Uncategorized

Comcast Blames Widespread Service Outage on Cut Fiber Lines Owned by CenturyLink & Zayo

Comcast Corp, which has more than 29 million business and residential customers, today blamed cuts in two fiber lines for a widespread system failure that knocked out cable, internet and phone services around the country.

It was unclear how many customers were affected as the system failure, which appeared contained to Comcast’s network, also disrupted connectivity services like Netflix Inc. and Okta Inc. as other internet service providers routed internet traffic through Comcast’s network, according to network research firm ThousandEyes.

![]()

Comcast service problems today (June 29, 2018):

https://outage.report/us/xfinity

………………………………………………………………………………………………………………………………………………………

Comcast, one of the dominant cablecom companies in the U.S., said most service had been restored by late Friday. The Philadelphia-based company said in a statement that “one of Comcast’s large backbone network partners had a fiber cut that we believe is also impacting other providers.” Later, Comcast said the damaged fiber optic lines are owned by CenturyLink Inc. and Zayo Group Holdings Inc.

A spokeswoman for CenturyLink issued a statement saying CenturyLink’s network was working normally, though the company had “experienced two isolated fiber cuts in North Carolina affecting some customers that in and of itself did not cause the issues experienced by other providers.” The spokeswoman, Francie Dudrey, didn’t comment further. Attempts to reach Zayo were unsuccessful. Fiber networks, which make up the backbone of the internet, transmit vast amounts of internet traffic, processing everything from online purchases to 911 calls.

Down Detector and Outage.Report, two websites that monitor the running of consumer-technology services, ranked the system failure as extreme and posted maps indicating large numbers of customers affected in the New York, Philadelphia and Washington, D.C., metro areas as well as San Francisco, Chicago and Denver.

Reports of outages, according to the websites, spiked early Friday afternoon. Some customers took to social media to discuss the outages, saying they were having trouble getting through the company’s phones and online chats. Comcast, on Twitter, directed customers to an internal website that was at one point down as well, eliciting a second round of customer complaints.

https://www.wsj.com/articles/comcast-blames-widespread-service-outage-on-cut-fiber-line-1530308633

Write to Maria Armental at [email protected]

IHS Markit: Ethernet switching market +12% YoY; data center and campus upgrades

By Matthias Machowinski, senior research director, enterprise networks and video, IHS Markit

Highlights:

- Worldwide Ethernet switch revenue totaled $6.1 billion in the first quarter of 2018 (Q1 2018), growing 12 percent on a year-over-year basis

- 100GE continued to ramp, increasing more than twofold year over year and reaching 1.7 million ports in the quarter; 40GE ports were flat year over year

- Power-over-Ethernet (PoE) port shipments grew 11 percent in Q1 2018

- Number-one Cisco grew 7 percent year over year, number-two Huawei rose 43 percent, number-three HPE (Aruba) was up 2 percent and number-four Arista grew 40 percent

IHS Markit analysis:

Ethernet switch revenue declined 10 percent sequentially in Q1 2018 due to a seasonal slowdown in demand, but the longer-term growth outlook remains positive and strengthened further during the quarter, with year-over-year growth hitting 12 percent, up from 7 percent the previous quarter.

The market enjoyed its strongest growth in seven years in 2017, and the momentum continued into 2018, fueled by continuing data center upgrades and expansion, as well as growing demand for campus gear due to improving economic conditions. The transition to 25/100GE architectures in the data center is in full swing, driving strong gains in 25GE, 100GE and white box shipments. And power over Ethernet is growing once again, a sign of strengthening campus switching demand.

Growth is well balanced around the globe and not driven by any single geography. In Q1 2018, Europe, the Middle East and Africa (EMEA) and Asia Pacific were the top growth markets, increasing 15 and 16 percent, respectively, year over year, while growth in North America remained solid at 8 percent.

IHS Markit forecasts low- to mid-single-digit growth for the Ethernet switching market from 2019 to 2022. The bright spots will be the 10GE, 25GE, 100GE, 200GE and 400GE segments, where significant growth is expected over the next few years.

Ethernet switch report synopsis

The IHS Markit quarterly Ethernet switch report provides worldwide and regional market size, vendor market share, forecasts through 2022, analysis and trends for unmanaged, web-managed and fully managed fixed and chassis switches by port speed (100ME, 1GE, 2.5GE, 10GE, 25GE, 40GE, 50GE, 100GE, 200GE, 400GE) and revenue.

…………………………………………………………………………………………………………………………………………………………………………………………………

Related articles on Ethernet Switch Market:

IDC’s Worldwide Quarterly Ethernet Switch and Router Trackers Show Marked Improvement for Q1 2018

IDC: Global IT, telecom spending=$4T in 2018; Economic risks loom for 2019

Global IT and telecom spending will grow 3.7 percent to $4 trillion in 2018, but economic concerns could derail growth in 2019, according to IDC.

