T-Mobile Earnings Beat + 5G Network Status + 600 MHz and Spectrum Position

T-Mobile US beat analysts’ estimates for quarterly revenue and profit on Thursday, as the wireless carrier added more mobile phone subscribers to its monthly plans, some of which come bundled with a Netflix Inc service.

The third-largest U.S. wireless carrier by subscribers has been awaiting a decision on its proposed merger with Sprint Corp. The two U.S. telcos delivered closing arguments in a federal court last month against a multi-state lawsuit that argues the merger will increase prices for the consumers.

T-Mobile’s fourth-quarter net income rose to $751 million from $640 million, a year earlier. Excluding items, the company earned 87 cents, beating analysts’ average estimate of 83 cents. Revenue rose to $11.88 billion from $11.45 billion, edging past analysts’ average estimate of $11.83 billion, according to IBES data from Refinitiv.

………………………………………………………………………………………………………………………………………………………………………………………

Highlights from the T-Mobile Investor Factbook website:

Strong Customer Growth:

• 1.9 million total net additions in Q4 2019 – 7.0 million in 2019 – 6th year in a row of more than 5 million total net additions

• 1.3 million branded postpaid net additions in Q4 2019, best in industry – 4.5 million in 2019, best in industry

• 1.0 million branded postpaid phone net additions in Q4 2019, best in industry – 3.1 million in 2019, best in industry

• 77,000 branded prepaid net additions in Q4 2019 – 339,000 in 2019

• Branded postpaid phone churn of 1.01% in Q4 2019, up 2 bps YoY – 0.89% in 2019, down 12 bps from 2018

First Nationwide 5G Network:

• Launched the first nationwide 5G network utilizing 600 MHz spectrum, forming the foundational 5G coverage layer for

New T-Mobile; network covers more than 200 million people and more than 5,000 cities and towns

• 4G LTE on 600 MHz now covers 248 million people and 1.5 million square miles

• Currently, more than 33 million 600 MHz compatible devices already on our network

Strong Standalone Outlook for 2020:

• Branded postpaid net additions of 2.6 to 3.6 million

• Net income is not available on a forward-looking basis(2)

• Adjusted EBITDA target of $13.7 to $14.0 billion, which includes leasing revenues of $450 to $550 million

• Cash purchases of property and equipment, including capitalized interest of approximately $400 million, are expected

to be $5.9 to $6.2 billion. Cash purchases of property and equipment, excluding capitalized interest, are expected to

be $5.5 to $5.8 billion

• In Q1 2020, pre-close merger-related costs are expected to be $200 to $300 million before taxes

• Net cash provided by operating activities, excluding payments for merger-related costs and any settlement of interest

rate swaps, is expected to be in the range of $7.9 to $8.5 billion

• Free Cash Flow, excluding payments for merger-related costs and any settlement of interest rate swaps, is expected

to be in the range of $5.4 to $5.8 billion

Total Customers:

• Total net customer additions were 1,863,000 in Q4 2019, compared to 1,747,000 in Q3 2019 and 2,402,000 in Q4 2018. This is the 27th consecutive quarter in which TMobile added more than one million total net customers.

• T-Mobile ended Q4 2019 with 86.0 million total customers, of which 67.9 million were total branded customers.

• For the full-year 2019, total net customer additions were 7,011,000 compared to 7,044,000 in 2018. This was the sixth consecutive year in which total net customer additions exceeded 5 million.

______________________________________________________________

5G NETWORK:

On December 2, 2019, T-Mobile launched America’s first nationwide 5G network, including prepaid 5G with Metro by T-Mobile, covering more than 200 million people and more than 5,000 cities and towns across over 1 million square miles with 5G. In addition, we introduced two new 600 MHz 5G capable superphones, the exclusive OnePlus 7T Pro 5G McLaren and the Samsung Galaxy Note10+ 5G and anticipate offering an industry-leading smartphone portfolio built to work on nationwide 5G in 2020. This 5G network is our foundational layer of 5G coverage on 600 MHz low-band spectrum.

Should we close our merger with Sprint, we will rapidly deploy 5G on Sprint’s 2.5 GHz spectrum, completing the “layer cake” of spectrum and providing consumers with an unmatched 5G experience. On June 28, 2019, T-Mobile introduced its 5G network using high-band millimeter wave (mmWave) spectrum in conjunction with the introduction of our first 5G handset, the Samsung Galaxy S10 5G. The 5G network on mmWave spectrum has been rolled out in parts of seven cities (New York City, Los Angeles, Dallas, Atlanta, Cleveland, Las Vegas and Miami).

600 MHz Spectrum:

- At the end of Q4 2019, T-Mobile owned a nationwide average of 31 MHz of 600 MHz low-band spectrum. In total, T-Mobile owns approximately 41 MHz of low-band spectrum (600 MHz and 700 MHz). The spectrum covers 100% of the U.S.

- As of the end of Q4 2019, T-Mobile had cleared 275 million POPs and expects to clear the remaining 600 MHz spectrum POPs in 2020.

- T-Mobile continues its deployment of LTE on 600 MHz spectrum using 5G-ready equipment. At the end of Q4 2019, we were live with 4G LTE in nearly 8,900 cities and towns in 49 states and Puerto Rico covering 1.5 million square miles and 248 million POPs.

- Combining 600 and 700 MHz spectrum, we have deployed 4G LTE in low-band spectrum to 316 million POPs.

Currently, more than 33 million devices on T-Mobile’s network are compatible with 600 MHz spectrum.

Spectrum Position:

- At the end of Q4 2019, T-Mobile owned an average of 111 MHz of spectrum nationwide, not including mmWave spectrum. The spectrum comprises an average of 31 MHz in the 600 MHz band, 10 MHz in the 700 MHz band, 29 MHz in the 1900 MHz PCS band, and 41 MHz in the AWS band. On June 3, 2019, the FCC announced the results of Auctions 101 (28 GHz spectrum) and 102 (24 GHz spectrum). In the combined auctions, T-Mobile spent $842 million to more than quadruple its nationwide average total mmWave spectrum holdings from 104 MHz to 471 MHz.

- We will evaluate future spectrum purchases in upcoming auctions and in the secondary market to further augment our current spectrum position. We are not aware of any such spectrum purchase options that come close to matching the efficiencies and synergies possible from merging with Sprint.

Network Coverage Growth:

- T-Mobile continues to expand its coverage breadth and covered 327 million people with 4G LTE at the end of Q4 2019.

- At the end of Q4 2019, T-Mobile had equipment deployed on approximately 66,000 macro cell sites and 25,000 small cell/ distributed antenna system sites.

