Month: June 2026

Dell’Oro: AI RAN revenue forecast: $35B from 2026-to-2030; 3 types of AI RAN explained

According to a new AI RAN Advanced Research Report published by Dell’Oro Group, cumulative AI RAN revenue is projected to reach $35 B over the next five years (2026-2030). However, AI RAN is not expected to expand the overall RAN market.

“Our market assessment and long-term AI RAN position remain unchanged,” said Stefan Pongratz, Vice President at Dell’Oro Group. “AI RAN is already happening and will scale ahead of 6G. At the same time, these tools will enhance the RAN, but they are unlikely to expand the overall RAN market. Even as suppliers introduce new software-based subscription models, we expect AI RAN to generate little, if any, incremental RAN revenue the end of the forecast period,” continued Pongratz.

Additional highlights from the June 2026 AI RAN Advanced Research Report:

- The base-case forecast assumes that AI RAN will not expand the RAN market. Nevertheless, AI RAN is expected to become an important technology enabler as operators incorporate greater virtualization, intelligence, automation, and O-RAN capabilities into their RAN roadmaps.

- GPU RAN projections have been revised upward—GPU RAN is now expected to be a $1 B+ market by the end of the forecast period.

- In the near term, the AI RAN market will remain centered on AI-for-RAN, single-purpose deployments, non-GPU architectures, D-RAN, and 5G.

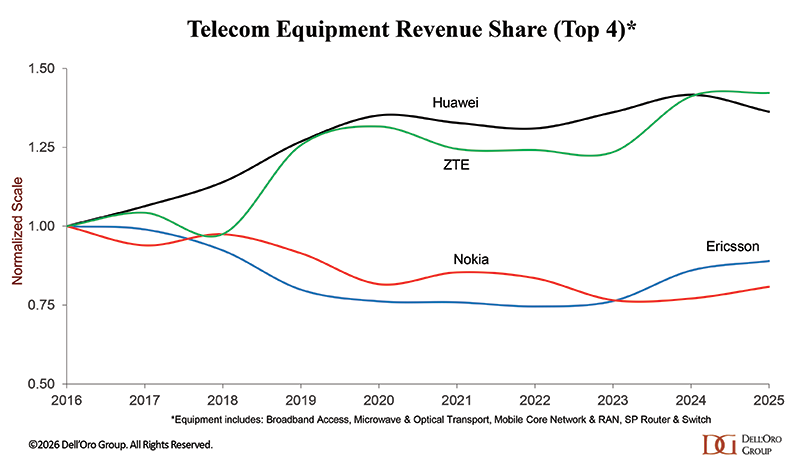

- Incumbent RAN radio and baseband suppliers are well-positioned in the initial AI RAN phase, driven primarily by AI-for-RAN upgrades leveraging existing hardware. Per Dell’Oro Group’s regular RAN coverage, the top five RAN suppliers contributed approximately 96 percent of 2025 RAN revenue. See charts below.

Dell’Oro Group’s AI RAN Advanced Research Report includes a 5-year forecast for AI RAN by location, tenancy, technology, and region. To purchase this report, please contact us at [email protected].

………………………………………………………………………………………………………………………………………………………………………….

Total & Wireless Telecom Equipment Revenue- top 4 and top 3:

………………………………………………………………………………………………………………………………………………………………………………….

Analysis (Source: Perplexity.ai AND Google Gemini):

There are three versions of AI-RAN which are not mutually exclusive:

- AI for RAN: Embeds AI into the base software stack to automatically manage radio waves, optimize spectrum efficiency, enhance beamforming, and reduce energy consumption in real time. Nokia, Ericsson, NVIDIA.

- AI on RAN: Uses cell towers and base stations as decentralized computing nodes. This allows telecom networks to host AI workloads locally rather than sending all data to distant cloud servers, providing ultra-low latency for applications like robotics, AR/VR, and autonomous vehicles. Nokia, NVIDIA, and operator trial partners like T-Mobile, Indosat, and SoftBank.

- AI and RAN: Combines the two to support “Networks for AI,” where distributed telecom networks act as an active, intelligent backbone to serve end-user AI traffic. AI-RAN Alliance plus Nokia and NVIDIA as the most visible industry champions.

References:

AI RAN to Reach $35 B Over Next Five Years, According to Dell’Oro Group

NVIDIA AI RAN video: youtube.com/watch?v=hwLLBfzoSko&t=26

AI-Era Cloud Network Transformation: A Reference Architecture and Implementation Roadmap

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

AI-RAN Reality Check: hype vs hesitation, shaky business case, no specific definition, no standards?

Analysis: Nvidia’s rumored new 6G AI-RAN – likely features/functions and industry impact

Dell’Oro: 2H2026 Data Center Capex to Accelerate due to massive AI Deployments

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

Analysis of AWS-3 Spectrum Results: Verizon Wins Big; Urban Capacity vs. Propagation

AWS-3 Auction Results:

Of the $3.57 billion total spent in the recent AWS-3 auction, $3.2 billion of it was accounted for by Verizon alone (bidding as Cellco Partnership). That bought it 82 of the 200 licenses on offer, with the price premium explained by a bias towards high value urban licenses. The remaining AWS-3 spectrum allocation was primarily secured by T-Mobile and, to a lesser extent, AT&T. SpaceX bid conservatively, indicating its recent spectrum acquisitions from Dish Networks will likely serve as supplementary capacity rather than signaling a shift to build a comprehensive, standalone terrestrial mobile network.

T-Mobile took home more raw licenses than Verizon, but spent a fraction of the capital. This architectural split is dictated by existing network layouts. T-Mobile used its capital to snap up cheap, fragmented regional licenses to patch coverage holes in its massive 2.5 GHz (Band 41) rural backbone. Conversely, Verizon spent heavily because its existing grid configuration requires deeper, cleaner mid-band spectrum to keep up with urban data density without triggering catastrophic inter-cell interference.

Here’s a breakdown of winning bids and assigned spectrum:

| Carrier | Licenses Won | Total Spend | Strategic Context |

|---|---|---|---|

| Verizon | 82 | $3.20 billion | Dominant bidder to acquire significant mid-band capacity. |

| T-Mobile | 102 | $278 million | Acquired the largest volume of licenses for rural and edge-market coverage. |

| AT&T | 10 | $121 million | Targeted smaller holdings to bolster localized network capacity. |

| SpaceX | 2 | $8.5 million | Acquired two regional licenses to complement supplemental coverage from space (SCS) initiatives. |

Here are the full results, published by the FCC:

“After years on the sidelines, FCC auctions are finally back,” said Chairman Brendan Carr. “Today’s successful auction generated billions of dollars in competitive bids to put spectrum to effective commercial use, and it bolsters competition in the wireless marketplace. We will carry this momentum forward as we prepare for the Upper C-Band auction in the year ahead.”

“Up to $3.3B of the auction’s proceeds will be used to cover amounts borrowed to support the FCC’s “rip and replace” program and other Commerce Department programs,” said the FCC press release. “The auction made available 200 spectrum licenses in the 1695-1710 MHz, 1755-1780 MHz, and 2155-2180 MHz bands which were subject to bid defaults or bid withdrawals in the 2014 auction and thus have remained unused in the FCC’s inventory since then.”

………………………………………………………………………………………………………………………………………………………………………………..

Let’s examine how cellular network operators are navigating the fundamental physics of RF propagation:

As 5G networks transition from initial deployment to hyper-dense optimization, Auction 113 highlights a widening divergence in network architecture strategies: Verizon’s aggressive pursuit of premium urban capacity versus T-Mobile’s tactical rural densification.

The Physics of the Premium: Why Verizon Paid Up for AWS-3

To the casual observer, Verizon’s multi-billion-dollar bet on AWS-3 (operating in the 1.7 GHz uplink / 2.1 GHz downlink bands) seems redundant given their massive 2021 C-band (3.7 GHz) holdings. However, looking at the link budget reveals that all mid-band spectrum is not created equal.

[1.7 GHz / 2.1 GHz (AWS-3)] ---> Lower Path Loss, Better Indoor Penetration

[3.7 GHz (C-Band)] ---> Higher Path Loss, Requires High Node Density

By securing AWS-3 blocks in high-density markets like New York, Boston, and Chicago, Verizon is solving a specific structural challenge in urban network topology:

- Free-Space Path Loss (FSPL): Operating at 1.7/2.1 GHz provides a significant propagation advantage over 3.7 GHz. According to the Friis transmission equation, signal attenuation increases with the square of the frequency. Moving from 3.7 GHz down to 1.7 GHz yields a theoretical path loss improvement of nearly 6 to 7 dB, drastically extending the effective cell radius.

- Building Penetration Indices: Higher-frequency C-band signals suffer from severe attenuation when interacting with concrete, low-E glass, and brick. AWS-3 signals possess longer wavelengths that penetrate urban building envelopes far more effectively, reducing the reliance on costly indoor small-cell deployments.

- Offloading the Core: Rather than burning valuable C-band capacity on edge-case indoor users with degraded Signal-to-Interference-plus-Noise Ratios (SINR), Verizon can utilize the AWS-3 layer to maintain robust, high-throughput indoor links, preserving the 3.7 GHz layer for line-of-sight macro capacity.

