Uncategorized

FTTH/FTTP Update: Migration from HFC to Distributed Access Architecture for MSOs

by Jon Baldry, Director Metro Marketing at Infinera

Fibre to the Home (FTTH) or Building (FTTP) is now a very popular choice for new housing developments and business parks across the globe. Extending broadband availability and raising public expectations provides a major boost for the industry, but there is a greater challenge in regions with a well-established copper or cable infrastructure. Telcos are already stretching DSL technology to discourage customer churn. Cable too has significant territory to defend: it begins with a more powerful offering, but MSOs cannot be complacent.

QoS is the new battle cry, and Distributed Access Architecture (DAA) offers a major challenge to the spread of Fibre to the Home. The migration to DAA is inevitable, but not to be undertaken lightly. The global advance of FTTH has been dramatic, and it is expected to provide nearly 50% of all broadband subscriptions by 2022. But it is worth noting that this has been driven by exceptional uptake in certain countries, notably the Far East, where the legacy copper and cable infrastructure was less established.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

China accounts for over a third of the global broadband total, and over 70% of those connections are on FTTH. Singapore has 95% FTTH, South Korea over 80% and Hong Kong over 70% according to the Fibre Broadband Association. Compare that with Europe, with its legacy copper and cable infrastructure, where FTTH penetration is barely 10%.

Editor’s Note: Point Topic said that in 12 months to the end of Q1 2018, China added nearly 63 million FTTH connections. This figure constituted 80% of global FTTH net adds in the period.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Fibre still has a long way to go, and installation will take time in the old world with its stricter planning regulations and narrow old-town streets. What does the world want from broadband?

Expectations are changing rapidly. Optical fibre now delivers about six times the capacity that DSL can manage. There is still huge demand for downloads and streaming video and services like 4K HDTV are pushing demand way beyond the capabilities of current DSL technology. More significantly, in addition to the video demands, users also use a broad range of services such as social media, gaming and potentially, in the not too distant future, virtual or augmented reality where upload speeds and latency become much more important. Here legacy cable delivery does have a distinct disadvantage – although it has accelerated its download speeds to stay around 80% of fibre capacity, cable’s upload speeds are more like one third of what FTTH can offer. Cable was in a strong position in the days of asymmetric Internet usage, but today’s soaring demand for massive bandwidth, fast uploads, low latency and high reliability presents a serious challenge, and the industry is looking to a new Distributed Access Architecture (DAA) to meet this challenge. This is a radical move that will impact the entire system for cable multiple service operators’ (MSOs) optical networks, from “fiber-deep” access networks to support Remote PHY Devices (RPDs) to the need for enormous bandwidth scalability throughout their entire networks.

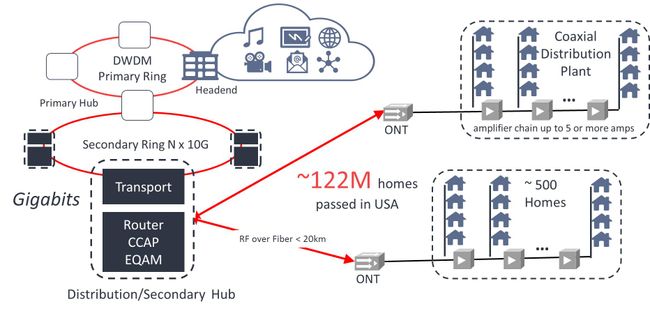

For a couple of decades cable operators have used Hybrid Fibre Coax (HFC) to connect the core to the access networks. The fibre carries the data as analogue radio frequency (RF) signals, similar to those in the coaxial access cables, rather than digital packets as in a typical fibre network like FTTH (Fig 1). This analogue infrastructure is expensive to operate and maintain. Digital signals are more tolerant of signal to noise degradation and are therefore less affected by attenuation, whereas analogue signals need a chain of power hungry amplifiers along the route to maintain signal strength and quality. This analogue technology was designed to suit earlier network requirements, which it supported well, but it cannot scale to meet today’s increasing demands.

Figure 1: The Current HFC Access Network

Figure 1: The Current HFC Access Network

Note also that each Optical Network Terminal (ONT) typically serves several hundred homes, requiring costly analogue equipment that requires considerable maintenance. With so many subscribers per node, the system struggles to support bursts in demand, slowing down delivery at those most critical times.