Network Capacity Growth:

- Due to industry spectrum limitations (especially in mid-band), T-Mobile continues to make efforts to expand its capacity and increase the quality of its network through the re-farming of existing spectrum and implementation of new technologies including Voice over LTE (“VoLTE”), Carrier Aggregation, 4×4 multiple-input and multiple-output (“MIMO”), 256 Quadrature Amplitude Modulation (“QAM”) and License Assisted Access (“LAA”).

- VoLTE comprised 90% of total voice calls in Q4 2019, flat with 90% in Q3 2019 and up from 87% in Q4 2018. Carrier aggregation is live for T-Mobile customers in 969 markets, up from 956 markets in Q3 2019 and 923 in Q4 2018.

- 4×4 MIMO is currently available in 708 markets, up from 683 markets in Q3 2019 and 564 in Q4 2018.

- T-Mobile customers have 256 QAM available across the Un-carrier’s entire 4G LTE footprint.

Source: Opensignal USA Mobile Network Experience Report January 2020, based on data collection period from 9/16/2019 to 12/14/2019 - T-Mobile is the first carrier globally to have rolled out the combination of carrier aggregation, 4×4 MIMO and 256 QAM. This trifecta of standards has been rolled out to 701 markets, up from 674 markets in Q3 2019 and 549 markets in Q4 2018.

- LAA has been deployed to 30 cities including Atlanta, Austin, Chicago, Denver, Houston, Las Vegas, Los Angeles, Miami, New Orleans, New York, Philadelphia, Sacramento, San Diego, Seattle, and Washington, DC.

Network Speed:

- Based on data from Opensignal for Q4 2019, T-Mobile’s average download speed was 25.8 Mbps, AT&T at 27.5 Mbps, Verizon at 25.3 Mbps, and Sprint at 23.9 Mbps.

- Based on data from Opensignal for Q4 2019, T-Mobile’s average upload speed was 8.6 Mbps, compared to Verizon at 7.9 Mbps, AT&T at 6.0 Mbps, and Sprint at 2.7 Mbps.

…………………………………………………………………………………………………………………………………………………………………………

References:

https://investor.t-mobile.com/financial-performance/quarterly-results/default.aspx

https://www.youtube.com/watch?v=CHPuI289U-Q&feature=youtu.be

U.S. government & tech companies to create software standards for 5G telecommunications networks

The White House wants U.S. tech firms to collaborate on one or more 5G infrastructure software standard(s). The plan would build on efforts by some U.S. telecom and technology companies to agree on common engineering standards that would allow 5G software developers to run code on machines that come from nearly any hardware manufacturer.

That would reduce, if not eliminate, reliance on Huawei equipment.according to Larry Kudlow, Director of the National Economic Council. That would reduce, if not eliminate, reliance on Huawei equipment. The U.S. contends Huawei has strong links to the Chinese military, making use of its equipment a national-security risk. Huawei has denied such links and says it operates independently of the Chinese government.

“The big-picture concept is to have all of the U.S. 5G architecture and infrastructure done by American firms, principally [1],” Larry Kudlow said in an interview with the Wall Street Journal. “That also could include Nokia and Ericsson because they have big U.S. presences.”

Note 1.: That is highly unlikely to happen, because there are ZERO U.S. firms producing 5G infrastructure. The only non-Asian 5G infrastructure equipment makers are Nokia and Ericsson- both headquartered in Europe. 5G network operators AT&T and Verizon are working with Cloud Service Providers, Microsoft and Amazon, respectively on integration of mobile edge computing with their 5G networks.

……………………………………………………………………………………………………………………………………………..

AT&T, Microsoft and Dell [2] are among the companies working with the administration on the project. “Dell and Microsoft are now moving very rapidly to develop software and cloud capabilities that will, in fact, replace a lot of the equipment,” Mr. Kudlow said. “To quote Michael Dell, ‘Software is eating the hardware in 5G.’

Note 2.: None of those companies are now or will in the future make 5G infrastructure. AT&T is a network operator that purchases 5G infrastructure equipment, Microsoft is primarily a Cloud Service Provider (AZURE), while Dell is an IT infrastructure company that primarily sells to enterprise data center customers.

Kudlow is likely referring to virtualization of the 5G radio access and 5G core networks when he mentioned “software and cloud capabilities that will, in fact, replace a lot of the equipment.” Yet there’s already a lot of work that’s been done in vRAN and cloud RAN (sometimes referred to as “cloud native radio access networks.”

For open source cellular hardware, there is an OpenRAN project within the O-RAN Alliance, which involves disaggregating a cellular Base Station into its constituent components and defining interfaces between those. The Open Network Foundation (ONF) is collaborating with the O-RAN Alliance to generate open source software for that project. There are also several RAN projects within the Telecom Infrastructure Project (TIP), including OpenRAN, vRAN Fronthaul and OpenRAN 5G NR Base Station.

…………………………………………………………………………………………………………………………………………….

White House officials say they are taking the effort seriously because of the potential value of 5G technology to the broader economy. Industry boosters say the new 5G engineering standard will power an “Internet of Things” in which factories, household appliances and vehicles are connected in the way mobile phones are now. They say 5G can do for future tech startups what 4G technology did for smartphone apps like Uber Technologies Inc. and Snapchat Inc., building a foundation for future innovation.

“Talk is a good start,” said Roger Entner, an analyst for industry researcher Recon Analytics. “But in the end it needs action. More funding will accelerate everything.”

……………………………………………………………………………………………………………………………………………..

Similar U.S. government initiatives and proposals:

The effort appears to line up very closely with a new program at the U.S. military’s Defense Advanced Research Projects Agency (DARPA) called “Open Programmable Secure 5G” (OPS-5G). As noted by Data Centre Dynamics, the program promises to “create open source software and systems enabling secure 5G and subsequent mobile networks such as 6G. The signature security advantage of open source software is increased code visibility, meaning that code can be examined, analyzed and audited, either manually or with automated tools. In addition, the portability of open source serves, as a desired side-effect, to decouple the hardware and software ecosystems. This significantly raises the difficulty of a supply-chain attack and eases the introduction of innovative hardware into the market.”

U.S. lawmakers have proposed funding research and development into open 5G software standards. A bipartisan group of senators in January proposed tapping proceeds from the Federal Communications Commission’s coming spectrum license auctions to pay for research grants into those technologies. The administration is looking into those efforts but hasn’t yet decided whether to back them, Mr. Kudlow said.

If U.S. and European companies work separately, it could take longer to develop world-beating technology. If they work together, it could raise antitrust concerns. However, Kudlow said he didn’t believe antitrust would be an issue, saying the companies would compete in providing 5G technology. “We’re taking a coordinating role among leading companies,” he said.

