IHS Residential Gateway Survey Highlights + Softness in Cable Broadband Equipment Market to End Later This Year

DEFINITION & SURVEY:

Residential gateways (RGs) combine a DSL, FTTH, cable or 3G/LTE modem with routing and switching capabilities and a WiFi access point, and are increasingly used by service providers to deliver voice, data and video services. For example, this author has a RG for AT&T U-verse, which includes a VDSL modem, WiFi AP for home internet use, and a separate WiFi bridge/ private network for U-verse wireless receivers.

IHS-Infonetics conducted in-depth interviews with service providers across the globe who use residential gateways to provide broadband services and found that only 31% of respondents plan on virtualizing their residential gateways by 2017.

RESIDENTIAL GATEWAY SURVEY HIGHLIGHTS:

- 75% of respondents currently offer Gigabit Ethernet connections on residential gateways, growing to 88% in 2016.

- Among the wireless interfaces IHS asked about, 802.11ac shows the most growth, with 69 percent of respondents saying they plan to include it in their residential gateways by next year.

- Consistent with last year’s findings, Arris topped the list of perceived top residential gateway vendors, followed once again by Pace.

Analyst Quotes:

“Despite the obvious benefits of virtualizing residential gateways in the home-namely shortening of provisioning time and elimination of truck rolls-our survey respondents aren’t completely convinced it’s something they will implement in the next couple of years. Nearly 70 percent said they weren’t planning on doing so or didn’t know if they would be virtualizing their gateways by 2017,” said Jeff Heynen, research director for broadband access and pay TV at IHS.

“Unlike the data center, where virtualization has been in place for some time, it will take longer for service providers to virtualize their residential access networks and CPE,” Heynen said.

SURVEY SYNOPSIS:

The 25-page 2015 “IHS Infonetics Residential Gateway Strategies and Vendor Leadership: Global Service Provider Survey” captures service providers’ strategies for deploying residential gateways and delves into which applications will be the primary drivers for residential gateway deployments. The study also covers service provider opinions of manufacturers including Actiontec, Alcatel-Lucent, Arris/Motorola, Comtrend, D Link, FiberHome, Huawei, Netgear, Pace, Technicolor, ZTE, ZyXel, and others.

Separately, IHS Infonetics said that softness in cable broadband equipment spending seen in the first quarter of 2015 continued into the second, with global revenue dipping 2 percent quarter-over-quarter, according to IHS. Traditionally, the second quarter has been a very good one for cable broadband expenditures.

“Right now, the cable broadband market is like seeing the forest for the trees. The second quarter of the year was slower, but looking at year-over-year revenue comparisons, the market grew by double digits. There’s no question that the continued rollout of 100Mbps+ services via DOCSIS 3.0 today and DOCSIS 3.1 later this year will continue to drive the market forward. There are committed initiatives in place at Comcast and Liberty Global, with others certain to follow as the year progresses,” said Jeff Heynen, research director for broadband access and pay TV at IHS.

In an email, Mr. Heynen wrote to this author: “First, let’s make sure we are talking specifically about the cable broadband CPE market only (DOCSIS modems, etc.) and not the CMTS/CCAP business, which is network infrastructure. If we are comparing revenue for just DOCSIS CPE (no set-top boxes), then pre-Motorola ARRIS had around a 20-25% market share in terms of global revenue, compared with Cisco’s 15-20%. Once ARRIS gobbled up Motorola Home, its global revenue share jumped to 35-40%, while Cisco’s stayed at roughly 15%.”

Author’s Note on Arris:

In an email, Kim Howard, IHS-Infonetics Marketing Manager (and this author’s principal contact at the firm) wrote:

“We’ve been tracking ARRIS for as long as I can remember. The report I looked at goes back only to 2005, but we have older data too. At that time, ARRIS’s cable broadband equipment revenue was only about a quarter of Cisco’s, but then they pulled ahead of Cisco in 2009 by a bit.”

From an April 13, 2010 Forbes article:

“Time Warner Cable and Comcast have increased their business offerings through Arris. Arris has upgraded its modems to the latest DOCSIS 3.0 technology which supports higher broadband speeds up to 100 Mbps. Cable operators like Comcast and Time Warner Cable are now offering higher broadband speeds through Arris modems.”

In April 2013, Google sold its Motorola Home business to Arris. (Google later sold it’s Motorola mobile handset business to Lenovo). Motorola Home covers cable TV modems/set top boxes and internet devices, which combined with Arris’ existing businesses creates what it’s calling “the Premier Video Delivery and Broadband Technology Company.”

In a June 10, 2015 report IHS-Infonetics said “ARRIS dominated the cable broadband market again in 1Q2015, supported in part by the early availability of its E6000 CCAP-capable product.”

CABLE BROADBAND MARKET HIGHLIGHTS:

- Global CCAP, CMTS, CMC and edge QAM revenue totaled $465 million in 2Q15

- In the key North American market, DOCSIS channel shipments were down 25 percent sequentially in 2Q15 after increasing 13 percent in 1Q15; revenue was also down 19 percent due to a slowdown among a handful of larger operators

- Coax media converters are being used in emerging markets, particularly China and Southeast Asia, to provide lower-cost C-DOCSIS services to multiple dwelling units; IHS expects this trend to continue through at least 2019

- Thanks to the early availability of its CCAP-capable product, Arris dominated the cable broadband market once again in Q2, capturing over half of worldwide revenue

To purchase any of the IHS-Infonetics reports, please visit www.infonetics.com/contact.asp

WEBINAR: CABLE SERVICES IN THE CLOUD ERA

Join Jeff Heynen Sept. 29 at 11:00 AM ET for Delivering Cable Services in the Cloud Era, an event examining how virtualization will impact the MSO network and looking at key residential and commercial offerings enabled by NFV and SDN. Register here.

IHS-Infonetics: Mobile Infrastructure Market= $11.4 Billion in Q2; Maturing Market ROI; Ericsson Outlook

Overview:

Driven by strong 3G W-CDMA capacity projects in EMEA and unabated LTE activity in China, the global macrocell mobile infrastructure market was up 2 percent in the 2nd quarter of 2015 (2Q15) from the prior quarter, and up 2 percent year-over-year, according to the IHS Infonetics Mobile Infrastructure Equipment report from IHS (NYSE: IHS).

“This time around, W-CDMA alone pulled the 2G/3G market out of the dumps and contributed to the growth of the whole mobile infrastructure market. Substantial 3G deployments took place in Brazil, India, the Middle East, Myanmar, Thailand and Vietnam,” said Stéphane Téral, research director for mobile infrastructure and carrier economics at IHS.

“Brazil kicked off a massive 2G GSM to 3G W-CDMA migration, and Thailand has ordered mobile operators to shut down their GSM network to re-use the spectrum for LTE,” Téral said.

MOBILE INFRASTRUCTURE MARKET HIGHLIGHTS:

- In 2Q15, the worldwide macrocell mobile infrastructure market totaled $11.4 billion

- LTE revenue was essentially flat (+1 percent) in 2Q15 from 1Q15, but grew 10 percent from the year-ago 2nd quarter

- IHS believes LTE will peak at $23 billion in 2015 and then start to decline as a result of diminishing rollouts worldwide

- 422 commercial LTE networks have been launched as of July 2015, 363 of which are of the FDD (frequency division duplex) variety

- Ericsson and Huawei share the LTE infrastructure market share lead in 2Q15, each claiming just over 20 percent

- Mobile infrastructure software is forecast by IHS to grow at a 5-year (2014–2019) compound annual growth rate of 8 percent

MOBILE INFRASTRUCTURE REPORT SYNOPSIS:

The quarterly IHS Infonetics Mobile Infrastructure Equipment market research report tracks more than 50 categories of equipment, software and subscribers based on all existing generations of wireless network technology, including radio access networks (RANs), base transceiver stations (BTSs), mobile softswitching, packet core equipment and E-UTRAN macrocells. The research service provides worldwide and regional market size, vendor market share, forecasts through 2019, deployment trackers, in-depth analysis and trends. Vendors tracked include Alcatel-Lucent, Cisco, Datang Mobile, Ericsson, Fujitsu, Genband, HP, Huawei, NEC, Nokia Networks, Samsung, ZTE, others.