In 2017, IT and telecom spending grew at a 4.2 percent clip. IDC said economic issues like tariffs, rising interest rates and growth in China could cut IT spending to less than 3 percent.

Indeed, Daimler issued a profit warning based on Chinese tariffs on its U.S. made cars.

By 2022, annual IT spending should hit $4.5 trillion with software and services, cloud, and digital transformation seeing the most demand. Infrastructure spending has stabilized largely due to cloud spending.

IDC said there’s a likelihood for a mild U.S. recession by 2020, but spending on cost saving software and cloud should provide a buffer for IT spending.

Last year saw a significant rebound in spending on devices, driven by the improving economy and pent-up demand for PC upgrades. The smartphone market performed better than forecast in terms of value, with price increases making up for slowing shipments in many countries. Tablets continued to struggle but will return to modest growth in some countries over the next few years as premium and commercial devices begin to account for an increasing proportion of shipments. Meanwhile, server/storage spending is increasingly driven by cloud hyperscale datacenter buildout but is also benefiting from a significant enterprise upgrade cycle related to product refreshes. IT infrastructure spending, including network equipment, increased by 11% in 2017 and will continue to post annual growth in the range of 8-12% over the next five years even while spending on devices slows again.

“The infrastructure market is increasingly stable because a large proportion is now tied to the service provider model and overall demand for cloud services, which shows no sign of slowing down even in the event of a weakening economy,” said Stephen Minton, vice president, Customer Insights & Analysis. “To some extent, this spending will be more insulated against economic downturns than end-user capital spending, and therefore the IT market will be less vulnerable than it was in the past when any kind of GDP slowdown would translate into big declines for hardware spending. Nevertheless, economic risks are now higher than three months ago.”

US Demand is Stable, but China Facing Slowdown

All regions saw strong demand for technology in 2017, thanks to the broad-based strength of economic performance. The U.S. rebounded from 1.9% growth in 2016 to 4.5% in 2017. Tax cuts will help to ensure another strong year for the U.S. market in 2018, before overall growth is expected to slow. Many economists now expect a mild recession in the U.S. by 2020 at the latest, but the impact on ICT spending will be less than previous downturns due the growth of the service provider model and the increasing adoption of cost-saving software. Meanwhile overall growth in China slowed from 9% in 2016 to 8% last year and will drop to 6% in 2018.

“The economy is gradually slowing in China, but the real reason for slowing ICT growth is because the market is still heavily reliant on mobile devices, which are now seeing higher penetration rates,” said Minton. “Software and services are growing strongly, but still represent a very small proportion of average ICT budgets in China compared to other countries.”

Economy, Cloud, and Mobile Driving Growth

Other regions which posted improving growth in 2017 included Japan (+3%), Western Europe (+2%), Central & Eastern Europe (+3%), Canada (+5%), Asia/Pacific (excluding Japan) (+5%) and the Middle East/Africa (+2%). All of these regions benefited from improving business and consumer confidence, which enabled ICT buyers to work off the pent-up demand that had swelled during the prior years of subdued growth.

“Cloud and mobile are still the big drivers for traditional ICT spending, as legacy products and services like desktop PCs and fixed-line networks either stagnate or begin to decline,” added Minton. “This means what while the overall market is broadly tracking GDP, there is a lot of variation by product category. cloud-related hardware, software, and services are posting strong rates of growth. For example, Infrastructure as a Service (IaaS) is expected to grow by another 37% this year and will continue to grow by around 30% per year over the forecast. This in turn will ensure that cloud service providers continue to invest in server/storage and network infrastructure.”

https://www.idc.com/getdoc.jsp?containerId=prUS44021718

Point Topic: 931.6M Fixed Broadband Connections at end of Q4-2017; VDSL Growth but Copper Connections Continue Decline

