Month: December 2019

Huawei’s Revenue Hits Record $122 Billion in 2019 Despite U.S. Ban

By Dan Strumpf, Wall Street Journal

What ban? Huawei Technologies said its revenue rose to a record $122 billion this year, showing the Chinese tech giant’s continued rise despite the Trump administration’s campaign to curtail its global business.

The pace of growth was slightly slower than expected, said Eric Xu, Huawei’s chairman, predicting more challenges in 2020 and saying the company doesn’t expect to be removed from a U.S. blacklist that has cut it off from certain U.S. technologies.

“We won’t grow as rapidly as we did in the first half of 2019, growth that continued throughout the year owing to sheer momentum in the market,” Mr. Xu said in a New Year’s message to employees titled “Forging Ahead to Survive and Thrive.”

“It’s going to be a difficult year for us,” Mr. Xu continued. ”We will have nothing to rely on but the hard work of our people as well as the ongoing trust and support of our customers and partners.”

Huawei’s finance chief, Meng Wanzhou, remains under house arrest in Vancouver more than a year after her initial detention, as she continues to fight a U.S. extradition request on charges of evading sanctions on Iran. Ms. Meng and Huawei have denied wrongdoing.

Despite those obstacles, Mr. Xu said revenue grew roughly 18% in 2019 to more than 850 billion yuan, or about $122 billion. The unaudited figure was lower than the company initially projected for the year, he said, and was a slowdown from the 19.5% revenue jump recorded in 2018—though exceeded its 2017 growth clip.

Huawei didn’t break out its 2019 revenue by region, but in past years about half of its revenue came from China, while the rest came from Europe and other overseas markets. The U.S. accounts for a tiny share of its revenue.

Huawei shipped 240 million smartphones this year, Mr. Xu said, a 17% increase over 2018 shipments. The company is continuing to invest in other gadgets, including PCs, tablets and wearable devices, he said.

Several U.S. administrations have long suspected that Huawei’s telecom equipment could be used by Beijing to eavesdrop on communications, a charge that Huawei—the world’s largest maker of such gear—repeatedly denies. Huawei gear is effectively off-limits to major American telecom operators, though it is widely used in much of the rest of the world.

A major reason for Huawei’s growth this year has been the company’s ability to withstand being added to the Commerce Department’s “entity list” in May. The listing prevents companies from selling U.S.-sourced technology to Huawei without a license, threatening Huawei’s access to many critical chip and software suppliers.

However, the measure proved less potent than expected. Many American companies assemble chips overseas, allowing them to continue selling to Huawei. At the same time, Huawei turned to alternate sources—including its in-house chip supplier, HiSilicon—for many components. The company now is capable of building 5G equipment entirely free of any U.S. parts.

Its smartphone business continues to grow sharply in its home market of China, and the company has dozens of 5G contracts around the world. So far, Australia and New Zealand have followed the U.S. in blocking Huawei from their 5G networks. In October, German authorities signaled that they won’t exclude Huawei, while a final decision is pending in Canada and the U.K.

Huawei’s CEO and founder, Ren Zhengfei, gave a series of interviews this year boasting of the company’s ability to survive without the U.S. In an interview in November, he told The Wall Street Journal: “We can survive very well without the U.S.”

“Huawei has a fighting culture where aggressive goals are set and with the whole company committed to win,” said Handel Jones, CEO of International Business Strategies Inc., a consulting firm.

One risk to Huawei in the coming year is a slowdown in the adoption of 5G technology, Mr. Jones said. Another is whether its formidable smartphone business can continue to grow in markets outside of China.

Under the entity listing, Huawei remains cut off from selling new smartphones with Google’s suite of Android apps, including the Play app store, Google Maps and other software Western smartphone users take for granted. Mr. Jones said he expects Huawei to ship between 250 million and 260 million smartphones in 2020.

Relief could come in the form of a trade deal between the U.S. and China that makes allowances for Huawei, such as additional Commerce Department licenses. A victory for Ms. Meng in her extradition fight would be met with triumph inside the company. However, Mr. Xu, in his New Year’s note, signaled that the company is keeping expectations in check.

“Survival will be our first priority,” he said.

Write to Dan Strumpf at [email protected]

China to complete Beidou satellite-based positioning system by June 2020- to be used with 5G

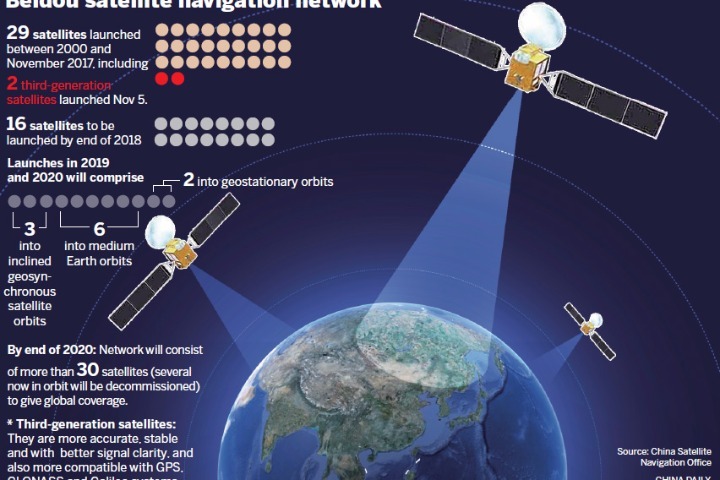

The Nikkei Asian Review reported on Friday that China will soon be completing its Beidou satellite-based positioning system as it moves to reduce its reliance on America’s GPS in both in telecommunications and for its military. The final two satellites for its Beidou satellite-based positioning system will be launched by June 2020, completing the 35-satellite network, Ran Chengqi, spokesperson for the Beidou Navigation Satellite System, told reporters in Beijing.

From modern farming to smart ports to a text messaging service, China is trying to build an ecosystem independent of the GPS and open it to Southeast Asia, South Asia, Africa and Eastern Europe. This effort pushes decoupling between Washington and Beijing, which are poised to enter year three of a trade war, to the final frontier of space.

Over 70% of Chinese smartphones are equipped to tap into Beidou’s positioning services, Ran said. The system also plays a role in fifth-generation wireless communications (5G), an area where China’s Huawei Technologies is in the vanguard of technological development.

“The integration of Beidou and 5G is an important sign on the path toward China’s development of information technology,” Ran said. “As a major space infrastructure for China to provide public services to the world, the Beidou system will always adhere to the development concept of ‘China’s Beidou, the world’s Beidou, and the first-class Beidou,’ serving the world and benefiting mankind,” he added.

China’s goal for Beidou is to rely less on the US for both its telecommunications and its military and to build an ecosystem independent of the GPS that would be open to Southeast Asia, South Asia, Africa and Eastern Europe.

Beidou was named after the Chinese term for the Big Dipper constellation. Beidou said its services will be enhanced by the end of next year. For example, the level of positioning accuracy will improve from within 5 meters to within centimeters, an advance that will aid search-and-rescue missions and also prove crucial for self-driving vehicles. Both Beidou and 5G will be employed by self-driving buses set to begin operation soon in the city of Wuhan. Beidou will also differentiate itself from GPS by supporting communication through its constellation of satellites.

China has launched 53 Beidou satellites since 2000, including those no longer in operation. The navigational system began worldwide services in late 2018. Beidou started offering positioning services to private-sector companies in late 2011.

The economic scale of services and production of goods tied to Beidou will grow to 400 billion yuan ($57 billion) in 2020, according to Chinese media.

Beijing aims to expand the system worldwide. China and Russia have allied on satellite positioning. Chinese officials are also pouring resources into collaborating with global organizations representing the airline industry and other sectors.

Space is one of the priority areas of Beijing’s “Made in China 2025” plan for boosting self-reliance in vital technologies. By 2030, China aims to become a “space power” alongside the US and Russia. The launch of a Martian probe is set for as early as next year, followed by the completion of a Chinese space station around 2022.

May 27, 2020 Update: Measuring the height of Mt. Everest

China’s network of Beidou satellites are being used in the survey to determine Mt. Everest’s current height and natural resources, the Xinhua News Agency reported. Data on snow depth, weather and wind speed is also being measured to aid in glacier monitoring and ecological protection.

……………………………………………………………………………………………………………………………………………..

