Broadband Status

Comcast claim: #1 Gigabit Service Provider in the U.S. but what about “5G” BWA?

Comcast says its Xfinity Gigabit Internet and Comcast Business Gigabit services are now available to nearly all of the 58 million homes and businesses the company’s infrastructure passes in 39 states and the District of Columbia (it’s not available in Santa Clara, CA where top downstream speed is 400M bits/sec). That makes the cable MSO the largest provider of gigabit Internet service in the U.S. based on the number of potential homes passed.

Gigabit Internet service is a residential XFINITY Internet service that delivers download speeds of up to 1 Gbps and upload speeds of up to 35 Mbps to customer homes via Comcast’s next technology DOCSIS 3.1 Hybrid Fiber-Coax (HFC) network. Gigabit Pro is a newer ultra-fast tier delivered via a fiber-to-the-home solution and offers symmetrical upload/download speeds of up to 2 Gbps.

Comcast notes it has increased speeds 17 times in the last 17 years and that the capacity of its broadband network has doubled every 18-24 months. The company uses Xfinity xFi to give customers control over their internet; xFi is a digital dashboard that allows users to personalize, monitor, and manage WiFi connected devices inside the home or business.

“Comcast continues to offer an unmatched Internet experience that combines gigabit speeds with wall-to-wall WiFi, personalized tools and controls, and enough capacity to stay ahead of tomorrow’s innovations,” said Dana Strong, president of Consumer Services, Comcast. “We’ve built an innovative high-speed data platform that combines speed, coverage and control features and really sets our broadband experience apart from the competition.”

“One of the ways that we compete, of course, is ensuring that we’ve got the fastest and the most reliable network,” Matt Strauss, executive vice president of Xfinity Services at Comcast, told Fortune. “What’s partly behind the announcement is reinforcing that now we have one gig deployed across our entire footprint.”

Comcast started deploying gigabit service in earnest about three years ago. The company, which has 24.4 million total home broadband customers, wouldn’t say how many people have signed up so far, disclosing only that 75% of all its customers now receive speeds of 100 megabits/sec or higher.

However, a Morgan Stanley survey released on Thursday said that only a tiny fraction of U.S. households—3% of cable Internet customers nationwide—have 1 gigabit/sec speeds or higher.

But 1 GB speeds may gain in popularity in the future. While a typical high-definition movie file is about 3 GB or 4 GB, a growing number of movies are available in 4K, for which files sizes can exceed 100 GB.

………………………………………………………………………………………………………………………………………………………………………………………………

The top two U.S. fixed line telecom carriers Verizon and AT&T are just starting to introduce competing home Internet services with new “5G” (proprietary) fixed broadband wireless access (BWA) technology. Those “5G” BWA services are 10 to 40 times faster than current 4G LTE wireless networks, which are generally NOT used for BWA. Those two mega carriers along with Comcast are ranked among the best ISPs.

Google Fiber may not be too far behind in it’s use of fixed BWA technology to deliver triple play residential services. Alphabet, Google’s parent company, has put Google Fiber projects on hold in San Jose, Portland, and California. Google states that the move to wireless is inevitable, it will not neglect existing markets and will continue signing up new customers with wireless instead of fiber. Plans are underway to provide cities such as Dallas, Los Angeles, and Chicago with wireless internet service. Wireless technology is less expensive as it does not require labor-intensive constructions, the issues with the telephone owners, current copper and fiber providers and much cheaper to roll out.

In October 2016, Google bought Webpass, a company that specializes in the provision of wireless internet that at speeds of 1GBps at around $60. Webpass uses antennas on a building’s rooftops to provide internet connections to both businesses and residences. Unlike in conventional ISPs where you would need to have a modem, with Webpass you only need to have a router where you can plug in an Ethernet cable and distribute the internet to your office or residence.

http://fortune.com/2018/10/18/comcast-declares-victory-in-gigabit-home-internet-race/

https://hothardware.com/news/comcast-gigabit-internet-rollout

https://medium.com/@artiedarrell/fiber-no-more-google-fiber-is-switching-to-wireless-57e871ee8bc4

https://www.reviews.org/internet-service/best-internet-service-providers/

http://www.thurstontalk.com/2018/10/22/comcast-now-nations-largest-provider-of-gigabit-internet/

Globe Telecom Extends Internet Reachability in Europe via DE-CIX Interconnect

Globe Telecom [1] has extended internet reachability further in Europe by connecting its network to Deutscher Commercial Internet Exchange (DE-CIX), the world’s largest internet exchange point (IXP) [2] by size. DE-CIX is a carrier and data center-neutral IXP operator situated in Frankfurt, with a peak traffic of over 6.4 Terabits per second, interconnecting more than 800 member networks from around the world.

In total, DE-CIX globally serves over 1,500 network operators, internet service providers (ISPs), and content providers from more than 100 countries with peering and interconnection services at its 13 locations in India, the Middle East, Europe, and North America. Globe Telecom recently peered at the DE-CIX in Germany.

“This initiative will further complement existing infrastructure and enable users direct access to European content. At the same time, it functions as alternate internet gateways to the Philippines from that region as the internet is two-way,” said Gil Genio, Chief Technology and Information Officer at Globe.

In total, DE-CIX globally serves over 1500 network operators, internet service providers (ISPs), and content providers from more than 100 countries with peering and interconnection services at its 13 locations in India, the Middle East, Europe, and North America.

“We are pleased to welcome Globe Telecom within our broad range of customers. With the DE-CIX services, Globe Telecom will be able to enhance its customers’ internet user experience and connect to all major international content providers available at DE-CIX Frankfurt,” said Theresa Bobos, Director for DE-CIX Southern Europe.

…………………………………………………………………………………………………………………………………………………………………………………….

Editor’s Notes:

- Globe Telecom, commonly shortened as Globe, is a major provider of telecommunications services in the Philippines. It operates one of the largest mobile, fixed line, and broadband networks in the country. The company’s principal shareholders are Ayala Corporation and Singapore Telecommunications.