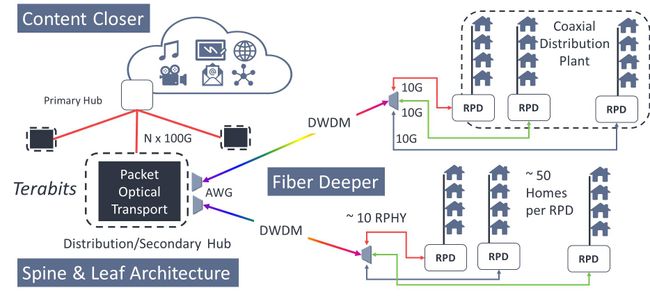

The new “fibre deep” approach pushes today’s default packet-based digital fibre technology out closer to the end point (see Figure 2). Replacing analogue channels and the older transmission protocol also frees up spectrum in the remaining shorter coaxial plant for more efficient use of capacity, enabling Full Duplex delivery so that upload speeds will be able to match download speeds. This narrows that gap between FTTH and Cable for interactive gaming, virtual reality and social media purposes – as well as increasing its potential for future Internet of Things (IoT) applications where masses of data may be uploaded from countless small devices.

Note also in Figure 2. below that increasing in the number of nodes closer to the end users means that each one serves around one tenth of the number of subscribers, and this facilitates exceptional interactive services. The cable network has for many years supported on-demand content, and the updated network architecture makes room for more locally stored content. Being closer improves responsiveness and Quality of Service (QoS), especially during peak hours. These developments will present a serious challenge to the arrival of FTTH providers, who already have to compete against an existing infrastructure and established customer base.

Figure 2: HFC to Distributed Access Architecture (DAA)

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Huge potential versus tricky demands of DAA:

Selecting suitable equipment will no longer be a simple matter of asking a preferred supplier to meet the required performance levels, it will be necessary to look closely at the specifications to see if devices are sufficiently compact and power efficient to optimise scarce secondary hub real estate and to provide additional capabilities that can address the significant operational challenges of managing such a high density aggregation. With a tenfold or so increase in the number of RPDs terminating the DWDM network, installation and operating expenses will soar unless care is taken to choose the most compact, reliable and easy to maintain equipment.

Optical equipment suppliers are aware of these concerns and are rising to the challenge of mass deployment of DAA networks. Great advancements are being made in terms for density, power consumption and addressing the operational challenges of managing potentially 1000s of fibers within a secondary hub rack. What’s more, the industry has been working to bring the International Telecommunications Union’s (ITU) vision of autotuneable WDM-PON optics up to the performance levels required to support the reach and capacity requirements of DAA networks. This eases the pressures of commissioning and maintaining extensive DWDM optical networks by replacing the technicians’ burden of determining and adjusting wavelengths at every installation. Autotuneable technology will automatically select the correct wavelength without any configuration by the remote field engineer enabling them to treat DWDM installations with the same simplicity as grey optics.

These are the sort of challenges that will be faced as MSOs migrate to DAA, and they will need to take a very close look at their choice of equipment and solutions in order to meet the very specific challenges of fibre-deep access networks. However, a successful DAA rollout is not just about what happens in the access network. DAA will also create a surge in bandwidth demand throughout the entire infrastructure – from access through transport to core. Unless steps are taken to reinforce, optimise and automate the entire network capability, the most powerful, responsive and efficient access network could become its own worst enemy.

Conclusions:

Already nearly a half of all US consumers are using streaming video services and 70% “binge watch” TV series, while virtual and enhanced reality services and 4K high definition TV are still poised to go mainstream. So future-proofing a cable MSO’s network means preparing for a highly uncertain future.

Network operators will need help from specialist optical equipment providers to optimise optical transport platforms to their specific needs, creating network architectures that will be highly scaleable, that simplify operations, accelerate the launch of new services, and minimize total cost of ownership. Something that will only be achieved by installing intelligent networks that integrate best-in-class technology and automate a significant proportion of manual operations.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………..

