Uncategorized

Comment & Analysis of Century Link’s 2nd Quarter results

broadband units. Consumer legacy revenue declined 8.8% Y/Y – lower access lines.

in employee-related expenses.

“We are confident our continued investment in high-quality, high-bandwidth broadband network infrastructure positions Century Link well for long-term growth,” said Glen F. Post, III, Century Link chief executive officer and president.

“Enterprise demand for high-bandwidth data services remains strong and, while consumer broadband units were weaker than expected, we are encouraged by the higher-value customers our improved offerings are attracting. We accelerated our capital investment in high-bandwidth services and broadband infrastructure during the second quarter, which we believe better positions us to increase revenues in the second half of 2017 and beyond. We anticipate second half and full year 2017 capital expenditures of approximately $1 billion and $2.6 billion, respectively.

“We achieved our expected adjusted EBITDA for the quarter as our employees did a great job managing costs, while core revenues were below our expectations primarily due to the decline in legacy revenues and the decline in broadband units being higher than anticipated. We continue to make good progress in obtaining the necessary approvals for the pending Level 3 acquisition, having received clearance in 23 of 25 required states and territories. Integration planning is progressing well and we continue to anticipate completing the acquisition by the end of September 2017. We remain excited about the value we believe this transaction will create for our customers, our shareholders and our employees,” concluded Mr. Post.

……………………………………………………………………………………….

Century Link’s presentation – 2ndQ 2017 Highlights & Trends:

1. Strategic services:

◦ Enterprise high-bandwidth data – solid growth in MPLS revenue offset by decline in Ethernet revenue; grew 5% Y/Y on a normalized basis

◦ IT & Managed services – continued growth in IT Services along with stabilization of managed hosting revenue

◦ Enterprise other strategic – ~$100 million Y/Y and Q/Q decline due to Colo-cation sale

◦ Consumer broadband – fewer subscribers Y/Y

◦ Consumer video – impact of satellite video contract restructuring

2. Acquisition of Level 3 Communications:

◦ Continued good progress in obtaining necessary approvals; received shareholder

approval and regulatory approvals/clearances in 23 states or territories, with 2 states

remaining

◦ Integration planning process continues to go well; remain confident with cash synergy target of $975 million

◦ Named combined company senior leadership team, effective at close; overall

organization design progressing well

◦ Continue to anticipate closing by end of September 2017

Forward Guidance:

Based on first half 2017 results and current expectations for the remainder of the year, Century Link anticipates coming in slightly below its full-year 2017 revenue and adjusted diluted EPS guidance, primarily driven by higher legacy revenue declines and lower consumer broadband revenue growth than anticipated. The company continues to expect adjusted EBITDA and adjusted free cash flow to be near the lower end of prior guidance.

Century Link is not providing updated guidance ranges for full-year 2017 due to the pending acquisition of Level 3, currently anticipated to be completed by the end of third quarter of 2017, and the expected consolidation of results for the combined companies in fourth quarter 2017.

Earnings Call:

The call will be accessible for replay through August 9, 2017, by dialing 855-859-2056. Investors can also listen to Century Link’s earnings conference call and webcast replay by accessing the Investor Relations portion of the company’s website at www.centurylink.com through August 24, 2017. Here are a few highlights:

First, we continue to outperform MPLS market growth projections forecasted by leading industry analysts. In second quarter, we had nearly 2,000 MPLS customers. This performance was driven in particular by our SMB customers, where we are seeing improved install intervals of nearly 20%, which should help accelerate our revenue recognition as we move into the third and fourth quarters of this year. Next, we launched a number of new products and – we’ve launched a number of new products in the past few months including our CenturyLink Ethernet service.

We’ve also had three simplified bundles of SD-WAN plus network packages. We rolled out a competitively priced cloud-enabled small business VoIP offering. And we rolled out a new comprehensive managed Enterprise offering that is an end-to-end solution that includes WiFi management, network management, video surveillance, security and mobility management, all from a single interface. Also we have increased focus on customer retention and we are seeing lower credits and adjustments as a result.

In addition, CenturyLink continues to be one of the leaders in network virtualization through the deployment of software-defined networking and network virtualization capabilities. Based on initial results, we expect these services to create significant value in the months ahead. Also the continuous onslaught of new security threats, such as WannaCry has brought greater interest in and sales of our strong network and cyber security capabilities, as we believe CenturyLink is growing in recognition as a leading provider of security services that are so important to our Enterprise customers.

And lastly, based on third-party research support, U.S. Enterprise high-bandwidth data services are forecast to grow at mid-single-digit compounded annual growth rates through 2021, and U.S. Enterprise Managed Network Services are forecast to grow at mid to upper single-digit compounded annual growth rates through 2021. Now this forecast gives even more confidence in the opportunity to continue to grow Enterprise business in the months ahead.

Second, our IT services revenue, which is primarily driven by IT consulting, cyber security, IT service management and big data and analytics, is growing. And our managed hosting business also showed a solid turnaround this quarter. The team overcame the market confusion and sales disruption created by the colocation sale and grew cloud revenue, especially driven or aided by our Cloud Application Manager suite.

Next as expected, we had a seasonally challenging quarter from consumer broadband subscribers approximately 65,000 residential subscriber loss was higher than anticipated. This was driven to a great degree of our stronger cable competition, particularly 1 gig offerings in some of our key markets, coupled with aggressive pricing. Over the past year, we have made a pivot towards higher-quality, more profitable consumer broadband sales by removing several low-priced promotional offers and increased credit standards.

……………………………………………………………………………………………….

References:

http://ir.centurylink.com/Cache/1500102071.PDF?O=PDF&T=&Y=&D=&FID=1500102071&iid=4057179

http://ir.centurylink.com/Cache/1500102077.PDF?O=PDF&T=&Y=&D=&FID=1500102077&iid=4057179

http://services.choruscall.com/links/ctl170802.html

http://www.centurylink.com/business/enterprise/cloud/public-cloud.html

https://techblog.comsoc.org/2017/05/24/centurylinklevel-3-says-its-fiber-assets-will-attract-smbs/

J.D. Power: SMB a Growth Opportunity; Telecom ARPU Falling in Every Region

Comment & Analysis of Century Link’s 2nd Quarter results

broadband units. Consumer legacy revenue declined 8.8% Y/Y – lower access lines.

in employee-related expenses.

