Verizon brings 100G to U.S. Metro & Regional Areas

Verizon Communications (VZ) is rolling out 100G technology on select high-traffic metropolitan and regional networks in the U.S. The telco is implementing Fujitsu’s FLASHWAVE 9500 platform and the Tellabs+ 7100 system in its metro networks. Verizon will target metro areas where “traffic demand is highest,” the company said. It did not identify which markets will see the deployments.

“Metro deployment of 100G technology is the natural progression of Verizon’s aggressive deployment of 100G technology in its long-haul network,” said Lee Hicks, vice president of Verizon Network Planning. “It’s time to gain the same efficiencies in the metro network that we have in the long-haul network. By taking the long view, we’re staying ahead of network needs and customer demands as well as preparing for next-generation services.”

Verizon says the benefits of 100G scalability are especially relevant for signal performance, which is improved by using a single 100G wavelength as opposed to aggregating 10-10G wavelengths. Also, less space and reduced power requirements are needed to support 100G technology, compared with traditional 10G technology, so fewer pieces of equipment are needed to carry the same amount of traffic.

Verizon claims it’s been a leader in 100G technology and we tend to agree. Beginning in November 2007, the company successfully completed the industry’s first field trial of 100G optical traffic on a live system. Verizon currently has 39,000 miles of 100G technology deployed on its global IP network.

+ In Dec 2013, Tellabs was acquired by Marlin Equity Partners for $891 Million in cash (compare that to Google paying $19B for WhatsApp). http://www.tellabs.com/news/2013/marlin-completes-acquisition.pdf

References:

http://newscenter.verizon.com/corporate/news-articles/2014/04-15-100g-te…

http://www.channelpartnersonline.com/news/2014/04/verizon-unleashes-100g…

Infonetics: VoIP and Unified Communications to grow to $88 billion market by 2018

Infonetics Research released excerpts from its 2014 VoIP and UC Services and Subscribers report, which tracks service providers and their voice over IP (VoIP) and unified communications (UC) services revenue and subscribers.

VOIP AND UC SERVICES MARKET HIGHLIGHTS:

. The global business and residential VoIP services market grew 8% in 2013 from 2012,

to $68 billion

. SIP trunking shot up 50% in 2013 from the prior year, driven predominantly by activity in North America; EMEA is expected to be a strong contributor in 2014

. Sales of hosted PBX and unified communication (UC) services rose 13% in 2013 over 2012, and seats grew 35% due to continued demand for enterprise cloud-based services

. Global residential VoIP subscribers totaled 212 million in 2013, up 8% year-over-year

. Managed services are benefitting from the continued adoption of IP PBXs: Roughly 10%-20% of new IP PBX lines sold are part of a managed service or outsourced contract

. Infonetics expects continued strong worldwide growth in VoIP services revenue through 2018, when it will reach $88 billion

RELATED REPORT EXCERPTS:

. Infonetics’ April Voice, Video, and UC research brief: http://bit.ly/1iDYtXO

. Videoconferencing and collaboration show strongest growth among UC apps

. Carrier VoIP and IMS market gains 30%; Huawei, ALU, Ericsson, NSN ride the VoLTE wave

. Enterprise SBC market grew 42% in 2013

. Mergers and buyouts stir enterprise telephony market; UC revenue climbs 31% in 2013

. Exploding mobile device traffic, acquisitions heat up Diameter signaling controller market

“Business VoIP services have moved well beyond early stages to mainstream, strengthened by the growing adoption of SIP trunking and cloud services worldwide. Hosted unified communications are seeing strong interest up market as mid-market and larger enterprises evaluate and move more applications to the cloud, and this is positively impacting the market,” notes Diane Myers, principal analyst for VoIP, UC, and IMS at Infonetics Research.

VoIP AND UC REPORT SYNOPSIS:

Infonetics’ annual VoIP and unified communications report provides worldwide and regional market share, market size, forecasts through 2018, analysis, and trends for residential and business VoIP and UC services and subscribers. The report also includes a Hosted PBX/UC Tracker highlighting deployments by service provider, region, and vendor platform. Residential VoIP providers in the report include AT&T, Cablevision, Charter, Comcast, Cox, Embratel, Iliad, J:Com, Kabel Deutschland, KDDI, KPN, KT, LG Uplus, Liberty Global, NTT, ONO, Orange, Rogers, SFR, Shaw Communications, SK Broadband, Sky, SoftBank, TalkTalk, Telecom Italia, Time Warner Cable, Verizon, Vonage, and others.

To buy the report, contact Infonetics: http://www.infonetics.com/contact.asp

Related Article:

VoIP, The PSTN Killer, Won’t Kill Local Loops

- Many carrier frequencies on a pair. Orthogonal Frequency Division Multiplexing (OFDM) put hundreds of virtual modems in parallel, each on its own carrier frequency, over one wire pair.

- More efficient coding. How a bit appears on the wire changed from simple on/off signals (T-1) to 4-level signals (ISDN), to adding a phase change (quadrature coding in modems). The number of bits per baud (how many bits each digital symbol conveys) went from 1 to 64 and may go higher.

- Improved signal-to-noise (SNR) ratio. Echo canceling, first applied to voice, does wonders for data too.

- Interference canceling. The latest is highly adaptive “vectoring” among all the pairs in a cable.

Related Webinar: IMS IN THE CLOUD WITH NFV:

Join analyst Diane Myers April 16 for Deploying IMS in the Cloud with NFV, a live event that investigates the benefits of using IMS to leverage the cloud to achieve network scalability, cost, and flexibility, as well as how network functions virtualization (NFV) enables innovation:

http://w.on24.com/r.htm?e=763407&s=1&k=6DD532531DA28F11FF4CCCE20A63DBDE

Packet Optical & Long Haul Transport Market Experiencing Modest Growth- Market Research Firm Findings

Key Optical Market Trends 2013-2018:

- Continued demand for capacity driving the need for DWDM equipment and specifically 100 Gbps wavelengths. Dell’Oro Group expects the DWDM market to grow at an average annual rate of eight percent through 2018 and for 100 Gbps wavelengths to contribute the largest share of DWDM capacity shipments, approaching 80 percent by 2018.

- Movement towards OTN and packet transport driving the demand for optical packet platforms with OTN switching features. Dell’Oro Group projects optical packet platform revenue to grow at a 15 percent compounded annual growth rate.

- Ratio of equipment sales in metro optical versus core optical applications to drift over the next five years, with the majority of spending in metro applications.

– See more at: http://www.delloro.com/news/optical-transport-equipment-market-to-reach-15-billion-by-2018#sthash.PAZxiMjT.dpuf

From the Del’Oro Group: Key Optical Market Trends 2013-2018:

- Continued demand for capacity driving the need for DWDM equipment and specifically 100 Gbps wavelengths. Dell’Oro Group expects the DWDM market to grow at an average annual rate of eight percent through 2018 and for 100 Gbps wavelengths to contribute the largest share of DWDM capacity shipments, approaching 80 percent by 2018.

