Synergy Research: Ethernet Switch & Router revenues drop to 7 year low in Q1-2020

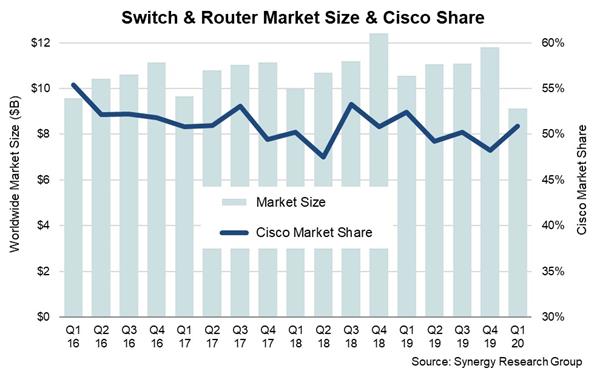

Revenues from the Ethernet switch and router market fell 14 percent to a seven-year low of $9.1 billion in Q1 2020, according to Synergy Research Group. Ethernet switches, enterprise routers and service provider routers all saw double digit declines in Q1-2020.

Ethernet switching is the largest of the three segments accounting for 62% of the total Q1 market. While GbE switches remain the largest segment in both fixed and modular Ethernet switches, the most notable feature of the market is the rapid deployment of 100 GbE and 25 GbE fixed switches. Both of these segments actually grew in the first quarter.

In Q1-2020, revenues from enterprise routers were down 15% from 2019, but on a trailing twelve month basis the market still grew thanks to strong numbers in the previous three quarters. Service Provider routers saw the biggest decline in the first quarter, down 19% from 2019. In Q1 North America remained the biggest region accounting for almost 40% of worldwide revenues, followed by APAC, EMEA and Latin America. In aggregate across all switch and router segments, year-on-year revenue declines were broadly similar across the major regions.

Comment from IEEE 802.3 Ethernet standards veteran Geoff Thompson:

Revenue is deceptive in this market which has been characterized by falling prices per function for many years. In a market where the dominant function is trunk switching and higher speeds per lane are coming on line every year that is a very difficult ride.

You have to keep the functional volume growing enough to overcome both the price erosion per transistor and the higher cost efficiency of faster lanes as well as maintain your market share in order to grow your revenue. That is very, very tough.

Cisco’s market share in switches and routers was 51% in Q1, meaning that for eight of the last twelve quarters it has been over the 50% mark. Across the three main markets, Cisco’s Q1 share was 57% for Ethernet switches, 65% for enterprise routers and 35% for service provider routers. Behind Cisco the ranking of vendors was different in each of the three markets, but in aggregate Cisco is followed by Huawei, Nokia, Juniper, Arista Networks and HPE. Beyond this leading group, other active vendors include Ericsson, Extreme, H3C and ZTE.

“In a market that is usually characterized by relative stability and predictability, the first quarter represented a sharp change from the norm, clearly as a result of COVID-19. In a pre-pandemic world we’d have expected total vendor revenues from switches and routers to have been a billion dollars higher that what we actually saw,” said John Dinsdale, a Chief Analyst at Synergy Research Group.

“On balance the Q1 hit was driven more by supply chain issues rather than by soft demand. We’d expect supply chain problems to be resolved reasonably quickly, but demand is a different story. On the service provider side demand remains robust as network traffic continues to grow, but enterprise demand will be a much spottier picture and some sectors will take several months before returning to some form of normality.”

![]()

……………………………………………………………………………………………………………………………

About Synergy Research Group

Synergy provides quarterly market sizing and segmentation data on networking, IT and cloud-related markets, including company revenues by segment and by region. Synergy Research Group ( www.srgresearch.com ) helps marketing and strategic decision makers around the world via its unique insights and in-depth analytics.

To speak to an analyst or to find out more about how to access Synergy’s market data, please contact Heather Gallo @ [email protected] or at 775-852-3330 extension 101.

Press Release:

One thought on “Synergy Research: Ethernet Switch & Router revenues drop to 7 year low in Q1-2020”

Comments are closed.

IDC on 4Q 2020 Ethernet Switch/Router Market:

The worldwide Ethernet switch market (Layer 2/3) recorded $7.6 billion in revenue in the fourth quarter of 2019 (4Q19), a decline of 2.1% year over year. For the full year 2019, the market recorded $28.8 billion in revenue for a year-over-year growth rate of 2.3%. Meanwhile, the worldwide total enterprise and service provider (SP) router market recorded $4.2 billion in revenue in 4Q19, a decrease of 7.7% on a year-over-year basis. For the full year 2019, the router market finished at $15.5 billion, essentially staying flat with an increase of 0.4% over 2018. These results are according to the International Data Corporation (IDC) Worldwide Quarterly Ethernet Switch Tracker and Worldwide Quarterly Router Tracker.

