Dell’Oro: Mobile Core Network and MEC Stagnant in 2021; Will Growth in 2022

According to a recently published report from Dell’Oro Group, the total Mobile Core Network (MCN) and Multi-access Edge Computing (MEC) market 2021 revenue growth slowed to the lowest rate since 2017. The growth rate is expected to go higher in 2022 with the expansion of the 21 commercial 5G Standalone (5G SA) MBB networks that were deployed by the end of 2021, coupled with new 5G SA networks readying to launch throughout the year.

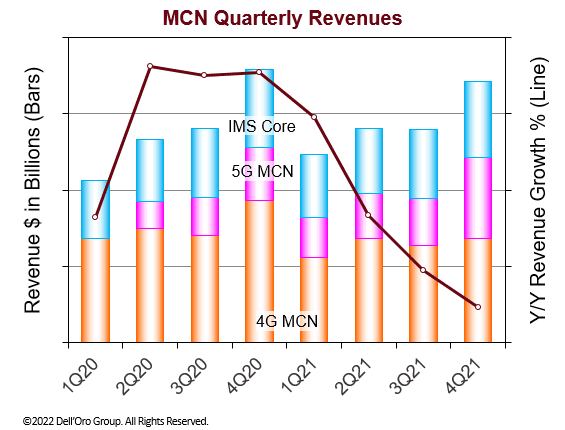

“MCN revenues for 2021 were lower than expected due to an unexpectedly poor fourth quarter performance. The revenues for 4Q 2021 were lower than in 4Q 2020. The last time that happened was in 4Q 2017,” stated Dave Bolan, Research Director at Dell’Oro Group. “The poor performance in 4Q 2021 was due to negative year-over-year revenue performance for the China region. The performance for the rest of the world was almost flat but still negative and obviously was not enough to offset the decline in China.

“The growth in 2021 came from the 5G MCN segment and was not enough to offset the decline in 4G MCN and IMS Core. Of the 21 5G SA networks commercially deployed Huawei is the packet core vendor in seven of the networks, including the three largest networks in the world located in China, and Ericsson is the packet core vendor in 10 of the networks. Not surprisingly, of the top five vendors, only Huawei and Ericsson gained overall MCN revenue market share during 2021.

“Looking at the MEC market, MEC is still a fraction of the overall MCN market, but we believe two recent announcements by Ericsson are noteworthy because, in our opinion, Ericsson will accelerate the adoption of MEC and help 5G MNOs monetize their networks by coalescing MEC implementations around the 3GPP standards. Ericsson claims to be the first to leverage recent advancements by the 3GPP standards body for edge exposure, and network slicing all the way through to a smartphone,” continued Bolan.

Additional highlights from the 4Q 2021 Mobile Core Network Report:

- Top-ranked MCN vendors based on revenue in 2021 were Huawei, Ericsson, Nokia, ZTE, and Mavenir.

- The EMEA region was the only region to grow in revenue in 2021.

- The APAC region was the largest region in revenue for 2021.

As of December 31, 2021 there were 21 known 5G SA eMBB networks commercially deployed.

|

5G SA eMBB Network Commercial Deployments |

|

|

Rain (South Africa) |

Launched in 2020 |

|

China Mobile |

|

|

China Telecom |

|

|

China Unicom |

|

|

T-Mobile (USA) AIS (Thailand) True (Thailand) |

|

|

China Mobile Hong Kong |

|

|

Vodafone (Germany) |

Launched in 2021 |

|

STC (Kuwait) |

|

|

Telefónica O2 (Germany) |

|

|

SingTel (Singapore) |

|

|

KT (Korea) |

|

|

M1 (Singapore) |

|

|

Vodafone (UK) |

|

|

Smart (Philippines) |

|

|

SoftBank (Japan) |

|

|

Rogers (Canada) |

|

|

Taiwan Mobile |

|

|

Telia (Finland) |

|

|

TPG Telecom (Australia) |

|

The Dell’Oro Group Mobile Core Network & Multi-Access Edge Computing Quarterly Report offers complete, in-depth coverage of the market with tables covering manufacturers’ revenue, shipments, and average selling prices for Evolved Packet Core, 5G Packet Core, Policy, Subscriber Data Management, and IMS Core including licenses by Non-NFV and NFV, and by geographic regions. To purchase this report, please contact us at [email protected].

