markit – Smartphone Intelligence Service

………………………………………………………………………………………………………………………………………………………….

About IHS Markit (www.ihsmarkit.com)

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions. Headquartered in London, IHS Markit is committed to sustainable, profitable growth.

…………………………………………………………………………………………………………………………………………………………………………………………………………………….

Analysts Weigh-in on Samsung’s Feb. 20 Galaxy 10 Launch?

Avi Greengart, a mobile device analyst with GlobalData, said a big challenge with every new phone model release for Samsung and other vendors is that as phones have matured, users are holding onto their phones longer.

“As much as Samsung needs to compete with Apple, it needs to compete with the phone consumers already have – the S10 needs to be a phone that entices existing Android phone owners to upgrade,” Greengart told eWEEK. “We know what phones are and what they do – no single new feature is likely to be groundbreaking. However, design is definitely an area of focus; Samsung was actually the first vendor with an edge-to-edge display, but now that’s not enough.”

The new phones will almost certainly include 5G capabilities for each of the major mobile carriers’ networks as they come online, but more will be needed to make a sales impact, he said.

“There is a tricky balance that Samsung must hit – it needs radical designs and bleeding edge technologies like folding displays and 5G that push the envelope for early adopters, but it also must make more traditional 4G phones exciting enough to entice mainstream consumers to upgrade as well,” Greengart said. “It’s not enough to just cram massive amounts of technology into the phone for the wealthiest consumers. In the U.S., the competition really is focused around Apple and Samsung, but in Europe and Asia, Chinese brands like Honor and Xiaomi are attacking Samsung with premium phones at lower price points.”

Charles King, principal analyst with Pund-IT, agreed. “At this point, Samsung is one of the two to three phone makers that can and do fight Apple to a draw,” King told eWEEK. “With phones like Samsung’s [current] Galaxy S9, it really comes down to the buyer’s operating system and applications preferences. That’s a significant contributor to Apple’s overall slowdown in iPhone sales growth over the last few months.”

For buyers, solid and noticeable improvements in cameras and displays in newer phones can help Samsung inspire more sales of its latest handsets, while a larger issue for many customers are the high prices of the devices, King said. “I believe the emergence of $1,000 handsets last year clarified the ceiling of what the vast majority or consumers will pay for a smartphone. So it’s important for Samsung to either deliver significant, compelling new features or performance capabilities, or to show greater flexibility in pricing.”

Tuong Nguyen, an analyst with Gartner, said a big issue that Samsung and other handset makers have to deal with when releasing new models nowadays is that for buyers, it’s tough to differentiate because all the major vendors have large screens, plenty of storage and all the rest.

For Samsung and other smartphone makers, there are no current “must-have” features that can be included in a handset to assure huge resulting sales of the phones, he said. “I think there are numerous features that are compelling, but they need to improve and come together in a way that increases the value proposition of smartphones in a significant way.”

What could boost sales for a phone would be the ability to use a smartphone as a hub or centralized device so users could control different aspects of their tech lives without having to open multiple apps or make other adjustments, Nguyen said. “I would categorize all this under learn, predict, surprise and anticipate. This is the type of step change we need to drastically attract users,” Nguyen said.

Another analyst, Rob Enderle, principal of Enderle Group, told eWEEK he expects the new Samsung flagship devices to include 5G, a bump in performance and features such as battery life and camera quality, as well as enhancements in wireless charging–including a rumored feature that enables the phone to charge another device wirelessly at the same time. What Samsung will have to try to overcome, though, is that because wide deployments of 5G is still more than a year away many users may be satisfied to hang on to their existing handsets for now, Enderle said.

“Smartphones have been really good for years now, and the natural need to replace them has dropped sharply over time,” said Enderle. “In the current period, this behavior is likely more directly related to a reduction in effective demand-generation.”

https://www.eweek.com/mobile/can-we-expect-5g-at-samsung-s-feb.-20-galaxy-10-launch

Huawei launches 5G multi-mode chipset and 5G CPE Pro Smartphone

Huawei officially launched its 5G multi-mode chipset Balong 5000 — along with the first commercial 5G device powered by it, the Huawei 5G CPE Pro. The Chinese tech giant claims that together, these two new products provide the world’s fastest wireless connections for one’s smartphone, home, at the office and on-the-go. We don’t doubt that.

