5G Market Status

PwC report on Monetizing 5G should be a wake up call to network operators!

A PwC report titled, “The challenge of monetizing 5G,” states that capital expenditures and operating expenses will likely be very high with the deployment of 5G standalone networks and their fully virtualized, cloud-native architectures. Yet returns have been anemic across all generations, ranging from 1.5% to 4.5% of return on assets.

PwC’s 26th Annual Global CEO Survey found that 46% of telco CEOs believe that if their companies continue on their current paths, their businesses would not be economically viable in 10 years.

Source: PwC

As 5G becomes an everyday reality for both investors and consumers, carriers are going to face increasing pressure on two fronts:

1. Improve return on assets

As capital markets and stakeholders begin to focus on investment returns in a high-inflation environment, there will be growing scrutiny on telcos and wireless carriers, especially in comparison to other capital-intensive investment opportunities. An exemplar cloud services provider (CSP) has demonstrated ROA of 17% to 20%+ over the past five years, which compares to the 2% to 3% ROA range of MNOs. The ROA of MNOs approximates that of regulated entities like utilities, which explains investor angst.

2. Deliver on demanding service-level agreements to support 5G “killer apps,” such as metaverse applications (really?)

Improving ROA is intrinsically tied to successfully managing the costs and revenues of 5G applications. Many operators face a growing clamor from application providers and up-stack players to create “metaverse-capable networks,” without much clarity on how application revenue will be shared with them. Network operators risk becoming trapped in a “give more, get less” scenario of providing pure-play connectivity, while up-stack companies monetize the 5G applications.

……………………………………………………………………………………………………………………………………………………………………

For those who believe 5G FWA is the way to monetize 5G, PwC warned that’s not likely. The market research firm’s analysis showed FWA services could cost more than 22-times as much as mobile connectivity services. That’s due to costs associated with delivering data tied to specific latency or QoS service-level agreements (SLAs). Immersive and augmented experiences — such as virtual-reality apps, mobile metaverse and gaming — could cost three to four times as much. Network costs related to the Internet of Things (IoT) are even more challenging to estimate and track, primarily because of the extremely wide range of connected devices and applications available.

The report also found that FWA services could have up to 40-times less revenue potential. This is due to FWA services being price limited by competing fiber or cable internet options.

“Most FWA subscribers are willing to pay only as much as wireline plans cost, yet they expect a similar quality of service for internet connectivity,” the report notes.

PwC Partner Dan Hays explained during an interview with SDx Central at the MWC Barcelona 2023 event that operators should approach FWA and other alternative 5G connection services like IoT with reasonable financial and operational expectations. “Fixed-wireless access is a great way to fill out excess capacity, if you have it,” Hays said. “You see some of the carriers making that play.”

“It’s not a cure all by any means,” Hays said, explaining, “we look at it as not a business model but really a technology. It’s a technology choice that you can use.”

Hays said that operators are indeed being “really thoughtful” in managing capacity to serve FWA customers, but that can potentially run into a problem down the road where a particular site can no longer support a high-bandwidth FWA connection. “Do they fire you as a customer at some point,” he said.

In conclusion, PwC states:

Carriers will be increasingly challenged to demonstrate better returns on invested capital for massive 5G capital outlays, while simultaneously meeting the demanding service-level agreements of future 5G applications. Network costs are likely higher — and revenue potential is likely lower — than carriers understand for these applications. Critical strategies for improving ROA and monetizing 5G successfully involve accurately valuing network features, quantifying network costs and communicating them to all stakeholders, as well as improving 5G offer management, pricing and service evolution.

References:

https://www.pwc.com/us/en/tech-effect/emerging-tech/5g-monetization.html

GSMA Intelligence: 5G connections to double over the next two years; 30 countries to launch 5G in 2023

GSMA Intelligence forecasts 5G connections are expected to double over the next two years, expedited by technological innovations and new 5G network deployments in more than 30 countries in 2023. Of the new networks to be deployed in 2023, it is expected that 15 will be 5G Standalone (SA) networks. As of January 2023, there were 229 commercial 5G networks globally and over 700 5G smartphone models available to users.