- An IXP is where IP networks meet to exchange traffic, similar to malls where different stores are present at a common location. It provides the facility that promotes and enables multi-network traffic exchange. This provides for the lowest latency path possible and therefore greatly enhances Globe customers’ internet experience.

…………………………………………………………………………………………………………………………………………………………………………………….

Genio said connecting to European IXPs is a step forward to reinforce the Philippines’ ICT ecosystem in terms of global IP connectivity as it enhances the flow of IP traffic in both directions. “Improvements may also be observed in reaching networks that are part of the exchanges as the set-up will avoid the traditional via US traverse,” he added.

Globe is currently the local telecommunications company with the most number of connections to IXPs, with 23, based on information from Hurricane Electric. This reflects the Philippines’ presence in the global IP landscape.

References:

https://www.globe.com.ph/about-us/newsroom/corporate/globe-telecom-extends-internet-reach.html

Separately, Globe Telecom was recognized as Asia’s Best Workplace of the Year at the Asia Corporate Excellence & Sustainability Awards (ACES). “We are glad to be recognized as Asia’s Best Workplace of the Year at the prestigious ACES. Being an integral part of the company’s and nation’s success, we put a premium on ensuring our employees find purpose and meaning in their work. By allowing their work to serve a purpose beyond just livelihood, we ensure the ability of our people to lead happy and meaningful lives. This, more than anything else, is what sets Globe apart from any other company,” said Renato Jiao, Chief Human Resource Officer at Globe.

Cogent Communications still growing strongly -18 years after the Fiber Optic Bust

Cogent Communications, one of the world’s largest ISPs, is carrying more traffic on its network than most incumbent telcos. During its most recent earnings report, Cogent said its quarterly traffic growth came in at 10%, while year-over-year traffic growth hit 44%. Let’s break that down into on-net and off-net services/customers:

On-net service is provided to customers located in buildings that are physically connected to Cogent’s network by Cogent facilities. On-net revenue was $93.0 million for the three months ended June 30, 2018; an increase of 0.7% from the three months ended March 31, 2018 and an increase of 8.7% over the three months ended June 30, 2017. Cogent’s more than 65,000 on-net customer connections and its nearly 2,600 on-net office buildings and carrier-neutral data centers send traffic over its all-IP-over-DWDM network, protected at Layer 3, using Ethernet as its network interface. On-net customers are obviously the most profitable customers for Cogent.

Off-net customers are located in buildings directly connected to Cogent’s network using other carriers’ facilities and services to provide the last mile portion of the link from the customers’ premises to Cogent’s network. Off-net revenue was $36.1 million for the three months ended June 30, 2018; the same amount as the three months ended March 31, 2018 and an increase of 6.3% over the three months ended June 30, 2017.

Total customer connections increased by 13.8% from June 30, 2017 to 76,193 as of June 30, 2018 and increased by 3.1% from March 31, 2018. On-net customer connections increased by 14.1% from June 30, 2017 to 65,407 as of June 30, 2018 and increased by 3.2% from March 31, 2018. Off-net customer connections increased by 12.3% from June 30, 2017 to 10,480 as of June 30, 2018 and increased by 2.3% from March 31, 2018. The number of on-net buildings increased by 161 on-net buildings from June 30, 2017 to 2,599 on-net buildings as of June 30, 2018 and increased by 58 on-net buildings from March 31, 2018.

Cogent classifies all of their customers into two types: NetCentric customers and Corporate customers.

- NetCentric customers buy large amounts of bandwidth from us and carrier neutral data centers and our Corporate customers buy bandwidth from us in large multi-tenant office buildings. Revenue in customer connections by customer type. There were 33,520 NetCentric customer connections on our network at quarter-end, which declined from last quarter due to significant circuit grooming, consolidating multiple 10 gig circuits to fewer 100 gig circuits at the same location from some of our larger NetCentric customers.

- Corporate customer revenue grew sequentially by 2.7% to $83.3 million and grew year-over-year by 11.9%. We had 42,673 Corporate customer connections on our network at quarter-end. Quarterly revenue from our NetCentric customers declined sequentially by 3.4% and grew year-over-year by 1.4%.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

CEO Dave Schaeffer’s Earnings Call Remarks:

The size and scale of our network continues to grow. We have over 927 million square feet of multi-tenant office space on-net in North America. Our network consists of over 31,900 metro fiber miles and over 57,400 intercity route miles of fiber.

Cogent remains the most interconnected network in world, where we are directly connected with over 6,360 networks. Less than 30 of these networks are settlement-free peers. The remaining over 6,330 networks are paying Cogent transit customers.

We are currently utilizing 27% of the lit capacity in our network. We routinely augment capacity in sections of our network to maintain these low utilization rates. For the quarter, we achieved sequential quarterly traffic growth of 10% in what is traditionally a slow seasonal period for traffic growth and we saw a significant improvement in our year-over-year quarterly traffic growth to over 44%.

We operate 52 Cogent-controlled data centers with 587,000 square feet of space and we are operating those facilities at 32% utilization. Our sales force turnover rate in the quarter was 4.8% per month, again better than our long-term average turnover rate of 5.7% per month. And I think a testament to the training and retention programs that we’ve put in place. We ended the quarter with 438 reps selling our services.

Cogent remains the low cost provider of internet access and transit services. Our value proposition to our customers remains unparalleled in the industry. Our business remains entirely focused on the Internet and IP connectivity and data colocation services. Our services provide a necessary utility to our customers. Beginning at the start of Q2 and April 1st, we began selling our SD-WAN services. We do not expect a material contribution from these services for the next several quarters.

We expect our annualized constant currency long-term revenue growth to be consistent with our annualized guidance of 10% to 20%, and our long-term EBITDA margin expansion rates to remain approximately 200 basis points per year for the next several years.

