Data Center, Cloud & Campus Networking Equipment + Cisco Beats

by Patrick Seitz of IBD (edited by Alan J Weissberger)

AI and machine learning have crept into the computer networking gear business as hardware vendors look to add more smarts to their routers and switches to help customers better manage data traffic and solve problems.

Cisco, Arista, Netgear and Extreme build a range of wired and wireless network switches and routers for moving data.

“The overall business is pretty healthy,” IDC analyst Rohit Mehra told Investor’s Business Daily.

Spending on Ethernet switches alone is expected to rise 3% to $26.3 billion this year, he said.

Business campus and enterprise deployments are the largest subsegment, accounting for 57% of Ethernet switch spending in 2016, the most recent year for which research firm IDC has full-year data. Data centers accounted for the remaining 43% of spending.

Cisco is by far the largest name in the industry, with a market capitalization of over $200 billion. At a fraction of that size, Arista is next in line, with a market cap near $20 billion.

While Cisco has a full portfolio of networking products across customer segments, Arista Networks is focused today on data center customers.

On Wednesday, investment bank Goldman Sachs initiated coverage of Cisco and Arista with buy ratings and Juniper at neutral. The report noted that enterprise spending intentions for networking gear are at their highest levels since 2007.

“Almost two-thirds of respondents indicated that they expect to increase networking spend in 2018, with only 6% expecting a decrease,” Goldman analyst Rod Hall said in the report.

Arista Networks Targets High-Speed Cloud Data Centers:

Arista has high exposure to the hyperscale data center side of the market, which is expected to accelerate slightly to 29% capital-expenditure growth this year, Hall said.

“We are modeling for revenue upside (at Arista) from consensus, as cloud capex looks set to accelerate again in 2018,” he said. “Arista has established itself as the dominant vendor of high-speed data center networking solutions, with nearly 25% share of 100G data center switches.”

Other Network Equipment Vendors:

Juniper Networks has been hurt by large data-center customers buying more commodity networking hardware from so-called white-box vendors, analysts say.

Commodity networking hardware from ODMs/white box vendors uses merchant silicon from semiconductor firms such as Broadcom, Cavium, and Mellanox Technologies rather than purpose-built chips called application-specific integrated circuits (ASICs) from traditional network gear makers like Cisco and Juniper.

Networking gear vendors have avoided the commoditization price trap partly by placing greater emphasis on software and services.

Because of surging data traffic, network administrators need more tools to help them solve bottlenecks, security issues and other concerns.

Cisco (see Update below) has been a laggard in providing predictive analytics and high-level network monitoring and management capabilities, which created opportunities for a host of companies to step in and fill the gap.

But in late January, Cisco announced initiatives to provide more automation and network management capabilities to its product offerings. It introduced tools designed to help information technology teams become more proactive rather than reactive to problems.

Cisco said IT workers today spend 43% of their time troubleshooting. Software innovations should make IT operations more automated, proactive and agile, the company says.

“There’s more of a realization at Cisco that network monitoring, analytics and visibility is key to delivering automation,” IDC’s Mehra said. “If you don’t build automation into your network systems, you’re not going to be there as the market for IoT (Internet of Things) explodes and as cloud continues to gain more affinity in the enterprise.”

Mergers and acquisitions could play a role in the networking gear space this year, especially with cash-rich Cisco. Cisco could make a meaningful acquisition in 2018, Barclays analyst Mark Moskowitz said in a Jan. 17th report.

“We think CEO Chuck Robbins could make a larger, synergistic acquisition (i.e., north of $5 billion to $7 billion) – something that bolsters the company’s cloud, software, security or services presence on day one,” he said.

On Feb. 2nd, Cisco completed its acquisition of BroadSoft for $1.9 billion. BroadSoft adds cloud calling and contact center solutions to Cisco’s calling, meetings, messaging, customer care, hardware endpoints and services portfolio.

Meanwhile, Arista has been a thorn in the side of Cisco’s core networking business, but could become a bigger threat, Moskowitz said.

“If Arista is able to penetrate the enterprise vertical and also gain traction with its routing foray, the headline and fundamental risks (for Cisco) could start to become more meaningful,” he said.

RELATED:

Netgear Plans IPO For Fast-Growing Arlo Security-Camera Business

Juniper Offers Earnings Beat, Buyback — But Outlook Falls Short

Will Resurgent Cisco Slow Down Arista Networks In Cloud Computing?

…………………………………………………………………………………………………………………

Update – Cisco Fiscal 2nd Quarter Earnings Report:

Cisco today (February 14, 2018) reported a fiscal second-quarter loss of $8.78 billion, or $1.78 a share, compared with net income of $2.35 billion, or 47 cents a share, in the year-ago period. Adjusted earnings, excluding $11.1 billion in charges from the U.S. tax overhaul, were 63 cents a share. Of the 26 analysts surveyed by FactSet, Cisco on average was expected to post adjusted earnings of 59 cents a share; the company had forecast 58 cents to 60 cents a share.

Revenue rose 2.6% to $11.89 billion from $11.58 billion in the year-ago period, breaking a streak of six straight quarters of year-over-year revenue declines. Wall Street had expected revenue of $11.81 billion, according to 23 analysts polled by FactSet. Cisco had predicted revenue of $11.7 billion to $11.93 billion.

- Product revenue, which makes up 73% of the top line, increased 2.6%.

- Services revenue rose 2.9% to $3.18 billion, while analysts had expected a 0.9% rise to $3.13 billion. Security revenue, on the other hand, rose 6% to $558 million, while Wall Street had expected a 10% gain to $582.8 million.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Repatriation of overseas cash, mostly to pay for share buybacks and dividends:

Cisco said it would repatriate $67 billion of its foreign cash holdings to the U.S. this quarter, in one of the largest repatriation plans yet revealed. The company plans to spend much of the newly repatriated cash on share buybacks and dividends, it said Wednesday while reporting earnings, amounting to about $44 billion over the next two years. At the end of the quarter, Cisco had $73.7 billion of cash and equivalents, with the vast majority held outside the U.S. Under the new tax law, the company will be able to access its money at a significantly lower rate than was previously required.

Critics of the U.S. tax law have said increases in share repurchases and dividends show money saved from the law is going to shareholders instead of being invested in new U.S. jobs, infrastructure, research and development, and related areas.