|

|

|

IHS Markit: Optical Network Equipment Market off to slow start in 2018

By Heidi Adams, senior research director, IP and optical networks, IHS Markit

Highlights

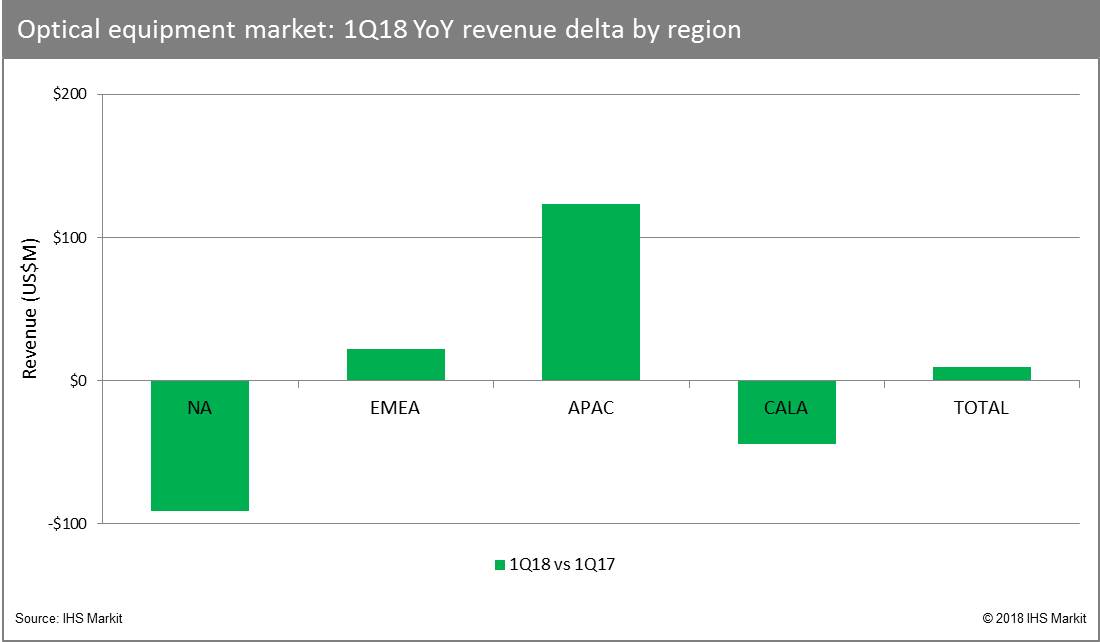

- Global optical network hardware revenue totaled $3.1 billion in the first quarter of 2018 (Q1 2018), declining 25 percent sequentially and remaining flat on a year-over-year basis.

- The global Q1 2018 optical equipment market net of China was down 2 percent year over year. China itself was up 7 percent year over year, and continues to be a key market for optical transport equipment.

- Huawei remained the overall optical equipment market leader in Q1 2018, with 26 percent market share.

Our analysis

After a strong close to 2017, the optical equipment market got off to a lackluster start in 2018. Modest year-over-year growth in Europe, the Middle East and Africa (EMEA) and Asia Pacific was not sufficient to overcome year-over-year spending declines in North America and the Caribbean and Latin America (CALA) regions in the quarter. Total optical equipment market spending was down 25 percent on a sequential basis, with all regions seeing quarter-over-quarter declines.

Wavelength-division multiplexing (WDM) continues to be the growth engine for the market. In Q1 2018, the WDM segment totaled $2.9 billion, up 3 percent year-over-year, thanks to gains in EMEA and Asia Pacific. Both the metro and long haul segments experienced low single-digit year-over-year growth in Q1 2018.

Synchronous optical networking (SONET)/synchronous digital hierarchy (SDH) continued its overall decline. Global revenue came to $206 million in Q1 2018, down over 25 percent year over year. This segment represented less than 10 percent of the total optical network equipment market in the quarter.

Huawei continued to lead the total optical equipment market by a wide margin in Q1 2018. Nokia secured second place based on continuing strength in EMEA and increasing business in Asia Pacific. Ciena maintained its leadership position in North America and remained number three overall in the global market. ZTE rounded out the top four, but faces a difficult journey ahead with the impact of US sanctions and a subsequent halt in major operations.

Unstoppable bandwidth demand drives long-term growth

IHS Markit anticipates a continuing ramp in network capacity to address growing bandwidth demand. In the metro, the primary driver is burgeoning bandwidth demand—to, from and between data centers.

Not to be ignored is the coming broader introduction and adoption of consumer 4K and higher video content and services on a variety of devices. The shift from data to video to virtual reality (VR)/augmented reality (AR) will add yet another set of bandwidth-intensive and latency-sensitive services to the mix toward 2022.

Finally, a further evolutionary shift in mobile network architectures in preparation for 5G and a range of new fixed and mobile machine-to-machine (M2M) and Internet of Things (IoT) applications will set the stage for an investment cycle at the farthest reaches of the optical access network.

Based on these industry trends, the optical equipment market will grow at a compound annual growth rate (CAGR) of 4.5 percent from 2017 to 2022, according to IHS Markit forecasts.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

Editor’s Note:

We believe much of the anticipated fiber optic network growth will come from a variety of factors in the metro, including data center interconnect demands, higher-bandwidth video transmission (with the advent of 4K video) and eventually virtual and augmented reality. We think 5G mobile backhaul support is questionable in the next few years considering all the “5G” hype and lack of standards till IMT 2020 (5G radio aspects ONLY) recommendations are finalized in late 2020.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

Optical Network Hardware Market Tracker – Q1 2018

This report tracks the global market for metro and long-haul WDM and SONET/SDH equipment and SONET/SDH and WDM ports. It provides market size, market share, forecasts through 2022, analysis and trends.

NFIC Conference at SCU May 30, 2018 3PM-10PM: Accelerating Smart and Connected Communities

The joint IEEE-NATEA conference on an emerging technology is aimed to provide IEEE and NATEA members with an inexpensive solid overview of a technology that may affect their work and careers in the near future.

