Verizon to launch nationwide LTE Cat M1 wireless network for IoT

On March 31st, Verizon said it will launch a U.S. nationwide Category LTE M1 (Cat M1) wireless network designed to help developers, businesses, utilities and municipalities deploy secure internet-of-things (IoT) devices at lower cost. The LTE Cat M1 network will span 2.4 million square miles and will be the first of its kind, the company said. Cat M1 is competing head on with other Low Power Wireless Wide Area Networks (LPWANs) like LoRa, Sigfox, NarrowBand (NB) IoT, Weightless SIG, and various proprietary specs.

“We are very proud to again demonstrate our innovative leadership by providing this commercially available network for our customers, an industry first,” said Mike Haberman, Network Vice President at Verizon. “As the natural shift from CDMA-based IoT solutions to the more robust and cloud-based LTE technology occurs, it’s important we stay ahead of that technology evolution for our customers so we can continue to provide them service on the best and most advanced wireless network. Our commercial deployment of the nationwide LTE Cat M1 network does just that.”

……………………………………………………………………………………………………………………………..

LTE Cat 1 vs other LPWANs:

Many IoT network technologies have been slow to catch on, due to hype and confusion caused by too many alternatives. As noted above, LTE Cat M1 is a low-power, LPWAN technology that competes most directly with other LPWAN networks like LoRa, Sigfox and NB IoT. Cat M1 and Narrowband run on licensed spectrum, while the others run on unlicensed spectrum which is inherently prone to interference.

Verizon believes Cat M1 will also compete against Bluetooth, ZigBee and Z-Wave, wireless local area network (WLAN) technologies that connect to devices like thermostats and a wide array of appliances, such as washing machines and dryers.

Steve Hilton, an IoT analyst at Machnation thinks Verizon’s Cat M1 and similar networks will be game changers for IoT deployments. “Cat M1 competes directly with Zigbee, Z-Wave and … Bluetooth,” said Mike Lanman, Verizon senior vice president for IoT, in an interview. He added, however, “there will always be other connecting technologies, and some might make more sense economically.”

Hilton agreed that some companies and utilities might want to deploy a Cat M1 approach and pay Verizon a monthly charge for the wireless service instead of managing a WLAN themselves.

“It really depends on how long the enterprise expects the device to live, how much management control the enterprise wants over the IoT network and relative prices,” Hilton said.

LTE Cat M1 Silicon:

Sequans, Altair Semiconductor, Qualcomm, Telit, are among the LTE Cat M1 chip makers.

Verizon’s LTE Cat M1 partners include industry leaders including Sequans, Telit, U-Blox, Sierra Wireless, Gemalto, Qualcomm Technologies, and Altair, who together with Verizon are solving for the next generation of IoT use cases. Today, Verizon offers certified chipsets, modules and devices for Cat M1 from Sequans, Telit, Qualcomm Technologies, Encore Networks, Link Labs, and NimbeLink.

Devices running Cat M1, such as water and power meters and asset trackers, will get longer battery life and can be left unattended for up to a decade, Lanman said. The Cat M1 network will also provide broader and more consistent coverage, reaching areas like basements, and devices that are in-ground or behind walls.

Cat M1 operates at lower bandwidth than 4G LTE, usually between 300Kbps and 400Kbps. Verizon typically provides 4G LTE bandwidth download speeds of 5Mbps to 12Mbps.

Cat M1 would be suitable for wireless connections to devices like water meters that need to send their on-off status or usage readings on an hourly, weekly or monthly basis. It would be unsuitable for connecting to video monitors or devices needing fast video streams, Lanman said.

References:

Is Sprint Prepared for IoT Tsunami?

Sprint Business President Jan Geldmacher detailed the carrier’s vision for the Internet of Things (IoT) in a speech this week, saying the company needs to prepare for a future in which 1 trillion devices can connect to the web. Geldmacher spoke of a converging network in which half a dozen platforms will support IoT, adding:

“Our network infrastructure is not really prepared to deal with all these trends yet.”

Author’s Note:

That’s after at least seven years of a M2M/IoT R&D lab and showcase center in Burlingame, CA which was massively scaled down a couple of years ago. Sprint was a featured speaker at the IEEE ComSocSCV 2010 seminar on IoT/M2M.

……………………………………………………………………………………………………………..

Geldmacher said the network of the future will be a converged network, combining wireless, wireline, Bluetooth, LoRa, Sigfox and unlicensed spectrum. He said mobile networks are about to be part of a sea change that will impact all of society, which he described with a quote from Son.