GSMA Intelligence, announced its latest 5G forecast during MWC Barcelona 2023, point to a significant period of growth in terms of mobile subscribers and enterprise adoption. Consumer connections surpassed one billion at the end of 2022 and will increase to around 1.5 billion this year – before reaching two billion by the end 2025.

India will lead the 5G expansion globally in 2023, with the expansion of services from Airtel and Jio in 2023 expected to be pivotal to the region’s ongoing adoption. GSMA Intelligence predicts there will be four 5G networks in India by the end of 2025, accounting for 145 million additional users. With operators such as Jio announcing ambitions to connect as many as 100 million homes across India to its 5G FWA network, the number of FWA users looks likely to grow substantially over the next few years, the report added.

![]()

Growth will also come from key markets within APAC and LATAM, such as Brazil and India, which have recently launched 5G networks. India will be especially significant, with the expansion of services from Airtel and Jio in 2023 expected to be pivotal to the region’s ongoing adoption. GSMA Intelligence predicts there will be four 5G networks in India by the end of 2025, accounting for 145 million additional users.

Many of the new 5G markets scheduled to launch networks in 2023 are in developing regions across Africa – including Ethiopia and Ghana – and Asia. Today, 5G adoption in the sub-Saharan region sits below 1% but will reach over 4% by 2025 and 16% in 2030, largely thanks to a concerted effort from industry and government organizations to provide connectivity to citizens.

“Until now, 5G adoption has been driven by relatively mature markets and consumer use cases like enhanced mobile broadband, but that’s changing. We’re now entering a second wave for 5G that will see the technology engage a diverse set of new markets and audiences,” said Peter Jarich, Head of GSMA Intelligence. “The extension to new use cases and markets will challenge the mobile ecosystem to prove that 5G truly is flexible enough to meet these diverse demands in a way that’s both inclusive and innovative.”

The Rise of 5G Fixed Wireless Access (FWA):

As of January 2023, more than 90 FWA broadband service providers (the vast majority of which are mobile operators) had launched commercial 5G-based fixed wireless services across over 48 countries. This means around 40% of 5G commercial mobile launches worldwide currently include an FWA offering.

In the U.S., T-Mobile added over half a million 5G FWA customers in Q4 2021 and Q1 2022 combined. By 2025, it expects to have eight million FWA subscribers, while Verizon is targeting five million FWA subscribers for the same period. The conventional wisdom holds that FWA is primarily useful as a rural service, targeted mostly at the previously unserved or underserved. Verizon says their FWA service is primarily urban and suburban service with target customers that are dissatisfied with terrestrial broadband services. Verizon has increasingly come to view FWA as an integral part of their broadband access offering everywhere that FiOS isn’t available.

Reliance Jio (India) announced ambitions to connect as many as 100 million homes across India to its 5G FWA network, the number of FWA users looks likely to grow substantially over the next few years.

While the majority of current 5G FWA deployments focus on the 3.5–3.8 GHz bands, several operators around the world are already using 5G mmWave spectrum as a capacity and performance booster to complement coverage provided by lower bands.

Only 7% of 5G launches have been in 5G mmWave spectrum so far but this looks set to change given 27% of spectrum allocations and 35% of trials are already using 5G mmWave bands. Furthermore, in 2023 alone, the industry will see ten more countries assigned 5G mmWave spectrum for use – a significant increase from the 22 countries who have been assigned it to date. Spain received the first European 5G mmWave spectrum allocation this year, resulting in Telefónica, Ericsson and Qualcomm launching its first commercial 5G mmWave network at MWC Barcelona 2023.