Co-organized initially by IEEE Computer Society Silicon Valley Chapter and NATEA in 1999, the New Frontiers in Computing Conference aims to provide computer and engineering professionals with enough technical information on a developing field to make informed decisions as to its role in their professional careers. NFIC strives to make all this accessible through an inexpensive one-day conference on emerging technologies such as Cloud Computing, Nanotechnology, Multi Core Processors and RFID.

Innovation in edge cloud and increased automation of technologies drive urban agglomeration to meet our lifestyle demands. Through keynotes, panelists, and presentations, this conference provides a means to enhance your understanding of the problems and solutions that are at trial in communities and the workplace.

The conference will address the innovation in edge cloud and the increased automation of associated technologies that are driving urban agglomeration to meet our lifestyle demands. In addition, we will explore how these technologies are being used in:

-Mobile Edge Computing with Distributed Cloud

-Smart Devices and Gateways

-Location-Based Applications

At the end of this conference, we hope you are equipped with the knowledge and tools to collaborate with your communities. Most importantly, we hope that you will carry forth the vision of bringing cutting-edge technologies and innovations to ensure that all benefit from the improved standards of living that smart and connected communities offer.

More info at:

https://ieee-nfic.org/program/

https://ieee-nfic.org

Dell’Oro: Market for disaggregated WDM systems increased 142% YoY in 1Q-2018

A new report from market research firm Dell’Oro Group states the market for disaggregated WDM platforms increased at a 142% year-over-year (YoY) growth in sales in the first quarter of this year. This high growth was driven by the adoption of disaggregated WDM systems expanding beyond web-scale companies and data center interconnect (DCI).

“Small form factor, disaggregated WDM systems were developed for the hyperscalers,” said Jimmy Yu, Vice President at Dell’Oro Group. “And for a long period of time, they were the only large purchasers. However, now we see a growing number of buyers that include cable operators and wholesale carriers. We think this is just the start of a good thing, and expect demand for these disaggregated systems will continue to grow at a hyper-scale rate,” added Yu.

Disaggregated WDM systems reached an annualized revenue run-rate of $800 million in the first three months of this year and Dell’Oro projects the run rate will exceed $925 million for full-year 2018. Ciena and Infinera currently have enjoyed the most success in this niche, with a combined market share of approximately 60% for the trailing four quarters ending in 1Q-2018.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Author’s Note: The move towards disaggregated network equipment started in the Open Compute Project (OCP) Networking and Telco groups. It’s now being propelled forward by the the Telecom Infra Project (TIP) which aims to create greater innovation and flexibility through disaggregation of traditional (vendor specific/proprietary) network equipment. TIP is also attempting to disaggregate optical line terminal equipment (e.g. OLT) and transmission systems such as those that use mmWave frequencies. We first wrote about this disaggregation mega-trend almost three years ago in this article.

Here’s a schematic of an open line system (OLS), which allow transponders from many different suppliers to share a single line system:

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Dell’Oro Group’s “Optical Transport Quarterly Report” provides tables stating manufacturers’ revenue, average selling prices, and unit shipments (by speed, including 40 Gbps, 100 Gbps, 200 Gbps, and 400 Gbps). The report tracks DWDM long-haul terrestrial, WDM metro, multiservice multiplexers (SONET/SDH), optical switches, optical packet platforms, and data center interconnect (metro and long haul).

To purchase this report, call Daisy Kwok at +1.650.622.9400 x227 or email [email protected].

About Dell’Oro Group

Dell’Oro Group is a market research firm that specializes in strategic competitive analysis in the telecommunications, networks, and data center IT markets. Our firm provides in-depth quantitative data and qualitative analysis to facilitate critical, fact-based business decisions. For more information, contact Dell’Oro Group at +1.650.622.9400 or visit www.delloro.com.

Smart Cities Week Silicon Valley: Lots of Progress in Many Areas

Introduction:

Smart Cities Week Silicon Valley was held May 7-9, 2018 at the Santa Clara Convention Center. In addition to highlighting the many new technologies deployed, practicalities such as financing, procurement, stakeholder engagement and program management were also discussed. For example, projects become a much easier sell if an agency can find alternative funding methods. Panelists outlined five of those methods: Monetizing infrastructure, Revenue sharing, Monetizing data, Fees and fare collection, Cost savings.

This article presents just a few highlights of this outstanding conference which should be a must attend for city officials everywhere.

………………………………………………………………………………………………………………………………………………………………….

Summary of Selected Sessions:

May 7th Workshop: Industry Exchange: Smart City Technology and Planning Standards; Moderator: Zack Huhn – Founder, Venture Smarter

Standards and guidance documents play a critical role in describing good practice and clearly set out what needs to be done to comply with specified outcomes. They help in the planning, design, manufacturing, procurement and management processes to ensure goods and services supplied are fit for purpose. This workshop discussed the emerging IEEE standard on developing a technology and process framework for planning a smart city.