He didn’t provide a specific time frame, though others in the government have said they expect to have a system running within 18 months. Earlier, the White House considered subsidizing a new hardware competitor to Huawei or backing a government-owned 5G network but rejected both.

President Trump is squarely behind the effort, said Kudlow, who is leading the initiative as director of the National Economic Council.

“The president kept saying to me, ‘Can’t we just put it (5G) under one simple infrastructure?’” Kudlow said. “We’re trying to create an American soup-to-nuts infrastructure for 5G. He kept hearing that Huawei seems to be able to do it.”

…………………………………………………………………………………………………………………………………………………………………………………………

Huawei’s threat to U.S. and European tech companies:

Paul Triolo, head of global technology policy at the Eurasia Group, a business consulting firm agreed that Huawei has a formidable lead in 5G technology. “The problem is you’re starting late in the game to fix this problem,” Mr. Triolo said of the U.S. effort. He added that the initiative could also threaten Nokia and Ericsson by making their machines into commodities, Mr. Triolo said.

Perhaps the most insightful proceeding on Huawei and the Chinese threat to 5G in the US is playing out at the FCC, the US government agency charged with oversight of telecom networks. That agency is considering a proposal that would bar the purchase of Huawei equipment among US companies that receive government subsidies for network buildouts in rural areas. The FCC is also evaluating its own rip-and-replace program of existing Huawei equipment in US networks.

However, unlike some of the other Trump administration efforts against Huawei, the FCC’s proceeding is being held in the open, with publicly available comments from all the companies involved in the issue.

Huawei is the world’s largest supplier of wireless networking equipment, yet it generates less than 1% of its revenue from the US market, according to research and consulting firm GlobalData.

Huawei has denied any links to Beijing, but the Chinese government is largely responsible for Huawei’s success due to the immense funding it funneled to the company and the measures it took to block competitors from impeding Huawei’s rise in the China market. As a result, Huawei became a telecom juggernaut not just in China, but all over the world. Now, the US is trying to adopt a similar strategy to promote US firms, and it wants to do so ahead of more widespread rollout of next-gen 5G networks in the coming years.

“If the US wants 5G hardware and software developed by a US or European company, the government should encourage companies to begin negotiations with Huawei to license our 5G technology,” Huawei’s US security lead Andy Purdy told the WSJ. Purdy says that Huawei’s intellectual property is integral to fast 5G deployment, and that without it, “the combined product will be one to two years behind the comparable Huawei products in terms of functionality and assurance.”

…………………………………………………………………………………………………………………………………………………………………………

References:

https://www.wsj.com/articles/u-s-pushing-effort-to-develop-5g-alternative-to-huawei-11580831592

GSA: Number of 5G devices has doubled in last 5 months!

Global mobile Suppliers Association (GSA) today reported that the number of announced 5G devices has broken the 200 barrier for the first time. With 208 5G devices now announced from 78 vendors, the number of commercial devices has more than doubled in the last five months, having surpassed the milestone of 100 devices from 41 vendors in August 2019.

“During 2019, the number of announced 5G devices grew rapidly, starting with a few announcements and then gathering pace as operators in various parts of the world launched their first commercial 5G services,” commented Joe Barrett, President, GSA.

“This growth has continued into 2020 with the number of announced 5G devices exceeding 200 for the first time. Not only is this a symbolic milestone, but it also means we are starting to be able to identify trends in spectrum support and form factors. The diversity of both further reinforces how the industry is working hard to deliver on the 5G promise to markets and operators around the globe.”

- The latest market data reveals that over two-thirds (66.8%) of all announced 5G devices are identified as supporting sub-6 GHz spectrum bands.

- Only 17 of the commercially available devices (around 29% of them) are known to support services operating in mmWave spectrum.

- Slightly more than 27% of all announced devices are known to support both mmWave and sub-6 GHz spectrum bands. The bands known to be most supported by announced 5G devices are n78, n41, n79 and n77.

Part of the GSA Analyzer for Mobile Broadband Devices (GAMBoD) database, the GSA’s 5G device tracking reports global device launches across the 5G ecosystem and contains key details about device form factors, features and support for spectrum bands. Access to the GAMBoD database is only available to GSA Members and to GSA Associates subscribing to the service.

The January 2020 5G Ecosystem Report containing summary statistics can be downloaded for free from https://gsacom.com/paper/5g-device-ecosystem-report-february-2020/?utm=devicereports5g.

By the end of January 2020, GSA had identified:

o 69 CPE devices (indoor and outdoor, including two Verizon-spec compliant devices not meeting 3GPP 5G standards) at least 12 of which are now believed to be commercially available

o 62 phones, at least 35 of which are now commercially available.

o 35 modules

o 14 hotspots (including regional variants), at least nine of which are now commercially available

o 5 laptops (notebooks)

o 4 routers

o 3 robots

o 3 televisions

o 3 tablets

o 2 snap-on dongles/adapters

o 2 drones

o 2 head-mounted displays

o 2 USB terminals/dongles

o 1 switch

o 1 vending machine

GAMBoD is a unique search and analysis tool that has been developed by GSA to enable searches of mobile broadband devices and new global data on Mobile Broadband Networks, Technologies and Spectrum (NTS). The 5G devices database contains details about device form factors, features, and support for spectrum bands. Results are presented as a list or in charts. Charts may be inserted into documents or presentations, subject to accreditation of GSA as the source.

GAMBoD is a resource dedicated to promoting the success and growth of the Mobile Broadband (MBB) industry and ecosystem and is fully available to all employees of GSA Executive and Ordinary Member companies and GSA Associates who subscribe to the service.

About GSA

GSA is the voice of the mobile vendor ecosystem representing companies engaged in the supply of infrastructure, semiconductors, test equipment, devices, applications and mobile support services. GSA actively promotes the 3GPP technology road-map – 3G, 4G, 5G – and is a single source of information resource for industry reports and market intelligence. The GSA Executive board comprises of Ericsson, Huawei, Intel, Nokia, Qualcomm, and Samsung.

GSA Membership is open to all companies participating in the mobile ecosystem and operators, companies and government bodies can get access to GAMBoD by subscribing as an Associate. More details can be found at https://gsacom.com/gsa-membership

News/updates: RSS Feed: https://gsacom.com/rss-feeds/

GSA LinkedIn group: www.linkedin.com/groups?gid=2313721

Twitter: www.twitter.com/gsacom

Vodafone tests 5G Dynamic Spectrum Sharing (DSS) in its Dusseldorf lab

Vodafone announced that it has conducted what it claims is the world’s first test of 5G Dynamic Spectrum Sharing (DSS), based on a combination of two low spectrum bands in its VIP lab in Dusseldorf, Germany. The company used simultaneously the 700MHz and 800MHz bands on a 5G non-standalone device. The frequency in the 800MHz range was used as the “anchor band”, while the 700MHz frequencies were shared between 4G and 5G.

