Report from Open Compute Summit & Implications for the Networking Sector – Scott Thompson, FBR Capital Markets

Article written by Scott Thompson of FBR Capital Markets.

References provided by Alan J Weissberger of IEEE ComSoc

OCS Report:

On January 28 and 29, the Open Compute Summit held its annual gathering where hyperscale and large enterprises show cased the creative and cutting-edge work they have pioneered over the past year in a quest to drive costs and complications from the IT landscape. We attended the conference and present some of the more important points below.

* One of the messages with the most impact at Open Compute this year was delivered by Facebook CEO Mark Zuckerberg. He suggested that one of the top strategic priorities at Facebook is to find a way to deliver Internet service to a larger portion of the world’s population. Mr. Zuckerberg stressed that emerging markets (two-thirds of the planet’s population) often do not have the same access to the Internet as does the developed world. Facebook believes that finding a way to provide affordable access to the Internet for those markets represents one of Facebook’s largest growth opportunities. He added that the costs Facebook presently incurs to deploy networks that run its services would need to decline to one-tenth of current rates to make this goal financially achievable. He also added that Facebook has a plan to deliver those types of network efficiencies over the next five years and that the Open Compute Project is an essential cornerstone of that effort.

* We found a chorus of network pioneers at the event that agreed with Mr. Zuckerberg’s assessment. The networking and compute process, when combined in ways that webscale operations have been perfecting for several years, is likely to deliver significant savings, compared to traditional methods and architectures.

Intel is introducing reference designs for “rack-scale architecture” that, by 2015-2016, should dramatically change the way the world processes data and manages compute resources and networks both together.

During a panel hosted by Facebook’s Director of Infrastructure Najam Ahmad, a large number of panelists appeared to confirm that there is a clear and new reference design for how the IT community is beginning to measure efficient datacenter infrastructure.

Martin Casado, PhD & CTO of networking at VMWare, and J.R. Rivers of Cumulus Networks both seemed to agree that the new distributed datacenter model used by many hyperscale networks has achieved new levels of efficiency. Mr. Casado suggested these reference designs, across both enterprise and service verticals, are quickly becoming the de facto standard by which new and more efficient networking technologies can be deployed. He suggested that we may be nearly past the technical barriers required for achieving hypserscale efficiencies and that the primary constraint keeping enterprises and service providers from adopting similar technologies is now cultural. Casado believes that educating those who design and deploy IT systems is now the most effective way to bring about wholesale change across the networking landscape.

* The Open Compute Project (OCP) appears focused on this challenge in 2014. While the pure pace of innovative technology on display at this year’s Open Compute Summit appeared to have slowed, relative to the last one, the mechanisms and framework needed to effect and propagate change appear to be improving dramatically.

The OCP appears to be rapidly gaining the support of the vendor community, bringing it closer to an ecosystem for the acquisition of bespoke networking and compute equipment. From a logical perspective, we continue to have reservations that an “open community” will have the scale and purchasing power to effect change across vendors that might prefer other solutions, but we remain impressed by the scale, scope, and momentum that the OCP has created over the past few years. Whether it proves to be long term or not, Open Compute and its member organizations are changing the face of the IT landscape.

References:

1. SDN Central’s OCP Summit Report:

2. OCP-Network Group Charter & more

http://files.opencompute.org/oc/public.php?service=files&t=437680b2416f9…

3. Broadcom’s Leaf & Spine Network Switch Spec

http://www.opencompute.org/assets/Uploads/Open-Compute-Project-BRCM-Open…

4. Intel’s 10/40 Gigabit Ethernet Rack Mountable Switch Standard, by Michael Miller

Contact: [email protected] for a soft copy (pdf)

AT&Ts earnings report: Smartphone adds and low churn for wireless; Project VIP exceeds build out targets;U-Verse adds too

AT&T’s wireless revenues for the fourth quarter rose 4.8% year over year due mainly to a 16.8% increase in wireless data revenue. Wireless revenue hit $18.4 billion for the quarter and $5.7 billion of that came from data revenue. AT&T noted that data usage per smartphone increased 50 percent annually on its network.

1.2 million smartphones were added to AT&T’s wireless network during the fourth quarter from both new subscribers and from upgrades by existing subscribers. There were 5 million total smart phone additions in 2013. Smartphone adds are important because those subscriptions generate more average revenue per user than traditional cell phones.

While the revenue from mobile data rose, AT&T’s net postpaid adds, totaling 566,000 for the quarter, fell short of rivals Verizon (1.6 million) and T-Mobile (870,000). AT&T said there were tablet 440,000 net adds for the quarter.

AT&T reported a record-low Q4 postpaid churn of 1.11%- significantly lower than the 1.7% churn that T-Mobile says it experienced in the latest quarter.

AT&T added 194,000 TV subscribers in the fourth quarter, bringing the telecom’s total to 5.5 million. The carrier also added 630,000 U-verse broadband customers for a total of 10.4 million. “Plus we had our lowest TV churn ever in the fourth quarter,” Chief Financial Officer John Stephens told analysts Tuesday. Overall, AT&T earned 53 cents a share, higher than analysts had predicted, although the carrier warned of slowing growth in the current quarter. On the wireless side, AT&T added 809,000 subscribers, and profit margins exceeded analysts’ estimates on a 4.8% rise in revenue.

