Edge Computing

Is the “far edge” a bridge to far to cross for AI inferencing? What about “Distributed AI Grids”?

How Far is the Far Edge?

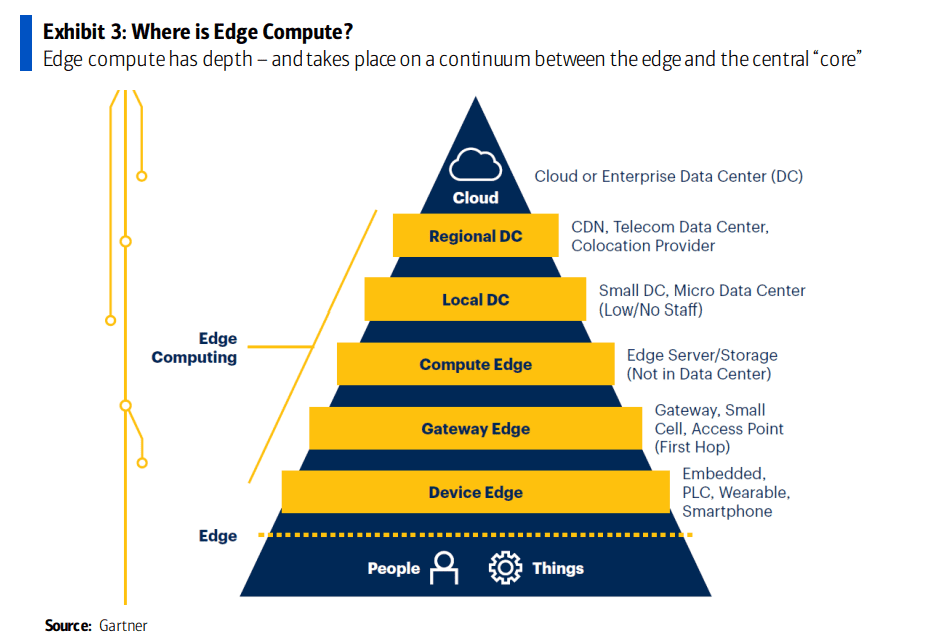

As major telcos size up distributed edge sites for a possible AI inferencing model, they’re trying to determine how far out the right place is in their networks to invest in AI computing capacity. According to Light Reading, the “far edge” is a divisive option for inferencing. According to Omdia, owned by Informa, the Far edge includes: radio access network (RAN) cell sites, aggregation hubs, exchange offices, optical line terminal (OLT) nodes, and Tier 2 metro hubs.

Many telcos are struggling to define how far is the edge from customer premises and how to serve various use cases with compute and intelligence? It seems that 5G SA core with network slicing would be mandatory to support multiple unique use cases, each with different QoS requirements.

According to Omdia’s Telco Edge Computing Survey last year, just 15% of telcos ranked network far edge as the top location for where most AI inferencing will take place, while even less (11%) said the network near edge would be the main spot (which includes central offices, headend sites and large telco data centers). The results showed AI inferencing is expected to be handled mostly on the end devices themselves and at the enterprise edge (e.g., offices, campus or manufacturing sites).

Kerem Arsal, Omdia senior principal analyst for telco enterprise and whoIe sale, predicted in a research note that this year will see telcos split into camps of “believers” and “doubters” of the far edge.

Image Credit: Sphere

…………………………………………………………………………………………………………………………………………………………………………………………………………………..

AT&T VP Yigal Elbaz, speaking at the recent New Street Research and BCG Global Connectivity Leaders Conference, expressed a cautious view on AI compute at the “far edge,” questioning how far the edge truly needs to extend to serve specific use cases effectively. He said the following (Source: Light Reading)

“The proliferation of compute and high-performing compute across the nation, in all metros is just happening, with a software layer on top of this [and] with the tools that developers need. So, I am not sure that there’s much value in extending that compute all the way to the far edge just to save another millisecond or two milliseconds of latency.”

“AT&T’s fiber and wireless networks can provide the “deterministic experience” needed between any new use cases and help them to “intelligently connect to the right model that they use, the context or the infrastructure that they need because that’s going to be heavily distributed across the US.”

“There’s no doubt that that AI is going to be embedded into wireless networks, and we’re going to call it AI-native and combine the physical space with the intelligence of the network. This is all true,” said Elbaz.

………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Distributed AI Grids:

- Ethernet with RDMA (RoCE): The foundation is built on Nvidia Spectrum-X Ethernet, which utilizes RDMA over Converged Ethernet (RoCE). This allows for direct memory access between edge GPUs (e.g., Nvidia RTX PRO 6000 Blackwell Server Edition) and the network core, bypassing CPU overhead to achieve near-line-rate performance.

- Scale-Across Networking: Using Nvidia Spectrum-XGS, the architecture extends standard RoCE to scale across geographically distributed sites. This creates a unified “AI Factory Grid” where remote edge nodes function as a single, programmable compute substrate.

- Silicon One Routing: Cisco’s Silicon One-based routing is utilized for AI-optimized traffic management, providing the high-speed, high-density throughput required for token-intensive inference workloads.

- Zero Trust & Secure Pathways: The interconnect includes a Zero Trust security layer embedded directly into the fabric. It utilizes localized traffic breakout and policy-enforced pathways to ensure that sensitive IoT and video data (such as public safety feeds) remain within the customer’s secure domain at the network edge.

- Orchestration Control Plane: A workload-aware control plane manages these protocols to intelligently route tasks based on real-time KPIs (latency, cost-per-token, and data sovereignty), ensuring that “mission-critical” inference happens at the optimal node.

- Proprietary Software Lock-in: Integrating network functions into a proprietary ecosystem (like Nvidia’s CUDA or AI Aerial) can create a “subscription trap,” where software is inseparable from specific hardware, making it nearly impossible to swap vendors without a total architectural overhaul.

- Data Fragmentation: Deploying AI across a distributed grid often leads to fragmented data sets across legacy and new multi-vendor platforms, which can result in inaccurate AI models and increased operational complexity.

- Standardization Lag: While industry bodies like the GSMA are pushing for Open Telco AI standards, the rapid deployment of proprietary AI systems often outpaces these frameworks, leading to entrenched, incompatible systems that require significantly more resources to reconcile later.

- Integration with Legacy Systems: Modern “agentic AI” and AI-native stacks often struggle to orchestrate processes across siloed legacy infrastructure, creating rigid operational environments that prevent the seamless flow of data needed for automated network troubleshooting.

Bottom Line: While the AI Grid may offer a more viable roadmap than AI-RAN, there is insufficient industry discourse regarding the strategic risks of a global, geographically distributed computing platform—as Nvidia defines it—reliant on a single-vendor hardware stack. Although Nvidia currently maintains undisputed market dominance, historical precedents such as Intel serve as a cautionary tale; long-term dominance is never guaranteed, and even market leaders face potential obsolescence. Furthermore, Nvidia’s practice of providing capital injections to entities that subsequently re-invest those funds back into Nvidia’s own ecosystem raises significant concerns regarding market sustainability and long-term financial health.

References:

https://www.lightreading.com/ai-machine-learning/at-t-cto-casts-doubt-on-ai-compute-at-the-far-edge

https://www.lightreading.com/5g/nvidia-lines-up-ai-grid-as-orange-cto-echoes-the-ai-ran-doubts

Edge AI Computing Explained: Key Concepts and Industry Use Cases

Will “AI at the Edge” transform telecom or be yet another telco monetization failure?

Analysis: Edge AI and Qualcomm’s AI Program for Innovators 2026 – APAC for startups to lead in AI innovation

Private 5G networks move to include automation, autonomous systems, edge computing & AI operations

Nvidia AI-RAN survey results; AI inferencing as a reinvention of edge computing?