“We are confident our continued investment in high-quality, high-bandwidth broadband network infrastructure positions Century Link well for long-term growth,” said Glen F. Post, III, Century Link chief executive officer and president.

“Enterprise demand for high-bandwidth data services remains strong and, while consumer broadband units were weaker than expected, we are encouraged by the higher-value customers our improved offerings are attracting. We accelerated our capital investment in high-bandwidth services and broadband infrastructure during the second quarter, which we believe better positions us to increase revenues in the second half of 2017 and beyond. We anticipate second half and full year 2017 capital expenditures of approximately $1 billion and $2.6 billion, respectively.

“We achieved our expected adjusted EBITDA for the quarter as our employees did a great job managing costs, while core revenues were below our expectations primarily due to the decline in legacy revenues and the decline in broadband units being higher than anticipated. We continue to make good progress in obtaining the necessary approvals for the pending Level 3 acquisition, having received clearance in 23 of 25 required states and territories. Integration planning is progressing well and we continue to anticipate completing the acquisition by the end of September 2017. We remain excited about the value we believe this transaction will create for our customers, our shareholders and our employees,” concluded Mr. Post.

……………………………………………………………………………………….

Century Link’s presentation – 2ndQ 2017 Highlights & Trends:

1. Strategic services:

◦ Enterprise high-bandwidth data – solid growth in MPLS revenue offset by decline in Ethernet revenue; grew 5% Y/Y on a normalized basis

◦ IT & Managed services – continued growth in IT Services along with stabilization of managed hosting revenue

◦ Enterprise other strategic – ~$100 million Y/Y and Q/Q decline due to Colo-cation sale

◦ Consumer broadband – fewer subscribers Y/Y

◦ Consumer video – impact of satellite video contract restructuring

2. Acquisition of Level 3 Communications:

◦ Continued good progress in obtaining necessary approvals; received shareholder

approval and regulatory approvals/clearances in 23 states or territories, with 2 states

remaining

◦ Integration planning process continues to go well; remain confident with cash synergy target of $975 million

◦ Named combined company senior leadership team, effective at close; overall

organization design progressing well

◦ Continue to anticipate closing by end of September 2017

Forward Guidance:

Based on first half 2017 results and current expectations for the remainder of the year, Century Link anticipates coming in slightly below its full-year 2017 revenue and adjusted diluted EPS guidance, primarily driven by higher legacy revenue declines and lower consumer broadband revenue growth than anticipated. The company continues to expect adjusted EBITDA and adjusted free cash flow to be near the lower end of prior guidance.

Century Link is not providing updated guidance ranges for full-year 2017 due to the pending acquisition of Level 3, currently anticipated to be completed by the end of third quarter of 2017, and the expected consolidation of results for the combined companies in fourth quarter 2017.

Earnings Call:

The call will be accessible for replay through August 9, 2017, by dialing 855-859-2056. Investors can also listen to Century Link’s earnings conference call and webcast replay by accessing the Investor Relations portion of the company’s website at www.centurylink.com through August 24, 2017. Here are a few highlights:

First, we continue to outperform MPLS market growth projections forecasted by leading industry analysts. In second quarter, we had nearly 2,000 MPLS customers. This performance was driven in particular by our SMB customers, where we are seeing improved install intervals of nearly 20%, which should help accelerate our revenue recognition as we move into the third and fourth quarters of this year. Next, we launched a number of new products and – we’ve launched a number of new products in the past few months including our CenturyLink Ethernet service.

We’ve also had three simplified bundles of SD-WAN plus network packages. We rolled out a competitively priced cloud-enabled small business VoIP offering. And we rolled out a new comprehensive managed Enterprise offering that is an end-to-end solution that includes WiFi management, network management, video surveillance, security and mobility management, all from a single interface. Also we have increased focus on customer retention and we are seeing lower credits and adjustments as a result.

In addition, CenturyLink continues to be one of the leaders in network virtualization through the deployment of software-defined networking and network virtualization capabilities. Based on initial results, we expect these services to create significant value in the months ahead. Also the continuous onslaught of new security threats, such as WannaCry has brought greater interest in and sales of our strong network and cyber security capabilities, as we believe CenturyLink is growing in recognition as a leading provider of security services that are so important to our Enterprise customers.

And lastly, based on third-party research support, U.S. Enterprise high-bandwidth data services are forecast to grow at mid-single-digit compounded annual growth rates through 2021, and U.S. Enterprise Managed Network Services are forecast to grow at mid to upper single-digit compounded annual growth rates through 2021. Now this forecast gives even more confidence in the opportunity to continue to grow Enterprise business in the months ahead.

Second, our IT services revenue, which is primarily driven by IT consulting, cyber security, IT service management and big data and analytics, is growing. And our managed hosting business also showed a solid turnaround this quarter. The team overcame the market confusion and sales disruption created by the colocation sale and grew cloud revenue, especially driven or aided by our Cloud Application Manager suite.

Next as expected, we had a seasonally challenging quarter from consumer broadband subscribers approximately 65,000 residential subscriber loss was higher than anticipated. This was driven to a great degree of our stronger cable competition, particularly 1 gig offerings in some of our key markets, coupled with aggressive pricing. Over the past year, we have made a pivot towards higher-quality, more profitable consumer broadband sales by removing several low-priced promotional offers and increased credit standards.

……………………………………………………………………………………………….

References:

http://ir.centurylink.com/Cache/1500102071.PDF?O=PDF&T=&Y=&D=&FID=1500102071&iid=4057179

http://ir.centurylink.com/Cache/1500102077.PDF?O=PDF&T=&Y=&D=&FID=1500102077&iid=4057179

http://services.choruscall.com/links/ctl170802.html

http://www.centurylink.com/business/enterprise/cloud/public-cloud.html

https://techblog.comsoc.org/2017/05/24/centurylinklevel-3-says-its-fiber-assets-will-attract-smbs/

J.D. Power: SMB a Growth Opportunity; Telecom ARPU Falling in Every Region

Sprint Reports 1st Net Income in 3 years; CEO Says Merger Decision Coming Soon

As we’ve previously reported, Sprint is exploring various M &A options, including a merger with rival wireless carrier T-Mobile US Inc as well as a tie-up with cableco/ MSO Charter Communications Inc. Japan’s SoftBank Group Corp owns approximately 80% of the company.