For RF engineers tracking the convergence of terrestrial and non-terrestrial networks (NTN), the most intriguing data point from Auction 113 was SpaceX’s calculated acquisition of two specific licenses—including the Gulf of Mexico footprint—for $8.5 million. This move offers critical clues regarding SpaceX’s Direct-to-Cell (D2C) Starlink framework. Fresh off its multi-billion-dollar spectrum onboarding from EchoStar, SpaceX is systematically hunting for terrestrial frequencies that can act as a safety valve. Winning the Gulf of Mexico AWS-3 block allows SpaceX to establish a seamless, interference-free maritime D2C testing ground. This block can bridge terrestrial terrestrial networks and satellite-to-phone links without violating the strict aggregate interference power-flux-density (PFD) limits imposed near land borders.

Engineering the Transition: Funding “Rip and Replace”:

Beyond network topology, Auction 113 serves a vital national security engineering mandate. Up to $3.3 billion of the auction’s proceeds are legally earmarked to fill the funding shortfall for the FCC’s Secure and Trusted Communications Networks Reimbursement Program.

For hundreds of regional and rural operators, this influx of capital directly funds the complex hardware migration away from legacy, non-compliant Huawei and ZTE cellular access networks. Engineers are replacing proprietary, single-vendor base stations with modern, Open RAN-ready or fully compliant Ericsson, Nokia, and Samsung network infrastructure—effectively rewriting the physical layer of rural American telecom.

Conclusions:

Auction 113 proves that even in an era dominated by software-defined networking and cloud-native cores, physical layer mechanics dictate market value. Verizon’s $3.16 billion investment confirms that superior propagation characteristics and favorable link budgets still command a premium. As carriers race to deliver uniform 5G performance indoors and out, AWS-3 remains an elite tier of wireless real estate where engineering reality justifies the corporate price tag.

References:

https://www.telecoms.com/spectrum/verizon-was-the-big-spender-at-the-aws-3-spectrum-auction

https://www.fierce-network.com/wireless/verizon-emerges-biggest-winner-aws-3-auction

Federal Communications Commission, “Auction of Advanced Wireless Services (AWS-3) Licenses Closes; Winning Bidders Announced for Auction 113,” FCC Public Notice (DA-26-633), Jun. 26, 2026. Available: FCC Official Document Announcement

M. Alleven, “Verizon emerges as biggest winner in AWS-3 auction,” Fierce Network, Jun. 29, 2026. Available: Fierce Network Article

F. Rayal, “Big Carriers Get Selective: Lessons from the $3.57 Billion AWS-3 Auction 113,” Frank Rayal Telecom Insights, Jun. 28, 2026. Available: Frank Rayal Strategic Analysis

G. Winslow, “FCC Raises $3.5 Billion in AWS-3 Wireless Auction,” TV Tech, Jun. 24, 2026. Available: TV Technology Regulatory Report

Reuters, “U.S. spectrum auction raises $3.5 billion, will fund replacing Chinese telecom equipment,” Yahoo Finance, Jun. 23, 2026. Available: Yahoo Finance / Reuters Coverage

SatNews Publishers, “$3.57 Billion Milestone: FCC Advanced Wireless Services (AWS-3) Spectrum Auction Concludes,” SatNews Space & Satellite Media, Jun. 24, 2026. Available: SatNews Auction Summary

Morningstar Equity Research, “US Telecom: Verizon Shells Out $3 Billion for Spectrum as SpaceX Treads Lightly,” Morningstar Investor, Jun. 29, 2026.

FT: SpaceX considering Starlink Direct-to-Consumer mobile service & terrestrial cellular network infrastructure in the U.S.

According to the Financial Times (FT), SpaceX is evaluating a strategic expansion of its Starlink satellite Internet service to include a direct-to-consumer mobile service in the United States, a move that could materially disrupt the established U.S. mobile network market. According to sources familiar with recent IPO roadshow discussions, President and COO Gwynne Shotwell indicated that the company is considering both a retail Starlink mobile offering and the potential development of a terrestrial cellular network infrastructure.

Such a shift would represent a transition from SpaceX’s current wholesale and partnership-driven model—where Starlink satellite capacity is integrated with incumbent MNO networks—to a vertically integrated retail service directly competing with Verizon, AT&T, and T-Mobile. To date, Starlink’s U.S. mobility strategy has primarily relied on enabling partner operators, notably T-Mobile, to extend coverage in underserved and rural areas via satellite augmentation.

Although commercial terms remain undisclosed, industry analysts infer that Starlink currently participates in revenue-sharing arrangements tied to satellite-enabled service tiers. A direct retail model would enable SpaceX to capture a larger share of end-user revenue while reducing dependence on intermediary operators.

……………………………………………………………………………………………………………………………………………………………………………………………….

Here are some details, as reported by Reuters:

-

SpaceX already offers direct-to-cell connectivity with T-Mobile in the U.S., providing supplemental coverage from space to extend internet access to remote areas. [1.]

-

SpaceX is now considering launching a Starlink retail product and could build its own terrestrial U.S. mobile network, President Gwynne Shotwell told investors during a recent IPO roadshow, the FT report said, citing sources.

-

Reuters could not immediately verify the report. SpaceX did not immediately respond to a Reuters request for comment outside regular business hours.

-

In September last year, SpaceX bought wireless spectrum licenses from EchoStar for its Starlink satellite network for about $17 billion and then again for $2.6 billion in November, giving it the ability to quickly create a strong and affordable direct-to-cell service by using EchoStar’s wireless airwaves.

-

SpaceX will disrupt the $1.6 trillion U.S. communications industry as its satellite broadband unit Starlink expands, brokerage firm Oppenheimer said in a note earlier this month.

-

SpaceX’s record valuation is grounded in Starlink, which has over 10 million subscribers, and a launch business that analysts and investors say has transformed access to orbit.

Note 1. T-Mobile US D2D service has lower than expected usage:

During T-Mobile US’s recent earnings call, CEO Srini Gopalan admitted that just under a year after its commercial launch, T-Satellite is experiencing lower-than-predicted usage. However, he put a very positive spin on the situation, insisting that the technology is doing exactly what it was designed for.

“Our partnership with SpaceX is very strong. We’ve worked closely with them to really invent an entire category, and that’s been putting an end to dead zones. We’re pleased with that,” Gopalan said.

“Most of the usage we’re seeing is in national parks and if anything, courtesy of the great network Dr Saw has built, we’re seeing a lot less usage than we were originally thinking,” he admitted, referring to Chief Technology Officer John Saw. “But it’s a great complementary product.”

……………………………………………………………………………………………………………………………………………………………………………………………….

SpaceX Satellite Launch using Falcon 9 Rocket. Image Credit: Space Center Houston

This potential expansion follows SpaceX’s recent IPO, which has intensified investor expectations for accelerated revenue growth and diversification. Starlink already operates in more than 150 countries, delivering broadband services via LEO satellite constellations, with approximately 10.3 million global subscribers as of March. A U.S. mobile retail offering would significantly expand its addressable market beyond fixed satellite broadband.

Importantly, SpaceX has not publicly confirmed plans to launch a retail mobile service. However, speculation has increased following its $17 billion acquisition of wireless spectrum licenses from EchoStar in September, widely interpreted as a foundational step toward mobility services. In its bond prospectus, the company noted that while Starlink Mobile is currently expected “to be most impactful for customers in remote areas uncovered by terrestrial mobile networks,” its long-term positioning is more expansive, stating it would “compete to be the preferred connectivity experience to our customers no matter where they are located, whether in rural, suburban or urban areas.”

Despite the strategic rationale, significant technical and economic barriers remain. U.S. MNOs collectively control approximately 1,020 MHz of spectrum, compared to SpaceX’s estimated 65 MHz, according to New Street Research. This disparity highlights the challenges associated with scaling a competitive terrestrial mobile network, particularly in spectrum-constrained and highly saturated markets.

David Barden of New Street Research emphasized the difficulty of such an undertaking, noting that building a “wireless network in saturated markets around the world would be incredibly hard.” However, he added that “[But,] as a starting point for negotiating the best possible revenue-sharing deal with mobile network operator partners? It makes tremendous sense.”

Conclusions:

While a Starlink retail mobile service offering could redefine the company’s role in the telecom value chain, near-term implementation would likely require a hybrid model leveraging both satellite and terrestrial assets, alongside continued strategic partnerships with incumbent operators.

The most useful follow-on question is whether “terrestrial cellular network infrastructure” means acquiring spectrum, building or buying towers, or simply partnering for access and backhaul. If it means an owned network, the economics look very different from satellite direct-to-device: capital spend rises, time-to-scale slows, and the business starts competing head-on with Verizon, AT&T, and T-Mobile instead of complementing them. If it means a hybrid model, then the more plausible path is a bundled satellite-plus-terrestrial offering targeted at coverage gaps, mobility, and emergency connectivity rather than a nationwide full replacement.

The strategic significance of the FT report is not simply another Starlink service tier, but a possible shift from supplemental coverage provider to vertically integrated U.S. mobile operator, with major implications for spectrum policy, carrier competition, and infrastructure investment.

……………………………………………………………………………………………………………………………………….