PCWorld/IDG News Service (1/28), Multichannel News (1/28), GigaOm (1/28), Bloomberg Businessweek (1/29)

AT&T’s press release:

AT&T Reports 20 Percent Adjusted EPS Growth, Record-Low Fourth-Quarter Postpaid Churn, Solid Smartphone Gains and Continued Strong U-verse Momentum in Fourth-Quarter Results

Full-Year 2013: Adjusted Revenue Gains of Nearly 2 Percent, Upper-Single Digit Adjusted EPS Growth and Nearly $23 Billion Returned to Shareowners

- $1.31 diluted EPS in the fourth quarter compared to $(0.68) diluted EPS in the year-ago period. Excluding significant items, EPS was $0.53 versus $0.44, up 20.5 percent year over year

- For full-year 2013, excluding significant items and Advertising Solutions, EPS was up 8.2 percent

- Fourth-quarter consolidated revenues of $33.2 billion, up 1.8 percent versus the year-earlier period

- More than 2 million new wireless and wireline high speed broadband connections added in the fourth quarter

- Full-year capital investment of $21 billion while exceeding Project VIP objectives

- $1.9 billion in share buybacks with 54 million shares repurchased in the fourth quarter; for the full year, the company repurchased 366 million shares, or more than 6 percent of shares outstanding, for $13.0 billion

- Nearly $23 billion returned to shareowners in 2013 through dividends and share repurchases

Nation’s Most Reliable 4G LTE Network Drives Revenue Growth, Smartphone Gains and Lowest-Ever Fourth-Quarter Postpaid Churn

- Wireless service revenues up 4.8 percent versus the year-ago quarter, total revenues up 4.5 percent

- Wireless data revenues up 16.8 percent versus the year-earlier period

- Total postpaid ARPU up 2.1 percent; phone-only ARPU up 3.9 percent

- Wireless operating income up $1.4 billion, or 54 percent; wireless EBITDA up $1.5 billion, or 35 percent; wireless operating income margin of 21.4 percent; EBITDA service margin of 37.4 percent

- Lowest-ever fourth-quarter postpaid churn at 1.11 percent

- More than one-half million branded smartphone net adds, both postpaid and prepaid

- 1.2 million new postpaid smartphones added (both upgrades and new subscribers); smartphones account for a record 93 percent of postpaid phone sales

- More than 1 million AT&T Next sales, 15 percent of all postpaid smartphone gross adds and upgrades

- 566,000 wireless postpaid net adds

- 440,000 branded tablet net adds

U-verse® Drives Wireline Consumer Growth and Broadband Gains

- Wireline consumer revenue growth of 2.9 percent versus the year-earlier period

- Total U-verse revenues, including business, up 27.9 percent year over year, now a $13 billion annualized revenue stream

- 10.7 million total U-verse subscribers (TV and high speed Internet) in service:

- 630,000 high speed Internet subscriber net adds; record annual net adds of 2.7 million

- 194,000 U-verse TV subscribers added, lowest churn in product history

- Continued U-verse broadband gains in the business customer segment, up 78,000, nearly doubling year-ago net adds

- Strategic business services growth accelerates with revenues up 17.4 percent year over year, now more than 25 percent of wireline business revenues

Note: AT&T’s fourth-quarter earnings conference call will be broadcast live via the Internet at 4:30 p.m. ET on Tuesday, Jan. 28, 2014, at www.att.com/investor.relations.

DALLAS–(BUSINESS WIRE)–

AT&T Inc. (NYSE:T) today reported solid fourth-quarter results with strong revenue and EPS growth driven by continued gains in the company’s key growth drivers — mobile and IP data, U-verse and strategic business services.

“2013 was the year of the network,” said Randall Stephenson, AT&T chairman and CEO. “With Project VIP, we’re delivering faster speeds and new services to millions more customers. And growth on these platforms is going strong. We exceeded build targets across the board. Our 4G LTE network is nearly complete and is the nation’s most reliable with lightning-fast speeds. U-verse is rapidly expanding, and our fiber-to-the-business build is off to a fast start.

“The next steps are to make our networks even more powerful and layer on services that will drive new growth in the years ahead. We have good momentum in areas like connected car, home automation and mobile business solutions. We’re also committed to transforming our operations to make them more responsive and efficient. To that end, we’ve launched Project Agile, a broad set of initiatives to streamline and improve every part of our business. Execution has begun and will be a focus area for us in 2014 and beyond.”

Infonetics: Little Change in Top Router/Switch Vendors Ranked by Carriers

Infonetics Research released excerpts from its recently published Router and Switch Vendor Leadership: Global Service Provider Survey, which explores service providers’ perceptions of edge router and carrier Ethernet switch (CES) manufacturers and their criteria for choosing vendors.

ROUTER/SWITCH VENDOR LEADERSHIP SURVEY HIGHLIGHTS

•Cisco, the long-term edge router/CES revenue market share leader, is also seen as the #1 edge router/CES manufacturer by operator respondents

•Carriers are looking for the best investment: Survey respondents ranked price-to-performance ratio the #1 criterion when selecting an edge router/CES vendor, followed by product reliability

•Surprisingly, financial stability was rated the least important selection criterion on average•When it comes to service provider familiarity with edge router/CES manufacturers, Tellabs and Brocade scored relatively high given their market share

“The top four vendors in global edge router and carrier Ethernet switch market share—Cisco, Juniper, Alcatel-Lucent, and Huawei—are likewise viewed as the leading manufacturers of edge routers and CES by service providers participating in Infonetics’ just-published router/switch survey,” notes Michael Howard, Infonetics Research’s co-founder and principal analyst for carrier networks. “There’s a big gap between these four and their competitors, and it just gets harder for any manufacturer who’s not already on top of the heap.”

Author’s Note: The above quote implies that Juniper has regained the #2 spot from Alcatel-Lucent. The Infonetics November 26, 2013 Router/Switch report ranked the top four vendors as follows: “Cisco maintains its lead with 38%, Alcatel-Lucent regains 2nd place, Juniper holds #3, while Huawei drops to #4 on the 3Q13 global router/CES revenue share leaderboard.”

ABOUT THE SURVEY

For its latest router/switch vendor leadership survey, Infonetics interviewed network equipment purchase-decision makers at 20 incumbent, independent wireless, competitive, and cable operators from EMEA, Asia Pacific, and North America. Together, the operators represent 36% of global telecom capex. The survey covers service providers’ familiarity with router and carrier Ethernet switch (CES) manufacturers, vendors installed and under evaluation, selection criteria, and their rankings of vendors’ technology innovation, product reliability, management software, security, pricing, price-to-performance ratio, service and support, product roadmap, and financial stability.

