Canalys & Gartner: AI investments drive growth in cloud infrastructure spending

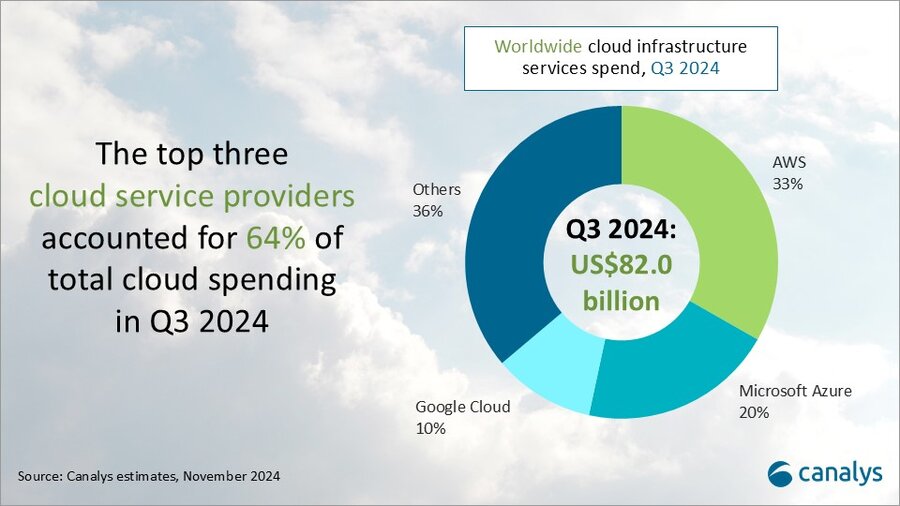

According to market research firm Canalys, global spending on cloud infrastructure services [1.] increased by 21% year on year, reaching US$82.0 billion in the 3rd quarter of 2024. Customer investment in the hyperscalers’ AI offerings fueled growth, prompting leading cloud vendors to escalate their investments in AI.

Note 1. Canalys defines cloud infrastructure services as services providing infrastructure (IaaS and bare metal) and platforms that are hosted by third-party providers and made available to users via the Internet.

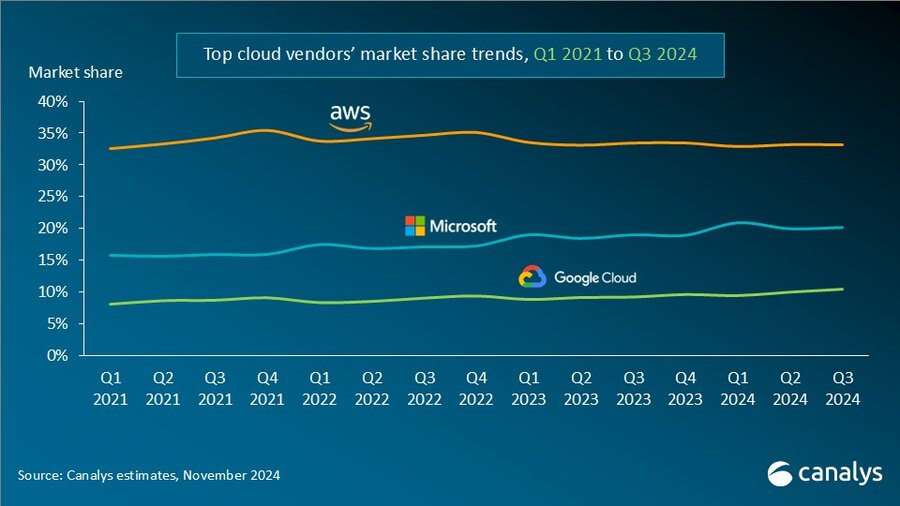

The rankings of the top three cloud service providers – Amazon AWS, Microsoft Azure and Google Cloud – remained stable from the previous quarter, with these providers together accounting for 64% of total expenditure. Total combined spending with these three providers grew by 26% year on year, and all three reported sequential growth. Market leader AWS maintained a year-on-year growth rate of 19%, consistent with the previous quarter. That was outpaced by both Microsoft, with 33% growth, and Google Cloud, with 36% growth. In actual dollar terms, however, AWS outgrew both Microsoft and Google Cloud, increasing sales by almost US$4.4 billion on the previous year.

In Q3 2024, the cloud services market saw strong, steady growth. All three cloud hyperscalers reported positive returns on their AI investments, which have begun to contribute to their overall cloud business performance. These returns reflect a growing reliance on AI as a key driver for innovation and competitive advantage in the cloud.