Nvidia’s networking solutions give it an edge over competitive AI chip makers

Will “AI at the Edge” transform telecom or be yet another telco monetization failure?

New Telco Opportunity – AI at the Edge:

At MWC 2026 last week, there were a flurry of claims that “AI at the Edge” would transform the telecom industry. One of many examples is an article titled, “The AI edge boom is giving telecom a new strategic role.” In that piece, Jeff Aaron, vice president of product and solutions marketing at Hewlett Packard Enterprise (HPE) spoke with theCUBE’s John Furrier at MWC Barcelona, during an exclusive broadcast on theCUBE, SiliconANGLE Media’s livestreaming studio. They discussed telecom edge AI and why networking is becoming a strategic foundation for data-centric services. Aaron said:

“A big reason for [reignited interest in routing] is AI workloads. They’re moving everywhere now. They have to move to the edge. For them to move to the edge, you’ve got to get them outside of the factory and to all the locations. We’re right in the core of that, and it’s super exciting.”

As AI expands to the edge, data will need to move not only to local compute, but also between many distributed edge sites, making routing paramount. There are four ways AI infrastructure is scaling — inside data centers and across distributed edge locations, according to Aaron.

“There’s scale-out, scale-across, scale-up, and on-ramp. Two are within the data center — scale-out and scale-up — but scale-across and edge on-ramp basically mean you got to figure out how to connect to those areas, and those are just networking,” he added.

Scale-across refers to connecting distributed data centers and edge locations, while edge on-ramp brings remote sites such as factories or branch locations into the network to access AI services. Supporting those distributed environments creates an opportunity for HPE to bring networking and compute together into a more integrated infrastructure stack. At MWC 2026 Barcelona, those trends are clearly coming into focus, according to Aaron.

“Data is moving everywhere right now, and the network is back. The network isn’t just plumbing. The network is how you build a value-added service using an AI workload as a telco infrastructure,” he added.

Telecom carriers are now urgently trying to move from being “dumb data pipes” to becoming “AI performance platforms” by leveraging their geographically distributed infrastructure to host AI closer to the end user. They urgently want to pivot from selling just bandwidth and connectivity to selling outcomes and intelligence with a heavy focus on industrial and enterprise-specific edge deployments. They are considering the following services and business models:

- Infrastructure as a Service (IaaS) & GPUaaS: Offering raw computing power, specifically GPUs, from edge data centers to enterprises that need low-latency processing without building their own facilities.

- Sovereign AI Clouds: Providing AI services that guarantee data remains within national borders, appealing to government and highly regulated sectors like finance and healthcare.

- API Monetization: Exposing real-time network data (e.g., location intelligence, predictive network quality, fraud risk scoring) via APIs that enterprises pay to integrate into their own applications.

- Outcome-Based Pricing: Charging for specific business results, such as a “guaranteed video call quality” or “fraud loss reduction share,” rather than just data usage.

- AI-as-a-Service (AIaaS): Bundling pre-trained models or specialized AI agents (e.g., for customer service or industrial monitoring) with connectivity

Major Carrier AI Edge Deployment Plans:

- AT&T:

- Launched Connected AI for Manufacturing in March 2026, which unifies 5G, IoT, and generative AI to provide real-time fault detection (claiming a 70% reduction in waste).

- Deploying “Edge Zones” in major U.S. cities (Detroit, LA, Dallas) to allow developers to run low-latency, cloud-based software locally.

- Partnering with AWS to link fiber and 5G directly into AWS environments for distributed AI workloads.

- Verizon:

- Unveiled Verizon AI Connect, a suite of products designed to manage resource-intensive AI workloads for hyperscalers like Google Cloud and Meta.

- Trialing V2X (Vehicle-to-Everything) platforms to provide carmakers with standardized APIs for low-latency edge processing in autonomous driving.

- Collaborating with NVIDIA to integrate GPUs into private 5G networks for on-premise AI inferencing in robotics and AR.

- SK Telecom (SKT):

- Announced an “AI Native” strategy at MWC 2026, including a roadmap for AI-RAN (Radio Access Network) that uses GPUs to optimize network performance and host user AI apps simultaneously.

- Building a Manufacturing AI Cloud powered by over 2,000 NVIDIA RTX GPUs to support digital twin simulations and robotics.

- Expanding AI Data Centers (AIDC) across South Korea and Southeast Asia (Vietnam, Malaysia) using energy-optimized LNG-powered facilities.

- Orange & Deutsche Telekom:

- Deploying AI-powered planning tools to cut fiber rollout costs and optimize site power consumption by up to 33% using AI “Deep Sleep” modes.

- Focusing on Sovereign AI strategies to ensure data governance for European enterprise customers.

- Vodafone:

- Utilizing AI/ML applications for daily power reduction at 5G sites and testing autonomous network healing via AI agents

- BT:

- Offers 5G-connected VR for manufacturing design teams (e.g., Hyperbat) to collaborate on 3D models in real-time.

| Product Category | Primary Target | Key Value Proposition |

|---|---|---|

| AI-RAN | Industry 4.0 | Seamless, ultra-low latency for robotics and sensing. |

| Connected AI Platforms | Manufacturing | Real-time predictive maintenance and waste reduction. |

| AI-as-a-Service (AIaaS) | Developers/SMBs | Access to GPU power and pre-trained models via telco edge nodes. |

| Network Slicing APIs | App Developers | Programmatic control over bandwidth for AR/VR and gaming. |

…………………………………………………………………………………………………………………………………………………………………………………………..

A Dissenting View of “AI at the Edge”:

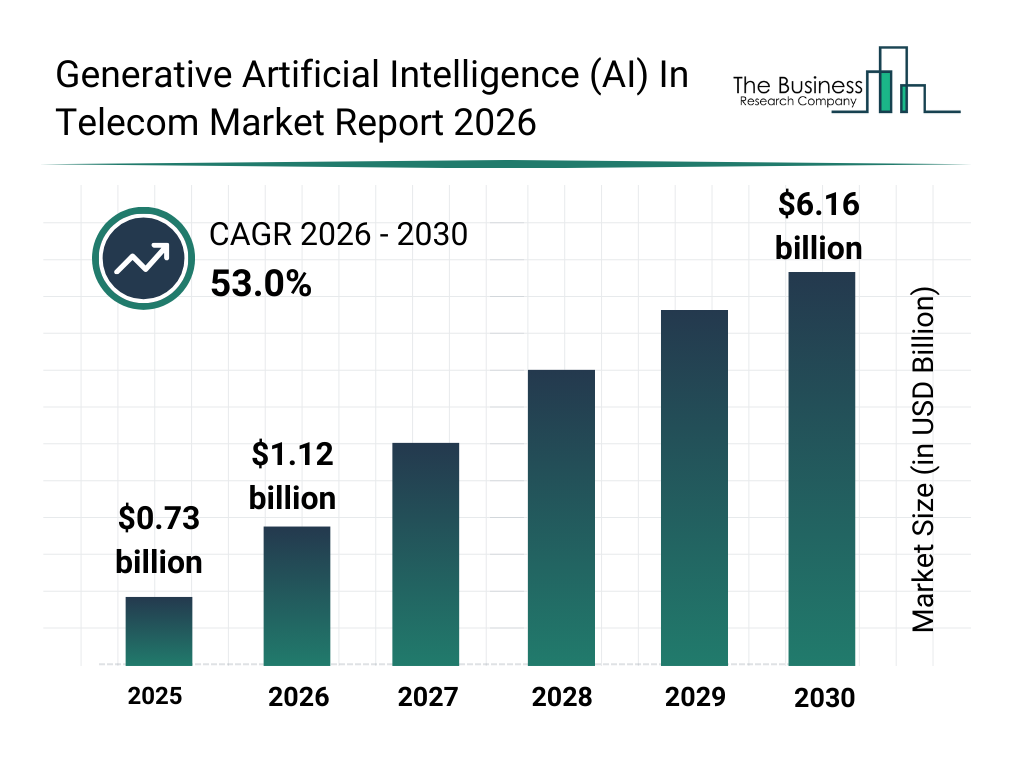

The global market for AI within the global telecommunications sector is valued at $6.69 billion in 2026, growing at a compound annual rate (CAGR) of 41.9% from 2025. The broader edge AI market—including hardware, software, and services—is forecast to reach $29.98 billion in 2026, according to The Business Research Company. We think those estimates are way too high.