2Q-2018 Status & Direction of AT&T Communications, by CEO John Donovan

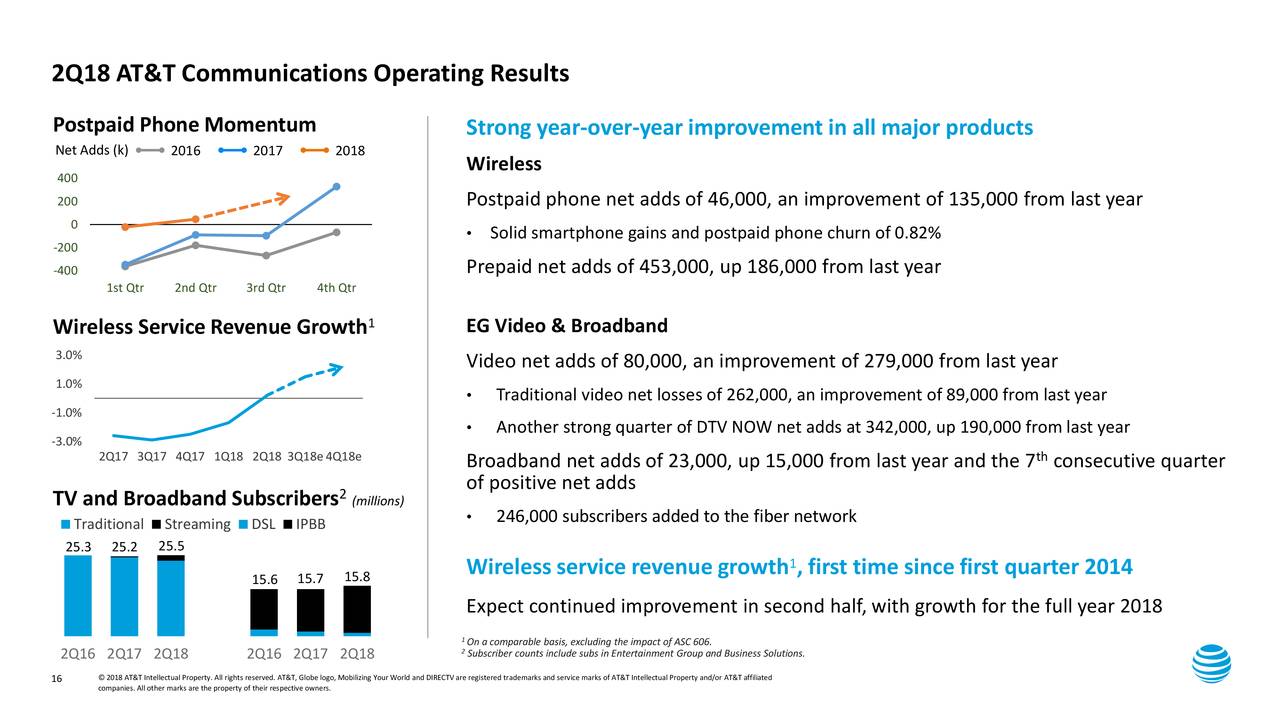

2Q-2018 for AT&T had 76,000 IP broadband net adds with 23,000 total broadband net adds. That’s the seventh consecutive quarter of broadband growth for AT&T Communications. About 95% of our consumer broadband base is now on our IP broadband as our transition from DSL is drawing to a close. Our fiber build continues at a fast clip, now passing more than 9 million customer locations, and we expect that this time next year to reach 14 million locations.

This gives us a long runway for broadband growth. We’re doing very well in our fiber markets, including a 246,000 net increase in subs on our fiber network in the second quarter.