- Movement towards OTN and packet transport driving the demand for optical packet platforms with OTN switching features. Dell’Oro Group projects optical packet platform revenue to grow at a 15 percent compounded annual growth rate.

- Ratio of equipment sales in metro optical versus core optical applications to drift over the next five years, with the majority of spending in metro applications.

http://www.delloro.com/news/optical-transport-equipment-market-to-reach-…

Martin Casado: How the Hypervisor Can Become a Horizontal Security Layer in the Data Center

Introduction:

“Security will never be the same again. It’s a losing battle,” said Martin Casado, PhD during his Cloud Innovation Summit keynote on March 27th. Currently, security spend is outpacing IT spend, and the only thing outpacing security spend is security losses. Clearly this isn’t an issue of investment, innovation, or priorities as huge industries are built around security. Mr. Casado believes there is a fundamental architectural issue: that we must trade off between context and isolation when implementing security controls. With today’s huge data centers, there is a very large potential “attack surface” for malware and other cyber threats.

Astonishingly, Martin said that approximately “40% of actual SDN adopters paying money for SDN network virtualization are doing it as a security use case.” The concept is to use network virtualization as a primitive, as building blocks to build micro-segments. if you put something within one of those virtual networks, or within one of those segments, the only thing that it can see are also in that same segment. For example, for every application running on a virtual network can have its own security services, ie. its own L4 through L7 services. And if it gets compromised, the attack gets localized to just the layer effected. As a result, this use case is driving a lot of the adoption of network virtualization, according to Mr. Casado.

Martin said, “This has become, I think, the driving use case (for the data center) going forward. And as things like SDN and network virtualization cross the chasm (and become a significant revenue generating business), I think it’s security that’s going to do it.”

A Horizontal Security Layer:

Security in the data center involves a basic trade-off between context and isolation. If security control, such as a firewall a monitoring/tracking agent, is implemented within the application, it’s got great context. It knows the users, the data, and the files. But there’s no isolation. As a result, the user doesn’t trust the application or the endpoint. “So putting a security control there is kind of like taking the on-off switch to an alarm system and putting it on the outside of a house. It doesn’t make any sense.”

“Maybe I’ll put the security control in the infrastructure. Let’s put ACLs or whatever on servers, switches and routers, which provides very good isolation between the two. If I’m able to break into a server, I haven’t broken into the router, necessarily. But while the attack surface is much smaller (with isolation between the separate boxes), there isn’t any context. The resident security control doesn’t know the users or applications. It doesn’t have access to local file systems.”

So there’s a fundamental trade-off between:

a] Great context (know everything about the operational environment) without any real security/isolation, OR….

b] Terrible context (know nothing about the operational environment), but have great security through isolation.

Can the industry build a “Goldilocks zone” that goes ubiquitously throughout the (virtualized) data center, which provides both context and isolation? The Goldilocks Zone would be a place where both visibility and security are possible — in a location that’s not too visible or not too inaccessible, but just right. A horizontal security layer that provides both context and isolation was proposed as that “Goldilocks layer” by Martin.

Casado said that since the majority of workloads are virtualized, (horizontal) security control could be placed in the hypervisor (a separate trust domain). That security entity could then peer into the application to pull out meaningful context (like users and applications and observe the state of the network). It could also protect that visibility and provide protection and enforcement. Therefore, the hypervisor seems to be an optimal place to implement security- where you have visibility, context and isolation.

“And so this is kind of a major area that I’m looking into, because again, given the state of the security industry and if things go the way we are, we’re going to be spending all our time and money on it, we do need something that will change the architecture (of the data center) and the way we view it. What we’re missing today is a horizontal layer that we can provide meaningful security.”

If this horizontal security layer is built out as a software platform (residing within a hypervisor), new security features can be included. Martin cited two examples:

- Next-generation firewalling with deep visibility in the end host.

- Network access control that understands objects and people or meaningful policies or vulnerability assessment.

–> Martin claims that data center security, whether it’s end host security, or network access control, vulnerability assessment, IDS, or IPS, etc. would all be enhanced by such a horizontal security layer. All of them need better isolation and all of them need more context.

“So if we can build out this horizontal layer in this “Goldilocks zone,” I think we can actually move security in very much the same way that we have moved networking over the past seven years. I mean, I dedicated my life to SDN, and I think that we have the same type of opportunity here.”

Author’s Note: When malware invades a (physical) server it immediately tries to block the operations of any anti-malware software. Since any process running on a virtualized server has no way to reach the hypervisor, a security layer that’s operating within the hypervisor can take action to mitigate the malware or security threat. However, there is currently no security layer in VMware’s or anyone else’s hypervisor.

Martin’s Summary:

The IT industry needs to develop a horizontal layer for security controls and to use micro-segmentation to limit the attack surface within within the data centers. That will protect the data center and the assets within it from malicious attacks.

“This is a once in a wave opportunity, as we’re redefining these new architectures, to actually build security in as a primitive, as a fundamental primitive. So we have a root of trust. So you have a horizontal security layer that you can build rich systems on top of.”

Martin in Conversation with Michael Howard:

In the interview with Infonetics’ Michael Howard, Martin called attention to the problem of detecting the imminent arrival of a large flow of data (an elephant) that would trample smaller data flows (the mice). “Nobody knows how to detect elephants, and we can’t do it from within the network,” he said.According to Casado, the hypervisor actually can see the future, in that it can detect the amount of data that is queued to be transmitted. The hypervisor can therefore sniff out elephant flows. You can go ahead and mark it, and then that will solve this long standing performance issue (between the elephant and the mice data flows) in networking.

In a subsequent email exchange, Martin wrote: “The hypervisor, with the aid of a guest presence, can look directly into the TCP send buffer to detect an “elephant” (large packet queued to be sent). This is likely to be a far more accurate approach than anything stochastic, such as flow tracking in the network.”

Q & A with this Author:

Alan: “Michael (Howard) asked you to explain the situation of SDN, NFV and telco service provider networks, and you mentioned what the problem is, but not the challenge telco’s face. The problem being that web hosting (provided by telco’s) is a low-margin business, the telco’s customers are building overlay networks to deliver cloud services and carriers want a part of that cloud business.What’s your opinion of whether or not they’ll succeed, and what really are the obstacles in building a carrier cloud?”

Martin Casado: “That’s a good question. NFV, I think at the most basic level, is just disaggregating the service from the box, and people have different ideas about what that service is. I see basically two camps. One camp is for big carrier, heavy gear that’s sold by the likes of Ericsson and Nokia Siemens, I want to decouple that software and that hardware.I think that’s going to be a very difficult journey.

I think the incentives aren’t aligned correctly. I’m not sure there’s a technical rationale for doing that. So when it comes to actually doing NFV for core carrier equipment, I don’t buy this is going to actually happen. I could be wrong, but just from an industry standpoint, I just don’t see the incentives aligned correctly.

Another way that you can view NFV is providing L4 through L7 services, things that are already virtualized and running in (Intel) x86 processors. So I’m going to offer security services, I’m going to offer load-balancing services. For that, I think that, A, this is already happening. I think the telcos are in a great position because they own the infrastructure to provide this. You hear about virtualization of VPN using top solutions. I think all of that will happen.