References:

https://time.com/5755791/china-beidou-completion/

https://www.space.com/china-launches-beidou-3-satellite.html

Gartner: Market Guide for 3GPP “5G New Radio (NR)” Infrastructure

Editor’s Note:

Most mobile 5G deployments to date are based on 3GPP Release 15 “5G NR” or “NR”in the data plane and Non Stand Alone (NSA), with LTE for everything else (i.e. control plane/signalling, mobile packet core, network management, etc). 3GPP Release 16 will hopefully add ultra low latency, ultra high reliability to the 5G NR data plane. Equally important will be the 5G systems architecture-phase 2 that will be specified in Release 16. That spec includes a 5G mobile packet core (5GC) which is a forklift upgrade from the 4G-LTE Evolved Packet Core (EPC). It remains to be seen which ITU study group will standardized 5GC when 3GPP Release 16 is completed in late June 2020.

From the paper titled Narrowband Internet of Things 5G Performance published in 2019 IEEE 90th Vehicular Technology Conference (VTC2019-Fall):

5G NR supports new frequency bands ranging all the way up to 52.6 GHz. These new frequency bands make large system bandwidths available that are needed to improve the mobile broadband data rates beyond what LTE can offer.

NR also supports a reduced latency by means of reduced transmission time intervals and shortened device processing times compared to LTE. To provide high reliability, NR supports low code rates and a high level of redundancy.

In the initial phase of the transition from 4G to 5G, NR is expected to be a complement to both LTE and NB-IoT, providing enhanced Mobile Broadband (eMBB) and critical IoT services. The past industrial practice suggests that the mobile network operators will stepwise re-farm parts of its LTE spectrum for enabling NR. Since NR supports a new range of frequency bands, an attractive alternative approach is to deploy NR in a set of new rather than existing bands. 3GPP Release 15 allows NR to connect to the EPC to support a seamless transition from LTE to NR.

The NR traffic volumes will eventually motivate a full refarming of the LTE MBB spectrum to NR. The longevity of NB-IoT devices is however expected to make NB-IoT a natural component within the 5G echo-system. For this reason, NR supports reservation of radio resources to enable LTE operation including NB-IoT, within an NR carrier. This allows NB-IoT to add NR in-band operation to its list of supported deployment options. Since both NR and NB-IoT employ an OFDM based modulation with support for 15-kHz subcarrier numerology, in the downlink (DL) true interference-free orthogonality can be achieved without configuration of guard-bands between the two systems.

………………………………………………………………………………………………………..

From Gartner report published Dec 16, 2019:

By Peter Liu, Sylvain Fabre, Kosei Takiishi

Introduction:

As communications service providers move forward with 5G commercialization, New Radio infrastructure investment is prioritized and crucial for 5G rollout success. We analyze the market direction and the product strategies of equipment vendors to help guide product managers in CSPs.

By 2021, investments in 5G NR network infrastructure will account for 19% of the total wireless infrastructure revenue of communications service providers (CSPs), elevated from 6% in 2019.

-

Support for new subcarrier spacing

-

Massive multiple input/multiple output (MIMO)/beamforming

-

Enhanced scheduling by hybrid automatic repeat request (HARQ)

-

Cyclic-prefix orthogonal frequency-division multiplexing (CP-OFDM) and discrete fourier transform spread orthogonal frequency-division multiple access (DFTS-OFDM)

-

Bandwidth part (BWP) and carrier aggregation (CA)

-

New Radio spectrum

-

Optimized orthogonal frequency-division multiplexing (OFDM)

-

Adaptive beamforming

-

Massive MIMO

-

Spectrum sharing

-

Unified design across frequencies

Key Findings:

-

The deployment of 5G New Radio (NR) products will accelerate in 2020, through high total cost of ownership (TCO), absence of “killer application,” unmatured millimeter wave ecosystem and inexpensive device availability that prevent rapid growth in capital investment.

-

Most of current commercial 5G sub-6 gigahertz (GHz) communications service providers (CSPs) also start building their multiband strategy which is in line with their business strategy; for example, sub-1GHz for coverage enhancement and millimeter wave for capacity.

-

Initial 5G deployment was based on non-stand-alone (NSA) architecture which couples the Long Term Evolution (LTE) with 5G NR radio layers to accelerate time to market and reduce cost. This coexistence will last for many years, though specific CSPs may move toward stand-alone (SA) deployment as early as 2020.

-

Open radio access network (RAN) and virtualized RAN (vRAN) have seen an increase in attention after Rakuten Mobile announced its commercial adoption in LTE. However, fragmented standards, incumbent vendor support, technology immaturity and poor fiber availability continue to hamper its success.

Market Description

-

Baseband unit capacity

-

Portfolio broadness

-

Deployment feasibility

-

Technology evolution

Recommendations for 5G Communications Service Providers (CSPs):

-

Build a step-wise 5G NR implementation strategy by initially focusing on best use of existing infrastructure investment, then simplifying the deployment in order to reduce the time to market and minimize risk.

-

Develop spectrum strategies based on business focus, frequencies available as well as ecosystem maturity. Choose the vendors that have preferred radio spectrum support with combinations of spectrum reframing and sharing.

-

Select the 5G NR solution by accessing a vendor’s capabilities of interworking with existing 4G/LTE networks and its ability to provide a high degree of continuity and seamless experience for users. In addition, explore a seamless software upgrade path to enable 5G SA evolution.

-

Build an end-to-end understanding of the Open Radio Access Network (O-RAN) impact on network, operations, performance and procurement by conducting a proof of concept (POC)/pilot.

…………………………………………………………………………………………………………

Acronym Key and Glossary Terms

| 2G |

second generation

|

| 3G |

third generation

|

| 3GPP |

Third Generation Partnership Project

|

| 4G |

fourth generation

|

| 5G |

fifth generation

|

| AAU |

Active Antenna Unit

|

| AI |

artificial intelligence

|

| AR |

augmented reality

|

| ASIC |

application-specific integrated circuit

|

| BBU |

baseband unit

|

| BWP |

bandwidth part

|

| C-RAN |

cloud radio access network

|

| CA |

carrier aggregation

|

| capex |

capital expenditure

|

| CBRS |

Citizens Broadband Radio Service

|

| CoMP |

coordinated multipoint

|

| CP-OFDM |

cyclic-prefix orthogonal frequency-division multiplexing

|

| CPE |

customer premises equipment

|

| CSP |

communications service provider

|

| CU |

centralized unit

|

| DAFE |

Digital/Analog Front End

|

| DFTS-OFDM |

discrete fourier transform spread orthogonal frequency-division multiple access

|

| DIS |

digital indoor system

|

| DL |

downlink

|

| DU |

distributed unit

|

| eCPRI |

enhanced Common Public Radio Interface

|

| eMBB |

enhanced mobile broadband

|

| EPC |

Evolved Packet Core

|

| FDD |

frequency division duplex

|

| FH |

fronthaul

|

| FWA |

fixed wireless access

|

| Gbps |

gigabits per second

|

| GHz |

gigahertz

|

| gNB |

Next Generation Node B

|

| HARQ |

hybrid automatic repeat request

|

| I&O |

infrastructure and operations

|

| IBW |

instantaneous bandwidth (ZTE)

|

| IC |

integrated circuit

|

| ICT |

information and communication technology

|

| IMT-2020 |

International Mobile Telecommunications-2020

|

| IoT |

Internet of Things

|

| ITU-R |

International Telecommunication Union Radiocommunication Sector

|

| LAA |

Licensed Assisted Access

|

| LTE |

Long Term Evolution

|

| LTE-V |

LTE Vehicle

|

| MAA |

Multiple Input/Multiple Output Adaptive Antenna

|

| MHz |

megahertz

|

| ML |

machine learning

|

| MIMO |

multiple input/multiple output

|

| mMTC |

Massive Machine Type Communications

|

| mmWave |

millimeter wave (frequencies above 24GHz)

|

| MOCN |

multioperator core network

|

| MORAN |

multicarrier radio access network

|

| MOS |

Multi-Operator Servers (Mavenir)

|

| NFV |

network function virtualization

|

| NR |

New Radio

|

| NSA |

non-stand-alone

|

| O-RAN |

Open Radio Access Network

|

| OBW |

occupied bandwidth

|

| OEM |

original equipment manufacturer

|

| OFDM |

orthogonal frequency-division multiplexing

|

| opex |

operating expenditure

|

| POC |

proof of concept

|

| PRB |

physical resource blocks

|

| QAM |

quadrature amplitude modulation

|

| R&D |

research and development

|

| RAN |

radio access network

|

| RAT |

Radio Access Technology

|

| RIC |

RAN Intelligent Controller (Nokia)

|

| RF |

radio frequency

|

| RFIC |

Radio Frequency Integrated Circuit

|

| RRU |

remote radio unit

|

| RU |

radio unit

|

| SA |

stand-alone

|

| SDN |

software-defined network

|

| SDR |

software-defined radio

|

| SON |

self-organizing network

|

| Sub-1GHz |

Low-band frequencies are those at 600MHz, 800MHz, and 900MHz.