The market research firm states:

………………………………………………………………………………………………………

Author’s Opinion:

Unless telcos change their corporate culture along with slowing the footprint growth of cloud service providers/hyperscalers, we think that AI at the Edge will be yet another telco monetization failure. Just like their failure to monetize: 4G LTE apps, the telco cloud, 5G, multi-access edge computing (MEC), OpenRAN, LPWANs and other telecom technologies that never lived up to their promise and potential.

That’s largely because telcos are very weak: developing IT platforms, compute services, killer applications, and rapid execution of new services (e.g. 5G services require a 5G SA core network which telcos were very slow to deploy). Telecom execs themselves cite cultural and speed‑of‑change issues: the industry is not organized like a software company, so it struggles to iterate products at AI/cloud pace. Also, telcos historically struggle with software. Managing distributed GPU clusters is vastly different from managing cell towers.

After spending billions on 5G with very little or no ROI, investors are skeptical of the increased capex required for AI-grade edge servers which must be maintained by telcos. Those servers will be expensive (especially if they contain clusters of Nvidia GPUs) and consume a lot of power, which is a critical issue at the edge of the carrier’s network.

Many network operators frame AI/edge as “network optimization” or “utilizing underused sites,” not as building monetizable AI platforms with APIs, SDKs, and ecosystems. This mirrors 5G, where huge RAN/core builds were not matched by a clear product and platform strategy, leaving value to OTTs and hyperscalers which are extending their control planes and protocol stacks to the network edge (local zones, operator co‑lo, on‑premises stacks).

Telcos risk becoming “dumb pipes” for AI traffic if they can’t provide a superior developer ecosystem. If they only sell space/power/connectivity, the cloud service providers will continue to own the developer and AI value chain. Analysts warn that edge is a “right to participate, not a right to win.” As such, value accrues to whoever owns the AI platform, tools, marketplace, and pricing power, not the entity that provides connectivity, PoP or cell towers.

Data fragmentation and weak “intelligence” layer:

-

AI monetization depends on high‑quality, cross‑domain data, but telco data is fragmented across OSS, BSS, probes, and partner systems; without unification, it is hard to expose compelling network/edge intelligence services.

-

Analysts emphasize that failure here reduces telcos to generic GPU landlords, while higher‑margin offers (real‑time quality, fraud, identity, mobility/context APIs) remain unrealized.

Narrow internal focus on cost savings:

-

Many operators’ early AI focus is inward (Opex reduction in assurance, planning, customer care) rather than building external, revenue‑generating products, echoing how early 5G was justified mainly on cost/efficiency.

-

Commentators warn that if AI/edge remains a “network efficiency” play, the commercial upside will go to cloud/AI natives that turn similar capabilities into products sold to enterprises.

What analysts say telcos must do differently:

-

Build “Sovereign AI factories” and edge AI clouds: GPU‑enabled sites with cloud‑like developer experience (APIs, self‑service portals, metering, SLAs) and clear sovereign/regional guarantees.

-

Combine differentiated connectivity with AI services (latency‑backed SLAs, AI‑on‑RAN, domain‑specific models for verticals) and use modern, flexible commercial models instead of just selling bandwidth or colocation.

Conclusions:

In summary, the main risk for telcos is to successfully transition from owning and maintaining network infrastructure to owning and operating AI platforms and products at software industry speed. AI at the edge is less of a new service or product and more an architectural upgrade. The two ways telcos can benefit are from:

- Internal cost reduction: If telcos use it to lower their own costs (fraud prevention, risk management, predictive maintenance, fault isolation, self-healing networks, etc.), it’s an automatic win but won’t increase the top line.

- Revenue from new AI -Edge services, e.g. Verizon uses edge-based video analytics in warehouses to improve inventory turnover by up to 40%. If they expect to charge a massive premium for “AI-enabled 5G,” they face the same monetization wall that has doomed them for the past 20 years!

References:

https://siliconangle.com/2026/03/04/telecom-edge-ai-makes-networking-strategic-mwc26/

https://www.nvidia.com/en-us/lp/ai/the-blueprint-for-ai-success-ebook/

AT&T and AWS to deliver last mile connectivity for AI workloads; AT&T Geo Modeler™ AI simulation tool

Analysis: Edge AI and Qualcomm’s AI Program for Innovators 2026 – APAC for startups to lead in AI innovation

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Private 5G networks move to include automation, autonomous systems, edge computing & AI operations

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

Nvidia AI-RAN survey results; AI inferencing as a reinvention of edge computing?

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

CES 2025: Intel announces edge compute processors with AI inferencing capabilities

T-Mobile and Google Cloud collaborate on 5G and edge compute

T-Mobile and Google Cloud announced today they are working together to combine the power of 5G and edge compute, giving enterprises more ways to embrace digital transformation. T-Mobile will connect the 5G Advanced Network Solutions (ANS) [1.] suite of public, private and hybrid 5G networks with Google Distributed Cloud Edge (GDC Edge) to help customers embrace next-generation 5G applications and use cases — like AR/VR experiences.

Note 1. 5G ANS is an end-to-end portfolio of deployable 5G solutions, comprised of 5G Connectivity, Edge Computing, and Industry Solutions – along with a partnership that simplifies creating, deploying and managing unique solutions to unique problems.

More companies are turning to edge computing as they focus on digital transformation. In fact, the global edge compute market size is expected to grow by 37.9% to $155.9 billion in 2030. And the combination of edge computing with the low latency, high speeds, and reliability of 5G will be key to promising use cases in industries like retail, manufacturing, logistics, and smart cities. GDC Edge customers across industries will be able to leverage T-Mobile’s 5G ANS easily to get the low latency, high speeds, and reliability they will need for any use case that requires data-intensive computing processes such as AR or computer vision.

For example, manufacturing companies could use computer vision technology to improve safety by monitoring equipment and automatically notifying support personnel if there are issues. And municipalities could leverage augmented reality to keep workers at a safe distance from dangerous situations by using machines to remotely perform hazardous tasks.

To demonstrate the promise of 5G ANS and GDC Edge in a retail setting, T-Mobile created a proof of concept at T-Mobile’s Tech Experience 5G Hub called the “magic mirror” with the support of Google Cloud. This interactive display leverages cloud-based processing and image rendering at the edge to make retail products “magically” come to life. Users simply hold a product in front of the mirror to make interactive videos or product details — such as ingredients or instructions — appear onscreen in near real-time.

“We’ve built the largest and fastest 5G network in the country. This partnership brings together the powerful combination of 5G and edge computing to unlock the expansion of technologies such as AR and VR from limited applications to large-scale adoption,” said Mishka Dehghan, Senior Vice President, Strategy, Product, and Solutions Engineering, T-Mobile Business Group. “From providing a shopping experience in a virtual reality environment to improving safety through connected sensors or computer vision technologies, T-Mobile’s 5G ANS combined with Google Cloud’s innovative edge compute technology can bring the connected world to businesses across the country.”