Balong 5000 officially unlocks the 5G era, according to Huawei. This chipset supports a broad range of 5G products in addition to smartphones, including home broadband devices, vehicle-mounted devices and 5G modules.

Photo courtesy of Huawei. Huawei’s 5G CPE Pro achieves a high speed of 3.2 Gbps in live network tests.

……………………………………………………………………………………………………………………………………………………………………………….

“The Balong 5000 will open up a whole new world to consumers,” said CEO of Huawei’s Consumer Business Group Richard Yu. “It will enable everything to sense, and will provide the high-speed connections needed for pervasive intelligence. Powered by the Balong 5000, the Huawei 5G CPE Pro enables consumers to access networks more freely and enjoy an incredibly fast connected experience. Huawei has an integrated set of capabilities across chips, devices, cloud services and networks. Building on these strengths, as the leader of the 5G era, we will bring an inspired, intelligent experience to global consumers in every aspect of their lives.”

Balong 5000 supports 2G, 3G, 4G and 5G on a single chip. It reduces latency and power consumption when exchanging data between different modes, and will significantly enhance user experience in the early stages of commercial 5G deployment.

“Balong 5000 is the first chipset to perform to industry benchmarks for peak 5G download speeds. At sub-6 GHz (low-frequency bands, the main spectrum used for 5G), Balong 5000 can achieve download speeds up to 4.6 Gbps. On mmWave spectrum (high-frequency bands used as extended spectrum for 5G), Balong 5000 can achieve download speeds up to 6.5 Gbps — 10 times faster than top 4G LTE speeds on the market today,” Huawei said.

On a 5G network, a 1-GB HD video clip can be downloaded within three seconds, and 8K video can be streamed smoothly without lag. This sets a new benchmark for home CPEs. In addition to homes, the Huawei 5G CPE Pro can also be used by small and medium-sized enterprises for super-fast broadband access.

Adopting new Wi-Fi 6 (IEEE 802.11ax) technology, the Huawei 5G CPE Pro delivers speeds of up to 4.8 Gbps. It is the first 5G CPE that supports HUAWEI HiLink protocols, bringing smart homes into the 5G era.

As a 5G pioneer, Huawei began research and development in 5G as early as 2009, and is currently the industry’s only vendor that can provide end-to-end 5G systems. Huawei has more than 5700 engineers dedicated to 5G R&D, including over 500 5G experts. In total, Huawei has established 11 joint innovation centers for 5G solutions worldwide

………………………………………………………………………………………………………………………………………………………………………………………………

The NY Times reported that in 2018, Huawei edged out Apple as the second-biggest provider of cellphones around the world. Richard Yu, who heads the company’s consumer business, said in Beijing several days ago that “even without the U.S. market we will be No. 1 in the world,” by the end of this year or sometime in 2020.

Last year, AT&T and Verizon stopped selling Huawei phones in their stores after Huawei began equipping the devices with its own sets of computer chips — rather than relying on American or European manufacturers. The National Security Agency quietly raised alarms that with Huawei supplying its own parts, the Chinese company would control every major element of its networks. The N.S.A. feared it would no longer be able to rely on American and European providers to warn of any evidence of malware, spying or other covert action.

For months, the White House has been drafting an executive order, expected in the coming weeks, that would effectively ban United States companies from using Chinese-origin equipment in critical telecommunications networks. That goes far beyond the existing rules, which ban such equipment only from government networks. “China’s 2017 National Intelligence Law requires Chinese companies to support, provide assistance and cooperate in China’s national intelligence work, wherever they operate.”

The White House’s focus on Huawei coincides with the Trump administration’s broader crackdown on China, which has involved sweeping tariffs on Chinese goods, investment restrictions and the indictments of several Chinese nationals accused of hacking and cyberespionage. President Trump has accused China of “ripping off our country” and plotting to grow stronger at America’s expense.

