ITU Global Resiliency Platform to keep information networks ‘safer, stronger’ throughout COVID-19 pandemic

ITU Tweet March 23, 2020:

Global Network Resiliency Platform to help countries + industry cope with the increasing stress put on global networks during the #COVID19 crisis itu.int/en/mediacentre#REG4COVID

Telecommunication networks have never before been as vital to “our health and safety, and to keep our economy and society working” as they are during the current crisis, where millions are being encouraged to stay put at home, the ITU chief maintained.

He has asked instructed his team to “leverage without any delay” the new platform in aid of existing networks “to help countries and industry cope with the increasing stress being put on global networks”.

“At stake is our ability, as one human family, to give health workers everywhere, the tools they need to carry out their duties, to allow all those that can to work from home, to trade online, to ensure that hundreds of millions of children and young people keep up with their studies, and to keep in touch with loved ones, wherever they are”, he detailed.

The Global Network Resiliency Platform will also share best practices and initiatives that have been put in place during the COVID-19 crisis to ensure that telecommunication services are available to the maximum extent possible.

The portal will collect relevant information and expertise on actions that telecommunication policymakers and others in the regulatory community can use to ensure that their networks serve their country’s needs.

“This new ITU platform will provide countries struggling to find appropriate solutions to ensure their networks’ resiliency with relevant and trustworthy information and expertise on how to cope with the stresses faced by their infrastructure”, assured the agency chief.

“And because time is of the essence, it will give those countries that still have time to prepare an opportunity to learn from what is being done elsewhere – from emergency spectrum reassignments to guidelines for consumers on responsible use.”

Serving initially as an informative tool, the portal will soon be expanded to provide an interactive and engaging platform for continuous sharing throughout the pandemic and beyond.

“The crisis we are in today calls for solidarity”, he spelled out. “In these uncertain times, we should not forget all those around the world who still lack access to the Internet”.

ITU has long promoted universal, reliable and affordable connectivity, and will continue to push on all these fronts and advocate until everyone is connected.

“I call on all ITU members, from the public and private sector alike, to come together to build the best platform we can so that information and communication technology can help defeat COVID-19 and make us safer, stronger and more connected,” concluded the ITU Secretary-General.

………………………………………………………………………………………………..

Coronavirus Portal Updates:

References:

China Telcos Lose Subscribers; 5G “Co-build and Co-share” agreement to accelerate

Decrease in China’s Mobile Subscribers:

China’s wireless carriers are reporting substantial drops in subscribers as the coronavirus crisis reduces business activity.

China Mobile Ltd., the world’s largest wireless carrier, reported its first net decline since starting to report monthly data in 2000. China Mobile subscriptions fell by more than 8 million over January and February, data on the company’s website show.

China Telecom Corp. said it lost 5.6 million users in February, while China Unicom Hong Kong Ltd. subscribers fell by 1.2 million in January.

The across the board China subscriber slump indicates that the coronavirus pandemic crisis, which first emerged in China late last year, is crimping growth, even at businesses that provide essential services and earn monthly revenue. ARPU will likely also decline, according to analysts.

Chris Lane, an analyst at Sanford C. Bernstein & Co said that part of the decrease in wireless subscribers could be due to migrant workers — who often have one subscription for where they work and another for their home region — canceling their work-region account after the virus prevented them from returning to work after the Lunar New Year holidays which began in late January.

While the drop in users is unusual, the total is small relative to total wireless subscriptions, which have risen to a combined 1.6 billion for the three carriers. Things may improve starting this month as work in factories and other businesses in China resumes, Lane said.

Net income fell 9.5% last year at China Mobile, partly on government mandates to cut prices and improve service, but also due to a spike in financing costs – up from RMB144 million ($20.2 million) to RMB3.25 billion ($460 million).

The company, which reported earnings last week, told analysts revenue would remain stable this year, a sign management was not worried about the fall in subscribers.

China Unicom overcame flat revenue growth to post an 11.1% increase in net earnings for 2019. The state-owned telco slashed opex by 22% and marketing cost by 5% to record a 11.3 billion yuan ($1.6 billion) full-year profit.

“In 2019, the domestic telecommunications industry development experienced a short-term pain with weak revenue growth and pressure on industry value,” Chairman and CEO Wang Xiaochu said.

………………………………………………………………………………………..

