5G SA/5G Core network

Optus and Ericsson achieve 180MHz across 2.3GHz and 3.5GHz bands using carrier aggregation on a live 5G SA network

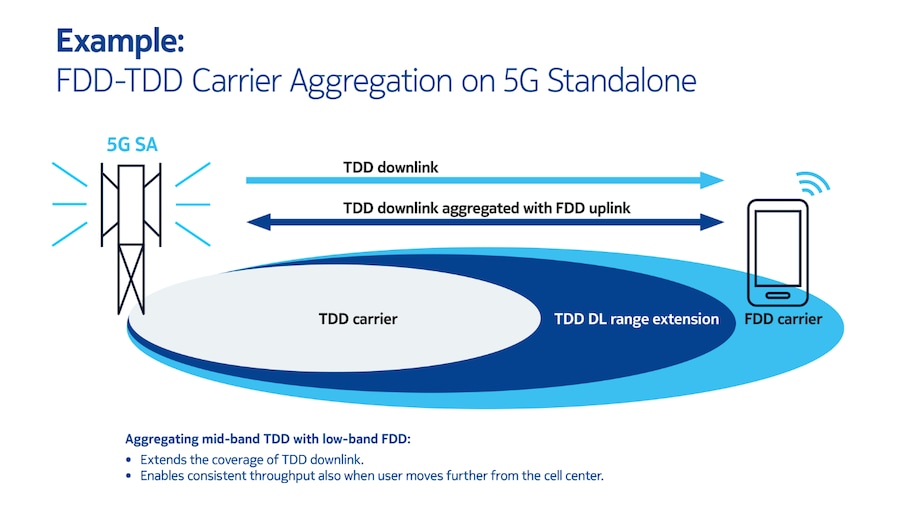

Australian telco Optus has demonstrated advanced 5G NR carrier aggregation (5G NR-CA) performance on its 5G standalone (SA) network by implementing four-component carrier aggregation (4CC CA) across low-, mid-, and upper-mid-band spectrum. Using Ericsson 5G SA network equipment and software, the configuration aggregates FDD bands at 900 MHz (Band n8) and 2.1 GHz (Band n1) with TDD bands at 2.3 GHz (Band n40) and 3.5 GHz (Band n78). Two-Component Carrier (2CC CA) uplink aggregation

This combined Optus’ unique two mid-band TDD spectrum holdings across 2.3GHz and 3.5GHz, achieving a record 180MHz TDD spectrum aggregation. In particular:

- Four-Component Carrier aggregation enabled 220MHz downlink bandwidth, leveraging spectrum across four different bands of 900MHz, 2.1GHz, 2.3GHz and 3.5GHz

- Two-Component Carrier uplink aggregation combined one Frequency Division Duplex (FDD) band from 900MHz and 2.1GHz with one TDD band from 2.3GHz and 3.5GHz

- Achieved peak speeds of 3.4Gbps (downlink) and 200Mbps (uplink) in a live network site with commercial devices, including the Samsung Galaxy S26 Ultra

The demonstration aligns with 3GPP Release 16 and Release 17 5G NR-CA enhancements (TS 38.300, TS 38.101-1/2), which extend carrier aggregation capabilities across heterogeneous duplex modes (FDD+TDD) and multiple frequency ranges within FR1. The downlink configuration leverages cross-band scheduling and advanced MIMO layers (likely up to 4×4 or higher per component carrier, depending on band support) to maximize spectral efficiency across aggregated carriers.

On the uplink, Optus and Ericsson reported 200 Mbps throughput using two-component carrier aggregation (2CC CA), combining FDD (n8/n1) and TDD (n40/n78) spectrum. This implementation is consistent with 3GPP Release 16 uplink enhancements, including uplink carrier aggregation and transmit (Tx) switching (TS 38.213), which enables efficient utilization of UE power resources across multiple uplink carriers, particularly in mixed duplex scenarios.

All results were achieved on a live commercial 5G SA network at Optus’ Sydney campus using commercial off-the-shelf (COTS) user equipment, including the Samsung Galaxy S26 Ultra. This indicates full compliance with 3GPP-defined UE capability signaling (TS 38.306) and the availability of device-side support for complex NR-CA band combinations, including inter-band and cross-duplex aggregation.

“This achievement demonstrates how we are translating cutting-edge 5G technology into meaningful benefits for customers in real-world environments. Through our ongoing collaboration with Ericsson, we are unlocking greater capacity and performance across our 5G network, enabling faster speeds and more reliable connectivity,” said Optus CTO Sri Amirthalingam. “This milestone marks an important step in our network evolution towards 5G Advanced, reinforcing our commitment to remain at the forefront of innovation and to deliver tangible value for our customers.”

Ludvig Landgren, head of Ericsson Australia and New Zealand operations said: “Optus continues to demonstrate strong leadership in adopting advanced 5G capabilities, and this milestone highlights the strength of our partnership. By expanding and combining multiple spectrum assets with Ericsson technology, we are helping Optus deliver meaningful performance improvements that translate directly into better everyday experiences for their customers.”

………………………………………………………………………………………………………………………………………………..

From a broader industry perspective, these results build on ongoing 5G NR-CA advancements. T-Mobile US has demonstrated approximately 6 Gbps downlink throughput using six aggregated carriers in FR1, as well as 550 Mbps uplink throughput leveraging uplink Tx switching across sub-6 GHz bands. In Europe, Vodafone and MediaTek achieved 277 Mbps uplink throughput using NR uplink CA, while Elisa, Ericsson, and MediaTek demonstrated 12CC aggregation reaching 8 Gbps downlink—highlighting the scalability of NR-CA as defined in 3GPP Release 17 and evolving into Release 18 (5G-Advanced).

Within Australia, Telstra has deployed Ericsson’s automated carrier aggregation (CA) optimization solution across more than 50 live 5G Advanced sites, leveraging dynamic CA configuration and traffic-aware scheduling—capabilities aligned with 3GPP Release 18 objectives for AI-assisted RAN optimization.

A notable aspect of the Optus/Ericsson demonstration is the aggregation of 180 MHz of mid-band spectrum across n40 (2.3 GHz) and n78 (3.5 GHz). While not a headline peak-rate milestone, this represents a first in terms of contiguous mid-band NR-CA deployment at this bandwidth scale. Mid-band aggregation is particularly significant within the 3.3–4.2 GHz “golden band” range defined in global 5G spectrum harmonization efforts, as it offers an optimal balance between coverage and capacity.

Operationally, this configuration is expected to deliver immediate gains in high-traffic scenarios—such as dense urban environments, transport hubs, and large venues—by increasing available cell throughput and improving user-level quality of service (QoS). Furthermore, the expanded mid-band capacity directly benefits fixed wireless access (FWA) deployments, where sustained throughput and cell-edge performance are critical. Because the demonstrated CA combinations are already supported by commercial UE categories, deployment can proceed without requiring new device classes, accelerating time-to-impact.

Ericsson was recently selected to modernize and expand SoftBank’s core networks, as well as accelerate the Japanese giant’s 5G SA adoption. Expanding on a previous 5G SA deal centered around its radio access network (RAN) products, Ericsson is providing SoftBank with its Core Networks’ portfolio, including a dual-mode 5G Core solution running on Ericsson’s Cloud Native Infrastructure Solution (CNIS).

……………………………………………………………………………………………………………………………..

References:

https://www.sdxcentral.com/news/ericsson-and-optus-claim-5g-sa-world-first/

https://www.ericsson.com/en/press-releases/7/2026/optus-and-ericsson-trial-ai-to-boost-5g-downlink

https://www.nokia.com/mobile-networks/ran/carrier-aggregation/5g-carrier-aggregation-explained/

China Unicom-Beijing and Huawei build “5.5G network” using 3 component carrier aggregation (3CC)

Nokia, BT Group & Qualcomm achieve enhanced 5G SA downlink speeds using 5G Carrier Aggregation with 5 Component Carriers

Finland’s Elisa, Ericsson and Qualcomm test uplink carrier aggregation on 5G SA network

T-Mobile US, Ericsson, and Qualcomm test 5G carrier aggregation with 6 component carriers

Ericsson and MediaTek set new 5G uplink speed record using Uplink Carrier Aggregation

BT tests 4CC Carrier Aggregation over a standalone 5G network using Nokia equipment

T-Mobile US achieves speeds over 3 Gbps using 5G Carrier Aggregation on its 5G SA network

GSA: 5G Non Terrestrial Networks, 5G SA and 5G Advanced gain momentum

5G NTNs:

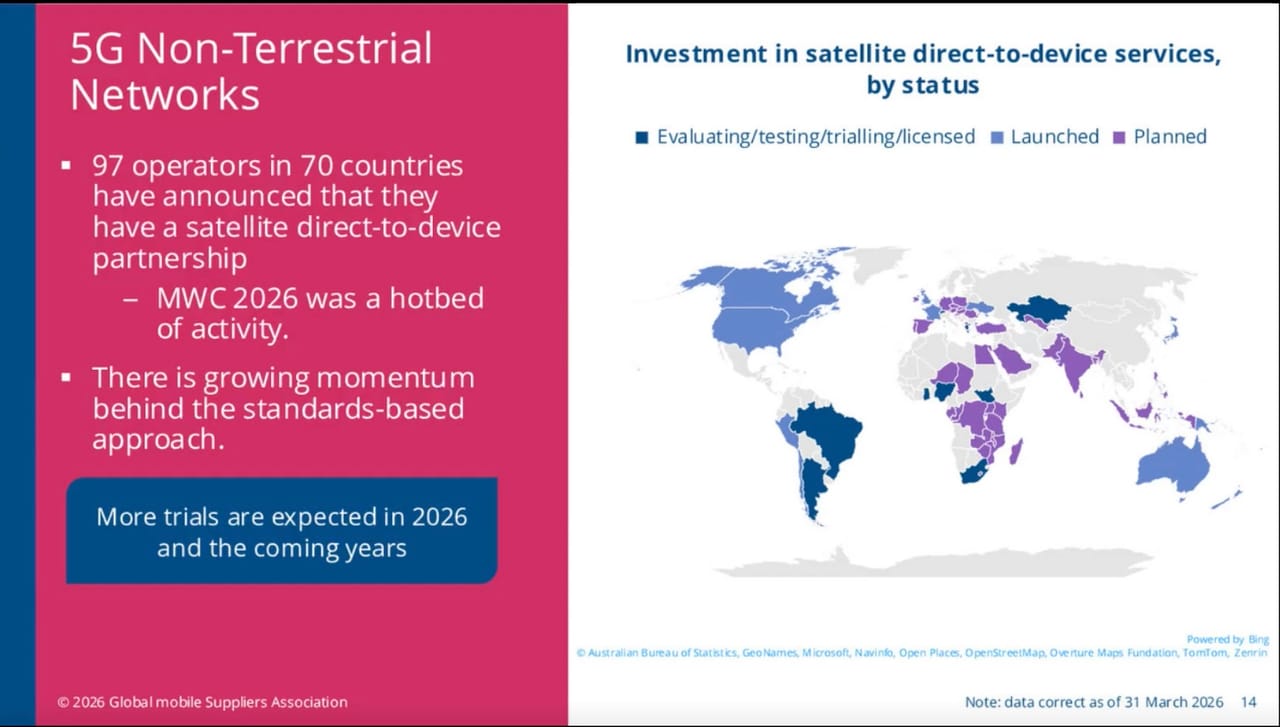

During an April 16th webinar titled “GSA Snapshot: 5G networks, spectrum & devices,” Joe Gardiner, market analyst at CCS Insight and a member of the GSA research team, said GSA data through March 31st reveal that 97 operators in 70 countries have announced they are investing in LEO satellite D2D technology.