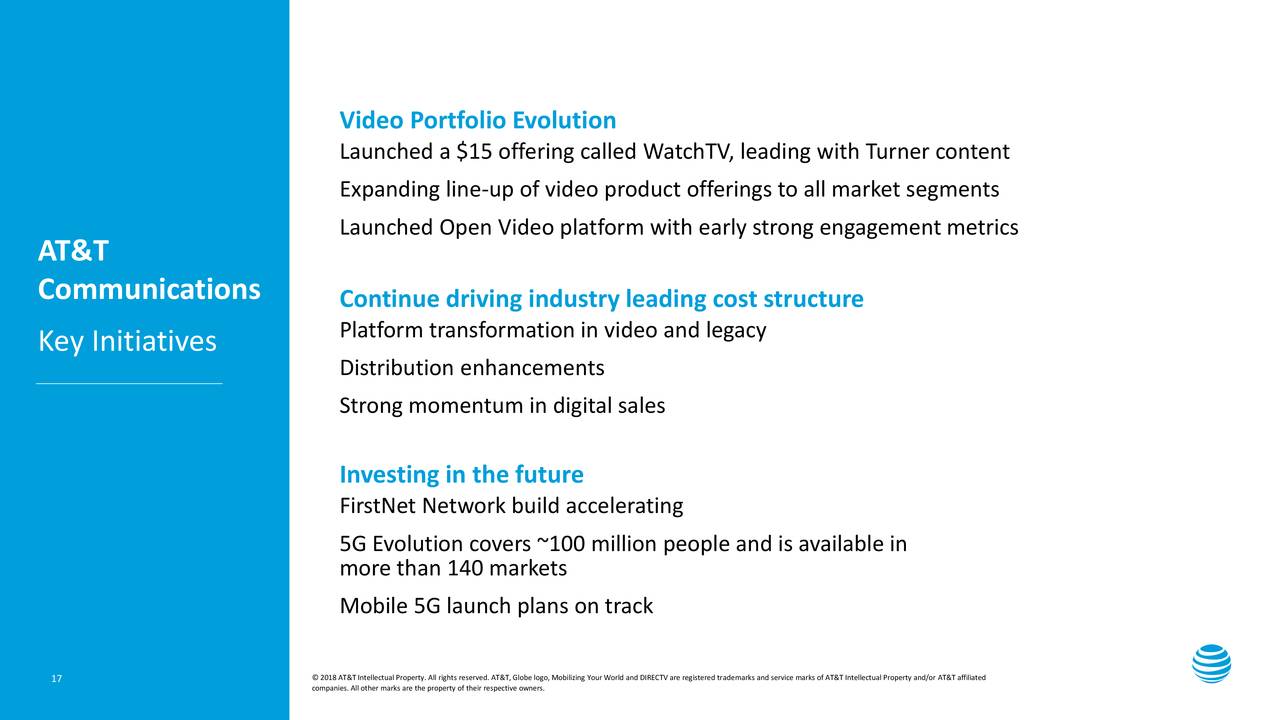

Now I’d like to update you on several key initiatives we have underway, so we’ll turn to Slide 17. Evolving our video portfolio is top priority for us. We believe we’re well positioned as our customers move toward a more personalized set of streaming products.

Our new platform was launched in May as the DIRECTV NOW user interface, and it’s now live on all supported device operating systems and has been well received with strong engagement by customers. It offers a new cloud-based DVR and more robust video-on-demand experience with new pay-per-view options. Over time, it will bring additional advertising and data insight opportunities. This new video platform gives us flexibility to adapt to the market with new offerings and products. Late in the quarter, we added our third video offering called WatchTV, a small package of 30 live channels and 15,000 on-demand titles.

We include WatchTV in our unlimited, more wireless plans where you can purchase it for $15 a month, making it perfect for customers who want video but not at the cost of a large package. This complements DIRECTV NOW where we continue to see success in attracting cord cutters and cord severs. And later this year, we will begin testing a premium product extension, which is a streaming product that will give the full DIRECTV experience over any broadband, ours or competitors’. It will have additional benefits of an improved search and discovery feature and an enhanced user interface. We’re excited that this will complement our top-end product for those who don’t want or can’t have a satellite dish.

Our open-video platform also dovetails nicely with our ongoing focus on driving the industry’s leading cost structure. The new platform is low touch with lower acquisition costs as streaming services becomes a bigger part of our business.

Digital sales are a cost-efficient way of customer engagement, and we’re seeing double-digit growth in our digital sales and service. We’re also seeing operating expense savings from our move to a virtualized software-defined network.

More than 55% of our network functions were virtualized at the end of 2017, and we’re well on our way to meet or exceed our goal of 75% virtualized by 2020. These and other cost management initiatives have helped drive 13 straight quarters of cost reductions in our technology and infrastructure group.

Finally, I’d like to give an update on our FirstNet build and other network investments. Our FirstNet network build is accelerating. We expect to have between 12,000 and 15,000 band 14 sites on air by the end of this year 2018, and we’re ahead of our contractual commitment. And don’t forget, when we’re putting in equipment for FirstNet, we’re also deploying our AWS and WCS spectrum, utilizing the one touch, one tower approach. This approach allows all customers access to our improved network. FirstNet also gives us an opportunity to sell to first responders. So far, more than 1,500 public safety agencies across 52 states and territories have joined FirstNet, nearly doubling the network’s adoption since April.

In addition to our efforts with FirstNet, 5G and 5G Evolution work continues its development in several different areas that will pave the way to the next generation of higher speeds for our customers.

We now have 5G Evolution in more than 140 markets, covering nearly 100 million people with theoretical peak speeds of at least 400 megabits per second with plans to cover 400-plus markets by the end of this year. Our millimeter wave mobile 5G trials are also going well, and we’re on track to launch service in parts of 12 markets by the end of this year.

References:

https://seekingalpha.com/article/4189949-t-inc-2018-q2-results-earnings-call-slides

Analysys Mason: Public WiFi to add $20B to India’s GDP

Public Wi-Fi can play a key role in driving ubiquitous connectivity and digital inclusion in India, as explored in an Analysys Mason report – ‘Accelerating connectivity through public Wi-Fi: Early lessons from the railway Wi-Fi project.’

Despite fast increases in number of people connected (316 million at the end of 2017, compared to 200 million the previous year), mobile broadband penetration in India stood at only 31% at the end of 2017, still significantly behind many of India’s peers. The report, prepared through the lens of Google and Railtel Public Wi-Fi project, support the Government’s ambition under the draft NDCP to reach 5 million access points in 2020 and 10 million in 2022, to provide an all-pervasive coverage and internet connectivity, for 600 million Indians.

David Abecassis, partner at Analysys Mason, said: “In the last few years, India has made significant progress in driving mobile data usage, thanks to improved networks, and low cost data. But to really achieve the connected India vision, India will need to further invest in developing public Wi-Fi as a complement to mobile and fiber broadband.”

According to Abecassis, the Google and RailWire project to deploy high speed Wi-Fi across 400 stations has shown that there was a technical and operational solution to providing high-quality public Wi-Fi to millions of Indians nationwide, on affordable terms.