|

| Sub-6GHz |

Frequencies under 6GHz but above the low-band frequencies (2.5GHz, 3.5GHz, and 3.7GHz to 4.2GHz).

|

| SUL |

Supplementary Uplink

|

| TCO |

total cost of ownership

|

| TD-LTE |

Time Division-Long Term Evolution

|

| TDD |

time division duplex

|

| TRX |

Transceiver/Receiver

|

| UBR |

Ultra Broadband RRU (ZTE)

|

| UL |

uplink

|

| URLLC |

ultrareliable and low-latency communications

|

| VR |

virtual reality

|

| vRAN |

virtualized radio access network

|

| WG2 |

Work Group 2

|

| WG3 |

Work Group 3

|

-

Gartner surveys

-

CSP and vendor briefings, plus discussions

-

Associated Gartner research

-

Gartner market forecasts

-

Gartner client discussions

……………………………………………………………………………………………….

References- related Gartner posts:

Gartner: Telecom at the Edge + Distributed Cloud in 3 Stages

Gartner Group Innovation & Insight: Cutting Through the 5G Hype

Gartner: Telecom at the Edge + Distributed Cloud in 3 Stages

Source: Gartner report on Top 10 Strategic Technology Trends for 2020

Communicating to the Edge — The Role of 5G

Connecting edge devices with one another and with back-end services is a fundamental aspect of IoT and an enabler of smart spaces. 5G is the next-generation cellular standard after 4G Long Term Evolution (LTE; LTE Advanced [LTE-A] and LTE Advanced Pro [LTE-A Pro]).

Several global standards bodies have defined it — International Telecommunication Union (ITU), 3rd Generation Partnership Project (3GPP) [NOT A STANDARDS BODY] and ETSI [Has submitted their IMT 2020 RIT to ITU-R WP5D jointly with DECT Forum].

Successive iterations of the 5G standard also will incorporate support for NarrowBand Internet of Things (NB-IoT) aimed at devices with low-power and low-throughput requirements. New system architectures include core network slicing as well as edge computing.

5G addresses three key technology communication aspects, each of which supports distinct new services, and possibly new business models (such as latency as a service):

■ Enhanced mobile broadband (eMBB), which most providers will probably implement first.

■ Ultra-reliable and low-latency communications (URLLC), which addresses many existing industrial, medical, drone and transportation requirements where reliability and latency requirements surpass bandwidth needs.

■ Massive machine-type communications (mMTC), which addresses the scale requirements of IoT edge computing.

Use of higher cellular frequencies and massive capacity will require very dense deployments with higher frequency reuse. As a result, we expect that most public 5G deployments will initially focus on islands of deployment, without continuous national coverage. We expect that, by 2020, 4% of network-based mobile communications service providers globally will launch the 5G network commercially. Many CSPs are uncertain about the nature of the use cases and business models that may drive 5G. We expect that, through 2022, organizations will use 5G mainly to support IoT communications, high-definition video and fixed wireless access. The release of unlicensed radio spectrum (Citizens Broadband Radio Service [CBRS] in the U.S., and similar initiatives in the U.K. and Germany) will facilitate the deployment of private 5G (and LTE) networks.

This will enable enterprises to exploit the advantages of 5G technology without waiting for public networks to build out coverage. Identify use cases that definitely require the high-end performance, low latency or higher densities of 5G for edge computing needs.

Map the organization’s planned exploitation of such use cases against the expected rollout by providers through 2023. Evaluate the available alternatives that may prove adequate and more cost-effective than 5G for particular IoT use cases. Examples include low-power wide-area (LPWA), such as 4G LTE-based NB-IoT or LTE Cat M1, LoRa, Sigfox and Wireless Smart Ubiquitous Networks (Wi-SUN).

……………………………………………………………………………………………………

Distributed Cloud examines a major evolution in cloud computing where the applications, platforms, tools, security, management and other services are physically shifting from a centralized data center model to one in which the services are distributed and delivered at the point of need. The point of need can extend into customer data centers or all the way to the edge devices.

A distributed cloud refers to the distribution of public cloud services to different locations outside the cloud providers’ data centers, while the originating public cloud provider assumes responsibility for the operation, governance, maintenance and updates. This represents a significant shift from the centralized model of most public cloud services and will lead to a new era in cloud computing.

Concept of Distributed Cloud:

………………………………………………………………………………………..

Gartner expects distributed cloud computing will happen in three phases:

■ Phase 1: A like-for-like hybrid mode in which the cloud provider delivers services in a distributed fashion that mirror a subset of services in its centralized cloud for delivery in the enterprise.

■ Phase 2: An extension of the like-for-like model in which the cloud provider teams with third parties to deliver a subset of its centralized cloud services to target communities through the third-party provider. An example is the delivery of services through a telecommunications

provider to support data sovereignty requirements in smaller countries where the provider does not have data centers.

■ Phase 3: Communities of organizations share distributed cloud substations. We use the term“substations” to evoke the image of subsidiary stations (like branch post offices) where people gather to use services.

Cloud customers can gather at a given distributed cloud substation to

consume cloud services for common or varied reasons if it is open for community or public use. This improves the economics associated with paying for the installation and operation of a distributed cloud substation. As other companies use the substation, they can share the cost of

the installation.

We expect that third parties such as telecommunications service providers will explore the creation of substations in locations where the public cloud provider does not have a presence. If the substation is not open for use by others outside the organization that paid for its installation, then the substation represents a private cloud instance in a hybrid relationship with the public cloud. The distributed cloud supports continuously connected and intermittently connected operation of like-for-like cloud services from the public cloud “distributed” to specific and varied locations. This enables low-latency service execution where the cloud services are closer to the point of need in remote data centers or all the way to the edge device itself.

This can deliver major improvements in performance and reduce the risk of global network-related outages, as well as support occasionally connected scenarios. By 2024, most cloud service platforms will provide at least some services that execute at the point of need.

References:

Gartner Group Innovation & Insight: Cutting Through the 5G Hype

WSJ: China’s financial support aided Huawei’s rise to #1 telecom vendor in the world

China’s tech champion got as much as $75 billion in tax breaks, financing and cheap resources as it became the world’s top telecom vendor

AJW Comment: This is something we’ve thought for years now, but it is not justification for accusing Huawei of spying or hacking for the Chinese government. In our opinion, Huawei’s rise to the top in telecom was greatly aided by China government financial aid/tax breaks and policy favoring domestic suppliers of both telecom equipment and smart phones/tablets and other network connected gadgets. Note that China’s three leading telecom network operators- China Telecom, Unicom and Mobile are state owned. Here’s some revealing documentation:

Huawei (including the HONOR brand) leads the China smartphone market with its market share growing to 36%, reaching a record high. Counterpoint Research, Nov 26, 2019.

“In the third quarter of this year, Huawei shipped 2.12 million tablets in China with a 37.4% market share, surpassing Apple for the first time as the country’s biggest tablet seller, according to statistics from market research firm IDC.” Nov 27, 2019.

Huawei’s Share of the Global Telecom Market Keeps Growing: “New research from Dell’Oro Group indicates that Huawei’s networking business remains almost completely unaffected by the ongoing political noise surrounding the company. Specifically, the firm found that Huawei’s market share grew from 27.7% in 2018 to 28.1% in the first half of 2019. When looking at Q2 2019 alone, Huawei’s market share improved to 29%. The figures put Huawei at the top of the heap in terms of global telecom equipment vendors. Nokia came in second with 15.7% share in the first half of 2019, according to Dell’Oro, while Ericsson was third with 13.1% share.”

