smartphones

TrendForce forecast: Chinese 5G smartphones to hold 4 of top 6 spots by production volume in 2020

Annual 5G smartphone production is expected to reach 235 million units in 2020, an 18.9 percent penetration rate, according to the latest research from TrendForce. Total smartphone production is forecast to reach 1.24 billion in 2020.

Ranked by production volume, Chinese brands are expected to account for 4 of the top 6 spots for 5G smartphone brands in 2020. Huawei tops the ranking, and is expected to produce around 74 million 5G smartphones in 2020. Apple is in 2nd place with a forecast yearly 5G smartphone production of around 70 million units. Samsung will be in 3rd place with production of 29 million 5G smartphones. They are followed by Chinese brands Vivo, Oppo and Xiaomi in 4th, 5th and 6th place with 5G smartphone production volumes of 21 million, 20 million and 19 million units respectively.

Note that this is a forecast, especially for Apple which has not yet announced a 5G smartphone.

Mid-to-low end 5G chipsets released by AP suppliers are expected to raise the penetration rate of 5G smartphones in 2021

TrendForce’s analysis of future developments in the 5G market shows that an aggressive push by mobile processor manufacturers will lead to the rapidly increasing presence of 5G chipsets in the mid-to-low end market, driving 5G smartphone production to surpass 500 million units in 2021, which will potentially account for about 40% of the total smartphone market. Once 5G chip prices reach a stable level this year, smartphone brands may look to gain additional shares in the 5G smartphone market by sacrificing gross margins. In doing so, they are likely to accelerate the drop of 5G smartphones’ retail prices, and the market may see the arrival of 5G smartphones around the RMB 1000 price level by the end of this year. Incidentally, it is worth noting that the penetration rate of 5G smartphones does not equal the usage rate of the 5G network, which depends on the progress of base station construction. Since the current 5G infrastructure build-out is pushed back as a result of the pandemic, the global 5G network coverage will be unlikely to surpass 50% before 2025 at the earliest, with complete coverage taking even longer.

Editor’s Questions:

In the absence of any true 5G standard, e.g. IMT-2020.SPECs, will any of these 5G smartphones work on a 5G network other than the one they are subscribed to? Or will they fall back to 4G-LTE? Will the 5G smartphones sold in 2020 be upgraded to comply with IMT-2020.SPECs and/or 3GPP Release 16 specs?

References:

http://www.trendforce.com/presscenter/news/20200722-10398.html

Omdia: Global smartphone shipments plunge in Q1-2020; Mobile communications revenue to drop 4.1% in 2020

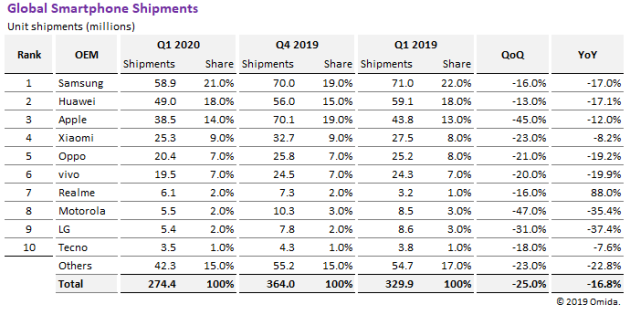

Omdia reported today that global smartphone shipments dropped by 16.8 percent in the first quarter of 2020 as vendors struggled to manage coronavirus-driven production shutdowns, product-launch delays and depressed consumer demand.

Shipments in the first quarter fell to 274.4 million units, down from 329.9 million during the same period in 2019, according to the Omdia Smartphone Intelligence Service. This plunge impacted all the major smartphone brands, with nine of the top-10 OEMs suffering shipment declines compared to the first quarter of 2019.

Editor’s Opinion: The decline will be much greater in Q2-2020 due to all the lockdowns all over the world. Who needs a smartphone when you’re confined to your residence? I hardly use mine at all as I prefer a laptop or tablet when at home.

“Early in the first quarter, the smartphone market was sent reeling by the shutdown of production at facilities in China, which halted the manufacturing of phones and their key components,” said Jusy Hong, smartphone research and analysis director at Omdia. “While concerns about this situation have been alleviated, the smartphone brands also faced new challenges, including disrupted launch schedules for new phones. Even more troubling for smartphone makers is a major decline in global demand due to government lockdown mandates.”

Despite expected rebounds in some countries, the rest of the year is expected to be challenging for smartphone OEMs. Omdia forecasts global smartphone shipments will decline to 1.20 billion units this year, down 13.1 percent from 1.39 billion in 2019.