Ethernet Switch Market Highlights

From a geographic perspective, the 4Q19 Ethernet switch market recorded strong growth in the Middle East & Africa segment, which rose 10.1% year over year in 4Q19 and 9.8% for the full year 2019. The United Arab Emirates grew 10.4% in the quarter and 6.9% for the year. The Central & Eastern European region rose 5.8% year over year in 4Q19 and was up 1.7% for the full year. Poland’s market in the region rose 17.4% in the quarter and 11.7% for the full year. The Asia/Pacific (excluding Japan) (APeJ) region increased 1.6% year over year in 4Q19 and was up 1.5% for the full year 2019. The People’s Republic of China, which makes up the largest share of the region’s total, rose 5.1% in 4Q19 and 3.6% for the full year. Japan rose 8.1% in the quarter and 4.2% for 2019.

In the Western European region, the Ethernet Switching market declined 8.5% year over year in 4Q19 and was down 2.9% for the full year 2019. Germany’s market contracted 5.5% in 4Q19, while the United Kingdom was down 12.0% for the quarter and off 6.8% for the full year. The Latin America region was flat, declining 0.2% for the quarter, but was down 2.6% of the full year. Mexico’s market contracted 12.5% in the quarter and was off 4.9% for the full year. Canada’s market fell 5.5% in the quarter and was off 1.1% for the full year. In the USA, revenues were off 5.0% for the quarter, but were up a healthy 4.5% for the full year.

“The Ethernet switch and router markets showed weakness in the final quarter of 2019, driven by a variety of factors. Macro-economic issues continued to impact the global economy from the ongoing trade war between the U.S. and China to growing clarity about Brexit. While the rise and spread of the novel coronavirus, COVID-19, did not impact these 4Q19 results, it will not ease these pressures in the early part of 2020 where we expect this softness to continue,” said Rohit Mehra, vice president, Network Infrastructure at IDC. “Despite these headwinds, enterprises are still prioritizing investments in digital platforms in order to transform their businesses and keep pace with competitors, which will ultimately continue to buoy spending in the networking market over the long term.”

Growth in the Ethernet switch market continues to be driven by high speed switching platforms. 100Gb Ethernet switch revenues grew 24.7% year over year in the quarter and made up 18.3% of the market, down just slightly from 19.6% in the prior quarter. 100GbE shipments reached 5.8 million ports and $1.4 billion in revenue in 4Q19. 25GbE switch ports continue to see strong growth with port shipments rising 57.1% year over year in the quarter and up 7.4% sequentially. 10GbE port shipments grew 7.0% year over year while revenues decreased 13.0%. 10GbE made up 27.3% of all 2019 Ethernet switching revenues. Meanwhile, 1Gb remains the primary connectivity technology for enterprise campus and branch deployments, driving 1Gb port shipments to 133.6 million in 4Q19, growing 4.1% year over year, and making up 67.8% share of all ports shipped in the quarter and 40.3% of Ethernet switching revenues.

Router Market Highlights

The worldwide enterprise and service provider router market fell 7.7% year over year in 4Q19 with the larger service provider segment falling 11.7% and the enterprise portion growing 6.2%. For the full year, the combined market grew 0.4% with the service provider segment off 1.5% and the enterprise segment growing 6.9%.

The combined enterprise and service provider router market had mixed results across the world, with APeJ falling 12.4% year over year in 4Q19 and down 1.1% for the full year. Middle East & Africa increased 2.4% year over year and 7.2% annually. In the USA, which is the largest worldwide market, revenues were off 11.5% year over year and down 3.1% for the full year.

Company Highlights

Cisco’s 4Q19 Ethernet switch revenues were down 6.4% year over year giving the company a 50.9% market share. For the full year 2019, Cisco switching revenues were flat, rising 0.1% over 2018. In the hotly contested 25GbE/100GbE segment, Cisco remains the market leader with 39.7% share in 4Q19. Cisco’s combined service provider and enterprise router revenue fell 18.5% year over year in 4Q19 and was off 3.4% for the full year giving the company 37.2% share in 2019.

Huawei’s Ethernet switch revenue grew 8.9% year over year in 4Q19 and was up 7.8% in 2019 compared to 2018. This gives Huawei 9.6% market share for the full year. Huawei’s enterprise and SP router revenue fell 4.1% year over year in 4Q19 but rose 4.1% for the full year, giving the company 29.8% market share in 2019.

Arista Networks’ Ethernet switching revenue fell 11.1% year over year in 4Q19 but rose 9.8% for the full year. 100GbE revenues for Arista cooled somewhat in 4Q19 falling 19.7% compared to 3Q19. Arista’s market share in the broader Ethernet switch industry stood at 7.0% at the end of 2019, up from 6.5% year over year.

Hewlett Packard Enterprise’s (HPE) Ethernet switch revenues were off 15.9% year over year in 4Q19. This contributed to a decline of 9.1% in annual revenues in 2019, putting the company’s full-year market share at 5.4% compared to 6.1% at the end of 2018.

Juniper’s Ethernet switch revenues rose 11.7% year over year in 4Q19 but were off 7.2% for the full year. Juniper’s 4Q19 router revenues declined 4.6% year over year and were off 11.7% for the full year. The company finished 2019 with 13.2% market share in the service provider routing market, down from 14.7% in 2018.