………………………………………………………………………………………………………………………………………………………………………………

By Chuin-Wei Yap, Wall Street Journal [email protected]

Tens of billions of dollars in financial assistance from the Chinese government helped fuel Huawei Technologies Co.’s rise to the top of global telecommunications, a scale of support that in key measures dwarfed what its closest tech rivals got from their governments. A Wall Street Journal review of Huawei’s grants, credit facilities, tax breaks and other forms of financial assistance details for the first time how Huawei had access to as much as $75 billion in state support as it grew from a little-known vendor of phone switches to the world’s largest telecom-equipment company—helping Huawei offer generous financing terms and undercut rivals’ prices by some 30%, analysts and customers say.

Huawei is vying to build next-generation 5G telecom networks around the world. While financial support for favored firms or industries is common in many countries, China’s assistance for Huawei, including tax waivers that began 25 years ago, is among the factors stoking questions about Huawei’s relationship with Beijing.

“While Huawei has commercial interests, those commercial interests are strongly supported by the state,” said Michael Wessel, a member of a U.S. congressional panel that reviews U.S.-China relations, in an interview. The U.S. has raised concerns that use of Huawei’s equipment could pose a security risk, should Beijing request network data from the company. Huawei says it would never hand such data to the (Chinese) government.

The largest portion of assistance—about $46 billion—comes from loans, credit lines and other support from state lenders, the Journal’s review showed. The company saved as much as $25 billion in taxes between 2008 and 2018 due to state incentives to promote the tech sector. Among other assistance, it enjoyed $1.6 billion in grants and $2 billion in land discounts.

Huawei said in a statement that it received “small and non-material” grants to support its research, which it said weren’t unusual. Much of the support—for example, tax breaks to the tech sector—was available to others, it noted.

Wu Bangguo—who as a Chinese vice premier oversaw state-owned companies—assembled a team of auditors after tax breaks for Huawei led to accusations around 1998 that it was evading taxes. Huawei was cleared. PHOTO: XINHUA/ZUMA PRESS

…………………………………………………………………………………………………………………………………………………………………………….

The Journal in its research made use of public records including company statements and landregistry documents. The Journal verified its methodology with subsidy analysts, including Usha Haley, professor at Wichita State University, and Good Jobs First, a Washington, D.C., organization that criticizes some tax incentives and provides widely consulted subsidy data.

State assistance for Huawei isn’t always quantifiable. In 1999, China’s central government arranged an unusual intervention to rescue the company from allegations of tax fraud, according to accounts by Chinese and other officials. Local tax breaks for Huawei drew anonymous accusations around 1998 that it was evading taxes. As the company’s business slumped, Li Zibin, then mayor of Shenzhen, where Huawei is based, said he took Huawei’s plight to Chinese then-Vice Premier Wu Bangguo.

Mr. Wu, who oversaw state-owned companies, wasn’t sure at first if he should act. He viewed Huawei as privately owned, according to a transcript of Mr. Li’s remarks at a state conference in 2012. Mr. Wu eventually agreed to assemble a team of auditors, Mr. Li said. Huawei was cleared

within weeks. Messrs. Li and Wu didn’t respond to requests for comment by the Journal.

Huawei’s official grants, disclosed in annual reports, total $1.6 billion since 2008. In the five years to 2018, they were 17 times as large as similar subsidies reported by Nokia Corp. of Finland, the world’s second-largest telecom equipment maker. Sweden’s Ericsson AB, the third largest, posted none in the period.

A Chinese flag flutters at the Beijing headquarters of China Development Bank, which has made a $30 billion credit line available for Huawei’s customers. PHOTO: FLORENCE LO/REUTERS

……………………………………………………………………………………………………………………………………………………………………………………………………………………

In China’s southern city of Dongguan, state records show, Huawei bought more than a dozen state-owned parcels in largely uncontested auctions between 2014 and 2018 for its research campus. The company paid prices that were 10% to 50% of average rates for similarly zoned land in Dongguan, according to Chinese property value databases. The discounts saved Huawei some $2 billion, according to a Journal review. Huawei declined to comment on the estimate. Other savings came from state policies to promote China’s tech sector. Tax deductions and exemptions helped Huawei save up to $25 billion in income, value-added and other taxes in at least the past decade, the Journal estimated. Responding to the estimate, a Huawei spokesman said the company is globally tax-compliant.

In his remarks at the conference, Mr. Li said local officials began waiving or reducing levies on Huawei, including income and value-added taxes, in the early 1990s. Financial support helped the company undercut rivals. In 2010, the European Commission found that Chinese modem exporters including Huawei had benefited from subsidies, according to a confidential report reviewed by the Journal. The commission cut short its probe after the complainant prompting it reached a “cooperation agreement” with the company. Huawei denied receiving such subsidies.

Besides subsidies, Huawei since 1998 has received an estimated $16 billion in loans, export credits, and other forms of financing from Chinese banks for itself or its customers, the Journal found. China’s state-controlled banking system underpins cheap loans that lower costs for Huawei and its customers to buy its products on credit. State lending facilities for Huawei were among the largest in history.

Mega-lenders China Development Bank (CDB) and Export-Import Bank of China in the last two decades made available more than $30 billion in credit lines for Huawei’s customers. World Bank and official data indicate these banks were lending to the company’s clients in developing economies at some 3% in at least Huawei’s first decade abroad, around half of China’s five-year benchmark rate in since 2004.

A Huawei spokesman told the Journal that CDB’s $30 billion credit line “has seldom been more than 10% subscribed” and that customers’ use of the facility “fluctuates over time.” In 2011, Huawei Deputy Chairman Ken Hu said CDB had lent Huawei’s customers $10 billion since 2004. Huawei said that lenders—which it said were mostly non-Chinese banks—account for only 10% of the company’s financing needs as of the end of last year, funded at commercial rates, with the rest coming from Huawei’s own cash flow and business operations.

“If you’re going to buy a house, and if you are able to say you got backing of a half-million-dollar line of credit, that’s going to make you a much stronger bidder,” said Fred Hochberg, former chairman of U.S. Export-Import Bank. “What Huawei did, cleverly, is to make sure that, when

they made a bid, it came with financing terms” that surpassed those of competitors.

Official data show Swedish export authorities provided some $10 billion in credit assistance for Sweden’s tech-and-telecom sector as of 2018; Finland authorized $30 billion in annual export credit guarantees economywide from 2017. Huawei’s largest American competitor, Cisco Systems Inc., received $44.5 billion in state and federal subsidies, loans, guarantees, grants and other U.S. assistance since 2000, Good Jobs

First data show. Cisco didn’t comment.

China’s foreign ministry said in a statement that Huawei is a private company “like many others in China” whose achievements “are inseparable from a good policy environment.”

In summer 2009, Huawei pitched to Pakistan a surveillance system for its capital, Islamabad. Pakistan’s prime minister accepted, but Islamabad lacked funds and its procurement rules required competitive bidding, Pakistan court filings say. The Chinese offered a solution. China Ex-Im would lend Pakistan $124.7 million for the project and waive most of the 3% annual interest on the 20-year loan. There was a condition, Pakistan Supreme Court filings show: Pakistan could choose only Huawei. Pakistan’s government

decided to proceed without competitive bidding.

“On the recommendation of Ex-Im Bank, the prime minister of Pakistan selected Huawei,” theninterior minister Ahsan Iqbal told Pakistan officials.

A Chinese embassy report showed Beijing’s then-ambassador to Islamabad officiating at the project’s inauguration in 2016 alongside Pakistan’s interior minister, standing before an array of glowing security monitors. “The Chinese government funded it and Huawei built it,” the embassy said.

—Matthew Dalton contributed to this article.

Original article appeared at: https://www.wsj.com/articles/state-support-helped-fuel-huaweis-global-rise-11577280736 (on line subscription required for access)

………………………………………………………………………………………………………………………………………………………………………………………………

WSJ Addendum: Aid has included tax savings, state credit facilities, land purchases and government grants

Huawei provides relatively limited disclosures on state incentives it receives. A Wall Street Journal review showed Huawei received as much as $75 billion in state financial assistance, including tax savings, state credit facilities, land purchases and government grants.

In its methodology, the Journal sought to estimate how key state fiscal incentives, adjusted to account for changes in their scope over the years, allowed Huawei to spend more freely. The calculations compared Huawei’s tax payments with the company’s projected tax liability in the absence of such incentives.

