Hyperscalers Dominance of Subsea Cable Capacity to Increase in the AI Era

Hyperscalers (AWS, Google, Microsoft, Meta/FB) now dominate global subsea cable capacity. Their share of total international bandwidth has surged from negligible levels in 2010 to approximately 75% today. According to data from TeleGeography, hyperscalers are participating in over two-thirds of all planned submarine cable deployments, with Google alone anchoring eight new systems in the Asia-Pacific (APAC) region. Despite this shift, traditional telecommunications operators remain critical to the subsea ecosystem.

Tier-1 telecom carriers provide the deep terrestrial reach and last-mile connectivity that both regional service providers and large content providers require to access edge markets. However, those network operators must increasingly architect their Wide Area Network (WAN) and long-haul transport infrastructure to integrate seamlessly with these massive hyperscale topologies.

Brian Washburn, Chief Analyst at Omdia’s Telco B2B Solutions Intelligence Service, notes that carriers face intensifying pressure to align their infrastructure with hyperscaler technical requirements. To achieve complete architectural control and establish fully isolated private networks, hyperscalers frequently seek to deploy proprietary optical transport equipment directly within carrier landing stations and co-location facilities. This shift toward self-contained infrastructure creates visibility challenges for the industry. Washburn noted Google’s extensive transpacific cable network as a primary example. Because this hyperscaler traffic is routed over fully private, dark fiber subsea segments, it remains entirely invisible to carrier networks and traditional traffic-modeling metrics, rendering these massive data volumes completely opaque.

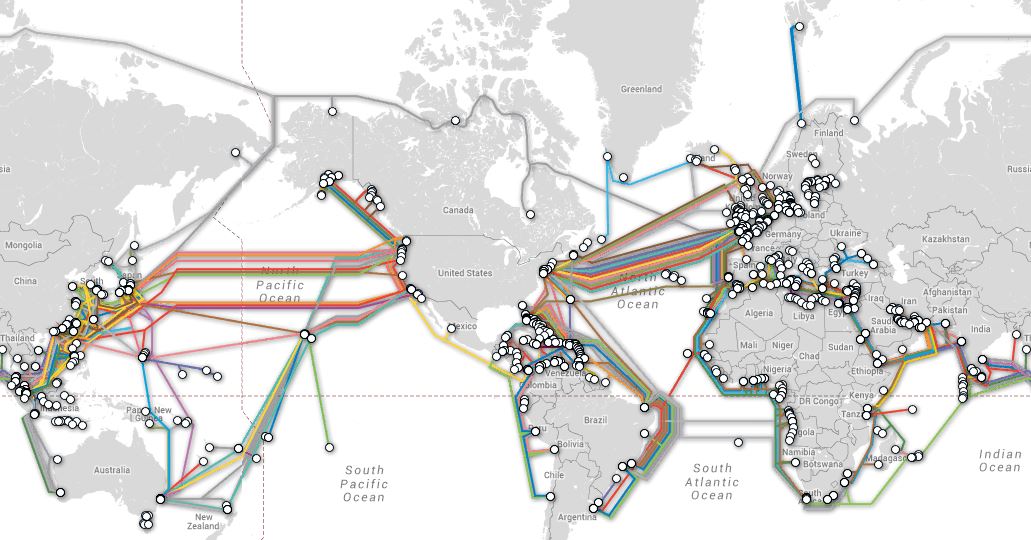

TeleGeography’s interactive submarine cable map shows the majority of active and planned international submarine cable systems and their landing stations. Selecting a cable route on the map provides access to data about the cable, including the cable’s name, ready-for-service (RFS) date, length, owners, website, and landing points. Selecting a landing point provides a list of all submarine cables landing at that station.

From a macro perspective, the deployment of next-generation physical infrastructure is increasingly tied to the rollout of raw, rack-scale data center capacity to support emerging AI workloads. Matt Walker, Chief Analyst at MTN Consulting, indicates that while Tier-1 US operators anticipate near-term traffic growth from centralized AI training models, they maintain a cautious, wait-and-see outlook regarding long-term network demand and the broader monetization of distributed inference at the edge. “With agentic, the potential for rapid growth in unexpected parts of the network is real, and it’s not clear how to plan for this,” he said. Operators are worried they will be stuck with the network costs to support “these pricey new AI-enabled services,” he also noted. Telco’s lack of visibility becomes a problem here. Walker stated in his research report: “The industry is flying partially blind. No comprehensive public study of AI traffic volumes, patterns, or growth exists. Nokia, Ericsson, and a handful of others have made partial contributions, but hyperscalers don’t share traffic data. For an industry spending over $600 billion in capex this year, this is a significant planning liability.”