To buy the report, contact Infonetics: www.infonetics.com/contact.asp

CLOUD RAN WEBINAR:

Join analyst Stéphane Téral Sept. 15 at 11:00 AM ET for How to Achieve Full-Blown Cloud RAN, an event exploring the benefits and challenges operators can expect to encounter on the road to a full-blown cloud RAN architecture. Register here.

RELATED RESEARCH:

- Good News for Mobile Networks in Large Venues: Carriers Adding More DAS

- 5G Hype Aside, True 4G Is Finally Materializing, Says IHS

- Mobile Services Market Dragged by Europe Again

- Operators Spent $67B Outsourcing Network Tasks in 2014

- LTE Peaking at $6 Billion a Quarter – Not Enough to Offset 2G/3G Decline

- Mobile Operators Using EDGE, HSPA+ to Improve User Experience on Road to LTE

Mobile Infrastructure Equipment Market:

The latest report from telecoms research firm Dell’Oro Group (July 2015) forecasts a 2% annual decline in the global mobile infrastructure market between 2014 and 2019.

What are the reasons behind this decline? Firstly, large-scale rollouts of LTE networks in the US and China, the world’s two biggest economies, are coming to an end. In China, operator rollouts of LTE are reaching their peak. Meanwhile, in the US, both Verizon and AT&T have announced their intention to slow down their capital spending after years of intense LTE investment.

Regardless of the rate at which data consumption is growing, CAPEX investment by operators is projected to grow globally at just 1% between 2013 and 2019, with most of this growth coming from emerging markets. In contrast, mature markets such as North America and Western Europe have already slowed to a halt and show negative CAPEX growth for this period.

Revenue trends for the period also highlight the problem for operators to monetize data. Globally, revenues are set to only grow by 1.6% annually up to 2019: once again, it will be emerging markets, and not mature ones, that will deliver this growth (source: Ericsson). This is a clear sign that mobile broadband (like voice before it) is on course to become a commoditised service that offers operators only limited opportunities for differentiation.

A maturing market with limited ROI:

It’s therefore high time to acknowledge that the network equipment market, after almost thirty years, has transformed from a fast-moving, high-growth emerging sector into an established mature market that delivers much lower returns.

The explanation for this is quite simple. Thirty years ago we had no mobile subscriptions and no mobile networks: today we have 7.1 billion mobile subscriptions worldwide and networks that cover 90% of the world’s population.

The success of the mobile industry was built with investment money attracted by the promise of lucrative growth prospects. In those early days, telecoms vendors made a fortune selling expensive infrastructure equipment for operators to build their networks.

However, those days are at an end: technology advances means that today, every node in the network not only costs just 10-20% of what it did 15 years ago, but can also handle 100x more network traffic.

With 90% of the world now covered by mobile networks, new rollouts are also coming to an end. Operators simply have no need to continue building out their macro networks at the same rate and scale as previous years.

Installing new infrastructure – for example, to deliver better coverage in rural areas: or to improve indoor coverage levels – is expensive and delivers only limited returns. Add in the paradox of the sharp rise in data traffic versus flat revenues for operators, and it’s easy to understand why operators are struggling to find new ways to boost margins and deliver growth.It’s this quest for better margins and an uptick in growth that explains the current trend for operator consolidation and the popularity of network-sharing deals. Of course, for equipment providers, these developments mean that their operator customer base is actually now shrinking.

From standardisation to commoditization:

Today’s global mobile telecoms sector could never have achieved the growth and the success it has without standardisation in the industry. This was vital in the early days in order to build a truly international market. Today, however, standardisation serves vendors rather less well. Infrastructure equipment has become a standardised commodity where large scale is all that matters. As a result, we now only have three global vendors competing in a market of ever-decreasing margins and returns.

http://telecoms.com/opinion/telecoms-vendors-reach-their-moment-of-truth/

Ericsson Outlook:

Ericsson has long been a leader in the global mobile infrastructure market, holding a market share of over 30%. However, its share has declined over the past three years due to a technology shift from CDMA to 3G-4G/LTE and growing competition from lower cost China vendors Huawei and ZTE. The company’s mobile infrastructure equipment revenues have been down 6% since 2011, and this trend is expected to continue in the near future, with the Nokia-Alcatel Lucent merger emerging as a threat in the U.S. and Huawei presenting a serious challenge in Europe.

Ericsson has an operating margin of 6-8% on equipment sales. It’s also currently undertaking yet another cost reduction program. The company is looking to build its capacity in the LTE equipment domain, mainly in markets such as India and China, where the LTE presence is still limited. While the technology shift from CDMA/2G/WCDMA to 3G-4G/LTE has negatively impacted Ericsson, the company is not dwelling much on its dominance in the older CDMA domain. Instead, it is evolving with the market, investing in research and development (R&D) related to 4G/LTE and 5G technologies.

Networking Highlights from 2015 Hot Interconnects Conference: Aug 26-28, 2015

Introduction:

The always excellent Hot Interconnects 2015 conference was held in Santa Clara, CA, August 26-28, 2015. This article summarizes presentations and a panel session relevant to Data Center and Wide Area Networking.

Facebook Panel Participation & Intra- DC invited talk by Katharine Schmidtke:

A 90 minute panel session on “HPC vs. Data Center Networks” raised more questions than it answered. While comprehensively covering that panel is beyond the scope of this article, we highlight a few takeaways and the comments and observations made by Facebook’s Katharine Schmidtke, PhD.

- According to Mellanox and Intel panelists, InfiniBand is used to interconnect equipment in HPC environments, but ALSO in large DC networks where extremely low latency is required. We had thought that 100% of DCs used 1G/10G/40G/100G Ethernet to connect compute servers to switches and switches to each other. That might be closer to 90 or 95%, with InfiniBand and proprietary connections making up the rest.

- Another takeaway was that ~80 to 90% of cloud DC traffic is now East-West (server to server via a switch/router) instead of North-South (server to switch or switch to server) as it had been for many years.

- Katharine Schmidtke, PhD talked about Facebook’s intra DC optical network strategy. Katharine is responsible for Optical Technology strategy at Facebook. [She received a PhD in non-linear optics from Southampton University in the UK and did post doctoral work at Stanford University.]

- There are multiple FB DCs within each region.

- Approximately 83% of active daily FB users reside outside the US and Canada.

- Connections between DCs are called Data Center Interconnects (DCIs). There’s more traffic within a FB DC than in a DCI.

- Fabric, first revealed last November, is the next-generation Facebook DC network. It’s a single high-performance network, instead of a hierarchically oversubscribed system of clusters.

- Wedge, also introduced in 2014, is a Top of Rack (ToR) Switch with 16 to 32 each 40G Ethernet ports. It was described as the first building block for FB disaggregatedswitching technology. Its design was the first “open hardware switch” spec contribution to the Open Compute Project (OCP) at their 2015 annual meeting. Facebook also announced at that same OCP meeting that it’s opening its central library of FBOSS – the software behind Wedge.

- Katharine said FB was in the process of moving from Multi-Mode Fiber (MMF) to Single Mode Fiber (SMF) for use within its DC networks, even though SMF has been used almost exclusively for telco networks with much larger reach/distance requirements. She said CWDM4 over duplex SMF was being implemented in FB’s DC networks (more details in next section).

- In answer to a question, Katherine said FB had no need for (photonic) optical switching.

Facebook Network Architecture & Impact on Interconnects:

FB’s newest DC, which went on-line Nov 14, 2014, is in Altoona, IA, which is just north of Interstate Highway 80. It’s a huge nondescript building which is 476K square feet in area. It’s cooled using outside air, uses 100% renewable energy and is very energy-efficient in terms of overall power consumption (more on “power as pain point” below). Connectivity between DC switches is via 40G Ethernet over MMF in the “data hall.”

Fabric (see above description) has been deployed in the Altoona DC. Because it “dis-aggregates” (i.e. breaks down) functional blocks into smaller modules or components, Fabric results in MORE INTERCONNECTS than in previous DC architectures.

As noted in the previous section, FB has DCs in five (soon to be seven) geographic regions, with multiple DCs per region.

100G Ethernet switching, using QSFP281 (Quad Small Form-factor Pluggable) optical transceivers, will be deployed in 2016, according to Katharine. The regions or DCs to be upgraded to 100G speeds were not disclosed.

