IHS-Infonetics: NFV Market to Grow More than 500% Through 2019; Alan Disagrees!

IHS-Infonetics released excerpts from its IHS Infonetics NFV Hardware, Software, and Services report, which forecasts the global network functions virtualization (NFV) hardware, software and services market to reach $11.6 billion in 2019, up from $2.3 billion in 2015.

NFV MARKET HIGHLIGHTS:

- Service providers are still early in the long-term, 10- to 15-year transformation to virtualized networks

- Revenue from outsourced services for NFV projects is projected to grow at a 71% compound annual growth rate (CAGR) from 2014 to 2019

- Revenue from software-only video content delivery network (CDN) functions for managing and distributing data is forecast by IHS to grow 30-fold from 2015 to 2019

Analyst Quote:

“NFV represents operators’ shift from a hardware focus to software focus, and our forecasts show this. We believe NFV software will comprise over 80 percent of the $11.6 billion total NFV revenue in 2019,” said Michael Howard, senior research director for carrier networks at IHS. “The software is always a much larger investment than the server, storage and switch hardware, representing about $4 of every $5 spent on NFV,” Howard said.

NFV REPORT SYNOPSIS:

The 2015 IHS Infonetics NFV Hardware, Software, and Services market research report tracks outsourced services for network functions virtualization (NFV) projects as well as service provider NFV hardware, including NFV infrastructure (NFVI) servers, storage and switches; and NFV software split out by service management and orchestration (NFV MANO) software and virtual network function (VNF) software, including virtual routers (vRouters) and the software-only functions of mobile core and EPC, IMS, PCRF and DPI, security, video content delivery networks (CDN), and other VNF software. The research service provides worldwide and regional market size, forecasts through 2019, in-depth analysis and trends.

To purchase the report, please visit:www.infonetics.com/contact.asp

NFV WEBINAR:

Watch analyst Michael Howard’s July 2015 webinar, SDN and NFV: Accelerating PoCs to Live Commercial Deployment, an event detailing how operators can validate VNFs, NFVI and network services to speed up commercial deployments. Log in to view:

http://w.on24.com/r.htm?e=1005675&s=1&k=826E5A0182C2844918E03AD1DC23AC11

Alan’s DIssenting View of NFV:

There’ve been many times in the last three or four decades where network operators were wildly enthusiastic about a new technology, which never really gained marrket traction. In the mid 1980’s, ISDN was to replace the PSTN phone system and usher in new world of data communicaitons. In the early 1990s it was SMDS (Switched Multi-Megabit Data Service) that never really saw the light of day. In the mid 1990s, ATM was going to take over the world. 10 years later, many operators including SPRINT believed that WiMAX would be the 4G technology of choice. Didn’t happen!

Now we have major telecom carriers all excited over NFV with many forecasts of huge growth of that market. We don’t think that will happen in the next five years or maybe ever. Here’s what’s missing from NFV:

- Implementable standards for exposed physical interfaces and APIs for virtual appliances1 implemented as software running on a generic/commodity compute server.

- Procedures and protocols for virtual appliances to communicate with physical box (legacy, non-virtual) appliances already deployed in carrier networks (otherwise known as backward compatibility with the installed base). An ETSI NFV Use Cases document states in section 7.4. Coexistance of Virtualized and Non-Virtualized Network Functions: “The communications with virtual network functions shall be based on standardized interfaces.” Yet those interfaces haven’t been standardized yet.

- New security methods and procedures to isolate and quarantine compromised virtual appliances so that all appliances running on the same compute server are not locked down.

- Hardware assists, possibly NICs for compute servers, to guarantee latency and throughput of virtual appliances running on commodity compute servers.

- Standardized Management & Orchestration (MANO) software, including “service chaining,” which will work with different virtual appliances from multiple software vendors. Standardized software interfaces (like APIs) will be required for this, perhaps as part of an open source MANO software package (from OPNFV?)

- Element Management Systems (EMSs) that are integrated into MANO. For decades, physical box network vendors provided their own proprietary EMSs which configured, managed, monitored and controlled their equipment. EMSs need to be converted to software modules within MANO or accessible to MANO via software interfaces.

- The ability of MANO or other software to manage, control, schedule appliances/services, etc from BOTH virtual appliances and physical box appliances. Note that both types of appliances will be used in telco central offices/data centers for many years.

- Procedures for testing, monitoring, OA&M, fault isolation, repair & restoration, etc are urgently needed.

- Open Source NFV software, perhaps from the OPNFV consortium. IMHO, this is the best hope for NFV being a commercial success/real market.

- There’s a lot of hype about virtualizing the LTE Evolved Packet Core (EPC) via NFV but that is nonsense because operators are not going to put in a new infrastructure after recently spending lot of money to install EPC equipment and software. Further, there are no standards for vEPC. Yet we see many blog posts/article that say the time is now for vEPC. Here’s one of many NFV -vEPC hype to Pluto blog posts:

http://www.rcrwireless.com/20150223/opinion/reader-forum-dont-wait-and-see-on-nfv-for-epc-tag1

Note 1. Examples of virtual appliances include: session border controllers, load balancers, deep packet inspection agents, firewalls, intrusion detection devices, and WAN accelerators.

Here’s an interesting quote from a Spirent white paper on NFV:

“Traditionally, the burden of validating the core functions is shouldered by the network equipment (box) vendors. Today’s NFV landscape shifts some of this burden to operators deploying NFV topologies while not absolving the need for network vendors to validate NFV software within different hardware (compute platforms, physical switching tiers) and software infrastructures (hypervisor, holistic cloud stacks public clouds, etc).”

Tom Nolle on Fixing NFV:

In a New IP blog post, Tom Nolle wrote:

“What’s needed in NFV is something like “NFVI plug-and-play,” meaning that any hardware that can be used to provide hosting or connectivity for virtual functions should be capable of being plugged into MANO and supporting deployment and management.”

Nolle goes on to elaborate on fixes for CAPEX, OPEX and business case. He concludes with this remark:

“If the ETSI NFV ISG, or Open Platform for NFV Project Inc. , or the New IP Agency, are serious about moving NFV optimally forward, I’d suggest this is the way to start.”

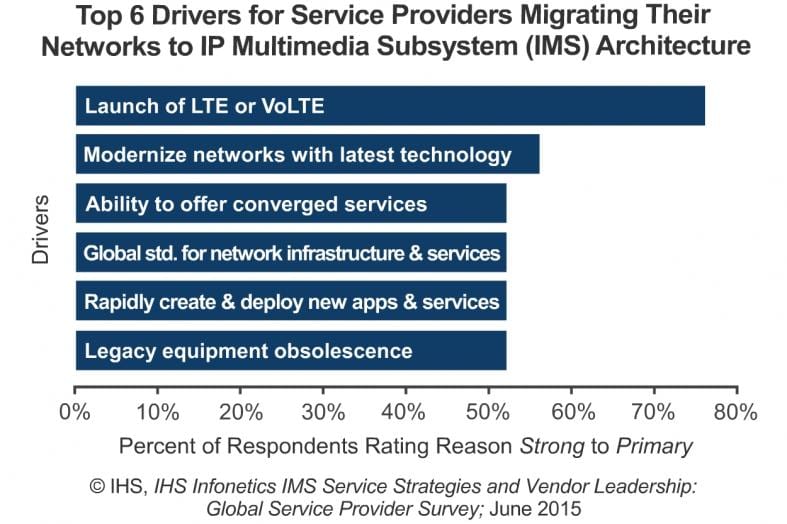

IMS (IP Multimedia Subsystem) Market Assessment & Vendor Scorecard from IHS-Infonetics

2015 IHS – Infonetics IMS (IP Multimedia Subystem) Vendor Scorecard profiles and analyzes the six top revenue producers of core IP Multimedia Subsystem network solutions: Alcatel-Lucent, Ericsson, Huawei, Mavenir, Nokia Networks and ZTE.

The only report of its kind, IHS’ IMS scorecard evaluates the leading IMS vendors on criteria using actual data and metrics, including market presence (market share, financials, solution breadth and buyer feedback on product reliability and service/support) and market momentum (market share momentum, NFV intensity, buyer feedback on vendors’ technology innovation). The report includes a Leadership Landscape Graph that classifies vendors as “Leader,” “Established” or “Challenger” based on their scores in these criteria. This approach eliminates subjectivity and ensures vendors are assessed accurately and fairly.

Quotes from Diane Myers, research director for VoIP, UC and IMS at IHS-Infonetics:

“IMS has been chosen by mobile operators as the core network for VoLTE deployments which has ramped shipments over the past 2 years as operators in the US, Japan, and South Korea ramped up for their launches. The IMS has been steadily growing for a number of years as operators worldwide, including cable MSOs, utilized it for fixed-line VoIP services but the sales volumes are significantly larger with VoLTE. The IMS market including SBCs grew 72% in CY13 as sales related to VoLTE kicked in and took volumes to a whole new level and grew 18% in CY14. We expect sales of IMS and SBCs to be $3.6B in CY15.”

IMS VENDOR SCORECARD HIGHLIGHTS:

- Ericsson’s market share, strong customer perceptions and deep relationships with mobile operators is helping it take advantage of the voice over LTE opportunity.