The Journal’s review excluded other forms of policy support available to Huawei, such as salary tax benefits, property-tax abatements and subsidized raw materials. The review also excluded tax breaks arising from standard accounting policy, such as tax deductibility for expenses including research and development, business and administration.

The Journal used third-party loan databases, company records and state media reports to calculate state loans made available to Huawei. The Journal’s review was based on the face value of the loans, which aren’t equivalent to subsidy amounts.

Founded in 1987 by former army engineer Ren Zhengfei, Huawei Technologies Co. is a Chinese colossus. The world’s largest supplier of telecom equipment and the No. 2 maker of mobile phones, its technology touches virtually every corner of the globe, and its massive R&D budget has made it a leader in 5G technology. Yet it has long faced scrutiny. Here’s how it found success……

https://www.wsj.com/articles/how-huawei-took-over-the-world-11545735603

…………………………………………………………………………………………………………………………………………………………………………………..

…………………………………………………………………………………………………………………………………………………..

Related NY Times article I thought was fascinating:

At the Edge of the World, a New Battleground for the U.S. and China: The Faroe Islands have become perhaps the most unexpected place for the United States and China to tussle over the Chinese tech giant Huawei.

Strand Consult: 5G in 2019 and 2020 telecom predictions

by John Strand – Strand Consult

Editor’s Note: This article is an abridged version of Strand Consult’s year end telecom review and 2020 forecast. Copy edits (spelling, grammar) were made for correctness- content has not been altered. Emphasis (bold font) was added in places the Editor deemed important.

Stand Consult’s full report is here.

…………………………………………………………………………………….

Introduction

Strand Consult has followed telecommunications industry for almost 25 years. 2019 was a year with much political and regulatory attention and a renewed appreciation for how the industry ensures the digital society that is ubiquitous, fast, safe, green, and inclusive.

5G became a mainstream topic in 2019 and rebooted the discussion of the value that telecommunications brings to society including innovation, security, and inclusion.

Consider the many transformations that the industry has delivered from the invention of the telephone, which required a person (a switchboard operator) to connect two people. Today the digital world, including its businesses, the communications of individuals, and the operations of the public sector is predicated on the advanced infrastructure that the telecom industry provides.

In 2019 Strand Consult published many research notes and reports to help telecom companies navigate a complex world. We focused heavily on the problem of Chinese equipment in telecommunications networks. While the media has largely focused on Huawei, the discussion should be broadened to the many companies that are owned or affiliated with the Chinese government including but not limited to TikTok, Lexmark, Lenovo, TCL, and so on. Although some of our customers disagree with our views, Strand Consult’s job is to publish what is actually happening and how policy decisions may affect their business in the future.

5G launched without a great vision

5G is coming faster and stronger than 2G, 3G or 4G. With each new G, implementation and adoption time gets shorter. However regulators in many countries are failing to keep pace with the technology, as they are behind on frequency allocation and rollout policy. Indeed few regulators have succeeded to make infrastructure rollout more efficient or auctions more speedy. The pressure is on the Federal Communications Commission (FCC) in 2020 to deliver an auction for the C-band so that the US can stay in the global 5G race and correct for the misguided history of handing out frequency to government users without accountability measures in place.

Strand Consult has worked on these problems for years and notes that it is still too difficult and expensive to role out new network in most countries. See our reports on How mobile operators can reduce cost for mobile masts and improve mast regulation, Why the Quality of Mobile Networks Differs, and How to deploy 5G: Best practices for infrastructure, regulation and business models which describe how to address these challenges effectively. In Denmark Strand Consult has helped to reduced total annual rental costs for mobile masts by about 20 percent. In most countries, 5G will be first marketed as an alternative to fixed line broadband. Wireless solutions based on 5G will help stimulate competition.

The performance of most EU countries on 5G is disappointing. Countries which used to lead the world in mobile standards are no where to be found with 5G. Unless the EU reverses course on its anti-investment telecom policy, don’t expect to see the EU lead in 5G or any other G in 2020, 2021, 2022, 2023 or for that matter in 2030. See Strand Consult’s research note Five Nordic Prime Ministers signed an agreement on 5G. Here are five reasons why Europe has already lost the 5G race.

5G will be a repeat of 4G in certain ways

Like 4G, most of the value in 5G will accrue to players other than the telecom operators providing the networks. In 4G, most of the value went to smartphone makers and over the top service (OTT) providers such as Google, Facebook, and Apple. In the vast majority of countries, ARPU and earnings for mobile operators have fallen year after year—even though the speed and quality of mobile networks has increased. Strand Consult would like mobile operators to focus on how partnerships and creative business models can use 5G to create value for their shareholders. Our new research How to deploy 5G: Best practices for infrastructure, regulation and business models can help. Mobile operators have had successful revenue partnerships with premium SMS to develop the service market and MVNO brand strategies to reduce their sales & marketing costs. Operators need to look at these models to find partners for 5G.

OTT, IOT, and all the other services

Already with 5G, we see the world moving to the over the top (OTT) providers and when it comes to Internet of Things (IoT). This creates a challenge for how mobile operators can engage in partnerships and business models. The big question is whether it will be a market that will be dominated by classic mobile operators or by MVNOs like Cisco IoT and Wireless Logic that offer corporate clients one stop shopping. Unless mobile operators are smart, they will relegate themselves to dumb pipes again.

Regulation will hit telecom operators again in 2020

The need for greater security in networks and removing vulnerable elements will hit operators in 2020 with new standards for resilience. While Huawei likes to spin that restrictions on its equipment are mere trade war tactics, the debate about security will become more holistic to encompass the many elements of security including software, practices, and risk management. See Strand Consult’s note on the topic The debate about network security is more complex than Huawei.

The need for network security can be traced through a century of telecom networks. More recently, Strand Consult documented that in 2005, restrictions were placed on Chinese technology for the 3G rollout. It is telling that the current US President defends European technology companies Ericsson and Nokia while many European operators defend their Chinese suppliers. It will be interesting to see whether the new European Commission will finally ”walk the walk” and demand the same safety and security standards of Chinese companies that European, US, Korean and Japanese firms have had to uphold in EU.

Similar to the financial industry, the telecommunications industry will be subject to accountability requirements and compliance to ensure security. The big question is whether it will be easier and cheaper to meet these requirements when using Chinese equipment. Strand Consult doubts this.

The mobile operator’s classic business model is probably dead and buried

Most of the world’s mobile operators have evolved their business model in face of competition and revenue erosion by OTT players. Mobile operator has realize that revenue from traditional streams of voice, SMS, and MMS is in free fall. In 2020 the industry will see a new direction in which operators divide into infrastructure companies and service companies. We believe that this split comes in many forms and models. We think we will see companies that make a classic split, but we also think that we will see companies that will make more creative splits in which divesting masters and towers is just the first step. We expect this trend could translate to spectrum. We envision an industry divided into three elements: infrastructure, services and spectrum.

Such fragmentation will require a new view of spectrum and who owns and how to use spectrum. When it comes to spectrum sharing, dynamic spectrum sharing will open up a number of new technical possibilities. The big question is who is going to use spectrum going forward and who is going to own spectrum on the other.

To see the future spectrum market, look at the introduction of CBRS in USA, a model likely to spread and which is creating a new value chain and dynamic market. Many new and exciting companies have already entered and created equipment and services. This is the same dynamic underpinning the introduction of premium SMS, MVNOs and in connection with the app industry that has emerged at the top of the smartphone universe.

There are now four models of spectrum:

1. Licensed spectrum owned by mobile operators.

2. Dedicated spectrum with optional synchronized sharing (see German model).

3. Unlicensed spectrum with asynchronous sharing.

4. Unlicensed spectrum with synchronized sharing.

Of note is massive rollout of 5G and fixed wireless access (FWA) solutions. If 5G is hot in 2020, then 5G/FWA will be super hot in 2020. Strand Consult’s forthcoming report on 5G/FWA will show how fixed line providers can extend their service and revenue with 5G. The business and economics of this development follow a similar dynamic to the MVNO market, and customers can reuse this knowledge from Strand Consult.

Editor’s Note: There is no standard for 5G/FWA, as IEEE refused to submit IEEE 802.11ax to ITU-R and there no other contenders have been submitted. FWA is not a IMT 2020 use case.