Note 1. The QSFP28 form factor is the same footprint as the 40G QSFP+.The “Q” stands for “Quad.” Just as the 40G QSFP+ is implemented using four 10-Gbps lanes or paths, the 100G QSFP28 is implemented with four x 25-Gbps lanes or paths.

Cost efficient SMF optics is expected to drive the price down to $1/Gbit/sec very soon. SMF was said to be “future proofing” FB’s intra DC network2, in terms of both future cost and ease of installation. The company only needs a maximum reach of 500m within any given DC, even though SMF is spec’d at 2km. Besides reach, FB relaxed other optical module requirements like temperature and lifetime/reliability. A “very rapid innovation cycle” is expected, Katharine said.

Note 2. Facebook’s decision to use SMF was the result of an internal optical interconnects study. The FB study considered multiple options to deliver greater bandwidth at the lowest possible cost for its rapidly growing DCs. The 100G SMF spec is primarily for telcos as it supports both 10Km and 2Km distances between optical transceivers. That’s certainly greater reach than needed within any given DC. FB will use the 2Km variant of the SMF spec, but only up to 500m. “If you are at the edge of optical technology, relaxing just a little brings down your cost considerably,” Dr. Schmidtke said.

A graph presented by Dr. Schmidtke, and shown in EE Times, illustrates that SMF cost is expected to drop sharply from 2016-to-2022. Facebook intends to move the optical industry to new cost points using SMF with compatible optical transceivers within its DCs. The SMF can also be depreciated over many years, Katharine said.

FB’s deployed optical transceivers will support Coarse Wavelength Division Multiplexing 4 (CWDM4) Multi-Source Agreement over duplex SMF. CWDM4 is a spec for 4 x 25G Ethernet modules and is supported by vendors such as Avago, Finisar, JDSU, Oclaro and Sumitomo Electric.

CWDM4 over duplex SMF was positioned by Katharine as “a new design and business approach” that drives innovation, not iteration. “Networking at scale drives high volume, 100s of thousands of fast (optical) transceivers per DC,” she said.

Other interesting points in answer to audience questions:

- Patch panels (which interconnect the fibers) make up a large part of Intra DC optical network system cost. For more on this topic, here’s a useful guide to fiber optics and premises cabling.

- Power consumed in switches and servers can’t keep scaling up with bandwidth consumption. For example, if you double the bandwidth, you CAN’T double the power consumed! Therefore, it’s critically important to hold the power footprint constant as the bandwidth is increased.

- More power is consumed by the Ethernet switch chip than an optical transceiver module.

- Supplying large amounts of power into a mega DC is the main pain point for the DC owner (in addition to the cost of electricity/power there are significant cooling costs as well).

- FB is planning to move fast to 100G (in 2016) and to 400G Ethernet networks beyond that time-frame. There may be a “stop over” at 200G before 400G is ready for commercial deployment, Katharine said in answer to a question from this author.

Recent Advances in Machine Learning and their Application to Networking, David Meyer of Brocade:

This excellent keynote speech by David Meyer, CTO & Chief Scientist at Brocade, was very refreshing. It demonstrated that real research is being done by a Silicon Valley company other than Google!

Machine learning currently spans a wide variety of applications, including perceptual tasks such as image search, object and scene recognition and captioning, voice and natural language (speech) recognition and generation, self-driving cars and automated assistants such as Siri, as well as various engineering, financial, medical and scientific applications. However, almost none of this applied research has spilled over into the networking space. David believes there’s a huge opportunity there, especially in predicting incipient network node/link failures. He also talked about Machine Learning (ML) tools for DevOps/ network operations (see below).

- OpenConfig (started by Google) aims to specify a vendor neutral/independent configuration management system. That management system has a big ML component from a telemetry configuration model.

- OPNFV consortium is specifying Operating System components to realize a Network Function Virtualization (NFV) system. There’s a Predictor module that includes an intelligence training system.

- One can envision a network as a huge collection of sensors that form a multi-dimensional vector space. The data collected is ideal for analysis/learning via deep neural networks.

- There are predictive and reactive roles for ML in network management and control.

- “We are at the beginning of a network intelligence revolution,” David said.

- ML tools for DevOps: domain knowledge is needed from an analytics platform, which should include a recommendation system.

- Application profiling was cited as an example to build tools for a DevOps environment: 1] Predict congestion for a given application. 2] Correlate with queue length to avoid dropped packets. 3] Anomaly detection of a pattern that doesn’t conform to expected behavior (if that behavior can be defined?)

Future of ML – What’s Next:

- Deep neural nets that learn computation functions.

- More emphasis on control- analyze sophisticated time series.

- Long range dependencies via reinforcement learning.

- Will apply to compute, storage, network, sensors, and energy management.

- Huge application in networking will be predictive failure analysis (and re-route BEFORE the failure actually occurs).

3. Software Defined WANs- a tutorial by Inder Monga of ESnet & Srini Seetharaman of Infinera

This was a terrific “tag team” lecture/discussion by Inder & Srini who alternated describing each slide/diagram. We present selected highlights below.

Inder summarized many fundamental problems in all facets of WANs:

- Agility requirements are not met for WAN provisioning (sometimes takes days or weeks to provision a new circuit or IP-MPLS VPN)

- Traditional wide-area networking is inflexible, opaque and expensive

- WAN resources are not efficiently utilized (over-provisioning prevails)

- Interoperability issues across vendors, layers and domains reduces chance of automation

- Hard to support new value propositions, like: Route selection at enterprises, Dynamic peering at exchanges, Auto bandwidth and bandwidth calendaring, Mapping elephant (very large) data flows to different Flexi-Grid channels

Srini commented that the Network Virtualization (NV)/ overlay model has more market traction than the pure SDN/Open Flow model.

Overlay networks run as independent virtual networks on top of a (real) physical network infrastructure. These virtual network overlays allow cloud service and DC providers to provision and orchestrate networks alongside other virtual resources (like compute servers). They also offer a new path to converged networks and programability. However, network overlays shouldn’t be confused with “pure SDN” which doesn’t permit overlays or network virtualization. [We’ve previously described both of these “SDN” approaches in multiple articles at viodi.comand techblog.comsoc.org]

Several vendors provide NV software on compute servers running in DCs (e.g. VMWare, Nuage Networks, Juniper, etc). They support VxLAN for tunneling L2 frames withing a DC network (in lieu of VLANs) and then map VxLAN frames to IP-MPLS packets for inter DC transport. However, none of those NV software vendor’s inter-operate with other vendors on an end to end basis. That confirms again that at least the NV version of SDN is not really “open,” as the same vendor’s NV software must be used on the compute servers.

Gartner Group finds that SDN in general (including all the myriad versions, twists and tweaks), is approaching the bottom of the “trough of disillusionment” after falling hard from the peak of inflated expectations that was built up due to all the hype and BS. This is illustrated in the graph below:

Image courtesy of Gartner

It’s interesting to note that SD- WANs, which have a much broader connotation than SDN for WANs, continue to ramp up the innovation trigger curve. They’ve yet to reach their peak of excitement and/or hype. White box switches, which we think is the future of true open networking, is on the downward path towards disillusionment, according to Gartner.

We totally disagree as we see years of tremendous potential ahead for open networking software running on bare metal switches (made by ODMs in China and Taiwan).

In closing, we note that National Research & Education Networks (NRENs) have deployed an East-West interface for multi-domain SDN – something we’ve screamed was missing from ONF specified SDN specs for a long time! Please refer to Dan Pitt’s remarks on that topic during my interview with him at the 2015 Open Networking Summit.

The NREN East-West/multi-domain interface is evidently based on a Network Services Interface (NSI) spec from the Open Grid Forum.

The OGF- NSI document Introduction states:

“NSI is designed to support the creation of circuits (called Connections in NSI) that transit several networks managed by different providers. Traditional models of circuit services and control planes adopt a single very tightly defined data plane technology, and then hard code these service attributes into the control plane protocols. Multi-domain services need to be employed over heterogeneous data plane technologies.”