To buy the survey, contact Infonetics:

http://www.infonetics.com/contact.asp

DEFINITIONS:

Carrier Ethernet switches (CE switches or CES) are designed for use in service provider networks, primarily for access/aggregation; may have routing functions.

Service provider routers route IP (supporting RIP, BGP, ISIS, and OSPF), support IETF MPLS and PWE3 (Pseudowire Emulation Edge to Edge) services.

For the router/CES data network, we use the terms: access (to buildings, consumers, DSLAMs, cellsites), which feeds up into the aggregation, which connects to the metro core data network.

We use 10GE/40GE/100GE to refer to Ethernet interfaces at speeds of 10G, 40G, and 100G.

NFV (network functions virtualization) is the use of network functions software running on COTS standard servers rather than on special built network products for on-net services, such as CDN, IMS,EPC, DPI, firewall, IDS, spam filter, and turbo charge downloads.

Packet-optical platforms are packet-optical transport systems (P-OTS) that have an architecture that provides all of the following:

- Optical transport features including WDM and ROADM

- Optical circuit switching (SONET/SDH crossconnect and/or OTN) across the chassis

- Support for both optical and layer 2 restoration

- Ethernet switching, including support for connection oriented Ethernet (COE) protocols (e.g.,MPLS-TP, PBB-TE, T-MPLS, switched VLANs) and carrier grade per-flow traffic management

Multi-layer data/transport control plane: combines the control planes of Layer3/Layer2routing/switching equipment with layer 0 (?) and layer 1 transport equipment.

Related: Michael Howard’s Dec 27, 2013 quotes:

“Service providers and vendors have been talking about how to use more optical transport withessential packet functionality to serve as the transport vehicle for packet traffic as an alternativeto routers. Our latest routing strategies study confirms that major changes are underway incarrier networks, with 75% of the operators we talked to using P-OTS (packet-optical transport systems) now or planning to by 2016.”

Howard adds: “Carriers are very interested in 100GE as well. We asked at what price they would buy 100GE for different applications — data center connections, aggregation, core, etc. — and by when. Some operators are already paying 15 times the price of 10GE for 100GE because theyneed it now, and we found that some operators are willing to pay more for 100GE for specificparts of their networks; for example, over a third are willing to pay a premium for routes with lowfiber availability. Still, most carriers will wait until 100GE pricing comes down to 10 times 10GE orlower, so it behooves manufacturers to continue developments that lower the price of 100GE.”

Chairman Tom Wheeler Describes FCC’s Top Priorities during CHM Speech; All-IP Network Transition at Jan 30th FCC Meeting

Introduction:

During his January 8th speech at the Computer History Museum (CHM), FCC Chairman Tom Wheeler told the CHM audience that the U.S. was in a transition to a “4th Network Revolution” that would be led by a transition to an “all-IP” network. The 4th Network is actually a multi-faceted revolution based on IP based packet communications (for voice, data and video) replacing digital circuit switching and analog transmission. Communications protocols are moving from circuit-switched Time-division Multiplexing (or TDM) to IP. 3G and 4G wireless voice and data services are increasingly prevalent, empowering consumers to connect at the place and time of their choosing.

The FCC is the public’s representative in the ongoing network revolution and plans to pursue three main areas in this regard:

1. Promote and incent competition

2. Network Compact with the public, which has four key elements –universal accessibility, reliable interconnection, consumer protection, and public safety and security.

3. Regulatory philosophy based on risk and economic growth.

Wheeler said there were three steps the FCC can take to remove obstacles and to supply inputs, tangible and intangible, to enable innovators to spur growth. These will be the FCC’s top policy initiatives in the coming months and years.

1. Spectrum policy that eliminates risks stemming from the government-mandated misallocation of spectrum. A key area here is the reworking (or repurposing) of analog/broadcast TV spectrum concepts to the new digital realities.

2. Speeding the transition to all-IP networks by preserving the Network Compact. That transition is important because it demonstrates that the Commission will adapt its regulatory approach to the networks and markets of the 21st century. Communications protocols are moving from circuit-switched Time-division Multiplexing (or TDM) to IP. 3G and 4G wireless voice and data services are increasingly prevalent, empowering consumers to connect at the place and time of their choosing.

3. Through the protection of the “Open Internet” that is, today, our largest, global channel of commerce. Unfortunately, the Open Internet and Net Neutrality are now in jeopardy, based on a federal district court ruling. Read the scoop, comment and analysis at: http://viodi.com/2014/01/17/net-neutrality-ruling-the-beginning-of-the-end-or-the-end-of-the-beginning/

Transitioning to an “all-IP” Network:

Wheeler told the CHM audience: “The best way to speed technology transitions is to incent network innovation while preserving the enduring values that consumers and businesses have come to expect. Those values are all familiar: public safety, interconnection, competition, consumer protection and, of course, universal access. They are familiar, and they are fundamental.”

Continuing, he said: “At the January 30th Commission meeting, we will invite proposals for a series of experiments utilizing all-IP networks. We hope and expect that many proposed experiments, wired and wireless, will be forthcoming. Those experiments will allow the networks, their users, the FCC and the public to assess the impact and potential of all-IP networks on consumers, customers and businesses in all parts of our country, including rural America.”

All-IP Network Topic at the FCC’s January 30th Open Commission Meeting:

The FCC Chairman then said that “no one would use a network without being able to make a 911 phone call (to report emergencies and seek help from law enforcement).” That implies that the all-IP (VoIP) network must support 911 calls in a consistent manner. It doesn’t now.