“There’s a lot of interest in this area, but there’s also a lot of interest and movement towards 3GPP standards (see Note below), and the convergence of the terrestrial and the non-terrestrial standards map” starting with 3GPP Release 17, Gardiner observed.

Skylo, for example, is following a standards-based approach and already has D2D partnerships with operators such as Orange in France, Verizon and Vodafone IoT.

“Other players are [also] looking to use the standards-based approach, and looking to purchase the spectrum that’s compatible with the standards,” Gardiner said.

Note that 3GPP is not a SDO- it depends on ETSI and ITU-R to rubber stamp its specs and transpose them into official standards.

Image credit: GSA

He said that “Part of the reason Amazon is acquiring satellite Globalstar, was because of the spectrum assets that Globalstar has.” Gardiner added that a “lot of trials are taking place that are looking at the next stage of the standards, Release 18 with 5G NR NTN services.”

Gardiner referenced the trial announced by the European Space Agency (ESA), together with Airbus Defence and Space, Eutelsat OneWeb, and industry partners in November 2025.

In addition, Spain’s Sateliot is following the standards-based approach and has launched a Series C financing round to raise €100 million (US$117 million) to help fund the deployment its IoT-focused 5G satellite constellation. “We expect more trials like this to take place over the next few months and years,” Gardiner said. There is a “movement towards using mobile satellite services (MSS) spectrum,” although the drawback with this spectrum is the current lack of compatible mobile devices on the market.

……………………………………………………………………………………………………………………..

5G SA and 5G Advanced:

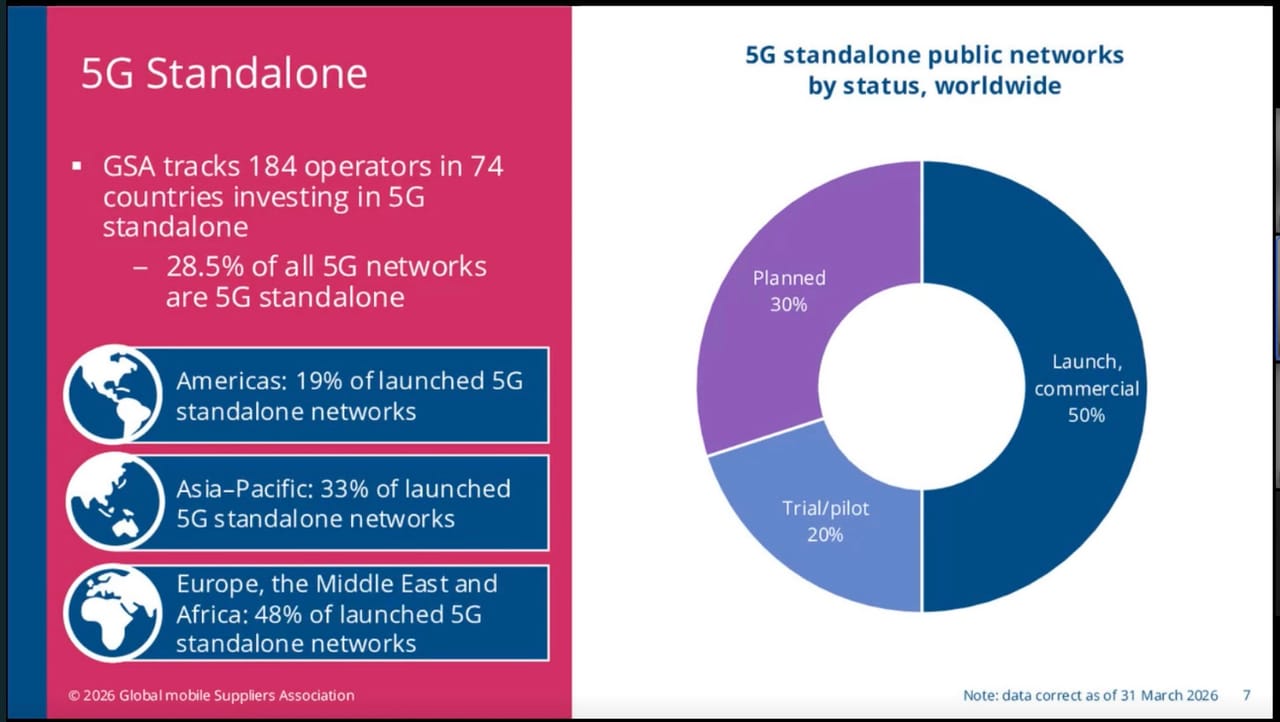

Ian Fogg, a research director at CCS Insight, who also works within the research team at the GSA, talked up the move towards 5G standalone (SA) and 5G Advanced networks.

“Globally, we have 184 operators in 74 countries investing in 5G standalone. This is publicly. 28.5% of all 5G networks are now 5G standalone. So there’s real momentum happening here,” Fogg said.

Source: GSA

5G Advanced “is something that’s happening at the moment. We have 36 operators globally publicly saying they’re investing in 5G Advanced. We’ve seen eleven 5G Advanced networks commercially launched,” Fogg said, citing activity in China, Canada, Japan, Kuwait and Vietnam.

“I think what will happen in the next few years is we’ll see the gap between an operator adopting 5G standalone and 5G Advanced narrowing, because if you go to 5G standalone, it’s a natural thing to move fairly quickly on to 5G Advanced, if possible, because you get a lot more capabilities once you’re on a 5G advanced network,” he added.

………………………………………………………………………………………………………………

References:

https://gsacom.com/webinar/5g-networks-spectrum-devices/

Orange set to claim European satellite first

Skylo’s trajectory toward the ‘standardized sky’ looks to include multiple orbits

MWC2026: Skylo makes universal connectivity a reality; Vodafone IoT teams with Skylo for satellite connectivity

Non-Terrestrial Networks (NTNs): market, specifications & standards in 3GPP and ITU-R

ITU-R recommendation IMT-2020-SAT.SPECS from ITU-R WP 5B to be based on 3GPP 5G NR-NTN and IoT-NTN (from Release 17 & 18)

Analysis: Amazon <- Globalstar – a strategic move for D2D and spectrum parity

Enterprise IoT and the Transformation of UK Telecom Business Models – Part 1

From LPWAN to Hybrid Networks: Satellite and NTN as Enablers of Enterprise IoT – Part 2

Keysight Technologies Demonstrates 3GPP Rel-19 NR-NTN Connectivity in Band n252

Telecoms.com’s survey: 5G NTNs to highlight service reliability and network redundancy

Dell’Oro: Mobile Core Networks +15% in 2025; Ookla: Global Reality Check on 5G SA and 5G Advanced in 2026

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

Dell’Oro: RAN market stable, Mobile Core Network market +14% Y/Y with 72 5G SA core networks deployed

AT&T deploys nationwide 5G SA while Verizon lags and T-Mobile leads

The Financial Trap of Autonomous Networks: Scaling Agentic AI in the Telecom Core

By Pavan Madduri with Ajay Lotan Thakur

The telecom industry wants autonomous, self-healing networks, but nobody is looking at the GPU bill. Running Agentic AI 24/7 “just in case” will bankrupt your IT department and ruin your ESG goals. The only way to survive the autonomous era is ruthless, event-driven orchestration that scales cognitive compute to absolute zero.

Introduction – The Compute Crisis:

The Compute Crisis Nobody is Talking About

Everyone in telecom right now is obsessed with “self-healing” autonomous networks. The vendor pitch sounds amazing. Just drop in some Agentic AI, let it watch your data plane, and watch it fix anomalies without a human ever touching a keyboard. But there’s a massive trap hiding underneath all that hype, and enterprise architects are completely ignoring it. It comes down to the raw physics of AI compute.

Unlike your standard microservices, which just run deterministic, compiled code on cheap CPU cycles, Agentic AI needs massive foundation models. To actually reason through a network failure, these models have to load gigabytes of weights into Video RAM and generate tokens. You need dedicated GPUs for this. We aren’t talking about cheap, stateless API calls here. These are the most expensive, power-hungry workloads in your entire datacenter.

If a telco tries to run an autonomous core the old-fashioned way by keeping high-end GPU nodes spinning 24/7 just in case a BGP route flaps, their cloud bill is going to wipe out any operational savings the AI was supposed to deliver.

The reality is that autonomy is no longer just a software problem. It’s a financial one. The telcos that actually win will not be the ones with the smartest AI. They will be the ones who figure out how to build a strict “scale-to-zero” environment. They need to spin up that expensive cognitive compute exactly when it is needed, and kill it the exact second the job is done.

Why Traditional Auto-scaling is Broken for AI:

When platform engineers first see the compute costs of running these AI agents, their first instinct is usually just to slap standard Kubernetes Horizontal Pod Autoscaling (HPA) on the cluster and call it a day. But standard HPA was built for stateless web servers, not massive cognitive engines. If you try to use it for Agentic AI in a telecom core, you’re going to fail for two big reasons.

The Cold-Start Penalty: Traditional autoscaling is entirely reactive. It sits around waiting for a CPU to hit 80% before it decides to scale up. In telecom, SLAs are measured in sub-milliseconds. If you wait for an anomaly to spike your CPU, then provision a new GPU node, pull a massive AI container image, and load the model weights into VRAM, you are talking about minutes of delay. By the time your AI agent actually wakes up to fix the problem, you have already breached your SLA.

CPU Utilization is a Liar: For AI workloads, standard hardware metrics are completely misleading. A GPU could be pegged at 90% utilization just thinking through a minor log warning, while a massive, critical network failure is stuck waiting in the queue. If your scaling logic is tied to hardware metrics instead of the actual severity of the event queue, you are just going to burn budget scaling blindly.

We have to abandon reactive resource metrics entirely and move to event-driven orchestration.

The Fix – Event-Driven Orchestration:

If standard HPA is broken for this, what is the fix? You have to completely decouple the infrastructure from the workload using strict, event-driven orchestration.

Instead of keeping baseline infrastructure running just to maintain a state, you treat cognitive compute as 100% ephemeral. You don’t scale based on how hard the CPU is working. You scale based on the exact depth and severity of the anomaly queue.