Kuddos to Inder and Srini for looking through all the marketing hype, identifying WAN problems and some potential solutions that might be solved by new software. The one that I’m most enthusiastic about is theOpenConfig project (described above in the Machine Learning section) for vendor neutral configuration. It’s purpose and functions are described in this tutorial article.

References:

http://viodi.com/2015/09/03/2015-hot-interconnects-summary-part-i-oracle…

http://viodi.com/2015/09/02/2015-hot-interconnects-summary-part-ii-huawe…

Surge in Carrier SDN Spending Forecast by IHS-Infonetics Lead Analyst

MARKET FOR CARRIER SDN FORECAST TO GROW EXPONENTIALLY:

As service providers seek service agility and operational efficiency in their networks to stay competitive, the global market for carrier software-defined networking (SDN) software, hardware and services is expected to grow from $103 million in 2014 to $5.7 billion in 2019, according to IHS.

“We’re still early in the long-term, 10- to 15-year transformation of service provider networks to SDN. Momentum is strong, but we won’t see widespread commercial deployments where bigger parts of — let alone whole — networks are controlled by SDN until 2016 through 2020,” said Michael Howard, senior research director for carrier networks at IHS.

ADDITIONAL CARRIER SDN MARKET HIGHLIGHTS:

- SDN software — including network apps, such as traffic analytics, and orchestration and controller software — is the critical piece that will convert a network into a software-defined network

- IHS predicts service providers around the world will increase their spending on SDN software by 15 times from 2015 to 2019

- Due to the newness of SDN technology and the fundamental changes it brings to networks, there is an incredible demand for expertise to design, deploy and operate SDN-based services, and carriers are looking to vendors for this expertise

- IHS expects outsourced services for SDN projects to grow at a 2014–2019 CAGR of 199%

SDN SURVEY SYNOPSIS:

The 2015 IHS Infonetics Carrier SDN Hardware, Software, and Services market size and forecast report, led by analyst Michael Howard, examines the markets and trends related to building service provider software-defined networks. Specifically, the report tracks software that provides orchestration, controller and application functions; outsourced services for SDN projects; and hardware in use for SDN networks, including routers, switches, WDM and video content delivery network (CDN) equipment, and other telecom equipment controlled by SDN orchestration and controllers, such as CPE.

To purchase the report, please visit www.infonetics.com/contact.asp

Editor’s Note: SDN is not necessarly an open network!

Contrary to popular belief, SDN does not always imply an “open network.” That’s because most of the SDN implementations are, in fact, proprietary extensions of network equipment vendor boxes (e.g. Cisco, Juniper, Arista Networks, etc). There is no mutli-vender interoperability other than when using accepted tunneling protocols like VxLAN for the network virtualization/overlay model. Is that SDN? Purists and the ONF say NO! Vendors that implement it (many) say YES!

The latest poll from the Open Network User Group (ONUG) found that 71% of respondents characterized their network(s) as “A Little Open or Not at All.” See reerence below or click here for ONUG’s Market Perspective of Open Cloud Infrastructure.

Recent SDN References:

https://techblog.comsoc.org/2015/07/26/my-perspective-on-ons-2015-sdn-open-networking

https://techblog.comsoc.org/2015/06/24/highlights-of-2015-open-network-summit-ons-key-take-aways

IHS-Infonetics: Optical Network Equipment Spending Trends + Huge Growth for 100G Optical Ports

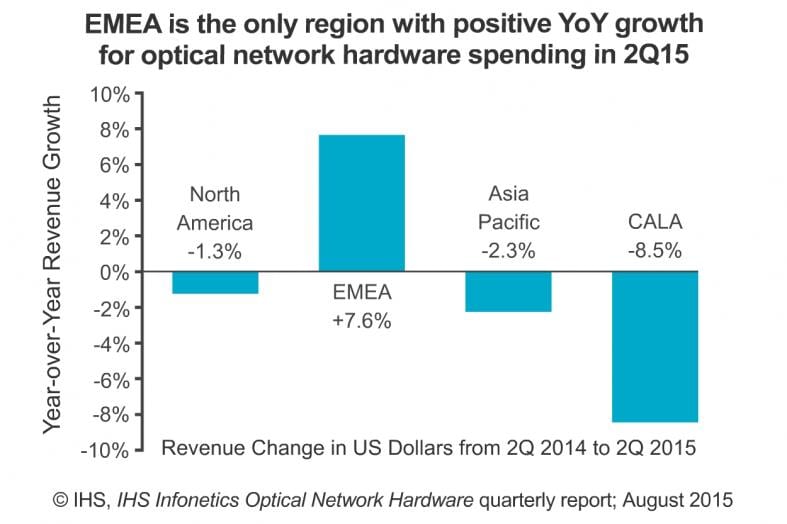

IHS-Infonetics just released vendor market share and preliminary analysis from its 2nd quarter 2015 (2Q15) IHS Infonetics Optical Network Hardware report (Full report published by August 24th). According to the report, global optical network hardware revenue (WDM and SONET/SDH) grew 22% sequentially in 2Q15, but was flat on a year-over-year basis. Europe is the only major world region that posted positive year-over-year growth in 2Q15, up 8%.

OPTICAL MARKET HIGHLIGHTS:

- On a rolling 4-quarter basis, WDM equipment spending further extended 3 years of consecutive growth

- Spending on WDM equipment grew 23 % in 2Q15 from 1Q15, and was up 6 % from 2Q14

- WDM gear comprised 86 % of total worldwide optical hardware revenue in Q2

- Spending on optical network hardware in Asia Pacific surged 36% in 2Q15 from the previous quarter, but is down 2% from one year ago

- Alcatel-Lucent announced an intention to merge with Nokia, an action IHS does not expect to have any transformative effects on ALU’s optical business or the competitive landscape

Analyst Quote:

“With three consecutive quarters of good results under its belt, Europe is signaling a reversal of the terrible optical spending that we’ve seen in the region over the last five years,” said Andrew Schmitt, research director for carrier transport networking at IHS. “This strength is concentrated in Alcatel-Lucent, Ciena and Infinera.”

“When taking into account currency effects, the results are even stronger – adjusted for exchange rate, optical spending in Europe saw a 30 % year-over-year growth rate in the second quarter when measured in euros,” Schmitt said.

OPTICAL REPORT SYNOPSIS:

The quarterly IHS Infonetics Optical Network Hardware market size, share and forecast report, led by analystAndrew Schmitt, examines the vendors, markets and trends related to metro and long haul WDM and SONET/SDH equipment used to build optical networks. The report also tracks Ethernet optical, SONET/SDH/POS and WDM ports. Vendors tracked include Adtran, Adva, Alcatel-Lucent, Ciena, Cisco, Coriant, Cyan, ECI, Fujitsu, Huawei, Infinera, NEC, Padtec, Transmode, TE Connectivity, Tyco Telecom, ZTE, others.

To purchase the report, please visit www.infonetics.com/contact.asp

RELATED RESEARCH

- Huge Growth for 100 Gigabit Optical Ports as Operators Increase Network Capacity

- Ciena, Cisco and Infinera Lead 2015 Optical Network Hardware Scorecard

- Packet-Optical Transport Deployments Slower Than Anticipated

- Europe Exiting Optical Spending Slump, Data Centers Bullish on 100G

- In Data Center Optics Market, 40G Transceivers Ubiquitous, 100G Accelerating

- In Telecom Optics Market, 100G Transceiver Growth Suppressed Until 2016

- OTN Switch Spending Up 40 Percent from a Year Ago

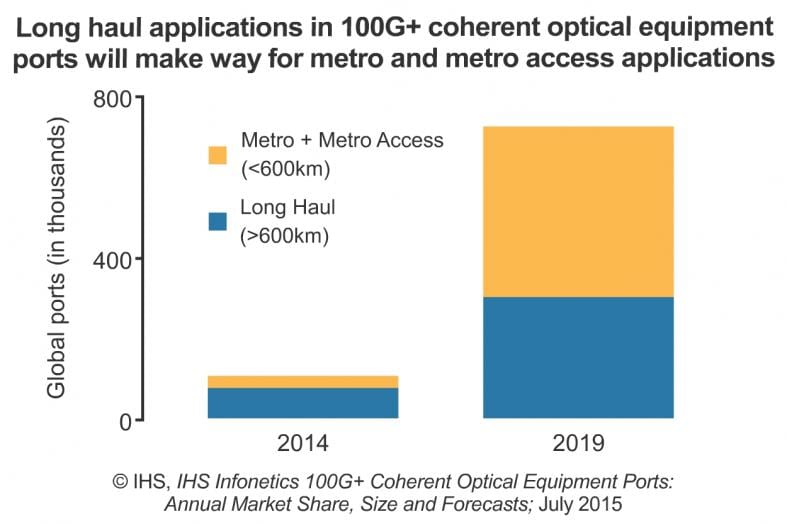

Separately, IHS-Infonetics reports that Coherent 100G port shipments for metro regional optical networks grew 145 % in 2014 from the prior year, and are anticipated to grow another 118 % in 2015.