References:

https://consumer.huawei.com/en/press/news/2019/huawei-launches-5g-multi-mode-chipset-and-5g-cpe-pro/

https://www.nytimes.com/2019/01/28/us/politics/meng-wanzhou-huawei-iran.html

IHS Markit: SDN deployed by 78% of global service providers at end of 2018

By Michael Howard, senior research director, carrier networks, IHS Markit

Highlights

- All of the 23 service providers surveyed reported that they will deploy SDN at some point. More than three-quarters (78 percent) of those providers will deploy or evaluate the architecture by the end of this year, growing to 87 percent by the end of 2019.

- Software-defined wide-area networks (SD-WANs) leads the list of SDN-based services expected to generate new revenue, with 78 percent of respondents identifying it as a key deployment goal, while nearly half (48 percent) plan to implement network slicing for IoT.

- Automation and reduction of capex and operating-expenditure (opex) are among the goals for the top domains for SDN deployments. By the end of 2019, 74 percent of respondents will use SDN to automate the delivery of new services, followed by operations and management at 65 percent.

Our analysis

Service providers are in the early stages of a long-term transition to software-defined networks (SDN), according to the sixth annual “Carrier SDN Strategies Service Provider Survey” in 2018 from IHS Markit. Various barriers and drivers have become more prominent, as operators get closer to commercial deployment, although the barriers remain. These barriers include the problem of products that are not carrier grade and difficulty with integration into existing networks.

Service providers around the globe – representing 44 percent of worldwide telecom capital expenditure (capex) and 44 percent of revenue – are investing in software defined networks (SDNs) as part of a larger move to automate their networks and transform their internal processes, operations, and the way they offer services to their customers. Providers view SDN as a key technology underpinning the fundamental changes in telecom network architecture that delivers benefits in new service agility, quicker time to revenue, automation, operational efficiency, and capex savings.

Many operators have some parts of their networks running under SDN control. The rest are moving from their proof-of-concept (PoC) investigations and evaluations for SDN toward commercial deployments in the tail end of 2018 and 2019.

The top two reasons service providers are investing in and deploying network SDN are the following:

- Simplification and automation of service provisioning, leading to service agility and quicker time to revenue

- End-to-end network management and control as part of increased automation

The majority of service providers are investing in SDN in order to simplify and automate the provisioning of their networks for end-to-end network and service management and control—with the goal of having a global view of network conditions across the various vendors’ equipment, network layers, and technologies. SDN figures in provider plans to generate revenue, with multi-cloud and network slicing for applications and IoT figuring more prominently this year.

Still, carriers will learn that some avenues are not as fruitful as expected, and telecom equipment manufacturers and software suppliers may well invent new approaches that open up new applications.

Carrier SDN Strategies Service Provider Survey – 2018

This sixth annual survey of global service providers explores plans and strategies of 23 operators for evaluating and deploying SDNs. The study identifies the drivers for this fundamental change in service provider network architecture and explores use cases, development stages, barriers, applications, target network areas, and timing of deployment plans.

……………………………………………………………………………………………………………………………………………………………………………………………………………………

Editor’s Note:

But what SDN model or version was implemented by these service providers? That is not stated in Michael Howard’s report.

There’s the classical SDN/Open Flow model from ONF, the overlay or virtual network model, the evolutionary model, hybrid model, DevOps management model, VMWare’s two NSX versions, etc

Also, most versions of SDN use a centralized controller and NOT segment or hop by hop routing. Yet Cisco and Juniper routers can handle segment-routing traffic. Their versions of SDN are ready for segment routing, as well. Moreover, Linux has an open source implementation of segment routing, and Cumulus Networks’ Linux-based network OS also supports it.

With so many different versions of SDN, it appears that network equipment and software built for one SDN based network will not work on ANY other service provider’s SDN unless multiple SDN versions/models are supported in the same equipment/software.

References:

https://www.rcrwireless.com/20170811/three-different-sdn-models-tag27-tag99

https://searchnetworking.techtarget.com/tip/Three-models-of-SDN-explained

https://searchvmware.techtarget.com/opinion/VMwares-two-NSX-versions-are-the-future-of-SDN

OpenVault: Broadband Internet Usage Accelerated in 2018

Executive Summary:

U.S. households consumed an average of 268.7 gigabytes (GB) of data in 2018, up from 201.6 GB for 2017, according to a new report about U.S. household broadband data consumption from OpenVault, a provider of data consumption and analytics software. Median usage was 145.2 GB per household in 2018, up from 103.6 GB in 2017. The increase in average consumption was 33.3% and the increase in median consumption was 40%.