I’m actually suggesting something even a little bit more radical. So, again, the NFV where you’re trying to disaggregate the big hardware boxes. I’m not sure there’s a technical justification. There’s a market justification. I don’t think there’s a technical justification. I think it’s going to be too difficult.

When it comes to kind of L4 through L7 services, these things are already on x86, virtualisation will happen. The carriers know how to provide these as a service. I think they’ll be successful with that. I’m suggesting something even more radical, which is why don’t you build an API and a platform that the guys that you typically have host have to use?

So instead of hosting BitTorrent or Netflix or whatever, have them program to your APIs. And so I’m not sure if anybody’s talking about that but me, but I do think that’s what NFV should become.”

Conclusions:

Lack of effective security remains the number one obstacle to cloud adoption for enterprise customers. Malware is getting worse and the evil people who create it are getting better at finding ways to insert malware/ spyware into both servers, switch/routers and virtual machines.

A solution like Casado proposes (the horizontal layer within a hypervisor) seems quite workable, but it hasn’t been implemented yet by any vendor we know of. Instead, there are a raft of add-on security appliances and agents that don’t provide a whollistic and effective security solution. Let’s hope that security becomes a competitive issue in the world of virtualized systems, especially within cloud resident data centers.

Addendum:

VMware: How the Hypervisor can be Security’s Savior

http://www.computerworld.in/news/vmware%3A-how-the-hypervisor-can-be-security’s-savior

Acknowlegement:

The author sincerely thanks Martin Casado, PhD Stanford, for his diligent review of this article and his helpful comments and corrections that made it more accurate.

Postscript:

A Sept 27, 2014 Barron’s article hints that VMWare may sell Hypervisor security software to commodity servers and bare metal switches:

“In an age of break-ins at major retailers like Target and Home Depot, he notes, more and more network attacks can’t be stopped by conventional network firewall devices sold by Cisco and Check Point Software Technologies. To Martin Casado of VMWare, the virtual machine will assume a new role of protecting all the precious containers running on each server.

“So, call it a security visor, call it whatever you want,” he says. “The nature of a hypervisor changes to one of providing isolation for those applications,” he says. Casado’s ambition is even broader. Some of the traditional network switching business of Cisco can be disrupted, he says. VMware hypervisor software can be sold as a program to manage inexpensive switches from Dell and others that undercut Cisco’s premium. It is, to Casado, a grand transformation of the networking business, one that clearly excites him as he draws various diagrams on a white board of the shifting architecture of networks. “We haven’t even seen yet what will happen with this fundamental change” in IT, he says.

The business he oversees, called NSX, is running at over $100 million annually, still small, but Casado has 3,000 VMware salespeople to help sell it, and 50 million VMware-enabled virtual machines running in data centers—”enormous” resources,” he says.”

If he can transition VMware to the next era of data centers and networking, Casado may both save the company from obsolescence and open up a new frontier on Cisco’s turf.

Alcatel Lucent introduces SDN Switch while Nuage Networks gets contract with Cloud Services Provider

Alcatel-Lucent has broadened its software-defined networking (SDN) portfolio with the introduction of a programmable access switch that features embedded analytics and can scale to deliver up to 32 10G uplinks. The OmniSwitch 6860 supports the OpenFlow and OpenStack protocols and will be commercially available next month.

It features 24 or 48 Gigabit Ethernet ports, four fixed 1G/10G SFP+ ports and two 20G Virtual Chassis link ports for stacking into a virtual chassis. Up to eight switches can be connected into a virtual chassis with up to 32 10G uplinks and 384Gigabit Ethernet ports.

The enhanced OmniSwitch 6860 “E” models also support four unique 1G PoE ports that offer up to 60 watts of power to support devices that require high power, such as small cells that combine cellular and Wi-Fi, and high definition video surveillance cameras. The 6860 also includes embedded analytics and programmability, Alcatel-Lucent says. It features an ASIC and coprocessor for deep packet inspection and policy enforcement. This is intended to give IT more visibility into applications passing through it, bandwidth consumption, and enforcement of prioritization, QoS and security policies.

More at: http://www.businesscloudnews.com/2014/04/02/numergy-selects-nuage-networks-for-sdn-to-support-cloud-datacentres/

Numergy selects Nuage Networks for SDN to support cloud data centers

One year old Nuage Networks provides a software defined networking (SDN) platorm for provisioning, orchestration, and control of virtual network resources/end points The wholly owned subsidiary of Alcatel Lucent provides needed software for that facilitates connectivity between virtual resources in data centers, inter-connection of federated data centers and tieing together of virtual private networks used by branch offices to access cloud services.

French cloud service provider and IT specialist Numergy recently announced that the company will deploy Alcatel-Lucent routers and Nuage Network’s SDN platform to support its cloud computing infrastructure. Numergy is owned by a French consortium that includes the government, SFR and Bull. It said the move is an essential stepping stone towards virtualising more of its datacentre resources. Their mission: to build a “sovereign cloud” that serves consumers and businesses, first in France and then in Europe, and to ensure the location and privacy of sensitive data in compliance with the laws of France and the European Union (EU).

Numergy implemented Nuage Networks’ virtualized services platform (VSP) and virtualized services gateway (VSG) as well as Alcatel-Lucent routers to manage and automate its datacentre networks. The company said the upgrades will make its internal networks more efficient, and that this is a key stepping stone in its broader strategy to virtualise more of its datacentre resources.

“We are pleased to implement the Nuage Networks product suite in our cloud infrastructure. The Nuage Networks SDN technology allows us to address key performance and compatibility requirements for an open environment,” said Erik Beauvalot, chief operating officer of Numergy. “This will allow us to virtualize our infrastructure and to offer our customers cloud services in a more dynamic way,” Beauvalot added.

During the Netevents Cloud Innovation Summit, CEO Sunil Khandekar said, “Look at application delivery as the product of the network. Because if we orient ourselves in making us think of networks and compute and storage in terms of allowing applications to be deployed very, very rapidly the whole model in how we build and automate these networks completely changes.” Sunil added that SDN was the technology that made rapid and robust application delivery happen. He said that the key attributes of SDN are abstraction, automation, control and visibility. Abstraction of the underlying network was defined as having the applications not be concerned about VLANs, IP addressing, what protocols they’re running, etc. in the network. They just specify what they need, what the application requirements are in an abstract format and the SDN tools facilitate the virtual connections.

Nuage Networks won Enterprise award at the 2014 NetEvents Cloud Innovation Summit held in Saratoga, California on March 27, 2014. All the award winners are listed in this article:

https://techblog.comsoc.org/2014/03/29/winners-of-the-netevents-cloud…

The Nuage Networks Portfolio includes:

- Nuage Networks Virtualization Services Platform (VSP) – lays the foundation for an open and dynamically controlled datacenter network fabric to accelerate application programmability, facilitate unconstrained mobility, and maximize compute efficiency for cloud service providers.