To actually build this, architects need purpose-built event-driven scalers like KEDA (Kubernetes Event-driven Autoscaling). KEDA lets your cluster completely bypass those reactive hardware metrics and listen directly to the network’s data plane.

But how do you avoid the cold-start latency of booting a fresh GPU pod? KEDA solves this by reacting to the event queue length itself rather than waiting for an existing pod’s CPU to max out. By the time a traditional HPA notices a CPU spike, the system is already overwhelmed. (To solve this exact issue in production, I open-sourced a custom KEDA scaler specifically designed to scrape and react to native GPU metrics, allowing the orchestrator to scale cognitive workloads preemptively. You can view the architecture on [GitHub])

KEDA intercepts the telemetry trigger at the source. When paired with a warm pool of paused GPU nodes and pre-pulled container images, KEDA can scale a pod from zero to active in milliseconds. The infrastructure is anticipating the load based on the queue, not reacting to the stress of it.

Here is what the workflow actually looks like when you do it right:

- The Trigger: Telemetry picks up a severe anomaly ,like a sudden 5G slice degradation, and pushes an event straight to a message broker like Kafka.

- The Scale-Up: KEDA intercepts that exact metric and instantly provisions a dedicated, GPU-backed AI pod from a warm standby pool.

- The Execution: The Agentic AI loads into VRAM, figures out the blast radius of the anomaly, and executes a fix. This is usually by reconciling the state through a GitOps controller.

- The Kill Switch: The absolute millisecond that the event queue clears and the network is stable, the orchestrator aggressively terminates the pod and gives the GPU back to the node pool.

You only pay the premium GPU tax during moments of active reasoning. The 24/7 idle tax is gone.

Architecting the Scale-to-Zero Core:

To make this scale-to-zero dream a reality, you have to fundamentally change how you handle network observability. The biggest mistake I see architects make is tightly coupling their monitoring tools with their AI execution layer. If your observability stack is running on the same hardware as your AI engine, you are literally wasting premium GPU compute just to watch logs.

You need a strict, physical separation of concerns:

The Watchers (The Lightweight Control Plane):

Your network data plane needs to be monitored by lightweight, CPU-efficient edge collectors like Prometheus or OpenTelemetry. These sit right at the edge, continuously eating millions of telemetry data points and BGP state changes. Because they don’t do any complex reasoning, they run incredibly cheap on standard CPU nodes.

The Thinkers (The Heavyweight Execution Plane):

Your expensive AI models are completely isolated in a separate, GPU-backed node pool that literally defaults to zero instances.

When the Watchers spot an anomaly, they don’t try to fix it. They just fire an alert to KEDA. KEDA then wakes up the Thinkers, spinning up the exact number of GPU pods needed to handle that specific blast radius. By decoupling the watchers from the thinkers, you guarantee that not a single cycle of GPU compute is wasted on baseline monitoring.

The Bottom Line:

Autonomous telecom networks are going to happen. But trying to brute-force the infrastructure provisioning is a fast track to bankrupting your IT department. The smartest Agentic AI in the world is useless if you can’t afford the cloud bill to run it.

Furthermore, this isn’t just about protecting the IT budget. Running idle GPUs 24/7 creates a massive, unnecessary carbon footprint. By enforcing a scale-to-zero architecture, telcos can drastically reduce the energy consumption of their autonomous networks, turning a massive ESG liability into a sustainable operational model.

Autonomy is no longer just a software engineering problem. It is an infrastructure balancing act. If Agentic AI is going to survive in the telecom core, we have to ditch legacy threshold scaling and embrace strict, event-driven orchestration.

Tools like KEDA give us the ability to build networks that are both cognitively brilliant and financially ruthless. We can spin up massive intelligence at the exact millisecond of failure and scale right back to zero the moment the network is healed.

References and Further Reading:

- Unlocking Energy Saving in Telecom Networks: A Path to a Sustainable Future – A deep dive into the operational and ESG mandates driving energy efficiency in modern telecom infrastructure.

- KEDA Documentation: Kubernetes Event-driven Autoscaling – Technical specifications for decoupling workload scaling from standard CPU/Memory metrics.

- keda-gpu-scaler – An open-source custom KEDA scaler I developed to enable event-driven autoscaling specifically tied to native GPU telemetry and queue depth.

Building and Operating a Cloud Native 5G SA Core Network

How Network Repository Function Plays a Critical Role in Cloud Native 5G SA Network

HPE Aruba Launches “Cloud Native” Private 5G Network with 4G/5G Small Cell Radios

…………………………………………………………………………………………….

About the Author:

Pavan Madduri is a Cloud-Native Architect, CNCF Golden Kubestronaut, and active IEEE researcher specializing in enterprise infrastructure automation, Agentic SREs, and Kubernetes networking. He designs scalable, zero-trust cloud environments and frequently writes about the intersection of AI governance and cloud-native infrastructure.

Connect with Pavan Madduri on [LinkedIn] .

Disclaimer: The author acknowledges the use of AI-assisted tools for structural formatting, language refinement, and copyediting during the drafting of this article. The core architectural concepts, technical opinions, and engineering strategies remain entirely original.

Telco investments in mobile core networks surge 83% in 2025-Q4, but what about ROI?

According to new data from market research firm Omdia (owned by Informa), 2025 Q4 investments 5G SA Core networks surged 83% year-over-year. For OEMs, this uptick suggests a pivot away from the stagnant 5G Standalone (SA) momentum of recent years. Omdia identified North America and EMEA as the primary growth engines for the quarter. “The surge in 5G core investment underscores CSPs’ strategic focus on enabling new revenue streams and digital transformation,” said Roberto Kompany, Principal Analyst Mobile Infrastructure at Omdia, in a statement. “This momentum is reflected in AT&T’s nationwide 5G SA and RedCap deployment and Verizon’s launch of a new enterprise-grade fixed wireless access (FWA) slice,” he said.

Ookla and Omdia recently noted accelerating 5G SA adoption in Europe, but the region continues to trail global leaders due to its low baseline. Spain remains a standout exception. Telefónica recently achieved a domestic milestone by deploying 5G SA in-building coverage via a Vantage Towers DAS, and has partnered with Airbus Helicopters to integrate 5G SA into manned and unmanned rotary-wing platforms for the Spanish armed forces. Despite broader deployments in the UK and Germany, a significant performance gap remains.

The GCC region ( Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the UAE.) currently delivers median 5G SA download speeds up to five times faster than European averages. This disparity highlights a capability gap rather than a coverage issue between mature and emerging markets. The industry footprint is expanding, with Omdia reporting 88 commercial 5G SA deployments to date—a notable increase from the 72 reported by Dell’Oro in late 2025.

…………………………………………………………………………………………………………………………………………………………………………………………….

While Dell’Oro confirms the 5G SA Core market growth, it emphasized that subscriber migration and active utilization, rather than just “flags in the ground,” are the true long-term drivers for infrastructure spend. For the first time, the 5G Mobile Core Network (MCN) market accounted for 50 percent share of the total MCN market.

“In 2025, the MCN market recorded its highest year-over-year revenue growth rate since 2014,” stated Dave Bolan, Research Director at Dell’Oro Group. “This was driven by record-setting growth rates in all market segments: 4G MCN (highest since 2019), 5G MCN (highest since 2022), and Voice Core (highest since 2007). 4G MCN gains came from Caribbean and Latin America (CALA) and Europe, Middle East, Africa (EMEA) regions; 5G MCN from all regions; and Voice Core, primarily from Asia Pacific and EMEA regions.

“5G MCNs led the way in 2025 growth, as 5G Standalone (5G SA) networks reached an inflection point and moved towards mass market appeal, as more 5G SA networks expand in population coverage in urban, suburban, and rural areas. Voice Core was the next major contributor to growth in 2025, driven by planned 3G MCN shutdowns, which required upgrades from Circuit Switched Core to IMS Core, and IMS Core modernization to a cloud-native IMS Core for VoNR in 5G SA networks. Meanwhile, 4G MCNs expanded due to subscriber growth in Africa and South America,” added Bolan.

Looking ahead, Omdia forecasts sustained double-digit growth for 5G Core investments through 2026, fueled by the requirement for nationwide service parity and increased network capacity. This outlook favors the leading 5G Core vendors—Huawei, Ericsson, and Nokia—who currently maintain the highest market shares.

……………………………………………………………………………………………………………………………………………………………………………………………

ROI for 5G SA Core Networks?

The return on investment (ROI) for 5G Standalone (SA) core networks is currently at a critical inflection point. While initial years were marked by “bemoaning” slow momentum, 2025 and 2026 have seen a shift from pilot testing to an execution-driven phase with measurable, albeit varied, returns. In the 2025–2026 market, enterprise ROI for 5G Standalone (SA) is primarily driven by three high-growth segments: Private 5G Networks, RedCap IoT, and Network Slicing. While public 5G consumer returns remain steady, these B2B use cases are where Mobile Network Operators (MNOs) are finding the most immediate “killer applications.”

- Operational Efficiency: 5G SA cores are cloud-native, allowing for microservices that can be deployed in hours rather than days. This reduces long-term operational costs (OpEx) by automating network functions and improving energy efficiency per gigabyte transmitted.

- New Revenue Streams: Unlike 5G Non-Standalone (NSA), the SA core enables Network Slicing and Ultra-Reliable Low-Latency Communications (URLLC). These are essential for high-margin B2B services like industrial robotics, emergency services, and “SuperMobile” slicing for enterprises.

- Monetization of “Capability”: In regions like the GCC (Gulf Cooperation Council), 5G SA delivers speeds up to five times faster than European averages, allowing operators to charge for performance-based tiers rather than just data volume.

- Consumer Benefits: Early data from the UK indicates that 5G SA can extend device battery life by 11% to 22% due to its unified control plane, creating a tangible value proposition for premium consumer plans.

- The “Value Perception Gap”: Despite nationwide rollouts, some operators (like AT&T in late 2025) saw mobile service revenue grow by only 3.4%, barely outpacing inflation.

- Regional Disparity: ROI is strongest in North America and China, where industrial policy and sovereign wealth have accelerated deployment. In contrast, Europe faces a “regulatory quagmire” and higher costs for removing legacy equipment, slowing its path to profitability.

- The 6G Factor: Some operators are hesitant to invest billions in a full 5G SA overhaul if the technology is viewed as a “transitional” generation that may be superseded by 6G-ready cores in the late 2020s.