…………………………………………………………………………………………………..

Wireless solutions will battle FTTH for supremacy, but will also partner for opportunity

Remember the many pundits and policymakers who described fiber to the home (FTTH) as the only ”future-proof” solution. Not only was that prediction proven false, but wireless solutions are complements and substitutes. Those FTTH providers which have seen their business languish can get a boost from 5G. Mobile operators aiming for 4G/5G solutions can sharpen competition in the broadband market and cannibalize the DSL/fixed line market.

The year 2020 will see many operators will switch off their 3G network while 2G is on life support. Operators will see value by refarming spectrum to focus on 4G and 5G LTE solutions. The benefits of having a clean 4G / 5G network are so great that upgrading 2G / 3G / 4G to 4G / 5G will mean that operators worldwide will recognize that a total network swap is best.

During the period 2011 – 2016, operators worldwide implemented 4G. At that time, it turned out that the costs associated with rolling out 4G were similar to a network swap and upgrading the existing 2G and 3G networks. During this time many operators replaced their 2G / 3G networks with new networks supporting 2G/3G and 4G. In connection with the introduction of 5G, we will experience the same, and operators such as TDC in Denmark and Telia in Norway have chosen to replace their entire existing network. Read more: The real cost to rip and replace Chinese equipment from telecom networks

Privacy: EU, US and the rest of the world

The drive for online privacy regulation worldwide reflects distrust and disappointment in the large platforms, however regulation frequently has the opposite of the intended effect. 2020 will mark the two-year anniversary of the General Data Protection Regulation (GDPR) in the European Union. For all the policymakers’ promise of a new level playing field, the largest platform companies have increaszed their market share and revenue in the region. In some two decades of successive data protection regulation in the EU, small and medium sized internet companies have failed to grow, and consumer trust online is at its lowest point ever, according to Eurostat. This serves as a proof point for the historical US approach, supporting its risk-based policy which focuses on making rules based upon the sensitivity of data; preserving the mutual interests in accurate data between the user and collector of data; and solving for real, not theoretical, harms. The US has some two dozen information privacy laws and is predicated on a 220 year legal tradition which can deliver tougher oversight, enforcement and penalties that the European approach. A new California law will come into play in 2020 which will likely precipate Congress to make federal rules.

A new appreciation for the role that telecom companies provide for society

2019 was the year in which the telecommunications industry may have to acknowledge that the demands placed on the communication solutions used by the police, the fire department and other emergency units will spread to the mobile networks. We are talking about requirements that are closely linked to the national security policy.

In Europe and in large parts of the world, the focus is on protecting a democratic social model where freedom, freedom of expression, privacy and human rights are important elements. Europe attempts to focus on the rights of citizens, including data protection, and many want to preserve a role for technology to improve the quality of life and add value to our society. In a dictatorship like China, technology is instrumental for the state to fulfill its goals, regardless of whether it improves quality of life or promotes human rights.

Conclusion

We hope that our research note inspires you over the year. 2019 was Strand Consult’s 24th year in business and its 19th year in making predictions in which we try to inform, delight, and challenge our audience. We invite you to see for yourself whether we were right over the years.

Thank you for another great year. Merry Christmas and all the best for 2020.

Sincerely,

John Strand, CEO

………………………………………………………………………………………

Reference:

Again, the complete (unedited and uncut) report is available to read at:

While 5G is live in 5 German cities only 4 cities covered by 4G

This past September, Deutsche Telekom said its 5G service was live in four German cities. Yesterday, it was reported that only five cities in Germany are fully covered with 4G-LTE. That’s according to a crowdsourcing test carried out by Umlaut (formerly P3) and published by the newspaper Die Welt.

German network operators Deutsche Telekom, Vodafone and Telefonica provide complete 4G coverage in Dortmund , Offenbach am Main, Erlangen, Frankenthal and Ludwigshafen get. In those cities, all households and the entire area have full 4G access.

According to the report, the city states of Hamburg , Bremen and Berlin are at the top of the federal states . Mecklenburg-Western Pomerania, Rhineland-Palatinate and Brandenburg are at the bottom of the list. Across Germany and across all three network operators, the Umlaut company rated the mobile network coverage in Germany with 914.5 out of a possible 1,000 points. 1000 points correspond to a full supply.

“The German networks are better than their reputation,” said umlaut telecommunications expert Hakan Ekmen.

In terms of federal states, the city-states of Hamburg, Bremen and Berlin rank at the top of the list for 4G coverage, according to Umlaut, while Mecklenburg-Western Pomerania, Rhineland-Palatinate and Brandenburg are at the bottom of the ranking.

The data collected included the quality of the signal of the network operators and the transmission speeds, among others. The study had access to nearly two billion samples from April to September. The data on network quality are measured automatically in the background of the smartphones in more than 900 different apps. The users do not have to carry out speed tests themselves.

………………………………………………………………………………………………….

Germany has worse 4G-LTE mobile network coverage than many of its European neighbors, according to a 2018 study by the Aachen-based consulting firm P3 that was seen by Agence France-Presse (AFP).

…………………………………………………………………………………………..

References:

https://www.telecompaper.com/news/only-five-german-cities-are-fully-covered-with-4g-study–1321161 (on-line subscription required)

Upstart Wytec International 5G small cell technology for cable operators

Wytec International, Inc., a small San Antonio based technology company with with 11 employees, is ramping up to bring 5G mobile wireless services to cable operators. The company wants to upend the MVNO industry in the U.S. so that cable operators are able to compete on par with mobile carriers. That means removing excess costs with which cable operators currently contend. Wytec owns patented small cell technology now recognized as a key component to delivering 5G fixed and mobile wireless services.

“Our 5G mobile services, offered through a Mobile Virtual Network Operator (MVNO) Agreement, will include a three-option plan designed for cable operators to “compete on par” with U.S. mobile carriers,” comments William Gray, CEO of Wytec.

Since the United States Patent and Trademark Office (USPTO) awarded Wytec its small cell patent known as the Light-Pole Node (LPN-16) on September 15th 2017, Wytec has been testing its unique features, capable of supporting a robust, “neutral host” dense wireless network, utilizing utility poles as its distribution access throughout America’s cities. This feature collaborates exceptionally well with cable operators due to its existing utility pole access. In conjunction with its LPN-16 technology, Wytec’s MVNO solution includes carrier “roaming agreements” allowing cable subscribers access to a worldwide mobile network.

Wytec is nearing completion of a multi-test trial in the Central Business District (CBD) of Columbus, Ohio in preparation of securing its first MVNO Agreement to prospective cable operators in early March of 2020.

As Robert Merola, Wytec’s Chief Technology Officer and President of Wytec, states, “Our initial network deployment originates from one of the top ten Tier One providers in the U.S. and will expand accordingly in support of multiple MVNO cable operators throughout the U.S. We are excited to provide 5G services to the cable industry.”

Wytec has invested more than five years advancing its intellectual property related to fixed and mobile wireless distribution. In September of 2017 Wytec was awarded a “utility” patent on its LPN-16 Small Cell technology from the U.S. Patent and Trademark Office (USPTO) clearing a path for the development of its first 5G network deployment in Columbus, Oho.

Columbus, OH is the site of Wytec’s first 5G trial

……………………………………………………………………………………….

In June of 2019, the FCC awarded an “experimental use” license to Wytec for the testing of the newly issued Citizens Broadband Radio Service (CBRS) spectrum operating in the 3.5 GHz frequency band. The company plans to add fifteen (15) additional markets under an agreement with the sixth largest cable operator in the U.S. (unnamed).

Wytec has been funding its LPN-16 R&D through private Regulation D 506c PPM Offerings (Wytec’s Pre-IPO Offering) to accredited investors and subsequently filed an SEC S-1 registration (Now Effective) in preparation for listing its shares on a public market.

About Wytec

Wytec International, Inc. is a facilities-based wireless operator located in San Antonio, Texas with wireless networks located in San Antonio, Texas; Columbus, Ohio; and Denver, Colorado. Wytec owns six wireless patents with its latest patent focused on 5G small cell technology called the LPN-16. Wytec was named one of San Antonio’s Best Tech Startups in 2018 and 2020 by The Tech Tribune. Learn more at www.wytecintl.com.