“The success of this rollout and Reliance Jio’s 80,000 public Wi-Fi access points as of mid-2017 provided valuable insights in further developing public Wi-Fi as a service that can truly achieve the Digital India vision,” he added.

The report further outlines an opportunity to develop a wider connectivity ecosystem with Public Wi-Fi as a key component, which can not only benefit users and wireless ISPs, but also telecom service providers, handset manufacturers and venue owners. ISPs can benefit by monetizing demand for faster mobile broadband and higher data volumes on their networks, as people get used to fast speeds and ubiquitous connectivity.

Analysis Mason found that around 100 million people would be willing to spend an additional USD 2 to 3 billion per year on handsets and cellular mobile broadband services, as a result of experiencing fast broadband on public Wi-Fi. In addition to driving productivity improvements from high speed Wi-Fi for the overall economy, public Wi-Fi can also translate into tangible benefits to GDP, by around USD 20 billion between 2017-19 and at least billion per annum thereafter.

References:

Google’s Internet Access for Emerging Markets – Managed WiFi Network for India Railways

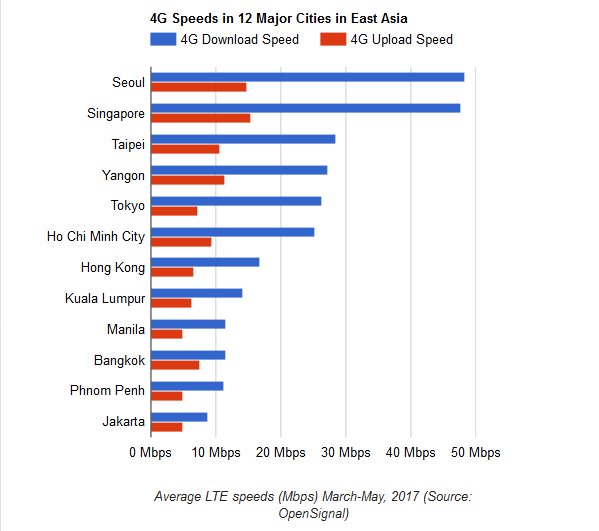

4G Speeds Increase in the U.S. and Asia: Seoul, Korea and Singapore fastest 4G cities

4G (LTE and LTE Advanced) speeds have increased all over the world in the last year. In the U.S., PC Mag wrote:

Peak speeds have jumped from the 200Mbps range to the 300Mbps range, average download speeds have bumped up by 10Mbps or more, and latency has dropped by 10ms. That’s an impressive change in one year, and it continues the trend of improvement that we’ve seen over the past several years of testing.

As we get to a world where we can assume 20Mbps or higher download speeds on 4G in most cities, other questions arise: Where are those speeds most consistent? Where is the network most responsive, especially when you’re downloading pages made of many small files?

Our tests cover data speeds and reliability; we don’t make voice calls. But our awards for data service apply more and more to voice, too. All of the carriers other than Sprint now use voice-over-LTE, piping their voice calls through their data networks. So the reliability of those LTE data networks translates into the reliability of your HD voice calls, as well.

………………………………………………………………………………………………………………………………………………………………..

In Southeast Asia (including Japan, but not China except for Hong Kong), Seoul and Singapore are the fastest 4G cities, according to a regional ranking of major cities from OpenSignal. An analysis of 12 cities in the region shows that Seoul recorded an average 4G speed of nearly 50Mbps, with Singapore close behind.

Four cities demonstrated 4G speeds of over 25Mbps – Taipei, Tokyo, Yangon and Ho Chi Minh. The latter cities have benefited from having launched 4G just two years ago, which OpenSignal said suggests that they have not yet filled their networks to the extent that speeds have started to decline.

The final six cities examined all had speeds at or below the global average of 16.9Mbps. Hong Kong was highest among this grouping, followed by Kuala Lumpur, Manila, Bangkok, Phnom Penh and Jakarta.

OpenSignal noted that Southeast Asian operators are focusing on improving coverage over speed. Singapore topped the list for average 4G upload speed at 15.4Mbps, followed by Seoul and Yangon. But the gap between the fastest and slowest upload speed was only around 10Mbps, with even the slowest cities in the region, Phnom Penh and Jakarta, averaging 4G upload speeds of 4.9 Mbps.

As 4G connections are far superior to 3G connections, Southeast Asia’s wireless network operators seem intent on making LTE services accessible to the vast majority of their customers before they turn their attention to raw speed.

Nokia, Tencent working together on 5G applications

Nokia and Tencent will collaborate on 5G applications, testing and rolling out offerings to WeChat and QQ users, the companies announced. Under the partnership, the two will focus on products for the transportation, finance, energy, intelligent manufacturing and entertainment sectors, including edge computing, “Cellular Vehicle-to-Everything” and cloud-based entertainment.