References:

https://www.telecoms.com/5g-6g/telcos-spend-more-on-the-core-as-5g-sa-picks-up

https://www.linkedin.com/pulse/february-newsletter-4q25-fy25-wireless-infrastructure-update-ug9ec/

Dell’Oro: Mobile Core Networks +15% in 2025; Ookla: Global Reality Check on 5G SA and 5G Advanced in 2026

Dell’Oro: RAN market stable, Mobile Core Network market +14% Y/Y with 72 5G SA core networks deployed

Dell’Oro: RAN market stable, Mobile Core Network market +14% Y/Y with 72 5G SA core networks deployed

Téral Research: 5G SA core network deployments accelerate after a very slow start

Analysts: Telco CAPEX crash looks to continue: mobile core network, RAN, and optical all expected to decline

Building and Operating a Cloud Native 5G SA Core Network

MCN Market Roared Back in 2025 With 15 Percent Growth, According to Dell’Oro Group

Nokia to showcase agentic AI network slicing; Ericsson partners with Ookla to measure 5G network slicing performance

Executive Summary:

Today, Nokia announced a strategic collaboration with Amazon (AWS), Du, and Orange to debut an industry-first agentic AI-driven network slicing [1.] capability on a 5G SA core network. Du and Orange will deploy this new technology which uses Nokia’s 5G AirScale base stations, MantaRay SMO and Agentic AI modules in tandem with Amazon’s Bedrock Artificial Intelligence platform. Autonomous AI agents are used to ingest and process real-time telemetry—including geospatial data, event triggers, and traffic patterns—the framework enables adaptive network slicing. This architecture allows communications service providers (CSPs) to dynamically orchestrate resources in response to fluctuating demand, such as prioritizing mission-critical throughput for first responders during emergency incidents.

Note 1. There are no ITU standards for network slicing or the 5G SA Core network required to implement that capability. 3GPP specifications define end-to-end network slicing architecture, covering slice management (TS 28.552, TS 28.554), service requirements, and security (NSSAA – Network Slice Specific Authentication and Authorization). The NSA and CISA have released specific, recognized guidance on designing, deploying, and maintaining secure 5G standalone (SA) network slices. ETSI publishes and adopts 3GPP technical specifications (specifically the 28-series) as European standards for network slicing management, including 5G RAN, core network, and NFV-MANO architecture. ETSI, as a 3GPP partner, ensures these specifications cover the lifecycle of network slices.

…………………………………………………………………………………………………………………………………………………………………………………………..

- Data Ingestion & Inference: Agentic AI modules, hosted on Amazon Bedrock, ingest real-world contextual data (e.g., emergency alerts, traffic sensors, weather) alongside live network KPIs.

- Intent-Based Policy Generation: The AI agents analyze this telemetry to determine the optimal network configuration required to meet specific Service Level Agreements (SLAs) or emergency “intents'”

- NEF & SMO Integration: These high-level intents are translated into actionable policies and pushed to Nokia’s MantaRay SMO (Service Management and Orchestration).

- Dynamic RAN/Core Adjustment: The Network Exposure Function (NEF) acts as the secure gateway, allowing the AI agents to interface with the 5G Core. It exposes network capabilities so the agents can dynamically adjust RAN policies and resource allocation across the 5G AirScale base stations.

- Autonomous Feedback Loop: The system operates in an autonomous mode where agents continuously monitor the results of their adjustments, performing forensic analysis to refine slicing parameters in real-time.

Nokia will host live technical demonstrations of this AI network slicing capability at its 2026 Mobile World Congress (MWC) Barcelona exhibit.

Quotes:

“This innovation marks a major milestone in the evolution of AI-native networks,” said Pallavi Mahajan, Chief Technology and AI Officer at Nokia. “By combining Nokia’s advanced network slicing capabilities with agentic AI, we are enabling operators to deliver premium, intent-based services that adapt dynamically to real-world conditions. Nokia is advancing connectivity by unlocking new value streams for telecommunication providers and supporting next-generation applications and differentiated services for enterprises, industries and consumers.”

Amir Rao, Global Director, GTM & Telco Solutions at AWS added: “Network slicing has long promised to unlock new revenue streams for operators, but manual configuration and static policies have prevented end customers from accessing on-demand provisioning. By integrating agentic AI capabilities through Amazon Bedrock with Nokia’s application, operators can now deliver intelligent, context-aware network slicing that responds dynamically to real-world conditions from traffic surges to emergency situations. This transforms network slicing from a technical capability into a true business enabler, allowing operators to monetize their 5G investments through differentiated, premium services that adapt automatically to customer needs. Agentic Network Slicing is the beginning of an era that will enable telecommunications providers to enable real-time intent-based service provisioning for end customers.”

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Competitive Network Slicing Solution:

Rival wireless equipment vendor Ericsson yesterday gave a preview of a network slicing related offering which it will be demonstrating at the 2026 MWC. Together with Ookla it has developed a specialized test version of its Speedtest app designed to measure and validate 5G network slicing performance. The tool enables the Speedtest app to identify and test specific network slices, which apparently demonstrates how Service Level Agreements (SLAs) for differentiated services can be verified in real-time by consumers and service providers.

Ericsson reported in its latest Mobility report that there were 65 commercial network slicing services worldwide providing so-called “differentiated connectivity” offerings. That’s out of a total of 118 network slicing cases discovered by Ericsson’s researchers. Yet in the UK, none of the three mobile network operators have launched a commercial 5G network slicing capability yet. According to Ofcom’s latest Connected Nations report, 5G SA is available across 83% of outside areas in the country and 5G SA accounts for nearly one-third of 5G traffic. However, 4G accounts for 72% of total monthly data traffic.

“Network slicing is no longer a future concept; it is a commercial reality. However, you cannot manage what you cannot measure,” said Tibor Rathonyi, Senior Advisor at Ookla. “Our work with Ericsson is a pivotal first step in providing the transparency needed to prove the value of these premium 5G services to both consumers and enterprises.”

Philipp Bichsel, Executive Vice President Mobile Network & Services at Swisscom, said: “Swisscom has retained the title as the country’s best-performing mobile network over many years by truly prioritizing the delivery of the best possible customer experience. This has meant embarking on a journey to fully exploit automation to enhance reliability and efficiency without compromising the service quality our customers expect. As we advance towards self-learning, autonomous networks, enabling Swisscom to build smarter and more adaptive network operations, we are leveraging the SMO framework as the foundation for this evolution. Within this framework, partner solutions such as Ericsson’s Intelligent Automation Platform and its ecosystem of rApps play an important role in helping us explore the potential of AI driven automation.”

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

References:

https://www.telecoms.com/5g-6g/nokia-and-aws-show-off-agentic-ai-powered-5g-advanced-network-slicing

https://www.telecoms.com/5g-6g/ericsson-and-ookla-launch-network-slicing-measurement-tool

https://www.lightreading.com/5g/eurobites-network-slicing-enjoying-a-moment-finds-ericsson-report

https://www.ericsson.com/en/reports-and-papers/mobility-report/reports/november-2025

https://www.lightreading.com/5g/5g-network-slicing-not-ready-for-prime-time-in-uk

https://www.awardsolutions.com/portal/resources/network-slicing

ABI Research: 5G network slicing market to hit $67.52 billion in 2030 with Asia Pacific in the lead

5G network slicing progress report with a look ahead to 2025

FCC Draft Net Neutrality Order reclassifies broadband access; leaves 5G network slicing unresolved

Telstra achieves 340 Mbps uplink over 5G SA; Deploys dynamic network slicing from Ericsson

ABI Research: 5G Network Slicing Market Slows; T-Mobile says “it’s time to unleash Network Slicing”

Ericsson, Intel and Microsoft demo 5G network slicing on a Windows laptop in Sweden

Ericsson and Nokia demonstrate 5G Network Slicing on Google Pixel 6 Pro phones running Android 13 mobile OS

Nokia and Safaricom complete Africa’s first Fixed Wireless Access (FWA) 5G network slicing trial

Is 5G network slicing dead before arrival? Replaced by private 5G?

5G Network Slicing Tutorial + Ericsson releases 5G RAN slicing software

Dell’Oro: Mobile Core Networks +15% in 2025; Ookla: Global Reality Check on 5G SA and 5G Advanced in 2026

A recent Dell’Oro market research report estimates that 4G/5G Mobile Core Network (MCN) revenues rose 15% YoY in 2025, which was the fastest growth since 2014. For the first time, the 5G MCN market accounted for 50% share of the total MCN market.

Editor’s Note: The 4G and 5G Non Standalone (NSA) mobile core network market (Evolved Packet Core) is experiencing long-term decline as investments are finally shifting toward 5G standalone (SA) networks.

“In 2025, the MCN market recorded its highest year-over-year revenue growth rate since 2014,” stated Dave Bolan, Research Director at Dell’Oro Group. “This was driven by record-setting growth rates in all market segments: 4G MCN (highest since 2019), 5G MCN (highest since 2022), and Voice Core (highest since 2007). 4G MCN gains came from Caribbean and Latin America (CALA) and Europe, Middle East, Africa (EMEA) regions; 5G MCN from all regions; and Voice Core, primarily from Asia Pacific and EMEA regions.

“5G MCNs led the way in 2025 growth, as 5G Standalone (5G SA) networks reached an inflection point and moved towards mass market appeal, as more 5G SA networks expand in population coverage in urban, suburban, and rural areas. Voice Core was the next major contributor to growth in 2025, driven by planned 3G MCN shutdowns, which required upgrades from Circuit Switched Core to IMS Core, and IMS Core modernization to a cloud-native IMS Core for VoNR in 5G SA networks. Meanwhile, 4G MCNs expanded due to subscriber growth in Africa and South America,” added Bolan.

Additional highlights from the 4Q 2025 Mobile Core Network and Multi-Access Edge Computing Report include:

- The top four vendors (Huawei, Ericsson, Nokia, and ZTE) posted very strong growth rates in 2025. Collectively, they accounted for about the same amount of market share as in 2024.

- The Multi-access and Edge Computing (MEC) market segment (a subsegment of the 5G MCN market) attained the highest growth rate of any MCN segment in 2025, with the China region remaining the dominant region for MEC implementations.

- Standard-setting bodies, vendors, and Mobile Network Operators (MNOs) communities are collaborating to expand the ecosystem with new products, applications, and monetization features that are expected to deliver future benefits.

- Examples include RedCap radios, which reduce the cost of IoT devices for consumer wearables and industrial applications; network slicing for both mission-critical and on-demand applications; IMS data channels to increase monetization opportunities and enhance user experience; and Open APIs that enable developers to scale their applications across all MNOs, attracting the app development community.

- Agentic AI is expected to change data traffic patterns and alter the duration that subscribers remain connected to the network as agents operate on their behalf. This could represent a paradigm shift in the future, requiring increased MCN capacity, expanded vendor opportunities, and enhanced monetization for MNOs through pricing tiers.

The Dell’Oro Group Mobile Core Network & Multi-Access Edge Computing Quarterly Report offers complete, in-depth coverage of the market with tables covering manufacturers’ revenue, shipments, and average selling prices for Traditional Packet Core, Evolved Packet Core, 5G Packet Core, Policy, Subscriber Data Management, Signaling, Circuit Switched Core, and IMS Core by geographic regions. To purchase this report, please contact us at [email protected].

…………………………………………………………………………………………………………………………………………………………………………………………………..