The tests were conducted with suppliers Ericsson, Huawei and Qualcomm which used its Snapdragon X55 5G modem (which supports 5G NR mmWave and sub-6 GHz spectrum bands and can deliver speeds of up to 7 Gbps over 5G and 2.5 Gbps on Cat 22 LTE).

Vodafone claims this is a world first in cellular radio. 2G, 3G and 4G standards were initially rolled out on dedicated blocks of spectrum, which meant that re-allocating for the next generation was an extremely slow – not to mention expensive – process. With dynamic spectrum sharing, this can be done overnight with a simple software upgrade.

………………………………………………………………………………………………………………………………

DSS allows network operators to deliver both 4G and 5G within the same spectrum, enabling a smooth transition between the two technologies and therefore a more cost-effective rollout. While the technology has already been demonstrated, the unique aspect of last month’s test was the simultaneous use of two low frequency bands (700MHz and 800MHz) on a 5G non-standalone device. 800MHz was used as the “anchor band” while 700MHz was shared dynamically between 4G and 5G, allowing operators to seamlessly allocate spectrum resources according to demands on the network.

Without DSS, an operator that has 20 MHz of mid-band spectrum would have to split that spectrum in two. In other words, they would have to allocate 10 MHz of spectrum to 4G LTE and cram all their LTE users into that 10 MHz of spectrum. Then the remaining 10 MHz of AWS spectrum could be used for 5G, even though initially there will only be a minimal number of 5G users.

With DSS, an operator doesn’t have to split that mid-band spectrum or have a dedicated spectrum for either 4G LTE or 5G. Instead, they can share that 20 MHz of spectrum between the two technologies.

For operators, DSS technology means they will be able to unleash the potential of 5G quicker, both for consumers and in industry, and ensure coverage over a wider area than ever before. It will also lay the foundations for the future technologies that will rely on 5G.

How does DSS benefit for the end-user? Most importantly, it means better 5G coverage, with lower latency and higher quality (in addition to faster download speeds) for consumers sooner. DSS on low bands will also be significant in enabling low latency applications and deeper in-building coverage.

Dynamic spectrum sharing will no doubt play an integral role in ensuring a seamless global rollout of 5G and this test is a significant step towards offering this next-generation connectivity for all. Through industry collaboration such as these, we can make that leap sooner, revolutionising the lives of consumers and enabling business innovation across the globe.

References:

https://www.vodafone.com/perspectives/blog/dynamic-spectrum-sharing

Juniper Research: Network Operators to Spend Billions on AI Solutions

A new study from Juniper Research has found that total network operator spending on AI solutions will exceed $15 billion by 2024; rising from $3 billion in 2020. The research identifies network optimisation and fraud mitigation solutions as the most highly sought-after AI based services over the next 4 years. AI-based solutions automate network functionalities including routing, traffic management and predictive maintenance solutions.

For more insights, download our free whitepaper, How AI Analytics will Boost Operators’ Revenue.

Network Optimisation & Fraud Prevention Driving Adoption in Developed Markets

The new research, AI Strategies for Network Operators: Key Use Cases & Monetisation Models 2020-2024, found that operators in developed regions, such as North America and Europe, would account for over 40% of AI spend by 2024, despite only accounting for less than 20% of global subscribers. It predicts that growing demand for operational efficiencies will drive operators in these regions to increase their overall investment into AI over the next 4 years.

The research urges operators to embrace a holistic approach to AI implementation across service operations, rather than applying separate AI strategies to individual use cases. It suggests network operators leverage AI to unify internal data resources and encourage cross-functional insight sharing into network efficiencies to maximise the benefits of collaboration across internal teams.

The research predicts that AI spend by Emerging Markets operators will exceed $5 billion by 2024, rising from only $900 million in 2020. It found that this growth will be driven largely by operators exploring early use cases of AI before expanding the presence of AI in their networks to include more comprehensive services.

The report forecasts that Indian Subcontinent and Africa & Middle East will experience the highest growth in spend on AI services, with operator spend in both regions forecast to grow over 550% over the next 4 years. It anticipates that operators in these regions will initially invest in AI-based CRM (Customer Relationship Management) solutions that yield immediate benefits.

Related post:

Dell’Oro: Cable Broadband Access Equipment Revenue to Decline from $13B in 2019 to $11B in 2024

According to a newly published report by Dell’Oro Group, sales of cable broadband access equipment will decrease with a meager 2 percent CAGR from 2019 to 2024. The virtualization of network infrastructure, which is already playing out in the cable market, will extend to other equipment areas, thereby reducing traditional hardware revenue.

The cable broadband category includes both network infrastructure and consumer premises equipment.

That expected decline will be driven by multiple factors, including a saturating broadband services market in regions such as North America and Europe. Another key factor is the lack of a near-term need for many cable operators to move ahead with big access network upgrades following their recent migrations to DOCSIS 3.1, a technology that gives cablecos the ability to deliver 1-Gig services, Jeff Heynen, senior research director at Dell’Oro Group, said.

“For the North American cable operators, there isn’t a competitive incentive for them to really force upgrades at this point,” Heynen said. “Virtualization, coupled with subscriber saturation in some mature markets will result in gradually declining revenue for broadband access equipment globally,”Heynen added .

Additional highlights from the Broadband Access 5-Year Forecast Report:

- Virtual CMTS/CCAP revenue will grow from $90 Million in 2019 to $418 Million worldwide in 2024, as cable operators move to these platforms to expand broadband capacity.

- Mesh-capable routers and broadband CPE units will reach 30 Million units in 2020.

Although AT&T is pushing FTTP and having some success in upgrading some of its existing customers, that has not had much of an impact on major US cable operators such as Comcast and Charter Communication, which added 424,000 and 313,000 broadband subs, respectively, in Q4 2019.

“There has to be a driver for them to spend, and I really don’t see it,” Heynen said.

The cable industry is fast at work on DOCSIS 4.0, a next-gen specification that will support multi-gigabit speeds alongside lower latency capabilities and a higher level of network security. An even longer-term target being pursued is “10G,” a cable industry initiative that’s aiming for 10-Gig symmetrical speeds on multiple types of access networks, including hybrid fiber/coax (HFC), FTTP and even wireless.

Speaking on the company’s Q4 earnings 2019 call last week, Tom Rutledge, Charter’s chairman and CEO, made it clear that these are longer-term initiatives that include features and capabilities that can be added on an incremental basis. “There’s no immediate need to deploy a new upgrade to the marketplace today,” Rutledge said. Charter wrapped up its D3.1 network upgrade in late 2018.

That scenario also gives operators time to push ahead with related projects, including migrations to distributed access architectures and network virtualization.

Even as the move to D4.0 is still out on cable’s horizon, virtualization efforts are expected to ramp up in the next few years. Dell’Oro expects virtual cable modem termination system (CMTS) and converged cable access platform (CCAP) revenues to climb from just $90 million in 2019 to $418 million worldwide in 2024. Heynen said the 2019 total represents about 12% of the total for the CMTS/CCAP core market.

Comcast, along with some small and midsize operators in the US and Western Europe, has begun to deploy virtualized access networks. Harmonic, a lead partner for Comcast’s virtual CMTS rollout, is set to announce Q4 2019 results later today and is expected to offer an update on its vCCAP business.

The bigger broadband picture

And cable isn’t the only market feeling some pain. Dell’Oro projects that revenues for the broader access equipment market, including DSL and PON technologies, will decline from $13 billion in 2019, to $11 billion in 2024.

A big culprit there is the ongoing decline of DSL spending, Heynen said. Another contributor to the decline in hardware revenues will come as the PON market starts to virtualize the OLT (optical line terminal), he added.

Dell’Oro’s forecast currently does not include opportunities around fixed wireless. Fixed wireless will have a role in the broadband market, but “I’m still reluctant that fixed wireless will be as big as others predicted it to be,” Heynen said.

References:

Verizon CEO Hans Vestberg’s technology related remarks on 4Q2019 earnings call

Note: Copy editing was done to correct grammar errors and delete extraneous words/phrases.

- Our partnership with AWS Amazon on the 5G mobile edge compute, is a totally new way of accessing a market that we have not been into.

- We fulfilled our 5G commitment to deploy in 30 cities. We made 31. We said we’re going to launch 5G Home with the NR standard. We did that, and we said we’re going to launch the first 5G mobile edge compute. We did that in Chicago in December.

- If you think about our priorities for 2020, first of all, continue to grow on the core business. We showed this year we can continue to grow 4G and our core business, and that we’ll continue to do in 2020 as well, including building our network to be the best network in this market. Secondly is leveraging our new assets that we’re building.

- We’re building out fiber. We’re building our 5G and seeing that we can start leveraging that with our customer.

- This year, we’ll continue to have a lot of focus on our 5G build-out and we will come back to that later on how we see the 5G market when we will have an Investor Day later in February.

Verizon claims 5G leadership with 31 mobile cities, 16 NFL stadiums, 4 basketball arenas; launched 5G Edge and NR-based 5G Home

………………………………………………………………………………………………………………………………………….

- We’re very excited about the opportunities that Verizon business group has, because that’s why we started building the Verizon Intelligent Edge Network some three, four years ago in order to actually address this market in the best way, and the traction we are seeing with our customers is really good.

- So I think that our technology department have no constraints on what they need to do in 2020. This is what they have plans for in order for us to continue to fortify our 4G network, to continue with strong additions in the 5G as well as continue with our fiber build. And when it comes to the monetization of the fiber build, we’re already starting to do that.

- Many of the fibers right now are going to our cell sites on air because that was a part of it. Then, of course, it has come a little bit later in monetization for our small and medium businesses and enterprise business, etc. But clearly, we’re already now seeing the benefits of doing that. So going into 2020, I think we have a very solid capital allocation for our capex.

- Ronan Dunne (VZ CTO) already said in the beginning of the year that we’re going to have some 20 5G devices coming out in the market this year. So of course, we’re going to see more 5G devices coming out. It’s going to be more build in the markets in 2020 than we had last year. So of course, this is a year that there is going to be even more 5G things coming in. When it comes to any particular phones coming out in the market, we cannot really comment on it because that, we’ll leave to the company to do.

- If this is a market which has a high degree of iOS, that means that when a 5G phone will come out from Apple, that will be important for many consumers to look into what they think is a good change. In our case, I think we’re building a unique 5G experience with our millimeter wave that nobody else is building and have the capability to do. So I think that’s really where the difference will come.

- We already have the best 4G network as you have seen in the latest J.D. Power and RootMetrics. We’re going to continue to have that. So we’re going to give the best experience for customers. And we — and I’m confident that how we are building the network will make a big difference. And that’s why we also feel very confident if — with all these devices coming out, including if the iPhone would come out, that we will have a good chance to actually grab more customers that want to be on our network. When it comes to the spectrum and all of that, I mean, I think that I might have talked about this so many times. We have all the assets to deploy our 5G strategy when it comes to millimeter wave and using dynamic spectrum sharing, be available nationwide when our customers are ready.

- Everything from spectrum to how you densify (wireless) networks and what type of software you put in, and that’s a long-term planning how to do that right. And I think that’s something where you — or people around us go wrong when I look at us because think about how we have been performing, and many actually thought that we would never sustain an unlimited. And the more the network is growing, we’re getting more and more headroom as we’re continuing deploying our software and the engineering capabilities we have in the company.

- We think the C-band (3.7-to-4.2 GHz) is an important spectrum for many reasons. That frequency will be global. So roaming will be done on it, and that’s very important for U.S. market to get into that. And it’s very important for Verizon to get into that. But it’s not hindering our strategy right now to deploy a great 5G network and be able to capture the market for 5G.

- On the CBRS, as you know, we have already started for quite a long time ago to do trials and see how it works, and it works fine. We think it’s a good addition to the portfolio that in order to see that we get good customer expectations. So we think CBRS is an important spectrum, even though it is sort of more share than anything else, but it’s going to be definitely something we’re using as it comes out.

- Secondly, when it comes to the 5G Home, you’re confirming, actually what we have in front of us. The next-generation chipset that goes into the CP for 5G Home will come out. At least, the plan right now is in third quarter, which means that commercial product is probably coming out a little bit later because it takes some time from the chipset to the device. By then, we will have, of course, deployed far more millimeter wave across the country, so we will be able to start launching many more markets when that happens. So that will come back to a little bit more about that when have our Investor Day the 13th of February, talk a little bit more about it. But that’s in the grand scheme, the plans for 5G Home, and that’s no different from what we said half a year ago.

- When it comes to the mix and match, we want to give our (residential) customers options on top of the broadband. If it’s the fiber broadband or if it’s the 5G Home broadband, we want to give them options. Of course, one option is always to have a broadband and having over-the-top services. But another is, of course, giving the mix and match option right now to see that they use the right packages that is more fitted for them. Still, of course, it’s what they can choose whatever channels you have because they come in packages. But the early — or early indication is, of course, that customers that has been on trial for a month, they clearly see what channels they’re using and what package we can suggest for that, that is going to be more optimized. So I think for us, we just think about our customers and where the market is going, and we want to give them the option of actually having different ways they can address the market when it comes to their content consumption. And I think it’s good for our customer experience, but it’s also good for our customers because all of them can do it. So as you said, it’s a little bit early, but I think that our customers are very happy that we’re giving them this option. And I think this is what everyone see where the market is going, meaning more and more over-the-top content is coming in and you want — you need thought, mixing and matching that. And here, we have a great opportunity given our service strategy, and we can work with all the type of option in the content market as we’re not owning any content.

- We always do the trade-off between owning and leasing or sharing fiber with someone, and that is a very prudent or financially disciplined way of looking at our deployment. In many cases, we see it as owning it has really an advantage for us because of the multi-use of our network. Now we’re doing sites all the time. We’re going to create revenue for our business side. So we probably have a couple of years left on doing that. But in general, I feel good about the pace we have right now and the multi-use of the fiber we have. And I think this is one of the most critical assets in a network today — in today’s world, especially as we build Verizon Intelligent Edge Network and you want actually to start delivering the 5G experience that we’re expecting. We need this fiber to be there. So that’s basically where we are with the fiber.

- We have already gotten Dynamic Spectrum Sharing (DSS) to work from the software point of view. And the majority of our baseband is ready for taking DSS. So what we have said, I’m not going to give you an exact date, but I’m going to tell you, we’re going to be ready when we feel the market is ready and our customers need to have that coverage. And again, remember, we want to have the best network performance-wise. We don’t want to deploy it because it’s called 5G. We want to see that we actually give a superior performance to our customers. And that’s why we think that the millimeter wave, what we’re doing there is extremely important because we talked about 10 to 20x, at least more throughput and speed than we have on the 4G network, and we still have the best 4G network. So I think that’s what we already assessed. When we meet at the Investor Day, we’re going to talk a little bit more about the technology sector.

- When it comes to the 5G and where we are, I think that you saw last year that we had a strong deployment coming in during ’19, but of course, we have even higher ambitions in ’20. And we will also come back and talk a little bit about — more about that. But it goes in all three directions in our multipurpose network. It’s for the mobility case, for the home case, and it’s also for the 5G mobile edge compute case, not forgetting that, because all three of them are using our multipurpose network. And when it comes to use cases, I can do some of them.

- On the mobile edge compute, we see a lot of optimization in factories. We see private 5G networks in order to keep the data and the security and the throughput in a facility, if that’s a campus, whatever, that use case has come up very early on.

- What we can do with millimeter wave in the stadium, how we can use broadcasting cameras with 5G, a lot of new innovation, both with consumer, but also for the distribution of content. With our spectrum positioning, we basically are limited on the uplink when it comes to stadiums, which is the big blocker today in a stadium. So I think you’re going to see quite a lot next four or five days on consumer cases (at the NFL Superbowl in Miami, FL) as well as we will continue to give you more insights to it the next couple of weeks and when we meet in New York here.

- We have told you where 5G will come in, which is more of 2021. So we work with assets we have right now, but we build also a great foundation on 5G going forward for the years after.

…………………………………………………………………………………………………….

2020 Priorities for Verizon: Executing 2020 from a position of strength

1. Strengthen & Grow Core Business

• Extend our network leadership through continued innovation

• Strengthen and grow core business in Consumer, Business & Media

2. Leverage Assets to Drive New Growth

• Scale 5G / MEC / OneFiber & other assets for new growth

• Differentiate brand through trust & innovation

3. Drive Financial Discipline & Strength in Balance Sheet

• Accelerate revenue and earnings growth to drive strong cash flows

• Disciplined capital and operating spend

4. Infuse a PurposeDriven & CustomerCentric Culture

• Put customers at the center of everything we do

• Drive responsible business as part of our strategy

References:

https://www.verizon.com/about/investors/quarterly-reports/4q-2019-earnings-conference-call-webcast

U.K. Allows Huawei to Build Non Critical Parts of its 5G Network

Huawei is given permission to build noncritical parts of the network, despite U.S. security concerns:

As widely expected, the UK government today decided to allow Huawei’s network equipment to play a limited role in its national 5G networks. After a security review, the UK’s National Security Council (NSC) made the decision today following a meeting chaired by Prime Minister Boris Johnson.

British officials from senior government departments held a meeting last Wednesday and made the recommendation to allow the world’s #1 network equipment vendor to play a “limited role” in national 5G networks. Today, that recommendation was made final.

Huawei is the leading 5G global network equipment vendor, with relatively few alternative providers — such as the European firms Ericsson and Nokia — none of whom are considered to offer a like-for-like option at this stage.

UK Digital Secretary Baroness Morgan said:

“We want world-class connectivity as soon as possible but this must not be at the expense of our national security. High-risk vendors never have been and never will be in our most sensitive networks.

“The government has reviewed the supply chain for telecoms networks and concluded today it is necessary to have tight restrictions on the presence of high-risk vendors.”

Huawei has been under scrutiny over alleged ties to the Chinese government, an allegation the company has repeatedly denied. The U.S. has urged the UK to ban equipment from the Chinese vendor over national security concerns and American officials issued their British counterparts with a dossier highlighting perceived risks earlier this month.

The UK has always maintained that any decision on Huawei would be evidence-led and based on its own reviews, but the result will nonetheless anger the U.S. which has been pushing for Huawei to be totally banned from 5G networks of allies.

Huawei, and other “high-risk” vendors, will face the following restrictions:

- Excluded from all safety-related and safety-critical networks in critical national infrastructure.

- Excluded from security-critical ‘core’ functions, the sensitive part of the network.

- Excluded from sensitive geographic locations, such as nuclear sites and military bases.

- Limited to a minority presence of no more than 35 percent in the periphery of the network, known as the access network, which connects devices and equipment to mobile phone masts.

Governing that Huawei has no more than 35 percent presence in the periphery of the overall 5G network is particularly interesting. This restriction ensures that if Huawei’s equipment was later compromised, or deemed too risky, around two-thirds of the UK’s 5G network would remain unaffected.

The UK is upgrading its wireless network technology for the rollout of 5G. PHOTO: DANNY LAWSON/ZUMA PRESS ………………………………………………………………………………………………………

John Strand of Strand Consult wrote today in a note to subscribers:

- The decision relates to the use of Huawei equipment in the United Kingdom. In practice, this means that the May 2018 total ban on ZTE equipment by the UK’s National Cyber Security Centre will continue.

- Huawei are now classified as a high risk vendor following the conclusions of the Telecoms Supply Chain Review.

- The use of Huawei equipment will be prohibited in core networks. This means that the backbone of UK mobile networks must not contain Huawei equipment. This policy demonstrates that UK authorities recognize the risk of equipment made by entities affiliated with the Chinese government. If Chinese-made equipment was safe, Huawei equipment would not be prohibited from the network core.

- The use of Huawei in the radio access network (RAN) will be limited to 35 percent of the active equipment. This limits the amount that Huawei can sell in the UK. It also means that UK operators will have to prioritize network upgrades in the Western part of the country where Huawei equipment is largely deployed. In practical terms, it will not be possible for an operator to use Huawei for more than 35 percent of the equipment and then use another Chinese or Huawei-white labeled product for the rest of the network, or a portion thereof. The goal of the policy is to limit equipment from Chinese owned and/or affiliated entities, even if it is not explicitly written.

- The use of Huawei equipment will be expressly prohibited in sensitive geographical areas in the UK, areas selected for national security reasons. Indeed, this is already practiced in France where Huawei equipment in restricted in Toulouse, home of Airbus and the European aerospace industry. A similar policy exists for Brest where French nuclear submarines are located. Read more about the French decision.

Overall, the UK policy will send a strong signal to the rest of Europe and the world that the use of Chinese equipment poses a security risk and should be limited. The UK and French decisions were developed to protect industries, institutions, and assets of national importance in specific geographical areas.

The U.S. model restricts its military from using Huawei and ZTE, regardless of location. Moreover, the Federal Communications Commission prohibits the use of its subsidies for the purchase of Huawei and ZTE equipment and is considering the requirement of removal of Huawei equipment for future subsidies.

Additional US policy restricts American firms from transacting business with Huawei for sensitive technologies. US telecom operators, noting the risk, have largely opted not for Huawei or ZTE, outside of a few exceptions. This is explained in Strand Consult’s research note The pressure to restrict Huawei from telecom networks is not driven by governments, but the many companies that have experienced hacking, IP theft, or espionage.

The UK new policy is a step in the right direction, and it underscores the need for greater scrutiny of technology from firms owned and/or affiliated with the Chinese government. The security risks are real and networks are key vulnerability. Indeed, scrutiny should extend beyond the network equipment to other vulnerable products and services; systems can be compromised by devices attached to networks as well as from software running over it. See Strand Consult’s research note “The debate about network security is more complex than Huawei. Look at Lenovo laptops and servers and the many other devices connected to the internet.”

Strand Consult expects that the security standards required for public safety networks will be strengthened and translated to commercial telecom networks. It is likely that some UK operators will claim that the new policy will be unduly expensive. Strand Consult examines such claims in the report ”The real cost to rip and replace Chinese equipment from telecom networks.”

Notably 2G / 3G / 4G equipment must be replaced anyway in the move toward 5G. Huawei is not the only vendor, and alternatives are price competitive. Moreover, when it comes to 5G, network rollout policy is far more consequential than the choice of equipment vendor. The view that Huawei is necessary for 5G is a myth; indeed, the US has taken a leadership position on 5G without using Huawei equipment.

Looking at the historical facts, it is not difficult to find operators which have swapped their networks with a new supplier. This need not come as a premium for shareholders. Strand Consult reviews the financial data and case studies from the major network swap it observed in 2010 – 2016.

The UK government, with Boris Johnson at the forefront, can improve the prospects for 5G in a meaningful way. In the UK, as in many other countries, it is both difficult and expensive to build mobile infrastructure. Strand Consult’s analysis show that the terms and costs associated with obtaining permits and leasing land for mobile masts and towers is artificially expensive. In the UK, operators have for many years and with limited success tried to change the terms.

In Denmark, on the other hand, Strand Consult has helped to create transparency so that authorities get the information they need to create the needed rollout policies. As a result, the total rental costs for mobile operators have fallen by over 20 percent, and it has become significantly cheaper and easier to upgrade and build existing and new mobile infrastructure. Learn more about the project here ”How to deploy 5G: Best practices for infrastructure, regulation and business models.”

Huawei will likely claim that the UK decision doesn’t hurt its prospects. This is probably to save face. The fact is that Huawei will be subject to increased restriction and will not be able to enlarge its market share. Moreover, there is no change on the ZTE ban. The UK makes clear that Chinese equipment is not allowed in the core network. Moreover, when it comes to RAN, there are also strict limitations.

………………………………………………………………………………………………………………

In September 2018, a Canadian official argued that allowing Huawei to operate improves security. If a specific vendor’s equipment is compromised, having others in operation means less of the overall network is affected.

While Huawei will be breathing a sigh of relief at the UK’s decision – so will the country’s providers. In a statement, BT wrote:

“This decision is an important clarification for the industry. The security of our networks is an absolute priority for BT, and we already have a long-standing principle not to use Huawei in our core networks. While we have prepared for a range of scenarios, we need to further analyse the details and implications of this decision before taking a view of potential costs and impacts.”

All four of the UK’s major operators had already begun deploying 5G equipment from Huawei. Stripping Huawei’s gear and buying and installing replacements would have been costly and time-consuming.

Andrew Stark, cybersecurity director at Red Mosquito, said:

“With Huawei kit already integral to the UK 3G and 4G networks, shifting to 5G with them offers the path of least resistance and increases chances of telecom companies meeting tight roll-out targets. There are currently only two other tech players capable of providing hardware for 5G, namely Nokia and Ericsson.”

The UK says its decision was made after the NCSC “carried out a technical and security analysis that offers the most detailed assessment in the world of what is needed to protect the UK’s digital infrastructure.”

However, not all of the UK government will be so welcoming of today’s news. Conservative MP Bob Seely recently said “to all intents and purposes [Huawei] is part of the Chinese state” and involving the company would be “to allow China and its agencies access to our network.”

While UK intelligence officials clearly decided the benefits outweigh the risks, several concerns have been raised about Huawei’s equipment in recent years.

The dedicated Huawei Cyber Security Evaluation Centre (HCSEC) reported in 2018 that it could no longer offer assurance that the risks posed by the use of Huawei’s equipment could be mitigated following the “identification of shortcomings in Huawei’s engineering processes”. Concerns were raised about technical issues limiting security researchers’ ability to check internal product code and the sourcing of components from outside suppliers which are used in Huawei’s products.

A follow-up report from HCSEC in March 2019 slammed Huawei as being slow to address concerns and claimed that “no material progress has been made by Huawei in the remediation of the issues reported last year, making it inappropriate to change the level of assurance from last year or to make any comment on potential future levels of assurance.”

Just a month earlier, the Royal United Services Institute (RUSI) – the world’s oldest independent think tank on international defence and security – warned about the use of Huawei equipment: “It is far easier to place a hidden backdoor inside a system than it is to find one,

“In the likely, but unacknowledged, battle between Chinese cyber attackers and the UK’s Huawei Cyber Security Evaluation Centre, the advantage and overwhelming resources lie with the former.”

The UK’s approach to Huawei has been decided, but it doesn’t feel like the end of the debate.

………………………………………………………………………………………………………….

References:

https://www.telecomstechnews.com/news/2020/jan/28/huawei-reprieve-uk-government-permits-5g-gear/

https://techcrunch.com/2020/01/28/uk-will-allow-huawei-to-supply-5g-with-tight-restrictions/

https://www.wsj.com/articles/u-k-allows-huawei-to-build-parts-of-5g-network-11580213316

Continued Growth for South Korea’s 5G Vendors: Samsung + Many Others!

by Shim Woo-hyun of The Korea Herald (Korea)

The earnings of South Korean 5G equipment companies could regain momentum as global telecom firms seek to increase their capital expenditure on 5G network infrastructure.

The improved prospects of Samsung Electronics, the major provider of telecom equipment here, will also lead to earnings improvements of other companies, local financial reports said.

At large, 5G equipment providers here recorded significant growth so far until the third quarter last year. Their stock price had also skyrocketed until October when the global demand eased.

Radio frequency company KMW is one of the local 5G equipment firms that is expected to mark better earnings. It supplies massive multi-input and multi-output (MIMO) devices to global telecom and tech players such as Samsung, Huawei, Ericsson, ZTE and Nokia.

KMW is anticipated to mark 740 billion won ($633 million) in sales and 160 billion won operating income in 2019. In 2018, the company posted sales of 296.3 billion won, while its operating loss was 26.2 billion won.

Other local players that look forward to better performance this year include SeoJin System, OE Solutions and Ace Technologies.

- SeoJin manufactures cabinets, cases and enclosures for network equipment. The sales improvement of SeoJin is largely backed by the increase in remote radio head orders from Samsung’s 5G access unit. SeoJin’s sales in 2019 are estimated to have increased by 30 percent to reach 430 billion won, while its operating profit soared 70 percent to 63 billion won.

- Optical transceiver provider OE Solutions will also continue upward trend as it has been receiving orders from key players — Samsung, Ericsson and Huawei. The Gwangju-based firm started supplying its products to Japanese telecommunication firm KDDI last year through Samsung Electronics which has partnered with the Japanese firm to provide 5G equipment over the next five years.

- Ace Technologies, a local provider of telecom antennas, filters and massive MIMO devices, is also expected to show improved performance from its major customers — Ericsson, Samsung Electronics, KT and SK Telecom. Ace’s 2019 sales are estimated to reach 410 billion won, up 10 percent compared to 2018. Its operating profit is also expected to improve at 13 billion won, a 70 percent increase on-year.

Local financial reports said that the earnings of GaN-powered transistor manufacturer RFHIC could also rise along with the expansion of its partner Samsung Electronics. The company’s sales to Huawei, however, could remain stagnant, experts said.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………….

According to reports, the sales of the above mentioned companies last year are expected to reach 1.8 trillion, an increase of 70 percent compared to the previous year. The combined operating profit of the firms are also anticipated to reach some 300 billion won, up 500 percent from 2018.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………

This article originally appeared at: http://www.koreaherald.com/view.php?ud=20200127000188

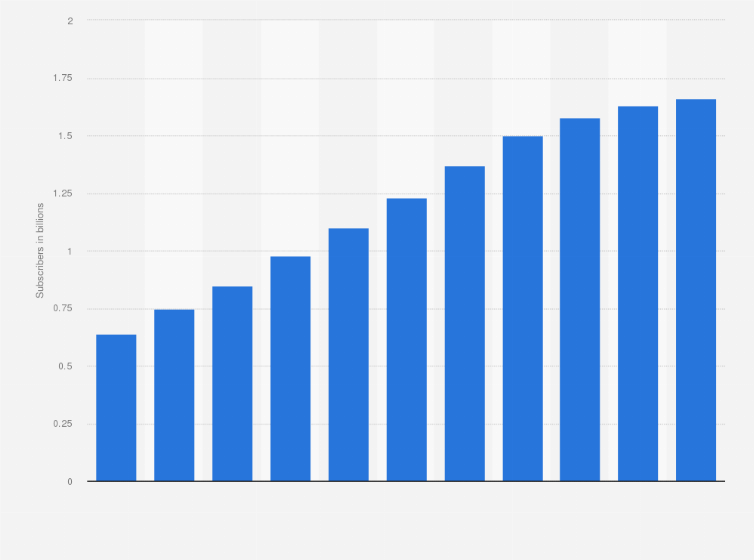

China has more than 1.6 billion mobile subscribers (> China’s entire population!)

China has a little more than 1.6 billion mobile subscribers as of year end 2019. That’s remarkable, considering China 2019 population is estimated at 1,433,783,686 people at mid year 2019 according to UN data.

- China Mobile gained more than 3.73 million new customers in December 2019, up from 2.95 new additions in November.

- China Telecom added 1.18 million new subscribers.

- China Unicom lost 2.7 million users in December.

China Mobile remains by far the largest Chinese cellular operator, with 950.2 million customers, of which 758 million are 4G users.

China Telecom, which has been growing steadily in the past year, has moved into second place with 335.57 million mobile customers, compared to 318.4 million at Unicom.

Number of mobile phone subscribers in China from 2008 to 2018 (Source: Statista.com)

………………………………………………………………………………………………………

China Mobile is also biggest in the fixed broadband market, ending 2019 with a total of 187.04 million users. However, in December 2019, it lost 609,000 fixed broadband customers, compared to a net addition of 694,000 in November and more than 1.9 million customer adds in October. China Telecom saw its fixed broadband subscriber base drop by 0.62 million in the month to 153.13 million, and Unicom lost 975,000 for a total of 83.47 million fixed broadband subscribers.

On November 1, 2019, Chinese operators China Mobile, China Unicom and China Telecom announced the rollout of 5G mobile phone services to customers. The three operators started by offering 5G plans for CNY 128 per month.

While the rollout of 4G in China took 46 months, 5G is expected to be available within ten months. China Mobile, the biggest of the three operators, already has 10 million customers interested in 5G, who are the first to access the services at launch. China Mobile earlier announced it expects to end 2019 with 5G coverage of 50 cities, and add another 340 cities in 2020, covering a population of 600-700 million people.

References:

https://www.telecompaper.com/news/china-ends-2019-with-more-than-16-billion-mobile-customers–1323638

China Internet penetration reached 61.2% in 1st half 2019; 99.1% access Internet via mobile phones!