Téral Research: 5G SA core network deployments accelerate after a very slow start

5G deployments started with the non-standalone (NSA) mode (using a 4G core network) and are now gradually migrating to Stand Alone (SA) core network to unleash a plethora of use cases. 5G SA offers improved latency and bandwidth, enabling advanced services and applications. 5G SA features a new sophisticated service-based architecture (5G SBA) developed by the 3GPP. Although many of the network functions (NFs) featured in the 5G SBA come from existing ones currently active in 2G/3G and 4G networks, novel functions such as the network slice selection function (NSSF) are being introduced.

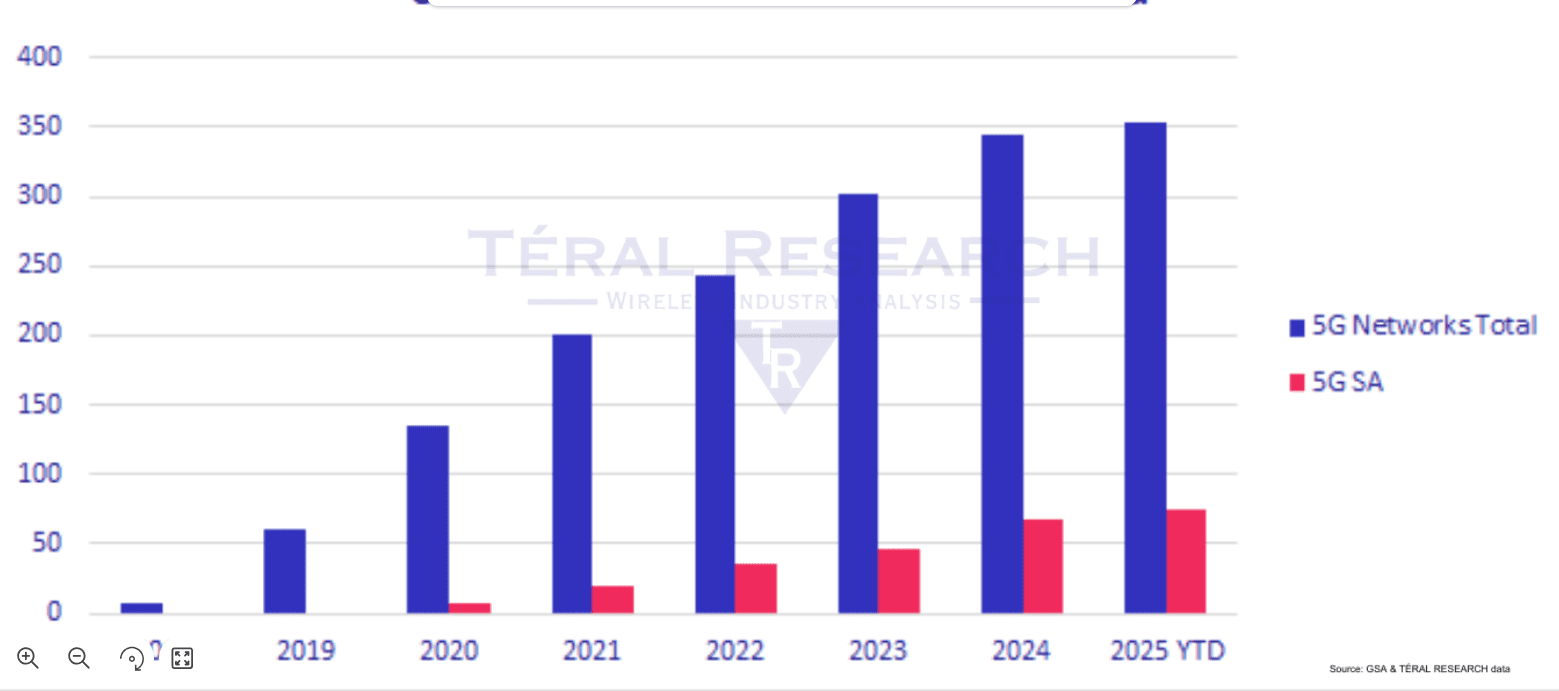

After a very slow start during the past five years, Téral Research [1.] says the migration to 5G SA has increased. Of the total 354 commercially available 5G public networks reported at the end of 1Q25, 74 are 5G SA – up from 49 one year ago. This growth is being driven by the success of fixed wireless access (FWA), a wider range of 5G SA-compatible devices, and the rise of voice over new radio (VoNR). Téral is also seeing increased adoption of private cloud for SA core deployments, with data sovereignty concerns shaping CSP strategies. Network slicing, which requires 5G SA, is moving from theory to practice—now extending to critical use cases like military applications.

Huawei, Ericsson, Nokia, and ZTE Corporation continue to lead the vendor landscape, but with more than 550 networks yet to migrate, the 5G SA Core market is only beginning to scale. With 20% growth expected this year, the next phase of 5G is officially underway.

Note 1. Based on a communications service provider (CSP) survey and discussions with many vendors, Téral Research’s 5G SA report analyzes several of the 5G Core SBA functions and provides global and regional market sizes and forecasts by focusing on the NFs implemented by CSPs (e.g., UDM, UDR, AUSF, NRF, NEF and NSSF, PCF, BSF, CHF) to enable use cases beyond enhanced mobile broadband (eMBB), fixed wireless access (FWA), and private 5G.