References:

https://www.ft.com/content/42af0f15-3aa9-49b7-b429-4a39540af03e?syn-25a6b1a6=1 (paywall)

Ookla: Starlink a viable competitor for hybrid 5G/NTN services due to network performance improvements and larger coverage area

Ookla: D2D satellite connectivity surged 24.5% during last 9 months; Starlink’s footprint expansion leads the way

US Mobile’s new bundle combines its multi-network mobile service with Starlink residential internet

Tutorial: LEO Satellite Internet connectivity, D2D, and major providers

Direct-to-Device (D2D) satellite network comparison: Starlink V2 (Starlink Mobile) vs “Satellite Connect Europe”

Starlink doubles subscriber base; expands to to 42 new countries, territories & markets

Elon Musk: Starlink could become a global mobile carrier; 2 year timeframe for new smartphones

GEO satellite internet from HughesNet and Viasat can’t compete with LEO Starlink in speed or latency

U.S. BEAD overhaul to benefit Starlink/SpaceX at the expense of fiber broadband providers

Telstra selects SpaceX’s Starlink to bring Satellite-to-Mobile text messaging to its customers in Australia

SpaceX launches first set of Starlink satellites with direct-to-cell capabilities

Blue Origin announces TeraWave – satellite internet rival for Starlink and Amazon Leo

Assessing LPWANs for IoT: NB-IoT, 4G LTE versions, 5G Redcap and LoRa WAN

Introduction – LPWANs (Low Power Wide Area Networks):

In April 2011, Cisco soothsayer Dave Evans predicted there would be 50 billion IoT devices in the world by 2020. Yet in 2025, there were only 22.3 billion IoT devices worldwide, according to the Ericsson Mobility Report. Evans forecast was off by 27.7 billion five years after the date for the 50 billion to be realized (2020). The real shocker was just how few of those devices used cellular networks for connectivity – 4.5 billion (again, Ericsson is the source). To add insult to injury, between 600 and 700 million of those cellular IoT connections used much older 2G and 3G systems, according to a chart in Ericsson’s Mobility report. The rest were split between what Ericsson calls “massive” IoT [NB-IoT]-and a separate category of broadband and critical IoT [5G RedCap, LTE Cat-1 and Cat-1 bis standards].

LoRaWAN, which exclusively uses unlicensed sub-gigahertz radio frequency spectrum, was not included in the Ericsson report, but is analyzed in this article (see LoRaWAN subhead below).

Narrow Band IoT (NB-IoT):

NB-IoT was first introduced in 3GPP Release 13 in June 2016. 3GPP Release 18 & 19 (2024–2026) provided physical layer enhancements for NB-IoT NTN, focusing on uplink capacity expansions and time-division duplex (TDD). Also, NB-IoT is included in the ITU-R M.2150 5G RIT/SRIT standard. According to the Ericsson report, NB-IoT accounted for only 1.3 billion IoT connections last year. Most are in China, where the government appears to have mandated rollout of NB-IoT to support Huawei, one of the technology’s original backers. In mid-2024, Omdia analysts, said that China was responsible for 90% of all NB-IoT connections worldwide! Regarding NB-IoT, Japan’s NTT Docomo switched off an NB-IoT network in 2020. AT&T decommissioned its NB-IoT network last year, saying it preferred LTE Cat-M.

NB-IoT still has meaningful deployments in Europe and other regions, especially in utilities and smart-metering, and roaming partnerships have improved its prospects. Omdia also reported that NB-IoT and LoRa together dominated LPWAN connections, with NB-IoT’s growth driven heavily by China but still expanding elsewhere. So the technology itself is alive; the issue is that its non-China commercial traction has been much weaker than its original promise.

The main problem was not radio performance so much as ecosystem economics. Outside of China, carriers often did not price NB-IoT aggressively enough for low-ARPU sensor use cases, and the lack of seamless roaming made global deployments harder than they needed to be. In practice, that left LoRaWAN with a freer runway in many regions, especially for private networks. In conclusion, NB-IoT has been a commercial underperformer outside China, but not a dead LPWAN. Its non-China adoption has been real but fragmented, while China became the scale engine that kept the standard commercially relevant.

Image Credit: Emnify

4G LTE Versions for IoT:

- LTE Cat 1 / Cat 1 bis: For medium-speed IoT (10 Mbps) like telematics, e-bikes, and POS terminals.

- LTE Cat M1 (LTE-M): For low-power, mobile IoT (1 Mbps) supporting voice and firmware updates.

5G RedCap:

As with earlier forms of IoT, one of the big problems with 5G RedCap (5G reduced capability) is module pricing. Any IoT connection generates far less in revenues than any smartphone, and component prices must also be sufficiently low for connecting large volumes of objects to be economical. Even if RedCap is reserved for higher-end devices, such as the Apple Watch, the hardware for it remains too expensive, according to Omdia. In a research note emailed this week, it complains that “adoption has been limited by high module prices.” Omdia says the real constraint is the slow rollout in some countries of 5G SA, without which RedCap won’t work. Numerous mobile network operators (MNOs) have not even launched 5G SA, explaining the displeasure of Ericsson’s CEO. While take-up is especially low in Europe, it is also down at 50% in the U.S., compared with 98% in China, according to Ericsson’s Ekholm.

A new report on 6G by the NGMN Alliance, a club of prominent telcos said, “It should be noted that some MNOs may struggle to identify clear value to migrate to 5G SA, after initially deploying 5G NSA.” Omdia has a much gloomier outlook for IoT than Ericsson. The Swedish vendor currently forecasts the overall number of cellular IoT connections will grow to 7.8 billion by 2031. Omdia does not expect the figure to reach 5.9 billion until 2035, by which stage 6G networks are likely to have been in commercial operation for some five or six years.

……………………………………………………………………………………………………………………………………………..

Proprietary LPWANs Using Unlicensed Spectrum:

1. Sigfox pioneered the concept of LPWANs for IoT. It was founded in 2009 by French entrepreneurs Ludovic Le Moan and Christophe Fourtet in Labège, near Toulouse, France (an area later dubbed “IoT Valley”). While the telecom industry chased high-speed 4G LTE and WiMax, Sigfox did the exact opposite. They built a lightweight protocol optimized for extremely tiny, infrequent messages (just 12 bytes per upload). This allowed endpoints to be extraordinarily cheap and operate on a single battery for over a decade. Sigfox adopted a “top-down” model. It acted as a global network operator, partnering with local companies (Sigfox Operators) to build physical cell towers worldwide. Starting in 2019, Sigfox faced intense competition from LoRaWAN (which offered an open, decentralized model where companies could build private networks) and cellular standards like NB-IoT and LTE-M, which were backed by massive telecom operators. In 2022, the firm filed for bankruptcy protection, before its assets were acquired by Singapore’s UnaBiz.

However imperfect, its business model was at least geared to IoT, which is not the case for nearly every mainstream mobile network operator (MNO). Financial reports from some major telcos have shown IoT contributing as little as 1% or 2% of total service revenues. When the returns are so minuscule, the commercial incentive remains weak.

2. LoRaWAN has been a success in its target markets, though it is not a universal mass-market wireless technology. A February 2026 LoRa Alliance report says LoRaWAN reached 125 million deployed devices globally, grew at a 25% CAGR, and is now used at scale in utilities, smart buildings, agriculture, and critical infrastructure. The evidence points to sustained adoption rather than a one-off technology spike. The LoRa Alliance says the ecosystem reached 360 members, surpassed 625 certified devices, and supports multi-million-device networks from multiple operators and vendors. Its 2024 report also cites more than 350 million end nodes and 6.9 million gateways with LoRa ICs deployed worldwide, plus use by major brands such as Starbucks, Volvo, Chevron, Chick-fil-A, and Logitech.

- LoRaWAN appears strongest in low-power, long-range, intermittent-data use cases. The 2025 report says utilities remain the largest vertical, smart buildings are a leading segment, and NTN/satellite-enabled.

- LoRaWAN is now commercially available from three service providers. That pattern suggests strong product-market fit for massive IoT, not for high-throughput consumer connectivity.

“Success” depends on the benchmark. If the bar is “won the IoT LPWAN market and built a durable ecosystem,” then yes; if the bar is “became a giant mainstream telecom platform,” then no. Independent commentary has also noted that some LoRaWAN companies have had uneven revenue growth and market acceptance even as deployments expanded.

In conclusion, LoRaWAN has been a commercial success in LPWAN/IoT, especially for private and enterprise deployments, but it remains a specialized niche rather than a broad consumer-wireless winner. The biggest adoption difference is that LoRaWAN has tended to win in private, operator-independent deployments, while NB-IoT has tended to win where carrier coverage and cellular integration matter. LoRaWAN adoption is often driven by enterprises, municipalities, and industrial users building their own networks or using community/public LoRa networks, whereas NB-IoT adoption is usually tied to mobile operators and SIM-based service models.tektelic+2

Here is a compact adoption-oriented comparison (Source: Google Gemini):

Here is a ranking for number of connections / scalability across LPWANs, using publicly available vendor/whitepaper comparisons. Because these systems are designed differently, this is best read as a relative ranking, not a single absolute device-count limit (Source: Perplexity.ai)

From Iain Morris, International Editor, Light Reading:

With 6G slowly approaching, the market is still held back by high module prices, inadequate coverage and support, and technological bewilderment, as the options continue to mushroom. Adoption is unsurprisingly not at the level that cellular IoT’s enthusiasts likely hoped for years ago. Yet the 6G story, paradoxically, seems to be all about new device types, from smart glasses to humanoids and other such physical AI.

Hence talk in Ericsson’s latest Mobility Report of a “supercycle, an unusually strong multi-year upgrade wave” that will carry smart glasses and other “connected physical AI device form factors” with it. Chipset vendors, says Ericsson, “are interested in being in the next generation from the start.”