“Google Cloud is committed to helping telecommunication companies accelerate their growth, competitiveness, and digital journeys,” said Amol Phadke, General Manager, Global Telecom Industry, Google Cloud. “Google Distributed Cloud Edge and T-Mobile’s 5G ANS will help businesses deliver more value to their customers by unlocking new capabilities through 5G and edge technologies.”

T-Mobile is also working with Microsoft Azure, Amazon Web Services and Ericsson on advanced 5G solutions.

References:

https://www.t-mobile.com/news/business/t-mobile-and-google-cloud-join-5g-advanced-network-solutions

https://www.t-mobile.com/business/solutions/networking/5G-advanced-solutions

AWS enabling edge computing, supports mobile & IoT devices, 5G core network and new services

In an AWS re-Invent Leadership session titled “AWS Wherever You Need It,” [1.] Wayne Duso, vice president of engineering and product at AWS, expressed similar goals. “Today, customers want to use AWS services in a growing range of applications, operating wherever they want, whenever they require. And they’re striving to do so to deliver the best possible customer experience they can, regardless of where their customers or users happen to be located. One way AWS helps customers accomplish this is by bringing the AWS value to our regions, to metro areas, to on-premises, and to the furthest and evolving edge.”

Note 1. You can watch the 1 hour “AWS Wherever You Need It” session here (top right).

“We’re helping customers by providing the same experience from cloud to on-prem to the evolving edge, regardless of where your application may need to reside,” Duso explained. “AWS is enabling customers to use the same infrastructure, services and tools to accomplish that. And we do that by providing a continuum of consistent cloud-scale services that allow you to operate seamlessly across this range of environments.”

Duso explained how AWS is enabling edge computing by adding capabilities for mobile and IoT devices. “There are more than 14 billion smart devices in the world today. And it’s often in things we think about, like wristwatches, cameras, cellphones and speakers,” he said.

“But more often, it’s the stuff that you don’t see every day powering industries of all types and for all types of customers.” Duso cited the example of Hilcorp, a leading energy producer, which is using smart devices to monitor the health of its wells, optimize production and proactively predict failures so it can minimize capital expenditures.

With IoT devices becoming common among energy providers, edge computing is on the rise to handle the volume of data these devices generate. “Now, AWS IoT provides a deep and broad set of services and partner solutions to make it really simple to build secure, managed and scalable IoT applications,” Duso added.

Duso pointed to Couchbase as a use case for flexible AWS services: “Couchbase is a non-SQL database company that uses AWS hybrid edge services such as Local Zones, Wavelength, Outposts and the Snow Family to deploy its applications and highly scalable, reliable and performant environments to reduce latency by over 18 percent for its customers.” Each of these AWS managed services enables Couchbase to move data from the edge to the cloud or manage and process it where it’s generated.

“What we built on these AWS compute environments was a highly distributed, managed or self-managed database,” Duso explained. “For the cloud, an internet gateway for accessing that data securely over the web and synchronizing that data down to the edge. And that works across cloud, edge and on the offline, first-compute environments.”

“Our goal is I want to make AWS the best place to run 5G networks. That is the overarching objective. How can I make AWS, whether we are running it in the region, in a Local Zone, on an Outposts, on a Snow device, how do we make it the best place to run a 5G network, and then provide that infrastructure.”

AWS’ 5G network efforts include a cloud architecture that can support an operator’s 5G SA core network and applications, similar to what AWS is doing with greenfield U.S. wireless network operator Dish Network. Sidd Chenumolu, VP of technology development and network services at Dish Network, recently explained that the wireless carrier’s 5G core network was using three of AWS’ four public regions, was deployed in “multiple availability zones and almost all the Local Zones, but most were deployed with Nokia applications across AWS around the country.”

AWS is also working with Verizon to support a part of that carrier’s public MEC system. This includes use of AWS’ Outposts and Wavelengths, the latter of which AWS recently expanded in the United Kingdom with Vodafone.

Hofmeyr continued, “I think you have a spectrum (of different wireless carrier networks), from the total greenfields like what we did with Dish to the large tier-ones. The one thing that’s common across the board is the desire to modernize and become more cloud-like. That is common. Everyone wants that. Each one has a very unique job. There’s not one way that they all are executing in the same way. They’re taking this one workload and then building, so all of them are focusing on different workloads in the network and put it in the cloud.”

In conclusion Hofmeyr said, “I think all over the edge we find these use cases for which purpose-built systems were designed to handle that. And our goal is how do you make that available in the cloud.”

References:

https://reinvent.awsevents.com/leadership-sessions/

https://reinvent.awsevents.com/on-demand/?trk=www.google.com#leadership-sessions

https://www.sdxcentral.com/articles/analysis/aws-wants-to-be-the-best-place-for-5g-edge/2022/12/

https://biztechmagazine.com/article/2022/12/aws-reinvent-2022-harvesting-data-cloud-edge

Analysys Mason: few private networks include edge computing, despite the synergies between the two technologies

In a report on Private LTE/5G network deployments, Analysys Mason said that “Only 58 of the 363 private network announcements in our tracker explicitly mention that the private network is working with edge computing.” That’s no surprise as per our recent IEEE Techblog post that edge computing has not lived up to its promise and potential.

The number of announced private networks increased from 256 during the third quarter of last year, to 363 announced deployments during Q3 of this year. Most of that growth is coming from more advanced countries and China “where the IoT markets are mature and are driving demand for private networks.” Private networks using 4G LTE technology continue to dominate the overall market “because it is able to meet the connectivity requirements of most private network applications.” However, 5G is gaining ground with more than 70% of new networks announced this year stating the use of 5G technology.

Private networks and edge computing are complementary as each adds value to the other. When combined, the technologies can support applications that have requirements for low latency and high bandwidth or that need to be located on site for security purposes.

The adoption of edge computing with private networks has been limited thus far due to several factors, such as the relative immaturity of edge technology. The drivers of private network adoption are also different to those of edge computing adoption.

Private LTE/5G networks are often introduced to replace existing Wi-Fi or fibre access networks, and no other changes are made. Nevertheless, the share of private network announcements that mention edge is growing, and more than 20% of the private networks that have been publicly announced in 2022 so far include edge. We expect that more private networks will include edge computing in the next 18–24 months. Some vendors are promoting edge as part of a packaged private network solution (such as Nokia with its NDAC solution).

A few operators, such as Verizon, Vodafone and the Chinese MNOs, are promoting the combination, and many other service providers have trials that combine the technologies.

Verizon Business CEO Sowmyanarayan Sampath who during a recent NSR & BCG Innovation Conference explained that private 5G network momentum was outpacing demand for the carrier’s mobile edge computing (MEC) services.

“On the MEC, what we are finding is demand is taking a little longer to go,” Sampath said. “And part of that is we are having to work back and integrate deeper into their operating system. So it’s going to be much stickier when it does happen [but] it’s going to take a little longer. We’ve got loads of proof of concepts and early commercial deployments, but we shouldn’t see revenue till the back half of next year and into 2024.”

References:

https://www.sdxcentral.com/edge/definitions/what-multi-access-edge-computing-mec/

Has Edge Computing Lived Up to Its Potential? Barriers to Deployment

Has Edge Computing Lived Up to Its Potential? Barriers to Deployment

Despite years of touting and hype, edge computing (aka Multi-access Edge Computing or MEC) has not yet provided the payoff promised by its many cheerleaders. Here are a few rosy forecasts and company endorsements:

In an October 27th report, Markets and Markets forecast the Edge Computing Market size is to grow from $44.7 billion in 2022 to $101.3 billion by 2027, which is a Compound Annual Growth Rate (CAGR) of 17.8% over those five years.