OEMs feel the pain in the first quarter

Almost across the board, smartphone OEMs faced significant declines in unit shipments compared to the first quarter of 2019.

Samsung retained the top position, with 58.9 million units shipped during the first quarter—a 17 percent decline compared to the first quarter of 2019. Second-ranked Huawei saw its shipments decline by more than 17 percent, to 49 million units, down from 59.1 million in the first quarter of 2019.

Apple, in third place, saw shipments decline to 38.5 million units, down from 43.8 million a year earlier. The 12.0 percent decline comes during the first quarter, historically the weakest period of the year for Apple.

Rounding out the Top 5 are Xiaomi and OPPO. Out of the Top 10, Xiaomi experienced the second least severe decline in the quarter, of 8.2 percent. Only Tecno, in 10th place, attained a lower decrease better with a 7.6 percent year-over-year decline. Xiaomi shipped 25.3 million units in the first quarter, compared to 27.5 million units in 2019. OPPO, on the other hand, suffered a 19.2 percent decline, with shipments falling to 20.4 million units, down from 25.2 million a year earlier.

Realme bucks the downturn

The rest of the Top 10 is made up of vivo, Realme, Motorola, LG, and Tecno. The bright spot here is Realme, which achieved year-over-year growth based on its continued success in India. seventh-ranked Realme was the only top-10 OEM to attain growth during the quarter, with shipments totaling 6.1 million units, up 88 percent from 3.2 million during the first quarter of 2019.

For the others in this group, the first quarter brought significant challenges. Looking at vivo, company shipments declined 19.9 percent, falling from 24.3 million units last year to 19.5 million this year. Motorola, in eighth place, saw shipments decline 35.4 percent to 5.5 million units. While Motorola finally launched its updated RAZR, featuring a foldable display, the publicity surrounding that high-profile device was not enough to support the overall performance of Motorola’s product portfolio.

With or without the impact of the pandemic, LG continues to struggle with its mobile handset division. Shipments declined to 5.4 million units, down from 8.6 million units a year ago—a drop of 37.4 percent. Rounding out the top 10 is Tecno, which saw units decline by a relatively modest 7.6 percent, declining from 3.8 million units last year to 3.5 million units in the first quarter.

First-half struggles

“The smartphone market will face major struggles in the first half of 2020 as different countries experience the initial shock and recovery periods at different times. That’s why OEMs are more afraid of second-quarter sales results,” Hong said. “However, Omdia does expect the smartphone market to start to recover in some countries and regions in the second half of the year.”

Early in the first quarter, the most severe impact on the smartphone market was the shutdown of production and supply chain facilities in China. However, fears over a prolonged closure of essential production, supply chain and logistics operations in China have been alleviated, as signs point to economic activity ramping up quickly in the country.

Smartphone makers in the first quarter also had their product-launch plans disrupted by the cancellation of the Mobile World Congress event in Barcelona, Spain, where many companies had planned to roll out new products.

“Because of the cancellation of the Mobile World Congress, and uncertainty in the supply chain, original product schedules had to be re-evaluated,” said Gerrit Schneemann, senior analyst, smartphones, at Omdia. “However, OEMs seem to have found their footing on how to address new device launches going forward.”

Demand disaster

The impact of the outbreak on the smartphone business has now shifted almost completely to the demand side of the equation.

“Although handsets can be produced at nearly normal levels, the markets for these handsets are mostly in some state of shutdown,” Hong said. “Some countries have made more progress in dealing with the outbreak, while others are still in the midst of fighting the pandemic, and still others won’t feel the full effects of the pandemic until later in the year.”

In Europe, where some countries have been under strict lockdown rules for some time, initial efforts have been made to ease restrictions. Similarly, South Korea has taken steps to open up. In other countries, like in some parts of the United States, only the last few weeks of the quarter were impacted by broad stay-at-home orders, while consumer behavior had remained unrestricted until then.