All this, however, sounds a world apart from the humdrum IoT of smart meters and temperature sensors. The connected humanoid or AI drone must look more exciting and potentially lucrative to the average big telco hunting for sales growth in a saturated smartphone market. If telcos can extract service fees from consumers for smart glasses, they will prioritize that over anything in LPWA.

Much of the IoT probably didn’t, doesn’t and won’t ever need 4G, 5G or 6G, explaining the delta between the overall number of connections and the cellular quantity in Ericsson’s report. By 2031, Ericsson thinks we’ll have 47.1 billion total connections, including 38.8 billion that use short-range technologies such as Bluetooth, ZigBee and good old Wi-Fi. The farm of the average AgBot owner might enjoy ubiquitous 6G by then, making the vehicle even more versatile. For the far less dazzling stuff that might benefit from cellular, the risk is of ending up forgotten.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

References:

https://www.lightreading.com/iot/the-internet-of-things-was-5g-s-big-fail-6g-risks-a-repeat

https://www.emnify.com/developer-blog/evaluating-nb-iot-and-lte-m-part1

LoRaWAN® Enters Its Next Growth Phase as Massive IoT Scales Globally

From LPWAN to Hybrid Networks: Satellite and NTN as Enablers of Enterprise IoT – Part 2

Enterprise IoT and the Transformation of UK Telecom Business Models – Part 1

GSA: 102 Network Operators in 52 Countries have Deployed NB-IoT and LTE-M LPWANs for IoT

5G Americas: LTE & LPWANs leading to ‘Massive Internet of Things’ + IDC’s IoT Forecast

LoRaWAN and Sigfox lead LPWANs; Interoperability via Compression

Semtech LoRa® PHY technology enables Amazon Sidewalk to expand while supporting fixed and mobile IoT endpoints

TM Forum’s DTW Ignite 2026: Open Digital Architecture (ODA); Nokia, Ericsson, IBM and Mavenir AI announcements/cloud partnerships

-

- Shift to Action: TM Forum Vice President Aaron Boasman-Patel and CEO Nik Willetts opened the summit emphasizing that the industry must move past abstract C-suite visions.

- The AI Economy: The flagship keynote officially launched the “Race to 2030,” a direct directive tasking operators to secure their market relevance by deploying high-velocity, production-grade architectures.

-

- On-Stage AI Co-Hosts: In an industry event first, agentic AI systems took the stage alongside human moderators to act as live panel co-hosts, digital analysts, and experts.

- Summit Intelligence Layer: Advanced AI systems recorded and indexed every keynote, panel, and breakout session, functioning as a real-time intelligence layer to deliver daily trend summaries to attendees.

-

- Autonomous Networks (AN): Featuring the largest showcase of live autonomous operating systems to date. Major case studies from carriers like China Mobile, China Telecom, TDC NET, and Telefónica showcased functional solutions for self-optimizing networks, RAN energy efficiency, and fast fault resolution.

- Trustworthy AI and Data: Discussions zeroed in on scaling responsible AI, exploring Models-as-a-Service (MODaaS) frameworks, managing tokenomics, and reinforcing cyber resilience.

- Composable IT and Ecosystems: Demonstrations focused on scaling Open Digital Architecture (ODA) from boardroom design into functional, interoperable engineering realities.

Practical Engineering & Showcases:

- Catalyst Showcases: The exhibition floor hosted over 60 collaborative proof-of-concept Catalyst projects and Innovation Engine live demonstrations.

- New Interactive Hubs: The event debuted dedicated “Mission Garages” for hands-on engineering collaboration, along with a specialized Future Skills program to help tech teams adapt to AI-native workflows. [1]

- Major Tech Partnerships: Industry titans—including IBM, Ericsson, Cisco, and Nokia—used the floor to debut subsea infrastructures, physical AI, and cloud-native automation frameworks.

Note 1. DTW Ignite 2026 is TM Forum’s flagship global connectivity event focused on accelerating AI-native telcos, autonomous networks, and composable IT. The event is from June 23 to June 25 at the Bella Center in Copenhagen, Denmark.

……………………………………………………………………………………………………………………………………………………………….

At the show, the TM Forum and its member alliance of over 850 companies across 180 countries, announced a major structural evolution for the Open Digital Architecture (ODA), shifting it from a cloud-native IT modernization blueprint into an AI-native execution environment. The core focus of these updates is to establish standardized, executable reference frameworks that allow operators to move beyond fragmented AI pilots and build an autonomous enterprise. The primary ODA updates and structural expansions announced at the summit include:

-

- Governed Execution Layer: TM Forum members launched AI-native extensions to the ODA specification, adding a governed execution layer. This allows autonomous AI agents and large language models to run natively within the existing ODA component architecture and Open APIs.

- Project Foundation & AI Canvas: Through the Demo ONE Catalyst project, tech leaders debuted an updated AI-Native ODA Canvas. This cloud-native runtime environment orchestrates data, AI models, and autonomous agents across fragmented BSS, OSS, and network domains to replace rigid legacy systems.

- Model-as-a-Service (MODaaS): To solve the challenge of rising token costs and fragmented model selection, an ODA-aligned MODaaS framework was introduced. It establishes a unified control plane to govern, secure, and manage AI model usage across the carrier architecture.

-

- Space-Telco Interoperability: In a major scope expansion, TM Forum officially launched the ODA for Satellite project. Supported by 16 foundational partners—including Airbus, Terrestar, and Vodacom—the initiative targets multi-billion dollar direct-to-device and space-connectivity markets.

- Unified Non-Terrestrial Frameworks: The project extends standard ODA components to satellite technology providers, standardizing how terrestrial mobile networks and non-terrestrial networks (NTNs) handle cross-industry billing, service delivery, and zero-touch roaming integrations.

- Plug-and-Play Validation: TM Forum rolled out its newly expanded ODA Component Certification. This toolkit gives vendors a programmatic way to verify that their commercial software components are truly plug-and-play ready, lowering custom integration costs for telecom buyers.

- “Running on ODA” Milestones: The alliance celebrated that 18 global Communication Service Providers (CSPs), representing over two billion subscribers globally, have officially achieved “Running on ODA” accreditation—confirming that modular, componentized architecture has reached full scale in production environments.

……………………………………………………………………………………………….

Vendor Announcements:

- Amazon Web Services (AWS) Expansion: Nokia and AWS expanded their partnership to run Nokia’s Autonomous Networks Fabric natively on AWS. The integration brings operators closer to Level 4 network autonomy, enabling networks to orchestrate, analyze, and heal themselves at machine speed.

- Google Cloud Integration: Nokia deepened its alliance with Google Cloud to integrate Gemini models into the Nokia Assurance Center. They unveiled six specialized generative AI agents (including a Router Agent and Event Triage Agent) to automatically process data and isolate the root causes of service faults. It launches as a SaaS offering in September 2026.

- Databricks Proof of Concept: Nokia and Databricks announced the completion of a joint project showing a unified, cloud-agnostic data platform. This resolves a legacy pain point by unifying hundreds of fragmented operational silo data architectures so multi-agent AI can run seamlessly across networks.

- GenAI-Native Operations: Instead of relying on traditional rules-based code, Nokia’s new interfaces allow field engineers to query complex multi-vendor topologies, generate diagnostic code, and run natural-language root-cause analyses on real-time traffic faults.

- Autonomous Network Scaling: Nokia presented multi-party Catalyst project solutions targeting network optimization, zero-touch slicing, and automated enterprise edge deployments tailored for the 5G-Advanced landscape.

……………………………………………………………………………………………………………………………………………………….

- EIAP Core Expansion: The headline announcement from the Ericsson Cloud Software and Services division was the expansion of the Ericsson Intelligent Automation Platform (EIAP). Formerly restricted to RAN operations, the platform now fully integrates and unifies Radio Access Network (RAN) and core network automation systems.

- Introduction of cApps: Ericsson claimed a major industry first by rolling out core-specific automation applications (cApps). These decentralized apps allow operators to run automated routines directly on core architectures, streamlining cross-domain workflows to cut operations costs.

- Business Value Pathways: Ericsson debuted a structured strategic blueprint designed to guide Communication Service Providers (CSPs) through the financial steps of scaling from Level 3 to Level 4 autonomous networks.

…………………………………………………………………………………………………………………………………………………….

- Addressing the “AI Trust Gap”: Responding to a TM Forum study revealing that only 14% of operators can prove their AI systems are fully reliable, IBM presented framework tools at DTW Ignite to address security and model bias.

- B2B2X Monetization: IBM focused its platform showcase on orchestrating automated workflows for multi-enterprise B2B2X networks, enabling secure data federation across third-party hyperscalers and edge servers.

……………………………………………………………………………………………………………………………………………………

- Telco-First Cloud Architecture: Stationed at Booth 334, Mavenir debuted its updated AI-by-design, cloud-native software portfolios built natively around TM Forum’s Open Digital Architecture (ODA) frameworks.

- Closed-Loop Automation: Mavenir demonstrated actionable frameworks that handle real-time resource adjustments, shifting power and processing capacity across base stations based on AI-predicted user demand cycles.

……………………………………………………………………………………………………………………………………………………

References:

https://www.tmforum.org/events/dtw/experience-dtw/new-for-2026

Inside TM Forum’s Catalyst project “Living Networks – Phase III”

Deloitte and TM Forum : How AI could revitalize the ailing telecom industry?