Open Vault attributed the different growth rates to growing consumption across service providers’ entire subscriber bases, rather than growth only among heavy users. Their year end 2018 data showed that:

U.S. Household Broadband Data Consumption:

- Average usage for households with flat-rate pricing was 282.1 GB per household, which was more than 9% higher than the 258.2GB average usage for households on usage-based billing (UBB) plans. Average usage for all households was 268.7GB/HH in 2018, up from 226.4GB/HH at the end of June 2018 and a 33.3% increase over the YE 2017 average of 201.6GB/HH.

- Median usage was 145.2GB/HH in 2018, up from 116.4GB/HH in June 2018 and a 40% increase over the YE 2017 median of 103.6GB/HH.

- The percentage of flat-rate (non-UBB) households exceeding 1 terabyte (TB) of usage was 4.82%, a full percentage point higher than the 3.81% of UBB households that exceeded the 1 TB threshold.

- The percentage of households using 1TB or more almost doubled in 2018, rising to 4.12% of all households from 2.11% in 2017, while the percentage of households exceeding 250 GB rose to 36.4% from 28.4% during the same time frame.

In addition to analyzing trends in broadband consumption, OpenVault also tracked expansion within the US consumer device landscape, observing a 5.3% increase in connected devices when comparing the week after Christmas with the week before Christmas. While Amazon, Samsung and Apple collectively accounted for the majority of the growth, the 15.6% rate of increase for Amazon devices was significantly higher than the rates of growth for Samsung (4.1%) and Apple (2.9%).

“As connected devices, streaming services and broadband speeds increase, service providers need an alternative to infrastructure upgrades that would enable them to keep up with demand,” said Josh Barstow, Open Vault executive vice president of corporate strategy and business development, in a prepared statement about the U.S. household broadband data consumption research. “Our analysis makes it clear that usage-based billing is among the most effective tools the industry has in managing consumption and reducing the need for massive capital expenditures.”

……………………………………………………………………………………………………………………………………………………………………………………..

3GPP RAN WG meeting in Taiwan: January 21 – 25, 2019: NTT DOCOMO’s URLLC Use Cases

3GPP RAN WG meeting in Taiwan: January 21 – 25, 2019:

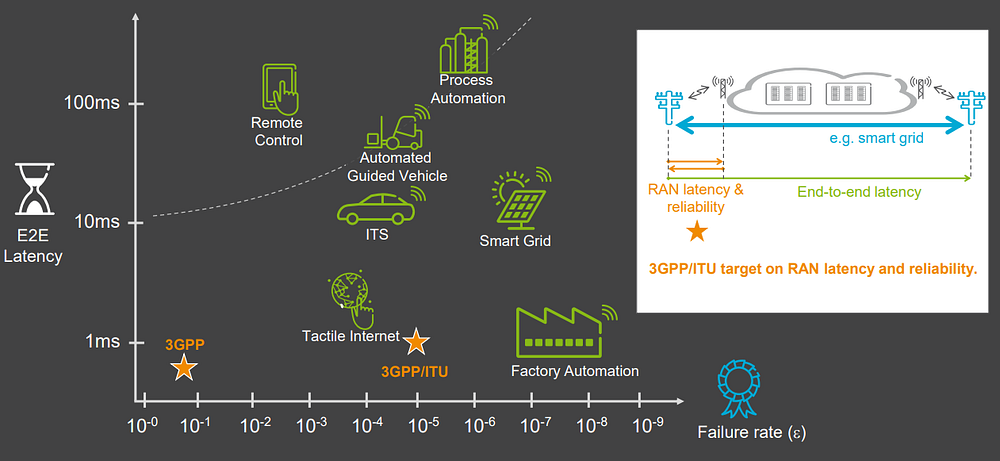

A five-day working group meeting of the 3rd Generation Partnership Project (3GPP) RAN WG opened in Taiwan on Monday January 21, 2019, with 459 registered delegates attending. The goal of the meeting is to progress 3GPP Release 16 which will include an important IMT 2020 Use Case: Ultra-Reliable Low-Latency Communications (URLLC). I counted over a dozen contributions on the URLLC topic at this 3GPP meeting’s document list which can be accessed here.