Media Contact:

Brianna Lohse, Media Relations

(210) 233-8980

[email protected]

References:

ITU Hosted ICT CxO Meeting: achieving ‘self-driving’ IMT-2020/5G networks

Introduction:

Innovation to achieve ‘self-driving’ IMT-2020/5G networks, collaboration in the interests of 5G security and the value of ‘open’ network concepts were among the key topics discussed at an invitation-only meeting of ICT industry executives (‘CxOs’) held last week in Dubai, UAE, in conjunction with the Telecom Review Leaders’ Summit. The CxO meeting’s discussions revolved around industry preparations for IMT-2020/5G.

CxOs shared insights gained from early 5G deployments and trials of 5G–enabled industrial Internet of Things (IoT) applications. They also discussed the importance of building public trust in autonomous driving and the safety-critical radiocommunications supporting Intelligent Transport Systems.

With a view to discussing industry needs and associated standardization priorities, the meeting brought together representatives of companies including du, Etisalat, Facebook, Fujitsu, Korek Telecom, Krypton Security, Nokia, Orange, Roborace, Rohde & Schwarz, SES Networks and TELUS.

The trends discussed at the CxO meeting reflect the evolution of ITU membership, in particular that of ITU’s standardization arm (ITU-T). ITU-T has welcomed 51 new members in 2019, following 45 new members in 2018.

New ITU-T members include companies in energy and utilities, shipping and logistics, mobile payments, over-the-top applications, automotive, IoT connectivity, blockchain and distributed ledger technologies, quantum communications, cybersecurity, and artificial intelligence and machine learning.

The meeting issued a communiqué summarizing ICT trends of growing relevance to ITU standardization.

< Download the CxO meeting communiqué >

The optimization of network management and orchestration – capitalizing on real-time network performance data, machine learning for prediction and self-learning, and the automated build and configuration of virtual network functions – will improve ICT services and introduce new cost efficiencies, said CxOs.

ITU-R WP 5D will produce a draft new Report ITU-R M.[IMT.C-V2X] on “Application of the Terrestrial Component of IMT for Cellular-V2X.”

3GPP intends to contribute to the draft new Report and plans to submit relevant material at WP 5D meeting #36. 3GPP looks forward to the continuous collaboration with ITU-R WP 5D for the finalization of Report ITU-R M.[IMT.C-V2X].

This optimization is becoming increasingly challenging, and increasingly important, as networks gain in complexity to support the coexistence of a diverse range of ICT services.

CxOs encouraged ITU to study the evolution of network operation and maintenance in view of increasing network complexity and the resulting importance of automation informed by machine learning.

CxOs discussed the progress achieved in responding to the ‘Ottawa Accord’ considered by ITU’s annual Chief Technology Officer (CTO) meeting in Budapest, Hungary, 8 September 2019.

The Ottawa Accord is a set of security priorities developed in June 2019 by network operators, standards bodies and industry associations.

The Budapest CTO meeting endorsed the findings of the Ottawa Accord in relation to three security priorities:

- Global threat exchange: Common understanding of security threats and common terminology to enable the sharing of threat intelligence.

- Best practices for operational security: Best practices for 5G security and widespread commitment to infrastructure protection.

- Security incentives: Measurement schemes based on agreed metrics could bring attention to prevailing levels of security and create incentives for investment in security.

CxOs echoed the sentiment of the Budapest CTO meeting that a holistic approach to 5G security could receive valuable support from a global centre for the development of security solutions and their testing and assurance. Such a ‘living lab’ open to multiple vendors, said CTOs in Budapest, could bring cohesion to 5G security efforts as well as reduce the costs of testing security solutions.

CxOs with experience in the early commercial deployment of 5G reiterated the importance of investment in fibre. Fibre-optic networks form the ‘backbone’ of the ICT ecosystem. Investment in fibre continues to rise, recognizing the importance of this investment to the 5G vision.

Experience with industrial IoT applications as part of the development of 5G-enabled smart sea ports and smart factories, said CxOs, has highlighted the importance of network slicing and shown edge computing to be capable of supporting low latencies. CxOs’ experience with 5G-enabled smart factories, in particular, has shown such factories to be capable of highly efficient production and quality control.

Infrastructure sharing has the potential to assist network operators in reducing time-to-market for new solutions, gaining cost efficiencies and increasing coverage in certain network deployment scenarios.

CxOs illustrated possible scenarios for the sharing of infrastructure such as core networks, central offices, backhaul infrastructure, towers, and RANs.

The meeting considered an example of ‘Multi-Core Operator Networks’, networks said to be capable of reducing an operator’s infrastructure investments through sharing, while improving network performance.

General-purpose ‘white box’ hardware, standardized interfaces and virtualized network elements are the foundations of the ‘open RAN’ concept, said CxOs.

Open RAN could support industry in avoiding the challenges that may result from proprietary RAN interfaces, challenges such as RAN equipment vendor lock-in, limited interoperability between different vendors’ RAN equipment, and limited scope for active RAN sharing.

CxOs offered the view that the standardization of open, interoperable RAN interfaces and RAN functional architecture could support a diverse business ecosystem in deploying and operating RANs with considerable cost efficiency.

ITU has established a new Focus Group on ‘Artificial intelligence for autonomous and assisted driving’ to work towards the establishment of international standards to monitor and assess the performance of the AI ‘Drivers’ in control of automated vehicles.

CxOs discussed the ITU Focus Group’s aim to devise a ‘Driving Test’ for AI ‘Drivers’. The proposed test could become the basis for an International Driving Permit for AI. The right to hold this permit would be assessed continuously, based on the AI Driver’s behavioural performance on the road.

CxOs highlighted their support for the Focus Group’s expected contribution to public trust in automated vehicles as well as the value of ITU collaboration with UNECE in this regard.

Recognizing the importance of new radio technology and applications to Intelligent Transport Systems (ITS), CxOs highlighted the importance of conformance assessment based on harmonized test requirements.

According to the CxOs, compliance, conformance and quality testing will make a key contribution to industry and consumer confidence in safety-critical radiocommunications in the ITS context. Conformance assessment would also support ITS interoperability and cost efficiency, said CxOs.

…………………………………………………………………………………………………………………………………………………………

The participating organizations were:

Arab Information & Communication Technologies Organization (AICTO), du, Etisalat, Facebook,

Fujitsu, Korek Telecom, Krypton Security, Nokia, Orange, Roborace, Rohde and Schwarz, SES

Networks, Telecom Review North America, Telecommunication Industry Association (TIA), TELUS

References:

Intelligence, security and cost efficiency: Industry executives highlight priorities for the 5G era

https://www.itu.int/en/ITU-T/tsbdir/CxO/Documents/Communique%20-%20CxO%20-%20Dubai%202019.pdf

ITU-R WP 5D Dec 2019 meeting #33: activity related to IMT 2020 RIT/SRIT

by ITU-R WP 5D Chair persons with Editor’s Note (and copy edits) by Alan J Weissberger, IEEE Techblog Content Manager

Main activities of WP5D WG Technology Aspects during meeting #33 (Dec 10-13 in Geneva) were:

i) Review additional materials provided by the candidate IMT-2020 RIT/SRIT proponents ETSI (TC DECT) and DECT Forum, Nufront and TSDSI, per the agreed way forward at the 32nd meeting of WP 5D regarding their respective submissions;

ii) Review of external activities in Independent Evaluation Groups (for candidate IMT 2020 RIT/SRITs) through interim evaluation reports;

iii) Continue work on revision of Recommendation ITU-R M.1457-14 (specification of terrestrial radio interfaces for IMT-2000)

iv) Start working on Report ITU-R M.[IMT-2020.OUTCOME].

v) Start working on Recommendation ITU-R M.[IMT-2020.SPECS].

During this meeting, WG Technology Aspects established three Sub-Working Groups (SWG):

– SWG Coordination (Chair: Mr. Yoshio HONDA)

– SWG Evaluation (Co-Chair: Ms. Ying PENG)

– SWG IMT Specifications (Chair: Mr. Yoshinori ISHIKAWA)

…………………………………………………………………………………………………………….

Review of updated materials of IMT-2020 submissions:

As per the agreed way forward at the 32nd WP 5D meeting regarding candidate IMT-2020 RIT/SRIT submissions of ETSI (TC DECT) and DECT Forum, Nufront and TSDSI, the respective proponents provided updated materials of their submissions on September 10th of 2019.