The Financial Trap of Autonomous Networks: Scaling Agentic AI in the Telecom Core

GSMA, ETSI, IEEE, ITU & TM Forum: AI Telco Troubleshooting Challenge + TelecomGPT: a dedicated LLM for telecom applications

SHIELD-6G with AI-native cyber threat intelligence platform to enhance cybersecurity for Europe’s future 6G networks

Verizon’s 6G Innovation Forum joins a crowded list of 6G efforts that may conflict with 3GPP and ITU-R IMT-2030 work

Private 5G networks move to include automation, autonomous systems, edge computing & AI operations

Ericsson integrates Agentic AI into its NetCloud platform for self healing and autonomous 5G private networks

SNS Telecom & IT: Private 5G Market to Reach $6.6 Billion as Physical AI Takes Hold

Private 5G networks are transitioning from limited-scale deployments to a more material segment of the wireless infrastructure market. SNS Telecom & IT estimates that annual spending on private 5G networks will exceed $6.6 billion by 2029, driven by multi-site and multi-national enterprise rollouts supporting industrial automation, “physical AI” systems, and mission-critical communications across both commercial and public-sector domains.

Historically, private cellular deployments remained a niche market during the 2G/3G era, with notable exceptions such as GSM-R for railway communications. The introduction of private LTE in the early 2010s established a foundation for dedicated enterprise connectivity; however, adoption remained constrained by performance limitations and ecosystem maturity. The evolution to 3GPP-defined 5G NPN architectures—both standalone (SNPN) and public network-integrated (PNI-NPN)—is now enabling broader applicability across industrial verticals, with a trajectory that exceeds prior-generation adoption levels. Concurrently, legacy systems such as GSM-R are expected to transition toward 5G-based FRMCS implementations aligned with 3GPP specifications.

From a technical perspective, 5G introduces capabilities that are better aligned with industrial communication requirements than LTE. Enhanced mobile broadband (eMBB), ultra-reliable low-latency communications (URLLC), and massive machine-type communications (mMTC) collectively support higher throughput, sub-10 ms latency targets, improved reliability, and significantly greater device densities. These characteristics enable 5G NPNs to address use cases traditionally served by wired Ethernet or deterministic industrial networks, particularly in scenarios requiring mobility and flexible topology. Additional attributes—including improved coverage per radio node, network slicing, time-sensitive networking (TSN) integration, and enhanced security mechanisms—position private 5G as a viable alternative to interference-prone unlicensed technologies in dense IIoT environments.

Deployment momentum is increasingly visible across manufacturing, logistics, energy, and transportation sectors. Production-grade implementations have demonstrated measurable operational benefits, including reduced downtime, improved safety, and expanded coverage in previously unconnected areas. A common pattern involves the migration of AGV and AMR connectivity from Wi-Fi to private 5G, enabling more deterministic performance and reduced susceptibility to interference. In parallel, private 5G is extending connectivity to challenging industrial zones where wired infrastructure is cost-prohibitive or operationally restrictive. Emerging use cases also include coordinated robotics and edge-controlled automation systems, often described as “physical AI,” where low-latency and reliable connectivity are critical for closed-loop control.

In the public-sector domain, private 5G is gaining traction for mission-critical communications. Applications span defense, public safety, railways, and utilities, where requirements include high availability, secure communications, and support for MCX services (mission-critical push-to-talk, video, and data). The evolution toward 5G-Advanced, as defined in 3GPP Releases 18 through 20, introduces further enhancements relevant to these deployments, including support for reduced channel bandwidth operation in dedicated spectrum, expanded frequency bands, and specific feature sets aligned with FRMCS and mission-critical service requirements.

Geographically, adoption is concentrated in markets with established industrial bases and supportive regulatory frameworks, including North America, Europe, and parts of Asia-Pacific. As enterprises scale digitalization initiatives—encompassing automation, AI-driven operations, and connected workforce applications—private 5G deployments are increasingly moving beyond pilot phases to multi-site, production-grade networks.

SNS Telecom & IT projects a compound annual growth rate of approximately 34% for private 5G investments between 2026 and 2029. Growth is expected to be led by localized enterprise and campus networks, alongside parallel expansion in mission-critical infrastructure. The combination of maturing 3GPP standards, improving device ecosystems, and demonstrated operational benefits is positioning private 5G as a foundational connectivity layer for next-generation industrial and public-sector systems.

References:

https://www.snstelecom.com/private5g

GSA: Global private mobile networks exceed 2,000 worldwide; Ericsson Private 5G from Verizon Business extends beyond U.S.

Private 5G networks move to include automation, autonomous systems, edge computing & AI operations

SNS Telecom & IT: Mission-Critical Networks a $9.2 Billion Market

SNS Telecom & IT: Private 5G Market Nears Mainstream With $5 Billion Surge

SNS Telecom & IT: Private 5G and 4G LTE cellular networks for the global defense sector are a $1.5B opportunity

OneLayer Raises $28M Series A funding to transform private 5G networks with enhanced security

Verizon partners with Nokia to deploy large private 5G network in the UK

AI-Era Cloud Network Transformation: A Reference Architecture and Implementation Roadmap

By Shazia Hasnie, PhD

Introduction:

The physical network infrastructure that underpins cloud computing was designed for an era that no longer exists. Distributed training across hundreds of thousands of GPUs, real-time inference at the edge, and autonomous agent coordination impose requirements that traditional cloud network designs were never intended to meet. The networks that served the cloud era were architected for north-south traffic, best-effort delivery, and human-scale applications. None of these assumptions hold for AI.

This article presents a framework for transforming cloud network infrastructure for the AI era. It is organized around two components: a four-pillar reference architecture that defines what must be built, and a five-phase implementation roadmap that defines how to execute the transformation. Together, they provide infrastructure transformation leaders with a complete program for preparing their organizations’ physical network infrastructure for the age of AI.

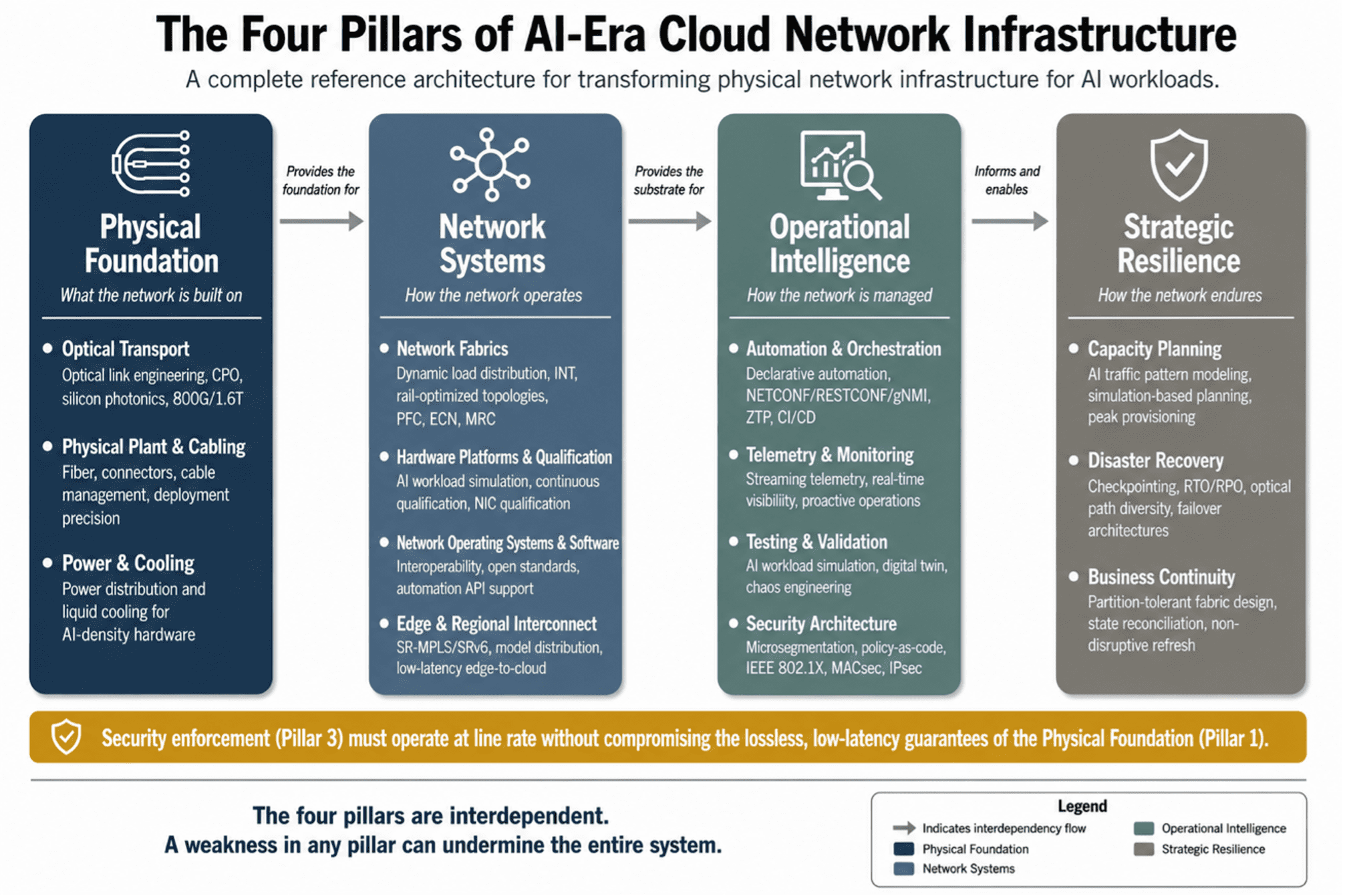

The Four-Pillar Reference Architecture:

The physical network infrastructure for AI-era cloud computing is organized around four interdependent pillars. Each pillar groups related layers of the infrastructure stack. Each depends on the pillars that precede it and enables the pillars that follow.