Related: The second edition of Ookla and Omdia’s report on the global state of 5G Standalone core network confirms that the technology has moved beyond launch announcements into an execution-driven phase. By the close of 2025, the “coverage gap” between major economic blocs had narrowed, but a more consequential “capability gap” has emerged, reflecting divergent spectrum strategies, investment depth, and the extent to which operators have moved beyond baseline SA deployment toward end-to-end network optimization.

For government and regulatory bodies, 5G Standalone (SA) has evolved into a high-stakes strategic imperative. The intersection of national competitiveness, digital sovereignty, and AI readiness is fundamentally reshaping Capex priorities across Tier-1 markets.

- User Equipment (UE) Performance: Impact of 5G SA on battery life and the transition to Voice over New Radio (VoNR).

- Application-Layer QoE: Benchmarking latency and jitter for cloud-native and gaming infrastructure.

- Commercial Monetization: A review of the first commercial deployments of Network Slicing, Enterprise SLAs, and 5G-Advanced (Release 18) segmentation.

- Geopolitical Drivers: Assessing how sovereign AI strategies in the GCC and legislative shifts in Europe are dictating the global SA evolutionary path.

……………………………………………………………………………………………………………………………………………………………………………………………..

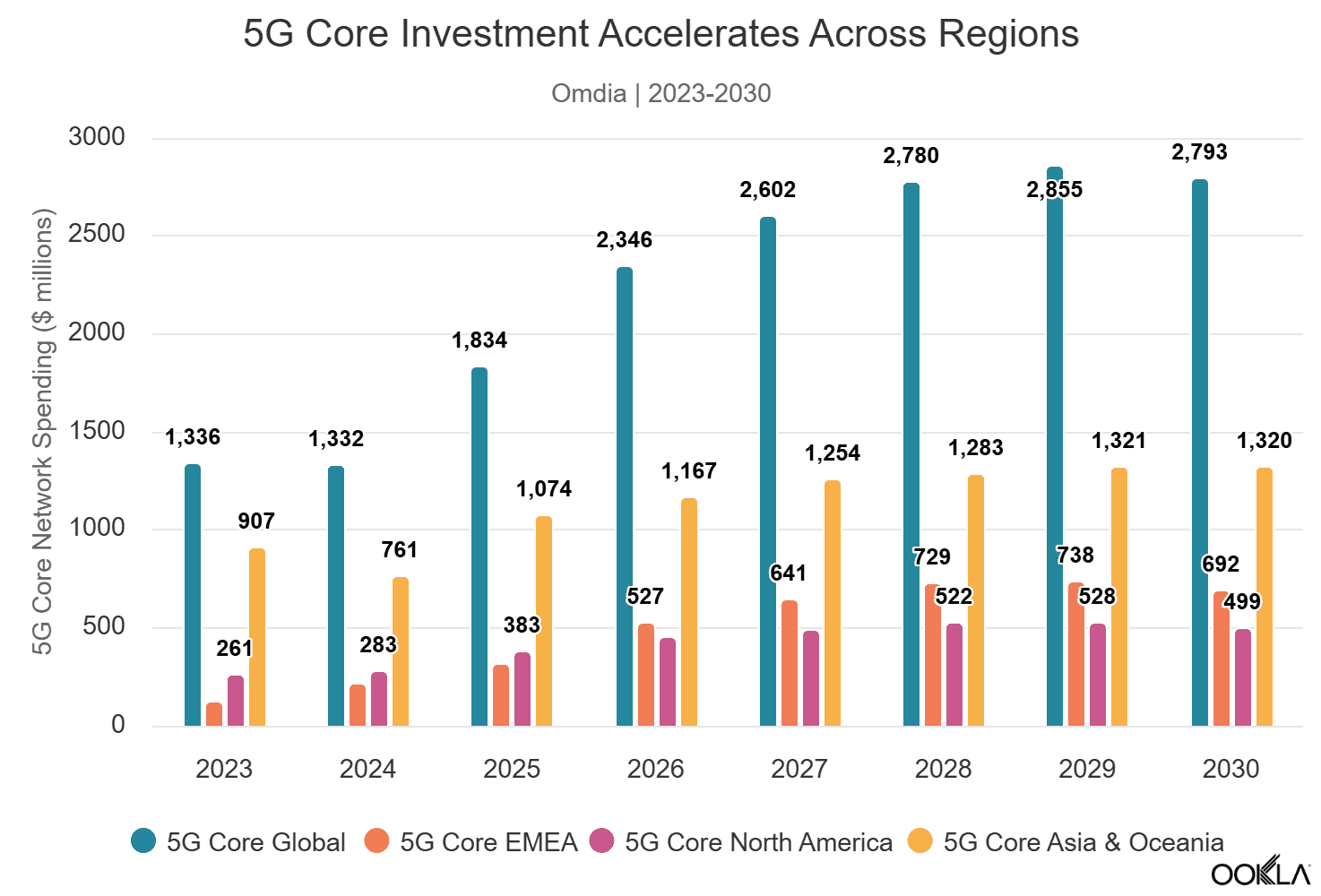

5G Core network investment is accelerating as monetization transitions from concept to selective execution:

Omdia’s latest forecasts confirm the industry’s shift toward software-defined core capability as the primary driver of next-cycle investment. Global 5G SA core network software spending is projected to grow at an 8.8% CAGR between 2025 and 2030, with EMEA leading at 16.7%, significantly outpacing North America (5.5%) and Asia & Oceania (4.2%). This reflects EMEA’s later position in the deployment cycle, as the region is entering its period of peak 5G core adoption, while North America’s 5G core spending trajectory is expected to have peaked in 2025 following the commercial launches by AT&T and Verizon. By end of Q3 2025, 83 operators worldwide had deployed 5G core networks, with 5G core investment accounting for 63.6% of global core network function software spending.

5G Core Investment Accelerates Across Regions:

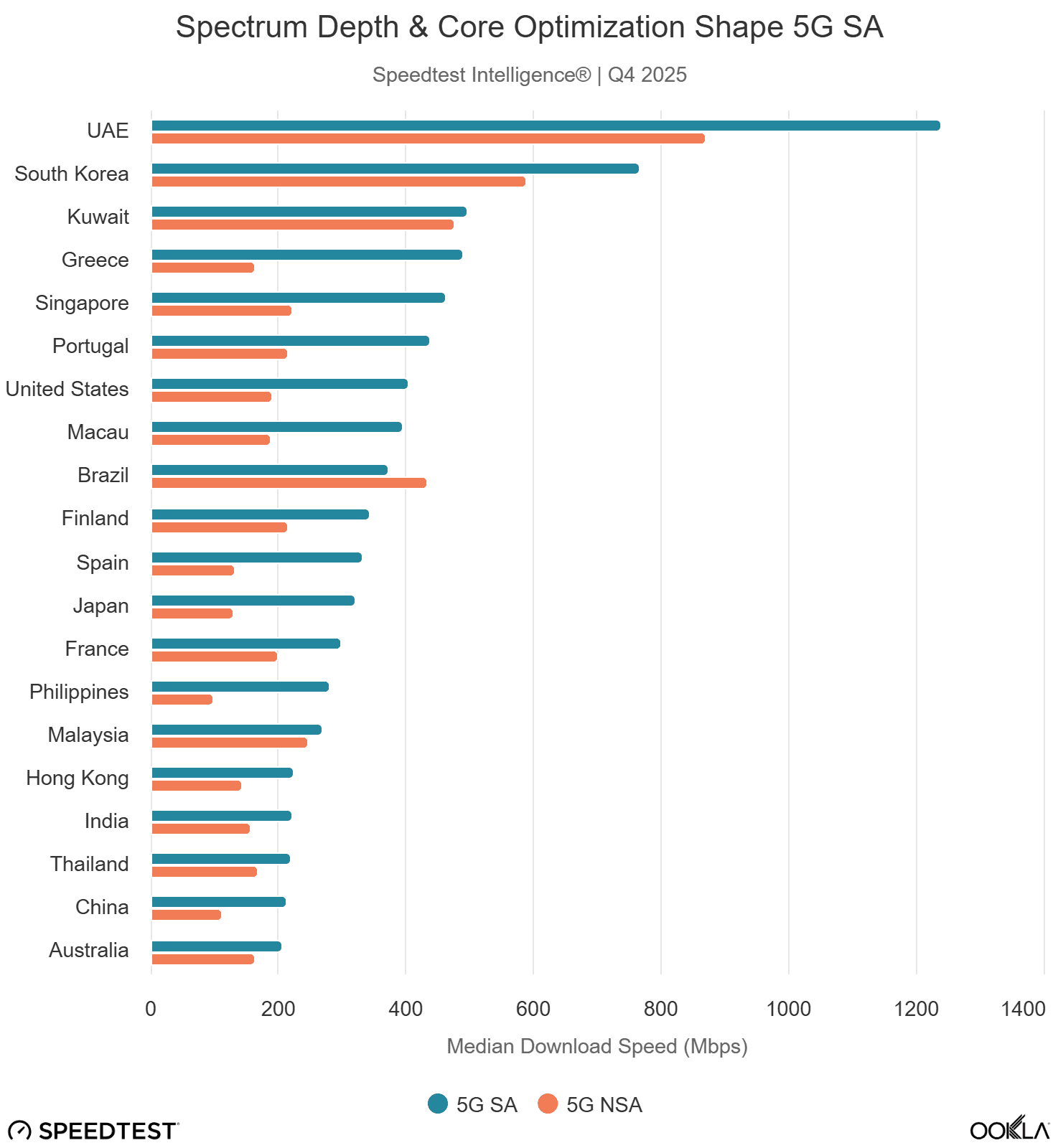

- 5G SA availability based on Speedtest® sample share reached 17.6% in Q4 2025, up modestly from 16.2% a year earlier, indicating that roughly one in six 5G Speedtests worldwide now occurs on a 5G standalone network. The headline global median SA download speed of 269.51 Mbps represents a 52% premium over non-standalone networks, though this figure masks significant regional variation driven by spectrum allocation depth, carrier aggregation maturity, and user-plane engineering.

- Asia leads in 5G availability: China continues to dominate with 80.9% 5G SA sample share and over 10 million 5G Advanced subscribers.

- Globally, 5G SA connections delivered a 52% download speed premium to 5G NSA (mostly an artifact of rich spectrum allocation and lower network load) and improved median multi-server latency by over 6% compared to NSA. However, this year’s report finds that a standalone core migration alone does not guarantee a better end-user experience. Quality of experience analysis reveals a nuanced picture: SA improves video and cloud infrastructure latency in Europe versus NSA, but underperforms NSA for gaming latency within the same region. North America records the lowest absolute SA cloud and gaming latency, consistent with dense hyperscaler adjacency and mature interconnect ecosystems.