“The boom in the rate at which we are starting to collect, analyze and ultimately glean knowledge from data is like the Cambrian explosion, the period during which prehistoric creatures developed the five senses,” Geldmacher said in quoting Son.

“When you think about what’s next you really need to think about the megatrends,” Geldmacher said, noting demographic changes, globalization and digitization are all impacting network traffic. “Our network infrastructure is not really prepared to deal with all these trends yet.”

“We are talking about an explosion of data volumes of probably a factor of 2,400. We are talking about creating latencies that come close to the reaction time of a human being,” he said.

Geldmacher compared today’s internet of things to the internet in 1997, meaning the basic technology is falling into place but people have not really figured out all the things they can do with it.

“It’s time to innovate now,” Geldmacher said. “If you talk about how the market is divided in the IoT space I think it’s not relevant, because we’re just beginning.

“I offer to those in the room that want to partner, we are ready to partner,” Geldmacher said, adding he encouraged companies that want to make IoT technology part of their business to be brave and to believe the future is not as unpredictable as it may seem. “I think the future looks predictable if you just anticipate what’s happening in technology and apply it in the right way.”

Geldmacher said 94% of IoT investments yield some return on investment. Geldmacher also shared results from a recent survey of enterprises looking at IoT deployments, and listed the benefits that companies say they expect. The expectation named most often was streamlined operations, followed by higher productivity; better safety, security and monitoring; better customer service; improved automation; and increased revenue.

References:

https://business.sprint.com/solutions/internet-of-things/

https://business.sprint.com/tag/internet-of-things/

http://www.iotglobalnetwork.com/companies/single/id/277/sprint

http://www.rcrwireless.com/20170329/internet-of-things/sprint-outlines-vision-for-iot-network-tag4

Vertical Systems Leaderboards (3) for U.S. Carrier Ethernet Services

On March 28th, Vertical Systems released their 2016 Leaderboard for U.S. competitive carrier, cable/MSO, and incumbent carrier Ethernet service providers.

The leaderboards ranks companies in order based on U.S. retail Ethernet port share. Sources for share calculations include Vertical’s base of enterprise installations, plus direct input from its biannual surveys of network providers selling data network services in the U.S. Let’s zero in on competitive carrier Ethernet service providers in this post.

“In order to compete with incumbents and MSOs, competitive providers must excel in key areas like network scalability, dynamic service features, fiber reach, SLAs or network resiliency,” said Rick Malone, principal at Vertical Systems. “Because of these distinctive competencies, it is no surprise that top companies like Level 3 and XO, as well as others in this segment, have been prime acquisition targets for larger service providers.”

Last month, Verizon completed its $1.8 billion purchase of XO Communications’ fiber-optic network business after the Federal Communications Commission’s approval of the deal last November. Year-end 2016 U.S. Ethernet share figures for XO and Verizon are reported separately. CenturyLink is in the process of acquiring Level 3.

Here are Vertical’s rankings:

Other companies in the competitive-provider segment include (in alphabetical order): Alpheus Communications, American Telesis, Birch Communications, EarthLink Business, Electric Lightwave, Expedient, FiberLight, Global Cloud Xchange, GTT, Integra, Lightower, LS Networks, Lumos Networks, Masergy, MegaPath, NTT America, Orange Business, Tata, TelePacific, Telstra, Unite Private Networks and US Signal.

…………………………………………………..

Here’s Vertical’s 2016 Cable/MSO Ethernet Service Leaderboard leaders:

……………………………………………………………………………………………………………………..

Finally, Vertical’s 2016 U.S. Incumbent Carrier Ethernet LEADERBOARD leaders:

Google Fiber Growth down sharply in 2016!

Google Fiber’s video growth dropped to 57.8% in 2016 from 78.8% the previous year, as per a Moffett-Nathanson analysis based on fresh data from the U.S. Copyright Office. Google Fiber ended 2016 with 84,232 pay TV subs, marking a sharp decline in the rate of growth, Moffett-Nathanson found in an analysis

Across all Google Fiber U.S. markets, year-on-year growth declined to 57.8%, from 78.8% a year ago, the market research firm found. But Google Fiber’s video business is still growing amid a rising cord-cutting trend that is affecting most major U.S. pay TV providers.