- Virtual Services Directory (VSD) – serves as a policy, business logic & analytics engine for the abstract definition of network services. Through RESTful APIs to the VSD, administrators can define and refine service designs and instantiate enterprise policies.

- Virtualized Services Controller (VSC) – serves as the robust control plane of the datacenter network, maintaining a full per-tenant view of network and service topologies. It is an SDN controller with advanced federation capabilities that ensure scaling and graceful interconnection to existing IP networks. Through interfaces such as Openflow, the VSC programs the datacenter network independent of networking hardware.

- Virtual Routing & Switching (VRS) – serves as a virtual endpoint for network services. Through the VRS, changes in the compute environment are immediately detected, triggering instantaneous policy-based responses in network connectivity to ensure that the needs of applications are met.

- Nuage Networks 7850 Virtualized Services Gateway (VSG) – extends the benefits of SDN automation seamlessly between virtualized and non-virtualized assets in the datacenter. The 7850 VSG is a high-performance gateway platform, offering up to a terabit of capacity in a single rack unit with full layer 2 to layer 4 capabilities for multi-tenant datacenter environments.

More at: http://www.alcatel-lucent.com/news/2014/numergy-and-secure-sovereign-cloud

http://www.businesscloudnews.com/2014/04/02/numergy-selects-nuage-networ…

http://www.nuagenetworks.net/resource-center/

Nuage Networks Launch Event April 2, 2013

http://www.youtube.com/watch?v=Y2WXJeOg5Ko

Stay tuned for a feature article on Nuage Networks, based on a visit to their Mt View, CA facility today (April 3, 2014) and their comments at last week’s Cloud Innovation Summit (March 27-28, 2014) in Saratoga, CA.

Regulatory Barriers to >95 GHz Wireless Technology

While ITU has spectrum allocations as high as 275 GHz and claims jurisdiction to 3000 GHz, FCC – and probably all nation spectrum regulators (“administrations” in ITU jargon) – have no specific rules, licensed or unlicensed, for frequencies greater than 95 GHz – with the minor exception of provisions for radio amateurs and ISM (e.g. microwave ovens) in a few small segments. This lack of rules and quick market access probably inhibits capital formation for innovative wireless products because it raises unusual and unquantifiable “regulatory risks”

The commentators of Fox News repeatedly comment on the “war on coal” and the “war on religion”. Well, the “war on millimeter (mmW) wave technology” at FCC is just as real and easier to document, although it is no doubt unintentional. There are 3 proceedings at FCC that document FCC’s present disinterest/apathy towards commercial use of cutting edge microwave technology, even as other national competitors advance in this area due to better collaboration between indusrial policy and spectrum policy.

The current situation of US regulation >95 GHz needs the urgent attention of communications technologists, especially researchers and firms dealing with millimeter wave technology. The lack of “service rules” beyond 95 GHz makes regular commercial licensed or unlicensed mmW use impossible. This in turn greatly complicates capital formation for such technology because VCs can easily find other technology to invest in that does not involve making a prominent communications lawyer member a member of your family for several years and paying his children’s college tuition while at the same time the entrepreneur has no access to market and bleeds red ink.

Sadly, with the exception of the IEEE 802 LAN/MAN Standards Committee (the techies behind Wi-Fi standards), Boeing, and the more obscure (at least in FCC circles) Battelle Memorial Institute and the rather obscure Radio Physics Solutions, Inc., no commercial interests have filed comments with FCC on 3 key issues blocking capital formation for technology above 95 GHz and by extension hindering US competitiveness in advanced radio technology.

The 3 dockets involved are:

- Docket 10-236 which as was supposed to encourage experimentation had the apparently unintended effect of complicating millimeter waver research by forbidding, for the first time and without an explanation, all experimental licenses in bands with only passive allocations – independent of whether there was any adverse impact on passive systems. Many mmW bands have only passive allocations and it is difficult a and expensive to avoid them in initial experiments with new technology and it is not important if there is no passive use near the experiment than could get interference. Since the text of the Report and Order contradicts itself on this issue, the simplest explanation is that a sentence was put in the wrong section. Your blogger filed a timely reconsideration petition when he noticed this 2 days before the deadline and that had been supported by Battelle and Boeing and has been opposed by none. But FCC doesn’t necessarily react in a timely way, specially when incentive auctions are very distracting and staffing is low, unless there are multiple expressions of concerns, preferably from corporate America.

- Docket 13-259 deals with the IEEE-USA petition seeking timely treatment of new technology proposals for this green field spectrum >95 GHz under the terms of 47 USC 157, although any clear statement from FCC on how to get timely decisions on such spectrum would be useful.

- Docket 13-84 has proposed updating the Commission’s RF safety rules. The rules currently only have numeric limits up to 100 GHz – the upper limit of the standard they were based on when they were last updated almost 2 decade ago – but the new proposals are silent on numeric limits above 100 GHz even though the standard that is now the base of the regulations now goes to 300 GHz! This lack of a specific safety standard above 100 GHz adds even more to the regulatory uncertainty of those interested in mmW technology. With today’s mmW technology, the specific numeric standard doesn’t really matter much because exposures will be low. But this proposal to leave ambiguity for mmW systems can be very damaging. Battelle has proposed one way to deal with a specific standard. Others interested in mmW technology should either support it or propose an alternative.

- RM-11713 A specific proposal from Battelle for rules to allow a licensed point-to-point service at 102-109.5 GHz (between 2 bands allocated for only passive use).

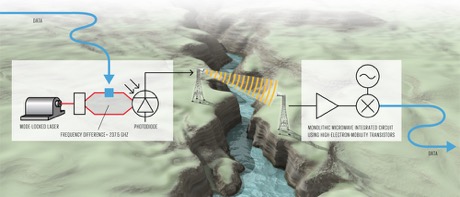

Technology above 95 GHz may not be available at retailers like Walmart and Radio Shack today, but it is not “blue sky” either. (Wi-Fi was not a household word – even even yet named – when FCC created the rules for it in 1985.) The pictures below shows a 120 GHz systems used 6 years ago and a recent German 237 GHz experiment.

Spectrum policy need not be a “spectator sport”. Wireless innovators should realize that access to capital for R&D depends on real business plans and that includes timely spectrum access in the case of wireless technologies. Listed above are 4 FCC proceedings that deal with technologies >95 GHz. The technical community has been oddly silent on all 4. You may not agree with all of them or even some of them, but the proper way to deal with that is make your voice known and tell FCC and/or you national spectrum regulator what you think about policies at the upper end of the spectrum.

vox populi, vox dei

Japanese 120 GHz system used at 2008 Beijing Olympics

German 237 GHz System exceeding 100 Gbits/s

( An experiment probably not permitted in USA under the terms of FCC’s recently revised experimental license rules)

Winners of the NetEvents Cloud Innovation Awards 2014: Martin Casado is Cloud Industry Idol

Winners of the NetEvents Cloud Innovation Awards 2014 were announced March 27th at the NetEvents Cloud Innovation Summit celebration dinner in Los Gatos, CA, USA. These annual Industry Innovation Awards celebrate organizations and individuals that lead the world by innovation and performance in the networking and telecommunications sector.