Nokia to build and test 5G apps in China with Tencent, leveraging 1B+ WeChat and QQ users

Comcast Blames Widespread Service Outage on Cut Fiber Lines Owned by CenturyLink & Zayo

Comcast Corp, which has more than 29 million business and residential customers, today blamed cuts in two fiber lines for a widespread system failure that knocked out cable, internet and phone services around the country.

It was unclear how many customers were affected as the system failure, which appeared contained to Comcast’s network, also disrupted connectivity services like Netflix Inc. and Okta Inc. as other internet service providers routed internet traffic through Comcast’s network, according to network research firm ThousandEyes.

![]()

Comcast service problems today (June 29, 2018):

https://outage.report/us/xfinity

………………………………………………………………………………………………………………………………………………………

Comcast, one of the dominant cablecom companies in the U.S., said most service had been restored by late Friday. The Philadelphia-based company said in a statement that “one of Comcast’s large backbone network partners had a fiber cut that we believe is also impacting other providers.” Later, Comcast said the damaged fiber optic lines are owned by CenturyLink Inc. and Zayo Group Holdings Inc.

A spokeswoman for CenturyLink issued a statement saying CenturyLink’s network was working normally, though the company had “experienced two isolated fiber cuts in North Carolina affecting some customers that in and of itself did not cause the issues experienced by other providers.” The spokeswoman, Francie Dudrey, didn’t comment further. Attempts to reach Zayo were unsuccessful. Fiber networks, which make up the backbone of the internet, transmit vast amounts of internet traffic, processing everything from online purchases to 911 calls.

Down Detector and Outage.Report, two websites that monitor the running of consumer-technology services, ranked the system failure as extreme and posted maps indicating large numbers of customers affected in the New York, Philadelphia and Washington, D.C., metro areas as well as San Francisco, Chicago and Denver.

Reports of outages, according to the websites, spiked early Friday afternoon. Some customers took to social media to discuss the outages, saying they were having trouble getting through the company’s phones and online chats. Comcast, on Twitter, directed customers to an internal website that was at one point down as well, eliciting a second round of customer complaints.

https://www.wsj.com/articles/comcast-blames-widespread-service-outage-on-cut-fiber-line-1530308633

Write to Maria Armental at [email protected]

IHS Markit: Ethernet switching market +12% YoY; data center and campus upgrades

By Matthias Machowinski, senior research director, enterprise networks and video, IHS Markit

Highlights:

- Worldwide Ethernet switch revenue totaled $6.1 billion in the first quarter of 2018 (Q1 2018), growing 12 percent on a year-over-year basis

- 100GE continued to ramp, increasing more than twofold year over year and reaching 1.7 million ports in the quarter; 40GE ports were flat year over year

- Power-over-Ethernet (PoE) port shipments grew 11 percent in Q1 2018

- Number-one Cisco grew 7 percent year over year, number-two Huawei rose 43 percent, number-three HPE (Aruba) was up 2 percent and number-four Arista grew 40 percent

IHS Markit analysis:

Ethernet switch revenue declined 10 percent sequentially in Q1 2018 due to a seasonal slowdown in demand, but the longer-term growth outlook remains positive and strengthened further during the quarter, with year-over-year growth hitting 12 percent, up from 7 percent the previous quarter.

The market enjoyed its strongest growth in seven years in 2017, and the momentum continued into 2018, fueled by continuing data center upgrades and expansion, as well as growing demand for campus gear due to improving economic conditions. The transition to 25/100GE architectures in the data center is in full swing, driving strong gains in 25GE, 100GE and white box shipments. And power over Ethernet is growing once again, a sign of strengthening campus switching demand.

Growth is well balanced around the globe and not driven by any single geography. In Q1 2018, Europe, the Middle East and Africa (EMEA) and Asia Pacific were the top growth markets, increasing 15 and 16 percent, respectively, year over year, while growth in North America remained solid at 8 percent.

IHS Markit forecasts low- to mid-single-digit growth for the Ethernet switching market from 2019 to 2022. The bright spots will be the 10GE, 25GE, 100GE, 200GE and 400GE segments, where significant growth is expected over the next few years.

Ethernet switch report synopsis

The IHS Markit quarterly Ethernet switch report provides worldwide and regional market size, vendor market share, forecasts through 2022, analysis and trends for unmanaged, web-managed and fully managed fixed and chassis switches by port speed (100ME, 1GE, 2.5GE, 10GE, 25GE, 40GE, 50GE, 100GE, 200GE, 400GE) and revenue.

…………………………………………………………………………………………………………………………………………………………………………………………………

Related articles on Ethernet Switch Market:

IDC’s Worldwide Quarterly Ethernet Switch and Router Trackers Show Marked Improvement for Q1 2018

IDC: Global IT, telecom spending=$4T in 2018; Economic risks loom for 2019

Global IT and telecom spending will grow 3.7 percent to $4 trillion in 2018, but economic concerns could derail growth in 2019, according to IDC.