……………………………………………………………………………………………………………………………………………………………………..

2024 had the highest number of 5G SA commercial launches: 21 networks went live to offer commercial 5G SA services last year. The success of FWA services, the introduction of smartphone plans enabled by the increasing number of available 5G SA devices, and the rise of VoNR drove this SA migration.

Key findings include:

-

Network slicing is taking off for various services, including for military use cases.

-

The single vendor approach remains predominant for each domain.

-

67% of 5G SA core deployment are cloud-based but due to data sovereignty concerns,

CSPs favor private cloud infrastructures.

-

The global 2024 market for 5G SA Core + SDM + Policy & Charging grew 12% YoY and hit $3.8B, slightly below our forecast.

-

Sustained by its domestic market, Huawei leads global 2024 sales for 5G SA Core + SDM + Policy & Charging, followed by Ericsson and Nokia, respectively. However, Nokia leads the global commercial 5G SA footprint. ZTE comes in fourth place for global total sales and second for 5G SA core sales behind Huawei.

In the meantime, technical challenges related to 5G network architecture complexity, 3GPP methods for exchanging information across 4G vs. 5G, policy orchestration and enforcement, real-time analytics and insights and data analytics are still lingering but being solved.

Built on a solid CSP pipeline of 559 cellular networks in the world that have yet to be migrated to 5G SA, Téral’s model produced a forecast that shows the global 5G SA Core/5G Data Management/5G Policy market to cross the $4B bar by year-end, which is 20% YoY growth. Last year’s downward revision put our forecast on track and therefore we have not made any significant change in this forecast update.

……………………………………………………………………………………………………………………………………

Editor’s Note: In 2025, about a dozen more mobile network operators (MNOs) are expected to deploy 5G Standalone (SA) networks, according to Fierce Network and Moniem-Tech. This will include some major CSPs like AT&T and Verizon, who have previously deployed 5G SA on a limited basis. ……………………………………………………………………………………………………………………………………

In the long run, Teral foresees a significant ramp up in CSPs’ migration to 5G SA that adds to the ongoing activity continuously fueled by the emergence of new use cases going beyond eMBB, FWA, and private 5G. Therefore, Téral expects the market to grow at a 2025-2030 CAGR of 11%. Asia Pacific will remain the largest market throughout the forecast period and 5G SA core the most important domain to start with, followed by 5G Data Management.

Finally, the disaggregated multi-domain nature of 5G core SBA brings a broad range of contenders that include the traditional telecom network equipment vendors, a few mobile core specialists, a handful of subscriber data management (SDM) specialists, a truck load of policy and charging rules function (PCRF) players, the OSS/BSS providers and the system integrators and providers of IT services.

References:

Téral Research :: June 2025 5G SA Core, SDM and Policy

Ookla: Europe severely lagging in 5G SA deployments and performance

Vision of 5G SA core on public cloud fails; replaced by private or hybrid cloud?

GSA: More 5G SA devices, but commercial 5G SA deployments lag

Building and Operating a Cloud Native 5G SA Core Network

Latest Ericsson Mobility Report talks up 5G SA networks and FWA

Global 5G Market Snapshot; Dell’Oro and GSA Updates on 5G SA networks and devices

Dell’Oro: Mobile Core Network market has lowest growth rate since 4Q 2017

5G SA networks (real 5G) remain conspicuous by their absence

One thought on “Téral Research: 5G SA core network deployments accelerate after a very slow start”

Comments are closed.

From Heavy Reading:

5G standalone (SA) deployments are becoming more widespread, but identifying the services potential for 5G SA remains a challenge. While 5G SA provides the opportunity to access new or better 5G services, such as RedCap and network slicing, service providers continue to grapple with how best to package 5G SA services and communicate the value of 5G SA to consumers and enterprise customers.

Gabriel Brown of Heavy Reading likens the difference between 5G non-standalone and 5G SA to driving a 20-year-old car in good condition to a newer model vehicle. Or, using a five-year-old iPhone versus the iPhone 16. In both cases, the older model will do the job required but there’s a stark difference in the features of the latest model.

“You’re not going to notice a few milliseconds of difference on your phone but I think incrementally we’re going to see basically better service,” says Brown.

The big Chinese (state owned) network operators and T-Mobile have been running 5G SA at scale for years, he adds. In addition, Reliance Jio in India is running a huge 5G SA network and has ten network slice types available in commercial operations, and EE in the UK has reached 50% population coverage for 5G SA. There’s plenty of evidence that 5G SA deployments at scale are doable so that supports a forecast of broader adoption, Brown.

In Heavy Reading’s 2025 5G SA Core Operator Survey, 35% of respondents said 5G SA is already generally available nationwide in their company’s wide area network, and 20% said it would be generally available by the end of the year.

During the podcast, Brown also explains the difference between 5G SA and 5G Advanced.

https://www.lightreading.com/5g/5g-standalone-deployments-are-scaling-now-comes-the-hard-part