- Huawei has built market share through fixed-line VoIP networks using IMS and is positioned to capture the next wave of IMS spending related to VoLTE.

- Long a top vendor in the service provider VoIP market, Nokia Networks should further boost market presence via its merger with Alcatel-Lucent.

- Alcatel-Lucent is the third-largest IMS vendor, has above-average market share, scores above average for product reliability and service and support by service providers, and is at the forefront of developing IMS virtualized network functions.

- The smallest IMS vendor in the group, Mavenir is viewed by service providers as a top innovator that’s been able to steadily gain market share by focusing almost exclusively on mobile operators.

- Well established in its home country of China, ZTE has built a growing IMS business with cost-effective solutions that are appealing to operators in developing countries.

UPCOMING IHS INFONETICS SCORECARDS:

IHS is publishing 15 vendor scorecards in 2015 on markets ranging from telecom and enterprise networking equipment to carrier WiFi, network security, LTE infrastructure, cloud unified communications and more.

To purchase reports, please visit www.infonetics.com/contact.asp, or learn more about the scorecards at www.infonetics.com/research.asp?cvg=Equipmentvendorscorecards.

RELATED RESEARCH:

Service Providers Optimistic about Moving IMS Networks to NFV, Rate Vendors:

http://www.infonetics.com/pr/2015/IMS-Survey-Highlights.asp

IHS-Infonetics conducted in-depth interviews with global service providers that have IP multimedia subsystem (IMS) core equipment in their networks or will by the end of 2017 and discovered that only 8 percent are running IMS network elements in a network functions virtualization (NFV) environment today.

“Though only a small number of service providers who took part in our IMS strategies survey are currently running IMS in a virtualized environment, more are on the path by starting to utilize software running on commercial off-the-shelf hardware as a stepping stone to full NFV,” said Diane Myers, research director for VoIP, UC and IMS at IHS.

“One of the biggest drivers for NFV is the ability to scale services up and down quickly and introduce new network services more efficiently and in a timely manner, which makes IMS a good early fit for NFV,” Myers said.

Carrier Voice-over-IP Market Off to Strong Start in 2015:

http://www.infonetics.com/pr/2015/1Q15-Service-Provider-VoIP-and-IMS-Market-Highlights.asp

To purchase IHS-Infonetics report(s), please visit www.infonetics.com/contact.asp

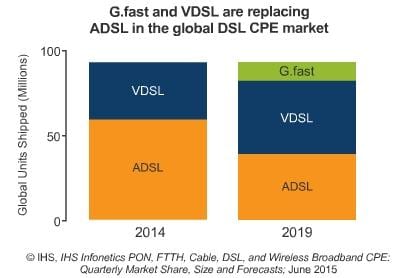

IHS-Infonetics on Broadband CPE Market: G.fast and VDSL Replacing ADSL

Worldwide broadband CPE revenue dropped to $2.8 billion in the first quarter of 2015 (1Q15), decreasing 2% sequentially, while unit shipments stayed flat at 54 million as service providers continued to expand their fixed broadband service capabilities in the highly-competitive customer premises equipment market, according to IHS-Infonetics.

“Overall, the CPE market remains strong, with revenue up 3 percent year-over-year. We expect both DOCSIS 3.1 and G.fast to help add momentum to the cable and DSL CPE market segments and FTTH to continue at its current pace, driven by deployments in China, North America and EMEA,” said Jeff Heynen, research director for broadband access and pay TV at IHS-Infonetics.

Author’s Note on G.fast:

In December 2014, the ITU-T approved the G.9701 (G.fast) specification, which is designed to provide gigabit broadband connection speeds (up to 1 Gbps) over a single twisted pair cable in an existing copper infrastructure. It allows faster deployment of services by enabling the introduction of plug-and-play remote DPUs and G.fast CPE devices self-installed by customers at home.

The Broadband Forum completed its G.fast equipment plugfest last month, as part of its ongoing program to drive widespread G.fast certification. Held at the University of New Hampshire InterOperability Laboratory’s (UNH-IOL) facilities in Durham, New Hampshire, the G.fast plugfest gave vendors developing remote Distribution Point Units (DPUs) and Customer Premises Equipment (CPEs) an opportunity to test and benchmark the interoperability of their products prior to full certification testing.

The forum said that a total of 14 chipset and equipment vendors participated in the event, illustrating the growing level of interest in G.fast technologies following the approval of the ITU-T’S G.fast standard in December 2014.

Participants included ADTRAN GmbH, Alcatel-Lucent, ARRIS, AVM GmbH, Broadcom, Calix Inc., Huawei, Ikanos, JDSU, Lantiq GmbH & Co. KG, Metanoia, Realtek Semiconductor Corporation, Sckipio Technologies and Technicolor. Sparnex Instruments and Telebyte provided additional test and measurement equipment for the event.

AT&T, BT, France Telecom/Orange, Swisscom and Deutsche Telekom are among many network operators planning to deploy G.fast to deliver broadband Internet access over copper.

BROADBAND MARKET HIGHLIGHTS:

- On a year-over-year basis, global broadband CPE unit shipments were up 9% in 1Q15 as operator investments in premium CPE continued.

- Looking at the product segments, the top performers in 1Q15 were EPON and fixed LTE, which both saw double-digit percentage increases in unit shipments.

- Regional pockets of growth include EPON ONTs and video gateways for cable operators in North America, GPON ONTs in Europe and VDSL CPE in Latin America.

- As service providers use mobile broadband to complement fixed broadband deployments, use cases for mobile broadband routers are anticipated to grow considerably, sending unit shipments to over 622,000 in 2019.

BROADBAND REPORT SYNOPSIS:

The quarterly IHS Infonetics PON, FTTH, Cable, DSL, and Wireless Broadband CPE market research report tracks DSL, cable and FTTH CPE; mobile broadband routers; and residential gateways. The research service provides worldwide and regional market size, vendor market share, forecasts through 2019, analysis and trends. Companies tracked include Alcatel-Lucent, Arris, AVM, Cisco, Comtrend, D-Link, Dasan Networks, Fiberhome, Hitron, Huawei, Mitsubishi, Netgear, OF Networks, Pace, Sagemcom, SMC Networks, Sumitomo, Telsey, Technicolor, TP-Link, Ubee Interactive, Zhone, ZTE, ZyXel, others.

To purchase the report, please visit www.infonetics.com/contact.asp

Meanwhile, DSL Reports says that AT&T’s ‘Fiber’ Expansion Possibly G.Fast DSL, Still Over-Hyped

“…the press (and Wall Street) are likely dramatically over-estimating the real impact AT&T’s plans are going to have. AT&T’s constantly-reduced fixed-line CAPEX budget makes it perfectly clear that the company’s tip priority is, and will continue to be, wireless.”

In an interesting twist, BTR says that G.FAST MAY SEE MORE NORTH AMERICAN USE IN BUILDINGS THAN OUTSIDE OF THEM.

“North American carriers increasingly see G.fast’s first role as a way to provide high-speed broadband over in-building copper as part of a fiber-to-the-building (FTTB) deployment. This growing consensus calls into question how soon – if at all – North American cable operators will see G.fast deployed to single-family homes in response to their upcoming DOCSIS 3.1 roll outs.”

SDN Standards Activities in ITU-T and other SDOs

The Joint Coordination Activity on Software-Defined Networking (JCA-SDN), was approved by ITU-T TSAG in June 2013. Mr. Takashi Egawa (NEC, Japan) was appointed as the Chairman and Ms Ying Cheng (China Unicom, China) as the vice chair of JCA-SDN, which will report its progress to TSAG.

From the ITU-T’s SDN Portal:

SDN is considered a major shift in networking technology which will give network operators the ability to establish and manage new virtualized resources and networks without deploying new hardware technologies. ICT market players see SDN and network virtualization as critical to countering the increases in network complexity, management and operational costs traditionally associated with the introduction of new services or technologies. SDN proposes to decouple the control and data planes by way of a centralized, programmable control-plane and data-plane abstraction. This abstraction will usher in greater speed and flexibility in routing instructions and the security and energy management of network equipment such as routers and switches.

Terms of Reference for the Joint Coordination Activity on Software-Defined Networking (JCA-SDN) is at:

http://www.itu.int/en/ITU-T/jca/sdn/Documents/ToR-JCA-SDN.pdf

The JCA-SDN found many SDN-related activities are ongoing in various Study Groups (SGs) of ITU-T and in other Standard Development Organizations (SDOs).

In ITU-T, items shown below are under study, listed by Study Group:

l ITU-T Study Group 13 (lead SG of SDN)

- Y.3300 (Framework of Software-Defined Networking)

- Y.3320 (Requirements for applying formal methods to software-defined networking)

- Y.3012 (Requirements of network virtualization for future networks)

- Y.3321 (Requirements and capability framework for NICE implementation making usage of software-defined networking technologies)

- Y.FNvirtarch (Functional architecture of network virtualization for future networks)

- Y.Sup-SDN-usecases (Use cases of Telecom SDN)

- Y.SDN-req (Functional requirements of software-defined networking)

- Y.SDN-arch (Functional architecture of software-defined networking)

- Y-NGNe-VCN-Reqts (Requirements of VCN (Virtualization of Control Network-entities) for NGN evolution)

From the latest draft of the ITU-T SDN Architecture spec:

“The functional architecture of SDN is based on [ITU-T Y.3300] which provides the framework of SDN. The key properties of the framework are logically centralized network control which allows for controlling and managing network resources by software, support for network virtualization, and network customization, for efficient and effective network deployments and operations.