Enterprise IoT Driving Growth:

The figures from GSMA Intelligence also suggest that, for operators, the enterprise market will be the main driver of 5G revenue growth over the next decade. Revenues from business customers already represent around 30% of total revenues on average for major operators, with further potential as enterprise digitization scales. Edge computing and IoT technology presents further opportunities for 5G, with 12% of operators having already launched private wireless solutions – a figure that will grow with a wider range of expected IoT deployments in 2023.

Another major development for the enterprise will be the commercial availability of 5G Advanced (3GPP Release 18) in 2025. Focusing on uplink technology, 5G Advanced will improve speed, coverage, mobility and power efficiency – and support a new wave of business opportunities. GSMA’s Network Transformation survey showed half of operators expect to support 5G Advanced commercial networks within two years of its launch. While this is likely optimistic, it presents the ecosystem with a clear opportunity to execute on.

Editor’s Note:

GSMA’s 5G forecast is a direct contradiction to Omdia’s which expects weaker 5G growth in the near term. Which forecast do you believe?

………………………………………………………………………………………………………………………………………………………………………..

References:

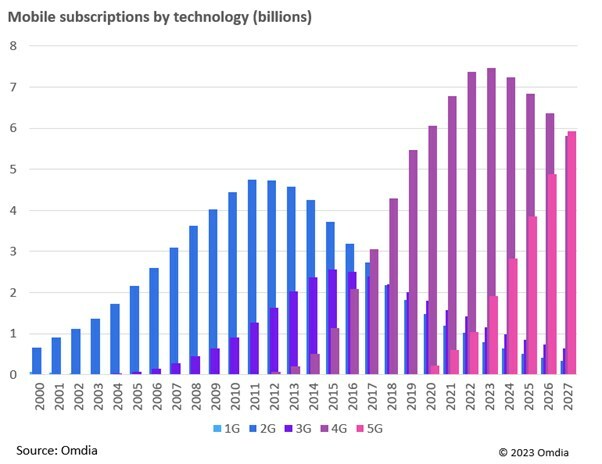

Omdia forecasts weaker 5G market growth in near term, 4G to remain dominant

Omdia forecasts weaker 5G market growth in near term, 4G to remain dominant

Multiple factors have slowed down the transition to 5G such as lower handset sales driven by cost-of-living crisis and inflation, poor network coverage, low performance gain perception, and lack of 5G specific applications. Furthermore, an increasing portion of mobile connections – approximately 30% – are not handsets and will be slower to convert to 5G (e.g., IoT, connected tablets/laptops, wearables).

Omdia Senior Market Forecaster, Garinder Shankrowalia, said: “5G subscription reporting in 2022 has led us to reduce our 2023 forecast by 7.2% -approximately 150 million subscriptions. We anticipate the industry will regain this loss from 2025, once global market conditions are improved.”

Omdia believes it is important for mobile operators to continue investing in next generation mobile networks to enable the application emergence and the overall digital economy to grow. However, having multiple cellular technologies running concurrently on mobile networks is having an adverse effect on operators whereby launching 5G increases complexity and cost for little return in the short term.

Omdia Research Director Ronan de Renesse said: “There needs to be a ‘net-zero’ approach to network development, removing the old as the new gets deployed. Operators are already starting to move capital from next generation network deployment to 3G decommission projects and digital transformation. Key stakeholders should remain realistic about the prospects for 5G and re-evaluate the business case before moving on to the next step.”

Omdia forecasts 5G will account for 5.9 billion subscriptions in 2027 equivalent to a population penetration of 70.9%.

Another Opinion: 5G Fails to Deliver on Promises and Potential

5G is a big letdown and took a “back seat” at CES 2023; U.S. national spectrum policy in the works

Ookla: State of 5G Worldwide in 2022 & Countries Where 5G is Not Available

Executive Summary:

In a new blog post, Ookla asseses The State of Worldwide 5G in 2022. The market research firm examined Speedtest Intelligence® data from Q3 2022 Speedtest® results to see how 5G performance has changed since last year, where download speeds are the fastest at the country level, and how satellite technologies are offering additional options to connect. Ookla also looked at countries that don’t yet have 5G to understand where consumers are seeing improvements in 4G LTE access.