In 2017, IT and telecom spending grew at a 4.2 percent clip. IDC said economic issues like tariffs, rising interest rates and growth in China could cut IT spending to less than 3 percent.

Indeed, Daimler issued a profit warning based on Chinese tariffs on its U.S. made cars.

By 2022, annual IT spending should hit $4.5 trillion with software and services, cloud, and digital transformation seeing the most demand. Infrastructure spending has stabilized largely due to cloud spending.

IDC said there’s a likelihood for a mild U.S. recession by 2020, but spending on cost saving software and cloud should provide a buffer for IT spending.

Last year saw a significant rebound in spending on devices, driven by the improving economy and pent-up demand for PC upgrades. The smartphone market performed better than forecast in terms of value, with price increases making up for slowing shipments in many countries. Tablets continued to struggle but will return to modest growth in some countries over the next few years as premium and commercial devices begin to account for an increasing proportion of shipments. Meanwhile, server/storage spending is increasingly driven by cloud hyperscale datacenter buildout but is also benefiting from a significant enterprise upgrade cycle related to product refreshes. IT infrastructure spending, including network equipment, increased by 11% in 2017 and will continue to post annual growth in the range of 8-12% over the next five years even while spending on devices slows again.

“The infrastructure market is increasingly stable because a large proportion is now tied to the service provider model and overall demand for cloud services, which shows no sign of slowing down even in the event of a weakening economy,” said Stephen Minton, vice president, Customer Insights & Analysis. “To some extent, this spending will be more insulated against economic downturns than end-user capital spending, and therefore the IT market will be less vulnerable than it was in the past when any kind of GDP slowdown would translate into big declines for hardware spending. Nevertheless, economic risks are now higher than three months ago.”

US Demand is Stable, but China Facing Slowdown

All regions saw strong demand for technology in 2017, thanks to the broad-based strength of economic performance. The U.S. rebounded from 1.9% growth in 2016 to 4.5% in 2017. Tax cuts will help to ensure another strong year for the U.S. market in 2018, before overall growth is expected to slow. Many economists now expect a mild recession in the U.S. by 2020 at the latest, but the impact on ICT spending will be less than previous downturns due the growth of the service provider model and the increasing adoption of cost-saving software. Meanwhile overall growth in China slowed from 9% in 2016 to 8% last year and will drop to 6% in 2018.

“The economy is gradually slowing in China, but the real reason for slowing ICT growth is because the market is still heavily reliant on mobile devices, which are now seeing higher penetration rates,” said Minton. “Software and services are growing strongly, but still represent a very small proportion of average ICT budgets in China compared to other countries.”

Economy, Cloud, and Mobile Driving Growth

Other regions which posted improving growth in 2017 included Japan (+3%), Western Europe (+2%), Central & Eastern Europe (+3%), Canada (+5%), Asia/Pacific (excluding Japan) (+5%) and the Middle East/Africa (+2%). All of these regions benefited from improving business and consumer confidence, which enabled ICT buyers to work off the pent-up demand that had swelled during the prior years of subdued growth.

“Cloud and mobile are still the big drivers for traditional ICT spending, as legacy products and services like desktop PCs and fixed-line networks either stagnate or begin to decline,” added Minton. “This means what while the overall market is broadly tracking GDP, there is a lot of variation by product category. cloud-related hardware, software, and services are posting strong rates of growth. For example, Infrastructure as a Service (IaaS) is expected to grow by another 37% this year and will continue to grow by around 30% per year over the forecast. This in turn will ensure that cloud service providers continue to invest in server/storage and network infrastructure.”

https://www.idc.com/getdoc.jsp?containerId=prUS44021718

Point Topic: 931.6M Fixed Broadband Connections at end of Q4-2017; VDSL Growth but Copper Connections Continue Decline