The requirements for SDN include: separation of SDN control from the network resources, programmability of network resources; abstraction of network resources, by means of standard information and data models and support for orchestration of network resources and SDN applications.”

Here’s the Mother of all cop-out disclaimers:

“The ITU-T framework description is a high level one which enables inclusion of many present and future SDN approaches [b-ETSI NFV][b-IETF I2RS][b-IETF RFC3746][b-ONF][b-OpenDayLight] which share the same objectives to provide the programmability of network resources.”

Note that there is no mention of the network virtualization/overlay model, favored by VMWare, Nuage Networks, and many other vendors.

l ITU-T Study Group 5

They informed JCA-SDN that their deliverables for energy saving and energy efficiency topics can be considered of interest for SDN.

l ITU-T Study Group 11

- Q.3315 (Signalling requirements for flexible network service combination on Broadband Network Gateway)

- Q.SBAN (Scenarios and signaling requirements for software-defined BAN (SBAN))

- Q.Supplement-67 (Framework of signaling for SDN)

- Q.IPv6UIP (Scenarios and signaling requirements of unified intelligent programmable interface for IPv6)

l ITU-T Study Group 15

- G.asdtn (Architecture for SDN control of Transport Networks)

- G.cca (Common Control Aspects)

- G.gim (“Generic Information Model”)

l ITU-T Study Group 16

- H.Sup.OpenFlow (Protocol evaluation – OpenFlow versus H.248)

- H.VCDN-RA (Functional requirements and architecture model for virtual content delivery network)

l ITU-T Study Group 17

- X.sdnsec-1 (Security services using the software defined network)

- X.sdnsec-2 (Security requirements and reference architecture for Software-Defined Networking)

Other SDN Standards Activity:

Regarding other standards bodies outside of ITU-T, JCA-SDN learned that there are SDN standardization activities in: ATIS, Broadband Forum (BBF), China Communications Standards Association (CCSA), Internet Engineering Task Force (IETF), Internet Research Task Force (IRTF), and Open Networking Foundation (ONF).

—>Why is ONF listed last?

SDN-related activities can also be found in 3GPP, ETSI ISG Network Function Virtualization (NFV) and IEEE P1903 (Next Generation Service Overlay Network (NGSON)).

JCA-SDN also learned that Open Source Software (OSS) projects are becoming important players in standardization ecosystem by providing reference implementations, providing feedbacks to specifications, demonstrate proof of concept, and others. In SDN arena OpenDaylight is playing an important role, and OpenStack and OPNFV in SDN-related area.

The details of each activity is shown in the latest version of JCA-SDN D.1 (SDN standards roadmap):

http://www.itu.int/en/ITU-T/jca/sdn/Documents/deliverable/Free-download-sdn-roadmap.docx

General context of the ITU-R work related to 5G & the future development of IMT systems

Backgrounder:

IMT (International Mobile Telecommunications) has been and will continue to be deployed. IMT-2000 =3G (including LTE) and IMT-Advanced = AKA LTE Advanced or “true 4G“ are benefiting from a global approach. The capabilities of IMT systems are being continually enhanced in line with market and technology trends. The next step is 5G which is now known as IMT-2020.

New technology concepts for wireless communications are envisioned. Coincidentally, there is an increasing trend towards convergence of different communication services and systems that come from completely different backgrounds. Such areas of convergence are, for example, mobile communications, Internet, broadcasting, wireless LANs, etc. Each of these represents a variety of applications, services and delivery mechanisms. Users desire these different information flows to be available regardless of the means and manner of delivery. A case in point: mobile communications offer voice, data messages, web browsing (with its varying content, such as information from radio and television broadcast stations), transmit and receive video, listen to MP3 music, etc. Future mobile radiocommunication systems’ users will continue to require higher data rates.

When developing future IMT systems, it is important to consider backward compatibility and interoperability. The ITU-R high-level framework1describes this point clearly as follows:

– That enhanced IMT-2000 systems should support a steady and continuous evolution of new applications, products, and services through improvements in data rates and enhancements to the existing IMT-2000 radio interfaces;

– That the framework for IMT-Advanced should be realized by the functional fusion of existing, enhanced and newly developed elements of new mobile access, nomadic local wireless and so forth, with high commonality and seamless interworking.

Therefore, as much flexibility as possible needs to be retained at the earlier stages of development to ensure that technological advancement can emerge and prosper. Attention is needed so that decisions are not made prematurely that would endanger the flexibility needed to take advantage of the opportunities offered by creating and exploiting convergence.

In conjunction with the future development of IMT, relationships will continue to develop between different radio access and communications systems, for example wireless personal area networks (WPANs), wireless local area networks (WLANs), digital broadcast and fixed wireless access (FWA).

IMT systems will continue to evolve. Studies will be required to determine the overall objectives of future IMT systems and their development in the long term, particularly as IMT-Advanced systems are being deployed. WP 5D already developed Report ITU-R M.2243 “Assessment of the global mobile broadband deployments and forecasts for International Mobile Telecommunications,” with the objective to review the framework and market forecasts for IMT that were developed in previous study periods (2000/2007), by making an assessment of the current perspectives of the future needs of wireless / mobile broadband to be supported by the IMT for the next ten years (2012-2022).

Further work will include spectrum requirements in support of the studies as set out in Resolution 233 (WRC-12), studies on potential frequency ranges and their suitability for IMT, studies of sharing, and compatibility & protection criteria for IMT systems.

Workplan, timeline, process and deliverables for the future development of IMT:

Working Party 5D has developed a work plan, timeline, process and required deliverables for the future development of IMT, necessary to provide by 2020 timeframe, the expected ITU-R outcome of evolved IMT in support of the next generation of mobile broadband communications systems beyond IMT-Advanced. Circular Letter(s) are expected to be issued at the appropriate time(s) to announce the invitation to submit formal proposals and other relevant information. It has been agreed that the well-known process and deliverable formats utilized for both IMT- 2000 and IMT-Advanced should be utilized also for IMT-2020 and considered as a “model” for the IMT-2020 deliverables to leverage on the prior work.

Detailed Timeline & Process for IMT-2020 in ITU-R is here.

General description of WP 5D work program plan:

ITU will continue to play a role as a catalyst to ensure that the correct environment is developed, including appropriate spectrum regulation, to allow new technologies and services to emerge.

The following high-level principles will be taken into account within WP 5D in the work directed towards further enhancement of IMT-2000 and of IMT-Advanced:

– The long range WP 5D work programme takes into account market related issues.

– The focus in WP 5D will include spectrum arrangements, radio interface framework, radio interface technologies and related processes for the development of global core specifications to be derived in an open and global manner.

– Due to the ongoing convergence of services and applications, a flexible and careful approach will be followed for the ITU involvement in definition of future services and technologies for new IMT systems.

– Encourage the development of open and global standards in external entities for referencing in framework Recommendations prepared in ITU.

Update of existing ITU-R M-Series Recommendations and Reports:

Working Party 5D is responsible for updating the relevant existing M-Series documents on IMT#2000 and IMT-Advanced. It should be noted that only those documents that are relevant to the future work of Working Party 5D will be updated; noting however that there is useful content and concepts available in documents developed previously that are still valid for this future work and many aspects will be considered when producing new deliverables. The Recommendations that are no longer applicable will be considered for suppression.

All the ITU-R Recommendations and Reports on IMT, including those that are outside the responsibility of WP 5D, are listed in the following web pages:

– List of ITU-R Recommendations on IMT: www.itu.int/itu-r/go/imt-rec

– List of ITU-R Reports on IMT: www.itu.int/itu-r/go/imt-rep

–>Working Party 5D will develop new Recommendations and Reports as appropriate for the terrestrial component of IMT.

ITU working relationships:

It is essential that all Sectors within the ITU work together to develop a coherent vision for the future development of IMT, which will require close cooperation. It should be noted that:

Resolution ITU-R 50-2 resolves:

“that a roadmap for ITU-R activities on IMT should be developed by the relevant Radiocommunication Study Group to ensure that this work is progressed effectively and efficiently with organizations external to the ITU”;

“That the effective coordination currently established between ITU-T and ITU-R for IMT, Mobile Telecommunication Networks and Next Generation Networks activities should be continued”;

“That work carried out by the Radiocommunication Sector on IMT should be communicated to the Director of BDT”.

This Resolution also invites the ITU-T to develop a complementary roadmap for all ITU-T IMT activities.

ITU-T Resolution 38 resolves:

“That ITU-T maintains a roadmap for all of its standardization activities relating to IMT;”

“that the effective coordination currently established between ITU-T, ITU-R and ITU-D for activities relating to IMT be continued so as to ensure full alignment and harmonization of the work programmes, including the roadmaps, of the three Sectors,”

This Resolution also encourages the Directors of the three Bureaux to investigate new ways to improve the efficiency of ITU work on IMT.