Update: Google Fiber hasn’t released sub numbers, but a person familiar with its business noted that the unit did double its Internet subs in 2016 compared to all previous years combined that Google Fiber has been in business, and that Google Fiber has generally been seeing strong growth for Internet-only subs, including those that are coming way of Webpass, which is being offered in markets such as San Francisco, San Diego, Chicago, Miami and Boston. Webpass does not provide video service alongside its baseline high-speed Internet offering.

Even without any specific broadband subscriber results provided by either the U.S. Copyright Office or Google parent Alphabet, Moffett said Google Fiber’s video numbers speak volumes about its efforts to make a mark in the broader pay TV industry. It’s not succeeding.

“Seven years after breaking ground in their first broadband market, Google Fiber still accounts for only 0.1% of the U.S. Pay TV industry,” Moffett explained.

Among Google Fiber’s largest individual markets, MoffettNathanson found that the company ended 2016 with 45,096 video subs in its largest market, Kansas City, MO, compared to 28,941 in Kansas City, KS; 5,889 in Austin, Texas; and 2,914 in Provo, Utah.

References:

http://www.multichannel.com/news/content/google-fiber-ended-2016-84232-pay-tv-subs-study/411758

Google Fiber Proposed for Santa Clara; AT&T bids to build CityLinkLA

http://www.mysanantonio.com/news/local/article/Construction-on-backbone-of-Google-Fiber-10851778.php

Google Wants India Telecom Operators to use its “SDN Platform”

Source: Economic Times Telecom

Google Inc is looking to bring more Indian telecom operators on board its software defined networking (SDN)-based platform. The internet search giant says its SDN-based platform enables telecom networks adapt to new services and traffic patterns efficiently.

The company has already teamed up with Bharti Airtel and South Korea’s SK Telecom to pursue this networking initiative.

“We are happy to share our knowledge and capabilities with operators. We are very open to talking about our capabilities on both client and application sides and cloud technologies to carriers across the spectrum,” Gulzar Azad, country head for connectivity at Google India, told ET. “We believe there will be more engagements as we move forward in India as well.”

Google’s (proprietary) SDN-based platform comes at a time when telecom networks are dealing with a huge upsurge in data consumption. The platform also aims to create richer APIs that will enable new operational models and help operators bring new features (such as Smart Offline) to consumers.

“Information on the Android side or devices side and information on app side need to come together with all the data availability on the carrier side to make smarter and intelligent networks in India,” Azad said.

“That’s the future we see where two worlds are coming together and make better experience for users and make much productive data consumption by the users,” he added.

According to Azad, more industry players need to contribute for network infrastructure and optimisation to ensure efficient running of applications and client devices, besides ensuring existence of public WiFi.

“This needs to be there to fulfill the government’s vision and create an environment where data revolution is fulfilled by way of consumption, which is 10 times higher than it is today,” Azad said, adding that the industry is moving towards a data revolution.

Meanwhile, Google is on track to equip another 400 railway stations in India with high-speed WiFi network. With the help of RailTel and Indian Railways, it is currently providing WiFi services at 115 stations.

The company recently won its first city Google Station WiFi deal from Pune Smart City Development Corporation Limited, a special purpose vehicle formed for the smart city mission in the city. The project will be executed in collaboration with companies like IBM, Larsen & Toubro and RailTel.

References:

Google’s Internet Access for Emerging Markets – Managed WiFi Network for India Railways

CenturyLink Delivers Broadband Services on CORD Platform

Less than one year after AT&T took its Central Office Re-architected as a Data center (CORD) to the Linux Foundation, which then produced a reference design, CenturyLink, Inc. says it is the first carrier to use its own virtualized Broadband Network Gateway (vBNG) to support broadband services using the a CORD based design.

This key step in CenturyLink’s efforts to virtualize its infrastructure within the central office is part of the company’s commitment to have full global virtualization coverage in its IP core network by the end of 2019.

Through CORD, CenturyLink is using some version (????) of software-defined networking (SDN) and network functions virtualization (NFV) to bring data center economics and cloud agility to its central offices for fast and efficient delivery of new network services to residential and business customers.

“Our CORD deployment is a significant milestone on our path to achieve full network virtualization,” said Aamir Hussain, CenturyLink’s executive vice president and chief technology officer. “This is a key component in our strategy to bring virtual network services to our customers while driving virtualization into our last-mile network, allowing us to quickly and efficiently deliver new technologies that meet our customers’ rapidly changing needs,” he added.