Services for latency sensitive devices for applications like factory automation, autonomous driving, and remote surgery. These applications require sub-millisecond latency with error rates that are lower than 1 packet loss in 10⁵ packets [ITU-R M.2410.0]. New techniques need to be devised to meet the stringent latency and reliability requirements for URLLC.

An interesting 3GPP RAN meeting contribution on Views and evaluations for URLLC scenarios by Kazuaki Takeda of NTT DOCOMO will be presented this week. In that contribution, NTT DOCOMO selected the following cases for evaluation:

| Case | Use-case | Reliability | Latency | Data packet size and traffic model | Description |

| 1 | Factory automation

@ 30GHz |

99.9999 (%) | 2ms for end-to-end

1ms for air-interface |

DL & UL: 32 bytes

Periodic and deterministic traffic model with data arrival interval 2ms |

Motion control |

| 2 | Factory automation

@ 4GHz |

99.9999 (%) | 2ms for end-to-end

1ms for air-interface |

DL & UL: 32 bytes

Periodic and deterministic traffic model with data arrival interval 2ms |

Motion control |

| 3 | Rel.15 enabled use-case in indoor hotspot

@ 4GHz |

99.9 (%) | 7ms for air-interface | DL & UL: 4096 bytes

FTP model 3 |

AR/VR |

| 4 | Rel.15 enabled use-case in urban macro

@ 4GHz |

99.999 (%) | 1ms for air-interface | DL & UL: 32 bytes

FTP model 3 |

Sporadic traffic |

| 5 | Power distribution

@ 700MHz |

– | – | – | UL/DL SINR CDF only |

There are high interests on supporting industrial IoT type of services at local area using carrier frequencies of around 4GHz and 30GHz [2]. It would be possible to evaluate NR performance in this type of scenario by simulating case 1, case 2, and case 3. For AR/VR type of services in a specific local area, it is not sure whether all the packets should be delivered as URLLC packets, or some specific type of packets (e.g., control packet) for AR/VR service should only be delivered as URLLC packets (i.e., other types of packets for AR/VR service can be delivered as eMBB). The simple way is to treat all the packets as URLLC packets as the evaluation assumption. Case 3 can be viewed as representing such situation. For emergency type of services in wide area, it can be represented by case 4. As the case 5, we partly evaluate the wide area performance at 700MHz.

…………………………………………………………………………………………………………………………………………………………………..

Taiwan 5G Commercialization Summit

In conjunction with the referenced 3GPP working group meeting, the Taiwan 5G Commercialization Summit organized by Taiwanese entities was also held in Taipei on Monday, January 21st. The organizers of the Taiwan 5G summit were: MediaTek, Chunghwa Telecom, the Taiwan Association of Information and Communications Standards, and the 5G Office of the Ministry of Economic Affairs (MOEA). Tung Tzu-hsien (童子賢), the head of iPhone assembler Pegatron Corp and a private sector group advising the government’s national innovation/new economy task force, said 5G technology is expected to drive sophisticated applications of the future such as smart medical care and the Internet of Vehicles. Many of those new applications will require URLLC.

Mr. Tung urged the Taiwan government to update regulations to meet the needs of a fast-changing telecom environment and prevent Taiwan from lagging behind other countries in 5G development. As long as Taiwan is successful in 5G development, it will create major commercial opportunities for the local Information and Communications Technology (ICT) sector, he added.

Since January 2018, Chunghwa Telecom has teamed up with the MOEA’s 5G Office, and the government-sponsored Institute for Information Industry (III) and Industrial Technology Research Institute in a 5G development alliance.

ZTE makes prototype smartphone call on China Unicom’s trial 5G network vs Huawei’s 5G NR @ 2.6GHz?