It appears the all-IP network transition will be the number one agenda item at the FCC’s January 30th Open Commission Meeting. The agenda and live streaming info is at: http://www.fcc.gov/events/open-commission-meeting-january-2014

Advancing Technology Transitions While Protecting Network Values is the first agenda item. It’s all about the transition to an all-IP network. “The Commission will consider a Report and Order, Notice of Proposed Rule making, and Notice of Inquiry that invites diverse technology transitions experiments to examine how to best accelerate technology transitions by preserving and enhancing the values consumers have come to expect from communication networks.”

In a November 19, 2013 blog post, Wheeler provided an overview of the all-IP network migration. He wrote: “The way forward is to encourage technological change while preserving the attributes of network services that customers have come to expect – that set of values we have begun to call the Network Compact.”

Wheeler provided an overview of the all-IP network migration. He wrote: “The way forward is to encourage technological change while preserving the attributes of network services that customers have come to expect – that set of values we have begun to call the Network Compact.” Wheeler noted various FCC Commissioner comments in that blog post:

-Commissioner Pai said that the FCC should “embrace the future by expediting the IP Transition.”

-Commissioner Rosenworcel told us that “as we develop a new policy framework for IP networks, we must keep in mind the four enduring values that have always informed communications law — public safety, universal access, competition, and consumer protection.”

-Commissioner Clyburn has called upon the Commission “to carefully examine and collect data on the impact of technology transitions on consumers, public safety and competition.”

AT&T Petition and FCC Technology Transitions Task Force are encouraging trials:

On November 7, 2012, AT&T petitioned the FCC to “Launch a Proceeding Concerning the TDM-to-IP Transition,” GN Docket No. 12-353 (AT&T Wire Center Trials Petition). http://www.att.com/Common/about_us/files/pdf/fcc_filing.pdf

That document requested the FCC to “open a new proceeding to conduct, for a number of select wire centers, trial runs for a transition from legacy to next-generation services, including the retirement of TDM facilities and offerings” and that “the Commission should also seek public comment on how best to implement specific regulatory reforms within those wire centers on a trial basis.”

AT&T requested that the FCC consider conducting trials where certain equipment and services are retired and IP-based services are offered. These geographically limited trial runs, conducted after a public comment period on how they should be carried out, would help “guide the Commission’s nationwide efforts to facilitate the IP transition.”9 Such an approach, AT&T notes, will “enable the Commission to consider, from the ground up and on a competitively neutral basis, what, if any, legacy regulation remains appropriate after the IP transition.”

AT&T has set a date of 2020 to retire its TDM network and has been upgrading its IP-based service capabilities in its wireline markets via Project Velocity IP (VIP). AT&T presented a progress report on the Project VIP at the June 2013 IEEE ComSocSCV meeting. The event summary can be read at: Telco Tours & Seminars Top ComSoc-SCV Activities http://www.comsoc.org/files/Publications/Magazines/gcn/pdf/gcn1213.pdf

The FCC’s new “Technology Transitions Policy Task Force” was asked to move forward with real-world trials to obtain data that will be helpful to the Commission. The goal of any trials would be to gather a factual record to help determine what policies are appropriate to promote investment and innovation, while protecting consumers, promoting competition, and ensuring that emerging all-Internet Protocol (IP) networks remain resilient. The FCC task force is seeking public comment on several potential trials relating to the ongoing transitions from copper to fiber, from wireline to wireless, and from time-division multiplexing (TDM) to IP based packet switched networks.

Technology Trials Proposed:

The aforementioned FCC task force has proposed the following trials related to the all-IP network transition:

http://www.fcc.gov/document/technology-transitions-policy-task-force-see…

-VoIP Interconnection

-Public Safety – NG911

-Wireline to Wireless

-Geographic All-IP Trials

-Additional trials: numbering and related data bases, copper-to-fiber transition, retirement of copper?

The US Telecom Association was very supportive of such trials as well as the previously referenced AT&T petition. In comments submitted on January 28, 2013, the trade organization wrote: “The idea that the Commission should conduct real-world trials in order to better inform itself as to the technological and policy implications of the IP-transition is a way the Commission can continue its commitment to data-driven policy making. The Commission itself has urged carriers to ‘begin planning for the transition to IP-to-IP interconnection’ and the Commission-guided trials urged by AT&T would facilitate this effort.”

“In particular, the AT&T Petition offers an opportunity for the Commission and state regulators to conduct informative, but geographically limited, trial runs for regulatory reform in discrete wire centers. AT&T correctly notes that such an approach will enable the Commission to consider, from the ground up and on a competitively neutral basis, what, if any, legacy regulation remains appropriate after the IP transition.”

US Telecom’s comments can be read at:

http://www.ustelecom.org/sites/default/files/documents/USTelecom-IP-Tran…

Important Unanswered Issues for an all-IP network (i.e. retiring the PSTN/TDM/Digital Circuit Switched Network):

Transition to an “all-IP” network implies retiring the PSTN, TDM/Digital Circuit Switched and all Wireless networks other than 4G with VoIP over LTE. In our opinion, that is a huge undertaking that will be incredibly disruptive and take many years, if not decades. Here are just a few point to ponder:

-Telcos and MSOs must universally deploy broadband for wireline VoIP to be ubiquitous. Currently, they make their deployment/build out decisions strategically- based on reasonable ROI. Not every area in the U.S. has or will have wired broadband as a result.

-Many rural areas have little or no wireless coverage and certainly not 4G-LTE. What happens to people who live in those areas, e.g. Arnold, CA.

-Even if wired or wireless broadband is available in many regions, there is likely to be only one or two network providers at most. Hence, there is little or no choice in service which is effectively a monopoly. Santa Clara, CA is in the heart of Silicon Valley, yet we now have only two choices for wired broadband- AT&T or Comcast.

-There is currently no Universal Service Fund/ Lifeline or discounted rate (for low income folks) for VoIP service. Lifeline service is ONLY available for the PSTN/POTS.