“Adoption of 100G coherent technology has surged, first in long haul networks and now becoming a material part of metro networks. The expansion of 100G into new markets was the catalyst for our 100G+ coherent optical ports report, which provides an accurate, in-depth picture of how 100G technology is being used today and how it’ll be used in the future as the landscape grows increasingly complex,” said Andrew Schmitt, research director for carrier transport networking at IHS.

“100G is poised to explode in 2016 as new equipment built specifically for the metro reaches the market, allowing 100G technology to economically reach new portions of the network such as metro edge and metro regional,”Schmitt said.

100G+ COHERENT OPTICAL PORT MARKET HIGHLIGHTS:

- 2014 was a banner year for 100G port shipments, led by massive purchases in China from China Mobile

- Most of 100G coherent technology deployed in 2014 was for long haul applications, but metro regional (<600km) and metro access (<80km) applications will start ramping in 2016

- 100G market share is concentrated in a small circle of players: Alcatel-Lucent, Ciena, Huawei, Infineraand ZTE; the only potential catalyst for shifts will come from deployment in shorter reach metro and datacenter applications—the next growth vector for 100G

- Sometime in 2017–2018, 100G coherent will make another quantum jump, displacing 10G in the 80km or less metro-access market

100G OPTICAL REPORT SYNOPSIS:

The 20-page IHS Infonetics 100G+ Coherent Optical Equipment Ports market size, vendor market share and forecast report provides detailed granularity for 100G+ coherent and non-coherent port shipments on optical transport equipment, tracking the evolution of 100G as operators increase the flexibility and capacity of their networks. The report tracks 100G by application, including metro regional, metro access and long haul, as well as specific technology derivatives such as flex-coherent and direct-detect 100G.

To purchase the report, please visitwww.infonetics.com/contact.asp

Competing market research firm Dell’Oro Group says the optical transport network equipment market will grow at a 10% compounded annual growth rate (CAGR). Demand for metro WDM capacity will drive up the overall optical transport revenues to $15 billion by 2019 according to this Dell’Oro report.

Exposed url:

During this four-year period, service providers will continue to deploy a mix of 100G and 200G wavelengths in their networks. The research firm forecast that over 75 percent of WDM capacity will be from 100G wavelengths, while 200G will contribute nearly 25 percent of WDM metro equipment revenue by 2019.

Jimmy Yu, VP of optical transport market research at Dell’Oro Group, said in a release that the majority of metro equipment sales will come from traditional service providers, but content providers and financial trading companies will contribute to overall growth as they install their own 100G networks.

“The majority of metro equipment purchases will still be made by telecom service providers, expanding their metro network capacity for higher speed services, but we also see a strong trend towards enterprises such as Internet content providers and financial institutions procuring and installing their own high speed 100 Gbps links. This trend is being powered by the increasing importance of data centers to a company’s core business,” Yu said.

“The network still needs a lot of raw bandwidth and WDM is the best equipment to deliver that. While high demand for long haul equipment will continue, the biggest growth that we are projecting is in metro applications. The majority of metro equipment purchases will still be made by telecom service providers, expanding their metro network capacity for higher speed services, but we also see a strong trend towards enterprises such as Internet content providers and financial institutions procuring and installing their own high speed 100 Gbps links. This trend is being powered by the increasing importance of data centers to a company’s core business,” added Mr. Yu.

Verizon conducts field trial of 10 Gb/sec Nex Gen PON2 service; ITU-T rec’s for NG PON2

Verizon has completed a field trial of NG-PON2 fiber-to-the-premises technology that could provide the infrastructure for download speeds up to 10 Gbps for residential and business customers. The huge telco’s current top download speed for its residential FiOS service is 500 Mbps. The new technology could “open the door” to speeds as high as 80 Gbps, according to Verizon.

The field trial took place on a network link between the company’s central office in Framingham, MA and a home three miles away served by Verizon FiOS. The test required installation of a new optical line terminal (OLT) at the central office supporting four wavelengths, each capable of delivering speeds up to 10 Gbits/s downstream and 2.5 Gbits/s upstream. Verizon also said it was able to demonstrate the simultaneous use of standard GPON and NG-PON2 on a single fiber, and a successful fail-over scenario where its new ONT autonomously restored 10G service by tuning to a new wavelength after a simulated fault was introduced.

Vendor partners in the trial included Cisco Systems Inc. and PT Inovação (part of the Portugal Telecom Group) which provided the NG-PON2 equipment system.

For Verizon’s upcoming NG-PON2 RFP, there are vendors like Alcatel-Lucent, Adtran Inc. Calix Networks Inc, Huawei Technologies Co. Ltd. and of course Cisco.

“The advantage of our FiOS network,” said Lee Hicks, vice president of network technology at Verizon, “is that it can be upgraded easily by adding electronics onto the fiber network that is already in place. Deploying this exciting new technology sets a new standard for the broadband industry and further validates our strategic choice of fiber-to-the-premises.”

ITU-T recommendations for NG PON2 specify up to 40G b/sec speed:

Recommendation ITU-T G.989.1 series describes 40 Gigabit-capable passive optical network (NG-PON2) systems to an optical access network for residential, business, mobile backhaul, and other applications.

Recommendation ITU-T G.ngpon2.1 addresses the general requirements of 40 Gigabit-capable passive optical network (NG-PON2) systems, in order to guide and motivate the physical layer and the transmission convergence layer specifications. This Recommendation includes principal deployment configurations, migration scenarios from legacy PON systems, and system requirements that are requested by network operators. This Recommendation also includes the service and operational requirements to provide a robust and flexible optical access network supporting all access applications.

The physical layer specifications for the NG-PON2 physical media dependent (PMD) layer is described in Recommendation ITU-T G.989.2 (ex G.ngpon2.2, draft). The transmission convergence (TC) layer is described in ITU-T Rec. G.987.3, with unique modifications for NG-PON2 captured in Recommendation ITU-T G.989.3 (ex G.ngpon2.3, draft). The ONU management and control interface (OMCI) specifications are described in ITU-T Rec. G.988 for NG-PON2 extensions.

http://www.itu.int/rec/T-REC-G.989.1-201303-I

References:

http://www.multichannel.com/news/technology/verizon-tests-10-gig/392933

http://www.lightreading.com/gigabit/fttx/verizon-revs-up-wireline-race-with-ng-pon2/d/d-id/717555

http://www.telecompaper.com/news/verizon-tests-ng-pon2-to-seek-proposals-later-this-year–1096954

https://www.ntt-review.jp/archive/ntttechnical.php?contents=ntr201503gls.html

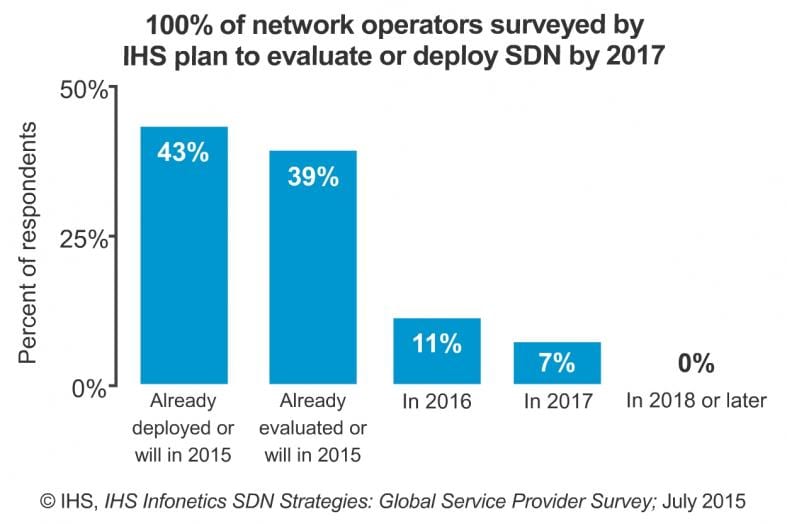

IHS-Infonetics Survey: Network Operators Reveal SDN Plans,Timing & Challenges/Alan's Take

IHS-Infonetcs latest report: “SDN Strategies: Global Service Provider Survey” of worldwide carriers says that global network operators are moving toward software-defined networking (SDN). The carriers surveyed represent 49% of the world’s telecom capex and 46% of global telecom revenue.