We expect to grow the sales force at between 7% and 10% per year for the next several years, while we expect operational head count growth to be slower at probably 2% to 3%. So the mix will increasingly become more sales-centric. Because of the efficiencies in running our business and the standardization of our products and the systems that we’ve deployed, we can sustain 44% traffic growth, 20% growth in unit number of connections and do that with a increase in operational and overhead employees of only about 2% to 3% per year. The sales force, however, is the engine that will drive accelerating revenue growth. And investing in that sales force has been and continues to be our major focus.

Analysis:

Cogent is trying to provide the most bandwidth at the lowest possible price, which means it’s in a race to run its network at the lowest possible cost, which means it’s in a race to take every advantage of new optical networking and routing technologies, as soon as they’re available.

“We divide the network into four big technology regions — edge routing, core routing, metro transport and long-haul transport,” Schaeffer told Light Reading. “In all of those functional areas we are on our third generation of equipment — we’ve done two complete forklift upgrades in 19 years — and, you know, I’m sure we’ll go to a fourth generation soon,” he added.

Webcast Replays:

The KeyBanc Capital Markets 20th Annual Global Technology Leadership Forum was held at the Sonnenalp in Vail, CO. Dave Schaeffer will be presenting on Monday, August 13th at 10:00 a.m. MT. Investors and other interested parties may access the live webcast of the presentation by visiting the webcast page.

The Oppenheimer 21st Annual Technology, Internet & Communications Conference was held at the Four Seasons Hotel in Boston, MA. Dave Schaeffer will be presenting on Wednesday, August 8th at 1:05 p.m. ET. Investors and other interested parties may access the live webcast of the presentation by visiting the webcast page.

The Cowen 4th Annual Communications Infrastructure Summit was held at the St. Julien Hotel and Spa in Boulder, CO. Dave Schaeffer will be presenting on Tuesday, August 7th at 3:30 p.m. MT. Investors and other interested parties may access the live webcast of the presentation by visiting the webcast page.

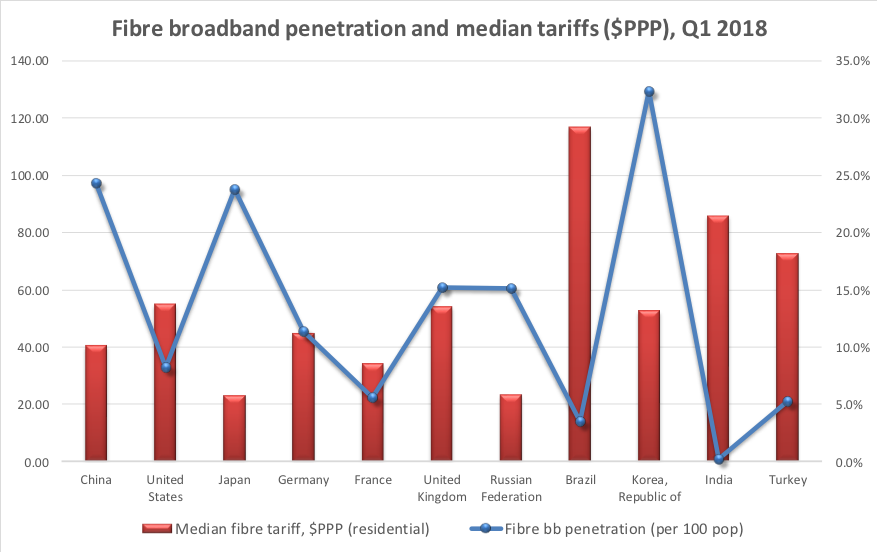

Point Topic: China leads FTTH adoption with 80% of net adds through 1Q-2018

|

|

|

PointTopic: Fiber & cable make up 3/4 of global fixed broadband subscriptions

Fiber and cable networks are dominating the global broadband market, with the technologies now servicing 77% of fixed subscriptions, new figures from Point Topic have revealed.

According to the Global Broadband Statistics, which take into account subscriptions up to the end of 2017, more than 50% of people in more than 40 countries, including Singapore (97%), China (89%), United States (87%), and the UK (55%), are connected via full-fiber, fiber-fed copper or cable.

Point Topic Research Director Dr Jolanta Stanke told the Broadband Forum:

“We are finding that customers across most global regions increasingly prefer faster broadband services delivered over fiber and cable platforms, as opposed to ADSL. This trend will continue as more bandwidth-hungry young consumers become paying decision makers, even though superfast 4G LTE and 5G mobile broadband services will compete for their wallets.”

Fiber-fed subscriptions – including Fiber-to-the-Home (FTTH), Fiber-to-the-Building (FTTB), Fiber-to-the-Cabinet (FTTC), Very High Bitrate Digital Subscriber Line (VDSL), VDSL2 and G.fast – accounted for 57% of broadband subscriptions, with more than 530 million connections. Stanke agreed VDSL and Gfast were together largely responsible for the growth that fiber has seen, with more than 30 operators across all continents deploying or trialing G.fast.

“G.fast gives operators a more cost-effective variant of fiber that will be used by operators who want to upgrade their existing networks quicker and more easily,” she added. “This could enable them to serve more customers in less densely populated areas, where direct fiber investment is less economically feasible.”

In total, cable, including hybrid fiber-coaxial, accounted for 20% of all fixed broadband connections. According to the report, the latest standard of this technology is currently deployed across several markets, being especially popular in North America, and can deliver gigabit download speeds.

Broadband Forum CEO Robin Mersh said the figures reflect the fact that new technologies that let operators deploy fiber deep into the network without having to enter buildings themselves are quickly moving from trials to mass deployment.