“We’ve had sufficient conversations with several parties and soon we’re going to start making decisions,” Sprint CEO Marcelo Claure said on a conference call Tuesday (see Reference 1. below for the replay) after the company reported results for the three months ending June 30. The company achieved net income of $206 million, compared to a loss of $302 million one year earlier. This was the first time in three years Sprint did not have a loss for any quarter. However, the positive net income was achieved via cost cutting. Sprint reported almost $370 million of combined year-over-year reductions in cost of services and selling, general and administrative expenses.

Sprint is in the middle of a turnaround plan and has sought to strengthen its balance sheet to compete in a saturated market for wireless service. Although Sprint has cut costs, analysts have said the company is highly leveraged. While its customer base has expanded under Mr. Claure, growth has been driven by heavy discounting. It recently offered free wireless service (including unlimited data) for one year to new subscribers. Sprint’s CEO had previously hinted that the #4 U.S. wireless carrier doesn’t have the necessary funds to invest in 5G infrastructure, which gives more impetus to some type of M&A deal if Sprint is to survive.

A person familiar with the matter told Reuters that SoftBank CEO Masayoshi Son is considering making an acquisition offer for the cable company to combine it with Sprint as early as the end of August. The deal would entail SoftBank buying the Sprint shares it does not already own, the Reuters source said.

“The talks with T-Mobile have been encouraging, the talks with other partners have been encouraging,” Mr. Claure said. “Everybody has shown a high level of interest in evaluating Sprint as a potential merger partner,” he added.

The Wall Street Journal reported (on line subscription required) that the offer being considered by Sprint’s chairman and SoftBank founder, Masayoshi Son, would be to form a new publicly traded entity that would use SoftBank money to buyout shareholders of both Sprint and Charter at a premium. The transaction would be funded with roughly half cash and half stock. The deal would result in SoftBank controlling the combined company.

SoftBank has already lined up financing from at least three banks to fund the deal, according to people familiar with the matter. One of them cautioned that it could still take several weeks or more to reach an agreement with either company.

Mr. Claure said a deal with T-Mobile might be the preferred option, but it would be tougher to get past antitrust regulators in Washington. Sprint and T-Mobile held merger talks in 2014 but backed down in the face of regulator opposition.

“If you were to merge with another wireless carrier, the synergies are enormous. I mean, this is a scale business, and today you need to operate two competing networks to offer the same service, having half the amount of customers that AT&T and Verizon have,” Mr. Claure said.

A Charter deal poses its own hurdles, particularly since the company said Sunday that it isn’t interested in buying Sprint. Mr. Claure said Tuesday that Sprint didn’t offer to sell itself, so he was “surprised to see Charter’s announcement.”

Were Sprint to go it alone, the results it reported on August 1st show it has a rough road ahead. The carrier drew praise from analysts for posting its first quarterly profit in three years—$206 million compared with a loss of $302 million a year ago—but revenue fell 4.5% to $8.2 billion and it added fewer customers than rivals. While Sprint started investing more money in network improvements, its quarterly profit came primarily from cost-cutting.

The company said it had 88,000 postpaid phone additions during the quarter, the eighth consecutive period of expansion. However, the pace of growth has slowed from a year ago when the company reported 173,000 postpaid additions. Overall, it still suffered a net loss of 39,000 postpaid subscribers (a figure that includes things like tablets and smartwatches.)

Mr. Claure said Sprint will be fine without a deal, but “doing a strategic transaction will always be significantly better than having a stand-alone entity.”

……………………………………………………………………………………………………

“The obvious risk in so openly courting one potential suitor after another is that Sprint will increasingly be viewed as damaged goods,” said analyst Craig Moffet in a research note to clients. “Like an unsold house that has sat too long on the market, an asset that has been shopped too often without success takes on an air of taint.”

……………………………………………………………………………….

References:

1. Sprint’s earning call webcast- available on demand requires registration at:

2. Sprint Reports Net Income for the First Time in Three Years with 1st Quarter of Fiscal 2017:

3. Earnings Results Presentation:

http://s21.q4cdn.com/487940486/files/doc_financials/quarterly/2017/q1/02_Q1FY17-Slides_Final.pdf

BT offers to spend up to £600M on rural broadband in the UK

BT has offered to spend up to £600M to connect the final 1M homes and businesses in rural areas of Britain to a broadband connection suitable for most needs. The telecom company said every home and business in the UK would have a broadband speed of at least 10 megabits per second (Mbits/s), fast enough to stream movies, video conference and browse the web.

Broadband endpoints will either be connected via the Openreach network through fiber-optic cables, a network of copper lines via xDSL, or through the fixed broadband wireless system, where connections use radio and, in some cases, satellite signals.

BT’s plan is for 99% of the UK population to be able to obtain a broadband service of at least 10 Mbit/s by 2020. That speed meets the needs of a typical household, according to UK regulatory authority Ofcom, but is less than the 2015 FCC broadband speed minimum of 25M bit/s (downstream).

About 93% of the UK population can already access a service of at least 24 Mbit/s, according to the UK government, but there has been concern about a growing “digital divide” as rural communities miss out on the broadband revolution.

The government said it was weighing BT’s proposal against a regulatory approach. “We warmly welcome BT’s offer and now will look at whether this or a regulatory approach works better for homes and businesses,” said Culture Secretary Karen Bradley in a weekend statement. “Whichever of the two approaches we go with in the end, the driving force behind our decision making will be making sure we get the best deal for consumers.”

Actual network construction is not due to finish until late 2021 or 2022, because of work on the rollout of fixed network technologies.

The UK government said rollout would take longer under a regulatory approach but highlighted the pricing implications of BT’s plan for rivals and broadband consumers.

“It is also proposed that BT would fund this investment and recover its costs through the charges for products providing access to its local access networks,” it said. “The approach to recovering these costs will be considered in Ofcom’s current wholesale local access review.”

Gavin Patterson, CEO of BT, said:“ We are pleased to make a voluntary offer to deliver the Government’s goal for universal broadband access at minimum speeds of 10Mbps. This would involve an estimated investment of £450m — £600m depending on the final technology solution.”

At the top end of this range, the investment would equal about 2.5% of BT’s revenues in its last fiscal year (to end-March 2017) and about 17% of overall capital expenditure across the Group.