The top prize was the “Cloud Industry Idol” award, won by Martin Casado, CTO Networking, VMware (and founder of Nicira, which was acquired by VMware in 2012 for $1.26 billion). Mr Casado, PhD Stanford, is quite a humble gentleman. He is an ultra marathon runner who actively competed in multiple races per year before his arduous business air travel shut him down. He wrote in an email to this author: “Thanks Alan, it was a pleasure to meet you. Flying 320K miles last year was brutal. I’m on track for the same this year….”

Mr Casado maintains a personal ultra running web page at: http://yuba.stanford.edu/~casado/ultrarunning.html

At the awards ceremony, NetEvents CEO Mark Fox said: “Martin’s vision and innovations have helped ignite a vibrant SDN research community with potential to bring about one of the most radical transformations the networking industry has witnessed in the past 20+ years.”

That’s likely because Martin is credited as the inventor of OpenFlow API/protocol (between the separate Control and Data Plane equipment) while a PhD student in 2007. “SDN and OpenFlow came out of work we were doing at Stanford,” Casado said. The term SDN was coined in 2009, but has become quite vague now. Neither Nicera or VMWare use OpenFlow in their implementations of Network Virtualization. The latter is effectively an overlay networking model, rather than the pure SDN model which requires all new -SDN complaint- networking equipment.

Other Cloud Innovation 2014 award winners were:

Cloud Security Solution – for the most innovative, practical and effective contribution to cloud security – was won by HyTrust DataControl™ encryption and key management for its ability to give the data owner control of the keys to their cloud based data encryption solution. The other finalists were Juniper Networks & Wedge Networks (joint solution submission) and F-Secure.

SDN Solution for the Enterprise – for SDN solutions that offer easy migration, that deliver early ROI, and generally encourage businesses to take the first steps to tomorrow’s networking. The result was a shared win for Nuage Networks’ Virtualized Services Platform (VSP) and HP’s Network Optimizer SDN application.

Hottest Cloud Company – this award was open to wide interpretation and was a difficult choice between AirWatch, NetSuite and one year old Nuage Networks. “NetSuite’s one integrated offering allows companies of any size to move seamlessly move through most business operations” according to the judges, who awarded it also on the strength of its easy set-up and operation.

NFV Solution for Carriers – from a finalist line-up of Cyan, Gigamon and a joint submission from Juniper Networks & Wedge Networks, the judges picked out Cyan Blue Planet, notably for its support of an open cloud environment “whether Cyan hardware products are involved or not.”

Cloud/Datacenter Solution – for the most innovative Cloud/Datacenter solution, providing major business benefits – was won by Citrix’s CloudPlatform unified cloud management. The other finalists were CoreSite and RedHat

Cloud Mobility Solution – for cloud mobility solutions that offer useful and seamless service, but without compounding IT headaches. The judges decided that AirWatch’s superb security solution, and the choice of ways to implement their solutions added up to a winning formula – over fellow finalists Aerohive and AdaptiveMobile

Cloud Services for the Enterprise – won by Comcast over finalists Basho and RedHat, notably on the strength of its superb friendly service to smaller business customers, including the Cloud Desk “concierge service” for hosted applications and the simplified customer support and billing.

Summing up Mark Fox, said: “These awards offer a rare opportunity to raise a company’s profile in front of the world’s leading media gatekeepers – reaching a massive global audience of high-level decision makers. What’s more, these awards have also raised over $100K for charities to-date.”

For information about the NetEvents program of events plese visit:

http://www.netevents.org/events/events-overview

NetEvents PR contact:

Helen Whitworth

NetEvents International

[email protected]

+44 (0) 870 760 6464

Cloud Innovation Summit Snapshot:

A key theme of this conference was that new approaches to cloud security are urgently needed. Martin Casado said he and VMware will be working on that. “Security will never be the same,” he said pointing to increased threats and requirements for malware and network protection along with vulnerability assessment/management.

Martin’s Stanford PhD Thesis (published in December 2007): ARCHITECTURAL SUPPORT FOR SECURITY MANAGEMENTIN ENTERPRISE NETWORKS presents a principled approach to network redesign that creates moresecure and manageable networks. It proposes a new network architecture in whicha global security policy defines all connectivity. The policy is declared at a logically centralized Controller and then enforced directly at each switch.

One panelist suggested that security functionality should be included in the application program and executed in the cloud. Others advocated building security into the lowest layer and implementing it in silicon (as Intel has done after their purchase of McAfee).

We will be covering Mr Casado’s keynote presentation as it relates to Cloud Security as well as selected others in forthcoming articles. We will also consider writing up some of the 1 on 1 industry chat sessions that took place Thursday and Friday afternoons.

Stay tuned….

Internet of Things (IoT) Key Messages- Part 2: IDC DIrections 2014 + Market Survey Abstracts

Introduction:

I attended three of four IoT sessions at IDC Directions 2014 plus sat in on a lunchtime roundtable discussion of IoT devices and semiconductors led by Mario Morales. All of the above were excellent. This article provides highlights of two presentations and abstracts of various IoT market studies.

On the Cusp of a Demand-Driven Internet of Things (IoT) Market, by Carrie MacGillivray

- 30B Connected Things Predicted by 2020!

- 2012 -2020 CAGR = 6% from 19B connected devices in 2012

- IoT Revenue Almost 2x by 2020 to $8.9T from $4.8T in 2012

- IoT has been a supply driven market with vendors looking for new opportunities and revenue sources.

- IoT has potential to complement product and service portfoliosOngoing development of connected Smart Cities/Cars/Houses/Things Regulatory environment

- Age of “Big Data” will be used to analyze information collected from Internet connected devices

- Connected Culture -High affinity for full-time connectivity

-Device & semiconductor manufacturers

• Market transformation means change from top to bottom at your organization

• Markets are being redefined

• The next big markets are all ready here

• Intelligent systems unlock opportunity

• Appetite for data drives sustainable growth

• From the cloud to client

• Technology alone does not guarantee success

• Moving away from shipping hardware to system level value and solutions

• Focus must be on execution and solutions that address a diverging set of customers and vertical markets

• Ecosystem is fragmented, vertical market focused

Key technologies enabling IoT business transformation:

• Heterogeneous SoCs

• Low power connectivity and SoCs, energy harvesting/reduction

• Security in silicon

• Large solid state capacity to support appetite for data and eventually analytics

• Natural User Interfaces (NUIs)

• Intelligent sensor fusion

• Audio and visual search, real time system learning

Proliferation of sensors are tied to their User Interface (UI):

• Providing systems with contextual awareness

• Connecting with our environment

• 40 year effort to replicate human senses

• Market still looking for viable usage scenarios, applications, and business models

IoT Transformation Drives the Monetization of Data

Today: Function & data, Connected, Limited Security

Tomorrow: Data drives function, Interoperable, Scalable, Security is fundamental to IoT solution

IoT Markets with potential:

During his closing keynote, UT Professor of Innovation (and Ethernet inventor) Bob Metcalfe, PhD, said that “software defined networking (SDN) hasn’t really found it’s niche yet. Perhaps, it will in managing the Internet of Things.” Even though SDN was never intended to be used to provision, control and manage the IoTs/connected devices, we suggest that it could do so along with managing internal network equipment from source to destination route.