- The Gulf Cooperation Council (GCC) was the global 5G SA performance leader, with the UAE setting the speed benchmark Led by e& and du’s aggressive 5G Advanced deployments, the delivered the world’s fastest 5G SA median download speeds in Q4 2025 at 1.13 Gbps, nearly five times that of Europe. The UAE alone reached a median of 1.24 Gbps on SA networks, a speed that would be considered exceptional even for full-fiber broadband in developed markets. The deployment of four-carrier aggregation and enhanced MIMO technology, coupled with the strategic allocation of premium mid-band spectrum to the SA network, demonstrates the performance ceiling that a fully realized 5G SA architecture can achieve.

- South Korea followed at 767 Mbps, driven by wide 3.5 GHz channel bandwidth, with the U.S. at 404 Mbps following the completion of nationwide SA deployments by all three Tier-1 operators. Europe, at 205 Mbps, trails all developed regions, though the region’s SA networks still deliver a 45% download speed premium over NSA, confirming the performance value of the SA transition where material spectrum depth is allocated.

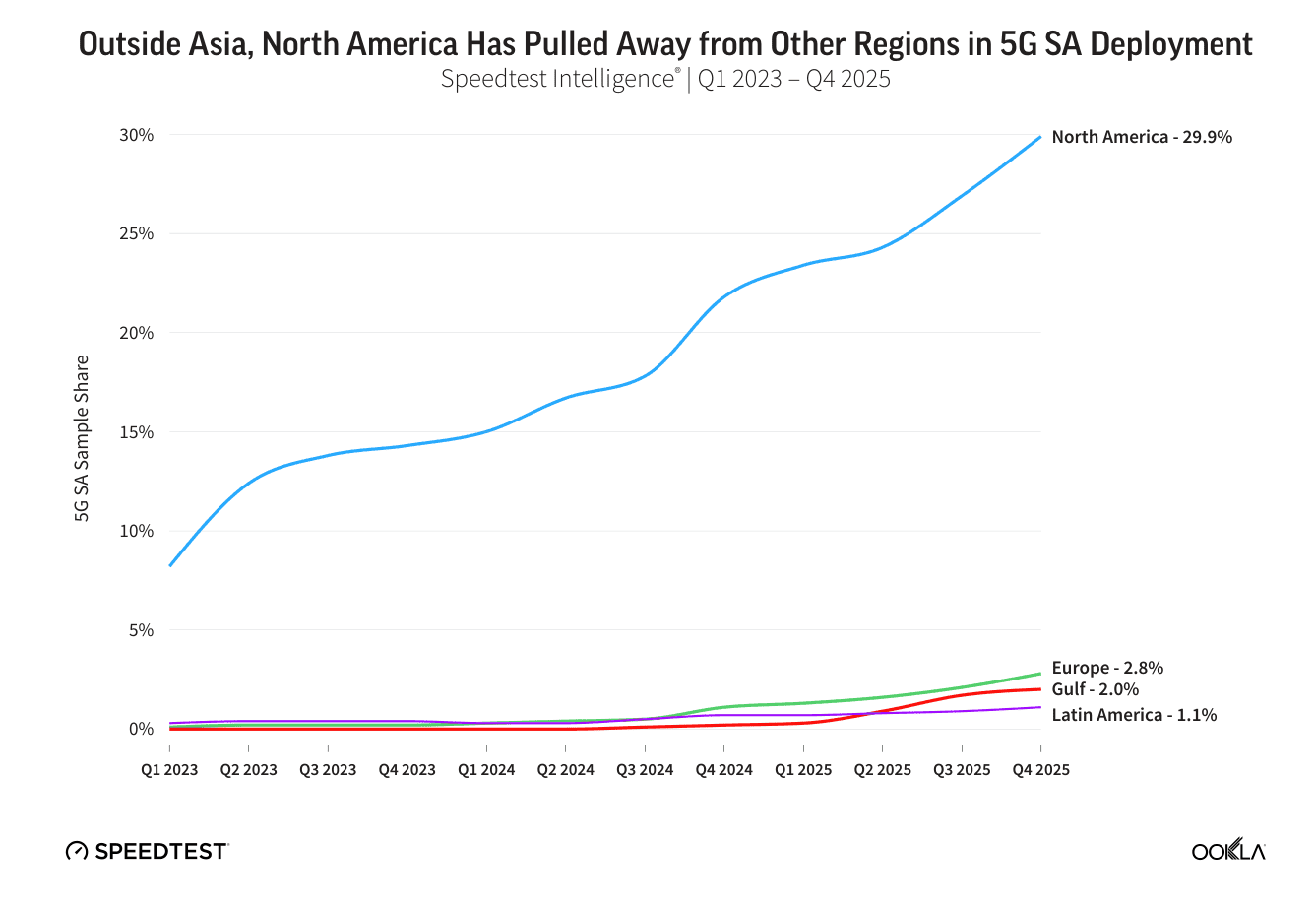

Europe’s 5G SA sample share more than doubled from 1.1% to 2.8% between Q4 2024 and Q4 2025, driven by accelerated deployments in Austria (8.7%), Spain (8.3%), the United Kingdom (7.0%), and France (5.9%). These four markets now account for the vast majority of European SA connections. The United Kingdom and France registered the strongest year-on-year acceleration in Europe, each gaining 5.3 percentage points, reflecting the impact of investment-linked merger conditions and competition in the United Kingdom, as well as targeted R&D policy support in France.

Among European markets, France (41ms to cloud endpoints), Austria (48ms), and Finland (50ms) demonstrate what is achievable where backbone quality, peering density, and routing discipline are strong. These outcomes reflect an underappreciated end-to-end network stack optimization dividend, encompassing data-center proximity, fiber backhaul depth, and user-plane topology, rather than a pure “SA dividend” alone.

However, Europe still trails North America by 27% and emerging Asia by 30%. At the global level, the U.S. remains the largest accelerator in absolute terms over the last year, with SA sample share rising 8.2 percentage points to 31.6% year-on-year, driven by the sequential rollout of SA across all Tier-1 operators beyond T-Mobile. Firmware fragmentation, where handset OEMs gatekeep SA network access pending individual carrier certification, and tariff structures that fail to incentivize migration from NSA, remain the primary barriers to faster European adoption.

The report also presents early evidence that battery life is a tangible consumer benefit of 5G SA. In the UK, devices on EE’s 5G SA network recorded median discharge times approximately 22% longer than those on 5G NSA, with O2 showing an 11% advantage. These gains likely stem from features like SA’s unified control plane, which eliminates the dual-connectivity overhead of NSA configurations.

Consumer strategies now span speed tiers (primarily Europe), 5G network slicing (Singapore, France, and the U.S.), and 5G Advanced segmentation packages (China). Enterprise 5G network slicing presents the much larger long-term revenue opportunity, with T-Mobile’s SuperMobile representing the first nationwide commercial B2B slicing service in the U.S. Countries with coordinated regulatory frameworks, implementing clear coverage obligations, investment incentives, or infrastructure consolidation policies with deployment remedies, consistently outperform those with fragmented or reactive approaches, reinforcing the report’s finding that policy has emerged as a primary competitive differentiator in 5G SA outcomes globally.

…………………………………………………………………………………………………………………………………………………………………………………………

References:

MCN Market Roared Back in 2025 With 15 Percent Growth, According to Dell’Oro Group

https://www.ookla.com/articles/5g-sa-2026

Dell’Oro: RAN market stable, Mobile Core Network market +14% Y/Y with 72 5G SA core networks deployed

AT&T deploys nationwide 5G SA while Verizon lags and T-Mobile leads

Ericsson CEO’s strong statements on 5G SA, WRC 27, and AI in networks

Ookla: Uneven 5G deployment in Europe, 5G SA remains sluggish; Ofcom: 28% of UK connections on 5G with only 2% 5G SA

Ericsson reports ~flat 2Q-2025 results; sees potential for 5G SA and AI to drive growth

Téral Research: 5G SA core network deployments accelerate after a very slow start

Google Fiber and Nokia demo network slicing for home broadband in GFiber Labs

Analysts: Telco CAPEX crash looks to continue: mobile core network, RAN, and optical all expected to decline

Global 5G Market Snapshot; Dell’Oro and GSA Updates on 5G SA networks and devices

Dell’Oro: Mobile Core Network market has lowest growth rate since 4Q 2017

ABI Research: 5G network slicing market to hit $67.52 billion in 2030 with Asia Pacific in the lead

ABI Research forecasts that the global 5G network slicing market will surge from $6.1 billion in 2025 to $67.52 billion by 2030, reflecting a compound annual growth rate (CAGR) of 70%. This represents a sharp upward revision from its 2023 outlook, which projected a market value of $19.5 billion by 2028.

Editor’s Note: 5G network slicing, as well as ALL 5G features and functions (including 5G Security) require a 5G Standalone (SA) core network, which up until recently had not been widely deployed. Also, there are no ITU standards or recommendations for either 5G SA or 5G network slicing or any other 5G features/functions. Those are all specified by 3GPP, for example TS 23.501 5G Systems Architecture which includes network slicing.

In a recent blog post, Dimitris Mavrakis stated that the ABI’s revised forecast is driven by intensified monetization efforts from major network operators, including China Mobile, Deutsche Telekom and T-Mobile US, together with the growing installed base of 5G Standalone (SA)-capable smartphones. At the same time, he highlighted that progress is moderated by the proven complexity of integrating 5G SA cores and cloud-native tooling into existing telco network and IT environments.

ABI indicates that so-called “carpeted” industry verticals—like retail, stadiums, and financial services do not deal with mission- and safety-critical applications. Therefore, slicing deployments are more simplistic and provide a quicker Return on Investment (ROI) than in more demanding industry sectors such as oil and gas. ABI says that industrial manufacturing will remain an important vertical for network slicing, albeit at a substantially slower growth rate than carpeted verticals.

The analysis further suggests that, for certain enterprises, network slicing delivered over public 5G infrastructure is becoming a more attractive option than 5G private networks, which introduces additional headwinds for the private networking market. While B2B use cases are expected to account for 64% of total network slicing market value by 2030, consumer applications are projected to be the single largest segment, contributing approximately $24.3 billion of revenue by the end of the period.

5G network slicing progress report with a look ahead to 2025

ABI Research: 5G Network Slicing Market Slows; T-Mobile says “it’s time to unleash Network Slicing”

Ericsson, Intel and Microsoft demo 5G network slicing on a Windows laptop in Sweden

Ericsson and Nokia demonstrate 5G Network Slicing on Google Pixel 6 Pro phones running Android 13 mobile OS

BT Group, Ericsson and Qualcomm demo network slicing on 5G SA core network in UK

Telstra achieves 340 Mbps uplink over 5G SA; Deploys dynamic network slicing from Ericsson

Samsung and KDDI complete SLA network slicing field trial on 5G SA network in Japan

Is 5G network slicing dead before arrival? Replaced by private 5G?

