Infonetics and Frost & Sullivan on Optical Network Hardware and 100G WAN Market

1. Infonetics Research released vendor market share and preliminary analysis from its 1st quarter 2013 (1Q13) Optical Network Hardware report. (Full report published May 24). This new report provides worldwide and regional market size, market share, forecasts through 2017, analysis, and trends for metro and long haul SONET/SDH and WDM equipment, Ethernet optical ports, SONET/SDH/POS ports, and WDM ports. Companies tracked: ADVA, Alcatel-Lucent, Ciena, Cisco, Cyan, ECI Telecom, Fujitsu, Huawei, Infinera, NEC, Coriant (Nokia Siemens Networks), Tellabs, Transmode, Tyco Telecom, ZTE, and others.

OPTICAL MARKET HIGHLIGHTS:

. Worldwide, the overall optical network hardware market, including SONET/SDH and WDM equipment, totaled $2.6 billion in 1Q13

. North America was the only region to post growth in overall optical hardware revenue on a quarterly basis in 1Q13, up 7.5% from 4Q12

. Topping the optical market share leaderboard in 1Q13 are, in alphabetical order, Alcatel-Lucent, Ciena, Fujitsu, Huawei and ZTE

. Ciena is now a larger supplier of WDM gear than Alcatel-Lucent and is 2nd only to Huawei

. Cyan, now publicly traded, grew revenue 86% year-over-year (and is now tracked in Infonetics’ Optical Network Hardware report)

. Nokia-Siemens completed its divestiture of its optical division, now called Coriant (also tracked in Infonetics’ optical report)

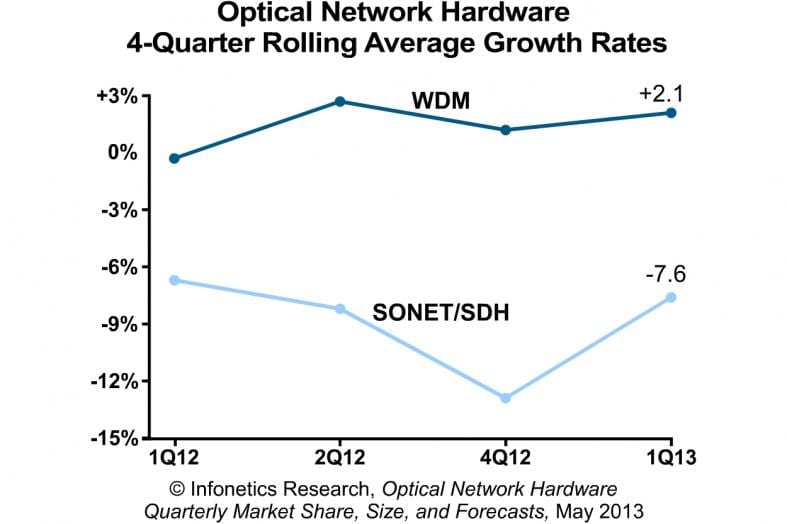

“The 4-quarter rolling average for global optical WDM equipment revenue notched a third consecutive quarter of growth in 1Q13, and we believe the market will continue trending in a positive direction this year,” notes Andrew Schmitt, principal analyst for optical at Infonetics Research.

Schmitt adds: “On a year-over-year basis (1Q12 vs. 1Q13), total optical spending is down 5%, but this is only a result of massive cuts in legacy (SONET/SDH) spending over the past 12 months (down 30%). The WDM segment is up 10% year-over year, a welcome sign that spending in this more relevant segment is returning to long-term trend levels. I won’t call it a recovery until WDM revenue is up by double-digit percents for several quarters on a year-over-year basis, but 2013 is looking good, especially in North America and China, where 100G rollouts are picking up speed.”

To buy the report, contact Infonetics: http://www.infonetics.com/contact.asp

INFONETICS WEBINARS

Visit https://www.infonetics.com/infonetics-events to attend, view on demand, or sponsor Infonetics webinars. Topics available for sponsorship include 100G, OTN, P-OTS, and ROADMs. See http://www.infonetics.com/downloads/Infonetics-Webinars-Available-for-Sponsorship.pdf.

. 100G Optics: Why Operators Are Upgrading Now (Available on demand)

. Leveraging Next-Gen Policy Management Solutions (June 11)

. Integrating SDNs Into the Service Provider Network (June 26)

RELATED OPTICAL RESEARCH from Infonetics:

. Latest Infonetics Optical research brief: http://bit.ly/14JNNRg

. OTN switching reaching mainstream status with service providers

. 100G optical transceiver shipments more than doubling in 2013 and 2014

. Optical transport network (OTN) market to top $13 billion by 2017

. Breakout growth ahead for OTN switching

. Optical transceiver market bolstered as 100G arrives in force

2. Frost & Sullivan Estimates Global 100G Market to Continue to Grow, Reaching $4.8 Billion by 2016

Enterprises and data centers are fueling the global 100G optical network market, which is predicted to increase at a 52.2 percent compound annual growth rate (CAGR), reaching $4.8 billion by 2016, according to market research firm Frost & Sullivan. Since its inception in 2010, the market has growth by 210 percent in 2011 and 387 percent in 2012, according to the research firm.

Alcatel-Lucent, Huawei, Infinera, Ciena and ZTE are the top five 100G vendors, accounting for over 76.2 percent of the market share by unit shipments. The research firm expects these firms to continue to dominate the market because of high barriers to market entry.

According to Frost & Sullivan, the market is mainly driven by the demand for high quality broadband network services, especially by the growing IP traffic and number of broadband subscription during recent years and in the future.

Implementing a 100G optical network results in high network efficiency and reduced per byte transmission costs for data, the research firm noted. Future 100G applications include 4G LTE broadband wireless, metro optical networks and ultra-long reach networks.

Read more: http://www.frost.com/prod/servlet/press-release.pag?docid=278508117

Last week, DukeNet Communications, a regional fiber network provider in the southeastern United States, announced the deployment of 100G across its service area.

http://www.lightwaveonline.com/articles/2013/05/dukenet-communications-touts-100g-capabilities.html