The focus on stock buybacks and an increased dividend suggests Cisco isn’t likely to use the cash on a major acquisition, said RBC Capital Markets analyst Mitch Steves (that contradicts the IBD story above). Instead, he expects Cisco to focus on smaller deals, perhaps in a range of $1 billion to $10 billion.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Since taking the helm of Cisco, Chief Executive Chuck Robbins has focused on subscriptions, common in the software industry but more difficult for a hardware company. That kind of transition can have a negative effect on revenue in the short term, as less of the sale is recognized up front with the rest deferred to later quarters, which Cisco has seen in the past couple of years.

Cisco introduced a new switching family called the Catalyst 9000, a software-centric switch that is delivered as a service with subscription fees and long-term contracts, last June. While previously, a sale of a switch — Cisco’s biggest business — would have been recognized in full up front, Chief Financial Officer Kelly Kramer explained that a healthy portion of that sale is now considered to be for software support and recognized over the length of the contract.

“Of total product revenue, 13% of product revenue is recurring,” Kramer said; at the beginning of Cisco’s fiscal 2015, recurring revenue was about 6% of total revenue, she said.

“The Catalyst 9000 is our fastest ramping product in our history,” Robbins crowed on a conference call.

Kramer largely echoed Robbins’s positive tone in a later interview, while avoiding any grand pronouncements. When asked whether the company’s transition was at an inflection point, she said, ‘I am always hesitant to call any inflection, but I am not surprised about the improvement. Overall, we feel very, very good about our portfolio, this is where we have been focused for a long time.”

Robbins has focused on software as a path, making big-money acquisitions like AppDynamics and BroadSoft, and analysts were curious in Wednesday’s conference call about what may be next for the acquisitive company. Company executives said they plan to bring back all of Cisco’s cash that is outside the U.S. by the end of this quarter under the new tax laws that are now taking hold.

After recognizing an $11.1 billion charge largely from repatriation in Wednesday’s report, Cisco will have many billions of dollars to play with, even after adding $25 billion to its stock-repurchase authorization and increasing its dividend 14% Wednesday.

“We are seeing the benefits of the strategy we started executing on 10 quarters ago,” Kramer said. “We are seeing the benefits as we shift the business model and you are seeing it translate through fantastic financials.

https://investor.cisco.com/investor-relations/news-and-events/events-and-presentations/default.aspx

https://seekingalpha.com/article/4146882-cisco-systems-csco-q2-2018-results-earnings-call-transcript

https://investor.cisco.com/investor-relations/financial-information/Financial-Results/default.aspx

https://www.wsj.com/articles/cisco-returns-to-growth-after-two-year-sales-slump-1518645580

Moore’s law alive in the Data Center; Ethernet adapter revenue up 43% YoY

by Cliff Grossner, Senior Research Director & Advisor Cloud & Data Center Research Practice at IHS-Markit

Introduction:

We cannot measure Moore’s law simply in time between generations. Even though it took Intel longer than 2 years to move from 14nm to 10nm silicon, the number of transistors in their 10nm CPUs exceeded Moore’s Law expectation of 2x per 2 years, according to new research by IHS Markit.

For example, improving transistor IC design helped Intel grow transistor density from 37.5 Million Transistor per Square Millimeter (Mtr/mm2)to 100.8 Mtr/mm2 between 2014 and 2017.

“Since 2007 we’ve seen an immense growth in consumer devices, apps, user-generated content and streaming services, as smart phones and social media gained popularity, driving the need for additional data center (DC) server computational capacity to support them. Connected devices and data-intensive applications will continue to fuel global demand for DC compute and push it up significantly ahead of the average growth of the number of transistors on a CPU,” said Cliff Grossner, Ph.D., Senior Research Director and Advisor for the Cloud and Data Center Research Practice at IHS Markit.

“Strong growth in the demand for DC server computation will compel designers of server hardware to think beyond general purpose compute and consider new server architectures purpose-built for parallel computation that will enable artificial intelligence, advanced driver assistance systems and real-time rendering for virtual and augmented reality amongst others,” Cliff added.

More Data Center Compute Market Highlights:

· Cloud service providers are expected to buy 37% of 2017 DC servers shipped, telco 15% and enterprise 48%.

· White Box – including all vendors that produce rack server hardware with OS software sold separately, such as QCT, Wiwynn and Inventec – was #1 in units shipped in 3Q17 (23% share) for DC servers.

· HPE took the #1 sport in server revenue market share (23%), Dell was #2 (19%), and White Box was #3 (17%) in 2Q17

· Programmable Ethernet adapter revenue was up 7% QoQ and up 43% YoY, hitting $22M in 3Q17

Research Synopsis:

The IHS Markit Data Center Compute Intelligence Service provides quarterly worldwide and regional market size, vendor market share, forecasts through 2021, analysis and trends for (1) data center servers by form factor[rack, blade, open compute and tower], server class[entry-level, enterprise, large-scale enterprise, large-scale compute and high performance compute], and market segment[Enterprise, Telco and Cloud Service Provider], and (2) Ethernet network adapters by CPU offload[Basic, Offload and Programmable NIC], port speed [1/10/25/40/50/100GE], form factor [stand-up, piggyback and open compite], usage case [storage and server] and market segment. Vendors tracked include Dell, HPE, Lenovo, Cisco, Huawei, Inspur, IBM, Supermicro, Cray, Intel, Broadcom, Mellanox, Cavium, and others.

……………………………………………………………………………….

In a separate IHS Markit report:

Hyperscale data center owners are driving growth of renewable energy in data centers

By Maggie Shillington, analyst, cloud and data centers, IHS Markit

Highlights

- Between 2 percent and 3 percent of developed countries’ electricity consumption is currently attributed to data centers. For most data centers, the largest operational cost is the electricity used for cooling.

- Onsite generation is the ideal way to implement renewable energy in data centers. The two most popular renewable energy methods are solar and wind power, due to their high-energy production and relative ease of implementation.

- Offsite renewable energy sources — primarily utility companies and renewable energy suppliers — are typically the easiest way for data centers to obtain renewable energy. Offsite generation removes the large upfront capital expenses to produce onsite renewable energy and the geographical limitations of renewable energy production methods.

- Although small data centers have a distinct advantage in using onsite options, owners of hyperscale data centers (i.e., Apple, Google, Microsoft, Amazon and Facebook) are driving the growth of renewable energy for data centers.