“If operators want to deliver competitive broadband services, maximizing their investments through the use of technologies like G.fast is vital,” said Mersh. “Expanding the footprint of their existing fiber networks in this way is cost-effective and delivers the gigabit speeds consumers crave. The growing trend towards fiber, whether its fiber-fed copper or full fiber, and cable deployments highlighted by Point Topic’s report confirms that the Forum’s work on interoperability and management of ‘fiber-extending’ technologies is vitally important.”

The voracious demand for connectivity is evident in the increased demand for fiber, cable and coax despite the parallel growth of LTE and MAYBE (?) “5G.”

Though “5G” is in currently proprietary to each wireless network operator, huge investments in fiber, coax and copper are being made because strategic planners expect 5G to be mainstream in the next several years (we think NOT until late 2021 at the earliest when IMT 2020 recommendations are finalized and implemented in base stations and endpoint devices.

Last month, Broadbandtrends’ Global Service Provider G.fast Deployment Strategies surveyed 33 incumbent and competitive broadband operators from across the globe. The market research firm found that four in five service providers have G.fast plans for this year and that 27% are in active deployments. AT&T is a huge supporter of G.fast while Verizon is not.

About the Broadband Forum

Broadband Forum, a non-profit industry organization, is focused on engineering smarter and faster broadband networks. The Forum’s flagship TR-069 CPE WAN Management Protocol has now exceeded 800 million installations worldwide.

Cable Companies/MSOs Continue to Dominate U.S. Broadband Access with 64% Market Share

by Karl Bode edited by Alan J Weissberger

The nation’s biggest cable companies continue to dominate traditional telcos when it comes to quarterly broadband additions. According to the latest data by Leichtman Research, the nation’s top cable operators added 845,000 subscribers during the first quarter, while the nation’s telcos lost 45,000 broadband subscribers during the quarter. That’s largely thanks to many phone companies (Verizon, Frontier, Windstream, CenturyLink) refusal to upgrade aging DSL users at any real scale, resulting in a slow but steady exodus as users flee to cable to obtain the FCC’s definition of broadband (25 Mbps).

According to Leichtman, that’s eight straight quarters during which the nation’s telcos have lost subscribers.

Leichtman’s findings for the quarter include:

- Overall, broadband additions in 1Q 2018 were 83% of the 965,000 net adds in 1Q 2017

- The top cable companies added about 845,000 subscribers in 1Q 2018 – 84% of the net adds for the top cable companies in 1Q 2017

- The top telephone companies lost about 45,000 subscribers in 1Q 2018 – similar to the net losses in 1Q 2017

- Telcos have had combined net broadband losses in each of the past eight quarters

- At the end 1Q 2018, cable had a 64% market share vs. 36% for Telcos – compared to 61% for cable vs. 39% for Telcos at the end of 1Q 2016

“With the addition of 800,000 subscribers in the quarter, top broadband providers in the U.S. cumulatively now account for about 96.5 million subscribers,” said Bruce Leichtman, president and principal analyst for Leichtman Research Group, Inc. “Over the past year, there were about 1,950,000 net broadband adds, compared to about 2,550,000 net adds over the prior year.”

………………………………………………………………………………………………………………………………

At the end of the first quarter, cable had a 64% market share versus 36% for Telcos — compared to 61% for cable versus 39% for Telcos at the end of 2016. This expanding monopoly not only reduces the incentive on cable to to improve historically-terrible customer service, but it also gives them the green light to abuse these captive markets via a bevy of price hikes — especially arbitrary and unnecessary usage caps and overage fees.

Overall, broadband growth continues to slow, which is driving many of these companies into additional markets (like online advertising).

References:

Telcos Refusal to upgrade period.

quote:

That’s largely thanks to many phone companies (Verizon, Frontier, Windstream, CenturyLink) refusal to upgrade aging DSL users at any real scale, resulting in a slow but steady exodus as users flee to cable to obtain the

The mess the US is in goes back to the break up ATT, and possibly further.

The RBOC’s and other ILEC were in the cat bird seat, and BLEW IT! They could have taken their already wired to practically every one position and just blown the MSO’s out of the water in the early days of @Home etc..

INSTEAD they chose to just let the MSO’s develop things, and DO NOTHING In most cases to some DSL, and some fiber. When VZ started to get its act togehter and try to right the ship, Gordon Gecko’s just backed up and ran into the iceberg again!

I honestly believe had ISDN been pushed harder by ATT in the 70’s we would see ubiquitous HSD to everyone via ATT. WHY Well starting with a DIGITAL LINE to the premises in the 70’s… then upgrade from there…128K in the 70’s compared to what most were getting 110 or 300 or even if you were lucky 1200 baud! 2400 baud was not that old into the early 80’s! I had a 2400 baud for QLink..

The ILEC/RBOC’s blew their chance, they had everything there and all they had to do was continue to ugprade. They chose not to! Now we have this mess.

FCC approves SpaceX plan for low orbit broadband satellite network

On Thursday the FCC gave formal approval to a plan by SpaceX to build a global broadband satellite network using low-Earth orbit satellites. The FCC order approving SpaceX’s application came with some conditions, like avoiding collisions with orbital debris in space. Some of the other conditions imposed by the FCC relate to signal power levels and preventing interference with other communications systems in various frequency bands.

SpaceX intends to start launching operational satellites as early as 2019, with the goal of reaching the full capacity of 4,425 satellites in 2024. The FCC approval just requires SpaceX to launch 50 percent of the satellites by March 2024, and all of them by March 2027. SpaceX has been granted authority to use frequencies in the Ka (20/30 GHz) and Ku (11/14 GHz) bands.

“This is the first approval of a U.S.-licensed satellite constellation to provide broadband services using a new generation of low-Earth orbit satellite technologies,” the Federal Communications Commission said in a statement.

The Federal Aviation Administration said on Wednesday that SpaceX plans to launch a Falcon 9 rocket on April 2 at Cape Canaveral, Florida. “The rocket will carry a communications satellite,” the FAA said.