With the increasing adoption of AI technologies, demand for high-performance computing and storage continues to rise, putting pressure on cloud providers to expand their infrastructure. In response, leading cloud providers are prioritizing large-scale investments in next-generation AI infrastructure. To mitigate the risks associated with under-investment – such as being unprepared for future demand or missing key opportunities – they have adopted over-investment strategies, ensuring their ability to scale offerings in line with the growing needs of their AI customers. Enterprises are convinced that AI will deliver an unprecedented boost in efficiency and productivity, so they are pouring money into hyperscalers’ AI solutions. Accordingly, cloud service provider capital spending (CAPEX) will sustain their rapid growth trajectories and are expected to continue on this path into 2025.

“Continued substantial expenditure will present new challenges, requiring cloud vendors to carefully balance their investments in AI with the cost discipline needed to fund these initiatives,” said Rachel Brindley, Senior Director at Canalys. “While companies should invest sufficiently in AI to capitalize on technological growth, they must also exercise caution to avoid overspending or inefficient resource allocation. Ensuring the sustainability of these investments over time will be vital to maintaining long-term financial health and competitive advantage.”

“On the other hand, the three leading cloud providers are also expediting the update and iteration of their AI foundational models, continuously expanding their associated product portfolios,” said Yi Zhang, Analyst at Canalys. “As these AI foundational models mature, cloud providers are focused on leveraging their enhanced capabilities to empower a broader range of core products and services. By integrating these advanced models into their existing offerings, they aim to enhance functionality, improve performance and increase user engagement across their platforms, thereby unlocking new revenue streams.”

Amazon Web Services (AWS) maintained its lead in the global cloud market in Q3 2024, capturing a 33% market share and achieving 19% year-on-year revenue growth. It continued to enhance and broaden its AI offerings by launching new models through Amazon Bedrock and SageMaker, including Anthropic’s upgraded Claude 3.5 Sonnet and Meta’s Llama 3.2. It reported a triple-digit year-on-year increase in AI-related revenue, outpacing its overall growth by more than three times. Over the past 18 months, AWS has introduced nearly twice as many machine learning and generative AI features as the combined offerings of the other leading cloud providers. In terms of capital expenditure, AWS announced plans to further increase investment, with projected spending of approximately US$75 billion in 2024. This investment will primarily be allocated to expanding technology infrastructure to meet the rising demand for AI services, underscoring AWS’ commitment to staying at the forefront of technological innovation and service capability.

Microsoft Azure remains the second-largest cloud provider, with a 20% market share and impressive annual growth of 33%. This growth was partly driven by AI services, which contributed approximately 12% to the overall increase. Over the past six months, use of Azure OpenAI has more than doubled, driven by increased adoption by both digital-native companies and established enterprises transitioning their applications from testing phases to full-scale production environments. To further enhance its offerings, Microsoft is expanding Azure AI by introducing industry-specific models, including advanced multimodal medical imaging models, aimed at providing tailored solutions for a broader customer base. Additionally, the company announced new cloud and AI infrastructure investments in Brazil, Italy, Mexico and Sweden to expand capacity in alignment with long-term demand forecasts.

Google Cloud, the third-largest provider, maintained a 10% market share, achieving robust year-on-year growth of 36%. It showed the strongest AI-driven revenue growth among the leading providers, with a clear acceleration compared with the previous quarter. As of September 2024, its revenue backlog increased to US$86.8 billion, up from US$78.8 billion in Q2, signaling continued momentum in the near term. Its enterprise AI platform, Vertex, has garnered substantial user adoption, with Gemini API calls increasing nearly 14-fold over the past six months. Google Cloud is actively seeking and developing new ways to apply AI tools across different scenarios and use cases. It introduced the GenAI Partner Companion, an AI-driven advisory tool designed to offer service partners personalized access to training resources, enhancing learning and supporting successful project execution. In Q3 2024, Google announced over US$7 billion in planned data center investments, with nearly US$6 billion allocated to projects within the United States.

Separate statistics from Gartner corroborate hyperscale CAPEX optimism. Gartner predicts that worldwide end-user spending on public cloud services is on course to reach $723.4 billion next year, up from a projected $595.7 billion in 2024. All segments of the cloud market – platform-as-a-service (PaaS), software-as-a-service (SaaS), desktop-as-a-service (DaaS), and infrastructure-as-a-service (IaaS) – are expected to achieve double-digit growth.

While SaaS will be the biggest single segment, accounting for $299.1 billion, IaaS will grow the fastest, jumping 24.8 percent to $211.9 million.