IDC defines edge computing as the technology-related actions that are performed outside of the centralized datacenter, where edge is the intermediary between the connected endpoints and the core IT environment.

“Edge computing continues to gain momentum as digital-first organizations seek to innovate outside of the datacenter,” said Dave McCarthy, research vice president, Cloud and Edge Infrastructure Services at IDC. “The diverse needs of edge deployments have created a tremendous market opportunity for technology suppliers as they bring new solutions to market, increasingly through partnerships and alliances.”

IDC has identified more than 150 use cases for edge computing across various industries and domains. The two edge use cases that will see the largest investments in 2022 – content delivery networks and virtual network functions – are both foundational to service providers’ edge services offerings. Combined, these two use cases will generate nearly $26 billion in spending this year (2022). In total, service providers will invest more than $38 billion in enabling edge offerings this year. The market research firm believes spending on edge compute could reach $274 billion globally by 2025 – though that figure would be inclusive of a wide range of products and services.

HPE CEO Antonio Neri recently told Yahoo Finance that edge computing is “the next big opportunity for us because we live in a much more distributed enterprise than ever before.”

DigitalBridge CEO Marc Ganzi said his company continues to see growth in demand for edge computing capabilities, with site leasing rates up 10% to 12% in the company’s most recent quarter. “So this notion of having highly interconnected data centers on the edge is where you want to be,” he said, according to a Seeking Alpha transcript.

Equinix CEO Charles Meyers said his company recently signed a “major design win” to provide edge computing services to an unnamed pediatric treatment and research operation across a number of major US cities. Equinix is one of the world’s largest data center operators, and has recently begun touting its edge computing operations.

……………………………………………………………………………………………………………………………………………………………..

In 2019, Verizon CEO Hans Vestberg said his company would generate “meaningful” revenues from edge computing within a year. But it still hasn’t happened yet!

BofA Global Research wrote in an October 25th report to clients, “Verizon, the largest US wireless provider and the second largest wireline provider, has invested more resources in this [edge computing] topic than any other carrier over the last seven years, yet still cannot articulate how it can make material money in this space over an investable timeframe. Verizon is in year 2 of its beta test of ‘edge compute’ applications and has no material revenue to point to nor any conviction in where real demand may emerge.”

“Gartner believes that communications and manufacturing will be the main drivers of the edge market, given they are infrastructure-intensive segments. We highlight existing use cases, like content delivery in communications, or

‘device control’ in manufacturing, as driving edge compute proliferation. However, as noted above, the market is still undefined and these are only two possible outcomes of many.”

Raymond James wrote in an August research note, “Regarding the edge, carriers and infrastructure companies are still trying to define, size and time the opportunity. But as data demand (and specifically demand for low-latency applications) grows, it seems inevitable that compute power will continue to move toward the customer.”

……………………………………………………………………………………………………………………………………………

BofA Global Research – Challenges with Edge Compute:

The distributed nature of edge compute can pose several risks to enterprises. The number of nodes needed between stores, factories, automobiles, homes, etc. can vary wildly. Different geographies may have different environmental issues, regulatory requirements, and network access. Furthermore, the distributed scale in edge compute puts a greater burden on ensuring that edge compute nodes are secured and that the enterprise is protected. Real-time decision making on the edge device requires a platform to be able to anonymize data used in analytics, and secure data in transit and information stored on the edge device. As more devices are added to the network, each one becomes a potential vulnerability target and as data entry points expand across a corporate network, so do opportunities for intrusion.

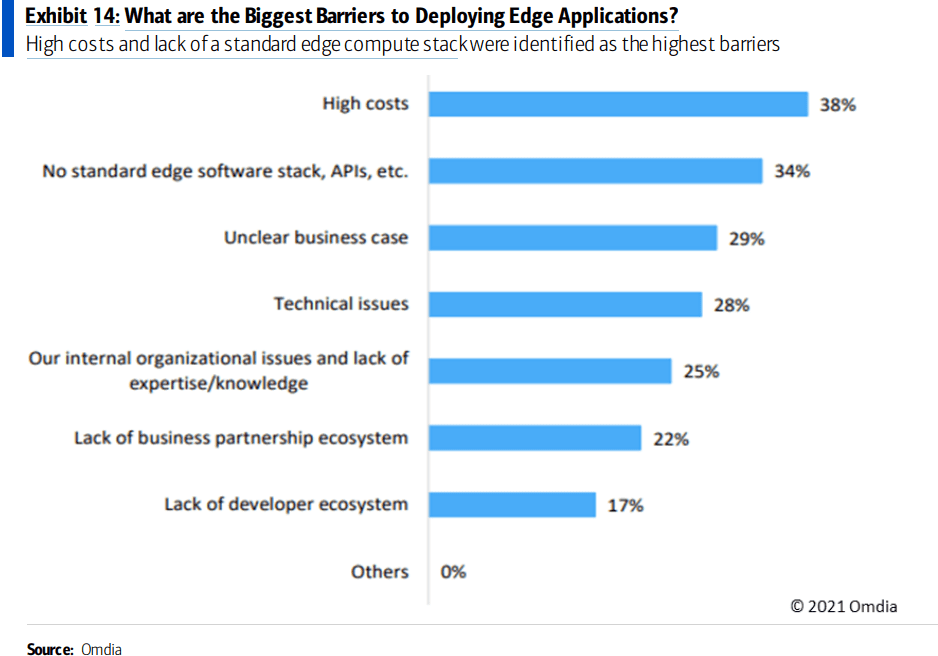

On the other hand, the risk is somewhat double-sided as some security risk is mitigated by keeping the data distributed so that a data breach only impacts a fraction of the data or applications. Other barriers to deploying edge applications include high costs as a result of its distributed nature, as well as a lack of a standard edge compute stack and APIs.

Another challenge to edge compute is the issue of extensibility. Edge computing nodes have historically been very purpose-specific and use-case dependent to environments and workloads in order to meet specific requirements and keep costs down. However, workloads will continuously change and new ones will emerge, and existing edge compute nodes may not adequately cover additional use cases. Edge computing platforms need to be both special-purpose and extensible. While enterprises typically start their edge compute journey on a use-case basis, we expect that as the market matures, edge compute will increasingly be purchased on a vertical and horizontal basis to keep up with expanding use cases.

References:

The Amorphous “Edge” as in Edge Computing or Edge Networking?

Edge computing refuses to mature | Light Reading

Multi-access Edge Computing (MEC) Market, Applications and ETSI MEC Standard-Part I

ETSI MEC Standard Explained – Part II

Lumen Technologies expands Edge Computing Solutions into Europe

NTT, VMware & Intel collaborate to launch Edge-as-a-Service and Private 5G Managed Services

Japan’s NTT Ltd. today announced the launch of Edge-as-a-Service, a managed edge compute platform that gives enterprises the ability to deploy quickly, manage and monitor applications closer to the edge.

NTT and VMware, in collaboration with Intel (whose role was not specified), are partnering to innovate on edge-focused solutions and services. NTT uses VMware’s Edge Compute Stack to power its new Edge-as-a-Service offering. Additionally, VMware is adopting NTT’s Private 5G technologies as part of its edge solution. The companies will jointly market the offering through coordinated co-innovation, sales, and business development.

NTT’s Edge-as-a-Service offering is a globally available integrated solution that accelerates business process automation. It delivers near-zero latency for enterprise applications at the network edge, optimizing costs and boosting end-user experiences in a secure environment.