ZTE, which recently completed the 3rd phase of CMIIT IMT-2020 5G core network tests, just announced it made the a 5G mobile call using its 5G prototype smartphone on the Guangdong branch of China Unicom’s trial 5G network in Shenzhen, China. The trial was conducted in collaboration with China Unicom and involved placing a 3GPP Release 15 compliant New Radio (NR) non-standalone (NSA) mobile call using the prototype smartphone. It used ZTE’s 5G end-to-end solution, including radio access network, core network, transport network and prototype device. In addition to demonstrating a 5G call, the test verified key 5G technologies including Massive MIMO, 5G NR, non-standalone (NSA) dual connectivity, FlexE transport technology and 5G common core architecture (defined by who?).

ZTE says “the future 5G system should be a unified network adaptable to different scenarios.”

…………………………………………………………………………………………………………………………………………………………………………………

“ZTE’s 5G solution has passed the end-to-end test in the three months after the release of the 3GPP Rel-15,” ZTE said in a statement. “It showcases ZTE’s strong competency in 5G R&D and commercialization, demonstrating ZTE’s role as a reliable partner to global 5G operators and a key player in the 5G industry.”

Last year, ZTE announced a series of new-generation 5G base stations. The Chinese telecom and mobile phone vendor said that the new generation of 5G high/low frequency Active Antenna Unit (AAU) base stations support 3GPP release 15 “5G NR” NSA specification for the data plane. The latest ZTE base stations combine the radio and antenna parts. It is capable of integrating multiple frequency bands, which create what is known as the “AAU solution.” AAU supports 5G functions such as Massive MIMO and Beamforming.

Meanwhile, Huawei says it completed a 5G New Radio (NR) trial in the 2.6 GHz spectrum band. Huawei said 2.6 GHz is one of the “excellent choices for operators to deploy 5G NSA/SA commercial network.” The company noted that 2.6 GHz is an “abundant spectrum resource around the world, but not fully used in many areas.” Huawei’s tests in the 2.6 GHz band follows earlier trials in the 3.5 GHz and 4.9 GHz bands.

The two Chinese telecom vendors are vying to take the lead in 5G testing under the jurisdiction of China’s IMT-2020 (5G) Promotion Group, which was established in 2013 as China’s platform to promote 5G research in that country. The 5G R&D trial established three separate phases for verifying a 5G solution: key technologies, technical solutions, and system networking.

References:

https://www.zte.com.cn/global/about/press-center/news/201901/20190118

https://www.zte.com.cn/china/topics/zte-5g-en/index.html

https://www.sdxcentral.com/articles/news/huawei-takes-5g-supremacy-shot-at-zte/2019/01/

https://techblog.comsoc.org/tag/chinas-imt-2020-promotion-group/

ATIS endorses 3GPP IMT 2020 RIT submission to ITU-R WP 5D; sees no need for separate LMLC India national option

IMT-2020/VVV: “Process, use of the Global Core Specification (GCS), references, and related certifications in conjunction with Recommendation ITU-R M.[IMT 2020.SPECS]”

From Alliance for Telecommunications Industry Solutions (ATIS):

The 3GPP candidate radio-interface technology (RIT) for IMT-2020 (or 5G as it is known commercially) has demonstrated via the current in-progress submissions (including initial self‑evaluations to ITU-R WP 5D) that it is capable of meeting and, in fact, exceeding the requirements and evaluation criteria of IMT-2020 as expressed in Reports ITU-R M.2410 (requirements), ITU-R M.2411 (submission), and ITU-R M.2412 (evaluation), which were published in November 2017. It is widely anticipated that the 3GPP specifications in Release 15 and Release 16 will meet the futuristic vision of IMT-2020, as expressed in Recommendation ITU-R M.2083 for both developed and developing countries.

Global Activities of Telecommunications Standards Development Society India (TSDSI):

a) ITU-R:

TSDSI members’ proposal on Low Mobility Large Cell (LMLC) configuration has been included as a mandatory test configuration under the Rural eMBB test environment in IMT 2020 Technical Performance Requirements (TPR) in ITU-R with an enhanced Inter Sire Distance (ISD) of 6 km. Incorporation of LMLC in IMT2020 will help address the requirements of typical Indian Rural settings and will be a key enabler for bridging the rural-urban divide with 5G rollouts.