………………………………………………………………………………………………………………………………

Earlier today, Omdia issued this press release:

Coronavirus crisis deals a $51 billion blow to the global mobile communications industry outlook Mobile revenue to drop 4.1 percent worldwide; regional impact to vary

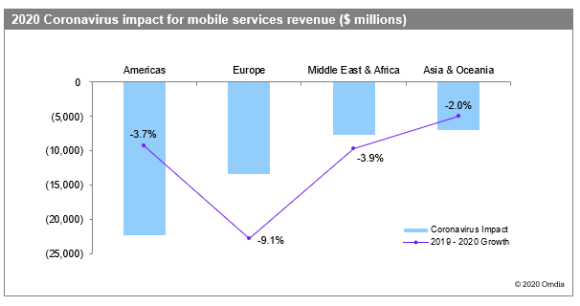

LONDON (April 30, 2020) — Mobile services represent critical infrastructure that’s allowing people to stay connected during the coronavirus crisis. However, that doesn’t mean these services are immune to the pandemic’s economic shock, with 2020 market revenue now expected to come in about $51 billion short of the previous forecast, according to Omdia.

Worldwide mobile communications services market revenue will total $749.7 billion this year, down from the prior forecast of $800.3 billion. This compares to $781.5 billion in 2019. Annual revenue will fall by 4.1 percent this year, with the decline amounting to $31.8 billion.

“Mobile phone companies around the world are experiencing usage spikes as more countries encourage or enforce social distancing and work-from-home rules to slow the spread of the COVID-19,” said Mike Roberts, research director at Omdia. “However, the spikes aren’t enough to overcome the impact of the pandemic on consumer behavior. These rules are having a dramatic impact on various regions of the world, halting new subscriptions and upgrades in the United States, while slashing revenue for operators in Europe.”

Consumer uptake of 5G will be slower than previously forecasted, due to the economic situation as well as the possibility of delays in 5G network deployment and in the availability of 5G devices. Omdia will release more details on 5G shortly.

In the Americas, mobile service revenue is set to decline by 3.7 percent to $237 billion in 2020. Most of that loss will come in the United States as both net additions and upgrades to higher data plans slow or stop altogether.

Europe will suffer the largest impact of the crisis, with mobile service revenue falling 9.1 percent to $131 billion, representing a downgrade of 9.3 percent compared to Omdia’s previous forecast. This decline will be driven by significant reductions in mobile prepaid revenue and a dramatic drop in inbound roaming revenue.

Vodafone UK, for example, said mobile Internet traffic has increased by 30 percent and mobile voice traffic by 42 percent due to the crisis. At the same time, mobile service providers are seeing new business grind to a halt as retail stores close and consumers stop buying new phones as job losses mount. One example of this widespread trend is AT&T, which is closing 40 percent of its retail stores in the United States.

The Middle East and Africa will see a 3.9 percent decline in mobile service revenues to $84 billion, representing a downgrade of 8.4 percent from Omdia’s previous forecast. Major factors for the decline include the impact of low oil prices on Gulf economies and the fragility of economies and health care systems in parts of Africa.

While the impact of the coronavirus on the mobile market is significant in every region, it pales in comparison to the impact the crisis is having on sectors such as travel, tourism, hospitality and retail, which have suffered partial or complete shutdowns. The International Monetary Fund now expects the global economy to contract by 3 percent in 2020, according to its latest World Economic Outlook, which was released earlier this month.

“The massive contraction will clearly impact every segment of the economy, including mobile, but how long it will last in each country and region is virtually impossible to predict,” Roberts said. “One bright spot is that in China, the first country hit by the pandemic, there are signs that the mobile market and broader economy is starting to come back to life.”

Given the high level of economic and commercial uncertainty created by the COVID-19 pandemic, Omdia will be producing a full revision of its global mobile forecasts next quarter.

About Omdia

Omdia is a global technology research powerhouse, established following the merger of the research division of Informa Tech (Ovum, Heavy Reading and Tractica) and the acquired IHS Markit technology research portfolio*.

We combine the expertise of over 400 analysts across the entire technology spectrum, analyzing 150 markets publishing 3,000 research solutions, reaching over 14,000 subscribers, and covering thousands of technology, media & telecommunications companies.

Samsung and Huawei dominate global 5G smartphones; Samsung expects sales to be down significantly due to COVID-19

Strategy Analytics reports that Samsung has become the leader of the 5G smartphone market, shipping 8.3 million handsets across the world during the first quarter of 2020 for a 34.4 percent market share. The South Korean conglomerate took advantage of its strong global distribution networks and operator partnerships and the popularity of its S20 5G and S20 Ultra 5G devices to top the ranking. Strategy Analytics stated that the biggest markets for 5G smartphones were China, South Korea, the U.S. and Europe.

Huawei was the #2 global smart phone vendor with a 33.2 percent market share after shipping 8.0 million 5G smartphones, nearly all in China. Note that Apple isn’t listed because the Cupertino, CA company has yet to announce a 5G smartphone.