|

|

|

IHS Markit: Optical Network Equipment Market off to slow start in 2018

By Heidi Adams, senior research director, IP and optical networks, IHS Markit

Highlights

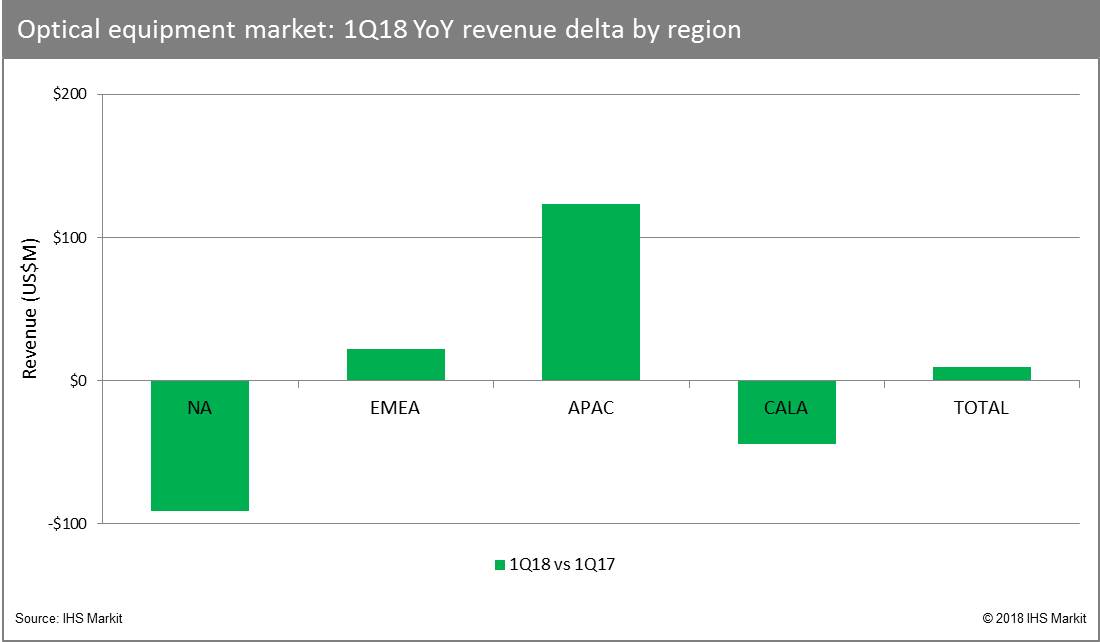

- Global optical network hardware revenue totaled $3.1 billion in the first quarter of 2018 (Q1 2018), declining 25 percent sequentially and remaining flat on a year-over-year basis.

- The global Q1 2018 optical equipment market net of China was down 2 percent year over year. China itself was up 7 percent year over year, and continues to be a key market for optical transport equipment.

- Huawei remained the overall optical equipment market leader in Q1 2018, with 26 percent market share.

Our analysis

After a strong close to 2017, the optical equipment market got off to a lackluster start in 2018. Modest year-over-year growth in Europe, the Middle East and Africa (EMEA) and Asia Pacific was not sufficient to overcome year-over-year spending declines in North America and the Caribbean and Latin America (CALA) regions in the quarter. Total optical equipment market spending was down 25 percent on a sequential basis, with all regions seeing quarter-over-quarter declines.

Wavelength-division multiplexing (WDM) continues to be the growth engine for the market. In Q1 2018, the WDM segment totaled $2.9 billion, up 3 percent year-over-year, thanks to gains in EMEA and Asia Pacific. Both the metro and long haul segments experienced low single-digit year-over-year growth in Q1 2018.

Synchronous optical networking (SONET)/synchronous digital hierarchy (SDH) continued its overall decline. Global revenue came to $206 million in Q1 2018, down over 25 percent year over year. This segment represented less than 10 percent of the total optical network equipment market in the quarter.

Huawei continued to lead the total optical equipment market by a wide margin in Q1 2018. Nokia secured second place based on continuing strength in EMEA and increasing business in Asia Pacific. Ciena maintained its leadership position in North America and remained number three overall in the global market. ZTE rounded out the top four, but faces a difficult journey ahead with the impact of US sanctions and a subsequent halt in major operations.

Unstoppable bandwidth demand drives long-term growth

IHS Markit anticipates a continuing ramp in network capacity to address growing bandwidth demand. In the metro, the primary driver is burgeoning bandwidth demand—to, from and between data centers.

Not to be ignored is the coming broader introduction and adoption of consumer 4K and higher video content and services on a variety of devices. The shift from data to video to virtual reality (VR)/augmented reality (AR) will add yet another set of bandwidth-intensive and latency-sensitive services to the mix toward 2022.

Finally, a further evolutionary shift in mobile network architectures in preparation for 5G and a range of new fixed and mobile machine-to-machine (M2M) and Internet of Things (IoT) applications will set the stage for an investment cycle at the farthest reaches of the optical access network.

Based on these industry trends, the optical equipment market will grow at a compound annual growth rate (CAGR) of 4.5 percent from 2017 to 2022, according to IHS Markit forecasts.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

Editor’s Note:

We believe much of the anticipated fiber optic network growth will come from a variety of factors in the metro, including data center interconnect demands, higher-bandwidth video transmission (with the advent of 4K video) and eventually virtual and augmented reality. We think 5G mobile backhaul support is questionable in the next few years considering all the “5G” hype and lack of standards till IMT 2020 (5G radio aspects ONLY) recommendations are finalized in late 2020.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

Optical Network Hardware Market Tracker – Q1 2018

This report tracks the global market for metro and long-haul WDM and SONET/SDH equipment and SONET/SDH and WDM ports. It provides market size, market share, forecasts through 2022, analysis and trends.