C Spire – Entergy Mississippi Partnership to Build Fiber Network along 5 routes

U.S. service provider C Spire today announced a partnership with electric utility Entergy Mississippi which aims to bring more than 300 miles of fiber to remote areas of Mississippi. C Spire will build and own the network, with Entergy contributing construction costs, according to C Spire Vice President of Government Relations Ben Moncrief in an interview with Telecompetitor.

Entergy will lease capacity on the network from C Spire to support its smart grid initiatives, he said. C Spire eventually expects to extend the middle-mile network to end user locations to support retail services, he added, although he emphasized that any such plans are not part of today’s news.

Details about the C Spire – Entergy partnership can be found in this press release. Clearly there were a lot of synergies for these companies to work together.

“This opens the door to offering service to residences and industrial parks,” Moncrief said. “But today is just about getting the (fiber optic) backbone in place.”

When Entergy Mississippi sought the Mississippi Public Service Commission’s approval to build a network to support its smart grid plans, one of the commissioners asked whether that network could also be “at least a foundation for broadband services,” Moncrief explained.

That idea led Entergy to a meeting with C Spire at which representatives of both companies had an “aha moment,” Moncrief recalled.

C Spire initially was a wireless carrier, as well as a provider of wireline business services, but in recent years has been quite aggressive in deploying fiber-to-the-home (FTTH) and other broadband network infrastructure in numerous rural markets in Mississippi. Meanwhile, Moncrief said, “Here’s an electric utility that for security reasons is keeping infrastructure away from population centers.”

The network will be installed with a minimum of 144-count fiber, “in some places more,” Moncrief noted. Each company will have its own fiber. The areas that the network will run through are “very rural” and might have been too costly for C Spire to build out to without the Entergy investment, Moncrief added.

C Spire also will gain connectivity from the rural areas to population centers, Moncrief said.

C Spire Entergy Fiber Network Map

……………………………………………………………………………………………………………………………….

The construction project will involve placing fiber optic cable along five separate routes as follows:

- Delta: a 92-mile route through Sunflower, Humphreys, Madison and Hinds counties and near the cities of Indianola, Inverness, Isola, Belzoni, Silver City, Yazoo City, Bentonia, Flora and Jackson.

- North: a 51-mile stretch in Attala, Leake and Madison counties, including near the towns of McAdams, Kosciusko and Canton.

- Central: a 33-mile route through Madison, Rankin and Scott counties and near the towns of Canton, Sand Hill and Morton.

- South: a 77-mile route passing through Simpson, Jefferson Davis, Lawrence and Walthall counties and near the towns of Magee, Prentiss, Silver Creek, Monticello and Tylertown.

- Southwest: a 49-mile stretch in Franklin and Adams counties that’s near the communities of Bude, Meadville, Roxie, Natchez and Eddiceton.

“We’re excited about partnering with C Spire to modernize our electrical grid and expand rural broadband access in some hard-to-reach areas across the state,” said Haley Fisackerly, president and CEO of Entergy Mississippi. “We have about 30,000 customers within five miles of the proposed routes who could potentially have access to broadband service when the project is complete. In addition, all of our customers will benefit from the enhancements to our communication systems that connect our facilities, substations, offices and radio sites.” The company provides electric service to an estimated 445,000 customers in 45 counties across the state.

“A robust broadband infrastructure is critical to the success of our efforts to move Mississippi forward by growing the economy, fostering innovation, creating job opportunities and improving the quality of life for all our residents,” said Hu Meena, CEO of C Spire, a Mississippi-based diversified telecommunications and technology services company.

Verizon to deploy NG-PON2 in Tampa, FL using Calix network equipment

Verizon will initiate its NG-PON2 deployments in Tampa, FL, with Calix network equipment. The telco is expected to use the technology for higher-speed enterprise broadband, small-cell and fixed wireless backhaul. “We’re looking at this platform to cover residential, business and wireless carriers,” said Verizon’s Vincent O’Byrne.

Verizon and other carriers are expected to use NG-PON2 to support higher-speed business services, as well as backhaul for small cell networks. In Verizon’s case, the technology also will be used to provide backhaul for fixed wireless, according to O’Byrne.

“As we go forward, we’re looking at this platform to cover residential, business and wireless carriers,” said O’Byrne. NG-PON2 will be the access portion of Verizon’s vision for the “intelligent edge” network, which also will comprise unified transport and core network changes, he said. “NG-PON2 is the part that hits customers,” he added.

Although the Tampa, FL NG-PON2 deployment will use equipment from Calix, Verizon continues to test a second supplier in the lab, O’Byrne said.

Verizon NG-PON2

Vincent O’Byrne

The NG-PON2 equipment that service providers initially will deploy will support four wavelengths, but providers can turn up just a single wavelength to start or can add an additional four wavelengths in the future, O’Byrne said.

Each wavelength can support 10 Gbps in each direction, supporting speeds of up to 8.5 Gbps for customer traffic. NG-PON2 standards specify a bonding option that would enable a service provider to combine multiple wavelengths together to support a single higher-speed connection, he explained.

Verizon has been testing NG-PON2 in the laboratory for several years. The Tampa customer trials, which will run for about three months, will make sure the carrier has the IT systems in place to support the offering, O’Byrne noted. A key function that will be examined is the ability to move services between wavelengths — a capability that will provide added protection from the consumer perspective and will enable Verizon to load balance. O’Byrne noted that during light traffic periods, Verizon might reduce the amount of power used by shifting customers to a single wavelength and turning off some line cards.

“You would have to be within Verizon to see the amount of positivity that is there that is similar to when we started to launch FiOS,” said O’Byrne, in an interview with Light Reading.

“We have a lot of big initiatives. These are exciting times. We do see ourselves on a positive cusp or tide of deploying new technologies and making a lot of changes to the network.” Vincent O’Byrne in an earlier video interview with Broadband World News. Vincent O’Byrne in an earlier video interview with Broadband World News. Those changes fit into what Verizon calls its Intelligent Network Edge strategy, designed to simplify and reduce costs across its network by eliminating the need for three separate network infrastructures and also speed its ability to deliver higher-speed services and bring fiber backhaul to the growing set of antennas that 5G deployment will require. Verizon had named two vendors for NG-PON 2 — ADTRAN Inc. and Calix.

It’s now moving forward initially with Calix because that vendor “was, from a timeline perspective, ahead and ready to go out and we have a need to get this deployment out there,” O’Byrne said.