NTT’s Edge-as-a-Service offering, powered by VMware’s Edge Compute Stack, includes Private 5G connectivity and will be delivered by NTT across its global footprint running on Intel network and edge technology. This work is an extension of NTT’s current membership in VMware’s Cloud Partner Program. VMware and NTT will each market their corresponding new services to their respective customer bases.

“Combining Edge and Private 5G is a game changer for our customers and the entire industry, and we are making it available today,” said Shahid Ahmed, Group EVP, New Ventures and Innovation CEO, NTT.

“The combination of NTT and VMware’s Edge Compute Stack and Private 5G delivers a unique solution that will drive powerful outcomes for enterprises eager to optimize the performance and cost efficiencies of critical applications at the network edge. Minimum latency, maximum processing power, and global coverage are exactly what enterprises need to accelerate their unique digital transformation journeys.”

“The whole premise behind it is that many of our customers are looking for an end-to-end solution when they’re buying either edge or private 5G architectures as opposed to buying edge compute from XYZ and then a private 5G from somebody else and an IoT solution from someone else. So we thought we would do a full one-stop solution for our customers, particularly those that are in manufacturing and industrial sectors.” Ahmed also said that NTT will also be able to break these services apart for customers that just want one of the services, but they will all be managed by NTT.

Ahmed added: “We have a very simple pricing structure, which is predictable and tier-based so the customer doesn’t have to put up upfront capex, it’s all opex based. Obviously, some verticals like to purchase or acquire technology as a capex, so we can do that as well.”

As factories increase their reliance on robotics, vehicles become autonomous, and manufacturers move to omnichannel models, there is a greater need for distributed compute processing power and data storage with near-instantaneous response times. VMware’s secure application development, resource management automation, and real-time processing capabilities combined with NTT’s multi-cloud and edge platforms, creates a fully integrated Edge+Private 5G managed service. VMware and NTT’s innovative offering resides closer to where the data is generated or collected, enabling enterprises to access and react to information instantaneously.

This solution, which leverages seamless multi-cloud and multi-tenant connectivity, combined with NTT’s capabilities in network segmentation, and expertise with movement from private to public 5G, provides critical benefits for multiple industries, including manufacturing, retail, logistics, and entertainment.

“Enterprises are increasingly distributed — from the digital architecture they rely on to the human workforce that powers their business daily. This has spurred a sea change across every industry, altering where data is produced, delivered, and consumed,” said Sanjay Uppal, senior vice president and general manager, service provider, and edge business unit, VMware. “Bringing VMware’s Edge Compute Stack to NTT’s Edge-as-a-Service will enable our mutual customers to build, run, manage, connect and better protect edge-native applications at the Near and Far Edge while leveraging consistent infrastructure and operations with the power of edge computing.”

NTT’s Edge-as-a-Service platform was developed to help secure, optimize and simplify organizations’ digital transformation journeys. Edge-as-a-Service is part of NTT’s Managed Service portfolio, which includes Network-as-a-Service and Multi-Cloud-as-a-Service, all designed for enterprises to focus on their core business.

References:

https://www.sdxcentral.com/articles/news/ntt-vmware-intel-team-for-private-5g-edge-tasks/2022/08/

Lumen Technologies expands Edge Computing Solutions into Europe

Lumen Technologies announced the expansion of its edge computing services into Europe. The low-latency platform businesses need to extend their high-bandwidth, data-intensive applications out to the cloud edge. This expansion is part of Lumen’s continued investment in next-generation solutions that transform digital experiences and meet the demands of today’s global businesses.

“Edge computing is a game-changer. It will drive the next wave of business innovation and growth across virtually all industries,” said Annette Murphy, regional president, EMEA and APAC, Lumen Technologies. “Customers in Europe can now tap into the power of the Lumen platform, underpinned by Lumen’s extensive fiber footprint, to deploy data-heavy applications and workloads that demand ultra-low latency at the cloud edge. This delivers peak performance and reliability, as well as more capability to drive amazing digital experiences. Customers can focus efforts on developing applications and bringing them to market, rather than on time-consuming infrastructure deployment.”

Today, Lumen Edge Computing Solutions can meet approximately 70% of enterprise demand within 5 milliseconds of latency in the UK, France, Germany, Belgium, and the Netherlands. Additional locations are planned by end of year. Lumen Edge Computing Solutions bring together the power of the company’s expansive global fiber network, on-demand networking, integrated security, and managed services, with edge facilities and compute and storage services. This allows for quick and efficient deployment of applications and workloads at the edge, closer to the point of digital interaction. Customers can procure Lumen Edge Computing Solutions online, and within an hour gain access to high-powered computing infrastructure on the Lumen platform.

Lumen offers several edge infrastructure and services solutions to support enterprise innovation and applications of the 4th Industrial Revolution. These include:

- Lumen Edge Bare Metal offers dedicated, pay-as-you-go server hardware hosted in distributed locations and connected to the Lumen global fiber network. Edge Bare Metal delivers enhanced security and connectivity with dedicated, single tenancy servers designed to isolate and protect data and deliver high-performance.

- Lumen Network Storage enables customers to take advantage of secure, scalable, and fast storage where and when they need it. The service allows enterprises and public sector organizations to ingest and update data at the edge using whatever file storage protocol meets their needs.

- Lumen Edge Private Cloud provides pre-built infrastructure for high performance private cloud computing connected to the Lumen global fiber network. Lumen Edge Private Cloud is fully managed by Lumen and helps businesses go-to-market quickly with the capacity needed for interaction-intensive applications.

- Lumen Edge Gateway is a scalable Multi-access Edge Compute (MEC) platform for the premises. The service offers a compute platform for the delivery of virtualized wide area networking (WAN), security, and IT applications from multiple vendors on the premises edge.

Key Facts:

- Lumen Edge Computing Solutions meet approximately 97% of U.S. enterprise demand and approximately 70% of enterprise demand in the UK, France, Germany, Belgium, and the Netherlands within 5 milliseconds of latency.

- For a current list of live and planned Lumen edge locations, visit: https://www.lumen.com/en-uk/resources/network-maps.html#edge-roadmap

- As part of the Edge Computing Solutions deployment in Europe, Lumen enabled an additional 100G MPLS and IP network connectivity, as well as increased power and cooling at key edge data center locations.

- Lumen manages and operates one of the largest, most connected, most deeply peered networks in the world. It is comprised of approximately 500,000 (805,000 km) global route miles of fiber and more than 190,000 on-net buildings, seamlessly connected to 2,200 public and private third-party data centers and leading public cloud service providers.

- In EMEA, the Lumen network is comprised of approximately 42,000 (67,000 km) route miles of fiber and connects to more than 2,500 on-net buildings and 540 public and private third-party data centers.

Additional Resources:

- Lumen Edge Computing Solutions: https://www.lumen.com/en-us/solutions/edge-computing.html

- Lumen Edge Bare Metal: https://www.lumen.com/en-us/edge-computing/bare-metal.html

- Lumen Network Storage: https://www.lumen.com/en-us/hybrid-it-cloud/network-storage.html

- Lumen Edge Private Cloud: https://www.lumen.com/en-us/hybrid-it-cloud/private-cloud.html

- Lumen Edge Gateway: https://www.lumen.com/en-us/edge-computing/edge-gateway.html

About Lumen Technologies and the People of Lumen:

Lumen is guided by our belief that humanity is at its best when technology advances the way we live and work. With approximately 500,000 route fiber miles and serving customers in more than 60 countries, we deliver the fastest, most secure platform for applications and data to help businesses, government and communities deliver amazing experiences.