5G Network Slicing Tutorial + Ericsson releases 5G RAN slicing software

Network Slicing and 5G: Why it’s important, ITU-T SG 13 work, related IEEE ComSoc paper abstracts/overviews

Dell’Oro: RAN market stable, Mobile Core Network market +14% Y/Y with 72 5G SA core networks deployed

Téral Research: 5G SA core network deployments accelerate after a very slow start

Building and Operating a Cloud Native 5G SA Core Network

Dell’Oro: RAN market stable, Mobile Core Network market +14% Y/Y with 72 5G SA core networks deployed

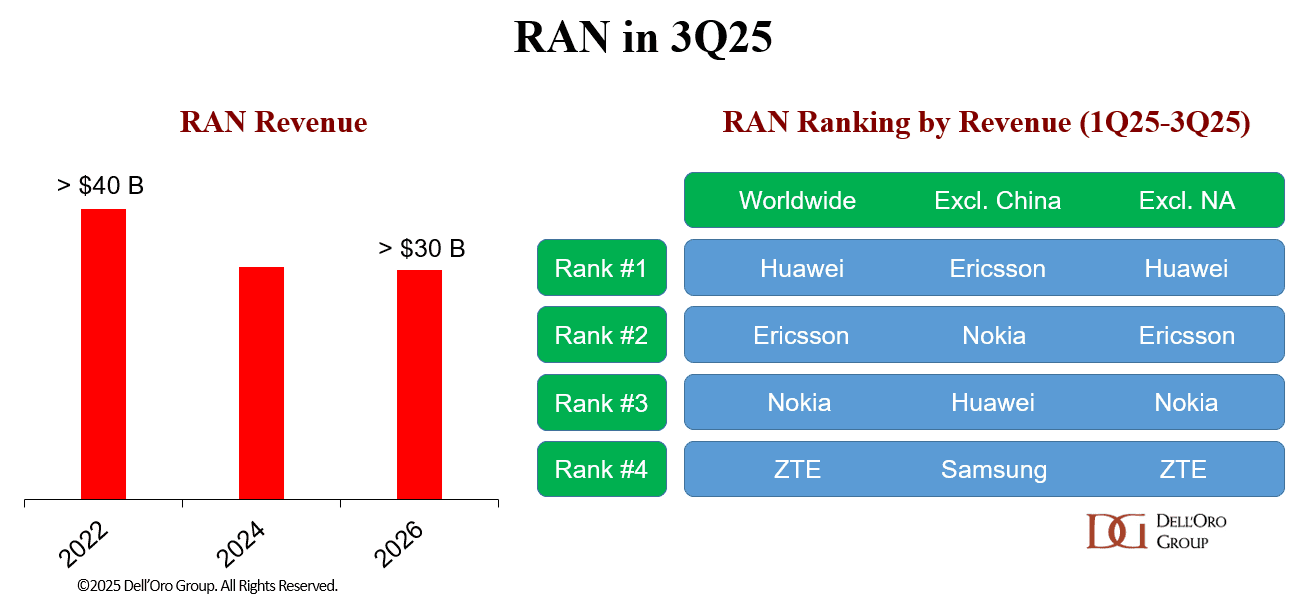

A recently published report from Dell’Oro Group notes that after two years of steep declines, initial estimates show that total Radio Access Network (RAN) revenue—including baseband, radio hardware, and software, excluding services—was flat outside of China and up when excluding North America.

“The nearly stable results for the 1Q25-3Q25 period bolster the flat growth thesis we have communicated for some time, reflecting the current state of the 5G network,” said Stefan Pongratz, Vice President of RAN market research at the Dell’Oro Group. “While near-term RAN expectations remain muted, some of the leading RAN suppliers are still cautiously optimistic that more investments are needed over the long-term to ensure the networks evolve from a connectivity pipe into an intelligence grid. Huawei and Ericsson are the clear #1 and 2 players globally – their combined share makes up nearly two-thirds of the RAN market (see table below).” Pongratz added.

Additional highlights from the 3Q 2025 RAN report:

- In the quarter, growth in EMEA was nearly enough to offset declining revenue in North America and the Asia Pacific regions.

- The top 5 RAN suppliers, based on worldwide revenues for the 1Q25-3Q25 period, are Huawei, Ericsson, Nokia, ZTE, and Samsung.

- Market is becoming more concentrated—the top five suppliers accounted for 96 percent of the 1Q25-3Q25 RAN market, up from 95 percent in 2024.

- Huawei and Ericsson’s worldwide RAN revenue share improved for the 1Q25-3Q25 period relative to 2024.

- Huawei and Nokia’s RAN revenue share outside of North America improved for the 1Q25-3Q25 period relative to 2024.

- The short-term outlook remains unchanged, with total RAN expected to remain mostly stable in 2026.

Dell’Oro Group’s RAN Quarterly Report offers a complete overview of the RAN industry, with tables covering manufacturers’ and market revenue for multiple RAN segments including 5G NR Sub-7 GHz, 5G NR mmWave, LTE, macro base stations and radios, small cells, Massive MIMO, Open RAN, and vRAN. The report also tracks the RAN market by region and includes a four-quarter outlook. To purchase this report, please contact us by email at [email protected].

………………………………………………………………………………………………………………………………………….

Data from Omdia, a Light Reading sister company, shows Ericsson, Huawei and Nokia were even more dominant last year than they were in 2023, growing their combined RAN market share by 2.3 percentage points over this period, to 77.4%. Besides China’s ZTE, the only other contender with more than a percentage point of market share was Samsung.

…………………………………………………………………………………………………………………………………………..

Another recent Dell’Oro Group report reveals that the Mobile Core Network (MCN) market revenue outside China surged 14% year-over-year (Y/Y) in 3Q 2025. Twelve Mobile Network Operators (MNOs) have now selected to move forward with 5G-Advanced (the marketing term used for the next phases of 3GPP’s 5G specs, which started with Release 18 and continues with Release 19 and beyond).

“The Chinese market experienced abnormally high growth in 3Q 2024. As a result, the China market revenue declined 39 percent Y/Y for 3Q 2025,” stated Dave Bolan, Research Director at Dell’Oro Group. “The revenue for all the other regions increased, between 9 percent and 17 percent Y/Y, resulting in a worldwide revenue decline of 2 percent Y/Y. As noted, revenue worldwide excluding China rose 14 percent Y/Y, continuing the trend in subscribers migrating to 5G Standalone (5G SA), and revenue worldwide excluding North America declined 5 percent Y/Y.

“MNOs are moving forward with 5G SA (72 in our last count) and moving forward to take advantage of monetization opportunities. Network Slicing announcements continued. Of note is Reliance Jio (India), which announced 10 network slices with guaranteed service level agreements (SLAs) at scale. In October, T-Mobile launched Edge Control, providing enterprises with what Dell’Oro Group refers to as an MNO-provided Mobile Private Network (MPN). This is in response to the challenges of implementing 5G SA Private Wireless networks in the shared CBRS spectrum in the US.

“We have identified 12 MNOs that have commercially launched 5G-Advanced networks (not all this quarter), to take 5G to the next level with new features and performance. MNOs include: China Mobile, China Telecom, China Unicom, CTM (Macau), Du (UAE), e& (UAE), HKT (Hong Kong), Singtel (Singapore), Telstra (Australia), T-Mobile (USA), YTL (Malaysia), and Zain (Kuwait),” added Bolan.

Additional highlights from the 3Q 2025 Mobile Core Network and Multi-Access Edge Computing Report include:

- Region rankings were: EMEA; Asia Pacific, excluding China; China and North America tied; CALA.

- Vendor rankings (with more than 5 percent share) were: Huawei, Ericsson, Nokia, and ZTE.

The Dell’Oro Group Mobile Core Network & Multi-Access Edge Computing Quarterly Report offers complete, in-depth coverage of the market with tables covering manufacturers’ revenue, shipments, and average selling prices for Traditional Packet Core, Evolved Packet Core, 5G Packet Core, Policy, Subscriber Data Management, Signaling, Circuit Switched Core, and IMS Core by geographic regions. To purchase this report, please contact us at [email protected].

About Dell’Oro Group:

Dell’Oro Group is a market research firm that specializes in strategic competitive analysis in the telecommunications, security, enterprise networks, and data center infrastructure markets. Our firm provides in-depth quantitative data and qualitative analysis to facilitate critical, fact-based business decisions.

For more information, contact Dell’Oro Group at +1.650.622.9400 or visit https://www.delloro.com.

References:

MCN Market Up 14 Percent Outside China in 3Q 2025, According to Dell’Oro Group

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

Omdia on resurgence of Huawei: #1 RAN vendor in 3 out of 5 regions; RAN market has bottomed

Omdia: Huawei increases global RAN market share due to China hegemony

Dell’Oro Group: RAN Market Grows Outside of China in 2Q 2025

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

Dell’Oro: Global RAN Market to Drop 21% between 2021 and 2029

Dell’Oro: RAN market still declining with Huawei, Ericsson, Nokia, ZTE and Samsung top vendors

Highlights of Dell’Oro’s 5-year RAN forecast

Dell’Oro: 2023 global telecom equipment revenues declined 5% YoY; Huawei increases its #1 position

Dell’Oro & Omdia: Global RAN market declined in 2023 and again in 2024

Dell’Oro: Mobile Core Network market has lowest growth rate since 4Q 2017

Dell’Oro: Mobile Core Network market driven by 5G SA networks in China

Dell’Oro: Mobile Core Network Market 5 Year Forecast

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Highlights of Ericsson’s Mobility Report – November 2025

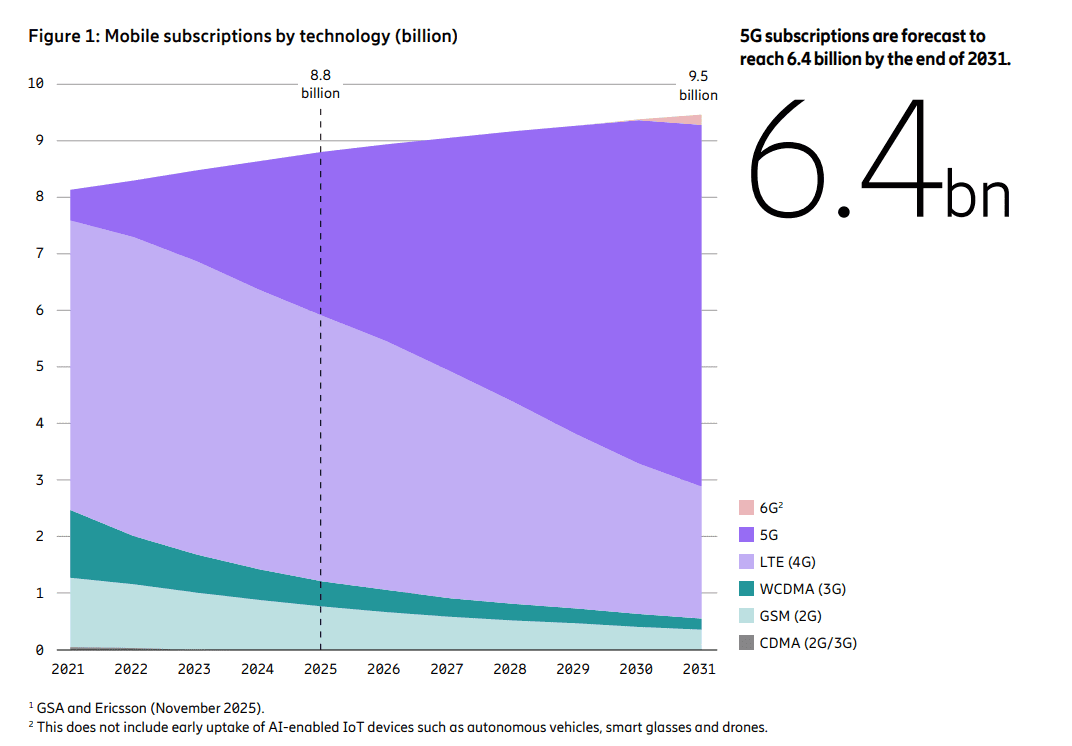

The latest issue of the Ericsson Mobility Report states that 5G subscriptions now account for one-third of total mobile subscriptions. Mobile network data traffic grew slightly more than expected – 20 percent between Q3 2024 and Q3 2025. As 5G evolves, service providers are increasingly exploring innovative use cases and new monetization opportunities such as offering differentiated connectivity services and modernizing enterprise IT with 5G.