Calix CEO and President Carl Russo shares O’Byrne’s excitement about what this move might mean for the bigger market. He credits Verizon with being willing and able to move quickly in adopting not just a new PON technology but a new overall approach to access networks. “When someone like Verizon, who is known for technical leadership and engineering orientation starts to deploy, it’s kind of like firing off the starting gun to the market saying, ‘Okay guys, this technology is go,’ ” he says in an interview.

“That doesn’t mean everybody rushes to it, it means you now have that legitimacy, that this is a production choice [operators] can make, as opposed to, ‘I’m not quite sure it’s ready.’ Now the market begins.”

Russo was impressed with the speed at which Verizon is working and the Agile processes it is using. “It has been an interesting partner approach because they have functioned as an Agile partner, it has been quite enjoyable,” he says. “It’s been hard, too, but they have engaged in a way that a lot of large customers find difficult to engage. There is a lot more exciting stuff coming, this market is real and it is going to get realer.” Verizon isn’t saying where it will initially deploy NG-PON 2 in Tampa because that will be a marketing decision, O’Byrne says, and will be driven by customer demand. Because NG-PON 2 can use the same physical fiber infrastructure that is already in use by GPON, Verizon will choose to deploy where customers need more than 1 Gbit/s service, he says. Because it’s newer, NG-PON 2 technology costs more than GPON, but those costs are offset by savings in many areas, as part of the transition to an intelligent edge and software-defined access.

For example, the AXOS E9-2 Intelligent Edge System combines subscriber management, aggregation and optical line terminal (OLT) functions into a single box, which offers both power and space savings and significant operational efficiencies, including greater automation, O’Byrne says. The net result is speeds up to 40 Gbit/s throughput and tunable optics for essentially the same cost. “The ability to move all three service sets into one box saves us an inordinate amount of money from processing, and just the ability to increase the speed at which we can provision systems reduces our OSS complexities that we would have,” O’Byrne says.

“That is why this overall intelligent edge network, we kind of see it as a big emphasis within the company.”

The Verizon executive says the company is continuing to work in the labs with Adtran. He calls it “standard practice” to work with two vendors, and move forward first with one and then the other. Thanks to the interoperability trial work that Verizon has already done, producing the Verizon OMCI specification — which is being incorporated into the ITU-T G.988 standard — Calix and Adtran gear will have common interfaces, he says. (See Verizon Proves NG-PON2 Interoperability). For Calix, however, this does represent market validation of its five-year journey to become a software platform company, Russo said.

“This helps people understand just how much that transformation has been completed,” he says. “AXOS being deployed at this level should make it clear what is going on with us, as a platform software company.” When Verizon was doing OSS work on FiOS we were working with the group in Tampa to make it operational. They were doing all the development there. That is consistent with your post Carol. The real question is this part of the rollout of 5G or is it a residential play. My guess is the former. Verizon was quiet open about the services to be offered when FiOS rolled out.

According to a Verizon spokesman, the company still has facilities in Tampa, and that is where they are doing the production testing of the systems and the various technology elements involved in the Intelligent Edge Network, including NGPON2. As Vincent O’Byrne says in the story, the company hasn’t publicly announced what services it will be offering as that is a marketing choice. The spokesman says that “over time we expect to support residential, business and wireless use cases. Once the testing is completed, I expect we’d have more to announce in terms of details.”

While the backhaul connection to the central office for GPON is 2.5 Gbps, that number rises to as much as 80 Gbps for NG-PON2, explained Calix CEO Carl Russo in a separate interview. But “that’s actually not the big thing” about NG-PON2, according to Russo. The big thing, he said, is “all the wavelengths and what they can do for you.”

The way Calix thinks about NG-PON2, he said, is that “it delivers the physical layer we’ve been in pursuit of for 10 years.”

The “efficiency of a shared PON,” he said, includes “the ability of a wavelength to run in a non-shared fashion – you can basically have a point-to-point connection.”

NG-PON2, he said, could be thought of as “the physical layer for unified access.”

Carl Russo

Calix had to make some modifications to its existing NG-PON2 equipment to meet Verizon’s needs for its converged access network, Russo noted. A key requirement was the ability to switch wavelengths on the fly in less than 25 milliseconds.

“That is a very challenging target to hit,” Russo said.

According to Russo, Verizon also will use Calix’s AXOS software-based management system to support “always on” operation. Modifications can be made to the network without taking the network out of service, Russo said.

Russo expects to see carriers deploying both GPON and NG-PON2 for years to come. The technology that may get squeezed is XGS-PON – an alternative approach to boosting FTTP speeds and capacity that adds only a single wavelength to existing PON infrastructure and which some people viewed as an intermediate technology until NG-PON2 was available, he said.

Nokia, Optus & Qualcomm Expect Rollouts of 5G Commercial Networks in 2019-2020

Nokia President and CEO Rajeev Suri expects 5G network deployments to be a major growth driver for the network equipment and services company. In prepared remarks he said:

“For 2019 and 2020, we expect market conditions to improve markedly, driven by full-scale rollouts of 5G networks. As those roll-outs occur, Nokia is remarkably well-positioned. Unlike previous generations of technology, 5G requires a coordinated, holistic approach across all network elements, far beyond radio. That requirement plays to the strength of our end-to-end portfolio and our 5G Future X architecture.”

Investments necessary to take advantage of this growth opportunity will hit the bottom line in 2018, but this is expected to be temporary:

“As a result of the acceleration of investment in 5G due to the opportunity provided by the accelerated time frame of 5G deployments, Nokia’s operating margin will come under some pressure in 2018. That investment, combined with continued strong execution of our strategy to expand to new vertical segments, build a stand-alone software business, and maximize the value of our licensing business, will allow us to target improved results in 2020. Therefore, the Board is committed to propose a growing dividend, including for 2018.”

“We’re getting a good sense of what 5G is going to be like. It is clear the demand is there on the basis of capacity increase,” as well as from the B2B environment where industrial, utility and transportation companies are asking operators to give them 5G capability from a capacity and latency perspective.

Of course, we look at it differently from another peer or some other peers because we have an end-to-end portfolio. This really is a reinvention of the network as we know it,” he said. “Our operators, if they go end-to-end with us, will get the benefit of a lower TCO, so total cost of ownership, [and] a higher throughput at the network level, not just at the radio level but at the network level.”