-If an individual or family doesn’t want or can’t afford high speed Internet and/or broadband TV service, then it will most likely be uneconomical for the Telco/MSO to ONLY provide VoIP service over broadband access. This is the case for many poor people and older Americans!

-What happens to faxes/fax machines, which are still overwhelmingly based on analog PSTN access? The death of fax has been predicted for over a decade, yet it is still alive and kicking!

-Battery backup is required for an all-IP network to make emergency phone calls when power is lost. There is a substantial montly charge for a battery backup box for AT&T’s U-Verse VoIP service. An AT&T subscriber must also have battery backup power for the Wi-Fi gateway to enable your AT&T U-verse services to function during a power outage.

http://www.att.com/esupport/article.jsp?sid=KB407650&cv=803#fbid=qLQu26G…

-There will be a huge impact on business customers that use digital circuit switched networks if the proposed all-IP changes happen soon in the affected areas or “wire centers.” What if a company’s main or branch office site(s) are located in an all-IP wire center coverage area? In that case, the business customer would have to give up it’s digital PBXs or hosted ISDN PRI voice trunks and move to SIP trunks–even though the company is not nearly ready for a total enterprise-wide transition to an IP voice network.

-The transition from the classic PSTN to an all IP infrastructure will mandate the end of Signaling System 7 and the entire infrastructure that supports it. This is a substantial undertaking, the consequences of which are not fully understood. Can SS7-based functionalities be replicated on a broadband IP-based network? What would be the equivalent of a “voice grade” circuit? Is a SIP connection a functional equivalent for the key functionalities of SS7 switches? What about SMS/texts?

-The telephone numbering system provides a way for callers served by virtually any service provided in the world to reach one another. What will replace that system has yet to be determined. It surely won’t be an IP address which is often dynamic and allocated for temporarilty reaching IP endpoints.

-Interconnection and Interoperability between IP and TDM networks is a work in progress.

-Quality of Service/Reliability/Resiliency is largely unknown with an all IP network, which would need to scale to replace and reach all PSTN/TDM endpoints. What would constitute an “outage,” and how should “outage” data be collected and evaluated? Here again, the battery back-up on power fail would need to be made mandatory and low cost or no cost to consumers and enterprises.

Closing Comment:

Surely, there are more questions and issues in decommissioning PSTN/TDM/non-4G wireless networks and replacing them with an all-IP network. BT tried to do that over a decade ago with it’s 21st Century Global IP Network, which is a very long way from being realized today. BT hoped to have over 50% of its customers transferred by 2008. Capital expenditure was put at £10 billion over five years, this being 75% of BT’s total capital spending plans in that period. But it didn’t happen and there seems to be no progress reports from BT on 21CN for years! Instead, it appears to have been renamed Next Generation Broadband Network which is described at: http://www.bt-ngb.com/home

This should be a lesson in reality or at least a wake-up call for the FCC, AT&T, US Telecom Association and others who believe that a rapid transition to an all-IP Network is feasible.

References:

http://www.infoworld.com/d/networking/fcc-chief-pushes-open-internet-rob…

http://www.broadcastingcable.com/news/washington/wheeler-fcc-will-look-d…

http://www.mercurynews.com/business/ci_24885303/mountain-view-anti-wirel…

https://www.youtube.com/watch?v=rn_1GjpbLnA

http://www.washingtonpost.com/blogs/the-switch/wp/2014/01/09/fcc-chairman-offers-his-strongest-endorsement-yet-of-net-neutrality/

http://www.networkworld.com/news/2014/010914-fcc-chief-wheeler-pushes-op…

http://www.pcworld.com/article/2086600/fcc-chief-wheeler-pushes-open-int…

http://www.fcc.gov/document/fcc-chairman-tom-wheeler-remarks-computer-hi…

http://www.fcc.gov/blog/ip-transition-starting-now

http://viodi.com/2013/09/25/tc3-part-2-likely-strategic-goals-for-next-f…

http://viodi.com/2013/12/09/fcc-delays-reverse-auction-till-2015-spectru…

http://viodi.com/2013/10/30/new-fcc-chair-tom-wheeler-faces-challenges-i…

Cisco to announce video service& Web conferencing at CES – after exiting consumer networking business

Cisco Systems is expected to announce a cloud-video service along with Web-conferencing capability on Samsung’s Galaxy smartphones, Olga Kharif writes. The company is also expected to tout the “Internet of Everything” and related devices, and a speech by CEO John Chambers today will focus on the platform. “We think the Internet of Everything is the biggest transition for the Internet since the birth of the Internet,” Cisco’s Sr VP Kip Compton said.

The world’s biggest maker of networking equipment has an exhibit on the main floor of the CES trade show this year for the first time. Cisco CEO John Chambers will use his CES keynote to talk about the Internet of Everything, or the idea of adding connectivity to the car, and objects inside homes, offices and retail shops. Last year, Cisco formed a group to focus on the concept, with projects include designing wristwatches for soldiers and centrally linking medical facilities and educational systems inside cities. With more devices coming online, Cisco is working to sell more networking gear as well as software and services.

Cisco said yesterday that it’s teaming up with Samsung to feature its Web conferencing WebEx Meetings app on the home page of some Galaxy tablets. Samsung’s Galaxy devices will let users share their screen, turn a call into a WebEx meeting or start a meeting from a contact list. Galaxy users will get WebEx Meetings Premium 8 accounts for free for six months.

“What you will see on the collaboration side for us is really increasing focus on the mobile devices,” Compton said.

FBR’s Scott Thompson expects strong Optical Networking Market in 2014

Traditional communications equipment companies may struggle through a challenging environment in lower-growth markets over the course of the upcoming year. However, we expect the optical space to experience stronger performance in 2014 versus 2013 as several catalysts combine to drive what will likely be one of the strongest optical cycles the industry has seen in more than two decades.