Like Canalys, Gartner also singles out AI for special attention. “The use of AI technologies in IT and business operations is unabatedly accelerating the role of cloud computing in supporting business operations and outcomes,” said Sid Nag, vice president analyst at Gartner. “Cloud use cases continue to expand with increasing focus on distributed, hybrid, cloud-native, and multicloud environments supported by a cross-cloud framework, making the public cloud services market achieve a 21.5 percent growth in 2025.”

……………………………………………………………………………………………………………………………………………………………………………………………………..

References:

https://canalys.com/newsroom/global-cloud-services-q3-2024

https://www.telecoms.com/public-cloud/ai-hype-fuels-21-percent-jump-in-q3-cloud-spending

Cloud Service Providers struggle with Generative AI; Users face vendor lock-in; “The hype is here, the revenue is not”

MTN Consulting: Top Telco Network Infrastructure (equipment) vendors + revenue growth changes favor cloud service providers

IDC: Public Cloud software at 2/3 of all enterprise applications revenue in 2026; SaaS is essential!

IDC: Cloud Infrastructure Spending +13.5% YoY in 4Q-2021 to $21.1 billion; Forecast CAGR of 12.6% from 2021-2026

IDC: Worldwide Public Cloud Services Revenues Grew 29% to $408.6 Billion in 2021 with Microsoft #1?

Synergy Research: Microsoft and Amazon (AWS) Dominate IT Vendor Revenue & Growth; Popularity of Multi-cloud in 2021

Google Cloud revenues up 54% YoY; Cloud native security is a top priority

3 thoughts on “Canalys & Gartner: AI investments drive growth in cloud infrastructure spending”

Comments are closed.

Oracle Cloud Infrastructure (OCI) is a cloud computing platform providing a suite of services like compute, storage, networking, and database capabilities to build and run applications in a highly available, high-performance environment. OCI competes with AWS, Azure and Google Cloud but is far behind them in revenue. OCI enables users to deploy applications across various cloud regions globally with features like high-performance computing and robust security options.

https://docs.oracle.com/en/cloud/paas/ociov/oci_intro.html

Elon Musk’s generative AI startup xAI has raised $6 billion in a Series C funding round. Investors include A16Z, Blackrock, Fidelity Management & Research Company, Kingdom Holdings, Lightspeed, MGX, Morgan Stanley, OIA, QIA, Sequoia Capital, Valor Equity Partners and Vy Capital, amongst others. GPU companies Nvidia and AMD also participated in the round.

The company last raised $6bn in May, and this summer launched its supercomputer in Memphis with up to 100,000 Nvidia H100 GPUs. Earlier this month, the Memphis Chamber of Commerce claimed that Musk eventually planned to expand the Colossus supercomputer to some one million GPUs.

The company pitches itself as an alternative to OpenAI, which Musk is currently suing for deviating from its non-profit roots. Before he broke away from OpenAI, Musk had pitched making the company a division of for-profit Tesla.

Musk has called OpenAI’s ChatGPT too “woke” and “politically correct,” and claimed that xAI’s Grok is “maximally truth-seeking.”

The company was founded in March 2023 and has grown rapidly since, with its products integrated deeply into Musk’s Twitter/X, and trained on the social media platform’s user-generated data.

https://www.datacenterdynamics.com/en/news/xai-raises-another-6bn-including-from-nvidia-and-amd/

Big Tech companies are engaged in an artificial-intelligence arms race, each building data centers at a blistering rate. All together, the four giants spent $95 billion on capex in the second quarter, and much more than that is in the pipeline.

The companies have been giving annual capex guidance. Microsoft, whose fiscal year ended this quarter, declined to issue a fiscal 2026 projection, but put out a big number—over $30 billion—for the current quarter’s investments. That would see expenses rise by 50% on the year, but Chief Financial Officer Amy Hood cautioned that the growth rate would moderate through the fiscal year.

By contrast, Meta isn’t slowing down. After raising its 2025 capex guidance last quarter and inching it up this past week, Chief Financial Officer Susan Li said on the earnings call that the company “expects to ramp our investments significantly in 2026.” This is exceptional because Meta is the only one from this group that doesn’t operate a cloud to rent out these AI servers; it’s all for its own use.

Amazon is also proceeding full steam ahead. It used almost every penny of its second-quarter operational cash flows for $31 billion of capex, and guided to around $60 billion for the second half, putting it on pace for a stunning $115 billion for the year. Amazon leads the pack here, but unlike the other AI contenders, its number is inflated by large retail investments for warehouses, vehicles, and robots.

Alphabet isn’t slowing down either, raising its 2025 capex guidance considerably. And though Apple spends much less—$3.5 billion in the quarter—that’s still 61% higher than last year.

https://www.barrons.com/articles/takeaways-big-tech-earnings-ai-68402f1a?mod=hp_WIND_A_3_2