Nokia this week announced its new ReefShark chipsets, which incorporate Nokia Bell Labs artificial intelligence (AI) technology as well as Nokia’s capabilities in antenna development for mobile devices and base stations. Nokia says the ReefShark chipsets significantly improve the performance of antennas, resulting in halving the size of massive MIMO antennas and reducing power consumption in baseband units by 64% compared to today’s units.

Suri also talked about Nokia’s expertise in network slicing, which he said would be a key component of 5G.

“There will be thousands and thousands” of network slicing, perhaps millions in the future, he said, and “our operators will be able to tap into the demand” of an SLA-based business where they can give slices to a group of clinics or hospitals, for example, including regionally and globally. “We would be able to slice the network at the network level,” he said, adding that somebody else who doesn’t have an end-to-end portfolio would only be able to do that at the core network of the radio, and that’s not good enough.

While Nokia’s results for 2018 are unlikely to impress, the company sees brighter skies ahead in 2019 and 2020 based on demand for 5G network technology. Nokia expects a dramatic improvement in profitability in 2020.

We remain skeptical, because we believe the pace of 5G rollouts won’t accelerate until the ITU-R WP5D IMT2020 standards are completed at year end 2020. 3GPP’s New Radio (NR) is one of several RIT proposals to be submitted for consideration later this year and in early 2019.

………………………………………………………………………………………………………………………

Separately, Australian teleco Optus said will begin the rollout of its “5G” network early next year for ‘key metro areas’, as recent tests with network partner Huawei have attained 2Gbps speeds using commercial customer devices.

Optus MD of Networks Dennis Wong explained that Optus can now “increase momentum” on 5G due to 3GPP approval of “5G” New Radio specs last December: “Throughout 2018, Optus is going to lead the Australian market in the development and deployment of pre-5G and 5G technologies,” he said.

……………………………………………………………………………………………………………………………..

Finally, Qualcomm and a handful of Chinese smartphone manufacturers are working together on a new initiative aimed at introducing 5G endpoint devices as early as next year. The initiative will support China’s smartphone industry and seeks to introduce commercial devices that comply with 3GPP New Radio specifications as soon as 2019, Qulacomm said.

The companies will also explore artificial intelligence and IoT technologies under the 5G partnership, Qualcomm added.

“Qualcomm Technologies has close relationships within China’s mobile and semiconductor ecosystem, and we’ll continue to work with this ecosystem to drive innovation as we move from the 3G/4G era to the 5G era,” said Qualcomm president Cristiano Amon.

A recent survey conducted by Qualcomm shows that Chinese mobile users are showing unprecedented interest in 5G, with 60% of Chinese consumers are likely to purchase 5G smartphones when available.

Qualcomm announced its “5G Pioneer” initiative at the 2018 Qualcomm China Tech Day in Beijing last month. At that time, Qualcomm executives were joined by representatives from six Chinese smartphone makers – Lenovo, Oppo, vivo, Xiaomi, ZTE and Wingtech.

Through the “5G Pioneer” Initiative, in addition to deep expertise and leadership in semiconductor solutions, Qualcomm Technologies anticipates being able to provide Chinese manufacturers with the platform they need to develop premium tier and global 5G commercial devices. Qualcomm Technologies, together with leading Chinese manufacturers, is not only exploring new mobile applications and experiences enabled by 5G, but also focusing on other transformative technologies such as Artificial Intelligence (AI) and the Internet of Things (IoT) to continue to drive technological evolution and industry transformation worldwide.

“5G will bring massive new opportunities to the mobile industry, and we are excited to work with these manufacturers on this 5G Pioneer Initiative,” said Cristiano Amon, president, Qualcomm Incorporated. “Qualcomm Technologies has close relationships within China’s mobile and semiconductor ecosystem, and we’ll continue to work with this ecosystem to drive innovation as we move from the 3G/4G era to the 5G era.”

………………………………………………………………………………………………………………………………………………………..

China was picked to lead global 5G adoption by 2023. According to CCS Insight’s 5G forecast, 5G connections will reach 1 billion worldwide in mid-2023, and China will account for more than half of all 5G subscribers as early as 2022. Meanwhile, China has many leading 3G/4G smartphone makers. According to Counterpoint Research, in 2017, seven of the top ten global 3G/4G smartphone manufacturers were from China.

…………………………………………………………………………………………………………………………………………………………….

In a separate announcement, Qualcomm signed a MoU with Lenovo, OPPO, vivo and Xiaomi for multi-year purchases of RF front end silicon worth $2 billion.

Qualcomm said its RF front end modules will support China’s current mobile ecosystem and also address the rapidly expanding complexity and challenges of (true) 4G-LTE Advanced and “5G” networks.

Verizon, KT and Samsung team up for SECRET “5G” Super Bowl Demo

Verizon, KT and Samsung have teamed up such that the CEO’s of the two telcos could have a secret video call with each other during the Superbowl.

- Verizon set up a temporary (and secret) 5G network at Super Bowl LII.

- Using the 5G network, guests were able to watch high-resolution streams of instant replays.

- Meanwhile, in New York City, engineers were able to view a stereoscopic 180-degree video of the game in nearly real time.

The video call was yet another pre standard “5G” demonstration taking place between Minneapolis, MN and Seoul, Korea. The trio have also stated, quite illogically, that such a grounded use case is an indication of how close the reality of 5G actually is.

“The fact that 5G is no longer a dream owes its debt to the collaborations we have carried out with operators like Verizon and vendors like Samsung,” said Hong-beom Jeon, Head of Infra laboratory at KT. “Our efforts have enabled some of the most demanding tasks to come to fruition.”

“Seeing Samsung’s 5G end-to-end solutions in action, including a working prototype 5G tablet, underscores how important our collaborative relationship has been in helping accelerate the availability of commercial 5G mobility for customers,” said Ed Chan, Senior Vice President and Chief Technology Architect, Verizon.

“As we say at Verizon, ‘we don’t wait for the future, we build it.’ We are glad to be working with like-minded partners to build the 5G future globally.”

Looking at the nitty gritty side, Samsung supplied the network Infrastructure composed of 28GHz 5G access units, 5G home routers(CPEs), virtualized RAN, virtualized core network and prototype 5G devices. The trio claim the exercise successfully demonstrated how to bring one of the smallest 5G radio base stations and 5G home routers (CPEs) to market.

As well as allowing the two telco CEOs to whisper sweet nothings across thousands of miles with no threat of buffering or losing sync between video and audio, Samsung also took the opportunity to showcase a new 5G tablet. The Samsung tablet is capable of running on multi-gigabit per second speeds via 5G networks, as well as the latest 4G LTE network speeds.