References:

https://www.delloro.com/news/mobile-core-network-stagnant-in-2021-poised-for-growth-in-2022/

https://techblog.comsoc.org/2021/12/01/delloro-5g-sa-core-network-launches-accelerate-14-deployed/

One thought on “Dell’Oro: Mobile Core Network and MEC Stagnant in 2021; Will Growth in 2022”

Comments are closed.

Bullish Forecast for Edge Computing:

The global edge computing market size is projected to reach USD 155.90 billion by 2030 and register a CAGR of 38.9% from 2022 to 2030. The integration of artificial intelligence (AI) into the edge environment is expected to propel market expansion. An edge AI system can assist businesses in making quick decisions in real-time.

Key Industry Insights & Findings from the report:

The COVID-19 outbreak has bolstered the use of edge computing and data centers as more and more businesses are prioritizing the development of communications infrastructure.

Based on component, the hardware segment captured a significant revenue share in 2021 due to the increasing number of IIoT and IoT devices. Edge cloud servers must have powerful routers that are flexible and able to handle a volume of incoming traffic while maintaining low latency.

The Industrial Internet of Things (IIoT) applications segment dominated the global edge computing market in 2021 owing to the rampant digitization of services and the emergence of industry 4.0.

Based on industry vertical, the energy and utility segment accounted for a revenue share of over 15% in 2021 as a result of the rising adoption of smart grids that mandates device edge infrastructure.

Smart grids are being installed to aid alternative renewable power generation from sources such as wind and solar. Smart grids enhance operational efficiencies, including incorporation with smart appliances, real-time consumption control, and microgrids to support power generation from dispersed renewable sources.

Geographically, Asia Pacific accounted for a significant market share due to the widespread development of connected device ecosystems in countries such as India and China.

Read 254 page full market research report for more Insights, “Edge Computing Market Size, Share & Trends Analysis Report By Component, By Application, By Industry Vertical, By Region And Segment Forecasts From 2022 To 2030”, published by Million Insights.

Edge Computing Market Growth & Trends:

Moreover, the necessity to reduce privacy breaches related to the transmission of massive volumes of data, as well as latency and bandwidth limitations that restrict an organization’s data transmission capabilities, is expected to drive market growth in the forthcoming years.

Precision monitoring and machinery control are a few use cases that employ AI on the edge. A fast-moving production line needs the minimum amount of latency possible, which can be achieved by using edge computing. It can be very beneficial to move data processing close to the manufacturing facility because it can be accomplished with AI. Many different endpoint devices, including sensors, cameras, smartphones, and other Internet of Things (IoT) devices, can make use of artificial intelligence-based edge devices.

Edge computing is currently in its early phases of development. Its operating and deployment models are still in their nascent stages; nonetheless, edge computing is anticipated to present considerable growth opportunities for new entrants in the coming years. As communications infrastructure continues to be developed, demand for edge computing will increase in the years following the COVID-19 pandemic. Working from home is gradually replacing traditional office work and the telecommunications industry is making strides in the development of video conferencing software.

Prominent platforms such as Zoom and Microsoft Teams are creating new solutions to cater to the growing demand. For example, in December 2020, Amazon Web Services and SK Telecom collaborated to launch 5G MEC-based edge cloud services. Energy & utility, healthcare, agriculture, transportation & logistics, retail, telecommunication, and real estate industries are rapidly adopting edge computing as it improves application performance and results, lowers operational costs, and eliminates centralized storage and redundant transmission expenditures.

https://www.prnewswire.com/news-releases/edge-computing-market-to-be-worth-155-90-billion-by-2030-million-insights-301683681.html