BT said it would look to recover the cost of its investment by leasing the rural networks to its rivals. The offer will also be reflected in Ofcom’s current review of how to regulate the market for super fast, fiber-based networks of the future.

Capex soared by about £3.5 billion ($4.6 billion) at BT last year, largely because of spending on broadband roll outs. BT is planning several major investments in the coming years: it plans to extend all-fiber networks to around 2 million UK premises by 2020, and connect another 10 million homes and businesses to a xDSL technology called G.fast, which boosts connectivity speeds over last-mile copper loops. (See BT to Cover 2M Homes With FTTP in $8.7B Plan.)

Earlier this month, BT CEO Patterson said he was considering the viability of a much more ambitious fiber roll out that would benefit around 10 million premises by 2025. (See BT Rejigs Consumer Biz as Profits Hit by £225M Italy Payout.)

He has also indicated that BT will participate in an upcoming auction of airwaves that could be used to support new 5G services. Operators made crippling payments for spectrum licenses during previous auctions, although experts do not expect a 5G auction to generate a similar windfall.

References:

https://www.ft.com/content/a4ba67a4-73b0-11e7-aca6-c6bd07df1a3c

http://www.itproportal.com/news/bt-unveils-600m-scheme-to-bring-broadband-to-every-rural-uk-home/

J.D. Power: SMB a Growth Opportunity; Telecom ARPU Falling in Every Region

J.D. Power Report Highlights:

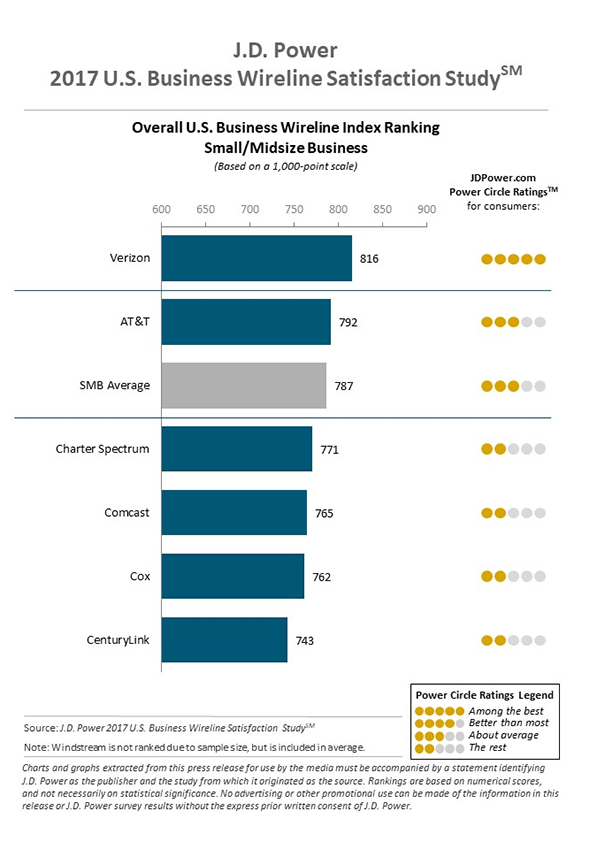

Enterprises with 500 or more employees are more likely to be satisfied with their telecom service, according to a report from J.D. Power, which sees the small- to medium-size business market as a growth opportunity for telcos. Medium-size businesses had an average satisfaction score of 787, J.D. Power said in a press release.

The J.D. Power report, which grades larger telecoms and cable companies, gives Verizon and AT&T the highest marks.

Verizon exceeded the average satisfaction level and topped the rankings for all three categories of businesses – small, mid-size and large. The company’s overall scores were 762, 816 and 821, respectively, for small, mid-size and large companies.

AT&T came in second place and exceeded the average score in the mid-size and large categories, with scores of 792 and 820, respectively. But Cox came in second among the smallest businesses, with a score of 744. AT&T followed at 730.

Cox was the only cableco to have a score above the average in any of the three categories. Among the telcos, CenturyLink also failed to have a score above the average in any category – a situation that company will want to address whenever its merger with Level 3 closes and the company becomes the most enterprise-focused of all the major service providers.

J.D. Power attributes the higher satisfaction level of the larger businesses to several factors, including higher satisfaction levels with communication, cost of service and customer service. Those companies with an account representative assigned to their business have notably higher overall satisfaction, researchers noted – and larger companies are more likely to have account representatives assigned to them.

Service providers in general have been emphasizing the business market in recent years and that emphasis seems to be yielding positive results. Scores for all the categories of companies were higher than for a similar study that J.D. Power conducted in 2015. Scores for 2015 were 783 for large companies, 747 for mid-size companies and 715 for small companies.

The business market has been a particularly strong focus for cable companies, which do not have wireless businesses but do have modern fiber network infrastructure. The J.D. Power results suggest cable companies still have a way to go in gaining business customers’ loyalty and trust, however.

The J.D. Power results suggest opportunities for service providers that can excel at serving SMBs – and tier two service providers such as Windstream and Frontier have been focusing on that market for a long time. So was TW Telecom (which was acquired by Level 3, which is in turn being acquired by Century Link) and XO Communications which was acquired by Verizon.

Tier two telcos were not included in the J.D. Power report.

…………………………………………………………………………………………

Telecom ARPU Falling in Every Region

Closing Comment:

Perhaps, the negative growth in telecom is causing telcos to merge to acquire scale and to go into other businesses (like Orange investing in on-line banking instead of its core telecom business).

Fierce Telecom reported on July 24th:

CenturyLink, Frontier, Windstream suffer worst 3 quarters in history

CenturyLink, Frontier and Windstream have continued to see pressure over the past three quarters as shares at each of these companies dropped dramatically due to issues at each company.

“Shares in the wireline ILEC/RLEC space (CenturyLink, Frontier, Windstream) have endured the worst three consecutive quarters in industry history, with shares plummeting an average of -20% in 4Q16, -21% in 1Q17, and -24% in 2Q17 (we note another -5% in 3Q17 thus far), mostly from Frontier and Windstream as CenturyLink shares are being supported by the Level 3 acquisition,” Cowen said in a research note.

Overall, the three companies face the industry-wide challenge of balancing strategic service growth with ongoing legacy service declines and losing market share to cable operators.