Co-build and Co-share Agreement:

In September 2019, China Unicom entered into a cooperation agreement with China Telecom to jointly build one 5G access network across the country. China Unicom would be doubling it’s own 5G network coverage, bandwidth, capacity and transmission speed, providing users with better experience.

China Unicom said it will actively step up the “co-build and co-share” with China Telecom in areas such as 4G indoor distributed antenna systems, server rooms, optical fiber and pipelines to further enhance network advantages and corporate value.

References:

https://www.bnnbloomberg.ca/china-s-mobile-carriers-lose-15-million-users-as-virus-bites-1.1410626

https://www.telecomlead.com/5g/china-unicom-reveals-5g-network-capex-plans-94530

AT&T boosts wireless network capacity in spectrum-sharing deal with DISH Network

DISH Network is loaning AT&T 20 MHz of spectrum in the AWS-4 band, as well as its entire supply of 700 MHz airwaves, for two months. This is the third spectrum-sharing arrangement that the satellite provider has made since Sunday as telecom network providers prepare for extra data traffic from people working at home.

“DISH is proud to join forces with AT&T to achieve a common, critical goal: supporting the connectivity needs of Americans during this challenging time,” said Jeff Blum, DISH SVP of public policy and government affairs, in a statement.

This follows last week’s news that DISH would lend its complete 600 MHz portfolio of spectrum to T-Mobile. In addition to loaning spectrum to T-Mobile and AT&T, DISH was given permission yesterday by the FCC to also loan spectrum to Verizon.

/cdn.vox-cdn.com/uploads/chorus_image/image/66528643/DSC_4155.0.jpg)

According to analyst Jonathan Chaplin at New Street Research, AT&T will be able to deploy the AWS-4 spectrum quickly and easily using its AWS-1 and AWS-3 equipment. In addition, AT&T can use Dish’s 700 MHz E-Block in conjunction with the D-Block that AT&T has started deploying in some markets. Analysts are speculating that these loans during the COVID-19 crisis might later be turned into ongoing leases.

Chaplin wrote: “All told, DISH has now loaned out spectrum that could be leased at an annual run rate of $940 million. They still have the PCS H-Block and another 20 MHz of AWS-4, which would be worth another $580 million.”

Chaplin of New Street says: “All we know at this stage is that DISH is helping in a crisis; we don’t know that either side would be willing to convert the loan to a lease.”

DISH’s generosity in lending its spectrum during the coronavirus scare is highlighting how helpful the spectrum is to other operators in order to increase their capacity.

Wells Fargo analyst Jennifer Fritzsche wrote, “Once this crisis passes, we believe the heavy demand on wireless and wired networks will shine the light on the need for additional spectrum allocation and continued programs to support push-out of broadband into rural areas to lessen the digital divide.”

………………………………………………………………………………….

PC Magazine has a breakdown of how Dish is distributing its unused spectrum over the next 60 days. Each provider is getting spectrum that can temporarily help bolster its 4G LTE data network and increase speeds. In AT&T’s case, Segan estimates that wireless customers could notice up to a 20Mbps uptick in data performance while the spectrum loan is in effect.

DISH has often been criticized for hoarding spectrum and not putting it to any actual use. The company even risked fines from the FCC for failing to build an actual wireless network with the spectrum it owns. But that was before the company was brought into the T-Mobile and Sprint deal and positioned as the replacement fourth “major” carrier once the merger is finalized.

Earlier today, T-Mobile issued a news release stating that the company remains prepared to close the merger with Sprint even as financial markets are in turmoil due to the coronavirus pandemic. All necessary US regulators have already approved it and the two providers emerged victorious over a challenge from several US states.

References:

https://www.fiercewireless.com/wireless/dish-lends-spectrum-to-at-t-during-covid-19-pandemic

https://www.pcmag.com/news/att-4g-gets-a-big-capacity-boost-in-coronavirus-crisis

China Mobile has 15.4 million 5G customers; 5G+ is primary focus area

China Mobile today published its 2019 annual financial report, stating that the company’s operating revenue reached CNY745.9 billion -a year-on-year increase of 1.2% – and its net profit was CNY106.6 billion ($15 billion) – a year-on-year decrease of 9.5%.

The fall in net profits was largely due to a spike in financing costs – up from RMB144 million ($20.2 million) to RMB3.25 billion ($460 million).

Operating revenue was just 1.2% higher, at RMB745.9 billion ($104.8 billion), while telecom services revenue improved by a meager 0.5%.