The top 5 was rounded out by three other Chinese vendors – Vivo, Xiaomi and Oppo – with 12.0 percent, 10.4 percent and 5.0 percent of the global market, respectively.

Table 1: Global 5G Smartphone Vendor Shipments and Marketshare in Q1 2020

The Strategy Analytics report stated that worldwide shipments of 5G smartphones in the first quarter of 2020 came to 24.1 million, easily topping shipments of 18.7 million in 2019 as a whole. That’s despite the firm’s earlier forecast that global smartphone shipments would be down 25% in 2020.

Chinese smartphone vendors captured 61 percent of top 5 vendor 5G smartphone shipment volumes in Q1 2020, with the majority of those volumes going to the China 5G market. This reflects the speed with which Chinese operators have rolled out 5G networks, as well as the underlying demand for 5G smartphones, despite the Covid-19 pandemic that shut down large parts of China during the Q1 2020 period. As China continues to ramp up economic activity, Strategy Analytics expects 5G shipments to this market to continue to expand dramatically in 2020.

Samsung Electronics disagrees with that forecast as they warned in today’s earnings report that 5G infrastructure investments may face reductions or delays – both internationally and domestically – during the second quarter of 2020.

Sales and profits of set products business, including smartphones and TVs, are expected to decline significantly as COVID-19 affects demand and leads to store and plant closures globally.

In the second half, uncertainties driven by COVID-19 will persist as the duration and impact of the pandemic remain unknown. The Company plans to focus on optimizing resource allocation in the short term, while continuing to strengthen its technology leadership and develop innovative set products.

The Mobile Communications Business aims to strengthen its product lineup by introducing new premium models and expanding offerings of 5G models for the mass market. The Networks Business will focus on developing technologies and enhancing global competitiveness to reinforce the 5G business.

For the Consumer Electronics Division, under the risk of current economic uncertainties, the Company will closely monitor the market situation and will continue to focus on minimizing negative impacts by investing in efficient marketing and promotions tailored to each region and by optimizing its logistics.

…………………………………………………………………………………………………………………………………………………………

A shrinking smartphone market and store closures will lead to an “inevitable” drop in earnings for the current quarter, Jong min Lee, Samsung’s vice president of mobile, said along with other important items on Samsung Electronics earnings call.

In the first quarter, overall market demand drastically decreased quarter-on-quarter as a result of supply chain issues in China caused by the COVID-19 break — outbreak only in this quarter and travel restrictions in the last few weeks of the quarter following the global spread of the pandemic. As the impact of COVID-19, including those on logistics, began to take effect in March, our smartphone shipments also decreased quarter-on-quarter. However, we maintained sound profitability quarter-on-quarter by efficiently deploying marketing investment by improving overall product mix while increasing the sales portion of our premium and 5G model.

Now let me move on to the outlook for the second quarter. With the global spread of COVID-19, demand is expected to drop sharply in most regions due to the economic downturn caused by lockdown across the globe and a corresponding decline in consumer sentiment. As the market shrinks and effects of store closures continue to have direct impact, a drop in sales of our major products and overall performance seems inevitable. Although market uncertainty is higher than ever, we will focus on improving cost effectiveness and strengthening online and B2B channels. In case there are additional disruptions at our production sites, we will respond by effectively utilizing our diversified manufacturing capabilities around the globe. However, we are committed to protecting the health and safety of our employees as well as preventing community spread. We have been thoroughly implementing disinfections and prevention measures in our offices and production facilities in all regions.

For the network business, it is possible that investments in 5G networks will be reduced or delayed domestically and internationally as more effects of COVID-19 unfold.

Finally, I will share our outlook for the second half. In the midst of uncertainties such as the possibility of the prolonged pandemic and the timing of market recovery, we expect the competition to intensify further as companies try to recover from weakness in the first half. For the mobile business, while continuing to offer differentiation in the premium segment with new foldable and Note model launches, we plan to widen the range of choices for our customers and enhance competitiveness within each price range by introducing 5G models to our mass market lineup.

In addition, we will also improve operational efficiency across all areas, including R&D, production, supply, channel and marketing. For the network business, despite uncertainties around the 5G invest plan, we will continue to strengthen our technological competitiveness while improving our 5G business compatibilities globally for the mid- to long term. Thank you.

References:

Strategy Analytics: Global Smart Phone Market to Decline 25% in 2020

https://news.samsung.com/global/samsung-electronics-announces-first-quarter-2020-results