Additionally, each of these companies has been dealing with specific headwinds in their businesses. Frontier has been challenged by integrating the properties it purchased from Verizon in California, Texas and Florida, while CenturyLink is dealing with a raft of lawsuits over alleged consumer fraud issues and Windstream is seeing declines in its legacy TDM-based wholesale business sector.

References:

http://www.jdpower.com/sites/default/files/2017108.pdf

Microsoft White Spaces Plan would bring 2 million Americans online by 2022

Microsoft today announced a project to bring broadband internet access to rural parts of the U.S. using TV white spaces, unlicensed and unused spectrum. Microsoft President Brad Smith unveiled details about the initiative at a Tuesday event in Washington, D.C. as a way to bridge the digital divide between urban and rural areas.

Microsoft’s ambitious plan, dubbed the Rural Air-band Initiative, will begin in 12 states, where the company said it will invest in broadband connectivity alongside local telecom services. The company said that it does not intend to enter the telecom business itself or profit directly from the initiative. Instead, Microsoft said it will supply the upfront capital required to expand broadband coverage, then recoup that cost by sharing in the revenue with local operating partners.

The company is calling for a combination of private and public investments to get about 2 million rural Americans online in the next five years. Microsoft plans to partner with telecommunications companies that serve rural counties in 12 states: Wisconsin, Michigan, North Dakota, South Dakota, Kansas, Washington, Texas, Arizona, Georgia, Virginia, New York and Maine. It’s also asking for regulatory support from the Federal Communications Commission.

Mr. Smith will also urge President Donald Trump and his administration to ensure that unlicensed white space is available in all U.S. markets. “As a country, we should not settle for an outcome that leaves behind more than 23 million of our rural neighbors,” Smith wrote in a blog post.

“To the contrary, we can and should bring the benefits of broadband coverage to every corner of the nation,” he added. Smith said the TV white spaces provides powerful bandwidth to allow wireless signals to travel over hills and through buildings and trees.

“Today, 34 million Americans still lack broadband internet access, which is defined by the Federal Communications Commission as a 25 Mbps connection,” Smith posted. “Of these, 23.4 million live in rural parts of our country. People who live in these rural communities increasingly are unable to take advantage of the economic and educational opportunities enjoyed by their urban neighbors.” Smith said Microsoft wants to eliminate the rural broadband gap by July 4, 2022.

“Our goal is to serve as a catalyst for market investments by others in order to reach additional rural communities,” he stated in his blog post.

Microsoft company faces many hurdles with the technology. For one, few manufacturers are making devices compatible with white-spaces technology, and some devices that can be used with the technology cost more than $1,000 each. The National Association of Broadcasters, a trade group, said that only 800 devices that worked with white-spaces technology had been registered with regulators.

“White spaces has tremendous opportunity to help with broadband coverage in rural areas, but it’s hard to justify the cost to device makers who don’t see economies of scale in rural areas,” said Doug Brake, a senior analyst at the Information Technology & Innovation Foundation, a research organization that is sponsored by tech companies including Microsoft.

Mr. Smith said that he would demonstrate four devices that work with white-space technology at Tuesday’s event, adding that prices for such gadgets would fall below $200 by next year.

Another challenge is a battle with television broadcasters who have long argued that devices on the unused airwaves can interfere with the broadcasts run on neighboring channels. This week, the National Association of Broadcasters filed comments with the Federal Communications Commission arguing against Microsoft’s request for one nationwide channel to be set aside for white-spaces use.

“Microsoft has been making promises about white-spaces technology for well over a decade,” Patrick McFadden, an associate general counsel for the association, wrote in comments to the commission. “At what point do we finally conclude that the white spaces project is a bust?”

References:

https://www.microsoft.com/en-us/research/project/dynamic-spectrum-and-tv-white-spaces/

http://whitespaces.microsoftspectrum.com/

https://www.theverge.com/2017/7/11/15953310/microsoft-rural-airband-broadband-strategy

http://www.detroitnews.com/story/tech/2017/07/11/rural-broadband-microsoft/103618818/

https://www.microsoft.com/en-us/research/project/networking-over-white-spaces-knows/

China Orders Telecom Companies To Block VPN Access to Global Internet

China’s government has reportedly directed telecommunications companies to block their users from accessing a secure internet network.

The country’s authorities are specifically mandating that state-run wireless carriers — like China Telecom, China Unicom and China Mobile — forbid people from using virtual private networks (VPNs). China is giving the quasi-private companies until Feb. 1, 2018 to comply with its orders, according to Bloomberg.

The technological capability gives users the ability to navigate the web anonymously through an encrypted, secure connection.

VPNs enable Chinese citizens with the ability to circumvent the country’s firewall (also known as the Great Firewall of China), which technically prohibits people from accessing many online services and sites that are available on the global internet. Social media sites like Facebook and Twitter, for example, are not accessible due to the firewall, so many Chinese citizens use Sina Weibo, a similar platform that is based in China and adheres to government’s calls for targeted censorship.

China’s propensity towards censorship manifests itself quite often, in fact, including in late June when the popular Netflix original “BoJack Horseman” was blocked just days after debuting in the country. (RELATED: China Battles For Internet Hegemony After America Gives Up Control)

“In the past, any effort to cut off internal corporate VPNs has been enough to make a company think about closing or reducing operations in China. It’s that big a deal,” Jake Parker, vice president of the U.S.-China Business Council, told Bloomberg.

“VPNs are incredibly important for companies trying to access global services outside of China,” he said, adding that the order also seems to affect individuals across the country.

References:

https://en.wikipedia.org/wiki/Internet_censorship_in_China

http://www.cnbc.com/2017/07/10/china-bans-vpns-to-further-tighten-internet-controls-says-report.html

https://www.theguardian.com/world/2017/jul/11/china-moves-to-block-internet-vpns-from-2018

https://www.bloomberg.com/news/articles/2017-07-10/china-is-said-to-order-carriers-to-bar-personal-vpns-by-february

5G in India dependent on fiber backhaul investments

Excerpts of an article in the Economic Times of India by Ankit Agarwal:

Executive Summary:

In the wake of growing awareness around Internet of Things (IoT) and the use cases it presents to Indian businesses and consumers, 5G will open a new era of opportunities for telecom operators and ecosystem partners in the country.

AJW Comment: However, fiber backhaul will be needed and that may take some time as India’s fiber infrastructure needs significant improvement.