ITU-T Resolution 57 resolves:

– “To invite the Radiocommunication (RAG), Telecommunication Standardization (TSAG) and Telecommunication Development (TDAG) advisory groups to assist in the identification of subjects common to the three Sectors and mechanisms to enhance cooperation and collaboration in all Sectors on matters of mutual interest;

– “To invite the Directors of the Radiocommunication (BR), Telecommunication Standardization (TSB) and Telecommunication Development (BDT) Bureaux to collaborate and report to the respective Sector advisory bodies on options for improving cooperation at the secretariat level to ensure that close coordination is maximized.”

While it may be feasible for the ITU-R and ITU-T roadmaps to be combined into a single document it is considered that there is little merit in doing so and such a combination would lead to a lengthy document that would be difficult to maintain because of the different meeting schedules of the ITU#R WP 5D and the ITU-T responsible group. A more pragmatic and useful course is for each group to independently create their respective roadmaps, update these roadmaps at their own chosen frequency, and to communicate via well-established liaison procedures the latest version of each of the roadmaps so that the ITU-R and ITU-T work activities are complementary.

It is also noted that ITU-R and ITU-D will work cooperatively to develop items of particular interest to developing countries.

Liaison with other groups within ITU-R responsible for systems, other than IMT, shall be done at appropriate points in time.

There is need for close interaction with ITU-R WP 4B in order to properly accommodate the IMT satellite perspective in the development of the service and radio environment. Direct involvement of satellite experts from WP 4B in the on-going sub-working group activities within the WP 5D meetings is important to ensure meeting the schedules outlined in this workplan.

Work with involved organizations, including research entities:

The strategy for ITU-R WP 5D going forward is to gather information from the organizations involved in the global research and development and those that have an interest in the future development of IMT and to inform them of the framework and technical requirements in order to build consensus on a global level.

ITU-R WP 5D can play an essential role to promote and encourage these research activities towards common goals and to ensure that information from the WP 5D development on the vision, spectrum issues, envisioned new services and technical requirements are widespread among the research community. In the same manner, WP 5D encourages inputs from the external communities involved in these research and technology developments.

It is evident that continuing dialogue between the ITU and the entities taking part in research is a key to the continuing success of the industry in advancing and expanding the global wireless marketplace.

Working Party 5D, as is the case with all ITU organizations, works from input contributions submitted by members of the ITU. In order to facilitate receipt of information from external entities who may not be direct members of ITU, the Radiocommunication Bureau Secretariat may be considered as the point of interface, in accordance with Resolution ITU-R 9-4.

The following major activities are foreseen to take place outside of the ITU, including WP 5D, in order to successfully complement the WP 5D work:

– Research on new technologies to address the new elements and new capabilities of IMT#Advanced;

– Ongoing development of specifications for IMT-Advanced and subsequent enhancements.

TABLE A: WP 5D structure with planned outputs/deliverables for WRC-15 agenda item 1.1

|

WP 5D Group |

SWG assignment |

Agenda item 1.1 |

General topic/Scope |

|

General Aspects |

SWG Traffic |

Draft new Report ITU-R |

Traffic and related market demand and users needs towards the years 2020 focusing on terrestrial IMT – including “traffic related” inputs and parameters for use with the terrestrial IMT spectrum estimate methodology. |

|

General Aspects |

SWG Vision |

Draft new Recommendation ITU-R M.[IMT VISION] |

Longer term new IMT & beyond vision for 2020 and beyond to drive the future developments for the radio access network. |

|

Spectrum Aspects |

SWG Estimate |

Draft new Report ITU-R M.[IMT.2020.ESTIMATE] |

Future spectrum requirement estimate for terrestrial IMT. |

|

Spectrum Aspects |

SWG Method |

Draft of Revision 1 of Recommendation ITU-R M.1768 |

Methodology for calculation of spectrum requirements for the future development of terrestrial IMT. |

|

Spectrum Aspects |

SWG Sharing |

Draft new Report ITU-R |

Sharing, compatibility, & protection criteria for IMT Advanced terrestrial systems for WRC-15 studies. |

|

Spectrum Aspects |

SWG-Suitable Frequency Ranges |

Liaison to JTG 4-5-6-7 and possible document M.[IMT.2020.FREQ RANGE] |

Identification and assessment of suitable frequency ranges for future terrestrial IMT including perspectives on current and planned use of the mobile service. |

|

Technology Aspects |

SWG Radio Aspects |

Draft new Report ITU-R M.[IMT.2020.INPUT] |

Future “technology related” inputs and parameters for use with the terrestrial IMT spectrum estimate methodology. |

|

Technology Aspects |

SWG Radio Aspects |

Draft new Report ITU-R |

Broad view of shorter term future aspects and trends of terrestrial IMT systems. |

|

Ad Hoc Workplan |

– |

Details in Chapter 2 of Chairman’s Report of WP 5D |

Maintenance of schedules and deliverable timings/planning for WRC 15 work in WP 5D including detailed workplans and coordination. |

TABLE C: Relationship of WP 5D Reports and Recommendations for WP 5D studies on agenda item 1.1 to information supplied to the JTG 4-5-6-7

|

JTG 4-5-6-7 |

Liaised topic |

WP 5D |

WP 5D deliverables |

Description |

|

– |

– |

Traffic data inputs |

Draft new Report ITU-R |

Traffic and related market demand and users needs towards the years 2020 focusing on terrestrial IMT – including “traffic related” inputs and parameters for use with the terrestrial IMT spectrum estimate methodology. |

|

– |

– |

Technology related inputs |

Draft new Report ITU-R M.2289-0 |

Future “technology related” inputs and parameters for use with the terrestrial IMT spectrum estimate methodology. |

|

– |

– |

Methodology |

Draft Revision of Recommendation ITU-R M.1768 (2006) |

“Spectrum calculation methodology for IMT 2000 and IMT-Advanced” |

|

Spectrum requirements |

Spectrum |

|

Draft new Report ITU-R M.2290-0 |

Future spectrum requirement estimate for terrestrial IMT. |

|

|

|

|

|

|

|

Candidate bands |

Suitable Frequency Ranges |

– |

Liaison and possible document ITU-R M.[IMT.2020.FREQ RANGE] |

Identification and assessment of suitable frequency ranges for future terrestrial IMT including perspectives on current and planned use of the mobile service. |

|

|

|

|

|

|

|

Sharing studies (JTG 4-5-6-7) |

Sharing , compatibility & protection criteria for IMT systems |

IMT-Advanced Parameters |

Draft new Report ITU-R |

Sharing, compatibility, & protection criteria for IMT-Advanced terrestrial systems for WRC-15 studies. |

|

IMT-2000 Parameters |

[Draft revision] of Report ITU-R M.2039 |

“Characteristics of terrestrial IMT-2000 systems for frequency sharing/interference analysis” |

||

|

Approved Existing IMT Sharing Studies |

Approved existing IMT Reports & Recommendations |

Listing of relevant existing Reports and Recommendations forwarded to |

|

– |

– |

Draft new Report ITU-R |

Broad view of future technology aspects and trends of terrestrial IMT systems. |

|

– |

– |

Draft new Recommendation ITU-R M.[IMT VISION] |

Longer term new IMT & beyond vision for 2020 and beyond to drive the future developments for the radio access network. |

TABLE D: Summary of information forwarded to JTG 4-5-6-7 from WP 5D related to WRC-15 AIs 1.1 and 1.2

|

“Liaised topic” |

Information liaised (16-20 July 2012) |

Information liaised (3-11 October 2012) |

Information liaised (30 Jan. – 6 Feb. 2013) |

Information liaised (10-17 July 2013) |

|

Spectrum |

– |

Spectrum requirements as set out in Resolution 232 (WRC-12) (Doc. 4-5-6-7/50) Initial information on spectrum requirements as set out in Resolution 233 (WRC-12) (Doc. 4-5-6-7/47) |

– |

Spectrum requirements as set out in Resolution 233 (WRC 12) (Doc. 4-5-6-7/237) |

|

Suitable Frequency Ranges |

Initial text on suitable frequency ranges (Doc. 4-5-6-7/38) |

Further elaboration on suitable frequency ranges and their suitability (Doc. 4-5-6-7/46) |

Further elaboration on suitable frequency ranges and their suitability (Doc. 4-5-6-7/118) (Doc. 4-5-6-7/117) |

Any final input to (Doc. 4-5-6-7/220) |

|

Sharing , compatibility & protection criteria for IMT systems |

Listing of relevant existing Reports and Recommendations related to sharing and compatibility studies (Doc. 4-5-6-7/38) |

Final input on sharing parameters for Resolution 232 (WRC-12) related work (Doc. 4-5-6-7/49) |

Adjacent band compatibility between IMT UL and DTT under WRC-15 agenda item 1.2 (Doc. 4-5-6-7/116) |