References:

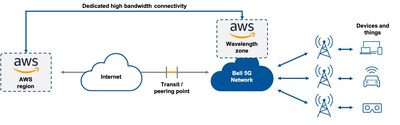

Bell Canada deploys the first AWS Wavelength Zone at the edge of its 5G network

In yet another tie-up between telcos and cloud computing giants, Bell Canada is the first Canadian network operator to launch multi-access edge computing (MEC) services using Amazon Web Services’ (AWS) Wavelength platform.

Building on Bell’s agreement with AWS, announced last year, together the two companies are deploying AWS Wavelength Zones throughout the country at the edge of Bell’s 5G network starting in Toronto.

The Bell Canada Public MEC service embeds AWS compute and software defined storage capabilities at the edge of Bell’s 5G network.

The Wavelength technology is then tied into AWS cloud regions that host the applications. This moves access closer to the end user or device to lower latency and increase performance for services such as real-time visual data processing, augmented/virtual reality (AR/VR), artificial intelligence and machine learning (AI/ML), and advanced robotics.

Source: Bell Canada

……………………………………………………………………………………………………………………………………………………………………………….

“Because that link between the application and the edge device is a completely controllable link – it doesn’t involve the internet, doesn’t involve these multiple hops of the traffic to reach the application – it allows us to have a very particular controlled link that can give you different quality of service,” explained George Elissaios, director and GM for EC2 Core Product Management at AWS, during a briefing call with analysts.

Network infrastructure is the backbone for Canadian businesses today as they innovate and advance in the digital age. Organizations across retail, transportation, manufacturing, media & entertainment and more can unlock new growth opportunities with 5G and MEC to be more agile, drive efficiency, and transform customer experiences.

Optimized for MEC applications, AWS Wavelength deployed on service providers’ 5G networks provides seamless access to cloud services running in AWS Regions. By doing so, AWS Wavelength minimizes the latency and network hops required to connect from a 5G device to an application hosted on AWS. AWS Wavelength is now available in Canada, the United States, the United Kingdom, Germany, South Korea, and Japan in partnership with global communications service providers.

Creating an immersive shopping experience with Bell Canada 5G:

Increasingly, retailers want to offer omni-channel shopping experiences so that consumers can access products, offers, and support services on the channels, platforms, and devices they prefer. For instance, there’s a growing appetite for online shopping to replicate the in store experience – particularly for apparel retailers. These kinds of experiences require seamless connectivity so that customers can easily and immediately pick up on a channel after they leave another channel to continue the experience. These experiences also must be optimized for high-quality viewing and interactivity.

Rudsak worked with Bell and AWS to deploy Summit Tech’s immersive shopping platform, Odience, to offer its customers an immersive and seamless virtual shopping experience with live sales associates and the ability to see merchandise up close. With 360-degree cameras at its pop-up locations and launch events, Rudsak customers can browse the racks and view a new product line via their smartphones or VR headsets from either the comfort of their own home or while on the go. To find out more, please click here.

Bell Canada Public MEC with AWS Wavelength is now available in the Toronto area, with additional Wavelength Zones to be deployed in the future. To find out more, please visit: Bell.ca/publicmec

AWS currently has Wavelength customers (see References below) in the United States, the United Kingdom, Germany, South Korea, Japan, and now Canada. It also has deals with Verizon, Vodafone, SK Telecom, and Dish Network.

Bell Canada explained that the service is targeted at enterprise customers. It will initially offer services to enterprises in Toronto, with expansion planned into other major Canadian markets.

“We’re excited to partner with AWS to bring together Bell’s 5G network leadership with the world’s leading cloud and AWS’ robust portfolio of compute and storage services. With general availability of AWS Wavelength Zones on Canada’s fastest network, it becomes possible for businesses to tap into all-new capabilities, reaching new markets and serving customers in exciting new ways. With our help, customers are thinking bigger, innovating faster and pushing boundaries like never before. Our team of experts are with customers every step of the way on their digital transformation journey. With our ongoing investments in supporting emerging MEC use cases, coupled with our end-to-end security built into our 5G network, we are able to give Canadian businesses a platform to innovate, harness the power of 5G and drive competitiveness for their businesses.”

– Jeremy Wubs, Senior Vice President of Product, Marketing and Professional Services, Bell Business Markets

“AWS Wavelength brings the power of the world’s leading cloud to the edge of 5G networks so that customers like Rudsak, Tiny Mile and Drone Delivery Canada can build highly performant applications that transform consumers’ experiences. We are particularly excited about our deep collaboration with Bell as it accelerates innovation across Canada, by offering access to 5G edge technology to the whole AWS ecosystem of partners and customers. This enables any enterprise or developer with an AWS account to power new kinds of mobile applications that require ultra-low latencies, massive bandwidth, and high speeds.”

– George Elissaios, Director and General Manager, EC2 Core Product Management, AWS

“With Bell’s Public MEC and AWS Wavelength we are able to offer new, fully immersive shopping experiences to our customers. Shoppers can virtually explore our new arrivals and interact in real-time with our staff and industry experts during interactive events and pop-ups. Thanks to the hard work, support and expertise of Bell, AWS and Summit Tech, we were able to successfully deliver our first immersive/interactive shopping event with the quality, innovation and excellence that our brand is known for.”

– Evik Asatoorian, President and Founder, Rudsak

“Canadian organizations across all industries are transforming their workflows by harnessing the power of new technologies to launch new products and services. In fact, 85% of Canadian businesses are already using the Internet of Things (IoT). In order to maximize the benefits of cloud computing, intelligent endpoints and AI, while adding emerging technologies like 5G, we need to modernize our digital infrastructure to embrace multi-access edge computing (MEC). Modernized edge computing interconnects core, cloud and diverse edge sites, enabling CIOs and business leaders to optimize their architectures to resolve technical challenges around latency, bandwidth and compute power, financial concerns about cloud ingress/egress and compute costs as well as governance issues such as regulatory compliance without losing advanced features like machine learning, AI and analytics. MEC offers the possibility of deploying modernized, cloud-like resources everywhere to support the ability to extract value from data.”

– Nigel Wallis, Research VP, Canadian Industries and IoT, IDC Canada

- Bell is the first Canadian telecommunications company to offer AWS-powered public MEC to business customers

- First AWS Wavelength Zone to launch in the Toronto region, with additional locations in Canada to follow

- Apparel retailer Rudsak among the first to leverage Bell Public MEC with AWS Wavelength to deliver an immersive virtual shopping experience

Bell is Canada’s largest communications company, providing advanced broadband wireless, TV, Internet, media and business communication services throughout the country. Founded in Montréal in 1880, Bell is wholly owned by BCE Inc. To learn more, please visit Bell.ca or BCE.ca.

References:

AWS looks to dominate 5G edge with telco partners that include Verizon, Vodafone, KDDI, SK Telecom

Verizon, AWS and Bloomberg media work on 4K video streaming over 5G with MEC

AWS deployed in Digital Realty Data Centers at 100Gbps & for Bell Canada’s 5G Edge Computing

Amazon AWS and Verizon Business Expand 5G Collaboration with Private MEC Solution

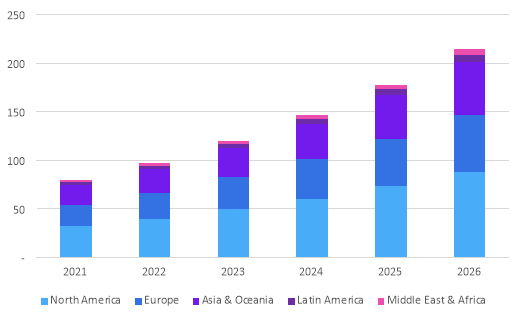

Omdia: Enterprise edge services market to hit $214 billion by 2026

According to a new report by Informa’s Omdia, revenue from edge services (where EXACTLY is the edge?) will reach $214 billion by 2026. That’s more than double the current size of the enterprise edge services market, which will reach $97.0 billion in 2022, says Omdia. With a compound annual growth rate (CAGR) of 20.4%, North America is predicted to dominate with 41% of global revenue share between 2021 and 2026.