FCC Chairman Ajit Pai in February had endorsed the SpaceX effort, saying: “Satellite technology can help reach Americans who live in rural or hard-to-serve places where fiber optic cables and cell towers do not reach.”

About 14 million rural Americans and 1.2 million Americans on tribal lands lack mobile broadband even at relatively slow speeds.

FCC Commissioner Jessica Rosenworcel, a Democrat, said on Thursday that the agency needs “to prepare for the proliferation of satellites in our higher altitudes.” She highlighted the issue of orbital debris and said the FCC “must coordinate more closely with other federal actors to figure out what our national policies are for this jumble of new space activity.”

SpaceX’s network (known as “Starlink”) will need separate approval from the International Telecommunication Union (ITU). The FCC said its approval is conditioned on “SpaceX receiving a favorable or ‘qualified favorable’ rating of its EPFD [equivalent power flux-density limits] demonstration by the ITU prior to initiation of service.” SpaceX will also have to follow other ITU rules.

Like other operators, SpaceX will have to comply with FCC spectrum-sharing requirements. Outside the US, coexistence between SpaceX operations and other companies’ systems “are governed only by the ITU Radio Regulations as well as the regulations of the country where the earth station is located,” the FCC said.

SpaceX and several other companies are planning satellite broadband networks with much higher speeds and much lower latencies than existing satellite Internet services. SpaceX satellites are planned to orbit at altitudes of 1,110km to 1,325km, whereas the existing HughesNet satellite network has an altitude of about 35,400km.

SpaceX has said it will offer speeds of up to a gigabit per second, with latencies between 25ms and 35ms. Those latencies would make SpaceX’s service comparable to cable and fiber, while existing satellite broadband services have latencies of 600ms or more, according to FCC measurements.

“SpaceX states that once fully deployed, the SpaceX system… will provide full-time coverage to virtually the entire planet,” the FCC order said.

The FCC previously approved requests from OneWeb, Space Norway, and Telesat to offer broadband in the US from low-Earth orbit satellites. SpaceX is the first US-based operator to get FCC approval for such a system, the FCC said in an announcement.

“These approvals are the first of their kind for a new generation of large, non-geostationary satellite orbit [NGSO], fixed-satellite service [FSS] systems, and the Commission continues to process other, similar requests,” the FCC said.

SpaceX launched the first demonstration satellites for its broadband project last month. In addition to the 4,425 satellites approved by the FCC, SpaceX has also proposed an additional 7,500 satellites operating even closer to the ground, saying that this will boost capacity and reduce latency in heavily populated areas. It’s not clear when those satellites will launch.

Space debris

FCC approval of SpaceX’s application was unanimous. But the commission still has work to do in preventing all the new satellites from crashing into each other, FCC Commissioner Jessica Rosenworcel said.

“The FCC has to tackle the growing challenge posed by orbital debris. Today, the risk of debris-generating collisions is reasonably low,” Rosenworcel said. “But they’ve already happened—and as more actors participate in the space industry and as more satellites of smaller size that are harder to track are launched, the frequency of these accidents is bound to increase. Unchecked, growing debris in orbit could make some regions of space unusable for decades to come. That is why we need to develop a comprehensive policy to mitigate collision risks and ensure space sustainability.”

FCC rules on satellite operations were originally “designed for a time when going to space was astronomically expensive and limited to the prowess of our political superpowers,” Rosenworcel said. “No one imagined commercial tourism taking hold, no one believed crowd-funded satellites were possible, and no one could have conceived of the sheer popularity of space entrepreneurship.”

SpaceX still needs to provide an updated debris prevention plan as part of a condition the FCC imposed on its approval.

The commission order said:

Although we appreciate the level of detail and analysis that SpaceX has provided for its orbital debris mitigation and end-of-life disposal plans, we agree with NASA that the unprecedented number of satellites proposed by SpaceX and the other NGSO FSS systems in this processing round will necessitate a further assessment of the appropriate reliability standards of these spacecraft, as well as the reliability of these systems’ methods for de-orbiting the spacecraft. Pending further study, it would be premature to grant SpaceX’s application based on its current orbital debris mitigation plan. Accordingly, we believe it is appropriate to condition grant of SpaceX’s application on the Commission’s approval of an updated description of the orbital debris mitigation plans for its system.

The approval of SpaceX’s application is conditioned on the outcome of future FCC rulemaking proceedings, so SpaceX would have to follow any new orbital debris rules passed by the FCC. We detailed the potential space debris problem in a previous article. Today, there are more than 1,700 operational satellites orbiting the Earth, among more than 4,600 overall, including those that are no longer operating.

SpaceX’s plan alone would nearly double the total number of orbiting satellites. SpaceX told the FCC that it has plans “for the orderly de-orbit of satellites nearing the end of their useful lives (roughly five to seven years) at a rate far faster than is required under international standards.”

Opposition from competitors

SpaceX’s application drew opposition from other satellite operators, who raised concerns about interference with other systems and debris. The FCC dismissed some of the complaints. For example, OneWeb wanted an unreasonably large buffer zone between its own satellites and SpaceX’s, the FCC said:

[T]he scope of OneWeb’s request is unclear and could be interpreted to request a buffer zone that spans altitudes between 1,015 and 1,385 kilometers. Imposition of such a zone could effectively preclude the proposed operation of SpaceX’s system, and OneWeb has not provided legal or technical justification for a buffer zone of this size. While we are concerned about the risk of collisions between the space stations of NGSO systems operating at similar orbital altitudes, we think that these concerns are best addressed in the first instance through inter-operator coordination.

If operators fail to agree on a coordination plan in the future, “the Commission may intervene as appropriate,” the FCC said.

4 U.S. Telcos ask FCC to support 3.5 GHz spectrum under Connect America Fund II

The Federal Communications Commission u (FCC) has received a petition from Windstream, CenturyLink, Frontier and Consolidated urging the agency to continue to support census tract license sizes in rural areas. The providers said this would help them deploy 3.5 GHz broadband wireless access technology under the agency’s Connect America Fund (CAF) II.