Final input on (Doc. 4-5-6-7/236) Status of compatibility study between FSS networks and IMT systems in the band 3 400-3 600 MHz for small cell deployments (Doc. 4-5-6-7/238) |

|

Frequency Arrangements |

– |

Channelling arrangements as per Resolution 232 (WRC-12) (Doc. 4-5-6-7/48) |

– |

– |

Draft detailed workplan for development of the draft new Report ITU-R M. [IMT-2020.SUBMISSION]

|

Title |

Requirements, evaluation criteria and submission templates for the development of IMT‑2020 |

|

Identifier |

ITU-R M.[IMT-2020.SUBMISSION] |

|

Document Type |

Report |

|

ITU-R WP 5D Lead Group |

WG Technology Aspects |

|

Sub-Working Group |

SWG Coordination |

|

Focus for scope and work |

This Report addresses the requirements, evaluation criteria, as well as submission templates required for a complete submission of candidate radio interface technologies (RITs) and candidate sets of radio interface technologies (SRITs) for “IMT-2020”. |

|

Related documents |

Recommendation ITU-R M.[IMT.VISION] Report ITU-R M.[IMT-2020. TECH PERF REQ] Report ITU-R M.[IMT-2020.EVAL] Report ITU-R M.[IMT.ABOVE 6GHz] Report ITU-R M.2320 Report ITU-R M.2133 IMT-2020/1, 2 Circular Letter 5/LCCE/xxx |

|

Milestones |

Meeting No. 23 (TBD, 2016) 1.Discuss document structure and table of contents

Meeting No. 24 (TBD, 2016)

Meeting No. 25 (TBD, 2016)

Meeting No. 26 (TBD, 2017)

Meeting No. 27 (TBD, 2017)

|

Draft detailed workplan for development of the draft new Report ITU-R M.[IMT-2020.TECH PERF REQ]

|

Title |

Requirements related to technical performance for “IMT-2020” radio interface technologies |

|

Identifier |

M.[IMT-2020.TECH PERF REQ] |

|

Document Type |

Report |

|

ITU-R WP 5D Lead Group |

WG Technology Aspects / SWG Radio Aspects |

|

Sub-Group Chair |

Mr. Marc GRANT; E-mail: [[email protected]] |

|

Editor |

TBD |

|

Focus for scope and work |

This Report describes requirements related to technical performance for “IMT-2020” candidate radio interface technologies. These requirements are used in the development of Report ITU-R M.[IMT-2020.EVAL]. This Report also provides the necessary background information about the individual requirements and the justification for the items and values chosen. Provision of such background information is needed for a broader understanding of the requirements. The Report is based on the ongoing development activities from external research and technology organizations. |

|

Related documents |

Recommandation ITU-R M.[IMT.VISION] Report ITU-R M.[IMT-2020.EVAL] Report ITU-R M.[IMT-2020.SUBMISSION] Report ITU-R M.[IMT.ABOVE 6GHz] Report ITU-R M.2320 IMT-2020/1, 2 Circular Letter 5/LCCE/xxx |

|

Milestones |

Meeting No. 23 (TBD, 2016)

Meeting No. 24 (TBD, 2016)

Meeting No. 25 (TBD, 2016)

Meeting No. 26 (TBD, 2017)

|

Conclusion:

As you can see from the above work plans, it won’t be till late 2016 till the 5G Vision reports are completed. Until then it is way too early to talk about the functional elements/composition of 5G radio interface technologies and their implementation.

References:

https://www.itu.int/net/ITU-R/study-groups/docs/workshop-wp5abc-wrc15/WP5ABC-WRC15-P4-4.pdf

http://www.itu.int/en/ITU-R/study-groups/rsg5/rwp5d/imt-2020/Documents/Antipated-Time-Schedule.pdf

https://www.itu.int/osg/spu/imt-2000/technology.html

https://en.wikipedia.org/wiki/3G

http://www.strandreports.com/sw4334.asp

Disclaimer:

This article was NOT written by Alan J Weissberger. It’s an edited version of the ITU-R workplan for 5G.

Separating 5G fact from hype: Is Massive MIMO a Solution or Dead End?

Background:

Despite only a “vision” with no definition or specs from ITU-R of fifth generation wireless networks (5G), mobile vendors and wireless network operators continue to keep talking about 5G ready products and deployment — even if they’re not really even sure what 5G is yet. In the last year, we have seen carriers announce “4.5G” and “Pre-5G” technology and island’s vying for the first 5G network. In reality, carriers are simply marketing 5G packages that include speeds that barely reach what is defined today as 4G.

For the record, true 4G is LTE Advanced (see reference below), which only a few features have been deployed, like Carrier Aggregation. Almost all the “4G-LTE” deployments are really 3.5G.

Karl Bode reported previously that the ITU-R declared no major wireless carrier was technically deploying 4G networks since none were capable of speeds over 100 Mbps. Yet many wireless carriers simply ignored the declaration, with T-Mobile arguing their HSPA+ build was the “largest 4G network,” while Sprint, AT&T and Verizon also made “4G” part of marketing for their respective Mobile WiMax, HSPA+ and LTE networks.

To turn their hype into reality, carriers pressured the ITU-R to redefine 4G so that almost every current wireless network was deemed 4G. Consequently, it’s looking more likely that over the next few years, the definition of 5G will be lowered to make sure that improved 4G networks are included in the definition of 5G.

ITU-R Status on 5G now called IMT-2020:

In early 2012, ITU-R embarked on a programme to develop “IMT for 2020 and beyond”, setting the stage for “5G” research activities that are emerging around the world. As of June 19, 2015, ITU-R finally established the overall roadmap for the development of 5G mobile and defined the term it will apply to it as “IMT-2020.”

With the finalization of its work on the “Vision” for 5G systems at a meeting of ITU-R Working Party 5D in San Diego, CA, ITU defined the overall goals, process and timeline for the development of 5G mobile systems. This ongoing 5G work plan is being done by ITU in close collaboration with governments and the global mobile industry.

The ITU-R Working Party 5D San Diego, CA meeting also agreed that the work should be conducted under the name of IMT-2020, as an extension of the ITU’s existing family of global standards for International Mobile Telecommunication systems (IMT-2000 and IMT-Advanced) which serve as the basis for all of today’s 3G and 4G mobile systems.

The next step is to establish detailed technical performance requirements for the radio systems to support 5G, taking into account the needs of a wide portfolio of future scenarios and use cases, and then to specify the evaluation criteria for assessment of candidate radio interface technologies to join the IMT-2020 family. The ITU-R Radiocommunication Assembly, which meets in October 2015, is expected to formally adopt the term “IMT-2020.” These new systems, set to become available in 2020, will usher in new paradigms in connectivity in mobile broadband wireless systems to support, for example, extremely high definition video services, real time low latency applications and the expanding realm of the Internet of Things (IoT).

We think a huge segment of the IoT market will require cellular communications (mostly 3G or LTE, but NOT LTE Advanced or 5G).

“The buzz in the industry on future steps in mobile technology – 5G – has seen a sharp increase, with attention now focused on enabling a seamlessly connected society in the 2020 timeframe and beyond that brings together people along with things, data, applications, transport systems and cities in a smart networked communications environment,” said ITU Secretary-General Houlin Zhao. “ITU will continue its partnership with the global mobile industry and governmental bodies to bring IMT-2020 to realization.”

Ongoing ITU information on the development of IMT-2020 will be available here.

5G NORMA project to help define 5G radio architecture:

The 5G Infrastructure Public-Private Partnership (5GPPP) initiative has started the 5G NORMA (5G Novel Radio Multiservice adaptive network Architecture) project, set up to define the overall 5G mobile network architecture, including radio and core networks, needed to meet 5G multiservice requirements. The consortium is composed of 13 partners among leading industry vendors, operators, IT companies, small and medium-sized enterprises and academic institutions.

5G NORMA will propose an end-to-end architecture that takes into consideration both radio access network (RAN) and core network aspects. The consortium will work over a period of 30 months from July, to meet the key objectives of creating and disseminating innovative concepts on the mobile network architecture for the 5G era.

The overall aim of the 30-month project is to propose an end-to-end architecture taking into account both the radio access network (RAN) and core networks. The project will seek to underpin Europe’s leadership position in 5G, breaking from the rigid legacy network paradigm. It will on-demand adapt the use of the mobile network (RAN and Core Network) resources to the service requirements, the variations of the traffic demands over time and location, and the network topology, which include the available front/backhaul capacity. The consortium envisions the architecture will enable unprecedented levels of network customisability to ensure that stringent performance, security, cost and energy requirements are met. It will also provide an API-driven architectural openness, fueling economic growth through over-the-top innovation.

The project partners, spread across six countries, include leading mobile operators (Orange, Deutsche Telekom, Telefonica), network vendors and IT companies (Nokia Networks, Alcatel-Lucent, ATOS), SMEs (Nomor Research, Azcom Technology) and Universities (King’s College London), Technische Universität Kaiserslautern, and Univerdidad Carlos III de Madrid). More info on NORMA is here.

Massive MIMO for 5G:

The next generation wireless networks need to accommodate 1000x more data traffic than contemporary wireless networks. Since the spectrum is scarce in the bands suitable for coverage, the main improvements need to come from spatial reuse of spectrum; many concurrent transmissions per unit area. This is made possible by the massive MIMO technology, where the access points are equipped with hundreds of antennas. These antennas are phase-synchronized and can thus radiate the data signals to multiple users such that each signal only adds up coherently at its intended user.