IEEE PROJECT 2784 – Guide for the Technology and Process Framework for Planning a Smart City

This guide will provide a framework that outlines technologies and the processes for planning the evolution of a smart city. Smart Cities and related solutions require technology standards and a cohesive process planning framework for the use of the internet of things to ensure interoperable, agile, and scalable solutions that are able to be implemented and maintained in a sustainable manner. This framework provides a methodology for municipalities and technology integrators to use as a tool to plan for innovative and technology solutions for smart cities.

Approval Date: 28-Sep-2017 PAR Expiration Date: 31-Dec-2021 Status: PAR for a New IEEE Standard 1.1 Project Number: P2784 1.2 Type of Document: Guide

“We have been working to create agile, secure, interoperable and financially sustainable technology standards and planning guidelines for municipal leaders to support the vision of building smart cities and connected communities – regardless of socioeconomic or geographical barriers.” — ZACK HUHN

–>Much more in a forthcoming article about this IEEE Smart Cities Standards Project.

…………………………………………………………………………………………………………………

May 8th Panel Session- Transportation Investments: the Building Blocks for Tomorrow’s City

Transportation officials addressed the progress city, regional and state agencies are making towards planning for the future of mobility through investments in transportation infrastructure. With objectives such as increasing transportation options, enhancing the quality of life and improving sustainability, practitioners will address how planning, coordination with other departments to bring a range of services, creative financing and public-private partnerships that modern mobility possible.

Moderator

Jason Goldman – Vice President, ITSA

Speakers

Roger Millar – Secretary, Washington State Department of Transportation

Stefano Landi – Global Sales, Business Development & Partnerships, Verizon

Dan McElhinney – District 4 Chief Deputy District Director, CalTrans

Some characteristics and attributes of smart cities are: intelligent lighting and energy, smart traffic management, traffic data collection, driver aware parking, public safety, and intersection control through safety analytics.

Verizon is partnering with cities to provide connectivity solutions including small cells, fiber backhaul, 4G/5G/WiFi, and NB-IoT.

CALTRANS District 4 (SF Bay Area) is trying to control traffic congestion by ramp metering which is key element of the state’s Transportation Management System (TMS). They are also working on Smart Corridors like Contra Costa I-80.

CALTRANS/CHP goal is to clear major highway accidents withing <=90 minutes of occurrence. That objective was achieved in 75% of such incidents in Fiscal Year 2015/2016 (the latest year for which figures were available).

Somewhat surprisingly, CALTRANS is putting in a lot more fiber optic communications near roads and highways- mainly because of its reliability and future proof bandwidth capacity.

A vision of the CALTRANS Intelligent Transportation System is depicted in the following figure:

Image courtesy of CALTRANS

……………………………………………………………………………………………………………………………………………..

Future Ready — Growing an Innovation Ecosystem in your Community — Learn from Experienced Practitioners:

Through governance, regulation and investment, the public sector can create an environment in which innovation occurs. Cities, counties, states and other units offer access to technology and data, set policies that support startups through simplified regulations and licensing, and host incubators and accelerators. In this session, you will hear from practitioners from the San Diego region, the state of California and an Australian NGO about their efforts to create a climate of innovation and entrepreneurship.

Moderator

Emma Hendry – CEO, Hendry

Speakers

Marty Turock – Strategic Projects Consultant, Clean Tech San Diego

Erik Stokes – Manager, Energy Deployment and Market Facilitation Office California Energy Commission

Johanna Pittman – Program Director, CityConnect

It seems like the city of San Diego has made tremendous progress in intelligent clean tech and micro-grids, which may have replaced the “smart grid” so many experts were talking about several years ago.

Meanwhile, the California Energy Commission established BlueTechValley as part of a major $60 million initiative Commission launched about 18 months ago to really try to create a state-wide ecosystem to support clean energy entrepreneurship across the state.

“As part of this initiative, we created four regional innovation clusters to manage a network of incubator-type services that can encourage clean tech entrepreneurs in the region and really try to help make what can be a very tough road towards commercialization a little bit easier,” Erik Stokes said.

“BlueTechValley and their partners were selected to be the Central Valley cluster. A big reason for that was their strength and expertise in the food and agricultural sector,” he explained. One of the focus areas of the incubator is to find areas in farming to save costs and minimize greenhouse gases. “We really want to focus on those technologies that can help both reduce water use, as well as energy use,” Stokes added.

In a private chat, Erike opined that a lot of the “smart grid” platform vendors had migrated their offerings to data analytics for energy consumption and prediction of future usage trends.