Sanyogita Shamsunder, the Executive Director of 5G Ecosystems and Innovation at Verizon, said, “This latest demonstration at Super Bowl LII and in New York City is another example of how we’re pushing 5G to exploit never-before-imagined uses cases and applications.”

This is not the first time Verizon has used football to demonstrate the power of 5G. A few days earlier, two football players in virtual reality headsets were able to pass a football and complete plays without ever physically looking at each other. The 5G network their helmets were connected to was so fast that the milliseconds of latency didn’t affect their ability to interact in nearly real time.

There’s currently an arms race going on between the four major telecommunications companies in the United States, for which will be the first to roll out a commercial 5G network. What does this show of 5G power say about Big Red’s stakes in the race?

References:

http://telecoms.com/487589/verizon-kt-and-samsung-team-up-for-yet-another-5g-proclamation/

https://www.androidauthority.com/verizon-secretly-5g-test-super-bowl-lii-835383/

Sprint to increase CAPEX to focus on mobile 5G deployment in 1H-2019

Sprint will increase its network capital expenditure by at least $1 billion for the coming year as promised on Friday morning’s earnings call. The #4 U.S. wireless carrier plans to deliver mobile 5G in the first half of 2019.

–>That’s 1 year before the IMT 2020 standards will be completed!

Sprint Corp talked about its mobile 5G plans: “We’re working with Qualcomm [and others] in order to deliver the first truly mobile 5G network in the US in the first half of 2019,” CEO Marcello Claure said on the call.

Mr Claure said that Sprint will be able to deploy mobile 5G nationwide on 2.5GHz band in 100MHz channels. “We have the spectrum to lead on 5G, and basically lead in a different way,” he noted. Claure said later in the question and answer session that Sprint had a commitment from a “leading Korean” device vendor that it will have a 5G device ready within its 2019 timeframe.

This implies an increase in capital expenditure spending for Sprint’s network for fiscal 2018, new CFO Michel Combes said. Sprint’s total capex spending for fiscal 2017 will be in the $3.5-$4 range. Capex will hit $5-$6 billion in fiscal 2018, which starts in April 2018.

Sprint will spend to increase the number macro cell sites by 20%, and support its 2.5GHz, 1900MHz, and 850MHz bands on nearly all of its existing macro sites. Currently, around half of its macro sites have tri-band support.

The CEO added that Sprint plans to deploy more than 40,000 outdoor small cells, and “more than 1 million Magic Boxes,” the wireless small cells that it uses to improve in-home coverage.

In the field, Sprint expects to update sites with multiple-antenna array hardware, or “Massive MIMO” in 2018. “Massive MIMO will serve as Sprint’s bridge to 5G,” Claure said. (See Sprint Says No to mmWave, Yes to Mobile 5G.)

This is because the MIMO hardware can be updated to 5G NR standard over-the-air, the CEO said.

Our strategy is predicated on creating on amazing customer-experience, offering customers the best products and services, while delivering superior financial results. First, we recognize that to be a truly great company we have to have a great product, which for us is our network. While our network is much improved, we believe our next-gen network will truly differentiate Sprint over the next couple of years, due to our strong spectrum assets that enables Sprint to be the leader in the true mobile 5G.

This is the biggest network capital program in many years. And I will share more details of our network strategy in a few moments. I cannot wait to, once and for all, be able to sell the product that is best in the industry with competitive coverage, the fastest speed and the highest capacity.

Second, we will continue to deliver the most compelling value proposition to our customers across all of our segments. We will continue to play from a position of strength by leveraging our spectrum holdings and continue to lead with the best-only net offering in the market. Data usage strength are projected to grow exponentially, especially with 5G.

By having the most spectrum, combined with new technology that massively increases our capacity, we’re certain that we’ll be best position for to support unlimited data in the future.

Third, we will continue to drive a smart distribution strategy, with over 1,000 new stores open year-to-date across our Sprint and Boost brand, and several hundred several hundred throughout next year. We have designed a dynamic distribution model that allows to continuously optimize the right balance of physical and distribution – and digital distribution.

Sprint will also leverage its partnerships with Altice and Cox Communications Inc. to expand its backhaul capabilities for LTE-Advanced and 5G. Sprint CTO John Saw chimed in briefly on the call to say that some of the capex spend could be on “dark fiber” for backhaul needs.

Against this backdrop, Claure said there would be continuing job cuts at Sprint, including at the executive level, aiming for “a leaner and more agile company across our non-customer-facing workforce.” Sprint has cut thousands of jobs during the past couple of years.

True to his reputation as a “turnaround specialist,” new CFO Michel Combes said he is looking at more ways to “decrease cost structures” at Sprint. He promised to reveal more details in the March quarter. (See Sprint Appoints Ex-AlcaLu Boss Combes as CFO.)

For the quarter, Sprint reported revenue of $8.24 billion, down from $8.55 billion a year ago. Net income for the quarter was $7.16 billion (or $1.76 per share) thanks almost entirely to tax reform gains of about $7.1 billion, compared with a net loss of $479 million a year ago.

References:

Deutsche Telekom to deploy 1 Gb/sec fiber optic lines to 7,600 enterprises

Deutsche Telekom says it will begin the second phase of its fiber-optic network for business parks, which will provide internet connections at speeds of up to 1 Gb/sec to as many as 7,600 enterprises.

Deutsche Telekom’s latest fiber project will include laying almost 500 km of fiber-optic cables and connecting company locations directly to the fiber-optic network in 33 German towns and cities. The company says it is using sustainable, cost-effective micro trenching technology during construction to avoid inconveniencing town and city residents.

The German towns and cities whose business parks are being upgraded include: Amberg, Bielefeld, Bochum, Bonn, Braunschweig, Bremen, Cologne, Dippoldiswalde, Dresden, Düsseldorf, Flörsheim, Frankfurt, Frechen, Großbeeren, Hamburg, Hermsdorf, Hildburghausen, Hürth, Kelkheim, Kriftel, Langen, Leipzig, Lindlar, Lübeck, Mannheim, Markkleeberg, Nienburg, Oldenburg, Pinneberg, Planegg, Potsdam, Sandersdorf-Brehna and Seevetal.

Deutsche Telekom will connect companies at no additional charge should they make the switch to its business parks’ fiber-optic network “early on.” (timing unspecified?)