CenturyLink’s SDN access controller is an OpenDaylight-based controller stack that integrates its legacy operations support systems (OSS) and latest generation orchestration platforms. In addition to virtualizing its infrastructure, CenturyLink continues to develop and implement virtualized services, including a virtual firewall, data center interconnection and software-defined wide area networking (SD-WAN) for enterprise customers. Through these virtualization efforts, CenturyLink is enhancing the customer experience by providing them with more control of their services.

The carrier said it’s also continuing to create and implement virtualized services along with virtualizing its own infrastructure spread out over 55 global data centers. These virtualized services include a virtual firewall, datacenter interconnection and software-defined wide area networking (SD-WAN) targeting enterprises.

Author’s Notes:

There are no implementation standards/interface specs for SD-WAN so there’s no vendor interoperability and hence, it’s a turnkey single vendor solution for a carrier.

While same is true for NFV, but the OPEN NFV (OPNFV) open source group is effectively creating a defacto standard by agreeing to a spec prior to generating open source code.

References:

https://virtualizationreview.com/articles/2017/03/23/centurylink-cord.aspx

AT&T & IBM Partner for New IoT Analytics Tool

AT&T and IBM have teamed up to give enterprise developers a cloud-based tool to analyze data coming from internet of things (IoT) devices. The companies hope to “leverage the data that’s coming off of these devices and create an analytics-as-a-service solution combining the IBM Watson capability sets with our capability sets at AT&T to provide those real meaningful insights across a number of vertical solutions,” said Chris Penrose president of IoT Solutions at AT&T Inc, in an interview with Light Reading. (See IBM to Use AT&T Flexware.)

The impetus behind the development of this new technology stemmed from business customers’ demand for faster data generation from IoT devices as well as rapid, meaningful analysis to make near real-time decisions for process improvements. (See AT&T Introduces IoT Solution Powered by IBM Watson on the Cloud.)

AT&T has connected over 30 million IoT devices globally on its network, and with the new IoT analytics solution, customers can not only connect devices, but also take action and gain insight on transforming their business, reduce costs and create new revenue opportunities, said Penrose.

Customers from a variety of verticals can utilize the technology for uses like detecting anomalies and predicting potential malfunctions in oil and gas wells, analyzing error codes in connected vending machines and determining if the machine is in an ideal location, and monitoring pallet and product location in real-time. The technology isn’t limited to industrial IoT applications, and can be utilized in other verticals such as healthcare, said Penrose.

“A lot of this, whether it’s in heavy equipment machinery or asset tracking, all of these spaces where you get can information off the machine to know if it is operating effectively, potentially diagnose the issue and predict future issues, are great areas of opportunity and we’re mining that data to make it a better solution,” said Penrose.

According to the release, the new analytics technology uses AT&T’s M2X, Flow Designer and Control Center; the IBM Watson IoT portfolio and Data Platform; and IBM’s Machine Learning Service.

References:

IHS Markit: Cloud Service Providers & Telcos to Reign Supreme in Data Center Switching by 2021

By Cliff Grossner, Ph.D., senior research director and advisor, cloud and data center research practice, IHS Markit

Highlights:

- Growth continues for the data center network equipment market, which grew both sequentially and for the full-year 2016

- By 2021, the cloud service provider (CSP) and telco market segments will squeeze the enterprise in data center switching revenue and transmission capacity

- Software-defined enterprise wide area network (SD-WAN) revenue is anticipated to reach $2.9 billion by 2021

IHS Markit Analysis:

Worldwide data center network equipment revenue—including data center Ethernet switches, application delivery controllers (ADCs), SD-WAN and WAN optimization appliances (WOA)—totaled $3.5 billion in Q4 2016, gaining 4 percent from Q3 2016. For the full-year 2016, revenue grew 10 percent to $12.9 billion. Revenue was up in all regions except the Caribbean and Latin America (CALA).

Some results by segment:

- Data center Ethernet switch revenue rose 8 percent in Q4 2016 from the year-ago quarter

- SD-WAN revenue was $31 million in Q4 2016 and hit $87 million for the full-year 2016

- Bare metal switch revenue was up 27 percent year over year in Q4 2016

- ADC revenue was down 3 percent sequentially in 4Q 2016 and down 8 percent year over year

- WAN optimization appliance revenue declined 9 percent in Q4 2016 and fell 20 percent from a year ago

We look for long-term growth in the data center network equipment market to slow to 2018 and then increase out to 2021 as SD-WAN reaches $2.9 billion.