Future Ready Cities — The Robust Mobile Network and Why You Need it Now:

Cities depend on mobile networks for day-to-day operations and delivery of citizen services, and this dependence is growing rapidly. In this session, mobile operators and local government officials will address the critical role of IoT applications for not only transportation, public safety and sustainability, but also for stimulating entrepreneurship, innovation and economic growth.

Speakers

David Witkowski – Executive Director of Civic Technologies, Joint Venture Silicon Valley

Peter Murray – Executive Director, Dense Networks

Rebecca Hunter – External Affairs, Corporate Development & Strategy, Crown Castle

Geoff Arnold – CTO, Verizon Smart Communities

Dolan Beckel – Smart City Lead, City of San Jose

……………………………………………………………………………………….

Closing Quotes:

“We need to be talking about smart regions, not smart cities” -Joy Bonaguro, Chief Data Officer, City of San Francisco.

“Most cities measure performance and miss the boat on measuring effectiveness. You can quantify subjective well-being and should” – Shanna Draheim, Michigan Municipal League Policy Director.

“The idea that we have to disrupt to move forward has poisoned our thinking. We should not discount incremental steps toward a solution. We should ask ourselves – what are the small changes we can make that over time lead to significant outcomes?” – Deb Socia, Executive Director of Next Century Cities – a public interest initiative helping cities that want fast, affordable, reliable broadband.

“The first-ever Smart Cities Readiness Hub at Smart Cities Week Silicon Valley paired cities that are starting their efforts with those who have already blazed a trail — and all gained useful insights.” – Smart Cities Council. Watch the video here.

…………………………………………………………………………………………………

About Smart Cities Council:

The Smart Cities Council, envisions a world where digital technology and intelligent design are harnessed to create smart, sustainable cities with high-quality living and high-quality jobs. A leader in smart cities education, the Council is comprised of more than 120 partners and advisors who have generated US$2.7 trillion in annual revenue and contributed to more than 11,000 smart cities projects.

…………………………………………………………………………………………………

Addendum: Smart Cities Market:

Global Smart Cities industry was valued at approximately $343 billion in 2016 and is anticipated to grow at a rate of more than 24.4% from 2017-2025 according to Research for Markets. The increasing demands for integrated security, safety systems improving public safety and the rising demand for system integrators are the key drivers for this market. Recent technological advancements in smart cities can also be included as a key driver.

Some of the important manufacturers involved in the Smart Cities market are Hewlett Packard Enterprise, Ericsson, General Electronics, Delphi, IBM Co., CISCO Systems Inc., Schneider Electric SE, and Accenture Plc. Those companies are investing in smart grid technologies. A major part of this is going into upgrading the outdated energy infrastructure with new and advanced infrastructure. Acquisitions and effective mergers are some of the strategies adopted by the key manufacturers.

GM and Toyota back DSRC to link connected cars to “smart” traffic lights; Ford, BMW, other auto makers favor “5G”

by Chester Dawson

Excitement around “5G” is eclipsing the prospects for a competing technology that General Motors Co. and Toyota Motor Corp. are backing, potentially giving rivals a leg-up in the race to debut vehicles with state-of-the-art internet connectivity.

The U.S. government has invested hundreds of millions of dollars in Wi-Fi-based technology known as DSRC (dedicated short-range communications)[1], that allows cars to link to “smart” traffic lights designed to smooth congestion and provide warnings about accidents or poor weather conditions ahead.

Note 1. DSRC (Dedicated Short Range Communications) is a two-way short- to- medium-range wireless communications capability that permits very high data transmission critical in communications-based active safety applications.

……………………………………………………………………………………………………………………………………………………………………………………………………

GM and Toyota strongly support DSRC technology. But Ford Motor Co., BMW AG and other auto makers are pressing the Trump administration to allow them to leapfrog that system by fast-tracking fifth-generation cellular broadband in automobiles. “5G” will transmits data at up to 10 times the speed of current broadband and improves reliability by potentially shrinking a self-driving car’s ability to stop to one inch, from one yard with today’s network.

The showdown between the Wi-Fi-based and 4G or 5G cellular-based standards for connected cars echoes winner-take-all format wars in other industries, and is a sign of how software is emerging as a new battleground for auto makers. The stakes are high as U.S. motor-vehicle deaths have risen in recent years. Car makers say vehicle-to-vehicle communication will ease congestion and improve safety.

Speeding up adoption of new technology is a priority for an industry that has lagged behind mobile-phone makers when it comes to connecting devices to the internet. The global market for connected cars is forecast to grow nearly threefold by 2022 with more than 125 million new internet-connected cars shipped over that five-year period, according to Counterpoint Research.

Current broadband, known as 4G, has enabled Wi-Fi hot spots and streaming, allowing passengers to surf the internet or watch videos in cars. The next wave of cellular technology will usher in new entertainment and safety features, enabling cars to access cameras on other vehicles that could alert them to accidents, obstacles and driving conditions.