IDC’s Worldwide Internet of Things Spending by Vertical Market 2014–2017 Forecast – Feb 2014

This IDC study analyzes the worldwide vertical market opportunity for the burgeoning Internet of Things (IoT) market. It provides a market outlook for 2012–2017 and sets the forecast within the context of the IoT ecosystem, including intelligent systems, connectivity services, platforms, analytics, and vertical applications in addition to security and professional services required to build out a complete picture. This study discusses the key vertical market trends contributing to the growth of the IoT on a worldwide basis. A worldwide vertical market revenue forecast is included.

“The Internet of Things market must be understood in terms of vertical markets because the value of IoT is based on individual use cases across all markets,” said Scott Tiazkun, senior research analyst, IDC’s Global Technology and Industry Research Organization. “Successful sales and marketing efforts by vendors will be based on understanding the most lucrative verticals that offer current growth and future potential and then creating solutions for specific use cases that address industry-specific business processes.”

https://www.idc.com/getdoc.jsp?containerId=246384

Addendum: IoT Market Research Studies

Mckinsey Global Institute’s Disruptive Technologies report calls out the Internet of Things (IoT) as a top disruptive technology trend that will have an impact of as much as $6 Trillion on the world economy by 2025 with 50 billion connected devices. The Internet of Things is the next huge wave of growth of the Internet. Big growth numbers and expectations are dramatically expanding for the Internet of Things in Silicon Valley and globally. Valuations for IoT startups have also increased dramatically and caught Wall Street and the venture capital community by storm, including Google’s acquisition of Nest for $3.2 billion dollars and Jawbone’s pre-IPO valuation at $1.5 billion.

Gartner Group: IoT to transform data center market

The Internet of Things (IoT) has a potential transformational effect on the data center market, its customers, technology providers, technologies, and sales and marketing models, according to Gartner, The IoT is expected to reach 26 billion units installed by 2020, and by that time, IoT product and service suppliers will generate incremental revenue exceeding USD 300 billion, mostly in services.

The report has also identified potential challenges, covering security, enterprise, consumer privacy, data, storage management, server technologies, and data centre network.

The increasing digitization and automation of the multitudes of devices deployed across different areas of modern urban environments are expected to create new security challenges to many industries. Significant security challenges will remain as the big data created as a result of the deployment of myriad devices will drastically increase security complexity. This, in turn, will have an impact on availability requirements, which are also expected to increase, putting real-time business processes and, potentially, personal safety at risk.

As is already the case with smart metering equipment and increasingly digitized automobiles, there will be a large amount of data providing information on users’ personal use of devices that, if not secured, can give rise to breaches of privacy. This is particularly challenging as the information generated by IoT is a key to bringing better services and the management of such devices.

The impact of the IoT on storage is two-pronged in types of data to be stored: personal data (consumer-driven) and big data (enterprise-driven). As consumers utilize apps and devices continue to learn about the user, significant data will be generated.

The impact of the IoT on storage infrastructure is another factor contributing to the increasing demand for more storage capacity, and one that will have to be addressed as this data becomes more prevalent. The focus today must be on storage capacity, as well as whether or not the business can harvest and use IoT data in a cost-effective manner. The impact of IoT on the server market is forecast to be largely focused on increased investment in key vertical industries and organizations related to those industries where IoT can be profitable or add significant value. Existing data center WAN links are sized for the moderate-bandwidth requirements generated by human interactions with applications. IoT is expected to dramatically change these patterns by transferring massive amounts of small message sensor data to the data center for processing, dramatically increasing inbound data center bandwidth requirements.

The magnitude of network connections and data associated with the IoT are expected to accelerate a distributed data center management approach that calls for providers to offer efficient system management platforms. This new architecture will present operations staffs with significant challenges, as they will need to manage the entire environment as a homogeneous entity while being able to monitor and control individual locations. Furthermore, backing up this volume of data will present potentially insoluble governance issues, such as network bandwidth and remote storage bandwidth, and capacity to back up all raw data is likely to be unaffordable. Consequently, organizations will have to automate selective backup of the data that they believe will be valuable/required. This sifting and sorting will generate additional big data processing loads that will consume additional processing, storage and network resources that will have to be managed.

http://www.telecompaper.com/news/iot-to-transform-data-center-market-stu…

Semiconductor Wireless Sensor Networks IoT Market to Hit $12 bil by 2020 Forecasts a Research Report

Worldwide markets are poised to achieve significant growth as the Semiconductor Wireless Sensor Network is used to implement the Internet of things and to monitor pipelines, oil wells, and health care patients to illustrate the variety of projects supported by these networks.

Semiconductor wireless sensor networks (http://www.reportsnreports.com/reports/275026-semiconductor-wireless-sensor-internet-of-things-iot-market-shares-strategies-and-forecasts-worldwide-2014-to-2020.html) are used for bridge monitoring, implementing the smart grid, implementing the Internet of things, and monitoring for security implementation. The systems are used to implement energy savings in homes and commercial buildings, almost anything can be monitored with sensors and tracked on a smart phone. Projects are ongoing.

With 9 billion devices connected to the Internet in 2014, phenomenal growth is likely to occur when that number rises to 100 billion by 2020. Businesses control devices with sensors and wireless sensor networks (WSNs).

The sensors connected to the Internet promise to bring a big data explosion. Much of the data will be discarded, as users get simply overwhelmed by vast volumes. Analytics will become popular inside the wireless sensor networks so that alerts are generated at the point of collection of data.

The issue is how to embed analytics into the wireless sensor network control units so that only the alert data needed is transmitted. Users of information need to be able to find, control, manage, and secure the information coming from sensors onto the network. Users need to analyze and exploit the information coming from sensors.

Advanced technologies for wireless sensor networks are associated with emerging ways of interconnecting devices that have never been connected before. Networking is based on leveraging the feasibility of making sensors work independently in groups to accomplish insight not otherwise available. Advanced storage devices are emerging simultaneously with the energy harvesting devices that are economical, making sensor networks feasible. Storage devices can leverage the power captured by energy harvesting when sensors and devices are interconnected as a network.

Data storage technologies connected to the sensors are permitting far better control of the world around us, implementing vastly improved energy efficiency as lights and hearting are turned on and off just as needed. Wireless sensor networks implement cost-effective systems.

Wireless sensor networks are developing a market presence. They are set to power wireless sensor network proliferation. Independent sensor devices located almost anywhere have attained workable levels of efficiency.

The proliferation of apps on smart phones will drive growth of semiconductor wireless sensor networks markets because the sensors work directly as they are installed without excess labor and wiring that has been necessary previously, making the systems more convenient to install and run.

Healthy lifestyle choices can increase the length of DNA sequences found at the end of a person’s chromosomes and reverse aging. This discovery is likely to increase interest in monitoring and testing DNA sequences and looking at the ends of the chromosomes. This discovery is likely to increase a shift toward wellness initiatives. It has stimulated the need for better communication between clinicians and patients. New sensor technology creates the opportunity for monitoring and testing. Wireless sensor network devices can be used to send alerts to at risk people who are exercising.