In a joint FCC filing, these telecom service providers, which are leveraging CAF-II funding to provide 10/1 Mbps rural broadband services, said they are testing and deploying 3.5 GHz-compatible broadband wireless technology in areas where deploying fiber and related facilities is cost prohibitive. By offering neutral access to the 3.5 GHz band in rural areas, these providers say they would be able to accelerate rural broadband rollouts. A key issue for these providers is that Partial Economic Areas (PEAs) aren’t aligned with how rural CAF areas are structured. A recent WISPA study illustrated that rural CAF areas tend to cluster around the edges of PEAs.

“To make these types of rural broadband deployments possible, the FCC must preserve census tract license sizes in rural areas—partial economic areas and even counties would preclude meaningful participation in the band by companies focused on providing broadband in the most rural areas,” the service providers said in the joint filing. “By licensing the 3.5 GHz band in rural areas on a census tract basis, the FCC can help enable faster broadband to more rural Americans.”

The other issue raised in rural areas is the amount of available spectrum. Although there’s a shortage of spectrum in urban areas like Boston and New York City, the service providers say “there is a relative spectrum abundance in rural areas.”

Proving out the economics for broadband deployments is also a challenge. In an urban area, there could be several providers vying for consumers’ and business’ attention, but in a rural area service providers rely on subsidies like the CAF-II program to make investments. Finally, the service provider group said that secondary markets are too costly and slow to allow for rural deployments.

“Rural players have not been able to realistically obtain spectrum in other bands,” the providers said. “At the same time, package bidding coupled with census tract license sizes reduces exposure risk for larger companies while promoting competition.”

The providers added that “there should be no concern that carriers are going to ‘cherry-pick’ licenses in rural areas.”

To make more spectrum available to service providers expanding rural broadband access, these service providers proposed that the FCC should allocate additional spectrum available for rural areas. Specifically, the group said that the FCC should consider allocating 80 MHz of spectrum as part of the CAF program.

“80 MHz in CAF CBs would enable carriers to deploy sustained speeds greater than 25/3 or more to over 200 customers per site,” the service provider group said. “Technology advances will allow for faster speeds in the future.”

Frontier is currently rolling out 25 Mbps speeds in some of its rural markets using the 3.5 GHz spectrum and will consider higher speeds as it procures new equipment and spectrum over time.

While it’s going to take time to see how these providers apply broadband wireless to their rural builds, it’s clear that they are showing some commitment to finding new ways to serve markets that have been traditionally ignored.

Ongoing tests, deployments

Seeing the 3.5 GHz band as another tool to reach rural Americans, these providers are in some stage of either testing or deploying broadband wireless.

Frontier, for one, confirmed in September it was testing broadband wireless with plans to deploy it in more areas if it meets its requirements. The service provider is also exploring 3.5 GHz deployments, including as a member of the CBRS Alliance, which is exploring CBRS specifications and spectrum use rules.

Already, the service provider has been making progress with its CAF-II commitments, providing broadband to over 331,000 and small businesses in its CAF-eligible areas, and the company has improved speeds to nearly 875,000 additional homes and businesses. The deployments reflect a combination of Frontier capital investment and resources that the FCC has made available through the CAF program.

Perley McBride, CFO of Frontier, told investors during a conference in September 2017 that broadband wireless could be a “good solution” to the deployment challenge “in very rural America[,] and if it works the way [Frontier is] expecting it to work, . . . [Frontier] will deploy more of that next year.”

Windstream is trialing fixed wireless and modeling 3.5 GHz deployments and is also a member of the CBRS Alliance.

CenturyLink is also advancing its CAF-II commitments, reaching over 600,000 rural homes and businesses with broadband over the past two years. While it has not revealed any specific plans yet, CenturyLink has obtained an experimental license for 3.5 GHz spectrum.

“The testing seeks to understand the viability of new technologies in this band that may be useful in providing fixed broadband services,” CenturyLink said in the filing.

References:

https://techblog.comsoc.org/2017/10/09/centurylink-asks-fccs-for-3-4-ghz-fixed-wireless-test/

https://www.agri-pulse.com/articles/10523-new-bill-would-set-up-rural-broadband-task-force

AT&T at DB Investor Conference: Strategic Services, Fiber & Wireless to Drive Revenue Growth

At the Deutsche Bank Media, Telecom and Business Services Conference, John Stephens, senior executive vice president and chief financial officer, AT&T discussed the company’s plans for 2018 and beyond. Mr. Stephens said AT&T remains confident that it is on the right track to get its wireline business services back to positive growth as more customers transition to next-generation strategic services like SD-WAN and Carrier Ethernet. However, the drag from legacy services will continue to be an issue for the near term. He then outlined the company’s priorities for 2018, which include closing its pending acquisition of Time Warner and investing $23 billion in capital to build the best gigabit network in the United States.

On the entertainment side of the business, AT&T plans to launch the next generation of its DIRECTV Now video streaming service in the first half of 2018. The new platform will include features like cloud DVR and a third video stream. Additional features expected to launch later in 2018 include pay-per-view functionality and more video on demand. Note that DIRECT TV Now can operate over a wireline or wireless network with sufficient bandwidth to support video streaming. Stephens said during the interview:

“……Giving us this opportunity to come up with a new platform later in this first half of this year, the second-generation plant for giving customers Cloud DVR, additional ability to pay per view and most sporting events and movies, and all kinds of other capabilities is what we’re seeing here, that’s what we want to do with regard to that entertain business and transitioning and we’re confident that we’re on the right track and it’s going quite well.”

The company’s 2018 plans also include improved profitability in its wireless operations in Mexico and, after the Time Warner acquisition closes, deployment of a new advertising and analytics platform that will use the company’s customer data to bring new, data-driven advertising capabilities within premium video. And, as always, AT&T remains laser-focused on maintaining an industry-leading cost structure.