Ultimately, drivers might even be able to order a Starbucks drink from their dashboard or take a nap while artificial intelligence operates the vehicle. Companies like BMW say faster data transmission through next-generation broadband is critical to accelerating this push.

“We are on a broader scale pushing the telecommunication companies to roll out 5G as quickly as they can,” said BMW management board member Peter Schwarzenbauer.

GM and Toyota, meanwhile, have models already equipped with DSRC, and are urging the Trump administration to support a 2016 proposal that would require auto makers to start phasing it into new cars as of 2021. The Transportation Department has yet to make a final ruling on that Obama-era proposal, even as auto makers are already well into the design phase of 2021 model year vehicles.

“Getting the rest of the industry to follow has been tough sledding,” said Steve Schwinke, director of GM’s advanced development and connected services.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

One issue with the technology backed by GM and Toyota is cost. Telecom companies plan to pay for upgraded cell towers and roadside antennas for 5G to service their existing networks. To fully deploy DSRC, billions of dollars in government-funded infrastructure is required, according to a U.S. Transportation Department estimate.

That short-range technology also would add about $300 to the price of a vehicle for dedicated equipment, the National Highway Traffic Safety Administration estimates. Most new vehicles come installed with cellular modems, so there would be little additional cost to drivers for 5G.

GM and Toyota alone account for about one-third of the new cars sold in the U.S., and roughly 20% of the vehicles sold world-wide. Toyota has delivered more than 100,000 cars equipped with DRSC in Japan and will offer it on most of its lineup in the U.S. by the mid-2020s in addition to cellular modems.

GM and Toyota see their Wi-Fi-based technology as a bridge to 5G, which has yet to be fully tested in vehicles and may take years to be fully deployed.

Critics say the government shouldn’t force car makers to use older Wi-Fi-based technology some say is out of sync with fast-evolving cellular broadband. Last month, Audi and Ford demonstrated cellular-based safety technology called C-V2X in what they said was the world’s first application of it using vehicles from different manufacturers.

“You will have, for the first time, cars speaking together and it’s important for them to speak the same language,” said Christoph Voigt, head of R&D connectivity for Audi. As chairman of 5GAA, a trade group supporting automotive 5G, Mr. Voigt petitioned federal regulators to avoid “directly or indirectly pick[ing] technology winners and losers” because he is confident 5G will become the de facto standard on its own merits.

Even as Volkswagen AG is aligning its premium Audi brand with 5G in the U.S. and China, it is hedging its bets by deploying a version of DSRC on VW branded vehicles in Europe starting next year. A representative for VW said the German auto maker currently has no plans to introduce that technology to its lineup in the U.S. market.

The Trump administration, pointing to the expected proliferation of 5G, this year blocked the takeover of U.S. chip maker Qualcomm Inc. by Singapore-based Broadcom Ltd. on national-security grounds. Qualcomm is negotiating chip supply contracts with at least half a dozen auto makers for coming models.

Industry experts say 5G smartphones will debut next year and the first cars with 5G modems will appear as soon as 2020. That is about twice as fast as the transition for current 4G technology, which was introduced for smartphones in 2011 but didn’t show up in cars until GMintegrated it into its latest version of OnStar remote communications in 2014.

“There is going to be 5G in every single next-generation car design,” said Nakul Duggal, the head of Qualcomm’s automotive business.

Write to Chester Dawson at [email protected]

References:

https://www.wsj.com/articles/auto-makers-at-odds-over-talking-car-standards-1525608000

https://www.its.dot.gov/factsheets/pdf/JPO-034_DSRC.pdf

https://www.its.dot.gov/factsheets/dsrc_factsheet.htm

https://en.wikipedia.org/wiki/Dedicated_short-range_communications

T-Mobile, Sprint Combo Bypasses Dish; With spectrum plus linear and OTT subscribers, satellite provider was seen as a logical partner

By Michael Farrell of Multichannel News

The announced merger of T-Mobile and Sprint, the third- and fourth-largest wireless carriers in the nation, answers many of the scale questions that have dogged the two companies over the past several years. But in creating a carrier with about 100 million customers and valued at a combined $146 billion, the deal bypasses what many had considered to be T-Mobile’s more perfect match: Dish Network.

With a large swath of wireless spectrum, 11 million satellite TV subscribers and 2.2 million customers for its over-the-top video service Sling TV, Dish was seen by many to be a logical target for T-Mobile. Combining the No. 3 wireless carrier, which has obvious video aspirations through its January purchase of Layer3 TV, with Dish would in many minds have created a strong competitor in the ongoing wireless-OTT-traditional video wars.

Investors apparently believed so too. Shares in Dish fell 3% ($1.19 each) to $33.55 per share on April 30, the first trading day after T-Mobile and Sprint announced their deal. The stock has continued to slip in subsequent trading, closing at $33.09 on May 3.