Additionally, we are in the early stages of a larger shift in the way large-scale data networks are built, in which the new architecture enables more intelligence and flexibility at the optical layer and creates savings at the switching and routing layers. The optical sector is likely to benefit significantly from the shift, potentially beyond what industry analysts are currently forecasting. We believe the optical network business cycle is still several quarters from a peak.

Packet networking, architecture shift, SONET to OTN transition, and hyperscale builds combine to deliver a more balanced, profitable, and prolonged upgrade cycle. Previous upgrade cycles have often been driven by large long-haul backbone upgrades and a mix of optical switching during a relatively short four- to -six-quarter cycle. We expect this cycle to be different, as it is driven by more diversified sources of demand, driving a more profitable mix of optical and electrical switching targeted at creating “large pools of intelligent optical bandwidth,” according to management.

As a result, we expect that growth rates across the sector may prove to be conservative, driving revenue growth well above the current consensus estimates for the sector.

Related networking forecasts from Ovum:

• Telcos will gain confidence to expand software-defined networking (SDN), network virtualization, and network functions virtualization (NFV) trials and early deployments. In 2014, new and revised standards and specifications related to software-defined networking (SDN), network virtualization, and network functions virtualization (NFV) will bring the industry closer to consensus.

• Lower-cost coherent optical metro solutions will hit the market in 2014. Network value will increasingly be driven by software-tunable capabilities, allowing new possibilities for transport network optimization and monetization.

http://ovum.com/press_releases/ovum-predicts-revenue-growth-and-resource…

Related market research from Infonetics:

Global Optical Network Hardware Sales Down, but Up in North America

https://techblog.comsoc.org/2013/11/21/global-optical-network…

Infonetics: 87% of Mobile Operators have Deployed Self Organizing Networks

Infonetics Research released excerpts from its 2013 SON and Optimization Strategies: Global Service Provider Survey, for which Infonetics interviewed wireless, incumbent, and competitive operators around the world about their network optimization strategies and self-organizing network (SON) deployment plans.

SON AND OPTIMIZATION SURVEY HIGHLIGHTS:

. 87% of operators participating in Infonetics’ survey have deployed SON in their networks, up 27% from a year ago

. SON is building momentum in 3.5G network optimization: A few large incumbents have already deployed SON as the key optimization tool for their 3.5G networks, and this trend appears unstoppable

. A large majority of operator respondents view “overall implementation” as the #1 technical challenge when implementing SON

. Two-thirds of respondents are evaluating centralized SON (C-SON) vendors Celcite and InfoVista to manage their distributed SON (D SON) LTE networks

. By 2015, 100% of those surveyed plan to use network- and handset/subscriber-based tools for mobile network optimization, reflecting the growing influence of SON on network self-learning

ANALYST NOTE:

“Mobile operators know they need to keep network operating expenses under control, and they’re placing a big bet on SON while acknowledging the complexity of and their unease with automation that minimizes human intervention and maximizes computerization,” notes Stéphane Téral, principal analyst for mobile infrastructure and carrier economics at Infonetics Research.

“Nonetheless, the ultimate goal is to use cell planning and field testing for zero-touch, self-healing networks,” Téral continues, “But it’ll take some time to get there. SON’s just started, after all.”

SON SURVEY SYNOPSIS:

For its 28-page SON and optimization survey, Infonetics interviewed independent wireless, incumbent, and competitive operators in EMEA, North America, Asia, and Latin America about their network optimization strategies and SON deployment plans. The study provides insights into SON features, drivers, implementation barriers, technical challenges, and vendors. Operators surveyed together represent 1/3 of the world’s telecom capex and carrier revenue and 25% of all mobile subscribers.

To buy the report, contact Infonetics: http://www.infonetics.com/contact.asp

A related Infonetcs report – 2013 Self-Organizing Networks (SON) and Optimization Software – tracks SON software by generation (3G, 4G) and by architecture (centralized, distributed) as well as 2G and 3G optimization software for the mobile network optimization market.

SON AND OPTIMIZATION SOFTWARE MARKET HIGHLIGHTS

. Following 17% growth in 2012 driven by major deployments at AT&T and KDDI and many smaller deals, the global mobile network optimization and self-organizing network (SON) market is on track to grow 13% in 2013

. In a large majority of cases, 3G network optimization, rather than LTE alone, is a key driver for using SON mobile network optimization and self-organizing network (SON) market is on track to grow 13% in 2013

. Over 80% of mobile operators worldwide are using SON for 3G/HSPA/HSPA+ optimization mobile network optimization and self-organizing network (SON) market is on track to grow 13% in 2013

. Centralized SON (C-SON) is predominant in optimization schemes

. The burgeoning SON segment of the market tripled in 2012

. Infonetics forecasts optimization and SON software to grow to nearly $5 billion by 2017

ANALYST NOTE:

“Self-organizing networks (SON) remain baked in LTE, but as an evolutionary 3GGP technology, SON will continue to evolve, offering more and more advanced features. So deploying SON for 3G optimization – with the zero-touch network as the long-term goal – is something that’s natural and logical for many operators,” notes Stéphane Téral, principal analyst for mobile infrastructure and carrier economics at Infonetics Research.

Téral adds: “There is at least one cumbersome task, however, that can’t be easily automated and will require human intervention for quite a long time: drive testing. Our discussions with large mobile operators confirm there’s no way to replace today’s rudimentary technique of having a crew cruising a neighborhood in a truck to measure what’s going on.”

SON AND OPTIMIZATION SOFTWARE REPORT SYNOPSIS:

Infonetics’ annual SON and optimization software report provides worldwide and regional market size, forecasts through 2017, analysis, and trends for the mobile network optimization market, including 2G and 3G optimization software and self-organizing network software by generation (3G, 4G) and by architecture (centralized, distributed). The report includes a mobile subscriber forecast (2G/3G/4G subscribers), a specialist vendor snapshot, and SON use cases from the Next Generation Mobile Networks (NGMN) Alliance.