“One of the fundamental requirements for 5G is strong backhaul which is simply not there and that is the most time consuming part and it is extremely expensive in today’s condition in India,” Jalaj Choudhri, EVP, Reliance Communications said. He adding that even if India is able to circumvent the challenges of standardization and 5G truly becomes available by 2020, yet a good 5G network cannot be expected unless we have a reliable and strong backhaul.

More in this article.

Current Status of 5G in India:

In India, Nokia has recently signed an MoU with wireless network operators BSNL and Airtel to collaborate on 5G technology solutions, and Reliance Jio is working with Samsung to explore various technologies and equipment for 5G.

In the wake of growing awareness around Internet of Things (IoT) and the use cases it presents to Indian businesses and consumers, 5G will open a new era of opportunities for telecom operators and ecosystem partners in the country. Though it’s difficult to get an accurate estimate of the market size right now, IoT is expected to provide a $15 billion market opportunity for Indian businesses by 2020, according to officials at Department of Telecom (DoT). Combine this with the unprecedented growth in the number of smartphone users in India, which is expected to overtake the U.S. in terms of smartphone shipment by 2019. Analysts are optimistic that India will hold around 15% of the world’s smartphone market share by that period – Indian consumers are ready for 5G.

Roadblocks for Indian Operators

Indian operators, however, need to address the issues surrounding 5G infrastructure and deployment. Challenges involving regulatory policies, investments and infrastructure readiness need to be addressed on priority.

Challenges ahead for telecom operators in India are multi-fold compared to their peers in the rest of the world. Diverse geography, disparate population and disparity in economic distribution among the rich and the poor pose serious challenges to operators, preventing uniform investments across different telecom circles. Also, issues such as Right of Way (RoW) have created uncertainty in fiber investments across different states. These apart, the rising cost of air waves and the challenges involved in migrating to new technologies bring additional challenges.

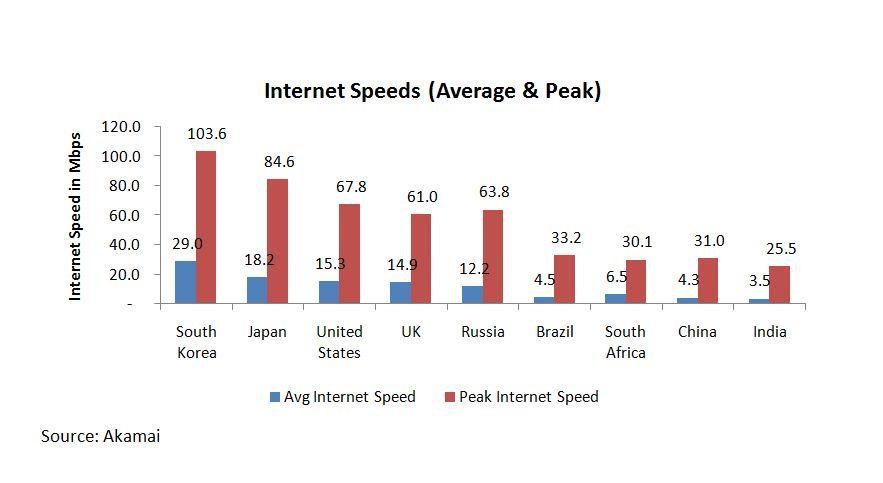

Moreover, the industry’s performance on key indicators such as network speed, coverage and customer service is not satisfactory. For example, average Internet speed in India stands at 3.5 Mbps compared to 29 Mbps in South Korea, 15 Mbps in the U.S., and 4.3 in China (see graph below).

In this context, it is worth analysing where telecom investments should be directed to make commercial 5G a reality in India by 2020.

Fiber to Drive 5G Rollouts

With a promise of 10Gbps speed, less than 1 ms latency and 90% reduction in network energy utilisation, 5G will spur the next round of telecom infrastructure investments across the globe, say experts. The growth of 5G will be fuelled by the sharp hike in consumer data and the proliferation of IoT devices.

ITU estimates the market for IoT devices will result in over USD 1.7 trillion in value added to the global economy by 2019. In view of these developments, ITU expects that investments on fibre infrastructure will surpass $ 144.2 billion during 2014 – 2019. The fact that 5G network will have to support bursty data from emerging applications like Video on Demand (VoD), IoT, Smart Cities, and the like also makes backhaul (from cell tower to network operators Point of Presence) a critical concern.

In several markets, operators are turning to fiber backhaul as an alternative to costly microwave technologies. Since fiber is essential for both wireline and wireless networks, investors show greater levels of confidence in fiber investment.

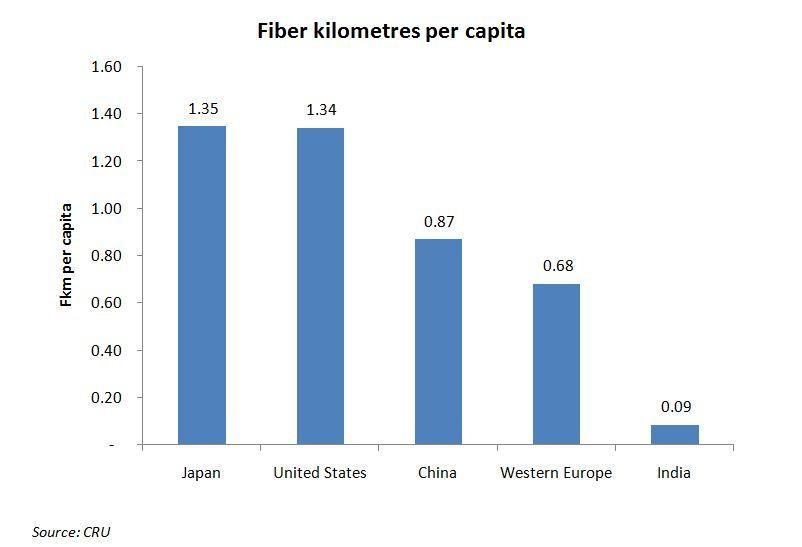

Fiber Investment: Where does India stand?

A comparison of optical fiber cable (OFC) rollout among the top performing telecom markets shows that the fiber kilometre (fkm) per capita is much less in India compared to several other key markets. For example, fkm per capita for China with 1.3 billion people is 0.87 whereas that of India with 1.2 billion people is just 0.09 (i.e. one-tenth of China consumption).

