Market Research Reports Assess the LTE & VoLTE Markets with Different Forecasts for 2015 and Beyond

Infonetics Research released excerpts from its 3rd quarter 2014 (3Q14) 2G, 3G, LTE Mobile Infrastructure and Subscribers report, which tracks more than 50 categories of equipment, software, and subscribers based on all existing generations of wireless network technology.

3Q14 MOBILE INFRASTRUCTURE MARKET HIGHLIGHTS:

. Operators are currently spending around $5.6 billion per quarter on LTE, and this has prompted Infonetics to raise its 2014 forecast for the global macrocell 2G, 3G, and 4G mobile infrastructure market to $45.4 billion, up from $43 billion the prior year

. Investments initially earmarked for 2015 have shifted to 2014, reinforcing Infonetics’ prediction that the LTE market will peak in 2015

. The worldwide macrocell 2G/3G/4G mobile infrastructure market totaled $11.2 billion in 3Q14, up 0.4% sequentially, and up 10% year-over-year

. Nokia Networks moved into the #1 spot for LTE revenue in 3Q14, propelled by strong performances in the U.S. and China

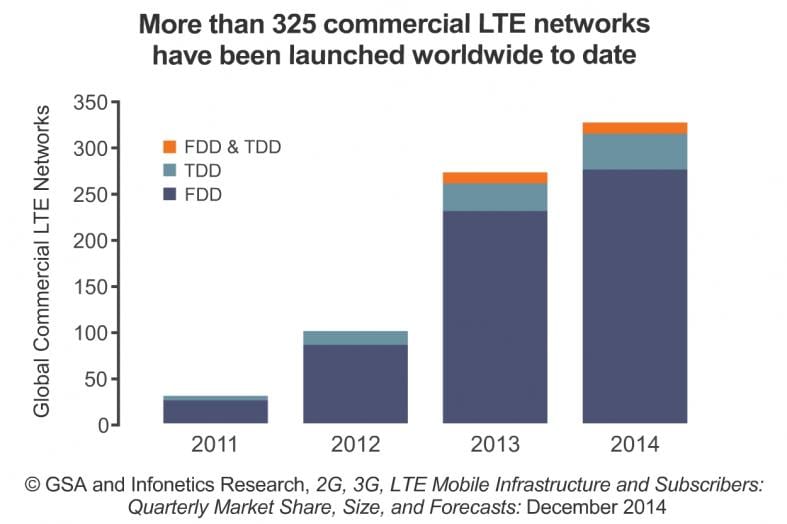

. China continues to push LTE through the roof, but the rest of the world is also moving fast to LTE, with 331 commercial networks launched as of September 2014, as per the GSA

“In the mobile infrastructure market, the third quarter of 2014 was almost a carbon copy of last quarter, and we are now reaching the peak of plain LTE rollouts, which are so brisk in China that they are overshadowing strong activity in Europe, the Middle East, and Russia,” notes Stéphane Téral, principal analyst for mobile infrastructure and carrier economics at Infonetics Research.

In an explanatory email to this author, Stephane wrote: “In our (Infonetics) reports, we explain why the LTE market revenues will peak next year: Simply it’s because we’re done with hardware deployments of eNodeB on this planet! I’ve been telling folks around the world for some time that they should enjoy the ride while they can because the market will start to go downhill in 2016.

One major factoid: China Mobile alone has deployed 570,000 eNodeBs this year. No one else (i.e. other network operator) – not even a single country on this planet can match that rollout! This is 10x the size of an AT&T or Verizon footprint!

Once you have those eNodeBs in place, you need the LTE core network such as EPC (Evolved Packet Core) to start with and then IMS (IP Multimedia System) to implement VoLTE. That’s why VoLTE will keep growing.

LTE-A is mainly a software upgrade, involving some level of hardware but no way near the magnitude of those plain LTE rollouts.

Bottom line: get on Virgin Galactic and go to another planet to roll out eNodeBs or move fast to software!

That’s the story.

Cheers, Stéphane

MOBILE REPORT SYNOPSIS:

Infonetics’ quarterly 2G, 3G, LTE mobile infrastructure report provides worldwide and regional market size, vendor market share, forecasts through 2018, deployment trackers, analysis, and trends for macrocell mobile network equipment, software, and subscribers. The report tracks more than 50 subsegments of the market, including radio access networks (RANs), base transceiver stations (BTSs), mobile softswitching, packet core equipment, and E-UTRAN macrocells. Vendors tracked: Alcatel-Lucent, Cisco, Datang Mobile, Ericsson, Fujitsu, Genband, HP, Huawei, NEC, Nokia Networks, Samsung, ZTE, others.

To buy the report, contact Infonetics:www.infonetics.com/contact.asp

VOLTE WEBINAR AND Free Report:

Join Infonetics analyst Stéphane Téral Dec. 9th at 11:00 A.M. ET for Improving the VoLTE Experience: Best Practices from Early Launches, a live event discussing the increasing importance of user experience measurement and analysis in live networks. Attendees receive an Infonetics companion report titled The State of VoLTE.

Attend live or access the replay:http://w.on24.com/r.htm?e=872675&s=1&k=64BD39225EC39496AAB3F16091F3FB04

Meanwhile, Research & Markets predicts a very bright future for VoLTE. In a new report titled ““Voice over LTE Market by Long-Term Evolution, by Technology, and by Geography – Analysis & Forecast to 2014 – 2020,” the market research firm states:

“The overall voice over LTE market is expected to increase at a CAGR of 64.40% from 2014 to 2020.”

Rich communication services, reduced latency, and increased revenue per user are the main reasons behind the increased adoption of the voice over long term evolution services.

The voice over LTE market report analyzes the ecosystem of the network technologies; and the key market, by technology, includes VoIMS, CSFB and dual radio/SVLTE; by LTE market includes LTE and voice over LTE subscriptions, network launches, LTE network modes and end user devices. The report also provides the geographic view for major regions such as the Americas, Europe, Asia Pacific (APAC), and the Rest of the World (ROW). This report also discusses the burning issues, market dynamics, and winning imperatives for the voice over LTE market.

Voice over LTE is garnering more value due to its various features and technologies that are used in the voice over LTE market. The advantages provided by VoLTE such as High Definition (HD) voice, Rich Communication Services (RCS), faster call setup times, and true device interoperability, integration of voice over LTE with voice over Wi-Fi service, and improved battery life over other network technologies have attracted the new users towards it. The CFSB technology held the highest market share in 2013 but the VoIMS technology is estimated to experience a better growth in the near future.

The report provides a detailed view of the VoLTE and LTE market with regard to the subscriptions, LTE and VoLTE network launches, and LTE and VoLTE technologies market; and also presents detailed market segmentation, with qualitative and quantitative analysis of each and every aspect of the segmentation; done by technology, LTE end user devices, and on the basis of the LTE and VoLTE market, by geography. All the numbers in terms of the volume and revenue, at every level of report, are forecasted from 2014 to 2020.

For more information:

http://www.researchandmarkets.com/research/vzx2lx/voice_over_lte