Figure 1: The Four Pillars of AI-Era Cloud Network Infrastructure — a complete reference architecture for physical network transformation.

PILLAR 1: PHYSICAL FOUNDATION

The physical foundation is the literal infrastructure on which all higher-layer network services depend. Optical transport determines the bandwidth, latency, and reliability of every interconnection between data centers, regions, and compute clusters. Physical plant and cabling provide the fiber, connectors, and cable management that make connectivity possible. Power and cooling provide the electrical and thermal infrastructure that keeps everything running.

Optical Transport. Optical link engineering for AI workloads requires a fundamental shift from traditional practice. Traditional optical link engineering treats traffic surges as anomalies and provisions for average utilization. AI workloads generate synchronized, high-bandwidth bursts—checkpointing incast can saturate multiple optical links for minutes at a time—that demand link budgets engineered for peak synchronized demand. The cost of insufficient capacity is not degraded optical performance; it is stalled training runs.

The optical technology roadmap is being reshaped by AI requirements. Co-packaged optics (CPO) integrate the optical engine directly with the switch ASIC, reducing power consumption by 30-50% while increasing port density. Silicon photonics leverage semiconductor manufacturing to produce optical components at scale. 800G and 1.6T per wavelength will be required as GPU bandwidth scales. Linear drive optics remove the digital signal processing from the optical transceiver, reducing power and latency. Breakout optics enable multi-planar topologies where each GPU connects to multiple parallel fabrics. Organizations must ensure that today’s optical investments are forward-compatible with these technologies.

Physical Plant and Cabling. Deployment precision at the physical layer determines whether the architectures designed at higher layers function as intended. Rail-optimized topologies depend on perfect physical cabling—a single miscabled port breaks the single-hop guarantee. Automated cabling verification, where the management interface validates each connection against the reference design, has reduced deployment time by up to 90% for early adopters. Continuous monitoring must detect cabling degradation before it causes performance issues.

Power and Cooling. AI network hardware consumes significantly more power than traditional cloud hardware. A rack of switches populated with 800G pluggable optics can consume over 10 kilowatts. CPO engines may require direct-to-chip liquid cooling. The transition to liquid cooling has implications that extend beyond the network—chilled water systems, heat rejection, building structural load—and retrofitting liquid cooling into a data center designed for air cooling is significantly more expensive than incorporating it into new construction.

PILLAR 2: NETWORK SYSTEMS

Network systems translate the physical foundation into functional network services. Modern data centers operate multiple physical networks—front-end, back-end, storage—each optimized for a specific traffic class. AI training demands a dedicated high-bandwidth, low-latency fabric for GPU-to-GPU communication that must interoperate with existing networks through well-defined interconnection points.

Network Fabrics. AI workloads generate east-west traffic that behaves differently from anything traditional cloud networks were designed to handle. It is dominated by a small number of high-bandwidth elephant flows—sustained, predictable data streams between GPU pairs—that produce synchronized bursts at predictable intervals. Worst-case path latency determines the completion time for collective communication operations, making the performance of the slowest path more important than average performance.

The industry has developed two distinct architectural paths to meet these requirements. For scale-up networks within a single rack or GPU pod, where distances are measured in meters and the cost of a stall is immediate, lossless transport via Priority-Based Flow Control (PFC) and Explicit Congestion Notification (ECN) remains the dominant approach. For scale-out networks connecting GPU clusters across data center halls or buildings, the industry is moving toward efficient utilization with low tail latency through fast recovery rather than absolute loss prevention. The Ultra Ethernet Consortium’s Ultra Ethernet Transport (UET) specification leads this effort, treating packet loss as a recoverable event rather than a failure.

The choice between paths is governed by three criteria: scale of deployment (≤256 GPUs favors lossless; ≥512 GPUs favors low-loss), workload characteristics (tightly coupled training benefits from lossless; loosely coupled inference tolerates low-loss), and organizational maturity (deep PFC expertise extends lossless viability to larger scales).

Four fabric capabilities support both paths. Dynamic load distribution—flowlet switching and packet spray—replaces static Equal Cost Multi-Path (ECMP) with congestion-aware path selection. In-band network telemetry (INT) provides the microsecond-granularity congestion visibility that makes intelligent load distribution possible. Rail-optimized topologies provide single-hop GPU-to-GPU connectivity for the most latency-sensitive collective operations. Advanced transport protocols, add selective retransmission via SACK and NACK that serves both scale-up and scale-out deployments.

Hardware Platforms and Qualification. Hardware must be qualified under AI workload conditions, not standard benchmarks. A switch that performs well under steady-state testing may exhibit unacceptable packet loss under synchronized burst patterns. The qualification process must answer a specific question: will this hardware maintain performance under the traffic patterns that AI workloads generate? Qualification is continuous—a firmware update, a new optics module, or a configuration change can alter behavior and must be validated before reaching production. The endpoint NIC plays a critical role, handling RDMA at line rate, packet-spray reordering, and selective retransmission. NIC qualification must be part of the same AI workload simulation process as switches and optics.

Network Operating Systems. The NOS must support PFC, INT, dynamic load distribution, and automation APIs. Interoperability is an architectural requirement in inherently multi-vendor AI infrastructure. Organizations should prioritize platforms that adhere to open standards—UET specifications, IETF YANG data models, OpenConfig—over proprietary extensions that create long-term supply chain constraints.

Edge and Regional Interconnect. AI inference increasingly occurs at the edge, requiring low-latency connectivity to cloud reasoning agents. Traffic engineering via Segment Routing over MPLS (SR-MPLS) and SR over IPv6 (SRv6) enables explicit path specification for latency-sensitive flows. Model distribution to edge endpoints requires versioned, efficient distribution protocols. Regional interconnect must be treated as a production input, not a shared utility—it is part of the AI supercomputer’s backplane.

PILLAR 3: OPERATIONAL INTELLIGENCE

Operational intelligence provides the control systems that make the network operable at scale. The AI-ready network cannot be managed through manual processes—a single AI cluster may contain thousands of switches requiring consistent configuration, where a single misconfigured buffer can stall thousands of GPUs.

Automation and Orchestration. The architectural response is declarative intent-based automation. The operator declares the desired network state using IETF YANG data models, and the automation framework translates this into device-level configuration via NETCONF, RESTCONF, and gNMI. Zero-touch provisioning enables switches to self-configure from the moment of installation. Configuration-as-code ensures every device conforms to architectural standards, with drift detected and corrected automatically. Network changes move through CI/CD pipelines that validate against policy and test under AI workload conditions before production deployment.

Telemetry and Monitoring. INT captures per-packet, per-path metrics at microsecond granularity. Streaming telemetry replaces polled monitoring with continuous, event-driven data push. The telemetry platform must ingest, store, and analyze millions of data points per second, enabling cross-layer correlation—tracing a GPU-level stall back through the fabric to the specific optical port and wavelength where the loss occurred. Predictive models detect performance degradation before it causes packet loss, shifting operations from reactive to proactive.

Testing and Validation. A dedicated testing environment must replicate production AI workload patterns—synchronized bursts, collective communication operations, checkpointing incast. Fault injection and chaos engineering validate network behavior under failure conditions. A digital twin of the production network, continuously synchronized, within a bounded delay, with real-time telemetry, enables what-if analysis for topology changes, capacity additions, and configuration updates before production deployment.

Security Architecture. Distributed AI dissolves the traditional network perimeter. The architectural response is in-fabric security: microsegmentation at the switch level validates every flow at the point of ingress, policy is bound to workload identity rather than network location, and the enforcement architecture relies on IEEE 802.1X, MACsec, and IPsec. Policy-as-code manages security rules through the same CI/CD pipelines as network configuration. The immutable audit trail serves double duty as both the security record and the compliance record.

PILLAR 4: STRATEGIC RESILIENCE

Strategic resilience ensures the network survives disruptions, scales with demand, and sustains itself over the long term.

Capacity Planning. Traditional capacity planning, based on historical averages and steady-state utilization, systematically underprovisions for AI. AI traffic is bursty, synchronized, and high-volume by design. Capacity must be provisioned for peak synchronized demand. Simulation-based planning models proposed network designs under projected AI workloads, identifying bottlenecks in the design phase before hardware is committed.

Disaster Recovery. AI training runs lasting weeks or months cannot be restarted from scratch. The network must support checkpointing at AI scale, with Recovery Time Objectives (RTO) and Recovery Point Objectives (RPO) defined per workload. The optical backbone must provide physically diverse paths with automatic protection switching. Failover architectures—active-active or active-passive—must be designed at the network level for inference workloads requiring high availability.

Business Continuity. The network fabric must tolerate WAN partitions without cascading failures, with local control planes capable of independent operation at each site. State reconciliation architecture—based on the shared event log pattern—must preserve causal ordering across partition boundaries. The network must support non-disruptive infrastructure refresh, with redundant paths and hitless failover enabling component replacement without interrupting workloads that run continuously for weeks or months.