In developed markets such as the US and Japan, the score is 1.3 and higher (See graph below).

Preparing 5G Networks in India

The latest Cisco VNI report estimates that global IP traffic will grow at a compound annual growth rate (CAGR) of 23% from 2014 to 2019, and reach 2 zettabyte per year by 2019. Given this, operators across the world are upgrading their backhaul networks with fibre technology. The fact that fibre-based networks are capable of delivering unlimited bandwidth makes them a winning formula for telecom investments.

Leading operators are now mulling ways to reduce the capex associated with fibre deployments. Infrastructure sharing and leasing are gaining popularity among mobile and cable operators in developing markets. In India, the DoT’s amendment of unified license scheme for active infrastructure sharing and the revised public private partnership (PPP) model for BharatNet project adopted last year are two timely steps to boost the infrastructure sharing efforts by operators. Combined with this, a consensus on RoW is also expected soon across all Indian states. A unified RoW policy will pave way for smooth fibre rollout, resulting in faster service rendering.

To rise to the global standards and solidify their stand in the country, Indian operators need to pump in more funds in optical fibre and related technologies. With fibre playing a pivotal role in improving broadband connectivity and building robust 4G/5G backhaul capabilities, operators will find the investment worth of a grab. As penetration improves, they will be in a position to lower tariffs and identify new monetisation opportunities. ARPU will improve, and the market will stabilise gradually.

As the second largest telecom market in the world, India promises great potential for investors. Industry watchdogs believe India and China combined are capable of transforming world’s telecom landscape in the next decade. Recent developments reveal that Chinese operators and technology vendors have come a long way in 5G tests and trials. Now, it’s the turn of Indian operators to prove their readiness to 5G.

This is an exciting time for India, and the impact of 5G and its associated enablement of M2M, IoT, Autonomous driving and AR/VR can be anticipated. Given the 5G requirement for latency reduction (from 50ms to 1 ms) and speed from 100 Mbps to 10Gbps, the fibre deployment in the country will need to increase from current market of 16-18 million fkm per year to at least 2-3x per year. 5G will also require a multi-fold increase in small cells deployment, with each small cell having backhaul on fibre. The percentage of tower backhaul on fibre for the operators will need to increase significantly from 20% to 70-80% levels.

The current main drivers for the increase in deployment lie in the increased 4G deployments in Tier 1 and Tier 2 cities, increased Fibre-to-the-Home (FTTH) deployments by telecom operators, ISP’s and MSO providers. For example, ACT has recently launched 1Gbps broadband service in Hyderabad, which 20x faster than the market average of 50 Mbps. The other drivers for increase in fibre demand include the rural broadband project – BharatNet and large connectivity projects by the Defence. Lastly, optical fibre is a critical component to make the Smart Cities project a success.

Enabling early adoption of 5G, Sterlite Tech is working closely with key stakeholders – DOT, TRAI, telecom operators, equipment vendors and start-ups to enable 5G deployments in the country. Sterlite Tech is actively involved in 5G readiness solutions, and, is a key member of the Telecom Infra Project (TIP) led by Facebook, to completely transform telecom networks using SDN/NFV and make them 5G ready.

DISCLAIMER: The views expressed are solely of the author and ETTelecom.com does not necessarily subscribe to it. ETTelecom.com shall not be responsible for any damage caused to any person/organisation directly or indirectly.

Sprint Merger with T-Mobile Gets Closer; Incompatible 2G/3G Technologies is an Issue

German newspaper Handelsblatt yesterday reported that T-Mobile US Inc.’s parent company (Deutsche Telekom AG) favors a merger with Sprint. Deutsche Telekom AG, which controls T-Mobile, aims to maintain control of the combined company after an all-stock deal with Sprint, according to Handelsblatt, which cited sources close to the German company’s management committee and board.

Bloomberg reported two weeks ago that Sprint and T-Mobile were considering an all-stock deal. Sprint and T-Mobile were also talking to other potential merger partners, Bloomberg reported then, citing people familiar with the matter. Executives of both companies have said a merger would produce billions of dollars in cost savings and help them compete against larger rivals AT&T Inc. and Verizon Communications Inc.

When the merger was rumored months ago, SoftBank — Sprint’s parent company — reportedly had not pushed the subject due to strict U.S. Federal Communications Commission rules prohibiting rival carriers from conspiring during airwave auctions.

Now, the report claims that final measures are being put in place to complete the merger and the all-stock agreement would eliminate transaction costs with a deal like this because both companies would be exchanging stock rather than actual money.

This news also comes right after Sprint introduced its new promotion to encourage customers to ditch their current carriers. Those who switched to Sprint would receive unlimited data for up to five lines for free — making it clear that the carrier might be in trouble.

Sprint has consistently been playing catch-up with its rival carriers — AT&T, Verizon, and T-Mobile. Last year OpenSignal reported the carrier took last place in all categories ranging from speed to latency. On the other hand, T-Mobile had an increase in 4G coverage at 81.2 percent — which was neck and neck with AT&T at 82.6 percent — trailing closely behind Verizon. Sprint came in last, yet again, at 70 percent.

T-Mobile has been making efforts to improve its service across the board after having rolled out LTE on the 700MHZ spectrum. The OpenSignal report also measured LTE speeds in 11 of the biggest metro areas where T-Mobile won in four cities — placing it ahead of Verizon’s three — but the two carriers tied in Atlanta, San Francisco, and Washington, D.C.

A merger would likely see T-Mobile and Sprint’s networks also unified, although that would take much longer than many pundits expect. That’s because Sprint uses CDMA technology to power its 2G and 3G networks, while T-Mobile uses GSM (like all of Europe). The two wireless digital transmission technologies are not compatible, and CDMA would likely have to be phased out (along with some customer devices) before the two networks could truly unify. In the short term, internetworking units would be needed for seamless connectivity between wireless endpoints.

Also, T-Mobile has announced a nationwide 5G network, while Sprint has not, although it’s working with several companies (including Intel) on 5G software technologies.

Verizon still remains champion when it comes to coverage nationwide and reliability. AT&T is a close number 2. T-Mobile, which this year passed Sprint as the #3 U.S. wireless carrier, has been very aggressive and is clearly working to toward getting ahead. Sprint has lagged behind, most likely because it had to jettison its WiMAX network and replace it with LTE.