After review of these updated materials of submissions under the IMT-2020 Process Step 3 – Submission / reception of the RIT and SRIT proposals and acknowledgement of receipt, the meeting determined that the submissions of ETSI (TC DECT) and DECT Forum, Nufront and TSDSI are “complete” per Section 5 of Report ITU-R M.2411 (Requirements, evaluation criteria and submission templates for the development of IMT-2020).

Editor’s Note: Also see ITU-R Report M.2412: Guidelines for evaluation of radio interface technologies for IMT-2020.

……………………………………………………………………………………………………………

During the course of this review, documents for observations on the submissions were updated.

Review of interim evaluation reports:

A workshop on IMT-2020 terrestrial radio interfaces evaluation was conducted at beginning of this WP 5D meeting (Dec 10-11, 2019), where the registered independent evaluation groups presented their activities and findings. In addition, some independent evaluation groups also submitted interim evaluation reports. The meeting reviewed these contributions and recorded them.

Report ITU-R M.[IMT-2020.OUTCOME]:

The meeting created the draft detailed workplan and draft working document towards a prelimininary draft new Report ITU-R M.[IMT-2020.OUTCOME] which will collect outcomes from Step 4 to 7 in IMT-2020 development process. Those two documents were carried forward to the next meeting for further work.

Detailed schedule for development of IMT-2020.SPECS:

Detailed workplan for development of draft new Recommendation ITU-R M.[IMT-2020.SPECS] and its working document were developed in the meeting. A related liaison statement to the external organizations was also developed.

……………………………………………………………………………………………………..

Editor’s Note:

IMHO, the IMT 2020.SPECS schedule is NOT realistic, mainly because there isn’t enough time for 5D WG Technology Aspects to evaluate 3GPPs expected Release 16 submission at their June 2020 meeting. Note that China, Korea and India (TSDSI) have all based their IMT 2020 RIT submissions on 3GPP Release 15 “5G NR” data plane which must be enhanced in IMT 2020.SPECs to meet the ultra high reliability/ultra high latency performance requirements for both the data and control planes.

There are only two more WP 5D meetings in 2020 (see last section below) after the June 2020 5D meeting, yet a complete IMT 2020.SPECs must be submitted by Nov 23, 2020 to ITU-R SG 5 (5D’s parent) for approval. If not, IMT 2020 will become IMT 2021 (or later if companion IMT 2020 recommendations have not been approved). What good is it to have a 5G data plane without ultra low latency/ultra high reliability and a 4G (EPC) packet core? With no 5G network management or 5G security specified (presumably by ITU-T)?

Specifically, what if the 5G Mobile Packet Core (3GPP 5GC), enhanced 5G control plane/signaling, 5G network management, 5G security, etc (all in 3GPP Release 16) are not completed in time to be considered by ITU-R or ITU-T in 2020?

Another danger is IMT 2020.SPECS revision control with multiple RIT submissions dependent on 3GPP 5G NR. What if some proponents stick with Release 15 NR while others adopt Release 16 NR in July 2020? And how can all the different proponent IMT 2020 RITs be harmonized to ensure interoperability and roaming?

……………………………………………………………………………………………………..

Objective for the 34th WP 5D meeting – Feb 2020 in Geneva:

The key objectives of WG Technology Aspects for the 34th WP 5D meeting are as follows:

i) Review of external activities and evaluation reports of Independent Evaluation Groups.

ii) Complete evaluation reports summary (IMT-2020/ZZZ).

iii) Continue working on a new Report ITU-R M.[IMT-2020.OUTCOME].

iv) Continue the work on “Over-the-air (OTA) TRP field measurements for IMT radio equipment utilizing AAS” based on the requested response from 3GPP and expected input from other organisations and administrations.

v) Continue working on revision of Recommendation ITU-R M.1457-14.

vi) Continue working on new Recommendation ITU-R M.[IMT-2020. SPECS]

Submitted by Ying Peng, Chair, SWG Evaluation

…………………………………………………………………………………………

M.[IMT-2020.SPECS]:

Under agenda item 4 (PDN Rec. ITU-R M.[IMT-2020.SPECS]), the meeting received two input contributions from Korea, Japan and China.

Both contributions proposed the detailed work plan for developing the new Recommendation ITU-R M.[IMT-2020.SPECS] and the working document towards a preliminary draft new Recommendation.

The meeting reviewed those proposals and discussed the work plan and contents for the working document and agreed the detailed work plan and the working document towards a PDNR (preliminary draft new report).

Detailed workplan and working document towards PDNR M. [IMT‑2020.OUTCOME]

The meeting created the draft detailed work plan and draft working document towards PDNR M.[IMT-2020.OUTCOME] based on the carried forward document and input contributions to this meeting. Two TEMP Documents were created accordingly and will be carried forward to the next meeting.

………………………………………………………………………………………………………

Meeting #33 also created a liaison statement to relevant External Organizations (RIT/SRIT Proponents, potential GCS Proponent(s) of IMT-2020) to request the inputs to 34th and 35th meetings in accordance with Doc. IMT-2020/21. WG-IMT Specification seeks approval of this liaison in WG Technology Aspects Plenary and WP 5D Plenary.

Submitted by Yoshinori ISHIKAWA, Chairman, SWG IMT Specifications

…………………………………………………………………………………………..

RECOMMENDATION ITU-R M.[IMT-2020.SPECS]:

Detailed specifications of the terrestrial radio interfaces of International

Mobile Telecommunications-2020 (IMT-2020)

Scope:

This Recommendation identifies the terrestrial radio interface technologies of International Mobile Telecommunications-2020 (IMT-2020) and provides the detailed radio interface specifications.

Korea, Japan:

[These radio interface specifications detail the features and parameters of IMT-2020, which enable worldwide compatibility, international roaming, access to the services under the usage scenarios including enhanced mobile broadband (eMBB), massive machine type communications (mMTC) and ultra-reliable and low latency communications (URLLC).]

China:

[These radio interface specifications detail the features and parameters of IMT-2020. This Recommendation includes the capability to ensure worldwi.de compatibility, international roaming, access to enhanced mobile broadband (eMBB), massive machine type communications (mMTC) and ultra reliability and low latency communications (URLLC).]

……………………………………………………………………………………………………………

For more details on skeleton IMT 2020.SPECs and related work plan, please see:

China ITU-R WP5D submission: work plan and working document for IMT-2020.SPECS

…………………………………………………………………………………………

Because of their ultra critical importance we repeat the objectives of the last three WP 5D meetings in 2020:

Meeting No. 35 (Jun. 2020, [China])

1 Receive and review information, including the texts for its RIT/SRIT overview sections, List of Global Core Specifications and Certification B by GCS Proponents[1].

2 Reach its conclusion on the acceptability of the proposed materials for inclusion in the working document towards PDN Rec. ITU-R M.[IMT-2020.SPECS].

3 Finalizes the working document including specific technologies (not necessarily including the detailed transposition references) and provisionally agree for promoting the document to preliminary draft new Recommendation.

4 Provide and send liaison of the provisionally agreed preliminary draft new Recommendation ITU-R M.[IMT-2020.SPECS] to the relevant GCS Proponents and Transposing Organizations for their use in developing their inputs of the detailed references.

Meeting No. 36 (Oct. 2020, [India])

1 Update PDNR if there are modifications proposed by GCS Proponent.

2 Perform a quality and completion check of the provisionally agreed final draft new Recommendation ITU-R M.[IMT-2020.SPECS] without the hyperlinks.

3 Have follow-up communications initiated with GCS Proponents and/or Transposing Organizations, if necessary.

Meeting No. 36bis (Nov. 2020, Geneva)

1 Receive Transposition references and Certification C from each Transposing Organization.

2 Perform the final quality and completeness check (with detailed transposition references) of the preliminary draft new Recommendation and promotes it to draft new Recommendation.

3 —>Send the draft new Recommendation ITU-R M.[IMT-2020.SPECS] to Study Group 5 for consideration (at their Nov 23-24, 2020 meeting).

[1] If the GCS Proponentrnal (potential GCS Proponent) decides to use DIS style, it doesn’t need to submit List of Global Core Specifications but needs to submit full materials for describing its RIT/SRIT in the Recommendation and Form B.

………………………………………………………………………………………………….