Video Plans ‘Ratchet Up’

On a conference call to discuss first-quarter results shortly after the Sprint deal was announced, T-Mobile chief financial officer Braxton Carter said the transaction “ratchets up” the wireless provider’s video plans by allowing the combined company to provide customers with an IPTV service via wireline and wireless broadband.

“So T-Mobile’s in the position as a new T-Mobile to be able to offer a quad play, if that’s what the market wants,” Carter said on the call.

The combined company will be controlled by T-Mobile management: CEO John Legere will continue that role in the new entity, as will T-Mobile chief operating officer Mike Sievert. T-Mobile parent Deutsche Telekom will own 42% of the combined company, with Sprint parent Softbank owning 27% and the remaining 31% held by the public. The deal is expected to close in the first half of next year.

This is the two companies’ third time on the merger dance floor together. They scrapped talks in 2014 over regulatory concerns and in 2017 over control issues. While the two have managed to work out their control issues, some analysts are skeptical that the current deal will sail easily through the regulatory process.

BTIG telecom analyst Walt Piecyk gave the merger a less than 40% chance of passing regulatory muster, primarily because he didn’t believe the deal, which will reduce the number of wireless competitors to three from four, will pass the antitrust smell test.

“It doesn’t look like a competitive market right now, and that’s what the regulator may focus on,” Piecyk told CNBC.

Columbia Law professor Tim Wu wrote an op-ed piece for The New York Times urging regulators to block the deal, adding that having four separate competitors has been most beneficial to wireless customers, leading to free unlimited data plans and lower prices. Transforming the wireless business into a “triopoly” like the airline business will only serve to raise prices and lower service.

“Competition has actually worked the way economists say it is supposed to, forcing firms to improve quality or face elimination,” Wu wrote in the Times. “But it takes competitors to compete, which is where blocking mergers comes in.”

Pivotal Research Group CEO and senior media & communications analyst Jeff Wlodarczak has said in research notes over the past year that pairing Dish and T-Mobile would “immediately vault the most disruptive U.S. wireless player into the leading U.S. spectrum position,” and at worst would force rival wireless company Verizon Communications to pay more for the satellite asset. For now, though, it looks like Dish will remain on its own. Other scenarios see the satellite company being acquired either by another wireless service provider, like Verizon, or even by the new T-Mobile. The latter scenario wouldn’t take place for at least another year. Dish has struggled over the past several quarters as the satellite business has dwindled. In the fourth quarter the company lost more than 100,000 satellite-TV subscribers and added 160,000 Sling TV customers.

Dish Misses Out on Buildout Relief

For Dish, a purchase by a wireless carrier would mean relief from its obligation to build its own wireless network. As a result of its success in bidding on spectrum in several of the government’s wireless auctions, Dish faces a March 2020 deadline to build out wireless service in 70% of the market territories it won.

Dish chair Charlie Ergen has said the company will spend about $1 billion on that initial phase, which will be more geared toward IoT services.

For T-Mobile, a Dish purchase would give it an instant video base through the satellite-TV offering, programming contracts with cable networks and the largest OTT service in the country, Sling TV.

But not all analysts believe that a T-Mobile-Dish deal is more palpable. In a research note in November, after T-Mobile and Sprint ended merger talks, MoffettNathanson principal and senior analyst Craig Moffett wrote that he never saw any synergies in combining those companies, other than as a source of additional spectrum.

The argument that the dissolution of the merger was bad news for Dish is equally compelling in that, if Dish does build its wireless network, it would become the fifth player in an already-crowded market, he added.

“However bad one might have imagined the ROI (Return on Investment) for network building, it has to be worse if the industry is more fragmented than expected,” Moffett wrote in November.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Dish’s Spectrum Yet to be Deployed:

Dish has quietly worked to cobble together a significant amount of spectrum via spectrum auctions and secondary-market transactions. The company’s first spectrum purchase was made through EchoStar’s relatively minor purchase of E Block licenses for $700 million in the FCC’s 700 MHz spectrum auction in 2008. But Dish in 2011 spent $2.77 billion to acquire 40 MHz of S-band satellite spectrum from bankrupt TerreStar and DBSD North America. Then, in 2014, Dish was the only bidder in the FCC’s H Block spectrum auction, essentially walking away uncontested with 10 MHz for around $1.6 billion. In 2015, Dish spent roughly $8 billion on AWS-3 spectrum licenses, and then just two years later it committed a whopping $6.2 billion to buy 486 licenses in the FCC’s 600 MHz incentive auction.

Dish recently outlined plans to build a NB-IoT network using its spectrum to provide connectivity to a wide range of devices other than traditional tablets and smartphones. Some analysts remain skeptical, though, believing that Dish plans to either sell or lease its spectrum, or partner with an existing service provider to join the wireless market.

Dish has to comply with Federal Communications Commission requirements that a network using the spectrum it owns be deployed by 2020, Josh Yatskowitz, an analyst at Bloomberg Intelligence, said last November.