–>The study found that 82 % of service provider respondents have either already deployed SDN, are now deploying SDN, or plan to evaluate it in 2015.

SDN STRATEGIES SURVEY HIGHLIGHTS:

- The #1 reason service providers are investing in SDN is to simplify and automate service provisioning, which they believe will lead to service agility and quick time to revenue.

- Various barriers are becoming more prominent as operators get closer to commercial deployment; respondents to this year’s survey cited integrating SDN into existing networks and immature technologies and products as the top 2 barriers.

- Operators want SDN in most parts of their networks, with the top domains for deployment consisting of cloud services offered to customers, within and between data centers, and access for businesses.

Lead Analyst Quotes:

“The successful field trials and a few commercial deployments of SDN in the last year keep moving toward more commercial deployments in 2015, still mostly on a limited basis as operators put one or two use cases to the test under real-world conditions in their live networks,” said Michael Howard, senior research director for carrier networks at IHS & co-founder of Infonetics.

“Carriers are starting small with their SDN deployments and focusing on only parts of their network to ensure they can get the technology to work as intended. We see in the results of our SDN survey that though momentum is strong, it will be many years before we see bigger parts or a whole network that is controlled by SDN,” Howard said.

SDN SURVEY SYNOPSIS:

- The 25-page 2015 IHS Infonetics SDN Strategies: Global Service Provider Survey is based on interviews with purchase-decision makers at 28 incumbent, competitive and mobile service providers from EMEA, Asia Pacific and North America that have evaluated or deployed SDNs in their networks or plan to do so. IHS asked operators about their strategies and timing for SDN, including deployment drivers and barriers, target domains, use cases and more.

To purchase the report, please visit www.infonetics.com/contact.asp

Author’s Rebuttal:

We firmly believe that the overwhelming majority of network operators, with the exception of NTT, will not be deploying classical/pure SDN-OpenFlow as standardized by the Open Network Foundation (ONF). Many are evaluating network virtualization (an overlay model where a logical network is mapped onto a physical network) as per the VMware schema.

However, the vast majority of carriers (and cloud service providers like Amazon, Google, and Microsoft) have invented their own version of SDN and instructed their equipment suppliers to implement that. In some cases, they use a specific vendor product with some user programmablity, e.g. Cisco Metro Ethernet switches used for AT&Ts Network on Demand service (a switched Ethernet WAN service).

The bottom line is that such carrier or network equipment vendor specific solutions are generally not inter-operable with any other SDN carrier or cloud service provider offering. Hence volumes will be limited and network equipment vendors will need different software for different carriers. As a result, we will likely see pockets of SDN in carrier WANs, but no mass deployment of ONF standardized SDN-OpenFlow anytime soon!

RELATED RESEARCH:

NFV Market to Grow More than 5-Fold through 2019:

https://www.infonetics.com/pr/2015/NFV-Market-Highlights.asp

Virtualizing Network Security with NFV and SDN – Whitepaper and Webinar:

https://www.infonetics.com/pr/2015/IHS-SDN-NFV-Security-Webinar-and-Whitepaper.asp

35 Percent of Operators Surveyed Will Deploy NFV This Year:

https://www.infonetics.com/pr/2015/NFV-Strategies-Survey-Highlights.asp

Virtual Routers on Track to Grow 125 Percent in the Next Year:

http://www.infonetics.com/pr/2015/1Q15-Carrier-Router-Switch-Market.asp

Data Center and Enterprise SDN Market to Grow More than 15-fold by 2019:

https://www.infonetics.com/pr/2015/2H14-Data-Center-SDN-Market-Highlights.asp

Network Operators Rate Router and Switch Vendors; Cisco #1 for 3rd Straight Year:

http://www.infonetics.com/pr/2015/Router-Switch-Leadership-Survey.asp

Mixed-Bag Carrier Ethernet Equipment Market Set to Top $29 Billion in 2019:

http://www.infonetics.com/pr/2015/Carrier-Ethernet-Market-Highlights.asp

RECENT AND UPCOMING RESEARCH:

Download the IHS Infonetics 2015 service brochure or log in: www.infonetics.com/login.

– Analyst Note: ONUG Spring 2015: Preparing for Open Networking (June)

– NFV Hardware, Software, and Services Forecast (July)

– Carrier SDN Hardware, Software, and Services Forecast (Aug.)

– Routing, NFV, and Packet-Optical Strategies: Service Provider Survey (Aug.)

– Data Center SDN Strategies: Global Service Provider Survey (Aug.)

– NFV Vendor Leadership Analysis (2015)

SDN AND NFV WEBINARS (https://www.infonetics.com/infonetics-events)

– SDN & NFV: Lessons Learned (Sept. 24: Learn more)

– SDN & NFV: Accelerating PoCs to Live Commercial Deployment (Watch now)

– White Box Switching: Is It Time to Jump In? (Watch now)

– Service Provider Experiences with NFV: The Good, the Bad & the Ugly (Watch now)

– Evolving Network Architectures: Cloud, SDN, NFV & Packet-Optical (Watch now)

– Router Bypass: Using NFV to Deliver Enterprise Services (Sponsor)

TO PURCHASE RESEARCH, CONTACT:

IHS Sales: +1 844-301-7334

https://www.ihs.com/about/contact-us.html

New Mobile Virtual Network Operator Service Agreement & Other Wireless Telco News

Wireless communications service providers are licensing their network infrastructure to mobile virtual network operators. Telco Cuba, Inc. (OTC: QBAN), a U.S. based mobile telecom and data connectivity service provider, announced today that it has immediately begun offering mobile voice and data services to consumers and corporations as a result of a Mobile Virtual Network Operator (MVNO) agreement with Next Mobility.

TelcoCuba now provides high-quality voice and data services to consumers and enterprises utilizing LTE, 4G, and 3G networks. Telco Cuba mobile services will be available in other countries via roaming agreements and services with other mobile service providers. Telco Cuba and its wholly owned subsidiary Amgentech, Inc. are already well established in the local market for Voice over IP (VOIP) services and communications technology. Amgentech, Inc. has provided services to multiple network operators, constructed its own highly reliable network to enable communications worldwide, and has built highly reliant networks for its client base. Going forward, it will now offer extra-flexible solutions that combine mobile voice and data communication services with existing services for blended communication solutions that include mobile voice and data, mobile VoIP, VoIP, International Dialing, top-off prepaid phone service, international roaming, and much more.

The MVNO agreement signed with Next Mobility is a major first milestone for Telco Cuba. It affords Telco Cuba the ability to enter the cell phone service provider market with a drastically reduced startup cost, allowing Telco Cuba to use its budget where it matters – customer acquisition and marketing. Speed to market is the single most important factor in the digital age. Next Mobility is a well-established entity in the space and our contracted services will afford Telco Cuba a time to market of just under 60 days.

—>Apple is reportedly in talks with telecom companies in the U.S. and Europe to let customers pay the Cupertino-based tech giant for wireless service directly, rather than going through wireless firms like AT&T or Verizon. The company is conducting private trials of the service in the U.S. and has engaged in discussions with European companies to offer a similar service there, Business Insider reports. Also see related RCR Wireless article.

MVNO – Mobile Virtual Network Operator is a term coined to describe a company that setups a platform for the resell of mobile phone services from one of the big three cell phone providers in the United States of America or elsewhere in the world. AT&T, T-Mobile & Sprint are the biggest of the Mobile Virtual Network Enablers.