Ethernet switch analysis by market segment:

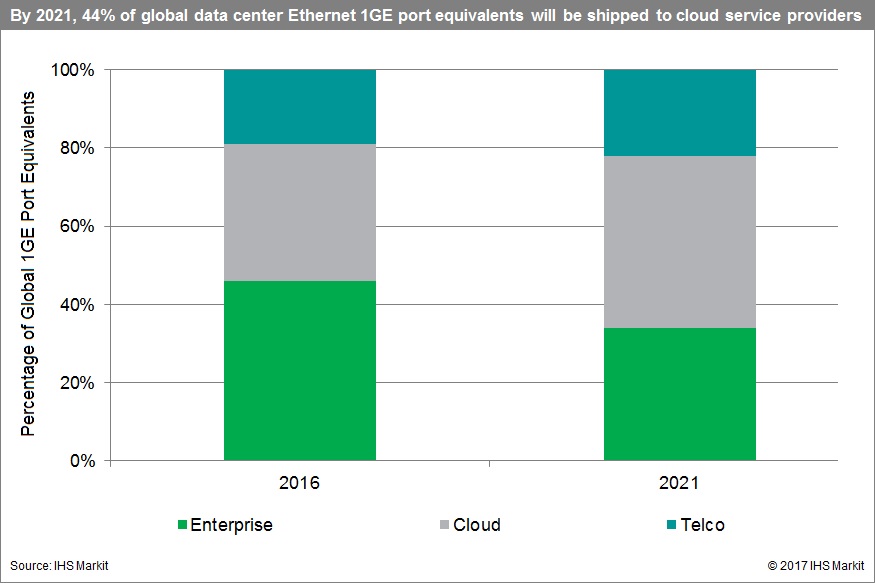

For this latest edition of our data center network report, we added Ethernet switch analysis by market segment: CSP, telco and enterprise—by revenue and port speed (1GE, 10GE, 25GE, 40GE and 100GE).

The CSP and telco segments are expected to squeeze out the enterprise in data center switching by 2021 as Ethernet capacity measured in 1GE port equivalents shipped to CSPs reaches 44 percent of total capacity (up from 25 percent in 2016), to telcos reaches 22 percent (up from 19 percent) and to the enterprise drops to 34 percent.

Barefoot Networks’ Tofino is now available in switches from Taiwan-based Edgecore Networks and WNC. Cavium’s Xpliant-based Wedge 100C switch design contributed to the Open Computer Project (OCP) targeting CSP and telco network virtual function (NVF) markets. Cumulus Networks announced the availability of its operating system for Backpack, Facebook’s white box bare metal chassis, and is partnering with Celestica to make Backpack available for preorder with Cumulus Linux. And Huawei is challenging Arista for the number-two spot in data center Ethernet switching.

Data Center Report Synopsis

The quarterly IHS Markit data center network report provides market size, vendor market share, forecasts through 2021, analysis and trends for data center Ethernet switches, bare metal Ethernet switches, Ethernet switches sold in bundles, application delivery controllers, software-defined enterprise WAN and WAN optimization appliances.

For information about purchasing this report, contact the sales department at IHS Markit in the Americas at (844) 301-7334 or[email protected]; in Europe, Middle East and Africa (EMEA) at +44 1344 328 300 or[email protected]; or Asia-Pacific (APAC) at +604 291 3600 or [email protected]

Century Link Enhances TV Service with 4 Epix Channels; Pay TV Subs Decline

CenturyLink will begin carrying Epix premium TV channels on its Prism TV platform, having reached a deal that includes four Epix channels. Subscribers will also gain access to Epix’s TV Everywhere app, which offers more than 3,000 titles.

Financial terms were not disclosed, but the multi-platform deal does include TV Everywhere access to more than 3,000 titles available from the premium programmer on Epix.com and via the Epix app.

Epix said the deal with CenturyLink marks the third to involve the top ten from NCTC (National Cable Television Cooperative) members within the last year.

It also comes amid some changes to CenturyLink’s video strategy that are well underway.

Multi-Channel News wrote that CenturyLink has already said it is de-emphasizing Prism TV, its current full-freight IPTV service that’s powered by the Ericsson Media room platform, as it moves ahead with a new slimmed-down OTT TV package that, it believes, will be more economically attractive.

Epix is a premium TV service which is a joint venture between Viacom, its Paramount Pictures unit, Lionsgate and Metro-Goldwyn-Mayer Studios Inc. (MGM), is available in more than 50 million homes. It carries block buster movies, a few original content programs, and occasional sports documentaries. Reuters recently reported that MGM is in talks with Viacom and Lionsgate to purchase their stakes in Epix.