The report tracks Tier 1 mobile infrastructure vendors with mobile network optimization tools, including Alcatel-Lucent, Ericsson, Huawei, NSN, Samsung, and ZTE, as well as specialist vendors: Actix/Amdocs, Aircom International, Airhop Communications, Aricent, Ascom, Astellia, Axis Technologies, Celcite, Cellwize, Celtro, Centri, Cisco (Intucell, Ubiquisys), Commsquare, Eden Rock Communications, Forsk, Infovista, InterDigital, JDSU/Arieso, Newfield Wireless, Optulink, P.I.Works, Plano Engineering, Reverb Networks, Schema, Teoco/Schema, Theta Networks, TTG International, Tulinx, Vector, and Xceed Technologies.

To buy the report, contact Infonetics: http://www.infonetics.com/contact.asp

Carrier WiFi: Market Research firms draw different conclusions..

Infonetics Research released excerpts from its latest Carrier WiFi Equipment report, which tracks WiFi equipment deployed by operators in public spaces for wireless internet access.

CARRIER WIFI EQUIPMENT MARKET HIGHLIGHTS:

. Globally, revenue for carrier WiFi equipment, including carrier WiFi access points and WiFi hotspot controllers, totaled $338 million in the first half of 2013 (1H13)

. Carrier WiFi revenue has already surpassed 2/3 of total revenue for the prior year

. The majority of carrier WiFi access points are WiFi hotspots

. North America has consistently dominated carrier WiFi revenue share since 2007, though by 2017 regional share shifts to Asia Pacific and EMEA

. As the carrier WiFi market evolves and more operators launch carrier WiFi services, Infonetics expects fluctuations in market share, with the top 5 positions-currently held by Cisco, Ericsson, Huawei, Ruckus, and Alcatel-Lucent-potentially shuffled

ANALYST NOTE:

“Over the 5 years from 2013 to 2017, operators will spend a cumulative $8.5 billion on carrier WiFi equipment, led by mobile operators using carrier WiFi for data offload,” said Richard Webb, directing analyst for microwave and carrier WiFi at Infonetics Research. “This strong growth will gain additional impetus from the proliferation of small cells with integrated WiFi over the coming years.”

REPORT SYNOPSIS:

Infonetics’ carrier WiFi report provides worldwide and regional market size, market share, forecasts through 2017, analysis, and trends for WiFi hotspot controllers and WiFi-only and dual-mode cellular/WiFi access points. The report includes carrier WiFi vendor announcements and customer wins and a Mobile Operator WiFi Offload Strategies Tracker. Vendors tracked: Airspan, Alcatel-Lucent, Cisco, Aruba Networks, Edgewater Wireless, Ericsson (BelAir Networks), Huawei, Motorola Solutions, NSN, Ruckus Wireless, and others.

To buy the report, contact Infonetics: http://www.infonetics.com/contact.asp

The “Wireless Network Infrastructure Bible: 2014 – 2020 – Macrocell RAN, Small Cells, RRH, DAS, Cloud RAN, Carrier WiFi, Mobile Core & Backhaul” report presents an in-depth assessment of 9 individual submarkets of the wireless network infrastructure opportunity. Besides analyzing the key market drivers, challenges, operator revenue potential, regional CapEx commitments, expert interviews and vendor strategies, the report also presents revenue and unit shipment forecasts for the market from 2014 to 2020 at a regional as well as a global scale. Historical figures are also provided for 2010, 2011 and 2013.

Key Findings:

The report has the following key findings:

- Between 2014 and 2020, the 2G, 3G & 4G wireless network infrastructure market is expected to grow at a CAGR of nearly 5%

- Vendors are increasing their focus on profit margins. Many are already cutting staff, embracing operational excellence, evolving their new business models, acquiring niche businesses and expanding their managed services offerings

- New CapEx commitment avenues such as HetNet infrastructure and virtualization will usher industry restructuring. The wireless network infrastructure market will consolidate so as to eliminate one of the current global players by 2020

- As wireless carriers look to offload traffic from their overburdened macrocell infrastructure, HetNet infrastructure will represent a market worth $43 Billion in 2020

- Operators will ramp up on backhaul, aggregation, transport, routing based on IP and Ethernet technologies for offering mobile broadband services

- Developing market growth will be a significant factor during the forecast period, with China and India seeing some of the highest levels of growth, both in terms of shipments and in the size of their installed base. After 2014, developing countries and their requirements will begin to shape future infrastructure technologies and architectures

- Due to the investments in a single RAN technology, future LTE investments will cost much less than early investments of the technology

- Supplemented with a drive towards virtualization, a limited amount of hardware installation will be needed when wireless carriers upgrade to LTE in the future

- From 2016 onwards wireless carriers and vendors will spend at least $1 Billion per annum in R&D spending to drive standardization and commercialization of 5G technology

- Voice over LTE (VoLTE) subscriptions will surpass 700 Million by 2020

In Nov 2013, Research & Markets released a similar report titled: Small cells & Carrier Wifi

The need for Wi-Fi offloading is assessed and the future for carrier Wi-Fi analyzed. The report also presents the firm’s mobile traffic forecasts and identifies the share of mobile traffic offloaded to Wi-Fi. There is also a synopsis in ppt format. The companies evaluated are:

