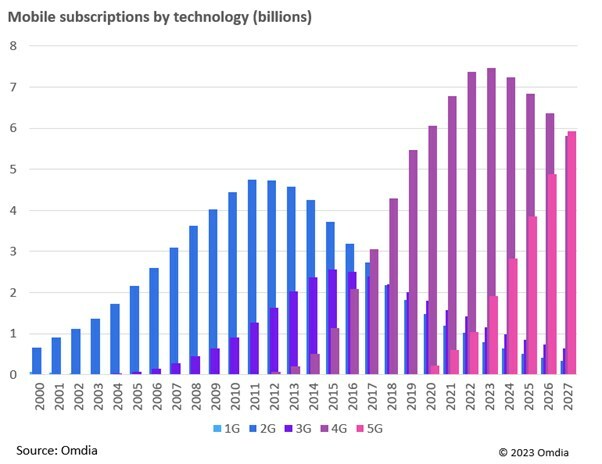

Omdia forecasts weaker 5G market growth in near term, 4G to remain dominant

Multiple factors have slowed down the transition to 5G such as lower handset sales driven by cost-of-living crisis and inflation, poor network coverage, low performance gain perception, and lack of 5G specific applications. Furthermore, an increasing portion of mobile connections – approximately 30% – are not handsets and will be slower to convert to 5G (e.g., IoT, connected tablets/laptops, wearables).

Omdia Senior Market Forecaster, Garinder Shankrowalia, said: “5G subscription reporting in 2022 has led us to reduce our 2023 forecast by 7.2% -approximately 150 million subscriptions. We anticipate the industry will regain this loss from 2025, once global market conditions are improved.”

Omdia believes it is important for mobile operators to continue investing in next generation mobile networks to enable the application emergence and the overall digital economy to grow. However, having multiple cellular technologies running concurrently on mobile networks is having an adverse effect on operators whereby launching 5G increases complexity and cost for little return in the short term.

Omdia Research Director Ronan de Renesse said: “There needs to be a ‘net-zero’ approach to network development, removing the old as the new gets deployed. Operators are already starting to move capital from next generation network deployment to 3G decommission projects and digital transformation. Key stakeholders should remain realistic about the prospects for 5G and re-evaluate the business case before moving on to the next step.”

Omdia forecasts 5G will account for 5.9 billion subscriptions in 2027 equivalent to a population penetration of 70.9%.

Another Opinion: 5G Fails to Deliver on Promises and Potential

5G is a big letdown and took a “back seat” at CES 2023; U.S. national spectrum policy in the works

6 thoughts on “Omdia forecasts weaker 5G market growth in near term, 4G to remain dominant”

Comments are closed.

The telecom marketplace, industry analysts and the press appear to be discovering what Alan J Weissberger, the principal and chief blogger of the IEEE Techblog (techblog.comsoc.org), pronounced nearly 8 years ago. He called 5G as an imminent and one of the biggest technology “trainwrecks” of all time.

Alan, a highly recognized professional in data communications and telecom standards development, foresaw activities (more appropriately, non-activities), mismanagement, incoordination (e.g. 3GPP and ITU-T for 5G non radio standards), and lack of ownership in several aspects of 5G systems architecture (e.g. 3GPP implementation spec for 5G SA core network). He also noted the deficiencies in the ITU-R 5G RAN standard (ITU-R M.2150): URLLC performance requirements (M.2410) not met as 3GPP Rel 16 URLLC in the RAN was not complete, failure to agree on a critical companion standard -5G frequency arrangements (revision 6 of M.1036), and use of pointer tables for detailed 3GPP 5G-NR specs (which could be modified without ITU-R knowledge or approval).

I believe that many 5G professionals and participants were also observing what Alan wrote about, but they opted to remain mostly silent. Today we witness a 5G which at best, brings minimally incremental benefits to most of its users. I have not heard of a single 5G use case that offers a compelling value proposition over 4G. 5G, as of today, is a colossal failure and a cruel joke on its users!

Basant, Many thanks for your kind words, For years, I was drowned out by 5G cheerleaders, especially from 5G Americas and GSMA, as well as the mainstream media. Finally, they are waking up to the truth about 5G being a commercial failure! What’s urgently needed is a URLLC spec that meets the ITU-R M.2410 performance requirements, a solid 5G SA implementation spec, coordination between 3GPP and ITU-T for 5G non radio standards, a standard for mobile roaming, and work to reduce power consumption of 5G base stations and endpoints.

Well said, Basant.

It is amazing that in 2023 we are at peak 4G, even though Alan was predicting this years ago. Even the marketing buzz has probably faded from 5G, as the hype machine moves to new 6G and beyond.

Thanks Ken. All should know that several years ago, Ken was leading an effort (along with Yigang Cai, PhD and myself) to make ITU-R WP5D, 3GPP, and US DoD/Dept of Commerce/etc AWARE OF THE PROBLEMS WITH 5G STANDARDS AND DISCONNECTS. We sent comprehensive emails to each of those entities, requesting a video chat or at least an email dialogue, but not one ever replied!

MWC 2023 – what’s the point of 5G? by Scott Bicheno at telecoms.com:

Four years into the 5G era, the technology is still struggling to find an identity. 3G was about the introduction of mobile data, which matured in the form of 4G, but what is 5G all about? We will be posing that question to everyone we meet at the show next week and expect to get a different answer each time.

Yes, 5G offers even faster and more capacious mobile broadband, but there is still a shortage of use-cases that require more bandwidth than 4G has to offer. IoT became conflated with 5G but has existed as a concept for decades and, as Qualcomm’s latest roll of the dice indicates, is still finding its feet as a commercial proposition.

Even more yawn-inducing are the various claims to greater efficiency and automation. In the absence of ARPU growth they represent another form of return on 5G investments for MNOs but notional opex savings are largely offset by increased demands on the network. That’s why there will be lots of talk about public sector interventions at the show, as well as other potentially margin-boosting initiatives such as Open RAN and the public cloud.

https://telecoms.com/520115/mwc-2023-whats-the-point-of-5g/

GSMA disagrees and offers a very bullish 5G growth forecast. Read about it at:

https://techblog.comsoc.org/2023/02/28/gsma-intelligence-5g-connections-to-double-over-the-next-two-years-30-countries-to-launch-5g-in-2023/