Wireless sensor networking is set to grow as sensors are freed from the grid and networks implement connectivity that is mesh architecture based. Converting ambient energy to useable electrical energy harvesting (EH) systems creates the opportunity to implement wireless sensor networks. These networks interconnect an inexpensive and compact group of devices and sensors. The networks use wireless capability to power portable electrical devices.

According to the semiconductor wireless sensor network market research study, “Semiconductor wireless sensor network markets are evolving as smart phone devices and technology find more uses throughout the landscape of the Internet of Things. Sensors can provide monitoring that has not previously been available. Differential diagnostic tools support provide differential information that helps manage our daily lives from traffic patterns to crime detections, to medical treatment.”

“The decision process take into account clinical findings from the home monitoring devices and from symptoms verbally communicated in a clinical services setting. Improved economics of healthcare delivery implementation is facilitated by wireless sensor networks. This is true across the spectrum of things that can be monitored by sensors”

Semiconductor Wireless Sensor Networks Markets at $2.7 billion in 2013 are forecast to reach $12 billion Worldwide by 2020. Wild growth, frequently measured as penetration rates is a result of the change out of wired sensor networks for wireless ones. In addition, the wireless networks have a broader reach than the wired ones did, spurring market extensions in a variety of applications, some not even thought of so far.

Market growth is dependent on emerging technology. As the wireless technology, the solid state battery, the sensor technology, smart phone technology and the energy harvesting technology all become commercialized, these devices will be used to implement wireless sensor networks. The semiconductor wireless sensor networks markets will be driven by the adoption of 9 billion smart phones by 2020, creating demand for apps that depend on sensor networks.

Inquire for Discount at: http://www.reportsnreports.com/contacts/discount.aspx?name=275026

IoT Key Messages from TiE-SV, IDC Directions 2014 and Yankee Group- Part I TiE-SV IoT event & TiECon 2014

Part I: TiE-SV Panel and IoT Track at TiECon 2014

Introduction:

In the past two weeks, we’ve attended Internet of Things (IoT) presentations at TiE-Silicon Valley (SV), IDC Directions 2014 and (via webinar) from Yankee Group. This three-part article summarizes the key take-aways from each of those events.

Backgrounder:

The confluence of efficient wireless protocols, improved sensors, cheaper processors, and a bevy of startups and established companies developing the necessary management and application software has finally made the concept of the Internet of Things (IoT) mainstream.

by 2020, Internet-connected devices are expected to number between 26 billion and 50 billion (depending on which forecast you believe). For every Internet-connected PC or handset there will be 5-10 other types of devices sold with native Internet connectivity. These will include all manner of consumer electronics, machine tools, industrial equipment, cars, appliances, and a number of devices likely not yet invented. In our view, the concept of the IoT will disrupt consumer and industrial product markets generating hundreds of billions of dollars in annual revenues, serve as a meaningful growth driver for semiconductor, networking equipment, and service provider end markets globally, and will create new application and product end markets that could generate billions of dollars annually

The IoT will result in profound changes in the way enterprises operate and the products they produce and consume. Although machine-to-machine (M2M) applications have existed for quite a while, these applications were closed, highly specialized and expensive. IoT opens up inexpensive connectivity to any device and couples this with the power of the cloud and big data analytics to enable enterprises to reduce costs, optimize resources, create new products, and explore new business models.

McKinsey Global Institute’s Disruptive Technologies report calls out the Internet of Things (IoT) as a top disruptive technology trend that will have an impact of as much as $6 Trillion on the world economy by 2025 with 50 billion connected devices! The economic impact of IoT has been variously estimated as between $14.4 and $19 trillion, and inevitably this will create unprecedented opportunity for entrepreneurs, be they in software, hardware or services. Valuations for IoT startups have also increased dramatically and caught Wall Street and the venture capital community by storm, including Google’s acquisition of Nest for $3.2 billion dollars and Jawbone’s pre-IPO valuation at $1.5 billion.

TiE Silicon Valley IoT March 12, 2014 – Overview presentation and panel session discussion:

The IoT overview was presented by Bill Bien, a partner at Waterstone Management Group LLC. “If software will eat the world, then the IoT will be the teeth that will do the eating,” according to Mr. Bien.

Opinion: That’s a heck of a statement, considering how much software goes into cloud c& mobile computing/ mobile apps, e-commerce, gaming, virtual reality and big data/analytics.

“Embedded intelligence is now growing at 11% per annum, but will grow to In this session, we 40% by 2017,” said Bien (see Note below). “There will be 50B connected devices by 2020,” he added. Vertical market segments such as transportation, retail, agriculture, health care, government and others will all embrace IoT. Investor interest is building up as evidenced by Google’s recent acquisition of smart thermostat maker NEST, according to Bill.

The drivers for IoT include: increased processing power in devices (courtesy of Moore’s Law) and sensors, wireless ubiquity (95% cell phone penetration rate in the U.S.), cloud computing and big data deployments.

IoT will change industries, according to Bill. A few examples: wearable electronics and connected self, connected home and car, industrial Internet, connected health.A Credit Suisse (investment bank) study said there was “significant upside” for the connected home, but which direction it takes isn’t clear. Will everything in the home be connected or will there be separate connected appliance solution depending on use or application, e.g. security, lighting and energy control, etc.

“The connected car will be a $54B opportunity,” according to Bill. That includes both mobile connectivity and services as well as telematics for remote management of the car.Industrial IoT was said to be a $3T to $6T market (by when?). That huge market includes: e-health, manufacturing, smart cities, power grid/smart grid, building controls, process automation.

An astonishing “$45B of the enterprise IoT market will be addressable by start-ups,” Bien predicted. That includes: data analytics, enterprise software and analysis, applications and services.

The Economist magazine stated that enterprise IoT is still in the planning phase with manufacturing in the lead. It has to cross a “chasm” before it can be a commercial success. While there’s great excitement and a lot of interest in enterprise IoT, the industry needs to change how software and services are sold to the customer. Mr. Bien concluded: “Drivers are in place for rapid growth of IoT. A diverse set of apps will soon be developed, but we’re still in the early days of IoT.”

Note: Mr. Bien stated many forecasts for market size, growth rate and number of connected devices, but generally did NOT provide the source for any of those. Part II of this series includes even more market size forecasts, which are all from IDC.

Panel Session Discussion:

Moderator: Brett Galloway, Founder and CEO, Xova Labs

Panelists:

-Thomas A. Joseph, PhD, Senior Vice President, SAP’s Office of the CTO

-Bill Bien, Partner, Waterstone Management Group LLC

-Jasper zu Putlitz, Founder and Managing Director, ansacloud LLC (formerly with Bosch)

-Sanjay Manney, Director of Product Management, Echelon Corporation

-Pradip Madan, Advisor, Board Member, and Investor

-Patrick Eggen, Investment Director, Qualcomm Ventures

The panel first addressed the question of whether or not IoT is a real market, rather than just another way of talking about industrial networking technology. The management and control of high value assets is one way IoT is different and distinct. It’s a platform where discrete data can be used to manage high valued assets, suc h as in health care. It’s a system where many devices talk to each other, e.g. Internet connected health care appliances/monitors.