……………………………………………………………………………………………………………………………………………….

Update: Sprint CEO interviewed on CNBC, June 22, 2017:

A combined T-Mobile–Sprint could pose a “powerful” threat to telecom giant AT&T, Sprint CEO Marcelo Claure told CNBC on Thursday, June 22, 2017.

“We have looked at every other alternative to make sure we are making the right decision,” Claure said on “Halftime Report.” “If the government works to allow us to combine, we’ll be No. 3, but we’ll be a formidable competitor and we’ll continue to disrupt the industry.”

The Sprint chief spoke after a meeting at the White House with President Donald Trump and other tech leaders to discuss the potential impact of emerging technologies on U.S. industrial workers, among other topics. Representatives from Verizon, AT&T and T-Mobile were also at the meeting, Claure said.

On Tuesday, German business newspaper Handelsblatt reported that Deutsche Telekom, T-Mobile’s parent, was prepping documents for a potential merger with Sprint. T-Mobile declined to comment but sources said the company is sounding out if there are any government objections to a deal, the newspaper reported.

T-Mobile did not immediately respond to a request for comment from CNBC.

Wall Street has frequently speculated about a possible merger of the two companies.

On the regulatory issues of such a deal, Claure said with more companies in the telecom market, like Comcast and Google, it is less likely to raise an eyebrow from the government. “You’re talking seven or eight formidable competitors today,” he said.

More importantly, “we’re going to need to make some serious investments in order to bring 5G to the United States,” he added. “And that’s going to require to the tune of $40 to $50 billion of investments.”

More at:

Colt plans to enter U.S. Metro Fiber Market in 2018 after Asia Metro Network Investments in 2017

UK based Colt, an alternative telco leader in software defined and virtualized WANs (see sections below for examples), is plotting an assault on the US metro fiber market next year (i.e. in 2018). According to the Financial Times (on line subscription required), Colt wants to become world’s largest metro fiber company within three years. That’s a truly optimistic goal considering all the legacy fiber facilities based network operators, including Century Link which now owns Level One’s fiber assets.

Colt remains one of the most substantial “alt-nets”(alternative or competitive facilities based wireline network operators) still in operation and this year has been investing in its networks in Singapore, Tokyo and Osaka as part of its expansion plan (see section below for more on this).

The telco hopes to build or buy networks in several large US cities that also says the provider might lease some facilities from other vendors. CEO Carl Grivner cited the expected fiber boom from cloud services and the internet of things (IoT) as Colt’s basis for optimism. The company will also look to expand its networks in the UK outside of London in Manchester and Birmingham in the UK.

………………………………………………………………………………………………………………………………………………………………………………………………………………….

On January 12, 2017, Colt announced it was investing in Asia metro area networks. In particular, it will expand and enhance the Colt IQ Network™ in Singapore and Hong Kong in 2017 as part of its plans to invest significantly into Asia over the next three years. In Singapore, these investments will revolve around a series of initiatives that include a large-scale expansion of existing coverage, provisioning of high-bandwidth capacity, and new digging projects for Colt’s next-generation fiber optics.

The Colt network expansion, comprising both Optical and Ethernet architectures, will provide high-bandwidth services to major buildings and data centers across Asia. The investment underlines the growing bandwidth demands of global organizations, particularly in digital, data-intensive industries.

……………………………………………………………………………………………………………………………………………………………………………………………………………………..

The move to target US fiber investment reminds us of the ill-fated strategy of Cable & Wireless in 2000-2001, when that UK network operator pumped billions of pounds into US acquisitions months before the market collapsed.

CEO Grivner, who worked at Cable & Wireless along with XO (now owned by Verizon), said that, with cloud computing and technology relating to the “internet of things” only growing, the bet on expansion looked safer than it did at the turn of the century. “I don’t think it is going to take a pause. The growth has caught up to the hype,” he said.

…………………………………………………………………………………………………………………………………………………………………………………………………………….

Other Voices:

Fierce Telecom wrote on June 19, 2017:

Colt’s plans to build a mixed network in the U.S. should not be a great surprise. In November 2016, Colt said it was expanding its North American sales and support teams. While the focus was to leverage type 2 facilities from other carriers, Colt’s initial foray into the United States could challenge AT&T and Verizon, attracting more multinational customers that need local and international connectivity services.

As a Pan-European provider, Colt operates in 20 countries across Europe and Asia. One of its first moves was to open two regional offices: one in Chicago and another in Jersey City, New Jersey.

………………………………………………………………………………………………………………………………………………………………………………………………………………

At the 2017 Open Network Summit, this author attended an impressive presentation by Colt’s experience in deploying SDN and NFV solutions in production both for Ethernet and IP services, the learning associated as well as their future plans. In particular, Javier Benitez covered Colt developments around Ethernet and IP on Demand, SD VPN, SDN controlled MPLS packet core and SDN/NFV NNI standardization. His presentation is available on reader request. Other 2017 Open Network Summit presentations can be downloaded for free here.

……………………………………………………………………………………………………………………………………………………………………………………………………………….

SDx Central wrote last November:

AT&T is working with Colt Technology Services to provision network services using a programmatic API-to-API interface between separate software-defined networking (SDN) architectures.

The test occurred between two networks — one in the U.S. and one in Europe — and demonstrated that enterprises can provision on-demand, scalable network services across multiple locations and multiple networks, even networks from different service providers. The trial took place between the East Coast of the U.S. and various locations in Europe, and it combined AT&T and Colt’s on-demand network capabilities. AT&T and Colt plan to share the network-to-network interface and open API code with standards bodies and industry forums.

This is an important finding for service providers that want to sell services to enterprises. With this capability, enterprises will be able to reserve ports, order a point-to-point Ethernet service, or adjust their bandwidth requirements on demand.

……………………………………………………………………………………………………………………………………………………………………………

About Colt:

Colt, formerly known as City of London Telecom, is owned by fund manager Fidelity which was an original investor in the business when it was founded 25 years ago. The company was briefly a rising star of the UK telecoms sector, achieving a valuation of £4bn and entering the FTSE 100. However, it struggled to fulfill its growth potential, as moves into IT services and data centers in the past decade failed to pay off. Fidelity de-listed the business in 2015.

Mr Grivner said it was easier to invest in the telecom business (as a network operator) outside the glare of the public markets. Therefore, there were no plans to relist the company’s shares.