– Airvana

– Alcatel-Lucent

– Broadcom

– Cisco

– Ericsson

– Huawei Technologies

– ip.access

– NEC Corporation

– NETGEAR

– Nokia Siemens Networks

– QUALCOMM

– Samsung Electronics

– UbeeAirWalk

– Ubiquisys

– ZTE

More info at: http://www.researchandmarkets.com/

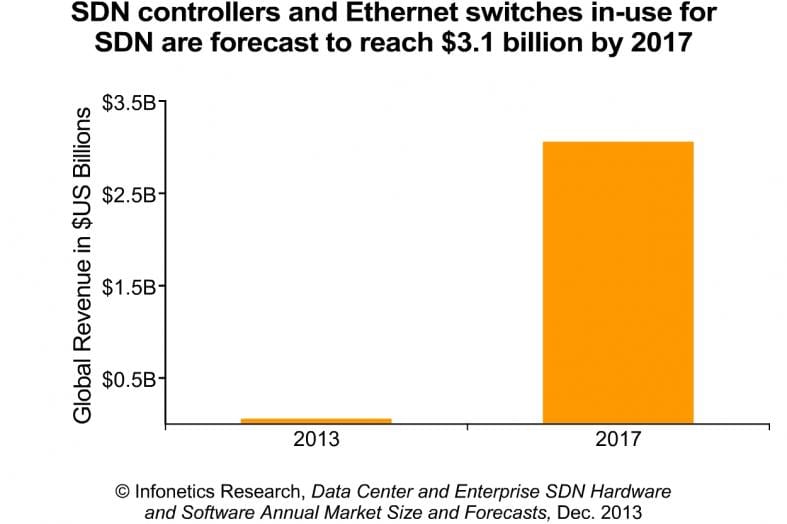

Infonetics: SDN to play big role in Data Centers/Enterprise Networking; IEEE ComSocSCV Jan 8, 2014 Meeting: "Open Networking"

Introduction:

Infonetics Research released market size and forecasts from its new Data Center and Enterprise SDN Hardware and Software report, which defines and sizes the market for software-defined networks (SDN). The report provides data for important SDN market characteristics including product categories, definitions, and worldwide and regional market size. Notably, the report tracks and forecasts SDN controllers and Ethernet switches in-use for SDN – the ‘real’ market for SDN – separately from SDN-capable Ethernet switches.

The report also includes SDN market analysis, trends, vendor announcements, and a tracker of SDN products currently shipping.

ANALYST NOTE:

“The important question that everyone wants answered is, ‘What’s the real market for SDN?’,” says Cliff Grossner, Ph.D., directing analyst for data center and cloud at Infonetics Research. “It’s still early days, but our research over the last two years confirms that SDN controllers and Ethernet switches in-use for SDN will play a role in enterprise and data center networks, growing to a $3.1 billion market by 2017.”

“Wide scale in-use SDN deployments will occur first in the data center with large enterprises and cloud service providers, followed closely by the enterprise LAN,” continues Grossner. “We’re already seeing significant use cases for SDN in the enterprise LAN providing security and unification of wired and wireless networks, and enabling BYOD (bring your own device).”

DATA CENTER AND ENTERPRISE SDN MARKET HIGHLIGHTS:

- SDN is going through a classic market adoption cycle, with many new entrants looking to gain a toe-hold, and the majority of enterprises still kicking the tires.

- Vendors shipping SDN products in 2013 include Alcatel-Lucent, Big Switch, Brocade, Cisco, Cumulus, Dell, Extreme, HP, Huawei, IBM, Juniper, Midokura, NEC, Pica8, Plexxi, Plumgrid, VMware and others.

- The few early deployments for SDN-Google, NTT, AT&T, Verizon, DT, BT, and China Mobile-are in large data centers of cloud service providers and large enterprises.

- 10% of Ethernet switches will be in-use for SDN by 2017.

- North America is where SDN got its start, and the region will claim nearly 50% SDN revenue market share through 2017

To learn more or buy the report, contact Infonetics: http://www.infonetics.com/contact.asp

Jan 8, 2014 ComSoc SCV meeting on Open Networking will address SDN and other approaches to “Open Networking”….

Session Abstract:

“Open Networking” is a very popular industry initiative that aims to make networking equipment programmable and efficient while also lowering costs, especially OPEX.

In this new paradigm, network operators may choose the software to control their networks- independent of their choice of networking hardware. There have been several architectures proposed to realize “Open Networking,” including: Software Defined Networking (SDN)- with strict separation of data and control planes, Overlay models, Network Virtualization (& ETSI NFV), Linux based Network OS’s -with embedded control plane software- running on bare metal switches, and many vendor proprietary solutions.

In this highly informative session, executives from three “Open Networking” vendors (all private companies with no installed base to protect) will address the topic from different perspectives.

-Big Switch Networks CEO will present an overview of recent developments in SDN, describe architectures and use cases and give examples of recent production SDN deployment models;

–Arista Networks CTO will higlight the benefits of a Linux based network OS, including “closed Linux”, “Bare linux”, and “Open Linux”

-Plexxi Co-founder will describe an open policy control and state implementation facilitating true open networking (more than just “programming” network equipment).

The three presentations will be followed by a lively panel session where both pre-submitted and live audience questions/issues will be addressed.

Session Chair: Saurabh Sureka, ComSocSCV Vice Chair

Session Organizer: Alan J Weissberger, ComSoc Community Content Manager

For meeting details and RSVP instructions, please visit: http://comsocscv.org/

Please submit any questions or panel discussion topics to session chair Saurabh Sureka : [email protected]

More Broadband Deployments Needed for Economic Growth

The U.S. labor force is projected to grow slower than in the past, putting negative pressure on the overall rate of economic growth. Broadband-enabled innovations are among the most important drivers of productivity growth, which can help to counterbalance the effect of slower work force growth. Faster, smarter, and more secure broadband networks are critical enablers, providing a mechanism to gather, process, and disseminate valuable information, services, and products.

A primary objective of communications policy should be to encourage the rapid and efficient deployment of more and better broadband capability across the economy, enabling the wide adoption of productivity-enhancing innovations. The U.S. can accomplish this by removing barriers to investment by broadband providers, eliminating legacy burdens, and encouraging the migration to Internet Protocol networks.

AJW Comment: We feel the phase out of the PSTN and replacement with IP Telephony/fax will take much more time than people expect. We’ll provide the reasons why in a forthcoming blog post.