Over the last the couple of years, massive MIMO has gone from being a theoretical concept to becoming one of the most promising ingredients of the emerging 5G technology. This is because it provides a way to improve the area spectral efficiency (bit/s/Hz/area) under realistic conditions, by upgrading existing base stations. Many experts think that massive MIMO is a commercially attractive solutionsince 100x higher efficiency is possible without installing 100x more base stations.

Maybe not? According to co-authors Jin Liu and Hlaing Minn, there are serious analog front end design challenges for Massive MIMO as noted in this just published IEEE ComSoc Technology News article.

More HYPE- does it ever end?

Telecom firm Ericsson is testing out a new 5G device on the streets of Stockholm, Sweden and Plano, Texas, the company says will revolutionize mobile technology.

“5G technology will also tap into new high-frequency spectrum known as the millimeter waves, which today are unusable for mobile communications. However, in the future the spectrum could open up thousands of megahertz of new frequencies for wireless broadband use, thereby adding tremendous amounts of bandwidth to mobile networks.”

Much of the work being done on 5G has little do with raw speed. Researchers are trying to bring down the latency of the network—the delay users experience after clicking on a link and before a web page loads—cutting it down from 30 milliseconds today to less than a single a millisecond in the future. By reducing the network’s reaction time, researchers open the door for a whole new set of real-time applications. For instance, autonomous cars could communicate their intentions to other vehicles over the network instantaneously, allowing them to coordinate their speed and lane position or avoid potential accidents.

“This is not only yet another system for mobile broadband,” says Sara Mazur, Ericsson’s head of research. “The 5G system is the system that will help create a networked society.”

5G could be all of these different technologies, or it could wind up being only one or two of them. The fact is 5G doesn’t yet have an official definition, and won’t for several years, while the mobile industry and global regulators settle on a standard. 5G is viewed by some as a way of bridging the digital divide between poor and rich countries or big cities and rural towns. Still others want 5G to become the glue connecting every conceivable device and application to the Internet.

To this author 5G is all about vision, hype, and speculation. We advise you to not believe ANY vendor or wireless network operator claims about their 5G network or products!

References:

ITU defines vision and roadmap for 5G mobile development

IMT Vision towards 2020 and Beyond

ICC 2015 Globecom Tutorial: 5G Evolution and Candidate Technologies

Cutting through the Hype: Will the real 4G (LTE-A) please stand up and tell us what 5G is?

Upcoming webinar:

5G: Separating hype from fact – understanding where the market really is at today, July 8, 2015 at 2pm BST (9am EDT)

Highlights of 2015 Open Network Summit (ONS) & Key Take-Aways

Executive Summary:

There were many significant announcements at this year’s Open Networking Summit (ONS), held June 15-18, 2015 in Santa Clara, CA. Unlike in past year’s conferences, there were no vendor sales pitches or infommercials. That was certainly refreshing! However, ONS continues to focus on “pure SDN” (as per the ONF definition) vs. various other SDN reference architectures, such as network virtualization/overlay model. That’s largely because the ONS is closely aligned with the Open Networking Foundation (ONF) and ON.Lab (which developed the open source Open Network Operating System). Surprisingly, there were several companies (Google, Microsoft, AT&T) that said they were using OpenFlow (but not how) in their proprietary versions of SDN.

THE MAJOR THEME OF THE CONFERENCE: Most SDN and NFV SOFTWARE IS GOING TO BE OPEN SOURCE – from organizations like OpenDaylight, ONOS lab, OPNFV, and ONF.

The open source movement will drastically disrupt many companies that had planned on their own vendor specific implementations of SDN Controllers, Open Flow, and NFV virtual appliances. The key missing piece of vendor neutral SDN and NFV software is MANAGEMENT & ORCHESTRATION (which includes scheduling and service insertion/chaining). Until that’s provided by one or more open source communities, proprietary implementations will inhibit widescale deployment of SDN (and even more so) NFV.

I believe the Atrium project (see description below) is a milestone for ONF in that it expands their scope to include open source software for SDN. Atrium will likely complement Open Daylight and ONOS open source projects. It’s still very early in the SDN Open Source space while OPNFV (for NFV) is in its infancy. Some efforts will succeed; others will fail. IMHO, commercial, supported Open Source SDN/NFV code will be critically important to the open networking industry.

Key Take-Aways:

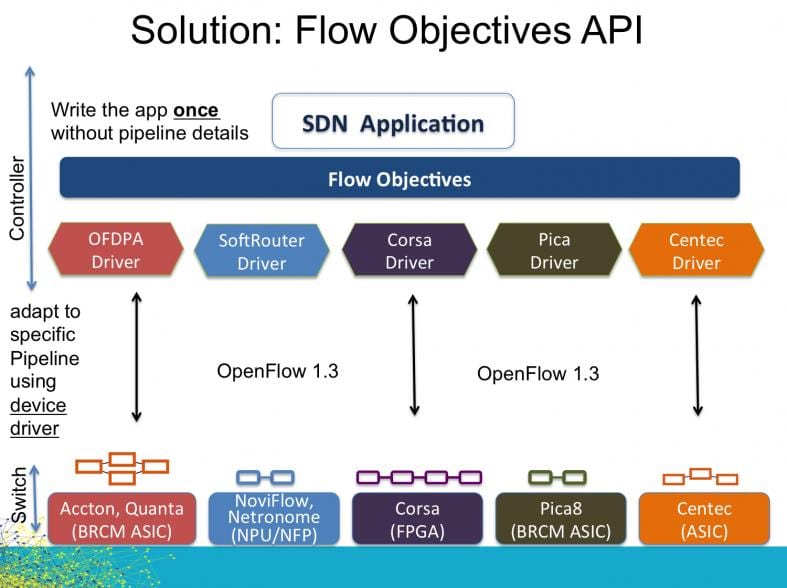

- The ONF’s Atrium open source software was demo’d at the ONF SDN showcase on the exhibit floor. ONF Executive Director Dan Pitt described it’s significance and ongoing trend setting work within ONF during an interview with this author.

- ONF also demonstrated OpenFlow hardware interoperability using SDN data plane switches from five different vendors (Accton, Quanta, NoviFlow, Netronome, Corsa, Pic8, and Centec). They achieved this by defining a mediation sublayer called “Flow Objectives,” which the data plane switch companies I/O driver software/firmware interfaces with. Hence, it masks the hardware differences/uniqueness of each data plane switch vendor’s product.

- ONOS, the community developing the open source SDN network operating system and control plane, announced that software’s first wide-scale production deployment on the Internet2 research network. It demo’d an open source SDN router running on white box hardware. The Internet2 deployment is the first big deployment of ONOS on a live network. ONOS sponsors fund the open source software development wihich is done in Menlo Park, CA by programmers that work there.

- Dell and Huawei expressed interest in the commercial open source business for SDN with Huawei favoring ONOS for teleco/carrier SDN and OpenDaylight for enterprise SDN as well as smart cities and IoT.

- John Donovan, AT&T’s senior EVP for technology and operations said the company only uses open source now for ~5% of its software, but would like to increase that to 50% in the next few years. He said AT&T’s “secret sauce” (proprietary) software should be used sparingly, “like tabasco sauce.” AT&T is an active participant in OpenDaylight and Open Platform for NFV (OPNFV). AT&T is also an active participant in TM Forum’s ZOOM program, which is actively building relationships with both OpenDaylight and OPNFV. AT&T is contributing a design tool to OpenDaylight that the company has been using it its quest to “disaggregate” its network as part of its Domain 2.0 initiative. That means disentangling all the various subsystems and stripping down to core components, Donovan explained. “We have to rethink how they’re constructed,” he said. Note that AT&T is not, and has never been, a member of the ONF.

- AT&Ts goal is to convert 75% of the network equipment hardware boxes in its network to software running on generic/commodity compute servers by 2020, according to Mr. Donovan. From a base of zero, 5% of AT&T’s network equipment will be implemented in software by the end of 2015, Donovan said.

- AT&T is on an “aggressive schedule” to make the optical transport layer more flexible, according to Andre Fuetsch, AT&T’s senior vice president of architecture and design. “We want to start pushing NFV down the stack. We want to push it to Layer 1,” Fuetsch said during a keynote panel at the Open Networking Summit (ONS) on Tuesday.

- CORD for GPON: AT&T, along with chip vendors PCM-Sierra and Sckipio Technologies, are using the ONOS SDN software on a proof-of-concept project called Central Office Re-architected as Data Center (CORD). The basic premise of CORD is to transorm AT&T’s Central Offices (COs) so that they look like cloud resident data centers with compute servers doing all the heavy lifting. AT&T plans to dis-aggregate the functions of each network element- in this case a GPON Optical Line Terminal (OLT) – so that as many software functions as possible to run on generic compute servers. The white box hardware for CORD-GPON is a “stackable OLT” with GPON blades that are connected via Ethernet to a top-of-rack switch. Here’s a paper on the CORD fabric.an open source leaf-spine CLOS fabric

- CORD for g.fast: AT&T also demo’d a CORD proof of concept project for G.fast. An OpenFlow-enabled G.fast distribution point unit (DPU) was connected to a G.fast CPE bridge from Sckipio. [G.fast is an ITU-T DSL standard for short local loops (<500 meters) with performance targets between 150 Mbit/s and 1 Gbit/s,]

- For the first time anywhere, Google disclosed its internal data center network architecture and Jupiter jumbo data center switch. Scale out, performance and availability are Google’s key challenge in network design. The company designed their own routing protocol and didn’t use any open source software. Google’s current data center network design has a maximum capacity of 1.13 petabits per second using merchant silicon with their own routing protocols and software. For comparison, the current data center throughput is more than 100 times as much as the first data-center network Google developed 10 years ago. The current network is a hierarchical design with three tiers of switches, but they all use the same “off the shelf” chips. Google’s control software treats all the switches as if they were a single switch.