AT&T’s investment plans include deployment of the FirstNet network, America’s first nationwide public safety broadband network specifically designed for our nation’s police, firefighters, EMS and other first responders.

“We were 56 out of 56, 50 states, 5 territories and the districts, probably all choose to put their public safety network, their FirstNet, their first responder network with AT&T, so that’s thrilling for us, that gives us the full funding of the program, it gives us the full authority to be the public service provider for the country, we’re really proud of that, and only because of the business aspects that’s serving our fellow citizens and being able to participate in the honorable job of saving lives and protecting people. So we’re really jazzed up about that.

Secondly, our plans were made last year for how to build out, and we’ve now been given the authority and the official build plans, approved build plans from the FirstNet authority. We spend last year investing in the core network, I think if people filed us in the fourth quarter; they said we actually got a $300 million reimbursement from the FirstNet authority for the expenditures we incurred last year. So the relentless preemption, the prioritized service refers to prices for police and fire and handling some emergency medical personal; all of that’s been done and now we’re out deploying the network, not only the 700 but also our AWS and WCS, our inventoried network that we now get to put into service on a very economic basis because we can do one tower client, we have the crane out there once, we have the people out there once and they’ve put all three pieces of spectrum at it once.”

The company will also enhance wireless network quality and capacity and plans to be the first to launch mobile “5G” service in 12 cities by the end of the year. AT&T announced in February that Atlanta, GA; Dallas and Waco, TX. will be among its first “5G” markets.

“We think about 5G is 5G evolution and I say that because it’s really important to put it all in perspective. So we think FirstNet, put WCS, AWS with 700 band 14 [ph], and use carrier aggregation and you use forward [indiscernible]; we’ve done that kind of test without the 700, we did that in San Francisco, we got 750 mag speeds in the City of San Francisco on this new network, this new 5G evolution; it’s using the LTE technology, it’s using the existing network but all this new technology. So if you think about that evolution now, when you lower that network hub, those 750 theoretical speeds might go down to 150 or 100 or somewhere down but tremendous speed even on a loaded network; so that’s the first step, we’re doing that now extensively and we’re going to do more of that as we build the first step that work out and put the 700 band in. So that’s the first step for us in this evolution.

Second, people might not think about this way but for us absolutely critical is the fiber bill. We’re taking a lot of fiber out to the Prime [ph], we’re taking a lot of fiber out to business locations, currently we have about 15 million locations with fiber between business and consumer, and by July next year, we’ll have about 22 million, about 8 million business, about 14 million to the Prime if you will, for consumers. So fiber is the key, and it’s a key not only delivering to the home or to the business but for the backhaul support. So if you’re an integrated carrier like we are and you’re building this fiber to go to the home, you’re going to pass the tower, you’re going to get fiber to that tower, you’re going to pass the business location, shopping mall, strip center, you’re going to build out to those.

So 5G is the second stage, we’ve got to think all the inter-gig this is the ability to deliver broadband overall electrical power lines, we’re testing that, we’ll see how that goes, that’s another step. If you think about using millimeter wave to do backhaul for small cells in really congested areas, we have high traffic volumes, you want to take a lot of traffic off, we have tested that, we have used millimeter wave to do that, we can do that. If you think about millimeter wave to do fixed wireless; so from the ally to my home, we have tested that we have the capability to do that, the challenges on that is where do you take it from the ally, where do you offload it, give it on to the network at what those costs are, but we can do that.

Lastly, you will see us put 5G into the core network. All of those things that were going to have to be measured by one of the chipsets ready for the handsets, we expect the chipsets might be next year, handset will come after that but we’re looking at the historically slow upgrade timeframe for phones. We had a couple of quarters last year that the upgrade rates were about 4%, that would equate the 25 quarters before your phone base turned over in an extreme example; so suggesting that things are going to be in the core network, it’s going to take a while, we’ll have pucks [ph] out by the end of the year, that will help but you have to have balance with regard to this.

When you think about those business cases, you think about those augmented reality and virtual reality and robotics and autonomous cars and things on the edge, those are going to be really important, that’s where the business cases will take us but we’ve got a long way to go before we get there. As we build FirstNet, we have been good fortunate being able to so to speak build the network house and leave the room for our 5G capability so that when it’s ready, we can just plug it in to do it with software defined network design, we had a great advantage for that but we’re going to have to make sure we have all of the equipment, not only switching equipment, the radio, the antenna but also the handset equipment before we start — if you will over-indexing on the revenues opportunities, they will be there, we will lead in the gigabit network.

We’ll have the best one because what FirstNet provides us and what the technology developments have allowed us and we will use 5G in that network but I want to be careful about how we think about when it’s going to be — you’re going to have a device in your hand and walking around on a normal kind of usage basis using 5G.”

Stephens said that AT&T reaches about 15 million customer locations with fiber. This includes more than 7 million consumer customer locations and more than 8 million business customer locations within 1,000 feet of AT&T’s fiber footprint. He expects this to increase to about 22 million locations by mid-2019.

…………………………………………………………………………………………………………………………………….

For 2018, AT&T expects organic adjusted earnings per share growth in the low single digits, driven by improvements in wireless service revenue trends, improving profitability from its international operations, cost structure improvements from its software defined network/network function virtualization efforts and lower depreciation versus 2017.

Like earlier quarters, the challenges in the fourth quarter for AT&T came from declines in legacy services like Frame Relay and ATM. The company noted that fourth-quarter declines in legacy products were partially offset by continued growth in strategic business services. Total business wireline revenues were $7.4 billion, down 3.5% year-over-year but up sequentially.

Stephens said that more AT&T customers are adopting next-gen services, creating a new foundation for wireline business revenue growth.

“What’s happened is our customers have embraced the strategic services,” Stephens said. “Strategic services are over a $12 billion annual business and are over 42% or so of our revenue and are still growing quickly.”

Indeed, AT&T’s fourth-quarter strategic business services revenues grew by nearly 6%, or $176 million, versus the year-earlier quarter. These services represent 42% of total business wireline revenues and more than 70% of wireline data revenues and have an annualized revenue stream of more than $12 billion. This growth helped offset a decline of more than $400 million in legacy service revenues in the quarter.

Stopping short of forecasting overall wireline business service revenue growth, Stephens said that AT&T will eventually see a point where strategic services will surpass legacy declines.

“As we get past this inflection point where strategic services are growing at a faster than the degradation of legacy, we can get to a point where we are growing revenues,” Stephens said. “We’re not predicting that but we see the opportunity to do that.”

To achieve these business services revenue goals, AT&T’s business sales team is taking a two-pronged approach: retaining legacy services or converting them to strategic services.

While wireline business services continue to be a key focus for AT&T, the service provider is not surprisingly looking at ways to leverage its wireless network to help customers solve issues in their business. The wireless network can be used to support a business customer’s employee base while enabling IoT applications like monitoring of a manufacturing plant or a trucking fleet. Stephens expanded on the role of IoT to close out the interview:

“…you (‘ve) got to realize that if you build this FirstNet network out, things like IoT, things like coverage for business customers, things like the ability to connect factories that are automated, the robotics that have to have wireless connectivity to a controlled center for business customers, all improves dramatically and with that comes this opportunity to sell these wireless services. When you’re in — with the CIO and you can solve his security business, you can solve his big pipe of strategic services but you can also solve some wireless issues that his HR guy has for his connectivity for his employees, you can solve some issues that his engineering department has because they want to get real-time information about how their products are working out, whether it’s a car or a jet engine or a tractor, how it’s working in the field in real-time or you can give them new product and services demand for their internal sources like their pipelines or their shipping fleet.

This IoT capability can solve a lot of issues, you can make that CIO as the success factor for all his related peers, that’s a great thing to great solutions approach to business and that’s what we’re trying to do. Our team is trying to provide solutions for the business customers and we think having those two things together are really important.”

References:

https://www.businesswire.com/news/home/20180306006770/en/John-Stephens-ATT-CFO-Discusses-Plans-2018

https://techblog.comsoc.org/2018/01/14/att-mobile-5g-will-use-mm-wave-small-cells/

C Spire – Entergy Mississippi Partnership to Build Fiber Network along 5 routes

U.S. service provider C Spire today announced a partnership with electric utility Entergy Mississippi which aims to bring more than 300 miles of fiber to remote areas of Mississippi. C Spire will build and own the network, with Entergy contributing construction costs, according to C Spire Vice President of Government Relations Ben Moncrief in an interview with Telecompetitor.

Entergy will lease capacity on the network from C Spire to support its smart grid initiatives, he said. C Spire eventually expects to extend the middle-mile network to end user locations to support retail services, he added, although he emphasized that any such plans are not part of today’s news.

Details about the C Spire – Entergy partnership can be found in this press release. Clearly there were a lot of synergies for these companies to work together.

“This opens the door to offering service to residences and industrial parks,” Moncrief said. “But today is just about getting the (fiber optic) backbone in place.”

When Entergy Mississippi sought the Mississippi Public Service Commission’s approval to build a network to support its smart grid plans, one of the commissioners asked whether that network could also be “at least a foundation for broadband services,” Moncrief explained.

That idea led Entergy to a meeting with C Spire at which representatives of both companies had an “aha moment,” Moncrief recalled.

C Spire initially was a wireless carrier, as well as a provider of wireline business services, but in recent years has been quite aggressive in deploying fiber-to-the-home (FTTH) and other broadband network infrastructure in numerous rural markets in Mississippi. Meanwhile, Moncrief said, “Here’s an electric utility that for security reasons is keeping infrastructure away from population centers.”

The network will be installed with a minimum of 144-count fiber, “in some places more,” Moncrief noted. Each company will have its own fiber. The areas that the network will run through are “very rural” and might have been too costly for C Spire to build out to without the Entergy investment, Moncrief added.

C Spire also will gain connectivity from the rural areas to population centers, Moncrief said.

C Spire Entergy Fiber Network Map

……………………………………………………………………………………………………………………………….

The construction project will involve placing fiber optic cable along five separate routes as follows:

- Delta: a 92-mile route through Sunflower, Humphreys, Madison and Hinds counties and near the cities of Indianola, Inverness, Isola, Belzoni, Silver City, Yazoo City, Bentonia, Flora and Jackson.

- North: a 51-mile stretch in Attala, Leake and Madison counties, including near the towns of McAdams, Kosciusko and Canton.

- Central: a 33-mile route through Madison, Rankin and Scott counties and near the towns of Canton, Sand Hill and Morton.

- South: a 77-mile route passing through Simpson, Jefferson Davis, Lawrence and Walthall counties and near the towns of Magee, Prentiss, Silver Creek, Monticello and Tylertown.

- Southwest: a 49-mile stretch in Franklin and Adams counties that’s near the communities of Bude, Meadville, Roxie, Natchez and Eddiceton.

“We’re excited about partnering with C Spire to modernize our electrical grid and expand rural broadband access in some hard-to-reach areas across the state,” said Haley Fisackerly, president and CEO of Entergy Mississippi. “We have about 30,000 customers within five miles of the proposed routes who could potentially have access to broadband service when the project is complete. In addition, all of our customers will benefit from the enhancements to our communication systems that connect our facilities, substations, offices and radio sites.” The company provides electric service to an estimated 445,000 customers in 45 counties across the state.

“A robust broadband infrastructure is critical to the success of our efforts to move Mississippi forward by growing the economy, fostering innovation, creating job opportunities and improving the quality of life for all our residents,” said Hu Meena, CEO of C Spire, a Mississippi-based diversified telecommunications and technology services company.