Fiber-optic lines for about 7,600 enterprises: In 33 business parks the companies that decide “early on” to switch to DT’s fiber-optic network will be connected at no additional charge.

……………………………………………………………………………………………………………..

The range of fiber-optic rate plans runs from asymmetric 100 Mbps business customer lines through to symmetric 1 Gbps lines. The line growth follows previous expansion in 2016 and 2017, during which Deutsche Telekom invested nearly €5 billion annually on its network (see “Deutsche Telekom touts fiber-optic network investments”).

Deutsche Telekom currently operates a fiber-optic network of 455,000 km, with business parks a focus of its fiber to the home (FTTH) efforts, alongside subsidized expansion activities and partnerships with competitors (see “Deutsche Telekom pilots small town FTTH”).

“Business parks are at the heart of our fiber-optic build-out strategy,” said Hagen Rickmann, Telekom Deutschland director for business customers. “We are thinking nationwide, urban and rural, north, south, east and west. The decisive factor for us is customer demand, and we are pleased to be able to offer our business customers fiber-optic lines in a further 33 communities across the country.”

“We will execute this project quickly and supply the businesses with ultramodern technology, offering them the best infrastructure for the digital transformation. The build-out continues, and our interim goal is to connect 3,000 business parks across Germany to our fiber-optic network (FTTH).”

Deutsche Telekom invests around five billion euros every year and operates Europe’s largest fiber-optic network.

…………………………………………………………………………………………………………………

More information at:

Hotline: + 49 (0)800 330 1362 77 (toll-free)

E-mail: [email protected]

www.telekom.de/vollglas

References:

https://www.youtube.com/watch?v=N4r1Wb0O2Sk&feature=youtu.be

Telcos need to do much more to gain significant cloud market share

Synergy Research Group said that the global cloud computing and storage market grew 24% annually for the period ending September 2017. The market research firm said that of the six cloud services and infrastructure market segments, operator and vendor revenues, IaaS (Infrastructure as a Service) and PaaS (Platform as a Service) had the highest growth rate at 47%, followed by enterprise SaaS (Software as a Service) at 31%, and hosted private cloud infrastructure services at 30%.

Data suggested that 2017 widened the gap between cloud services spending vs. hardware and software used to build public and private clouds. Synergy noted that 2016 was the year in which spending on cloud services overtook spending on cloud infrastructure.

John Dinsdale, a chief analyst and research director at Synergy Research Group, noted that in 2015 cloud became mainstream and by 2016 it started to dominate many IT market segments.

“Major barriers to cloud adoption are now almost a thing of the past, with previously perceived weaknesses such as security now often seen as strengths. Cloud technologies are now generating massive revenues for cloud service providers and technology vendors and we forecast that current market growth rates will decline only slowly over the next five years,” he concluded.

The researcher noted eight cloud services vendors were among the 2017 market segment leaders.

Figure 1: Movers and shakers in 2017 cloud market

…………………………………………………………………………………………………………….

Over the period Q4 2016 to Q3 2017, total spend on hardware and software to build cloud infrastructure approached $80 billion, split evenly between public and private clouds, though spend on public cloud is growing more rapidly.

Infrastructure investments by cloud service providers helped them to generate over $100 billion in revenues from cloud infrastructure services (IaaS, PaaS, hosted private cloud services) and enterprise SaaS – in addition to which that cloud provider infrastructure supports internet services such as search, social networking, email, e-commerce and gaming.

Meanwhile UCaaS (Unified Communications as a Service), while in many aspects is a different market, is also growing strongly and is driving some radical changes in business communications.

Carriers, for their part, are not standing still. According to Gartner Group, communications service providers (CSPs) worldwide face profound challenges related to traditional telco network-based to cloud-based service delivery across several functional and technical domains.

Gartner research director Martina Kurth said “CSPs are embarking upon an evolutionary path that unifies cloud instances of SDN/NFV, OSS/BSS (e.g. Paas/SaaS/Iaas) and enterprise IT. Coupled with microservices, container based service design principles and cloud integration services, CSPs endeavor to create synergies between their various cloud domains and drive flexibility and agility across their cloud deployments.”

Gartner predicts that vendors which are well positioned in the end-to-end Telco Cloud stack market, are also likely to take market share in corresponding future network and/or IT technology markets such as digital technology platforms and ecosystems, Data/AI, IoT and 5G.

Gartner Group says that a fully integrated, interoperable, cloud and virtualied telco protocol stack will pave the evolutionary technology adoption path from SDN/NFV to network slicing to 5G and IoT in the future. But no time frame was given for that to be realized.

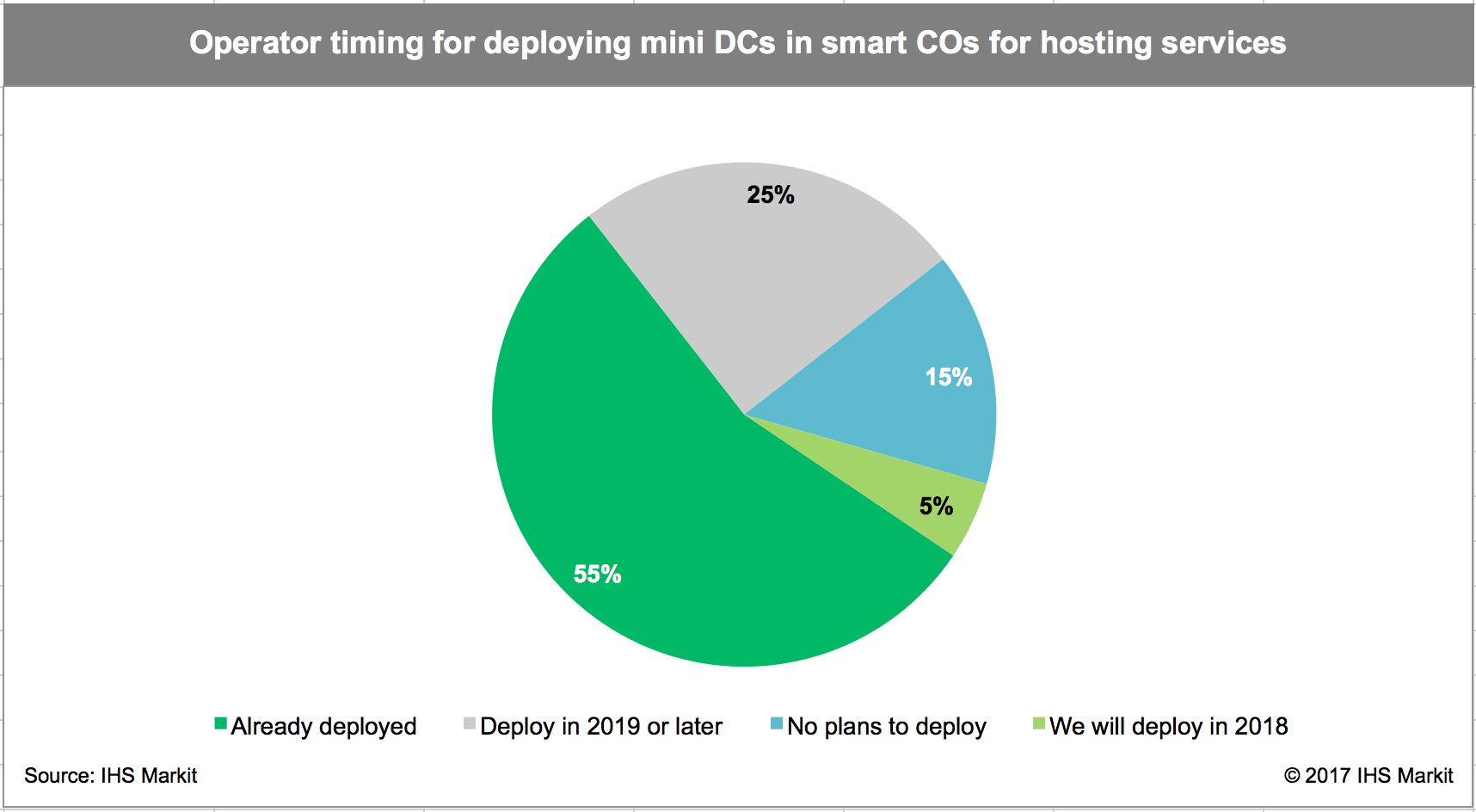

IHS Operator Survey: Smart Central Offices in 85% of Service Provider Networks in 2018

By Michael Howard, executive director, research and analysis, carrier networks, IHS Markit, and Heidi Adams, senior research director, IP and optical networks, IHS Markit

Highlights:

- In 2018, 85% of operator respondents to an IHS-Markit survey plan to create, or will have already deployed, smart central offices — that is, installing servers, storage and switching to create mini data centers in selected central offices. These mini data centers are used to offer cloud services, and as the network functions virtualization (NFV) infrastructure on which to run virtualized network functions (VNFs) such as vRouter, firewall, CG-NAT and IP/MPLS VPNs.

- More than half of operators (55%) surveyed plan to move each of 10 different router functions from physical edge routers to VNFs running on commercial servers in mini data centers in smart central offices, including customer edge (CE) router, route reflector (RR) and others.

- Seven out of 10 respondents plan to deploy central office rearchitected as a data center (CORD) in smart central offices.

- Operators expect 44% of their central offices will have mini data centers (or smart central offices) by 2023, and deploy CORD (Central Office Re-architected as a Data center) in half of those central offices.

IHS-Markit Analysis:

SDN and NFV are spurring fundamental changes in network architecture, network operations and how carriers are organized, which is illustrated by the purchasing decisions of operators worldwide. Nearly every operator around the world is undertaking major efforts.

More importantly, the move to SDN and NFV is changing the way operators make equipment purchase decisions, placing a greater focus on software. Although hardware will always be required, its functions will be refined, and software will drive services and operational agility.

A basic architectural change in motion is the deployment of new functions in large central offices that are closer to end customers. These also serve as locations for distributed broadband network gateways (BNGs), content delivery networks (CDNs), mini data centers and other new functions. Mini data centers (i.e., servers and storage) are used to deliver cloud services within a metropolitan area and house applications including augmented and virtual reality and gaming, to give users better response time as well as provide a place for NFV and VNFs, including vRouters, which run on servers. These central offices with mini data centers are known as “cloud central offices” or “smart central offices.”

Cloud services for business, and internet usage in general, have caused carrier network traffic patterns to change dramatically in and out of data centers. This is true not only for the hyperscale data centers of Google, Apple, Facebook, Amazon, Microsoft, Baidu, Alibaba and Tencent, but also for their smaller metro and regional megascale data centers, and large enterprises, as well as smaller data centers used by enterprises and government.

In a large metropolitan area, there might be 10 or more smart central offices aggregating traffic from smaller end offices. Based on our discussions with operators around the world, a common long-range plan is to identify 10 percent to 25 percent of central offices as smart central office locations — all candidates for CORD. The smart central office is the new location of the IP edge, which is creating a need for a new class of optical transport equipment and a new class of routers designed for data center interconnect (DCI) applications.

Routing, NFV and Packet-Optical Survey Synopsis

The 30-page 2017 IHS Markit routing, NFV and packet-optical strategies survey is based on interviews with router/CES purchase decision-makers at 20 global service providers that control a third of worldwide telecom capex and 27 percent of revenue. The survey covers hot and emerging topics in the carrier Ethernet, routing and switching space, with a focus on the IP edge. It looks at deployment plans, strategies and locations, router bypass, 100GE port mix, price per port and more.

…………………………………………………………………………………………………………………………………………

Notes & Clarifications:

- Smart central offices are simply central offices containing mini data centers that have servers, storage, and switching. Mini data centers can offer cloud services and typically include NFV infrastructure that supports virtualized network functions (VNFs) including vRouter, firewalls, carrier grade network address translation (CG-NAT), and IP/MPLS VPNs.

- IHS concluded that the reason more operators are leaning this direction is that deploying these functions in central offices brings them close to the end-user. This is part of the greater push by operators and service providers to focus on software to drive services, while refining hardware functions.

- If network operators re-architect their networks by distributing the core network, it would be closer to the end user. Virtualization allows operators to quickly deploy a core anywhere and to scale it at will. Edge computing could be deployed closer to the user without breaking the network topology. This is a major advantage that the telcos have over the cloud players – but they have not been able to capitalize on it. By pushing the core closer to the edge, and through virtualization of the network, operators could capitalize on this advantage.

- As operators push away from hardware into software, the smart central office is a new IP edge, and thus requires a class of routers for data center interconnect (DCI) applications and optical transport equipment.