- The Jupiter jumbo switch leverages the latest generation of merchant silicon, has 80 Tbit/s bandwidth, and uses some form of SDN (Google proprietary) with OpenFlow used in an undisclosed manner.

Google’s Jupiter “cluster switches” provide 40 terabits per second of bandwidth—about as much as 40 million home internet connections. SOURCE: Google.

Google’s Jupiter “cluster switches” provide 40 terabits per second of bandwidth—about as much as 40 million home internet connections. SOURCE: Google.

- We strongly suggest the reader view/hear Amin Vahdat, PhD keynote on Google’s evolving data center network architecture.. Amin is one of the best NO NONSENSE presenters on networking that this author has ever observed. His keynote speech is here. We also recommend you read Amin’srelated blog: A look inside Google’s Data Center Networks

- Microsoft Azure public cloud uses its own unique version of SDN, which was described by CTO Mark Russinovich during his keynote speech. Fifty-seven percent of the Fortune 500 use Azure (we find that remarkable as Amazon’s AWS is by far the #1 public cloud service provider for Infrastructure as a Service -IaaS). Microsoft’s cloud storage and compute usage doubles every six months, and Azure adds 90,000 new subscribers a month, and this places unprecedented demands on its network, Russinovich said. The number of host computers quickly grew from 100,000 to millions. Microsoft Azure needs a virtualized, partitioned and scale-out design, delivered through software, in order to keep up with the explosive growth of users and data. Microsoft uses virtual networks (Vnets) built from overlays and Network Functions Virtualization (NFV) services running as software on commodity servers. [Note that virtual networks and overlays are NOT permitted in “pure SDN” and are a completely orthogonal SDN reference architecture].

–Vnets are partitioned through Azure controllers established as a set of interconnected services, and each service is partitioned to scale and run protocols on multiple instances for high availability.

-SDN Controllers are established in regions where there could be 100,000 to 500,000 hosts. Within those regions are smaller clustered controllers which act as stateless caches for up to 1,000 hosts.

-Microsoft builds their SDN controllers using an internally developed the Azure Service Fabric, which has what Microsoft refers to as a “microservices-based architecture” that allows customers to update individual application components without having to update the entire application. Microsoft’s Azure Service Fabric SDK is available for download here.

-Microsoft Azure’s SDN doesn’t use any open-source software. Russinovich said that’s because open-source communities don’t provide the functionality Azure requires.

-Russinovich said Azure’s SDN gets a hardware assist from a SmartNIC FPGA. SmartNIC covers those functions that need a hardware boost, or that Microsoft would just prefer to offload from the CPU. User data traffic flows through the SmartNIC – for functions such as encryption, quality-of-service processing, and storage acceleration. “The sky’s the limit, really, with what we can do with an FPGA given its flexible programming,” Russinovich said. He said that compute servers are better at running virtual machines to serve Azure customers, rather than to take on mundane network processing tasks that could be better implemented in silicon. Mark’s keynote can be watched here.

—>NOTE that this is the exact opposite of AT&T’s position on disaggregating network element functions and moving as much software as possible to generic compute servers, leaving only physical layer transport in network equipment. Microsoft evidently believes that hardware assist from smart NICs is still a valuable proposition for SDN.

- Service provider adoption of SDN/NFV: From Talk to Action (?): Andre Fuetsch of AT&T, Kang-Won Lee of SK Telecom, and Yukio Ito of NTT communications shared their works, experiences, challenges and roadmap in the keynote panel, moderated by Guru Parulkar, Chair ONS, at the ONS-2015. The common aspects among all the three telcos were: (a) Importance of Open Source (b) Presence of both technical and non-technical challenges in adapting SDN/NFV (c) Experience in real-world deployments of NfV use-cases, and (d) Importance of role of SDN in transport networks, especially optical transport.

—>This author noted that the “attack surface” exponentially increases with SDN and NFV so asked a question on mitigation of cyber security attacks. As that issue has been “swept under the rug” for a long time, it seemed to stun the moderator with no clear solutions from the three carrier panelists. Checkout the video clip yourself to see if the answers were “on the mark” or not.

- Alibaba disclosed the China eCommerce giant was using BOTH the pure SDN/OpenFlow and the Network Virtualization/Overlay model in the same network. Panel moderator Guido Appenzeller, PhD of VMWare said that was the first time he’d heard of both SDN reference architectures being used within the same network. How do they inter-connect, if at all?

- During a Thursday, June 18th Opening Keynote Panel titled SDN in Enterprises, NSA’s Brian Larish said, “centralized control via OpenFlow is key” and “we are all in on OpenFlow.”

- Cavium’s XPliant® Switch was the winner of SDN Idol 2015, the open networking industry’s top award for the year’s hottest SDN solutions. The four finalists for SDN Idol 2015 were: Cavium, XPliant Switch; Huawei, 2015 SDN IDOL – DN-based IP & Optical Synergy; NEC, SDN Cyber Attack Auto Protection; and Pluribus Networks, Integrated Network Analytics.

Selected Quotes:

- “Embrace Open Source SDN or become irrelevant going forward.” Guru Parulker, PhD and Chair of the ONS (each year since its inception)

- “Open Networking is here now and encompasses disaggregation of networking technologies including hardware and software similar to Servers 20 years ago. We expect the momentum of ON/SDN/NFV to pick up in 2015 for both Carriers and Enterprises and we are excited that Dell was a leader in creating and embracing this disruption.” Arpit Joshipura, VP of Dell Enterprise Networking & NFV and a long time colleague who this author truly respects.

- “SDN and NFV are speeding up innovation, as seen in projects like CORD,” said Tom Anschutz, Distinguished Member of Technical Staff at AT&T in a press release. “These technologies create systems that do not need new standards to function and enable new behaviors in software, which decreases development time. Faster development time leads to rapid innovation, something the industry needs to continue satisfying data-hungry customers.”

-

“Data Center Anchored Communication Services (DACS) is one of the key motivations for using SDN….We are all on a leash when we use the public network. Sometimes we like it because we get “move around” with IP, sometimes we would have wanted more bandwidth. But there is a leash tied to an anchor for each communication service – statefull inline control.” Sharon Barkai, founder of Contextream which is now part of HP. [Note that ConteXtream has historically gone after service providers to deploy its software into data centers and centralize management of networks.]

- “The (networking) industry is porting anchors from network appliances, and Application Specific Integrated Circuits (ASICs), to software on standard (x86) compute servers. Getting these DACS to factory mode in a row of clusters involves flows, granularity, federation, overlays, mapping, Overlay Descriptor Lists, etc. The challenge is to map traffic to computed anchors dynamically per flow. Virtualization frees any given hardware from ties to specific service functions and specific subscribers. This is where the capex (utilization) and opex (factory) savings come from and how feature velocity enabled. SDN really determines what gets processed where, and therefore, done right, holds the key.” Sharon Barkai of HP (see previous quote).

-

“Open-source may, in the long-run, be more secure, but it’s a tough one to buy. I guess one would have to look historically at open-source software projects and ask if the mere fact that a project was open-source contributed to its robustness, or was it that the robustness was introduced by someone who took the open-source effort and really provided that additional software that made things secure.” Vishal Sharma, PhD, Principal Metanoia, Inc & IEEE ComSocSCV officer.

- “Software Defined Networking is now migrating from a discussion to actual implementation in the real world….The XPliant protocol independent programmable (Ethernet) switch silicon is providing a platform for innovation to further this reality.” Eric Hayes, VP/GM, Switch Platform Group at Cavium (winner of SDN Idol award as noted above).

- “This year’s ONS is rife with SDN and OpenFlow solutions such as the Atrium Project that demonstrate how these technologies provide a whole new tool-set for solving network problems. We now face the challenge of making the benefits this technology known to a wider audience, and affecting a truly fundamental change in how networking is done! It’s a fascinating time to be in the networking business!” Marc LeClerc, VP Strategy and Marketing at NoviFlow Inc. [Marc described the Atrium OpenFlow (ONF control plane to 5 different data plane switches) interop demo to this author and Ken Pyle – see above illustration].

Acknowledgement:

The author would like to thank Elise Vue, Publicist for EngagePR who was in charge of the media for this conference. Unlike most PR agencies that ignore or neglect accredited media, Elise went out of her way to ensure I was getting everything I possibly could from ONS 2015 each and every day (Tues, Wed, and Thurs). It was a truly refreshing and positive change from most conferences I’ve attended recently. Elise also followed up after the conference to provide feedback on the unscripted video interview I did with ONF’s Dan Pitt: “I agree with Dan, it was seamless! Great work, keep it up.” THANKS for your excellent support, Elise!