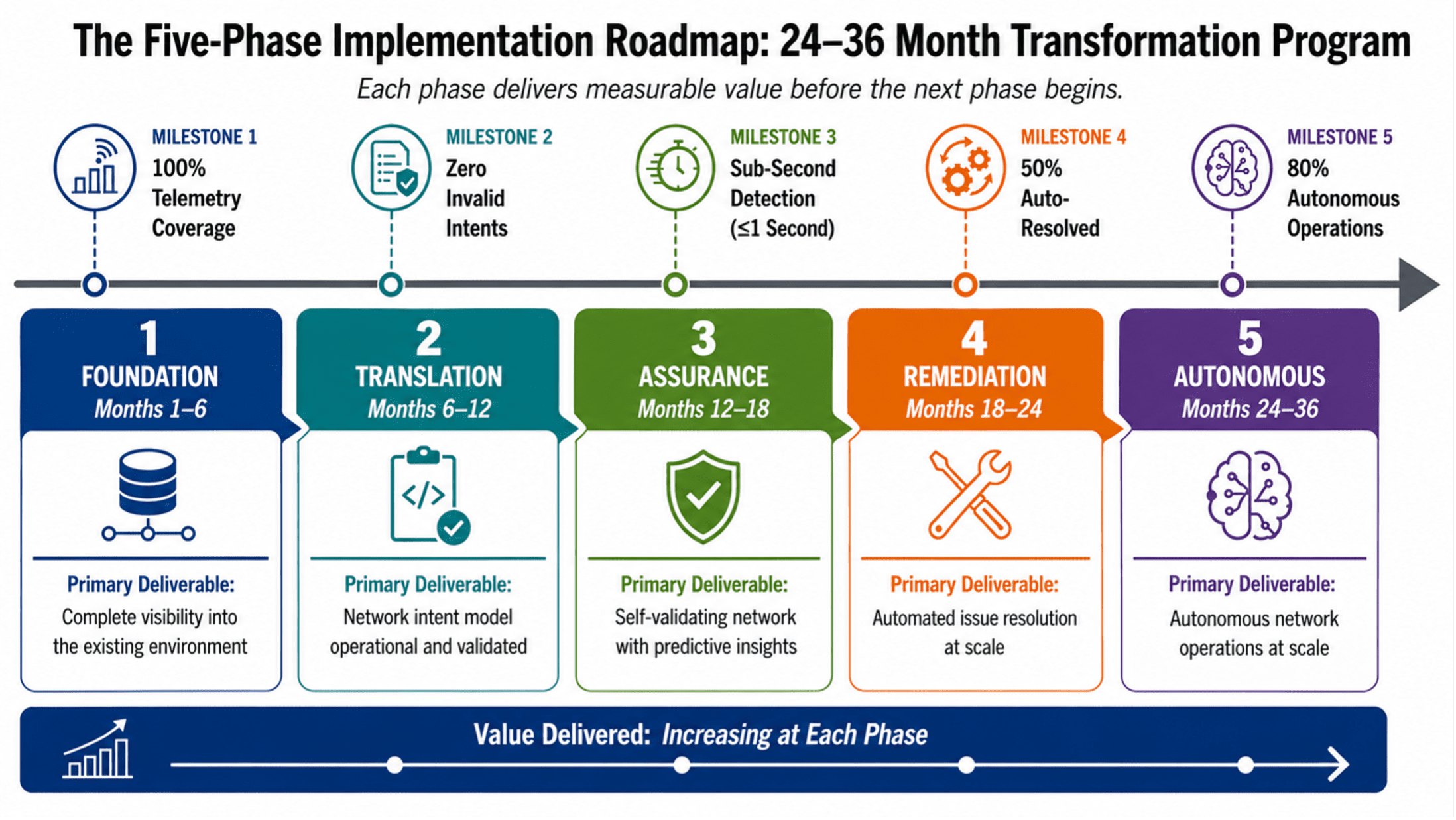

The Five-Phase Implementation Roadmap

The migration from legacy to AI-ready network infrastructure is a multi-phase program that must deliver value at each stage while building toward the target architecture. Each phase has defined activities, deliverables, and success criteria. Each phase delivers measurable value before the next begins. Phase durations are calibrated for a Tier-1 cloud services provider; individual organizational timelines may vary based on scale, complexity, and resource availability. The success criteria stated for each phase are drawn from industry benchmarks and practitioner experience with large-scale network transformation programs. They represent targets that are ambitious but achievable for a Tier-1 cloud services provider with dedicated transformation resources and executive sponsorship.

Figure 2: The Five-Phase Implementation Roadmap — A 24–36 Month Transformation Program.

PHASE 1: FOUNDATION (MONTHS 1–6)

The first phase establishes the essential building blocks. Nothing can be automated, optimized, or secured until the network is instrumented and its state is understood.

The starting point is telemetry. Streaming telemetry must be enabled across all network devices in the AI infrastructure path—switches, optics, fabric elements—using gRPC-based protocols and OpenConfig YANG data models. The deliverable is a centralized telemetry platform receiving continuous data streams from every device. The success criterion is 100% telemetry coverage. Without complete visibility, every subsequent phase operates on incomplete information.

With telemetry flowing, a topology knowledge graph must be built—a dynamic map of all devices, links, and interconnections, continuously updated from telemetry data and discovery protocols. The graph must reflect topology changes within seconds, not minutes. Accurate neighbor discovery across all fabric layers is the foundation on which intent-based automation will reason about the network.

Configuration management must be brought under version control. Every device configuration—PFC thresholds, QoS policies, dynamic load distribution parameters—must be stored in version-controlled repositories. Every change must be tracked and attributed. The success criterion is 100% configuration version control with no out-of-band changes permitted. An automation framework that deploys configuration changes cannot operate reliably if changes are also being made through manual processes that bypass the automation pipeline.

Finally, the foundational intent model must be established. This is a structured format for expressing network intent—topology, capacity, QoS policies—in machine-readable YANG-based models. The deliverable is five foundational intents, defined and validated against the existing network state:

- Lossless Transport Intent: “All Remote Direct Memory Access over Converged Ethernet (RoCE) traffic on the AI fabric shall receive PFC priority treatment with zero packet loss under sustained load.”

- Fabric Capacity Intent: “The AI fabric shall maintain a minimum of 30% headroom on all east-west links during peak utilization.”

- Optical Link Diversity Intent: “Every GPU cluster shall have at least two physically diverse optical paths to its checkpoint storage.”

- Configuration Compliance Intent: “All device configurations shall match version-controlled templates. Any deviation shall be detected and flagged within 60 seconds.”

- Telemetry Coverage Intent: “Every device in the AI network path shall stream telemetry data. Any device that stops streaming shall be flagged within 30 seconds.”

These five intents are scoped to be achievable within Phase 1 while covering the most critical dimensions of AI network operations: lossless transport, capacity, resilience, configuration compliance, and observability.

PHASE 2: TRANSLATION (MONTHS 6–12)

The second phase builds the machinery that translates intent into device-level configuration. This is where declarative automation becomes operational.

The centerpiece is the intent compiler—a translation engine that converts YAML or JSON intent specifications into device-level configuration via NETCONF, RESTCONF, and gNMI. The intent compiler is not merely a template engine. It must understand the capabilities and constraints of each target device, select the appropriate protocol for each configuration operation, and handle the transactional semantics that make configuration changes safe. The success criterion is that the five foundational intents from Phase 1 are compiled and deployed without manual intervention.

Before any compiled configuration reaches production, it must be validated in a digital twin—a virtual replica of the AI network, continuously synchronized with production telemetry. The digital twin enables what-if analysis: if this configuration is applied, what happens to fabric utilization, PFC pause events, and flow completion times? The success criterion is 100% of configuration changes validated in the digital twin before production deployment.

Validation checks must be automated. Every intent must pass feasibility validation (can the network support this intent given current capacity?), capability validation (do the target devices support the required features?), and policy validation (does this intent comply with security and operational policies?). The success criterion is zero invalid intents deployed to production.

Multi-domain support must be enabled. The intent compiler must support both data center fabric and optical backbone domains, translating a single intent into coordinated configurations across domains.

PHASE 3: ASSURANCE (MONTHS 12–18)

The third phase closes the loop between intent and reality. The network may be configured correctly at a point in time, but AI workloads cause continuous change—congestion patterns shift, optical performance degrades, buffer utilization fluctuates. Assurance ensures the network remains in its intended state.

Real-time telemetry monitoring must track SLA compliance for all AI network services, updated continuously from streaming telemetry rather than periodically from polled data. Sub-second detection latency for SLA deviations is the success criterion. A RoCE stall that lasts 500 milliseconds must be detected while it is happening, not after the training run has been disrupted.

Drift detection must compare the intended network state against the actual state continuously. Drift can take many forms: a configuration change applied outside the automation pipeline, a performance degradation that violates the intent without changing the configuration, a topology change due to a link failure. The success criterion is 99% detection accuracy for both configuration and performance drift.

The assurance dashboard must provide all stakeholders—network operations, compute operations, capacity planning—with real-time visibility into network state versus intent. Alerting must be integrated with the incident management system so that 100% of SLA breaches generate alerts within one second of detection.

PHASE 4: REMEDIATION (MONTHS 18–24)

The fourth phase enables the network to respond to drift and failures. Detection without response is observation without action. Remediation closes the loop.