After many years of hype, network slicing, which requires a 5G SA core network, is finally gaining market traction with 33 communications service providers now offering variations of the technology. Of the 118 network slicing cases discovered by Ericsson’s researchers, 65 have moved beyond proof of concept and into commercial services, either as standalone subscription services or as add-on packages for consumer or business customers. Ericsson attributes this growth spurt to more widespread deployment of 5G SA core networks.

Looking further ahead, the 6G RAN standardization process has begun in 3GPP and ITU-R WP5D, with the first commercial launches expected in front-runner markets.

–>However, there has been no work initiated on the 6G core network in either 3GPP or ItU-T.

Ericsson’s report says the U.S., Japan, South Korea, China, India and some Gulf Cooperation Council countries are the 6G leaders. Global 6G subscriptions are likely to reach 180 million by the end of 2031, the report predicts.

We think that forecast is highly unlikely as the IMT 2030 (6G) RIT/SRITs recommendation won’t be completed till the end of 2030 with initial deployments sometime in 2031.

…………………………………………………………………………………………………………….

Data from Omdia, a Light Reading sister company, shows Ericsson, Huawei and Nokia were even more dominant last year than they were in 2023, growing their combined market share by 2.3 percentage points over this period, to 77.4%. Besides China’s ZTE, the only other contender with more than a percentage point of market share was Samsung.

References:

https://www.ericsson.com/en/reports-and-papers/mobility-report/reports/november-2025

Dell’Oro: 4G and 5G FWA revenue grew 7% in 2024; MRFR: FWA worth $182.27B by 2032

Ericsson’s revenue drops, profits soar; deal with Vodafone and partnership with Export Development Canada look promising

Latest Ericsson Mobility Report talks up 5G SA networks and FWA

Ericsson Mobility Report touts “5G SA opportunities”

Ericsson Mobility Report: 5G monetization depends on network performance

Ericsson Mobility Report: 5G subscriptions in Q2 2022 are 690 million (vs. 8.3 billion total mobile users)

Omdia: How telcos will evolve in the AI era

Dario Talmesio, research director, service provider, strategy and regulation at market research firm Omdia (owned by Informa) sees positive signs for network operators.

“After many years of plumbing, now telecom operators are starting to see some of the benefits of their network and beyond network strategies. Furthermore, the investor community is now appreciating telecom investments, after many years of poor valuation, he said during his analyst keynote presentation at Network X, a conference organized by Light Reading and Informa in Paris, France last week.

“What has changed in the telecoms industry over the past few years is the fact that we are no longer in a market that is in contraction,” he said. Although telcos are generally not seeing double-digit percentage increases in revenue or profit, “it’s a reliable business … a business that is able to provide cash to investors.”

Omdia forecasts that global telecoms revenue will have a CAGR of 2.8% in the 2025-2030 timeframe. In addition, the industry has delivered two consecutive years of record free cash flow, above 17% of sales.

However, Omdia found that telcos have reduced capex, which is trending towards 15% of revenues. Opex fell by -0.2% in 2024 and is broadly flatlining. There was a 2.2% decline in global labor opex following the challenging trend in 2023, when labor opex increased by 4% despite notable layoffs.

“Overall, the positive momentum is continuing, but of course there is more work to be done on the efficiency side,” Talmesio said. He added that it is also still too early to say what impact AI investments will have over the longer term. “All the work that has been done so far is still largely preparatory, with visible results expected to materialize in the near(ish) future,” he added. His Network X keynote presentation addressed the following questions:

- How will telcos evolve their operating structures and shift their business focuses in the next 5 years?

- AI, cloud and more to supercharge efficiencies and operating models?

- How will big tech co-opetition evolve and impact traditional telcos?

Customer care was seen as the area first impacted by AI, building on existing GenAI implementations. In contrast, network operations are expected to ultimately see the most significant impact of agentic AI.

Talmesio said many of the building blocks are in place for telecoms services and future revenue generation, with several markets reaching 60% to 70% fiber coverage, and some even approaching 100%.

Network operators are now moving beyond monetizing pure data access and are able to charge more for different gigabit speeds, home gaming, more intelligent home routers and additional WiFi access points, smart home services such as energy, security and multi-room video, and more.

While noting that connectivity remains the most important revenue driver, when contributions from various telecoms-adjacent services are added up “it becomes a significant number,” Talmesio said.

Mobile networks are another important building block. While acknowledging that 5G has been something of a disappointment in the first five years of the deployment cycle, “this is really changing” as more operators deploy 5G standalone (5G SA core) networks, Omdia observed.

Talmesio said: “At the end of June, there were only 66 telecom operators launching or commercially using 5G SA. But those 66 operators are those operators that carry the majority of the world’s 5G subscribers. And with 5G SA, we have improved latency and more devices among other factors. Monetization is still in its infancy, perhaps, but then you can see some really positive progress in 5G Advanced, where as of June, we had 13 commercial networks available with some good monetization examples, including uplink.”

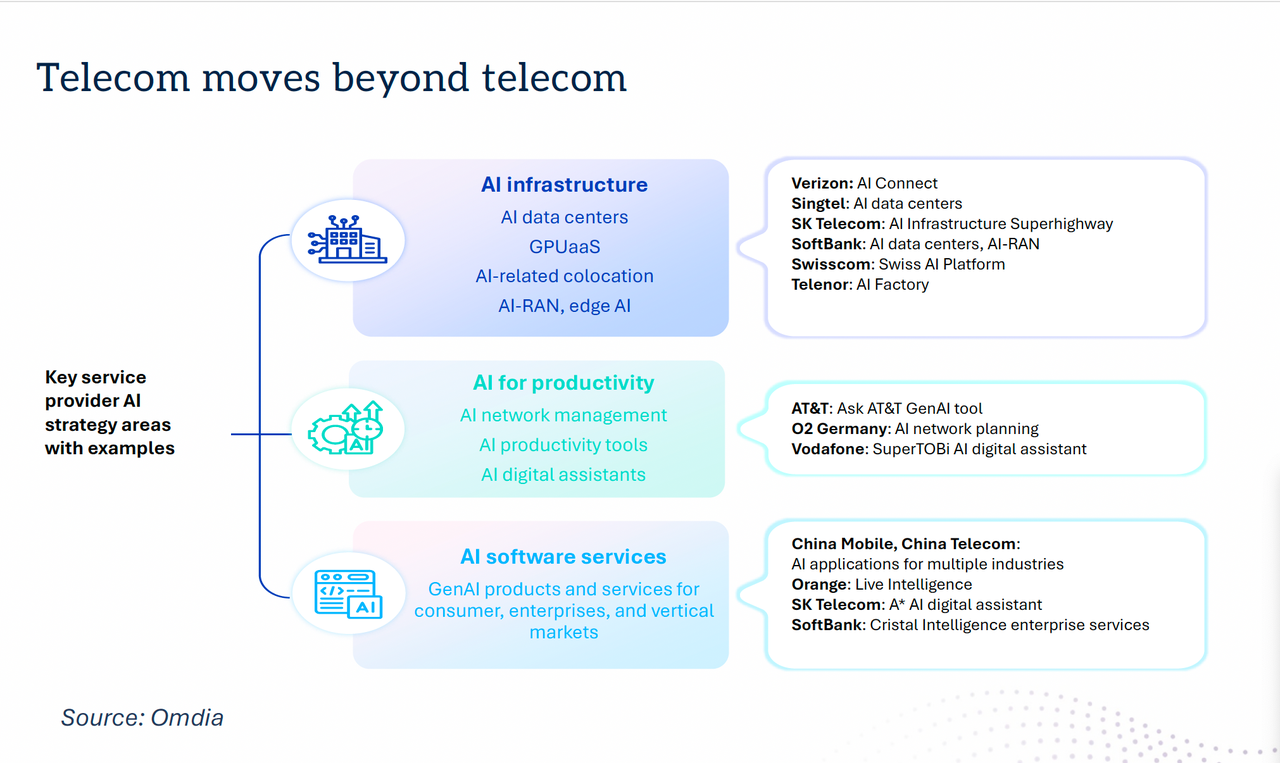

“Telecom is moving beyond telecoms,” with a number of new AI strategies in place. For example, telcos are increasingly providing AI infrastructure in their data centers, offering GPU as-a-service, AI-related colocation, AI-RAN and edge AI functionality.

Dario Talmesio, Omdia

……………………………………………………………………………………………………………………………………………………

AI is also being used for network management, with AI productivity tools and AI digital assistants, as well as AI software services including GenAI products and services for consumer, enterprises and vertical markets.

“There is an additional boost for telecom operators to move beyond connectivity, which is the sovereignty agenda,” Talmesio noted. While sovereignty in the past was largely applied to data residency, “in reality, there are more and more aspects of sovereignty that are in many ways facilitating telecom operators in retaining or entering business areas that probably ten years ago were unthinkable for them.” These include cloud and data center infrastructure, sovereign AI, cyberdefense and quantum safety, satellite communication, data protection and critical communications.

“The telecom business is definitely improving,” Talmesio concluded, noting that the market is now also being viewed more favorably by investors. “In many ways, the glass is maybe still half full, but there’s more water being poured into the telecom industry.”

References:

https://networkxevent.com/speakers/dario-talmesio/

https://www.mckinsey.com/industries/technology-media-and-telecommunications/our-insights/pushing-telcos-ai-envelope-on-capital-decisions

Omdia on resurgence of Huawei: #1 RAN vendor in 3 out of 5 regions; RAN market has bottomed

Omdia: Huawei increases global RAN market share due to China hegemony

Dell’Oro & Omdia: Global RAN market declined in 2023 and again in 2024

Omdia: Cable network operators deploy PONs