Editor’s Note: for some unknown reason, China is not included in Ookla’s report

- 5G speeds were stable at the global level with:

a] Median global 5G download speed of 168.27 Mbps in Q3 2022 as compared to 166.13 Mbps in Q3 2021

b] Median upload speed over 5G slowed slightly to 18.71 Mbps (from 21.08 Mbps) during the same period

- Ookla® 5G Map™: 127,509 5G deployments in 128 countries as of November 30, 2022, compared to 85,602 in 112 countries the year prior

- South Korea and the United Arab Emirates led countries for 5G speeds

- 5G Availability points to on-going challenges

5G Availability measures the proportion of Speedtest users with 5G-capable handsets, who spend a majority of time connected to 5G networks. It’s therefore a function of 5G coverage and adoption. We see wide disparity in 5G Availability among markets worldwide, with for example the U.S. recording 54.3% in Q3 2022, well ahead of markets such as Sweden and the U.A.E., with 8.6% and 8.3% respectively.

Critical levers for mobile operators to increase 5G Availability include:

- Increasing 5G coverage by deploying additional base stations

- Obtaining access to, or refarming, sub-GHz spectrum, to help broaden 5G coverage, as sub-GHz spectrum has superior propagation properties than that of higher frequency spectrum bands.

- Encouraging 5G adoption among users with 5G-capable handsets.

Speedtest Intelligence points to 5G adoption challenges in some markets, with 5G Availability dropping in Bulgaria, South Korea, the Netherlands, and the U.A.E. As more users acquire 5G-capable devices, operators need to balance their pricing models to ensure users have sufficient incentives to purchase a 5G tariff.

Countries where 5G is not readily available:

Speedtest Intelligence showed 29 countries in the world where more than 20% of samples were from 2G and 3G connections (combined) during Q3 2022 and met our statistical threshold to be included (down from 70 in Q3 2021). These are mostly countries where 5G is still aspirational for a majority of the population, which is being left behind technologically, having to rely on decades-old technologies that are only sufficient for basic voice and texting, social media, and navigation apps. We’re glad to see so many countries fall off this list, but having so many consumers on 2G and 3G also prevents mobile operators from making 4G and 5G networks more efficient. If operators and regulators are able to work to upgrade their users to 4G and higher, everyone will benefit.

Countries That Still Rely Heavily on 2G and 3G Connections

Speedtest IntelligenceⓇ | Q3 2021

| Country | 2G & 3G Samples |

|---|---|

| Central African Republic | 76.2% |

| Turkmenistan | 58.5% |

| Kiribati | 51.6% |

| Micronesia | 47.4% |

| Rwanda | 41.1% |

| Belarus | 39.7% |

| Equatorial Guinea | 37.7% |

| Afghanistan | 36.7% |

| Palestine | 33.5% |

| Madagascar | 27.5% |

| Sudan | 27.4% |

| Lesotho | 26.5% |

| South Sudan | 26.3% |

| Benin | 26.0% |

| Guinea | 25.5% |

| Cape Verde | 24.3% |

| Tonga | 24.3% |

| Syria | 23.4% |

| The Gambia | 23.4% |

| Ghana | 23.3% |

| Palau | 22.9% |

| Niger | 22.8% |

| Tajikistan | 22.7% |

| Mozambique | 22.4% |

| Guyana | 21.8% |

| Togo | 21.8% |

| Congo | 21.1% |

| Moldova | 20.8% |

| Saint Kitts and Nevis | 20.0% |

Conclusions:

Ookla was glad to see performance levels normalize as 5G expands to more and more countries and access improves and we are optimistic that 2023 will bring further improvements. Keep track of how well your country is performing on Ookla’s Speedtest Global Index™ or track performance in thousands of cities worldwide with the Speedtest Performance Directory™.

References: