Optical Network Equipment Market

Goldman Sachs report: Optical Networking is the next mega trend in AI infrastructure

Goldman Sachs analysts forecast a $154billion opportunity in optical networking driven by skyrocketing capacity demands from hyperscale cloud and AI workloads. Carriers and vendors are integrating 10GbE edge networking and AI-RAN (Artificial Intelligence Radio Access Network) trials on live 5G networks.

Goldman argues that AI infrastructure is creating a networking bottleneck phase, where optical interconnects become essential to connect more chips, keep latency low, and let AI clusters scale efficiently. The total optical networking market forecast 9x increase to $154 billion is due to both scale-up and scale-out AI data center architectures grow.

AI compute gains are no longer just about faster GPU and HBM chips; they depend on moving data fast enough between chips, racks, and super-nodes. Goldman Sachs emphasizes that networking now “unlocks computing capability” by enabling seamless exchange across multiple AI chips, which is exactly where copper-based links start to fall short. That makes fiber-optic connectivity, pluggable optics, and co-packaged optics central to the next phase of AI build-out. The report splits opportunity across scale-up and scale-out networking, plus component categories such as copper cables, pluggable optical modules, CPO, and PCB midplanes.

External coverage of this report says Goldman Sachs sees scale-up as the larger pool, about $106 billion or 69% of the $154 billion TAM, while CPO could represent about $91 billion or 59% of the total, assuming 29% penetration in scale-out networking. In practical terms, the report is signaling that the highest-value optical opportunity sits inside tightly coupled AI systems, not just in long-haul or metro transport.

………………………………………………………………………………………………………………………………………………………………………………………….

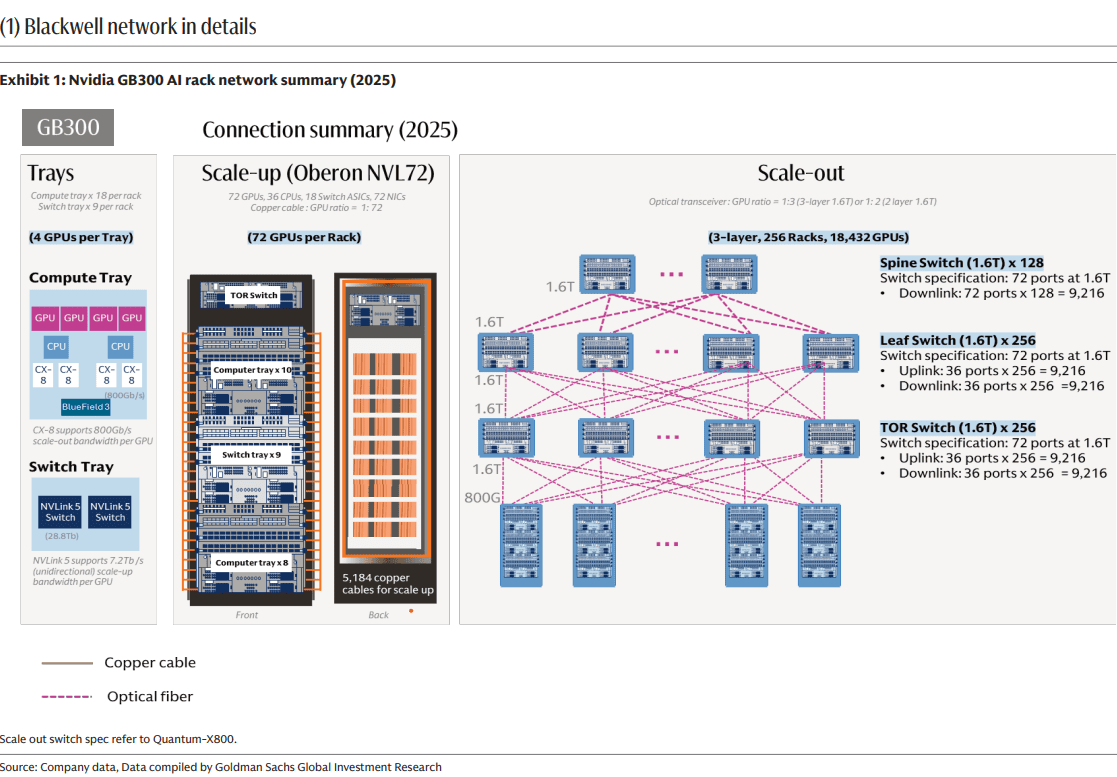

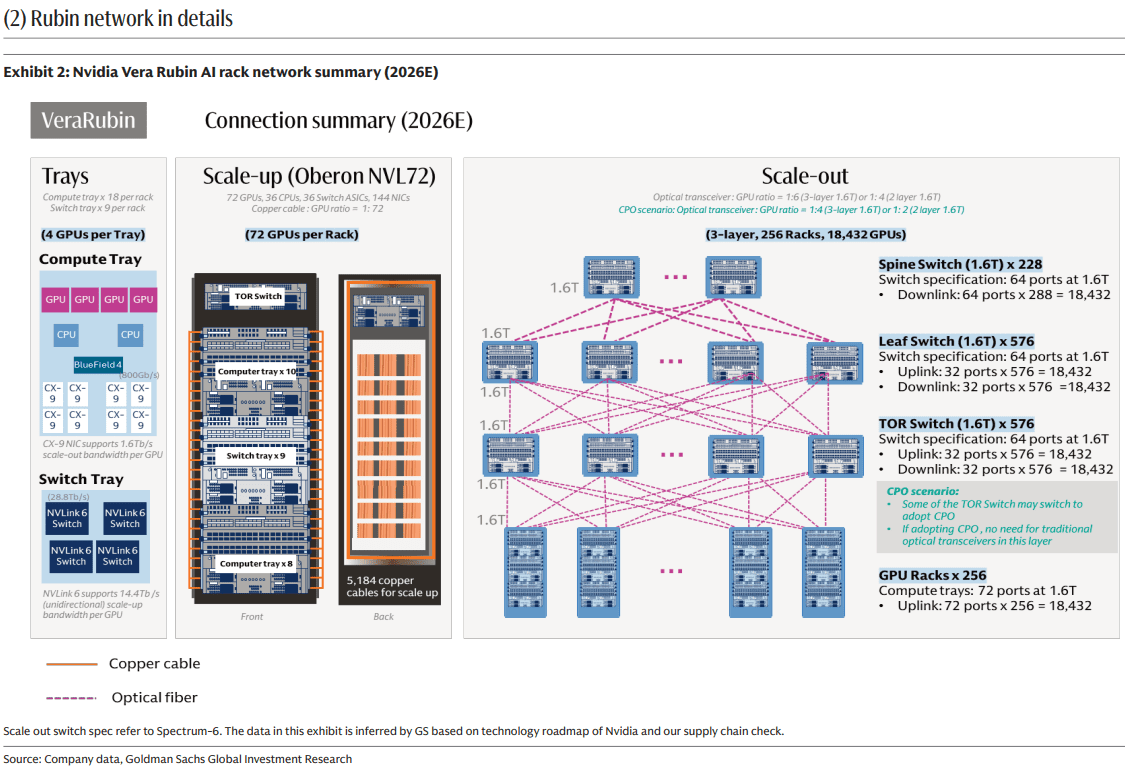

Goldman projects the following:

- Dollar content increase by 16x / 45x in Scale Out / Scale Up per computing unit from GB300 NVL72 (per computing unit means 72 GPUs per rack to reach NVL72) to Rubin Ultra NVL576 (per computing unit means 72 GPUs per rack, and 8 racks together to reach NVL576), with opportunities across pluggable optical modules, optical engines in CPO, copper cables, and PCB midplanes.

- A 13x larger addressable market for optical modules / optical engines expanding from scale out (e.g. GB300 NVL72) to scale up (e.g. Nvidia Rubin Ultra [1.] NVL576 level 2 scale up via CPO) per computing unit. n

- A 10x larger value market for pluggable optical modules in scale out per computing unit from GB300 NVL72 to Rubin Ultra NVL576, even with a 29% CPO penetration rate. The numbers of pluggable optical module (1.6T equivalent) per computing unit would increase from 216 units in GB300 NVL72 to 2.5k units in Rubin Ultra NVL576.

Note 1. Nvidia Rubin Ultra is a flagship, next-generation AI and high-performance computing (HPC) processor succeeding the standard Rubin architecture. Scheduled to debut in late 2027, it utilizes massive multi-die chiplet designs and unprecedented memory configurations to power the next wave of generative and agentic AI.

………………………………………………………………………………………………………………………………………………………………………….

Market Forecasts:

The investment bank expects the aggregate dollar content per computing unit across scale up and scale out to increase by 29x from US$315k in GB300 NVL72 to US$9.4bn in Rubin Ultra NVL576, and assuming the numbers of racks through the full product cycle are 48k racks for GB300 NVL72, and 16.5k computing units for Rubin Ultra NVL576, the aggregate value TAM across scale up and scale out would increase by 9x from US$15bn in GB300 NVL72 (mainly in 2026) to US$154bn in Rubin Ultra NVL576 (mainly in 2028).

Among the US$154bn value TAM, 69% goes to scale up, or US$106bn, and CPO contributes US$91bn, or 59% of the US$154bn value TAM, assuming CPO at 29% penetration rate in scale out.

For network architects, the important takeaway is that AI clusters are becoming optics-heavy at more layers of the network stack, not just at the edge of the rack. The likely winners are suppliers that can reduce power, improve density, and simplify packaging for very high-bandwidth links, especially around CPO and advanced pluggables. This is less a story about traditional telecom optics and more about datacenter interconnects optimized for GPU fabrics and AI training/inference throughput.

The most consistently cited “top beneficiaries” are Coherent, Lumentum, and Fabrinet. These companies sit close to the core optical component modules and manufacturing layers that scale with higher AI interconnect demand. That makes them the most straightforward proxies for the forecasted optics expansion. The report’s thesis favors companies with strong exposure to high-end optical transport, coherent optics, and data-center interconnect rather than the broader optical networking/PON equipment companies like Ciena, Nokia/Infinera, Cisco/Acacia, ADVA, or Calix.

Conclusions:

Strategically, Goldman Sachs maintains that optical networking is no longer a niche enabling layer; it is becoming a core enabler of AI capex scaling. That shifts investor attention toward optical component vendors, silicon photonics, transceiver suppliers, and adjacent packaging ecosystems. The report’s core message is simple: as AI clusters grow, the network fabric becomes a first-order constraint, and optics are the most likely answer.

References:

2026 Fiber Connect Keynote: “The Future of Fiber Optics: AI and the Quantum”

How will fiber and equipment vendors meet the increased demand for fiber optics in 2026 due to AI data center buildouts?

Big Fiber’s $250M financing deal to buildout dark fiber routes for AI Data Center expansion

Analysis: Fiber Broadband Association (FBA) whitepaper: Upgrading MSO Networks to Fiber to the Home (FTTH): A Technical Perspective

Fiber Optic Boost: Corning and Meta in multiyear $6 billion deal to accelerate U.S data center buildout

Fiber Optic Networks & Subsea Cable Systems as the foundation for AI and Cloud services

AI infrastructure investments drive demand for Ciena’s products including 800G coherent optics

DriveNets and Ciena Complete Joint Testing of 400G ZR/ZR+ optics for Network Cloud Platform

Analysis: Nokia’s strong growth in Optical Networks and AI network infrastructure

Executive Summary:

While Nokia’s first-quarter profitability improved across all reported metrics, year-over-year comparisons were significantly affected by a €120 million ($140 million) non-recurring charge recorded in the Mobile Networks business in the prior-year period. On a comparable basis, net profit increased 93% to approximately €295 million ($345 million). Despite ongoing cost restructuring initiatives, the company’s comparable operating margin remained at 6.2%, well below the ~11% levels observed in the corresponding quarters of 2021 and 2022, indicating continued margin compression relative to earlier cycle peaks.

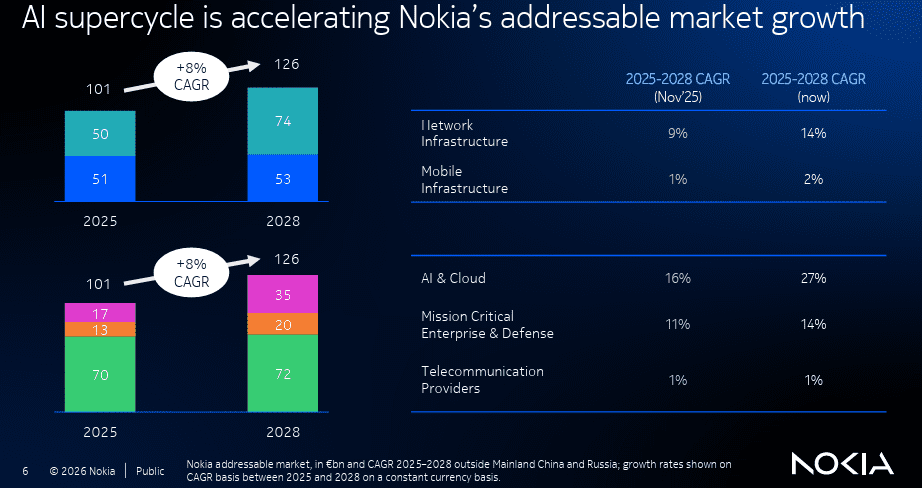

Optical networking has emerged as Nokia’s primary growth engine, significantly outpacing the company’s overall performance. At the group level, Nokia reported first-quarter comparable revenue growth of 3% year-over-year (4% in constant currency) to €4.5 billion ($5.3 billion). The acquisition of Infinera, which was completed in March last year, surely helped. As did massive investments by AI data center companies because Nokia’s optical gear is used for both intra and inter data center connectivity.

The company said Thursday that first-quarter sales of optical network infrastructure rose 12% on year, driven by demand from AI and cloud customers in the Americas. It booked 1 billion euros ($1.17 billion) of orders from AI & Cloud customers in the quarter and now sees overall sales in the network infrastructure business growing 12%-14% this year, having previously expected 6%-8%. The company had previously announced it was investing in additional manufacturing capacity to support growth and maximize the opportunity in this accelerating market.

When Nokia held its capital markets day last November, the company expecting hyperscalers to invest about $540 billion in total capital expenditure this year. That number has now been raised to more than $700 billion, Nokia CEO Justin Hotard told reporters. As part of that flows into Nokia’s order book, first-quarter optical sales grew 56% year-over-year, to €821 million (US$959 million).

Image Credits: NOKIA

……………………………………………………………………………………………………………………………………………………………………………………………………….

Performance across segments remains uneven. Key drags included the fixed broadband segment within Network Infrastructure (NI)—which also encompasses optical—as well as the Mobile Networks (MN) radio access business. Despite these headwinds, CEO Justin Hotard is positioning NI, particularly its optical and IP routing units, as the core drivers of near-term growth. The company has raised its full-year NI growth outlook to 12–14%, up from the 6–8% range communicated in January, reflecting stronger momentum in high-capacity transport and IP networking demand.

Nokia is also guiding for full-year comparable operating profit in the range of €2.0–2.5 billion ($2.3–2.9 billion). At the midpoint, this would represent approximately 11% year-over-year growth relative to 2025, indicating improving operational leverage as higher-growth segments scale. The strongest momentum remains in optical and IP networking, while the legacy radio access business is still working through margin pressure, mix shifts, and the higher capital intensity of next-generation RAN evolution.

Within this context, the Mobile Infrastructure (MI) segment remains the principal source of performance uncertainty. Following internal reorganization, the “radio networks” unit—comprising the majority of the former Mobile Networks business—accounts for 63% of MI revenue. While constant-currency performance was broadly stable, reported radio networks revenue declined 5% year-over-year to €1.58 billion ($1.85 billion), contributing to a 3% decline in total MI revenue to approximately €2.5 billion.

Segment-level profitability metrics require careful normalization. MI reported operating profit of €222 million ($259 million), representing a 68% year-over-year increase. However, adjusting for the absence of the prior-year €120 million charge, operating profit would have declined by approximately 12%. On a normalized basis, operating margin would have decreased from ~9.8% to ~8.9%, rather than increasing from the reported 5.1%, indicating underlying margin pressure in the radio access portfolio.

Additional analytical complexity arises from the inclusion of Nokia Technologies within MI reporting. This licensing-driven business has historically exhibited operating margins exceeding 70%. Assuming a comparable margin profile in the current quarter, its implied operating contribution (~€270 million / $316 million) exceeds the total reported MI operating profit. This suggests that the combined radio networks and associated software activities may be operating at or near breakeven when disaggregated from licensing revenues, highlighting the importance of segment-level transparency in assessing the underlying economic performance of Nokia’s RAN portfolio.

A restructuring program, initiated under Pekka Lundmark and continued by CEO Justin Hotard, is designed to deliver approximately €1.2 billion ($1.4 billion) in annualized cost savings by the end of 2026. This is primarily driven by a planned reduction of approximately 14,000 positions from a September 2023 baseline of ~84,000 employees (excluding subsequently divested businesses). As of year-end 2025, Nokia reported 74,100 employees, excluding Infinera, implying that the majority of targeted reductions have been completed and that approximately 4,000 additional reductions remain. Management has indicated that future efficiency gains are expected to be incremental rather than driven by further large-scale restructuring.

…………………………………………………………………………………………………………………………………………………………………………………………

Analysis:

From a systems perspective, the key signal is that transport and aggregation layers are gaining strategic weight relative to the traditional macro-RAN hardware layer. Optical growth reflects the continued densification of metro and backbone networks, driven by higher east-west traffic, AI and cloud interconnect demand, and the need for lower-latency transport to support distributed radio and edge workloads. That makes optical and IP less of a “supporting cast” and more of the enabling fabric for cloudified telecom architectures.

The RAN market is moving toward software-defined, cloud-native, and increasingly AI-assisted architectures, which raises the bar for vendor differentiation. Nokia has been emphasizing AI-RAN and anyRAN work with NVIDIA and operators including BT, NTT Docomo, T-Mobile, and others, positioning itself around AI-for-RAN, AI-on-RAN, and AI-and-RAN use cases. Architecturally, this suggests the company is trying to move beyond a pure radio-box supplier model toward a compute-centric platform strategy tied to 5G-Advanced and AI-native 6G.

This transition intensifies competition with vendors pursuing virtualized RAN, Open RAN, and multi-vendor disaggregation strategies. In that environment, the critical battleground shifts from integrated proprietary base stations to software portability, orchestration, open interfaces, cloud infrastructure integration, and accelerator support. For Nokia, the commercial challenge is that the economics of vRAN and AI-RAN depend not only on technical readiness, but also on whether operators can justify new compute and orchestration layers without eroding total cost of ownership.

The broader networking trend is convergence between mobile, optical, IP, and cloud infrastructure. The same traffic growth that pressures RAN capacity also increases demand for optical transport, IP routing, and security-aware automation across the transport and service layers. In that sense, Nokia’s segment mix highlights a wider industry direction: radio access is becoming only one part of a larger distributed compute and transport system, rather than the dominant center of gravity.

In conclusion, Nokia is benefiting as telecom architecture is becoming more horizontal and software-driven, while still facing friction in the vertically integrated legacy RAN model. Optical and IP are scaling nicely with increased high speed data center traffic; RAN is being redefined by cloud (vRAN), AI, and disaggregation; and the vendor that can best align silicon, software, orchestration, and transport will be better positioned for 5G-Advanced and early 6G/IMT 2030 transitions.

…………………………………………………………………………………………………………………………………………………………………………………………

References:

https://www.nokia.com/about-us/investors/results-reports/

Nokia in major pivot from traditional telecom to AI, cloud infrastructure, data center networking and 6G

Nokia’s AI Applications Study: “Physical AI” may require RAN redesign to support high‑volume, low‑latency uplink traffic

Nokia to showcase agentic AI network slicing; Ericsson partners with Ookla to measure 5G network slicing performance

Australia’s NBN and Nokia demonstrate multi-generation optical technologies concurrently over existing FTTP infrastructure

China’s telecom industry rapid growth in 2025 eludes Nokia and Ericsson as sales collapse

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

Indosat Ooredoo Hutchison, Nokia and Nvidia AI-RAN research center in Indonesia amongst telco skepticism

Nokia Bell Labs and KDDI Research partner for 6G energy efficiency and network resiliency

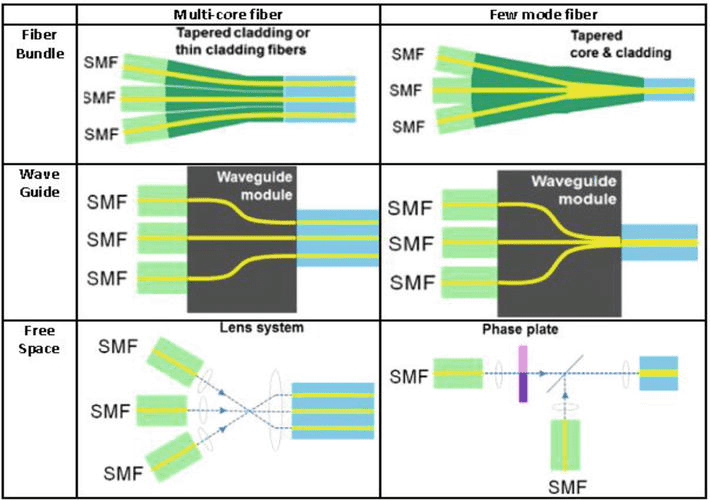

STL completes successful Multi-Core Fiber (MCF) trial with Colt in London, UK

India based STL, a global provider of optical and digital connectivity solutions for AI-era networks, has completed multi-core fiber (MCF) field trials with Colt Technology Services on Colt’s London metro optical network. The trial is a meaningful proof point for space-division multiplexing (SDM) in carrier environments, demonstrating that MCF can lift per-fiber strand capacity while staying within existing civil and duct constraints and improving overall network energy and cost metrics.

The deployment used STL’s Multiverse™ four-core MCF, designed with the same 125 µm cladding diameter as conventional single-mode fibre (SMF) and a 250/200 µm coating, enabling seamless handling with existing cable designs and installation practices. The trial route connected two Colt Points of Presence (PoPs) on the London metro network over spans of approximately 9 km and 63 km, representing both short-haul metro and longer metro-regional use cases.

From a transmission standpoint, the network achieved an 800 Gbps line rate with service validation for 100GE and 400GE, aligning with current high-capacity router and data-centre interconnect interfaces. STL and Colt validated performance across a broad set of optical and system parameters, including chromatic dispersion (CD), polarization mode dispersion (PMD), inter-core crosstalk, throughput, fault behavior, OTDR signatures, insertion loss, and optical return loss (ORL), with results within expected design envelopes. This indicates that Multiverse™ MCF can be engineered and operated to comparable performance baselines as legacy SMF while delivering higher spatial capacity.

Architecturally, STL’s MCF platform integrates four independent cores within a standard SMF cladding profile, effectively multiplying per-fibre capacity without increasing cable diameter. For operators, this directly addresses constraints in congested metro ducts, legacy civil infrastructure, and brownfield routes where augmenting capacity by pulling additional cables is either cost-prohibitive or operationally disruptive. In these scenarios, MCF creates a higher bit-per-mm² and bit-per-duct investment profile, improving both capex efficiency (less civil work, fewer ducts) and opex metrics such as energy per transported bit.

STL positions itself as one of the early movers in taking MCF from controlled lab demonstrations into operational networks, including buried and ducted plant, backed by a full ecosystem spanning fibre, cable, and connectivity hardware through its Optotec portfolio. Coupled with STL’s broader focus on AI-ready optical infrastructure and 5G-ready digital network solutions, the Colt trial underlines a practical migration path for carriers looking to future-proof metro and data-centre interconnect footprints against emerging AI, cloud, and 5G traffic patterns without wholesale rebuilds of underlying passive infrastructure.

“As network demand accelerates, customers are looking for more bandwidth without sacrificing security, performance, or sustainability,” said Buddy Bayer, Chief Operating Officer, Colt Technology Services. “At Colt, we continue to push optical networking forward, and this pilot represents an important step in Europe and the USA. It reflects our focus on building scalable networks that deliver growth in capacity without increasing environmental impact.”

Dr Badri Gomatam, CTO, STL, said the trial highlights the value of joint innovation in advancing optical infrastructure. “Collaborations like this speed up adoption of next-generation connectivity technologies. STL’s Multiverse MCF portfolio is designed for the high-density, ultra-low latency, and resilient connectivity requirements of AI, hyperscale cloud, and future digital platforms globally,” he said. STL stated that the trial results strengthen confidence in MCF as a viable technology for the growing bandwidth requirements driven by AI workloads, cloud scale-out, and new digital services.

“As network demand accelerates, customers are looking for more bandwidth without sacrificing security, performance, or sustainability,” said Buddy Bayer, Chief Operating Officer, Colt Technology Services. “At Colt, we continue to push optical networking forward, and this pilot represents an important step in Europe and the USA. It reflects our focus on building scalable networks that deliver growth in capacity without increasing environmental impact.”

Dr Badri Gomatam, CTO, STL, said the trial highlights the value of joint innovation in advancing optical infrastructure. “Collaborations like this speed up adoption of next-generation connectivity technologies. STL’s Multiverse MCF portfolio is designed for the high-density, ultra-low latency, and resilient connectivity requirements of AI, hyperscale cloud, and future digital platforms globally,” he said. STL stated that the trial results strengthen confidence in MCF as a viable technology for the growing bandwidth requirements driven by AI workloads, cloud scale-out, and new digital services.

………………………………………………………………………………………………………………………………………………………………….

About STL-– Sterlite Technologies Ltd:

STL is a global provider of advanced connectivity solutions, offering end-to-end products and services for building AI-ready networks across FTTx, rural broadband, enterprise, and data centres. With manufacturing operations in North America, Europe, and Asia, STL supplies connectivity solutions in more than 100 countries and works with telecom operators, cloud and data center companies, internet service providers, and large enterprises to build future-ready AI digital infrastructure.

On January 23, 2026, STL reported continued sequential improvement in Operational EBITDA margin for the fifth consecutive quarter, driven by a higher-margin product mix and increased contribution from the US market. With the US–India Bilateral Trade Agreement under advanced discussion, STL remains well-positioned to leverage emerging opportunities by offering reliable, high-quality solutions for building AI-ready digital infrastructure.

……………………………………………………………………………………………………………………………………………………

References:

https://www.intechopen.com/chapters/78908

How will fiber and equipment vendors meet the increased demand for fiber optics in 2026 due to AI data center buildouts?

Big tech spending on AI data centers and

AT&T sets 1.6 Tbps long distance speed record on its white box based fiber optic network

Dell’Oro: Optical Transport Systems market +15% year-over-year in 3Q2025 driven by Cloud Service Providers

Dell’Oro Group recently published its 3Q25 Optical Transport report, highlighting continued strength in the market as demand accelerates across customer segments and technology areas. Below is a summary of the key findings from this latest research.

The Optical Transport Systems market increased by 15% year-over-year (Y/Y) in 3Q2025, driven by robust demand across all major customer groups and technology segments. The most significant growth was seen in Cloud Service Providers (CSPs) which grew +58% Y/Y and the DWDM Long Haul segment which grew +24% Y/Y. Direct sales for data center interconnect (DCI) continued to be the driving application for optical transport equipment sales, growing 34% Y/Y. Non-DCI also performed well, rising 7% Y/Y, driven by increased spending by communication service providers (CSPs).

In the first nine months of 2025, two vendors—Ciena and Nokia—gained more than one percentage point of market share. Other vendors that gained some market share included 1Finity, Adtran, Cisco, and Smartoptics. Note that Nokia acquired Infinera -a fiber optic equipment company on February 28, 2025.

Image Source: Jimmy Yu, Dell’Oro Group

The Dell’Oro Group Optical Transport Quarterly Report offers complete, in-depth coverage of the market with tables covering manufacturers’ revenue, average selling prices, and unit shipments (by speed up to 1.6 Tbps). The report tracks DWDM long haul, WDM metro, multiservice multiplexers (SONET/SDH), data center interconnect (metro and long haul), disaggregated WDM systems, and IPoDWDM ZR/ZR+ Optics. To purchase this report, please contact us at [email protected].

…………………………………………………………………………………………………………………………………………………………………………………………

Backgrounder:

- Optical Transceivers: Convert electrical signals into optical signals for transmission over fibers, and vice versa, at the endpoints of a link.

- Wavelength Division Multiplexers (WDM/DWDM): Devices that combine multiple optical signals (each on a different wavelength) into a single fiber for transmission, and separate them at the receiving end, maximizing fiber capacity.

- Optical Add/Drop Multiplexers (OADMs): Allow specific wavelengths (channels) to be added or removed from a fiber link at intermediate points in the network without interrupting the other channels.

- Optical Cross-Connects (OXCs) / Optical Switches: Used to route optical signals from one incoming fiber to a different outgoing fiber in the optical domain, often used in core networks.

- Regenerators / Optical Amplifiers (EDFAs): Used to amplify or regenerate optical signals over long distances to maintain signal strength and quality.

- OTN Terminal Equipment / Muxponders & Transponders: These devices package client signals (like Ethernet, Fibre Channel, or even SONET/SDH signals) into the standard OTN frame format (ITU G.709) for efficient transport.

- SONET/SDH: These are legacy, connection-oriented, circuit-switched technologies originally designed for carrying voice traffic in North America (SONET) and globally (SDH). They operate at the physical layer (Layer 1) and use Time Division Multiplexing (TDM).

- Usage: They are still widely deployed in existing network infrastructure, especially where high reliability and stringent latency requirements for legacy TDM services are necessary.

- OTN: OTN (ITU-T G.709 standard) is the modern successor, designed to combine the management and protection capabilities of SONET/SDH with the bandwidth efficiency of WDM.

- Usage: OTN has largely replaced SONET/SDH in new core and metro networks due to its ability to transparently carry multiple types of traffic (Ethernet, IP, Fibre Channel, and SONET/SDH frames) over a single, high-capacity infrastructure. It offers enhanced performance monitoring, Forward Error Correction (FEC) for longer reach, and greater scalability.

- Huawei has consistently maintained a leading position in the global optical networking market.

- Ciena is a major leader, particularly in North America (holding nearly 50% share in the U.S. market) and among cloud providers, benefiting from strong demand for its WaveLogic 6e and 400ZR/ZR+ solutions.

- Nokia has significantly strengthened its position, becoming the second-largest optical networking vendor globally (with approximately 20% market share) following its acquisition of Infinera in February 2025. The combined company saw substantial growth in revenue from cloud customers.

- Cisco saw a 31% increase in revenue from cloud operators in Q2 2025, a key driver of market growth.

- ZTE and FiberHome are also among the top six, often noted for their competitive solutions in global and emerging markets.

- Excluding sales into China, the leading vendors are Ciena, Huawei, Nokia, Infinera (now part of Nokia), and Fujitsu, accounting for around 80% of that specific market segment.

References:

Optical Transport Market Surges 15% in 3Q25, According to Dell’Oro Group

Dell’Oro: Optical Transport market to hit $17B by 2027; Lumen Technologies 400G wavelength market

LightCounting: Q1 2024 Optical Network Equipment market split between telecoms (-) and hyperscalers (+)

Highlights of LightCounting’s December 2023 Quarterly Market Update on Optical Networking

Dell’Oro: Optical Transport Market Down 2% in 1st 9 Months of 2021

Dell’Oro: Optical Transport Equipment Market Stagnant in 1Q 2021; Jimmy Yu’s Take

Dell’ Oro: Huawei still top telecom equipment supplier; optical transport market +1% in 2020

AI infrastructure investments drive demand for Ciena’s products including 800G coherent optics

Artificial Intelligence (AI) infrastructure investments are starting to shift toward networks needed to support the technology, rather than focusing exclusively on computing and power, according to Ciena Chief Executive Gary Smith. The trends helped Ciena swing to a profit and post a 24% jump in sales in the recent quarter.

The company enables high-speed fiber optic connectivity for telecommunications and data centers, helping hyper-scalers such as Amazon and Microsoft support AI initiatives via data center interconnects and intra-data center networking. Currently, the company is ramping up production to meet surging demand fueled by cloud and AI investments.

“There’s no point in investing in these massive amounts of GPUs if we’re going to strand it because we didn’t invest in the network,” Smith said Thursday.

……………………………………………………………………………………………………………………………………………………..

Ciena sees a bright future in 800G coherent optics that can accommodate AI traffic. Smith said a global cloud provider has selected Ciena’s coherent 800-gig pluggable modules and Reconfigurable Line System (RLS) photonics for investing in geographically distributed, regional GPU clusters. “With our coherent optical technology ideally suited for this type of connectivity, we expect to see more of these opportunities emerge as cloud providers evolve their data center network architectures to support their AI strategies,” he added.

It’s still early innings for 800G adoption, but demand is climbing due to AI and cloud connectivity. Vertical Systems Group expects to see “a measurable increase” in 800G installations this year. Dell’Oro optical networking analyst Jimmy Yu noted on LinkedIn Ciena’s data center interconnect win is the first he’s heard of that involves connecting GPU clusters across 100+ kilometer spans. “It was a hot topic of discussion for nearly 2 years. It is now going to start,” Yu said.

……………………………………………………………………………………………………………………………………………………

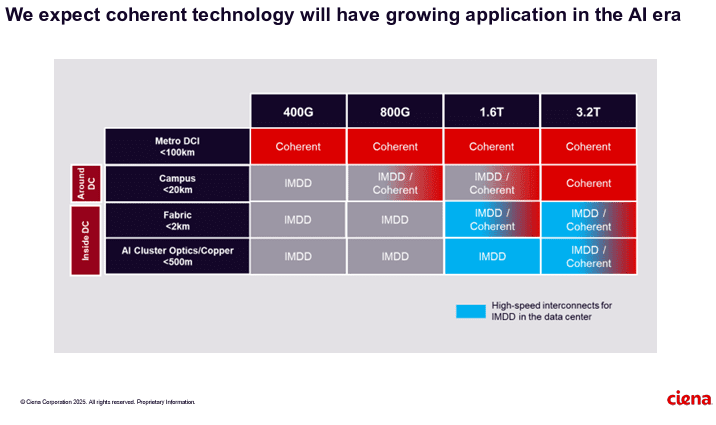

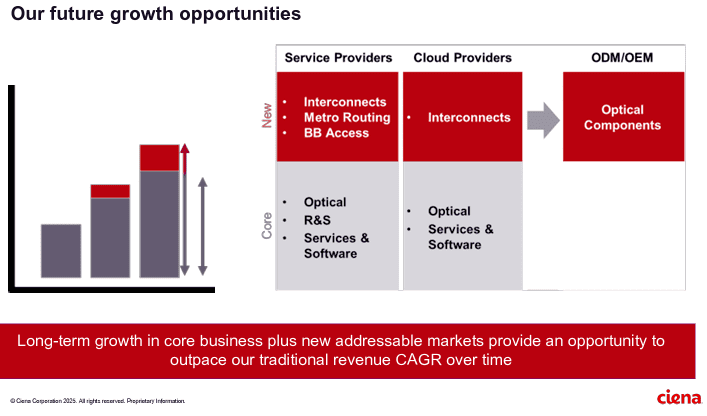

Ciena’s future growth opportunities include network service and cloud service providers as well as ODM/OEM sales of optical components.

References:

https://www.wsj.com/business/earnings/ciena-swings-to-profit-as-ai-investments-drive-demand-0195f30c

https://investor.ciena.com/static-files/d964ccac-74b3-43d9-a73e-ecf67fab6060

https://www.fierce-network.com/broadband/ciena-now-expects-tariff-costs-10m-quarter

Nokia to acquire Infinera for $2.3 billion, boosting optical network division size by 75%

Nokia has agreed to buy optical networking equipment vendor Infinera in a deal worth $2.3 billion. 70% of the sum will be paid in cash, the remaining 30% in Nokia shares. Nokia said it will accelerate its share buyback program to offset the dilution.

The acquisition will grow the size of its Optical Networks division by 75%, enabling the company to accelerate its product roadmap and increase its exposure to webscale customers, which account for around 30% of Infinera’s revenue.

![]()

Nokia and Infinera see a significant opportunity in merging to improve scale and profitability, enabling the combined business to accelerate the development of new products and solutions to benefit customers. The transaction aligns strongly with Nokia’s strategy, as it is expected to strengthen the company’s technology leadership in optical and increase exposure to webscale customers, the fastest growing segment of the market.

- Creates a highly scaled and truly global optical business with increased in-house technology capabilities and vertical integration.

- Strengthens Nokia’s optical position, specifically in North America.

- Accelerates Nokia’s customer diversification strategy, expanding webscale presence.

- Targeted net comparable operating profit synergies of EUR 200 million by 2027.

Nokia believes the transaction has compelling financial and strategic merit. The combination with Infinera is projected to accelerate Nokia’s journey to a double-digit operating margin in its Optical Networks business. Nokia targets to achieve EUR 200 million of net comparable operating profit synergies by 2027. This transaction along with the recently announced sale of Submarine Networks will create a reshaped Network Infrastructure built on three strong pillars of Fixed Networks, IP Networks and Optical Networks. Nokia targets mid-single digit organic growth for the overall Network Infrastructure business and to improve its operating margin to mid-to-high teens level.

The combined Nokia and Infinera will have a global market share of around 20%, broadly equal to Ciena (which acquired Nortel’s optical network division in November 2009 for $769 billion) but lagging behind Huawei’s 31%, according to J.P. Morgan analyst Samik Chatterjee.

“Ciena is less likely to make a competing bid given complexity in integrating competing optical portfolios as well as hurdles in regulatory approval given Ciena’s majority (51%) share of the North America market,” wrote Chatterjee in a research note.

Omdia (Informa) expects optical networking market sales to rise at a compound annual growth rate of 5% between now and 2029. A well-executed takeover may, then, give Nokia a growth story during a period of difficulty for its large mobile business group, responsible for about 44% of total sales last year.

The transaction is expected to be accretive to Nokia’s comparable EPS in the first year post close and to deliver over 10% comparable EPS accretion by 2027*, with a return on invested capital (RoIC) comfortably above Nokia’s weighted average cost of capital (WACC).

Pekka Lundmark, President and CEO of Nokia, said:

“In 2021 we increased our organic investment in Optical Networks with a view to improving our competitiveness. That decision has paid off and has delivered improved customer recognition, strong sales growth and increased profitability. We believe now is the right time to take a compelling inorganic step to further expand Nokia’s scale in optical networks. The combined businesses have a strong strategic fit given their highly complementary customer, geographic and technology profiles. With the opportunity to deliver over 10% comparable EPS accretion, we believe this will create significant value for shareholders.”

Federico Guillén, President of Network Infrastructure at Nokia, said: “Today, Network Infrastructure offers a unique portfolio across the fixed access, optical and IP networks domains built on leading technology innovation and a strong customer focus. This acquisition will further strengthen the optical pillar of our business, expand our growth opportunities across all our target customer segments and improve our operating margin. I am extremely pleased that we are bringing together these two talented and dedicated teams. Separately, we have long respected each other as competitors. Together, we find the logic of combination irresistible.”

David Heard, CEO of Infinera, said: “We are really excited about the value this combination will bring to our global customers. We believe Nokia is an excellent partner and together we will have greater scale and deeper resources to set the pace of innovation and address rapidly changing customer needs at a time when optics are more important than ever – across telecom networks, inter-data center applications, and now inside the data center. This combination will further leverage our vertically integrated optical semiconductor technologies. Furthermore, our stakeholders will have the opportunity to participate in the upside of a global leader in optical networking solutions.”

Compelling strategic benefits for Nokia, Infinera and customers:

- Improving global scale and product roadmap: The combination will increase the scale of Nokia’s Optical Networks business by 75%, enabling it to accelerate its product roadmap timeline and breadth; providing better products for customers and creating a business that can sustainably challenge the competition.

- The combined business will have significant in-house capabilities, including an expanded digital signal processor (DSP) development team, expertise across silicon photonics and indium phosphide-based semiconductor material sciences, and deeper competency in photonic integrated circuit (PIC) technology. The result will be a strong innovative player with a deep and diverse pool of optical networking talent and expertise.

- Gaining scale in North America optical market: The two companies have limited customer overlap, putting the combined business in a strong position in all regions (excluding China). Infinera has built a solid presence in the North America optical market, representing ~60% of its sales, which will improve Nokia’s optical scale in the region and complement Nokia’s strong positions in APAC, EMEA and Latin America.

- Building on Nokia’s commitment to investment in U.S. based manufacturing and advanced testing and packaging capabilities.

- Accelerating Nokia’s expansion into enterprise and particularly webscale: The combination of these two businesses is also expected to accelerate Nokia’s strategic goal of diversifying its customer base and growing in enterprise. Internet content providers (ICP or webscale as Nokia typically calls this segment) make up over 30% of Infinera’s sales. With recent wins in line systems and pluggables, Infinera is well established in this fast-growing market. Infinera has also recently been developing high-speed and low-power optical components for use in intra-data center (ICE-D) applications and which are particularly suited to AI workloads which can become a very attractive long-term growth opportunity. Overall, the acquisition offers an opportunity for a step change in Nokia’s penetration into webscale customers.

- Net comparable operating profit synergies of EUR 200 million: The combination is expected to deliver EUR 200 million of net comparable operating profit synergies by 2027*. Approximately one third of the synergies are expected to come from cost of sales due to supply chain efficiencies and the remainder from operating expenses due to portfolio optimization and integration along with reduced product engineering costs and standalone entity costs. Nokia expects one-time integration costs of approximately EUR 200 million related to the transaction.

- Creating value for shareholders: The transaction is expected to be accretive to Nokia’s comparable operating profit and EPS in year 1 and to deliver more than 10% comparable EPS accretion in 2027*. Nokia also expects the deal to deliver a return on invested capital (RoIC) comfortably above Nokia’s weighted average cost of capital (WACC). In addition, Infinera’s investors will have the opportunity to participate in the exciting upside of investing in a global leader in optical networking solutions.

Transaction details:

Under the terms of the definitive agreement, Nokia is acquiring Infinera for $6.65 per share, which equates to an enterprise value of $2.3 billion. For each Infinera share, Infinera shareholders will be able to elect to receive either: 1) $6.65 cash, 2) 1.7896 Nokia shares, or 3) a combination of $4.66 in cash and 0.5355 Nokia shares for each Infinera share. All Nokia shares will be issued in the form of American Depositary Shares. The definitive agreement includes a proration mechanism so that the Nokia shares issued in the transaction do not exceed an amount equal to approximately 30% of the aggregate consideration that may be paid to Infinera shareholders.

References:

https://www.barrons.com/articles/infinera-stock-price-buy-sell-nokia-ciena-658c7898

https://www.infinera.com/press-release/nokia-to-acquire-infinera/

LightCounting: Q1 2024 Optical Network Equipment market split between telecoms (-) and hyperscalers (+)

Infinera, DZS, and Calnex Successfully Demonstrate 5G Mobile xHaul with Open XR

Orange Deploys Infinera’s GX Series to Power AMITIE Subsea Cable

Infinera trial for Telstra InfraCo’s intercity fiber project delivered 61.3 Tbps between Melbourne and Sydney, Australia

LightCounting: Q1 2024 Optical Network Equipment market split between telecoms (-) and hyperscalers (+)

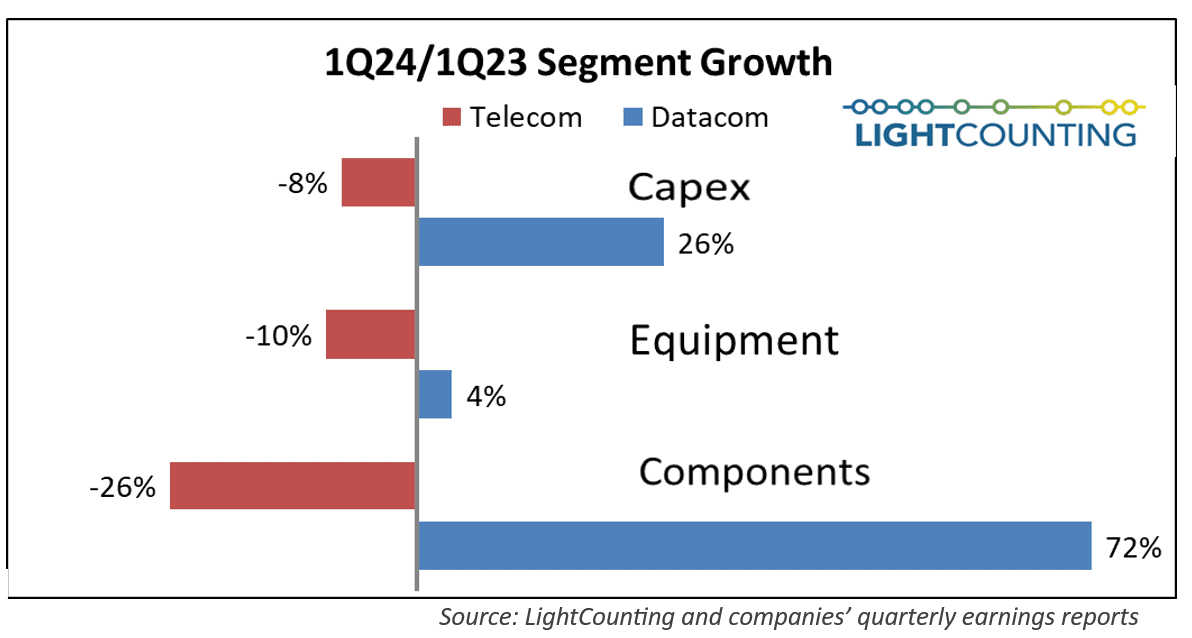

As has been the trend for the past several quarters, Q1 2024 results for the optical communications market were sharply split between very weak sales in the telecom segment (Communications Service Providers or CSPs) and continued strong demand by the hyperscalers (cloud giants). The combined capex of the Top 15 CSPs declined year-over-year for the sixth quarter in a row, while the Top 15 ICPs spending grew for the second quarter in a row, paced by Alphabet (+91%) and Microsoft (+66%). Chinese ICPs spending also increased dramatically, suggesting the AI boom is hitting China too.

Calix and Corning Weigh In: When Will Broadband Wireline Spending Increase?

Broadband wireline network operators (telcos and MSOs/cablecos) have cutback on CAPEX with decreased spending for network equipment. In its latest earnings call, Calix warned that broadband operator spending might not increase until 2025, when BEAD subsidies have been allocated. However, fiber vendor Corning and others suggested spending might increase earlier than that.

Calix specializes in providing optical network access equipment to smaller broadband service providers and has seen significant revenue growth in recent years, but near-term growth will be challenged. Calix management’s guidance was that the 2024 fiscal year will be soft for its business. Despite that softness, the company still believes that it has years of growth ahead for itself starting in 2025 due to BEAD regulatory stimulus that should prove beneficial for the enterprise.

The U.S. government’s BEAD program promises to funnel a massive $42 billion in subsidies through US states to telecom companies willing to build networks in rural areas. However, allocation of those funds is taking longer than expected, forcing network operators to stall their deployment plans until they have a better sense of how much funding they might get.

“We have seen a significant broadening in the number of customers interested in competing for BEAD [Broadband Equity Access and Deployment program] funds. Today, nearly all our customers are either assembling a BEAD strategy or actively pursuing funds,” Calix CEO Michael Weening said during the company’s quarterly earnings call, according to Seeking Alpha.

“While they do this, they slow their new [network] builds as BEAD money could be used instead of consuming their own capital, and thus, we’ll slow our appliance shipments until decisions are made and funds are awarded,” Weening said. “At that point, the winners will move ahead and those who decided to skip the BEAD program or did not receive BEAD funding, we’ll begin investing to ensure that the winner does not impinge on their market. This represents a delay but also represents a unique opportunity for Calix.”

……………………………………………………………………………………………………..

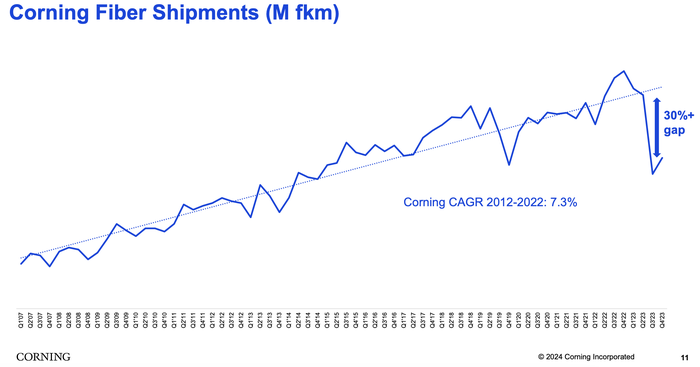

Corning manufactures and sells most of the physical fiber cabling used in U.S. fiber networks. Sales in Corning’s optical business unit – which houses its fiber products – continued to slide in the fourth quarter of 2023.

“We anticipate optical communications sales will spring back because we believe and our carrier customers have confirmed that they purchased excess inventory during the pandemic and that they’ve been utilizing this inventory to continue deploying their networks,” said Corning CEO Wendell Weeks during his company’s quarterly earnings call, according to Seeking Alpha.

“We believe these carriers will soon deplete their inventory and execute on the increased broadband deployment plans they’ve communicated to us over the last several months,” Weeks said. “As a result, we expect them to return to their normal purchasing patterns to service their deployments.”

He also noted that operators are waiting for BEAD funding. “We continue to expect BEAD funding really to start to translate into demand, the beginning of it, sort of late this year. They are progressing with awarding the grants and it will just take a bit for those to turn into real programs,” Weeks said.

Weeks suggested that the company is starting to see the glimmer of an uptick in demand from its broadband operator customers, but nothing definite yet. “We’ll know more in the coming months,” he said in his concluding remarks.

Meanwhile, executives at vendor Harmonic said this week they expect sales in the first half of this year to be relatively soft and then accelerate in the second half of the year as operators start to ramp up network upgrades, including moves to DOCSIS 4.0 technologies.

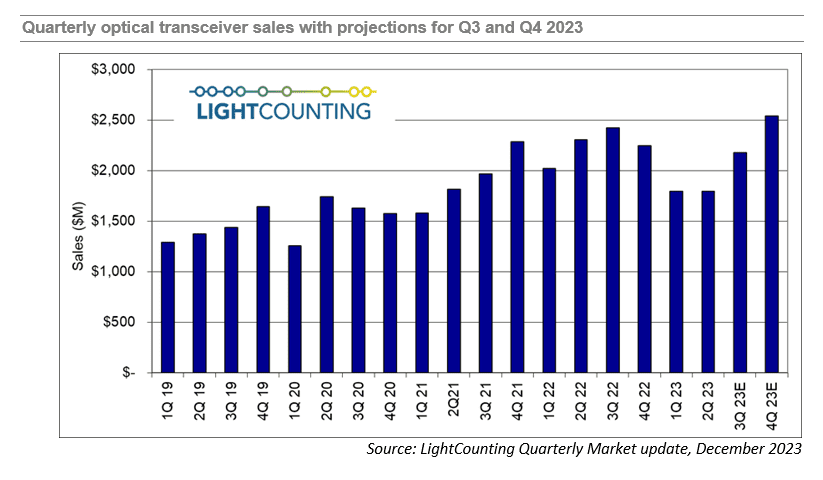

Highlights of LightCounting’s December 2023 Quarterly Market Update on Optical Networking

LightCounting’s Quarterly Market Update report [1.] for Q3 2023 revealed that the optical communications industry financial results were disappointing.

Every financial market indicator that the market research firm tracks – ICP (Integrated Communications Provider) and CSP (Communications Service Provider) capex, datacom and networking equipment, and semiconductor (x-Nvidia) and optical components sales – all had negative growth compared to Q3 2022.

Note 1. LightCounting’s Quarter Market Update reports are designed to provide an easy-to-digest snapshot of optical transceiver growth trends, backed up by detailed quarter-by-quarter sales data collected via LightCounting’s proprietary vendor survey. Performance metrics and commentary for top-tier telecom and internet service providers, network and datacom equipment makers, and optical component and semiconductor vendors are also included to provide an understanding of what drives sales trends at the transceiver level.

- Alphabet and Microsoft had record capital expenditures.

- Arista, Broadcom, Calix, Innolight, and Nvidia all reported record revenues.

LightCounting is projecting, based on its current analysis, that sales increased in Q3 and will increase further in Q4, to a new record high, as shown in the figure below. This data includes estimates for 400G and 800G transceivers manufactured by Nvidia internally.

The expectation of growth in Q4 carries over to 2024 as well and is consistent with the guidance given by several companies ranging from Alphabet and Amazon to Coherent and Lumentum. The big caveat is that growth in 2024 will be tightly focused on AI-related infrastructure, and growth in demand for those products is expected to far outstrip demand in other segments like traditional telco and enterprise networks. Most of the growth in the optical components and modules market will come from sales of 800G transceivers.

References:

https://www.lightcounting.com/report/december-2023-quarterly-market-update-199

LightCounting: Will Network Transformation resolve telecom’s paradox?

Industry Analysts: Important Optical Networking Trends for 2023

MTN Group and NEC XON deploy Africa’s first 400G optical transponder using TIP’s Phoenix

Openreach deploys Adtran’s FSP 3000 open optical transport system

Adtran today announced that Openreach, the UK’s largest wholesale broadband network, has deployed its FSP 3000 open optical transport technology to enable its new Optical Spectrum Access 100G Single enterprise service.

Openreach’s new product offers a dedicated fiber link that empowers more UK businesses to harness point-to-point 100Gbit/s data transport. The solution also brings efficiency benefits that reduce capital and operational expenditure. The latest collaboration builds on more than a decade of successful partnership between Adtran and Openreach.

“Corporate cloud applications and other data-intensive tasks such as data center backhaul are fueling a growing demand for bandwidth. Adtran’s scalable optical technology enables us to offer a managed, high-speed service that satisfies that demand at a highly competitive price point,” said Simon Williams, head of optical products at Openreach.

“With no filters or amplifiers required, our Optical Spectrum Access 100G Single service offers secure and always-on optical services that can transport enormous amounts of data. We’re also making dedicated, uncomplicated and customizable access available in a slimmed-down package that’s even easier to manage.”

Adtran’s FSP 3000 technology is helping Openreach deliver managed 100G connectivity to UK businesses. (Photo: Business Wire)

Openreach’s Optical Spectrum Access 100G Single offers a choice of point-to-point Ethernet links at 100Gbit/s or 10 separate channels at 10Gbit/s. Built on Adtran’s scalable, open FSP 3000 optical transport technology, the service empowers Openreach to meet the growing demand for data-intensive cloud-based applications. Engineered for operational simplicity, Adtran’s compact and highly efficient FSP 3000 platform offers a dedicated fiber link ensuring low latency, consistent service quality and unparalleled network reliability for Openreach’s customers.

“Our FSP 3000 technology gives Openreach a powerful optical transport solution that efficiently delivers high-bandwidth services for enterprise customers. Using the Optical Spectrum Access 100G Single service, businesses can now smoothly manage substantial data transfers, even during peak operational hours,” commented Stuart Broome, GM of EMEA sales at Adtran. “We have a great track record of partnering with Openreach to advance digital transformation across the UK. It’s a relationship based on trust and a shared dedication to deliver for customers. Together, we’re providing extra capacity and value for more businesses.”

About Adtran:

ADTRAN Holdings, Inc. (NASDAQ: ADTN and FSE: QH9) is the parent company of Adtran, Inc., a leading global provider of open, disaggregated networking and communications solutions that enable voice, data, video and internet communications across any network infrastructure. From the cloud edge to the subscriber edge, Adtran empowers communications service providers around the world to manage and scale services that connect people, places and things. Adtran solutions are used by service providers, private enterprises, government organizations and millions of individual users worldwide. ADTRAN Holdings, Inc. is also the largest shareholder of Adtran Networks SE, formerly ADVA Optical Networking SE. Find more at Adtran, LinkedIn and Twitter.

References:

BT’s CEO: Openreach Fiber Network is an “unstoppable machine” reaching 9.6M UK premises now; 25M by end of 2026

Adtran showcases coherent innovation at OFC 2023: FSP 3000 open line system & coherent 100ZR

Openreach on benefit of FTTP in UK; Full Fiber rollouts increasing

Analysts: Combined ADTRAN & ADVA will be a “niche player”