TSDSI’s initial proposal on candidate Radio Interface technology (RIT/SRIT) for IMT 2020 technologies, related to improving coverage and spectral efficiency performance, has been accepted in the WP 5D meeting #30 held in Cancun Mexico.

https://tsdsi.in/tsdsis-initial-proposal-on-candidate-rit-srit-for-imt-2020-accepted/

b) 3GPP:

TSDSI is Organizational Partner of 3GPP along with six other Regional Standardisation bodies. This entitles TSDSI members to become individual members of 3GPP through TSDSI and to take their IP into the global arena. Membership of 3GPP enables members to contribute in the development of upcoming standards such as 5G.

References:

Singtel, Ericsson and Singapore Polytechnic launch “5G Garage”

Singapore network operator Singtel has opened Singapore’s first live 5G facility in conjunction with Ericsson and Singapore Polytechnic. The 5G facility at Singapore Polytechnic’s Dover Road campus is named “5G Garage.” It is connected to Singapore’s pilot 5G network using the 3.5-GHz spectrum allocated by regulator IMDA for 5G trials. 5G Garage will serve as a training center, test bed and idea creation lab to develop Singapore’s 5G ecosystem.

The strategic objectives are:

• Build and operate a 5G facility where enterprises can develop and test 5G solutions

• Co-develop 5G solutions relevant to industries such as transportation, logistics, healthcare and manufacturing

• Develop and deliver 5G wireless technology curriculum for the SP’s School of Electrical and Electronic Engineering

• Develop 5G capabilities of our workforce

Mark Chong, Group Chief Technology Officer, Singtel, said, “Singtel is pleased to partner Ericsson and SP on our 5G Garage initiative. As Singapore advances its digital economy and becomes a Smart Nation, the benefits of 5G will first be seen in enterprises, especially in their digital transformation when they integrate technology into their processes, services and products. With 5G standards largely established (????), now is an opportune time for SMEs and enterprises to join us in shaping our 5G future.”

“As Singapore advances its digital economy and becomes a Smart Nation, the benefits of 5G will first be seen in enterprises, especially in their digital transformation when they integrate technology into their processes, services and products,” Chong added.

Martin Wiktorin, Country Manager Singapore, Brunei and the Philippines, Ericsson, states: “5G has the potential to transform industries and bring enhanced mobile broadband experience for consumers. At Ericsson, we are already collaborating globally with 42 operators, 45 institutes and 31 industry partners, to create a thriving 5G ecosystem. We are delighted to partner Singtel and Singapore Polytechnic towards the setting up of the 5G Garage, which we hope will stimulate SP students to come up with new 5G use cases.”

Enterprises will be able to use the facility to develop and test 5G solutions, and the three parties plan to co-develop 5G solutions for industries ranging from transport and logistics to healthcare to manufacturing. As part of the collaboration, around 250 final year students from the polytechnic’s Diploma in Electrical & Electronic Engineering and Diploma in Computer Engineering will integrate 5G education and training into their coursework. Students in Singtel’s Engineering Cadet Scholarship Program will be given the opportunity to take up internships in the 5G garage.

5G Garage is the latest project in Singtel and Ericsson’s 5G Centre of Excellence programme which focuses on upgrading of employees’ skills, technology demonstrations, live field trials and collaborations with educational institutions. Last November, Singtel and Ericsson made Singapore’s first 5G data call over their 5G pilot network at one-north.

Reference:

“The 5G Garage will be an exciting place where SP staff and students will work alongside Singtel, Ericsson and their partners to research and experiment with 5G technology, conduct 5G use case trials, and develop innovative 5G solutions and applications for businesses and industry,” said SP’s principal and chief executive, Mr Soh Wai Wah.

Out of more than 80 final-year projects developed by around 300 SP engineering students, three were chosen with potential for 5G Garage: an autonomous surveillance system that uses drones; a self-driving vehicle that can send real-time videos of the traffic situation to the cloud for data analysis and “intelligent” decision-making; and a pipe-climbing robot that uses magnetic wheels to attach itself onto metal structures and can provide a live feed of its surroundings via a mobile app.