Read more at:

http://www.multichannel.com/news/content/epix-centurylink-carve-out-carriage-deal/411616

See the new Epix channel content at:

http://watch.centurylink.net/networks/73083313

………………………………………………………………………..

Addendum: Pay TV Subscribers Decrease

Leichtman Research Group (LRG) noted that Cable TV firms (cablecos or MSOs) lost 278,000 pay-TV video subscribers in 2016. Comcast added 161,000, while telcos (like Century Link) lost 1.5 million, according to LRG. AT&T’s U-verse service accounted for 1.36 million subscriber losses as AT&T shifted marketing toward its DirecTV satellite TV service. DirecTV added 1.2 million customers last year, but Dish Network lost just over 1 million, said LRG.

Analyst say pay-TV industry subscribers could fall further. As cord-cutting goes on and the traditional video business for cable providers shrinks, their No. 1 product will be broadband and internet access. So even if internet video takes off, they still have broadband dominance.

Google-parent Alphabet (GOOGL) has announced YouTube TV, a $35 monthly paid subscription service. Hulu — a joint venture of Walt Disney (DIS), Fox-parent 21st Century Fox Entertainment (FOXA) and Comcast’s NBC Universal — is set to launch yet another live TV streaming service in the spring. And, Amazon.com (AMZN) could follow in 2018. Entertainment (FOXA) and Comcast’s NBCUniversal — is set to launch yet another live TV streaming service in the spring. And, Amazon.com (AMZN) could follow in 2018.

They’ll join AT&T’s DirecTV Now and Dish Network’s (DISH) Sling streaming services.

Reference:

http://www.investors.com/news/technology/comcast-charter-morphing-into-broadband-first-providers/

Highlights of ISQED Conference: March 14-15, 2017 Santa Clara, CA

ISQED Conference Backgrounder:

The 18th International Symposium on Quality Electronic Design (ISQED 2017) is the premier interdisciplinary and multidisciplinary Electronic Design conference—bridges the gap among Electronic/Semiconductor ecosystem members providing electronic design tools, integrated circuit technologies, semiconductor technology,packaging, assembly & test to achieve total design quality.

The ISQED 2017 event is held with the technical sponsorship of IEEE CASS, IEEE EDS, and IEEE Reliability Society.

Highlights of Two Sessions:

1. Terrific panel session on Cybersecurity Challenges for the Automotive Industry at the ISQED conference on Tuesday March 14th.

Abstract: In the past couple of years, we have witnessed one of the most dramatic transformations in automotive industry: vehicles are becoming intelligent and connected. They are not only a tool controlled by the so-called “drivers” to transport people and goods from one place to another. They are “talking” to each other as well as roadside infrastructure, making themselves autonomous or “driverless”. In this panel, we have invited experts to share their views on cybersecurity challenges such as safety, security, and privacy that the automotive industry are facing. Our panelists will also discuss how our life will be changed (again) by the next generation vehicles.

Chair & Moderator:

Professor Gang Qu – University of Maryland

Panelists:

Anuja Sonalker – STEER Tech

Gaurav Bansal – Toyota InfoTechnology Center

Navraj Nandra – Senior Director of Interface IP – Synopsys

………………………………………………………………………………..

2. Session on Design for Smart Sensors and Internet of Things (IoT): Low Power MEMS based Sensors

Author’s Notes:

In an enlightening and stimulating presentation on Low Power MEMS based Sensors, David Horsley, PhD described his research in this field along with commercially available piezo-electronics MEMS based sensors from ST Micro, Avago, and Vesper. He noted that low cost, low power and small footprint size sensors are needed for many IoT applications.

Another very real application of ultrasonic sensors (in a matrix configuration) is a fingerprint reader (and validator) for a smart phone. That would eliminate the need for a password to unlock the phone. Current ultra sonic sensors are too big for that application and also require a lot of external electronics.

David is the CTO of Chirp Microsystems which designs, develops, and manufactures a line of extremely low power, ultrasonic 3D-sensing solutions for consumer electronics, smart homes, industrial automation, and much more. Chirp’s technology was originally developed at the Berkeley Sensor and Actuator Center (BSAC) at UC Berkeley and UC Davis. Horsley showed the audience various functional block diagrams of those sensors used in the fingerprint reader application. The company says that their technology is an enabler for high volume, pervasive computing applications for the Internet of Things (IoT).

………………………………………………………………………………………….