This Omdia report discusses the latest global enterprise edge services forecast including edge consulting, integration, network, security, storage/compute and managed edge services considering use cases, verticals and edge deployment models.

Enterprise edge services forecast by region, 2021-26 ($ billions)

Source: Omdia (owned by Informa)

…………………………………………………………………………………………………………

While hyperscalers build out edge access points and systems integrators (SIs) design consulting and professional services for edge use cases, enterprises are looking to service providers to define business cases, run pilot projects and scope out different approaches to edge computing use cases, according to Omdia.

The Informa owned market research group outlines two main consumption models for edge services.

- In one model, enterprises will need consulting, systems integration and other support services to deploy physical edge infrastructure.

- The second method is a cloud-based, as-a-service and fully managed approach, where services provided by hyperscalers and independent software vendors (ISVs) are extended to the edge using local access points or gateways.

Omdia sees several opportunities for network providers to assist enterprises with the challenges that arise from implementing their edge strategies. The firm notes that telcos can help enterprises navigate data location and management considerations; regulatory compliance; network considerations such as the need for and availability of 5G, WAN/LAN and private networks; selecting the right edge setup and location; balancing use of internal skills with managed edge services; defining clear business cases; and more.

Edge consulting services from SIs, telcos, ICT solutions vendors and consulting firms form the largest part of the enterprise edge services market at 39.3% in 2022, says Omdia. While cybersecurity and network management subscriptions from service providers are critical to edge service packages, these subscription-based telco services are declining over time, the research group adds.

However, fully managed, cloud-delivered edge services, including multi-access edge computing (MEC) and workload and database management, are increasing in popularity. Omdia predicts that edge storage and compute services will be the strongest area of growth, with the services emerging as cloud services extensions to the edge provided by major hyperscalers, service providers and data center operators.

“As data volumes continue to grow and enterprises aim to move more workloads to the edge, they require more compute and storage capacity in the form of IaaS and PaaS at edge access points,”Omdia explained.

Edge locations will also shift from customers’ premises (53% in 2022 and 38% in 2026) to PoPs (point of presence) such as cloud access points and to a lesser extent, data centers.

“By 2026, over a third of edge services revenues will be realized as part of PoP deployments, which provides key opportunities and challenges for ICT service providers,” says Omdia.

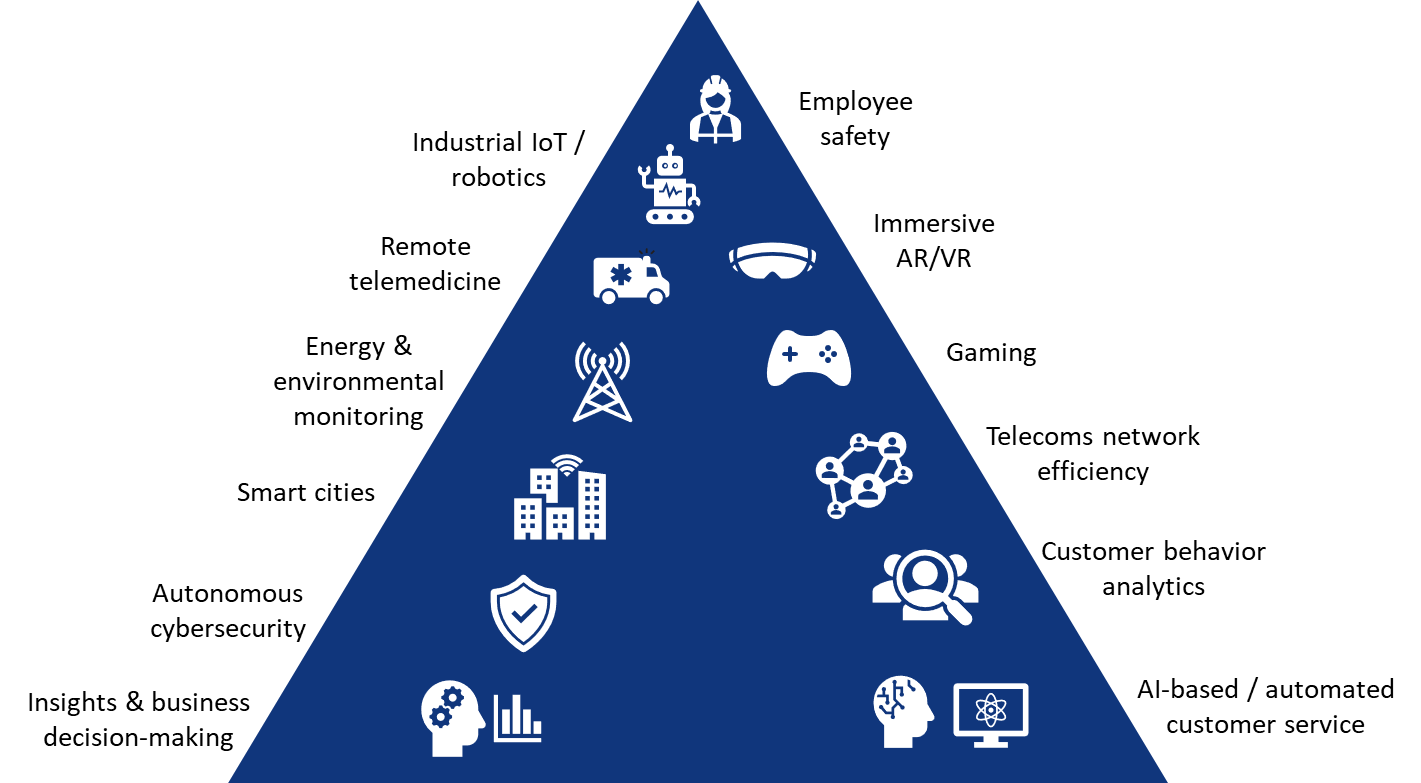

Emerging edge use cases

Edge use cases initially took flight in industrial applications and IoT use cases for worker safety, automated production lines, mining and logistics, explains Omdia. Over the next five years, the largest vertical forecasted to lead growth in edge services is the financial market, which could use AI-based analytics and cognitive systems for business decisions, market insight, risk assessment and customer service platforms.

Source: Omdia

Source: Omdia

…………………………………………………………………………………………………………………

Additional edge service use cases, which network operators could deliver as managed services, include smart meters for energy use and environmental monitoring; transport and container tracking; customer behavior analytics in retail; network efficiency; and data protection compliance and cybersecurity.

What applications do enterprises expect to run at the edge?

Omdia recommends several approaches for service providers, SIs, hyperscalers and ICT solutions vendors to consider when working with enterprises on edge services. Suggestions include developing vertical and workload-specific edge services that can be largely replicated to different customers, creating innovation hubs for edge solutions to test edge setups with customers, developing consulting services and creating a partner ecosystem to reduce vendor lock-in for customers.

References:

https://omdia.tech.informa.com/OM024012/Enterprise-Services-at-the-Edge–Forecast-202226

The Amorphous “Edge” as in Edge Computing or Edge Networking?

Multi-access Edge Computing (MEC) Market, Applications and ETSI MEC Standard-Part I

IBM says 5G killer app is connecting industrial robots: edge computing with private 5G

ONF’s Private 5G Connected Edge Platform Aether™ Released to Open Source