In other wireless and telecommunications news and developments:

- Verizon recently announced Grid Wide Utility Solutions, a new Internet of Things (IoT) platform service offering utility companies an easy on-ramp to grid modernization. Now available in the U.S., Grid Wide offers electric utility companies an integrated solution for smart metering, demand response, meter data management and distribution monitoring and control. With 147 million electric meters in the U.S. today, Verizon’s Grid Wide aims to transform the delivery and consumption of energy nationwide for investor-owned, cooperative and municipal utilities and their customers. Designed to maximize the benefits of smart meters, the solution comes equipped with a wide range of cloud-based applications intended to help utility companies drive incremental revenue, reduce operating costs, increase efficiency and improve customer experience.

- AT&T is promoting a $200 monthly cellphone and TV Everywhere bundle that it plans to offer throughout the U.S. — marking the first fruits of its merger with DIRECTV. Starting Aug. 10, the carrier will provide four phone lines with unlimited voice and texting, along with 10 gigabytes of sharable data. On the video side, AT&T will hook up four TVs with HD and DVR features and the ability to watch on any mobile device. The New York Times (free-article access for SmartBrief readers) (8/3), CNET (8/2)

- Vonage Holdings Corp, a leading provider of cloud communications services for consumers and businesses, today announced results for the second quarter ended June 30, 2015. Second Quarter Consolidated Financial Results – “We continue to drive market-leading growth at Vonage Business, while increasing profitability in Consumer Services,” said Alan Masarek, Chief Executive Officer of Vonage. “At Vonage Business, we delivered 118% revenue growth fueled by the successful execution of our acquisition strategy coupled with strong organic growth. We also made significant investments in our sales infrastructure, brand and leadership team to enhance our position in the rapidly growing Unified Communications-as-a-Service (UCaaS) market.”

- T-Mobile US Inc last week reported second quarter 2015 results reflecting continued strong momentum, industry-leading growth, and continued low churn. The Company again outperformed the competition in both customer and financial growth metrics. T-Mobile generated 2.1 million total net customer additions, marking the ninth consecutive quarter that T-Mobile has delivered over one million total net customer additions. Additionally, the Company delivered 14% total revenue growth and 25% growth in adjusted EBITDA compared to the second quarter of 2014.

“While the carriers continue to use gimmicks to confuse consumers, T-Mobile continues to listen to customers and respond with moves that blow them away,” said John Legere, President and CEO of T-Mobile. “On top of adding 2.1 million new customers in the second quarter, we delivered 14% year-over-year revenue growth and 25% year-over-year Adjusted EBITDA growth. Overall, I think our results speak for themselves.”

- U.S. Cellular to launch LTE roaming in next 60-90 days: CEO Ken Meyers said U.S. Cellular has completed its first LTE roaming agreement, though he declined to reveal the carrier partner. He said the companies are in the implementation phase of the deal and the respective engineering teams of the companies are working together. U.S. Cellular customers will be able to start benefiting from expanded LTE roaming in the next 60 to 90s days, he said. The partner is likely a Tier 1 carrier, so U.S. Cellular customers will get access to a more robust and nationwide LTE network. Meyers said he expects U.S. Cellular customers to see benefits more than he expects U.S. Cellular to reap inbound roaming revenue. Meyers said that the agreement is the first of multiple LTE roaming deals the company is working on.

IHS-Infonetics: MSOs Plan Massive DOCSIS Deployments; Shift to Remote/Distributed Access & HFC Optical Nodes

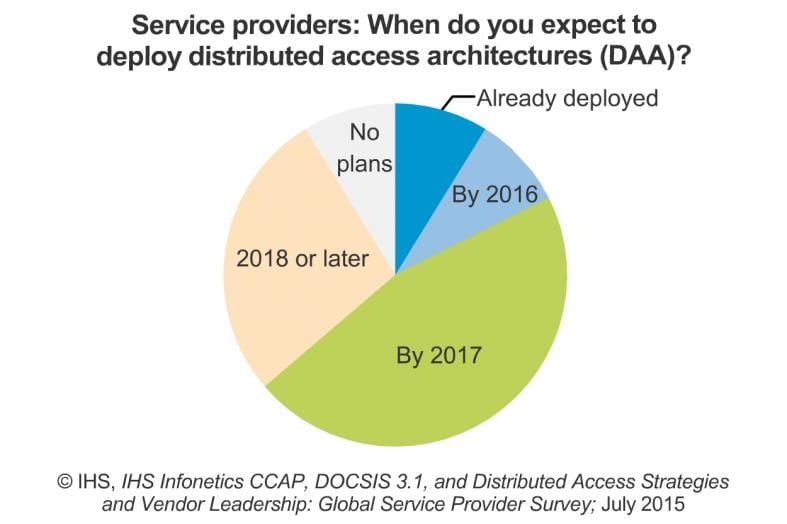

1. IHS-Infonetics conducted in-depth interviews with cable operators (MSOs) across the globe that collectively control 87 percent of the world’s cable capex and found that 42 percent of them plan to deploy a distributed access architecture (DAA) by 2017.

In the study, CCAP, DOCSIS 3.1, and Distributed Access Strategies and Vendor Leadership: Global Cable Operator Survey, respondent operators say their primary choices for distributed access are R-PHY, R-MACPHY and R-CCAP.

CABLE SURVEY HIGHLIGHTS:

- The operational benefits cable operators are reaping from moving from CMTS (cable modem termination system) to CCAP (converged cable access platform) are just the first step in a long-term transition to distributing data processing capabilities throughout the network

- Survey respondents, on average, say that about 1/3 of their residential subscribers will be passed by DOCSIS 3.1 (CableLabs spec) enabled headends by April 2017

- By 2017, nearly half of respondents will have return path (upstream) frequencies of 86–100MHz, while a quarter will have 101–200MHz of return path spectrum

“Cable operators are clearly committed to both DOCSIS 3.1 and distributed access architectures to increase bandwidth in their access networks. Though there is no consensus yet on which distributed access technology most will use, there’s no question they will distribute some portion of the DOCSIS layer to their optical nodes,” said Jeff Heynen, research director for broadband access and pay TV at IHS.

Definitions:

● Remote PHY (R-PHY): in this scenario, the entire DOCSIS PHY modulation is moved into the node while the MAC layer remains in the headend.

● R-CMTS: in this scenario, the DOCSIS MAC and PHY are removed from the headend and placed in the node

● R-CCAP: in this scenario, the DOCSIS MAC and PHY and video QAM capabilities are removed from the headend and placed in the node.

ABOUT THE REPORT:

The 29-page IHS Infonetics study, led by IHS analyst Jeff Heynen, focuses on DOCSIS 3.1, converged cable access platforms (CCAPs) and distributed access architectures, and how and when cable operators will deploy these technologies and architectures to improve their broadband and IP service offerings over the next 2 years.

The study includes operator ratings of CCAP and distributed access equipment suppliers (Arris, Casa Systems, Cisco, Gainspeed, Harmonic, Huawei and Pace/Aurora) on 9 criteria. Note from Jeff Heynen: “These are really the primary suppliers of node-based products. There are a number of Chinese ODMs. But they are really only present in China proper.”

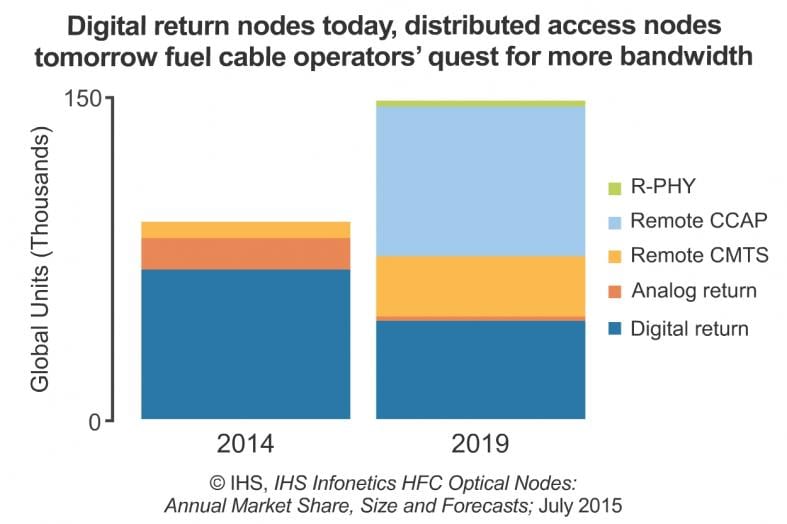

2. In a related report, IHS-Infonetics forecasts global hybrid fiber-coaxial (HFC) optical node shipments to more than double in the 5 years from 2014 to 2019, jumping from 92,000 to 200,000. Driving the boost are cable operators upgrading their networks with optical fiber cable, taking advantage of its high-bandwidth, low-noise, low-interference characteristics to deliver broadband video, data and voice services to homes and businesses.