Sanjay Manney of Echelon thinks the IoT foundation starts with Internet protocols. Then others are added to provide a “reliable form factor for the appropriate applications. There’s a real value in putting sensor data in a software context,” he said.

Patrick Eggen of Qualcomm ventures said that WiFi was probably the most likely wireless network to be used for the IoT. He said that cellular (3G, 4G) might be used in the future, but the economics of 3G don’t work today for many low cost applications. (Note that Sprint is using 2G for many of it’s IoT/M2M configurations). He identified smart cities, sensor based parking as applications while noting that many municipalities have their own proprietary wireless networks with cellular being too expensive to replace them.

Jasper zu Putlitz of ansacloud said the wireless carriers would be big beneficiaries of the IoT. Of course, that assumes that their cellular services (2G, 3G, and 4G) are used. Seven or eight wireless carriers control most global wireless access. 6% growth in service provider CAPEX is primarilly driven by wireless spending.

How IoT will change transportation (cars, trains, buses, etc) was the next panel discussion point. Connected transportation systems will include sensors with built in radios. Telematics will be used to ensure smoother traffic flows. This will be part of many smart city initiatives.The challenge will be integrating many diverse technologies, especially different sensor types. Much of the systems integration will need to be done in software.

One version of the connected home will be for optimized energy management, which will minimize wasted energy usage. Such a system will control heating, lighting and react to the ambient environment, e.g. smoke alarms. But standards for this are missing but needed to o beyond “hobbyist” endeavors. A connected home/IoT system has to work flawlessly and be intuitive to sense (and possibly act) on ambient conditions.The panel continued to debate many interesting aspects of the IoT.

While time and space don’t permit me to cover that, readers are invited to watch this TiE-SV event video at:

http://player.vimeo.com/video/89187936?title=0&byline=0

IoT Track at TiECon 2014:

Many, including this author, believe that the Internet of Things is the next huge wave of growth of the Internet, and TiEcon 2014 will explore this fast expanding field of entrepreneurial opportunities. Big growth numbers and expectations are dramatically expanding for the IoT in Silicon Valley and globally.

TiEcon 2014 (May 16, 2014) will explore all the major IoT trends and the disruptive opportunities they will create for startup innovation, consumer value and enjoyment, societal benefit, and wealth creation. If you are an entrepreneur and interested in surfing the next wave of the Internet, come join us at TiEcon 2014. We will be wrapping up the day with a panel of leading VCs talking about where they plan to invest!More info at: http://tiecon.org/internet-of-things

From TiECON: Why the ‘Internet of Things’ is relevant:

‣ $6 Trillion impact on world economy by 2025‣ 50 Billion connected devices by 2025

‣ Evolution of smart cars, buildings, factories & cities

‣ Proliferation of intelligent wearable technologies & smart devices

‣ Quantum leaps in innovations around healthcare, manufacturing & infotainment

What you will learn at TiECon 2014 IoT Track:

‣ Top market trends and projections in IoT

‣ Technology visions of the whose-who in IoT

‣ Shifts and transformations in value chains

‣ Demonstration of healthcare management through remote applications and sensors

‣ Innovative Ideas and breakthrough opportunities for entrepreneurs

TiECON 2014 Overview:

Infonetics: Data Center Network Market May Become Disaggregated; Caused by Bare Metal Switches

Market research firm Infonetics Research released excerpts from its full 4th quarter 2013 (4Q13) and year end Data Center Network Equipment and SAN and Converged Data Center Network Equipment reports, which now include forecasts for bundled solutions and ports-in-use for storage.

DATA CENTER NETWORK EQUIPMENT MARKET HIGHLIGHTS

. Data center Ethernet switch ports sold as part of a bundled solution made up 27% of all data center ports shipped in 2013, growing to 45% in 2018

. The bare metal switch market has the potential to transform a significant portion of the Ethernet switching market into a disaggregated model, similar to the server market

SAN AND CONVERGED DATA CENTER NETWORK MARKET HIGHLIGHTS

. Nearly half of all converged data center network ports shipped in 4Q13 will carry

storage traffic

. Infonetics forecasts Ethernet switch ports-in-use for storage to reach 55% of all data center purpose-built switch ports shipped in 2018

. Switch ports-in-use for Fibre Channel over Ethernet (FCoE) are expected to account for 22% of all data center purpose-built ports shipped in 2018

ANALYST NOTE

“There’s still room for best-of-breed in the Ethernet switch market, but as the industry moves beyond early adopters and the early market for data center fabrics, the next wave of adoption has to be made simpler for the ‘main street’ buyer,” notes Cliff Grossner, Ph.D., directing analyst for data center and cloud at Infonetics Research. “This will keep the market for best-of-breed solutions healthy even as a portion of the data center Ethernet switch market turns to bundled solutions.”

Grossner adds: “The shift to cloud-architected data centers with automated deployment of virtual workloads will require storage networking to be more agile, driving the need for a converged network with storage and application traffic on Ethernet.”

REPORT SYNOPSES

Infonetics’ quarterly data center network equipment report tracks data center Ethernet switches, application delivery controllers (ADCs), WAN optimization appliances, and Ethernet switches sold in bundles (companies tracked: A10, Alcatel-Lucent, Arista, Array Networks, Barracuda, Blue Coat, Brocade, Cisco, Citrix, Dell, F5, HP, Huawei, IBM (BNT), Juniper, Kemp, Radware, Riverbed, others). Infonetics’ quarterly SAN and converged data center network equipment report tracks chassis and fixed Fibre Channel switches; Fibre Channel HBAs; converged data center switch ports-in-use for storage (iSCSI, FCoE, FC-to-FCoE); and converged data center network adapters (iSCSI, CNAs, universal) (companies tracked: Alcatel-Lucent, Arista, ATTO, Brocade, Broadcom, Cisco, Dell, Emulex, HP, IBM (BNT), Intel, Juniper, QLogic, others).

To buy the reports, contact Infonetics: http://www.infonetics.com/contact.asp

IDC Data Network Prioritites Survey Results:

Reference:

A New Open Data Center Network: Disaggregating the Network Operating System from Switch/Router Gear

http://viodi.com/2013/06/25/a-new-open-data-center-network-disaggregatin…

FREE SDN REPORT AND WEBINAR:

Everyone who registers for analyst Cliff Grossner’s Virtualizing Networks with SDN NVOs and Bare Metal Switches webinar will receive a special Infonetics report, 2014: The Year SDN NVOs and Bare Metal Networking Get Serious. Join the live event March 25 at noon EDT or watch the replay. The webinar explores how network virtualization overlays (NVOs) and bare metal networking make data center network virtualization faster, easier, and more affordable:

http://w.on24.com/r.htm?e=746584&s=1&k=F8942DEE951A3E32B8495DE59289A1E3