Mr Mark Chong, Singtel group chief technology officer, said the engineering students demonstrated their capability to develop engineering solutions and help enterprises.

“The benefits of 5G will first be seen in enterprises, especially in their digital transformation when they integrate technology into their processes, services and products. With 5G standards largely established, now is an opportune time for SMEs and enterprises to join us in shaping our 5G future,” he said.

Infocomm Media Development Authority chief executive Tan Kiat How, the guest of honour at the event, said 5G will be an integral part of Singapore’s infrastructure. He said: “Apart from improved network speed and capacity, 5G’s significantly lower latency will allow us to maximize the potential of IoT (Internet of things) and smart city applications. These include autonomous vehicles, robotics or smart lamp posts.”

https://www.straitstimes.com/singapore/singtel-ericsson-spore-poly-set-up-5g-testing-centre

Gartner strategic roadmap for networking

The future-state network is an aspirational view of how enterprise network architectures should evolve to meet emerging business requirements and align more closely to critical business objectives.

The primary external forces driving network change are the adoption of digital business and the concept of “digital to the core.” This will result in increased adoption and investments in hybrid-cloud-based infrastructure, platform and application services to meet dynamic business requirements, and a greater focus on always-on service delivery to clients. Digital to the core will also drive IoT deployments to richer, more complex business models and processes, which will compound the pressure of increasing user expectations for consistently strong network performance, quality, reliability and security. This is overlaid with the fact that we anticipate increased pressure from the business to maintain flat networking budgets.

As expectations of greater network dynamism become the norm, network service providers will also follow suit with rapid delivery of new enterprise network services. These will be delivered through network function virtualization (NFV) capabilities, deployed on customer-located vCPE platforms, or within the service planning network, in next-generation, Central Office Re-architected as a Datacenter (CORD)-based architectures. We will see a continued trend to leverage software-based, virtualized network solutions deployed with enterprise networks — as xSP services and available as over-the-top (OTT) services from a growing number of players.

After decades of focusing on speed, network performance and features, future network innovation will target operational simplicity and business models that closely align with elastic cloud-based services. These services are becoming more prevalent in — and demanded by — organizations with strong digital transformation agendas. The evaluation of networking technology within the most successful enterprises will balance between functional, financial and operational requirements. Understanding when “good enough” is actually good enough will be critical to architecting networks that are ready for digital business.

One national need (expressed by India) was for capabilities to permit low mobility large cell (LMLC) deployments. This need was, in fact, part of the submissions to WP 5D in 2016 and 2017, which drove the ITU-R Performance requirements, the ITU-R evaluation criteria/scenarios and hence the 3GPP specifications in Release 15 to be suitably modified to accommodate LMLC needs, thus illustrating the success of working within the framework of the current 3GPP process. Additionally, through the use of the established process, currently familiar to the entire ITU membership, a “national need” was recognized to actually be a global need in both ITU and in 3GPP. As such, the added technical capability can take advantage of the economies of scale afforded to a global marketplace. It is further noted that in technical submissions so far received by ITU-R WP 5D from 3GPP that this requirement for LMLC is indeed satisfied by the 3GPP technology capabilities already included in Release 15 published in September 2018.

Conclusions:

ATIS urges that ITU-R Members, relevant external organizations, and others work within the established ITU-R IMT process and within the process established in the respective external organizations engaged in the development of IMT (and 5G) in order to ensure that IMT remains a unified and global technology with strong industry and governmental support. Only in this way, avoiding the division of the technical underpinnings, permits taking full advantage of the economies of scale to permit IMT-2020 to be available to the widest extent to ensure a globally-connected society at all strata, addressing both business and societal needs, while ensuring that IMT is technically capable of continuing global interoperability and roaming. The entire wireless industry and wireless user community will benefit from a single global standard; fragmentation of the standard reduces the benefits of a global ecosystem and diminishes the ITU IMT-2020 vision.

…………………………………………………………………………………………………………………………………………………………

It will be very interesting to see how India’s TSDSI delegation to ITU-R WP 5D responds to this ATIS contribution.

India’s TSDSI Backgrounder: