Colo

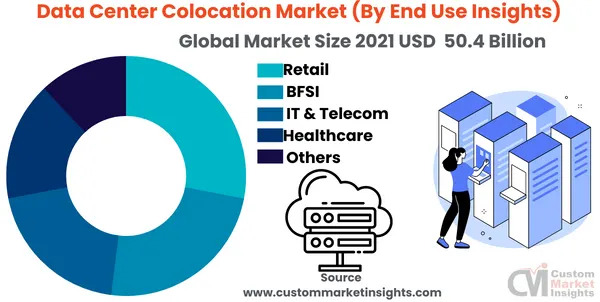

Global Data Center Colocation Market Size forecast = $131.8 Billion by 2030 at a 14.2% CAGR

According to a market research study published by Custom Market Insights, the Global Data Center Colocation Market size and share revenue was valued at approximately USD $50.4 Billion in 2021 and is expected to reach USD $57.2 billion in 2022 and is expected to reach around USD $131.8 Billion by 2030, at a CAGR of 14.2% between 2022 and 2030.

The key market players listed in the report with their sales, revenues and strategies are China Telecom Corp. Ltd., CoreSite Realty Corp., CyrusOne Inc., NaviSite, NTT Communications Corp., Cyxtera Technologies Inc., Digital Realty Trust Inc., Equinix Inc., Global Switch, Telehouse, and others.

“According to the latest research study, the demand for global Data Center Colocation Market size & share was valued at approximately USD 50.4 Billion in 2021 and is expected to reach USD 57.2 billion in 2022 and is expected to reach a value of around USD 131.8 Billion by 2030, at a compound annual growth rate (CAGR) of about 14.2% during the forecast period 2022 to 2030.”

Data center colocation market offers a comprehensive and deep evaluation of the market stature. Also, the market report estimates the market size, revenue, price, market share, market forecast, growth rate, and competitive analysis.

Data center colocation is when a service provider rents out vast amounts of floor space, internet bandwidth, and network from an existing data center to establish its own data center, store massive amounts of data, and oversee the server operations of big businesses. It enables data center colocation by sharing the existing infrastructure of data center resources.

As a result of the Covid-19 outbreak, colocation is becoming an essential component of staying connected, collaborating, and moving forward cost-effectively and safely. Healthcare organizations analyze patient outcomes using data and anticipate the spread of diseases using artificial intelligence. Robust network connectivity at Telehouse colocation centers in New York enables them to provide a range of commercial solutions.

Over the projected period, it is predicted that the fast expansion of structured and unstructured data and the rising demand for cloud computing will drive the growth of the global data center colocation market. Another factor anticipated to accelerate the development of colocation data centers is the rising capital expense associated with owning and maintaining sizable computing facilities.

A trend that is anticipated to continue during the projected period is that predictable prices, high dependability, simple scalability, and overall reduced costs are some of the primary reasons impacting colocation demand. High-capacity networks are becoming increasingly crucial as edge computing applications take off. Multi-locational hybrid data architectures have developed due to network latency challenges and the need for instantaneous real-time insights.

Data transmission between data centers or private exchange points has therefore become crucial. Additionally, as more companies move their operations to the cloud, more bandwidth is needed to support quicker data processing and smoother data transfer. The growth of immersive technologies like augmented reality, virtual reality, and artificial intelligence (AI), as well as 5G technology, has further contributed to the requirement for providing larger bandwidths for data transfer across organizations.

The continuous use of several disruptive technologies, including cloud computing, IoT, autonomous cars, and sophisticated robotics, is another factor driving the growing demand for colocation in data centers. In addition, lower latency has become increasingly in the market due to the ongoing development of these technologies and the ensuing adoption of intelligent devices. As a result, colocation gives cloud service providers a chance to relocate their data center facilities close to the consumers, resulting in high bandwidth and low latency in data transfer.

Key questions answered in this report:

- What is the size of the Data Center Colocation market and what is its expected growth rate?

- What are the primary driving factors that push the Data Center Colocation market forward?

- What are the Data Center Colocation Industry’s top companies?

- What are the different categories that the Data Center Colocation Market caters to?

- What will be the fastest-growing segment or region?

- In the value chain, what role do essential players play?

- What is the procedure for getting a free copy of the Data Center Colocation market sample report and company profiles?

Click Here to Access a Free Sample Report of the Global Data Center Colocation Market @ https://www.custommarketinsights.com/report/data-center-colocation-market/

Segmental Overview

The data center colocation market is segmented into type, enterprise size, and end-use insights. According to the class, the retail colocation category is expected to increase quickly. Numerous advantages this kind offers, including managed service, which results in cheaper costs for data center maintenance, high data security, and others, are credited with the segment’s rise.

The global market is divided into small and minimum-scale enterprises and large enterprises, depending on the enterprise size. However, large-scale organizations had the majority of the market share for data center colocation and are anticipated to keep expanding over the projected period. Heavy investment by big-size organizations in data centers is credited with this increase. Additionally, the worldwide market for data center colocation is being driven by significant enterprises’ increasing need for substantial data storage.

The market is divided into IT & Telecom, BFSI, Healthcare, and others. The IT and telecom industries had the most significant proportion in 2021, followed by the banking, financial, and insurance sectors. In the projection term, the CAGR for the IT & Telecom category is expected to be high. In addition, due to ongoing patient data monitoring and storage, which have greatly expanded since the COVID-19 pandemic in 2021, the healthcare subsegment also offers significant development potential throughout the projection period.

North America held the most significant market share in the data center colocation market. This is because several necessary cloud service providers are well-represented in the area, and SMEs also set up colocation data centers there. Additionally, rising e-commerce sales in the United States foster regional market expansion. To determine client buying habits and product requests based on several categories, such as area, gender, and age group, retailers are investing extensively in their IT infrastructure to keep customer data.

……………………………………………………………………………………………………………………………………………………..

Another forecast is even more bullish, predicting a Global Data Center Colocation market size of $202.71 Billion by 2030 as per this chart:

References:

https://www.yahoo.com/now/latest-global-data-center-colocation-023000887.html

MTN Consulting: Network operator capex forecast at $520B in 2025

Executive Summary:

Telco, webscale and carrier-neutral capex will total $520 billion by 2025 according to a report from MTN Consulting.. That’s compared with $420 billion in 2019.

- Telecom operators (telco) will account for 53% of industry Capex by 2025 vs 9% in 2019;

- Webscale operators will grow from 25% to 39%;

- Carrier-neutral [1.] providers will add 8% of total Capex in 2025 from 6% in 2019.

Note 1. A Carrier-neutral data center is a data center (or carrier hotel) which allows interconnection between multiple telecommunication carriers and/or colocation providers. It is not owned and operated by a single ISP, but instead offers a wide variety of connection options to its colocation customers.

Adequate power density, efficient use of server space, physical and digital security, and cooling system are some of the key attributes organizations look for in a colocation center. Some facilities distinguish themselves from others by offering additional benefits like smart monitoring, scalability, and additional on-site security.

……………………………………………………………………………………………………………………………………………………….

The number of telco employees will decrease from 5.1 million in 2019 to 4.5 million in 2025 as telcos deploy automation more widely and spin off parts of their network to the carrier-neutral sector.

By 2025, the webscale sector will dominate with revenues of approximately $2.51 trillion, followed by $1.88 trillion for the telco sector and $108 billion for carrier-neutral operators (CNNOs).

KEY FINDINGS from the report:

Revenue growth for telco, webscale and carrier-neutral sector will average 1, 10, and 7% through 2025

Telecom network operator (TNO, or telco) revenues are on track for a significant decline in 2020, with the industry hit by COVID-19 even as webscale operators (WNOs) experienced yet another growth surge as much of the world was forced to work and study from home. For 2020, telco, webscale, and carrier-neutral revenues are likely to reach $1.75 trillion (T), $1.63T, and $71 billion (B), amounting to YoY growth of -3.7%, +12.2%, and 5.0%, respectively. Telcos will recover and webscale will slow down, but this range of growth rates will persist for several years. By 2025, the webscale sector will dominate with revenues of approximately $2.51 trillion, followed by $1.88 trillion for the telco sector and $108 billion for carrier-neutral operators (CNNOs).

Network operator capex will grow to $520B by 2025

In 2019, telco, webscale and carrier-neutral capex totaled $420 billion, a total which is set to grow to $520 billion by 2025. The composition will change starkly though: telcos will account for 53% of industry capex by 2025, from 9% in 2019; webscale operators will grow from 25% to 39% in the same timeframe; and, carrier-neutral providers will add 8% of total capex in 2025 from their 2019 level of 6%.

By 2025, the webscale sector will employ more than the telecom industry

As telcos deploy automation more widely and cast off parts of their network to the carrier-neutral sector, their employee base should decline from 5.1 million in 2019 to 4.5 million in 2025. The cost of the average telco employee will rise significantly in the same timeframe, as they will require many of the same software and IT skills currently prevalent in the webscale workforce. For their part, webscale operators have already grown from 1.3 million staff in 2011 to 2.8 million in 2019, but continued rapid growth in the sector (especially its ecommerce arms) will spur further growth in employment to reach roughly 4.8 million by 2025. The carrier-neutral sector’s headcount will grow far more modestly, rising from 90 million in 2019 to about 119 million in 2025. Managing physical assets like towers tends to involve a far lighter human touch than managing network equipment and software.

Example of a Carrier Neutral Colo Data Center

RECOMMENDATIONS:

Telcos: embrace collaboration with the webscale sector

Telcos remain constrained at the top line and will remain in the “running to stand still” mode that has characterized their last decade. They will continue to shift towards more software-centric operations and automation of networks and customer touch points. What will become far more important is for telcos to actively collaborate with webscale operators and the carrier-neutral sector in order to operate profitable businesses. The webscale sector is now targeting the telecom sector actively as a vertical market. Successful telcos will embrace the new webscale offerings to lower their network costs, digitally transform their internal operations, and develop new services more rapidly. Using the carrier-neutral sector to minimize the money and time spent on building and operating physical assets not viewed as strategic will be another key to success through 2025.

Vendors: to survive you must improve your partnership and integration capabilities

Collaboration across the telco/webscale/carrier-neutral segments has implications for how vendors serve their customers. Some of the biggest telcos will source much of their physical infrastructure from carrier-neutral providers and lean heavily on webscale partners to manage their clouds and support new enterprise and 5G services. Yet telcos spend next to nothing on R&D, especially when compared to the 10% or more of revenues spent on R&D by their vendors and the webscale sector. Vendors who develop customized offerings for telcos in partnership with either their internal cloud divisions (e.g. Oracle, HPE, IBM) or AWS/GCP/Azure/Alibaba will have a leg up. This is not just good for growing telco business, but also for helping webscale operators pursue 5G-based opportunities. One of the earliest examples of a traditional telco vendor aligning with a cloud player for the telco market is NEC’s 2019 development of a mobile core solution for the cloud that can be operated on the AWS network; there will be many more such partnerships going forward.

All sectors: M&A is often not the answer, despite what the bankers urge

M&A will be an important part of the network infrastructure sector’s evolution over the next 5 years. However, the difficulty of successfully executing and integrating a large transaction is almost always underappreciated. There is incredible pressure from bankers to choose M&A, and the best ones are persuasive in arguing that M&A is the best way to improve your competitiveness, enter a new market, or lower your cost base. Many chief executives love to make the big announcements and take credit for bringing the parties together. But making the deal actually work in practice falls to staff way down the chain of command, and to customers’ willingness to cope with the inevitable hiccups and delays brought about by the transaction. And the bankers are long gone by then, busy spending their bonuses and working on their next deal pitch. Be extremely skeptical about M&A. Few big tech companies have a history of doing it well.

Webscale: stop abusing privacy rights and trampling on rules and norms of fair competition

The big tech companies that make up the webscale sector tracked by MTN Consulting have been rightly abused in the press recently for their disregard for consumer privacy rights, and overly aggressive, anti-competitive practices. After years of avoiding increased regulatory oversight through aggressive lobbying and careful brand management, the chickens are coming home to roost in 2021. Public concerns about abuses of privacy, facilitation of fake news, and monopolistic or (at the least) oligopolistic behavior will make it nearly impossible for these companies to stem the increased oversight likely to come soon from policymakers.

Australia’s pending law, the “News Media and Digital Platforms Bargaining Code,” could foreshadow things to come for the webscale sector, as do recent antitrust lawsuits against Facebook and Alphabet. Given that webscale companies are supposed to be fast moving and innovative, they should get out ahead of these problems. They need to implement wholesale, transparent changes to how they treat consumer privacy and commit to (and actually follow) a code of conduct that is conducive to innovation and competition. The billionaires leading the companies may even consider encouraging fairer tax codes so that some of their excessive wealth can be spread across the countries that actually fostered their growth.

ABOUT THIS REPORT:

This report presents MTN Consulting’s first annual forecast of network operator capex. The scope includes telecommunications, webscale and carrier-neutral network operators. The forecast presents revenue, capex and employee figures for each market, both historical and projected, and discusses the likely evolution of the three sectors through 2025. In the discussion of the individual sectors, some additional data series are projected and analyzed; for example, network operations opex in the telco sector. The forecast report presents a baseline, most likely case of industry growth, taking into account the significant upheaval in communication markets experienced during 2020. Based on our analysis, we project that total network operator capex will grow from $420 billion in 2020 to $520 billion in 2025, driven by substantial gains in the webscale and (much less so) carrier-neutral segments. The primary audience for the report is technology vendors, with telcos and webscale/cloud operators a secondary audience.

References:

………………………………………………………………………………………………………………………………………………….

January 8, 2021 Update:

Analysys Mason: Cloud technology will pervade the 5G mobile network, from the core to the RAN and edge

“Communications Service Providers (CSPs) spending on multi-cloud network infrastructure software, hardware and professional services will grow from USD4.3 billion in 2019 to USD32 billion by 2025, at a CAGR of 40%.”

5G and edge computing are spurring CSPs to build multi-cloud, cloud-native mobile network infrastructure

Many CSPs acknowledge the need to use cloud-native technology to transform their networks into multi-cloud platforms in order to maximise the benefits of rolling out 5G. Traditional network function virtualisation (NFV) has only partly enabled the software-isation and disaggregation of the network, and as such, limited progress has been made on cloudifying the network to date. Indeed, Analysys Mason estimates that network virtualisation reached only 6% of its total addressable market for mobile networks in 2019.

The telecoms industry is now entering a new phase of network cloudification because 5G calls for ‘true’ clouds that are defined by cloud-native technologies. This will require radical changes to the way in which networks are designed, deployed and operated, and we expect that investments will shift to support this new paradigm. The digital infrastructure used for 5G will be increasingly built as horizontal, open network platforms comprising multiple cloud domains such as mobile core cloud, vRAN cloud and network and enterprise edge clouds. As a result, we have split the spending on network cloud into spending on multiple cloud domains (Figure 1) for the first time in our new network cloud infrastructure report. We forecast that CSP spending on multi-cloud network infrastructure software, hardware and professional services will grow from USD4.3 billion in 2019 to USD32 billion by 2025, at a CAGR of 40%.

https://www.analysysmason.com/research/content/comments/network-cloud-forecast-comment-rma16/

Synergy Research: Strong demand for Colocation with Equinix, Digital Realty and NTT top providers

New data from Synergy Research Group shows that just 25 metro areas account for 65% of worldwide retail and wholesale colocation revenues. Ranked by revenue generated in Q2 2020, the top five metros are Washington, Tokyo, London, New York and Shanghai, which in aggregate account for 27% of the worldwide market. The next 20 largest metro markets account for another 38% of the market.

Those top 25 metros include eleven in North America, nine in the APAC region, four in EMEA and one in Latin America. The world’s three largest colocation providers are Equinix, Digital Realty and NTT. One of those three is the market leader in 17 of the top 25 metros. The global footprint of Equinix is particularly notable and it is the retail colocation leader in 16 of the top 25 metros. In the wholesale segment Digital Realty is leader in seven of the metros, with NTT, Global Switch and GDS each leading in at least two metros. Other colocation operators that feature heavily in the top 25 metros include 21Vianet, @Tokyo, China Telecom, China Unicom, CoreSite, CyrusOne, Cyxtera, KDDI and QTS.

Over the last twenty quarters the top 25 metro share of the worldwide retail colocation market has been relatively constant at around the 63-65% mark, despite a push to expand data center footprints and to build out more edge locations.

->That seems to indicate that edge computing hasn’t made a wider impact beyond the 25 largest colo metro areas.

Among the top 25 metros, those with the highest colocation growth rates (measured in local currencies) are Sao Paulo, Beijing, Shanghai and Seoul, all of which grew by well over 20% in the last year. Other metros with growth rates well above the worldwide average include Phoenix, Frankfurt, Mumbai and Osaka. While not in the group of highest growth metros overall, growth in wholesale revenues was particularly strong in Washington DC/Northern Virginia and London.

“We continue to see strong demand for colocation, with the standout regional growth numbers coming from APAC. Revenue growth from hyperscale operator customers remains particularly strong, demonstrating the symbiotic nature of the relationship between cloud and colocation,” said John Dinsdale, a Chief Analyst at Synergy Research Group. “The major economic hubs around the world are naturally the most important colocation markets, while hyperscale operators tend to focus their own data center operations in more remote areas with much lower real estate and operating costs. These cloud providers will continue to rely on colocation firms to help better serve major clients in key cities, ensuring the large metros will maintain their share of the colocation market over the coming years.”

About Synergy Research Group

Synergy provides quarterly market tracking and segmentation data on IT and Cloud related markets, including vendor revenues by segment and by region. Market shares and forecasts are provided via Synergy’s uniquely designed online database tool, which enables easy access to complex data sets. Synergy’s CustomView ™ takes this research capability one step further, enabling our clients to receive ongoing quantitative market research that matches their internal, executive view of the market segments they compete in.

References:

https://www.srgresearch.com/articles/top-25-metros-generate-65-worldwide-colocation-revenues

CignalAI: Cloud and Colo Optical Hardware Spending Increases by 50% in North America; Century Link’s impressive fiber buildout

by Cignal AI staff

Overview:

Cloud and colocation (colo) operator spending on optical communications hardware continued to spur market growth in the first quarter of 2019, according to the most recent Optical Customer Markets Report from research firm Cignal AI. Cloud and colo spending increased over 50% in North America, offsetting declines in other regions, with Ciena continuing to lead all sales to cloud operators.

In EMEA, traditional telco (incumbent and wholesale network operators) optical spending recovered and will grow by double digits during 2019. Spending growth by these operators is slowing in APAC as total spending reaches record highs. Huawei continues to lead this market in APAC, EMEA, and CALA, while Ciena leads in North America.

“Optical spending in North America continues to shift from traditional telco providers to the cloud and colo operators,” said Scott Wilkinson, Lead Analyst for Optical Hardware at Cignal AI. “Despite traditional telco operators accounting for most spending, the rapid growth in cloud spending combined with traditional operators now adopting cloud architectures has permanently changed supplier R&D priorities.”

The Cignal AI Optical Customer Markets Report is issued quarterly and quantifies optical equipment sales to five key customer markets: Incumbent, Wholesale, Cloud and Colo, Cable/MSO, and Enterprise and Government.

The latest report is now enhanced and includes optical equipment vendor market share for all customer markets as well as updated forecasts through 2023.

Additional findings in the 1Q19 Optical Customer Markets Report include:

- Ciena Waveserver Ai market share continues to increase as cloud & colo spending grows. New compact modular platforms targeted at this market are entering the market in 2Q19 with Cisco, Infinera, and Nokia among those expecting stronger sales in the next quarter.

- North American cable/MSO spending declined in the first quarter. However, moderate growth is still expected in 2019.

- Enterprise and Government spending shows pressure from consolidation and Cloud and Colo encroachment and isn’t expected to recover in the next two years.

About the Optical Customer Markets Report:

The Cignal AI Optical Customer Markets Report tracks optical equipment spending by end customer market type. It provides forecasts based on expected spending trends by regional basis. The report includes revenue-based market size and share for all end customer markets across all regions.

Vendors examined include Adtran, ADVA, Ciena, Cisco, ECI, Ekinops, Fiberhome, Fujitsu Networks, Huawei, Infinera, Juniper Networks, Mitsubishi Electric, MRV, NEC, Nokia, Padtec, TE Conn, Tejas Networks, Xtera and ZTE.

………………………………………………………………………………………….

About Cignal AI:

Cignal AI provides active and insightful market research for the networking component and equipment market and the market’s end customers. Our work blends expertise from a variety of disciplines to create a uniquely informed perspective on the evolution of networking communications.

To purchase the report contact: [email protected]

……………………………………………………………………………………………

July 25, 2019 Update-CignalAI comments on Cisco-Acacia:

Two weeks ago, Cisco announced it was acquiring Acacia, a move that could transform the company into a market leader in a new era of pluggable coherent optics and disaggregated networks. Cisco was already a growing customer for Acacia and was poised to be one of the leading consumers of Acacia’s AC1200 module that is now reaching the market. Between Cisco’s previous Luxtera acquisition for short-reach optical technology and its current addition of Acacia for long reach coherent, the company will have deep vertical integration.

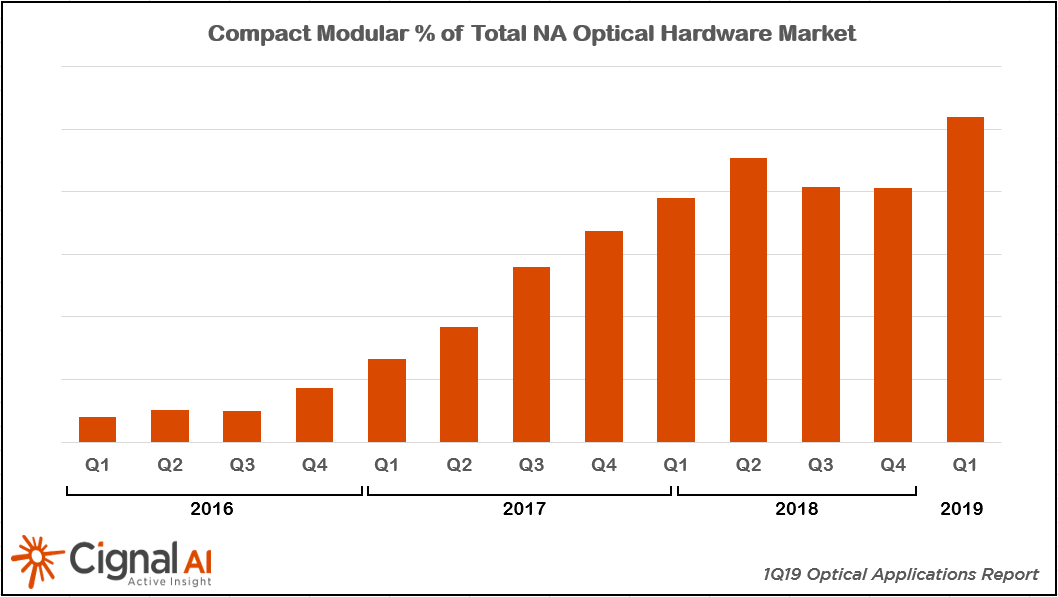

| Compact modular optical hardware is being used in more network applications than ever before, driving up sales during the first quarter of 2019 as reported in the latest Optical Applications Report. Worldwide, compact modular hardware sales are tracking to exceed $1 billion in revenue this year. |

………………………………………………………………………………………………………..

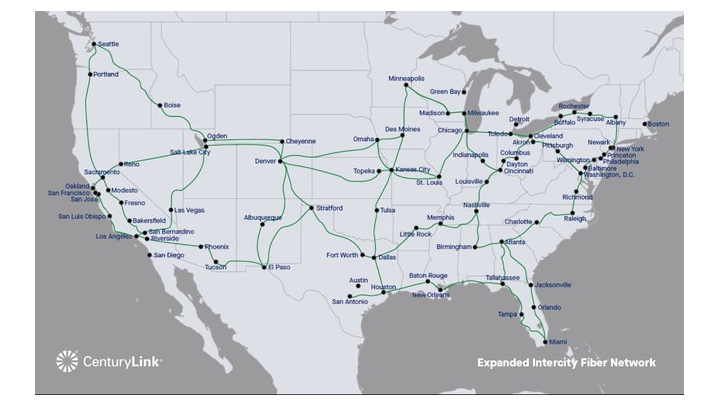

Separately, CenturyLink says it has completed the first of a two-phase build out that will see its fiber-optic networks in the U.S. and Europe grow by 4.7 million fiber miles. The new fiber infrastructure leverages ultra-low-loss fiber from Corning (NYSE: GLW) and will support businesses, government agencies, and other service providers who want access to fiber.

The first phase, completed in June, addressed CenturyLink’s U.S. requirements and connected more than 50 cities via 3.5 million new fiber miles. The European work, slated to finish in the first part of 2021, will see 1.2 million fiber miles installed. Both deployments leverage CenturyLink’s multi-conduit infrastructure, which the company says enables quick and economical fiber deploy and capacity expansion.

CenturyLink’s expanded fiber network connects more than 50 locations in the U.S. Image courtesy of Century Link

……………………………………………………………………………………………………

“Our newly built intercity fiber network, created with the latest optical technology, is another example of how our diverse fiber assets differentiate us from other network providers,” said Andrew Dugan, CenturyLink chief technology officer. “Our multi-conduit infrastructure has a significant amount of capacity for supporting the growing demand for fiber and will allow us to quickly and cost effectively deploy new fiber technology now and in the future. This uniquely positions CenturyLink to meet the needs of companies seeking highly reliable, low-latency network infrastructure designed to move massive amounts of data.”

CenturyLink was able to quickly and cost effectively complete the first phase of the project using multi-conduit infrastructure already in place. The company is currently selling routes to large enterprise companies and content providers in the U.S. and will work with customers to add additional routes as needed.

Key Facts:

- CenturyLink is creating an extensive 4.7-million fiber mile intercity fiber network across the U.S. and parts of Europe.

- The first phase, comprising 3.5 million fiber miles, was completed in June. An additional 1.2 million fiber miles will be added by early 2021.

- CenturyLink is currently selling fiber routes to large enterprise companies and content providers in the U.S.

- Multi-conduit infrastructure allows CenturyLink to quickly and economically deploy new fiber technology or add network capacity as needed.

- The investments in the first phase of the fiber upgrade are included in CenturyLink’s full year 2019 capital expenditure outlook.

- The expanded fiber network utilizes Corning’s SMF-28® ULL fiber and SMF-28® Ultra fiber, creating the largest ultra-low-loss fiber network in North America.

References:

http://news.centurylink.com/2019-07-23-CenturyLink-Expands-Fiber-Network-Across-U-S-and-Europe

Verizon Software-Defined Interconnect: Private IP network connectivity to Equinix global DC’s

Verizon today announced the launch of Software-Defined Interconnect (SDI), a solution that works with Equinix Cloud Exchange Fabric™ (ECX Fabric™), offering organizations with a Private IP network direct connectivity to 115 Equinix International Business Exchange™ (IBX ®) data centers (DC’s) around the globe within minutes.

Verizon claims its new Private IP service [1] provides a faster, more flexible alternative to traditional interconnectivity, which requires costly buildouts, long lead times, complex provisioning and often truck rolls: APIs are used to automate connections and, often, reduce costs, boasts Verizon. The telco said in a press release:

SDI addresses the longstanding challenges associated with connecting premises networks to colocation data centers. To do this over traditional infrastructure requires costly build-outs, long lead times and complex provisioning. The SDI solution leverages an automated Application Program Interface (API) to quickly and simply integrate pre-provisioned Verizon Private IP bandwidth via ECX Fabric, while eliminating the need for dedicated physical connectivity. The result is to make secure colocation and interconnection faster and easier for customers to implement, often at a significantly lower cost.

Note 1. Private IP is an MPLS-based VPN service that provides a simple network designed to grow with your business and help you consolidate your applications into a single network infrastructure. It gives you dedicated, secure connectivity that helps you adapt to changing demands, so you can deliver a better experience for customers, employees and partners.

Private IP uses Layer 3 networking to connect locations virtually rather than physically. That means you can exchange data among many different sites using Permanent Virtual Connections through a single physical port. Our MPLS-based VPN solution combines the flexibility of IP with the security and reliability of proven network technologies.

……………………………………………………………………………………………………………

“SDI is an addition to our best-in-class software-defined suite of services that can deliver performance ‘at the edge’ and support real-time interactions for our customers,” said Vickie Lonker, vice president of product management and development for Verizon. “Think about how many devices are connected to data centers, the amount of data generated, and then multiply that when 5G becomes ubiquitous. Enabling enterprises to virtually connect to Verizon’s private IP services by coupling our technology with the proven ECX Fabric makes it easy to provision and manage data-intensive network traffic in real time, lifting a key barrier to digital transformation.”

Verizon’s private IP – MPLS network is seeing high double-digit traffic growth year-over-year, and the adoption of colocation services continues to proliferate as more businesses grapple with complex cloud deployments to achieve greater efficiency, flexibility and additional functionality in data management.

“Verizon’s new Software Defined Interconnect addresses one of the leading issues for organizations by improving colocation access. This offer facilitates a reduction in network and connectivity costs for accessing colocation data centers, while promoting agility and innovation for enterprises. This represents a competitive advantage for Verizon as it applies SDN technology to improve interconnecting its Private IP MPLS network globally,” said Courtney Munroe, group vice president at IDC.

“With Software-Defined Interconnect, a key barrier to digital transformation has been lifted. By allowing enterprises to virtually connect to Verizon’s private IP services using the proven ECX Fabric, SDI makes secure colocation and interconnection easier – and more financially viable – to implement than ever before,” said Bill Long, vice president, interconnection services at Equinix [2].

Note 2. Equinix Internet Exchange™ enables networks, content providers and large enterprises to exchange internet traffic through the largest global peering solution across 52 markets.

………………………………………………………………………………………………………

Expert Opinion:

SDI is an incremental addition to Verizon’s overall strategy of interconnecting with other service providers to meet customer needs, as well as virtualizing its network, says Brian Washburn, an analyst at Ovum (owned by Informa as is LightReading and many other market research firms).

“Everything can be dynamic, everything can be made pay-as-you-go, everything can be controlled as a series of virtual resources to push them around the network as you need it, when you need it,” Washburn says.

For Equinix, the Verizon deal builds its gravitational pull. “It pulls in assets and just connects as many things to other things as possible. It is a virtuous circle. The more things they get into their data centers, the more resources they have there, that pulls in more companies to connect to the resources,” Washburn says. Equinix is standardizing its APIs to make interconnections easily.

SDI is similar to CenturyLink Dynamic Connections, which connects enterprises directly to public cloud services. And telcos are building interconnects with each other; for example, AT&T with Colt. “I expect we’ll see more of this sort of automation taking advantage of Equinix APIs,” Washburn says.

Microsoft also provides a virtual WAN service to connect enterprises to Azure. “It’s a different story, but it falls into the broader category of automation between network operators and cloud services,” Washburn said.

…………………………………………………………………………………………………………..

Verizon manages 500,000+ network, hosting, and security devices and 4,000+ networks in 150+ countries. To find out more about how Verizon’s global IP network, managed network services and Software-Defined Interconnect work please visit:

https://enterprise.verizon.com/products/network/connectivity/private-ip/

IHS Markit: Microsoft #1 for total cloud services revenue; AWS remains leader for IaaS; Multi-clouds continue to form

Following is information and insight from the IHS Markit Cloud & Colocation Services for IT Infrastructure and Applications Market Tracker.

Highlights:

· The global off-premises cloud service market is forecast to grow at a five-year compound annual growth rate (CAGR) of 16 percent, reaching $410 billion in 2023.

· We expect cloud as a service (CaaS) and platform as a service (PaaS) to be tied for the largest 2018 to 2023 CAGR of 22 percent. Infrastructure as a service (IaaS) and software as a service (SaaS) will have the second and third largest CAGRs of 14 percent and 13 percent, respectively.

IHS Markit analysis:

Microsoft in 2018 became the market share leader for total off-premises cloud service revenue with 13.8 percent share, bumping Amazon to the #2 spot with 13.2 percent; IBM was #3 with 8.8 percent revenue share. Microsoft’s success can be attributed to its comprehensive portfolio and the growth it is experiencing from its more advanced PaaS and CaaS offerings.

Although Amazon relinquished its lead in total off-premises cloud service revenue, it remains the top IaaS provider. In this very segmented market with a small number of large, well-established providers competing for market share:

• Amazon was #1 in IaaS in 2018 with 45 percent of IaaS revenue.

• Microsoft was #1 for CaaS with 22 percent of CaaS revenue and #1 in PaaS with 27 percent of PaaS revenue.

• IBM was #1 for SaaS with 17 percent of SaaS revenue.

…………………………………………………………………………………………………………………………………

“Multi-clouds [1] remain a very popular trend in the market; many enterprises are already using various services from different providers and this is continuing as more cloud service providers (CSPs) offer services that interoperate with services from their partners and their competitors,” said Devan Adams, principal analyst, IHS Markit. Expectations of increased multi-cloud adoption were displayed in our recent Cloud Service Strategies & Leadership North American Enterprise Survey – 2018, where respondents stated that in 2018 they were using 10 different CSPs for SaaS (growing to 14 by 2020) and 10 for IT infrastructure (growing to 13 by 2020).

Note 1. Multi-cloud (also multicloud or multi cloud) is the use of multiple cloud computing and storage services in a single network architecture. This refers to the distribution of cloud assets, software, applications, and more across several cloud environments.

There have recently been numerous multi-cloud related announcements highlighting its increased availability, including:

· Microsoft: Entered into a partnership with Adobe and SAP to create the Open Data Initiative, designed to provide customers with a complete view of their data across different platforms. The initiative allows customers to use several applications and platforms from the three companies including Adobe Experience Cloud and Experience Platform, Microsoft Dynamics 365 and Azure, and SAP C/4HANA and S/4HANA.

· IBM: Launched Multicloud Manager, designed to help companies manage, move, and integrate apps across several cloud environments. Multicloud Manager is run from IBM’s Cloud Private and enables customers to extend workloads from public to private clouds.

· Cisco: Introduced CloudCenter Suite, a set of software modules created to help businesses design and deploy applications on different cloud provider infrastructures. It is a Kubernetes-based multi-cloud management tool that provides workflow automation, application lifecycle management, cost optimization, governance and policy management across cloud provider data centers.

IHS Markit Cloud & Colocation Intelligence Service:

The bi-annual IHS Markit Cloud & Colocation Services Market Tracker covers worldwide and regional market size, share, five-year forecast analysis, and trends for IaaS, CaaS, PaaS, SaaS, and colocation. This tracker is a component of the IHS Markit Cloud & Colocation Intelligence Service which also includes the Cloud & Colocation Data Center Building Tracker and Cloud and Colocation Data Center CapEx Market Tracker. Cloud service providers tracked within this service include Amazon, Alibaba, Baidu, IBM, Microsoft, Salesforce, Google, Oracle, SAP, China Telecom, Deutsche Telekom Tencent, China Unicom and others. Colocation providers tracked include Equinix, Digital Realty, China Telecom, CyrusOne, NTT, Interion, China Unicom, Coresite, QTS, Switch, 21Vianet, Internap and others.

Cignal AI: Record Spending on Cloud Operator Optical Networks Drives Growth in 2018

|

|

|

Cignal AI: 2018 Cloud and Colo Spending Will Exceed $1.4 Billion

|

|

|

CignalAI: Cloud/Colo Spending Unexpectedly Drops in 1st Half 2017

by Andrew Schmitt, CignalAI

|

|

|