Root cause analysis (RCA) must be automated. When drift is detected, the system must correlate telemetry data across layers—optical, fabric, device—to identify the source. A packet loss event at the GPU layer may originate from a congested optical link three hops away. The RCA engine must trace the event across layers. The success criterion is greater than 80% accuracy for common incident types.

At least three remediation types must be implemented and validated in the digital twin before production enablement: rollback to the last known good configuration, traffic rerouting around congested or failed links, and dynamic QoS adjustment.

A policy engine must govern which remediation actions are fully automated, which require human approval, and which are prohibited. The policy framework must be machine-readable, version-controlled, and enforced at the automation layer. The success criterion is 100% of automated remediation actions comply with defined policies.

Supervised remediation must enable a human-in-the-loop approval workflow for actions that exceed the automated threshold. The goal is that 50% of detected issues are resolved automatically without human intervention, with the remainder escalated for approval.

PHASE 5: AUTONOMOUS (MONTHS 24–36)

The final phase extends over 12 months—longer than the preceding phases—because full autonomy is not a single deployment event. It requires progressive expansion of automation scope, validation of continuous optimization across diverse workload patterns, and accumulation of sufficient operational data for the learning system to deliver meaningful accuracy improvements. Each increment of autonomy must be earned through demonstrated reliability.

The automation scope must be expanded to cover all common incident types identified and validated in Phase 4. The success criterion is that 80% of all incidents are resolved automatically. The remaining 20% represent novel failures, complex multi-domain incidents, or situations where policy requires human judgment.

Continuous optimization must become a background process. The network self-tunes PFC thresholds based on observed congestion patterns, adjusts dynamic load distribution policies as workload distributions shift, and reallocates buffer resources as traffic characteristics evolve. The success criterion is a 20% reduction in SLA violations compared to the Phase 3 baseline.

Cross-domain coordination must achieve full automation for standard intents. When a new GPU cluster is provisioned, the orchestration layer coordinates optical link provisioning, fabric configuration, and security policy establishment across domains without manual intervention. Human involvement is reserved for novel or high-risk changes.

The learning system must improve from experience. Machine learning models trained on historical incident and remediation data must increase root cause analysis accuracy over time. The success criterion is a 10% quarterly improvement in RCA accuracy.

COEXISTENCE: RUNNING LEGACY AND AI-READY NETWORKS IN PARALLEL

The transformation cannot be accomplished through a flag-day cutover. The existing cloud network must continue to operate and generate revenue throughout the transition. The AI-ready network is deployed as a separate physical infrastructure—dedicated optical links, dedicated fabric, dedicated switches—wherever possible. Physical separation eliminates the risk that AI workload traffic patterns will disrupt legacy services. Where physical separation is impractical, logical isolation with strict QoS enforcement provides the necessary workload separation. Interconnection points between the two networks must be engineered with the same packet loss, latency and throughput requirements as the AI-ready network. Operational processes must govern both environments simultaneously during a transition measured in years.

ORGANIZATIONAL TRANSFORMATION

The AI-ready network cannot be operated by a team trained only on legacy network operations. Three new skill domains become critical: AI workload literacy (understanding the traffic patterns and failure modes of distributed training and inference), telemetry and data engineering (building and operating streaming telemetry platforms and correlation engines), and automation engineering (designing and operating intent-based automation and CI/CD pipelines). The talent strategy must balance retraining existing engineers—many of the required skills are extensions of existing knowledge—with external hiring for skills that cannot be developed internally in the required timeframe. Retention of critical talent during the transformation is essential: the engineers who understand the legacy infrastructure are essential to the coexistence strategy.

FINANCIAL MODELING

Network investment for AI must be justified on value generation—the network cost per training run completed, per inference served, per GPU-hour utilized—not traditional cost efficiency metrics. This shift from cost-per-bit to value-per-outcome transforms the investment conversation. A network that costs more per gigabit but enables higher GPU utilization generates a return that far exceeds its cost premium. The five-phase roadmap enables investment to be spread over 24 to 36 months, with each phase delivering measurable value before the next begins. The cost of inaction must be quantified and presented alongside the cost of transformation.

CONCLUSIONS:

The physical network is no longer a utility layer that can be taken for granted. It is the foundation on which AI performance depends. The optical backbone determines whether GPU clusters operate at full utilization or sit idle. The network fabric determines whether distributed training completes in days or weeks. The automation and telemetry infrastructure determines whether issues are detected proactively or discovered after customer impact.

The four-pillar reference architecture defines what must be built. The five-phase implementation roadmap defines how to execute the transformation. Together, they form a complete program for infrastructure transformation leaders.

The technologies described here are deployed and operational in production AI networks today. The challenge for infrastructure leaders is not whether these approaches work, but how to adapt them to their organization’s specific constraints, scale, and timeline.

REFERENCES:

[1] TM Forum, “Autonomous Networks: Business Requirements and Framework,” TM Forum IG1251, 2025. [Online].

[2] AMD, “Next Gen Networking Transport for Large Scale AI Training,” May 2026. [Online].

htt

[3] Tolly Group, “Dell Networking Data Center AI Switch Fabric Congestion Mitigation Evaluation,” April 2026. [Online].

[4] Tech Field Day, “Cisco AI Networking Cluster Operations Deep Dive,” November 2025. [Online].

htt

[5] Akamai / WWT, “East-West Is the New North-South: Rethink Security for the AI-Driven Data Center,” February 2026. [Online]. htt

[6] NIST, “Zero Trust Architecture,” NIST Special Publication 800-207, Aug. 2020. [Online].

[7] IETF, “Network Configuration Protocol (NETCONF),” RFC 6241, June 2011. [Online].

[8] IETF, “RESTCONF Protocol,” RFC 8040, January 2017. [Online]. htt

[9] IEEE, “Priority-based Flow Control,” IEEE Standard 802.1Qbb, 2011.

[10] IEEE, “Congestion Notification,” IEEE Standard 802.1Qau, 2010.

[11] OpenConfig, “OpenConfig: Vendor-Neutral Network Configuration and Telemetry,” [Online]. https://www.

[12] Cloud Native Computing Foundation, “gRPC: A High-Performance, Open Source Universal RPC Framework,” [Online]. https://grpc.io/

[13] Ultra Ethernet Consortium, “Ultra Ethernet Specification,” [Online]. https://

………………………………………………………………………………………………………………………………………………………….

References from IEEE Techblog:

Why Batch Pipelines Break AI Agents: The Case For Streaming-First Network Operations

The enterprise network stack is collapsing; AI’s impact; comparison with “Batch Pipelines Break AI Agents”

ABOUT THE AUTHOR:

Shazia Hasnie, Ph.D., is VP Product Strategy and Innovation at Cuber AI, focused on Agentic Network Operations. Her work explores the intersection of autonomous systems, cloud-native infrastructure, and the economic models that make AI operations sustainable at scale. She brings over 20 years of global experience in communications networks and holds a Ph.D. in Communications Engineering from the Australian National University.

AI-RAN and Agentic AI get real: Ericsson, Nokia, Verizon & other operators enter into a new network automation era

Disclaimer: Perplexity.ai was used for research in this article.

Executive Summary:

A cluster of announcements in early-to-mid June 2026 signals a real shift from AI research to commercial AI-driven network automation. Telcos are transitioning from isolated AI pilots to production-grade AI operations deployed across live networks.

-

Ericsson launched its AI in RAN commercial software subscription on June 11th, claiming up to 20% higher downlink throughput and up to 10% better spectral efficiency across more than 15 live deployments using existing baseband silicon.

-

Nokia and Indosat Ooredoo Hutchison (Indonesia) announced a GPU-accelerated AI-RAN partnership in Indonesia on June 8, expanding the Nokia–NVIDIA architecture already adopted by T-Mobile US, SoftBank, and Vodafone.

-

Verizon disclosed that its 60,000-site vRAN is now applying agentic AI to planned configuration changes, service assurance, and network optimization, while publicly calling for industry-wide interoperability standards for agentic systems.

-

Nokia launched an agentic AI framework for IP network operations within its Network Services Platform (NSP), marking its third agentic product announcement in a four-week period.

A growing number of network operators are transitioning from traditional connectivity providers into AI infrastructure operators. SK Telecom (South Korea) announced a gigawatt-scale AI Cloud built on NVIDIA DGX SuperPOD architecture; Deutsche Telekom (Germany) secured the German federal government’s sovereign AI cloud contract; and MTN Group (South Africa) detailed a plan to convert 18,000 African tower locations into a distributed AI inference grid.

Over a six-week window, six major network operators—SK Telecom, Deutsche Telekom, MTN Group, Verizon, SoftBank, and Indosat Ooredoo Hutchison—have converged on a single strategic premise: existing telecommunications infrastructure, including connectivity, physical real estate, and data center capacity, constitutes the foundational footprint for a commercial AI compute business.

………………………………………………………………………………………………………………………………………………………………………………………………

Government’s Buys Into AI Compute:

Government involvement in AI compute is intensifying, with direct implications for telecom strategy. China’s $295 billion program defines the upper bound of state-backed AI compute investment. Beijing announced plans to invest 2 trillion yuan ($295 billion) over five years in AI datacenter infrastructure. China Mobile and China Telecom are designated as the primary operators of a national AI compute network, while Huawei will supply the majority of AI chips—explicitly bypassing NVIDIA. The plan accelerates China’s original 2030 national computing network target to 2028, funded through sovereign debt.