“Optical nodes have rapidly become important platforms for cable operators to grow their broadband capabilities. By way of increased node splitting today for increased bandwidth and a transition to distributed access in the coming years, optical nodes will see significant unit growth and innovation,” said Jeff Heynen, research director for broadband access and pay TV at IHS.

OPTICAL NODE MARKET HIGHLIGHTS:

- Globally, HFC optical node revenue reached $356 million in 2014, up 14 percent from 2013

- In 2014, 80 percent of worldwide optical node revenue came from digital return nodes, and 15 percent from analog return nodes

- By 2019, IHS expects 35 percent of new physical nodes to be remote CCAP devices, 27 percent to be R-PHY units, and 23 percent to be traditional digital return nodes

- Arris led optical node global revenue and physical node unit shipments for the full-year 2014

ABOUT THE HFC OPTICAL NODE REPORT:

The 23-page IHS Infonetics HFC Optical Nodes market share and forecast report provides worldwide and regional market size, vendor market share, forecasts through 2019 and in-depth analysis for hybrid fiber-coaxial optical nodes. The annual market research service tracks physical node units, logical node segments and revenue for optical node types including analog and digital return, and remote PHY, converged cable access platform (CCAP) and cable modem termination system (CMTS).

RELATED RESEARCH:

- Biggest Trend among Cable Operators: Massive DOCSIS Deployments and a Shift to Remote/Distributed Access

- Broadband CPE Market Up 3 Percent from a Year Ago in 1Q15

- Reliable WiFi for Multiscreen TV Is Powering Growth in WiFi Extender Market

- Cable Broadband Equipment Market Off to Mixed Start in 2015

- 14 Percent Increase for Broadband Equipment Market from a Year Ago

- Pay TV Providers Embrace OTT Video, ‘Skinny’ Bundles to Stave Off Cord-Cutting

To buy Infonetics reports, visit: http://www.infonetics.com/contact.asp

My perspective on ONS 2015, SDN & Open Networking

The 2015 Open Networking Summit (ONS) was hosted on June 14th to June 18th in Silicon Valley. It featured a rich set of speakers, open networking panels and a wide audience base comprised of network service providers, network hardware and software vendors, web giants and the academia. ONS 2015 was the first of the fifth annual summit that I participated in. To this onlooker it provided an insight into the future direction of networking. The conference was a showcase of the solutions and challenges in achieving the goal of Software Defined Networking (SDN): to make the network programmable.

As Chair of the IEEE Communications Society Santa Clara Valley (SCV) chapter, I’ve had the opportunity to host several technical sessions on Open Networking and also track the rapid pace of change towards SDN. I am thrilled and enthused by the changes that SDN can provide. It opens up significant opportunities for new and existing players. However, I am equally skeptical of when and how SDN will become a mainstream technology, available to any enterprise data center or any end network consumer.

The basic idea of Software Defined Networking is to make the network user programmable. Sounds simple? It depends on how one defines the network:

- Is it a home network, enterprise Local Area Network (LAN) network, ISP / telco / carrier network, a web giant network, Cloud Service Provider Network or a Wide Area Network (WAN)?

- Is it a private network (located inside an enterprise and accessible only to an internal audience) or a public network (located on a premise not owned by the enterprise)?

- Is it a physical network (network functionality achieved using dedicated hardware) or a virtual network (network functionality achieved by using software and white box hardware)?

Each network type has it’s own set of solution pieces offered by multiple vendors, which consist of hardware and software components that are provisioned and maintained by a Service Provider (data center, telco WAN, enterprise/campus, cloud computing/storage, etc). Each network also has its own set of operational requirements. There are a wide range of issues and concerns, including: security, availability, provisioning, power, cost and serviceability.

The Open Network Foundation (ONF), which is progressing Open Flow based SDN, has a herculean task of bringing all these pieces under a single umbrella. Achieving SDN in an an “open,” “vendor agnostic” and “inter-operable” way is a challenge the purist can compare to finding extra terrestrial life.

Google’s Fellow and Technical Lead for Networking Amin Vahdat was an impressive keynote speaker at ONS2015. For the first time in company’s history, Amin disclosed Google’s internal Data Center Network. It’s design is based on the principles of Software Defined Networking, leverages CLOS topology, uses merchant silicon and has a single central administrative domain. A few statistics that are indicative of this massive network are that it handles 3.5 billion search results per day and has 300 hours of video uploaded every minute! Let’s pause for a minute and extrapolate, at roughly 5MB bandwidth consumption per minute for a 480p video – it translates into about 50 Petabytes of network traffic to watch the video content uploaded over a period of year (18000 years of uninterrupted viewing content stored and generated every year).

Microsoft’s Mark Russinovich, the CTO of the company’s Azure public cloud was also a keynote speaker. He talked about how Microsoft has embraced SDN into the Azure wide area network. That network can host millions of compute instances, and has exabyte scale storage and a Petabit capacity (Pbps) network.

Note that both Microsoft and Google are competing with Amazon’s AWS (Amazon Web Services) – a cloud-compute service provider platform.

Given the scale out requirement to handle the data generated by the human race today, one thing is clear: SDN is not an option – it is the solution. That’s because large networks that have to rapidly increase the number of users and the aggregate data capacity (e.g. Amazon’s AWS, Microsoft Azure public cloud, Google’s customer facing and backbone network, NTT and AT&T WANs, etc) require a software based approach with centralized domain specific control to scale out. The traditional hop by hop routing with expensive, closed, proprietary routers won’t make the grade.

AT&T’s SVP John Donovan, was another keynote speaker. He highlighted the journey of transformation which AT&T is pursuing with Open Networking, SDN and Open Source software. AT&T is on a grandiose mission to replace the traditional telephony network, based on Time Division Multiplexing (TDM) to an all Ethernet network by 2020.

The ONS2015 was spread over a week and had several panels on various important topics of SDN Adoption, Use Cases, Experiences, Hot Startups & VC investments, SDN WAN, Network Functions Virtualization (NFV), SDN for Optical Networks, OpenStack. The ONS2015 also had an expo floor, comprised of sponsor solution and demo booths from various companies like NEC, ADVA, AT&T, Dell, Brocade, Huawei, Cisco, and Broadcom.

There is a rapid pace of technology advancement, tremendous amount of energy and resources are being invested in this “second life of networking”. One pundit called it “a new epoch.” While there is market fragmentation and chaos, I see that as a positive sign. The industry is moving forward, asking new questions, facing new challenges. Consolidation is far ahead. Let’s continue to build and play by the ONF vision to build, promote and adopt SDN through open standards and open source software development.

I will close by a quote from Kitty Pang (Network Architect, Alibaba). It is bold and provocative, yet real:

“We want to run faster and faster. It does not matter if it’s hardware or software, open or closed, we choose low cost and high efficiency.”

Bonus:

Watch an insightful interview, where Alan Weissberger talks to ONF’s Dan Pitt on ONF’s path towards Open SDN: http://bit.ly/1erGes1

Editor’s Note:

Saurabh Sureka is the Chair of IEEE ComSoc Santa Clara Valley (SCV), which is by far the leading ComSoc chapter in the world in terms of both membership and technical programs. He joined the leadership team in 2011 as Treasurer and diligently continued to volunteer each year since then as a ComSocSCV officer. Saurabh is a Sr Product Manager at Emulex (now Avago Technologies) in San Jose, CA.

Related articles:

Highlights of 2015 Open Network Summit (ONS) & Key Take-Aways

Pica8 Open Networking OS/Protocol Stacks on Bare Metal Switches