References:

Alan’s interview with Dan Pitt, Executive Director of ONF:

How ONF is Accelerating the Open Software Defined Networking (SDN) Movement

http://www.archives.opennetsummit.org/archives-ons/archives-2015/

Cuba to expand Internet access and lower price of WiFi connections

The Cuban government announced plans to expand internet access throughout the island and lower the per-hour price of Wi-Fi. Cuba plans to add Wi-Fi to 35 state-run computer centers across the island, where internet access remains tightly controlled and illegal at home for most Cubans. Cuba will also lower the price of Wi-Fi based Internet access from $4.50 to $2 per hour.

The Internet initiatives were announced in Juventud Rebelde, an official newspaper aimed at the island’s youth, came amid new pressures to increase Internet access as the nation edges toward normalizing diplomatic relations with the United States. By this July, the state-run telecommunications company, Etecsa, will open 35 hot spots, mainly in parks and boulevards of cities, the company’s spokesman told Juventud Rebelde. Connection will cost just over $2 per hour, half of what it currently costs in an Internet cafe. However, it’s unclear exactly how quickly the Cuban government will conduct the expansion and how well the connections will actually work.

Gizmodo says: “Since the average salary in Cuba is only about $20 a month, that’s still pretty damn expensive. Nevertheless, it’s an improvement over a couple years ago when there was just one internet cafe in Old Havana. Things have been so bad there in recent years that young Cubans have taken things into their own hands and built an elaborate mesh network to create their own thriving underground internet. They also pass internet content around via USB sticks.”

Ted Henken, a professor at Baruch College in New York who has studied social media and the Internet in Cuba, said the decision could mark a “turning point. Their model was, ‘Nobody gets Internet,’ ” he said in a telephone interview. “Now their model is, ‘We’re going to bring prices down and expand access, but we are going to do it as a sovereign decision and at our own speed.’ ”

Nothing was announced for wireline Internet access to homes or business, probably because of very llimited DSL depolyment throughout the island. While the number of residential DSL Internet access lines has not been made public, that service was supposed to have been initiated last year as per this article:

Cuba’s ETECSA to provide residential DSL services in 2014

Also refer to:

Cuba’s WiFi access plan raises intresting questions

http://laredcubana.blogspot.com/2015/06/cubas-wifi-access-plan-raises.html

Addendum – Cuba’s Internet Infrastructure:

The country’s Internet capability was greatly boosted by the completion of an undersea fiber-optic cable from Venezuela that came online in January 2013. Venezuela financed it, a French company built it, and Doug Madory, the guy at Dyn Research who spotted that underwater cable, says it’s got potential you haven’t even tapped: “It’s improved their connectivity to the outside world. However, the improvement of greater access to the people of Cuba, that’s still slow going.”

Authorities say Cuba must prioritize its bandwidth for uses that are deemed to benefit society, such as schools and workplaces. Critics say government prohibitions are the main obstacle to access, although the state has gradually been loosening some controls.

Cuba’s poor Internet access is a grievance increasingly shared across political lines, by entrepreneurs and computer programmers as well as journalists and ordinary citizens who want to communicate with relatives overseas.

It is a source of frustration for young people, a growing number of whom — especially in Havana — own a smartphone that they cannot use to get online. The city’s one hot spot — at the workshop of the artistKcho — is constantly packed.

Over the past two years, the government has opened dozens of Internet cafes and introduced email service for the island’s million or so cellphone users. It signaled its willingness to expand connectivity this month in a leaked report that argued that lack of Internet access was holding back the economy. The report outlined plans to get broadband — albeit slow broadband — to half of Cuban homes by 2020.

According to Wikipedia, “The Internet in Cuba is among the most tightly controlled in the world.[2] It is characterized by a low number of connections, limited bandwidth, censorship, and high cost.[3] The Internet in Cuba stagnated since its introduction in the 1990s because of lack of funding, tight government restrictions, the U.S. embargo, and high costs. Starting in 2007 this situation began to slowly improve. In 2012, Cuba had an Internet penetration rate of 25.6%.[4]“

Reference:

https://techblog.comsoc.org/2014/12/21/u-s-cuba-rapprochement-telecom-internet-infrastructure-is-a-top-priority-for-the-cuban-government

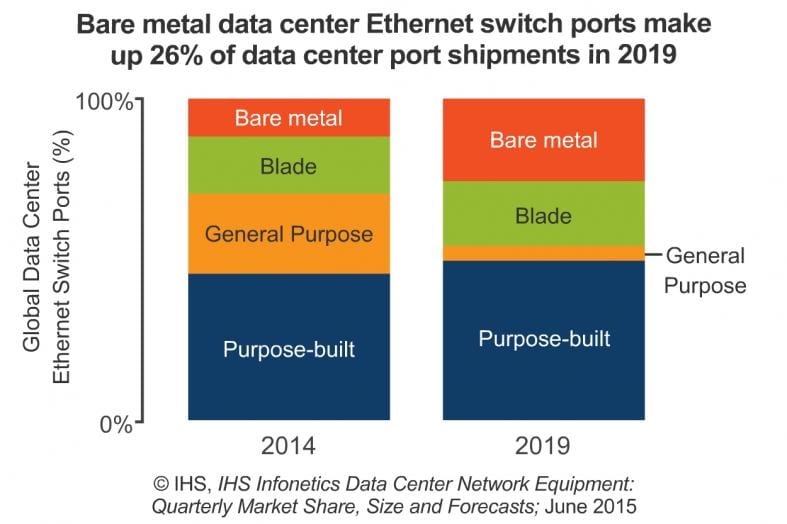

Open Networking/SDN Reference Models + Bare Metal Switches increase market share in Data Centers

Introduction:

“Open networking, which leverages open source software and open hardware designs and allows anyone to innovate, is set to change networking, just as open source changed the server and OS marketplace,” said Cliff Grossner, Ph.D., research director for data center, cloud and Software Defined Networking (SDN) at IHS.

“This move to open networking is heightening the importance of bare metal switches, as evidenced by all the vendor announcements at Interop in April. Dell is expanding its open networking portfolio with three new branded bare metal switches providing options from 1GE to 100GE Ethernet. And Citrix entered the SD-WAN market with Cloudbridge Virtual WAN Edition, which allows enterprises to create a virtualized WAN,” Grossner said.

Open Networking/SDN Reference Models:

Mr. Grossner and this author are collaborating on a report/article defining Open Networking Reference Architectures, Business Models, and Vendors Market Share. We’ve identified the following reference architectures:

DATA CENTER MARKET HIGHLIGHTS:

- The global data center network equipment market-including data center Ethernet switches, application delivery controllers (ADCs) and WAN optimization appliances (WOAs)-declined 14% sequentially in 1Q15, to $2.6 billion.

- The data center Ethernet switch segment continues to grow on a year-over-year basis (+4% in 1Q15 from 1Q14); positive forces include large enterprises and the public sector.

- F5 took the #1 spot for virtual ADC appliance revenue from Citrix in 1Q15.

DATA CENTER REPORT SYNOPSIS:

The quarterly IHS-Infonetics Data Center Network Equipment market research report tracks data center Ethernet switches, bare metal Ethernet switches, Ethernet switches sold in bundles, application delivery controllers (ADCs) and WAN optimization appliances (WOA). The research service provides worldwide and regional market size, vendor market share, forecasts through 2019, analysis and trends. Vendors tracked include A10, ALE, Arista, Array Networks, Aryaka, Barracuda, Blue Coat, Brocade, CloudGenix, Cisco, Citrix, Dell, Exinda, F5, HP, Huawei, IBM, Ipanema, Juniper, Kemp, NEC, Radware, Riverbed, Siaras, Silver Peak, Talari, VeloCloud, Viptela and others.

To purchase the report, please visit: www.infonetics.com/contact.asp

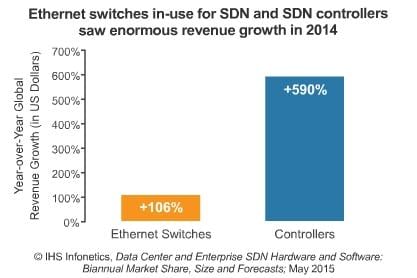

In an IHS-Infonetics report released earlier this month (June 3, 2015), Cliff forecast that the in-use software-defined networking (SDN) market (Ethernet switches and controllers) will reach $13 billion in 2019, up from $781 million in 2014, as the availability of branded bare metal switches and use of SDN by enterprises and smaller cloud service providers (CSPs) drive growth.

“The SDN market is still forming, and the top market share slots will change hands frequently, but currently the segment leaders are Dell, HP, VMware and White Box,” said Cliff Grossner, Ph.D., research director for data center, cloud and SDN at IHS.

“SDN will cross the chasm in 2016, with SDN in-use physical Ethernet switches accounting for 10 percent of Ethernet switch market revenue,” Grossner said.

SD-WAN WEBINAR:

Join analyst Cliff Grossner June 16 at 11:00 AM ET for Adopting Software-Defined WAN for Agility and Cost Savings, an event providing recommendations for buyers of new SD-WAN products and services.