MTN also revealed that telco capex remained subdued in 4Q2025, rising just 0.2% YoY to $86.6B as operators prioritized capital discipline, AI-enabled efficiency, and monetization of prior 5G investments. On an annualized basis, capex declined 0.9% to $295.7B, remaining below the $300B threshold for a second consecutive year. The strongest annualized capex growth rates were recorded by Swisscom (40.7%), Etisalat (40.5%), Airtel (24.4%), SoftBank (10.5%), and Deutsche Telekom (10.3%). The steepest capex declines came from China Telecom (-13.6%), Telefonica (-12.3%), China Unicom (-11.5%), Reliance Jio (-10.8%), and China Mobile (-8.1%).

Regionally, the Americas strengthened its lead in 4Q2025, accounting for 36.5% of global telecom revenues and 36.3% of capex, supported by resilient performance from T-Mobile US, AT&T, and Verizon. Asia’s revenue share moderated to 35.6% and capex share fell to 32.4%. This is notable given that Chinese telcos have been ramping AI and data center spending, while overall capex continues to decline as cuts to radio/hardware spending post-5G more than offset these gains.

References:

https://www.lightreading.com/ai-machine-learning/ai-is-going-to-transform-our-networks

https://www.submarinecablemap.com/

Cisco report: Agentic AI to reshape WAN traffic, AI inference will be ~25% of total traffic by 2035

Fiber Optic Networks & Subsea Cable Systems as the foundation for AI and Cloud services

Subsea cable systems: the new high-capacity, high-resilience backbone of the AI-driven global network

FCC updates subsea cable regulations; repeals 98 “outdated” broadcast rules and regulations

India’s Data Transmission Capacity to Quadruple in 2025 via New Submarine Cables

TechCrunch: Meta to build $10 billion Subsea Cable to manage its global data traffic

Google’s Bosun subsea cable to link Darwin, Australia to Christmas Island in the Indian Ocean

China seeks to control Asian subsea cable systems; SJC2 delayed, Apricot and Echo avoid South China Sea

“SMART” undersea cable to connect New Caledonia and Vanuatu in the southwest Pacific Ocean

Telstra International partners with: Trans Pacific Networks to build Echo cable; Google and APTelecom for central Pacific Connect cables

Orange Deploys Infinera’s GX Series to Power AMITIE Subsea Cable

Intentional or Accident: Russian fiber optic cable cut (1 of 3) by Chinese container ship under Baltic Sea

One thought on “Hyperscalers Dominance of Subsea Cable Capacity to Increase in the AI Era”

Leave a Reply

There’s no doubt that hyperscalers are dominating subsea cable capacity to support AI infrastructure. This article highlights the shift from traditional telecom usage to private, high-capacity, AI-focused pipelines driven by major big tech companies.

The piece is especially persuasive because it ties subsea capacity ownership to data-center geography, private transport control, and the difficulty telecom operators face in seeing or modeling hyperscaler traffic.

The core thesis aligns with current market structure: hyperscalers now account for a very large share of international bandwidth and are participating in most new planned submarine systems, which is consistent with the post’s claim that their share has risen dramatically since 2010. The article also correctly emphasizes that this is not just about “internet backbone” capacity, but about direct interconnection between cloud regions and AI infrastructure, where ownership and route control matter as much as raw bandwidth. Its focus on the opacity problem is also important. If hyperscalers are using private subsea assets and dark fiber-like arrangements, then traditional carrier traffic models will increasingly understate demand and misread where future congestion or monetization opportunities will arise. That is a meaningful strategic point for operators, vendors, and investors.

The post blends author commentary with material attributed to TeleGeography, Omdia/Brian Washburn, MTN Consulting/Matt Walker, and linked references. It assembles several external viewpoints into a coherent thesis: hyperscalers are taking a larger share of subsea capacity, and AI-related traffic growth is accelerating the strategic importance of subsea and terrestrial fiber. That makes the post useful as an analytical roundup, even if many of the strongest numbers and quotations are borrowed rather than newly generated.

In my opinion, the TeleGeography and MTN Consulting references carry most of the evidentiary weight, while the author’s role is to connect them and draw implications for carriers and hyperscalers