A few highlights:

- The largest China telecom network provider acquired 15.4 million 5G customers in the first three months after launch.

- In 2019, China Mobile’s mobile users increased by 25.21 million, reaching a total of 950 million. Its mobile Internet data traffic increased by 90.3% year-on-year and its mobile Internet DOU reached 6.7GB.

- Wireline broadband customers grew by 30.35 million to a total of 187 million.

- China Mobile’s family broadband users reached 172 million, an increase of 17.1% year-on-year. Its family broadband comprehensive ARPU reached CNY35.3.

- At the end of 2019, China Mobile’s government and corporate clients reached 10.28 million, a year-on-year increase of 43.2%. The company’s international business revenue saw a year-on-year increase of 31.4%.

![]()

Mr. Yang Jie, China Mobile’s Chairman of the Board said in the press release:

“We were faced with a challenging and complicated operating environment in 2019 where the upside of data traffic was rapidly diminishing and competition within the telecommunications industry and from cross-sector players was becoming ever more intense. Coupled with this was the impact of government policies, including the continued implementation of the “speed upgrade and tariff reduction.”

Against this backdrop, all of us at China Mobile joined together to overcome these hurdles and work towards our ultimate goal of becoming a world-class enterprise by building a dynamic “Powerhouse”. This was centred on the key strategy of high-quality development, supported by a value-driven operating system that leverages our advantages of scale to drive further convergence, integration and digitization across the board.

We structured our organization to enable effective and synergetic capability building and collaborative growth, while nurturing internal vitality. In addition, we further implemented our “5G+” plan to spearhead the development of “four growth engines”, comprising the “customer,” “home,” “business” and “new” markets. These measures have helped us obtain positive momentum in overall operating results, which was a hard-earned achievement for us in a tough year.”

Yang noted that the COVID-19 epidemic had driven more and more businesses and consumers online and encouraged greater takeup of digital and cloud-based services. “We will leverage these opportunities, as well as the 5G network, to further develop the information and communications services market.”

Business Market:

The “business” market was China Mobile’s new growth engine and we strove to nurture new growth points by fully leveraging our cloud and network convergence advantages, building on our DICT (data, information and communications technology) infrastructure comprising IDC, ICT, Mobile Cloud, big data and other corporate applications and information services. Buoyed by active promotion of our “Network + Cloud + DICT” smart services, customers and revenue recorded rapid growth.

As of the end of 2019, the number of corporate customers increased to 10.28 million, representing year-on-year growth of 43.2%.

Focusing on key sectors such as industry, agriculture, education, public administration, healthcare, transportation and finance, the company deepened go-to-market resources to promote DICT solutions that cater to sector-specific scenarios. This strategy has boosted DICT revenue to RMB26.1 billion, or growth of 48.3% year-on-year, contributing a larger portion of our overall revenue.

“5G+” Achieved a Good Start:

China Mobile sped up the development of 5G and have been fully implementing its “5G+” plan since June 2019, when we were granted the 5G licence. These initiatives have shown good initial results.

The company actively participated in setting international standards for 5G to drive technological development. It led 61 key projects in relation to 5G international standards setting and own more than 2,000 5G patents. It also helped to continuously strengthen the Standalone 5G (within 3GPP Release 15 and 16).

Its “six international standards (3GPP specifications are not standards) on 5G system architecture” and “38 international standards including 5G NR (New Radio) terminals and base station radio frequency” scooped all the top prizes in the 2019 Science and Technology Awards presented by the China Communications Standards Association, demonstrating our leadership in 5G communications standards.

At the same time, the company accelerated the implementation of “5G+” by formulating well- coordinated development of 5G and 4G. It constructed and began operating more than 50,000 5G base stations and launched 5G commercial services in 50 cities. Emerging technologies such as AI, IoT (Internet of Things), cloud computing, big data and edge computing were assimilated into 5G (5G+AICDE) and developed more than 200 critical capabilities, while making breakthroughs in over 100 5G joint projects.

In terms of 5G+Eco, we aimed to develop the ecosystem with other industry players. Through its 5G Innovation Centre and 5G Industry Digital Alliance, more than 1,900 partners were attracted.

The 5G Device Forerunner Initiative, guiding manufacturers to launch 32 5G devices, was established. The level of maturity was basically the same between the 2.6 GHz and 3.5 GHz industry chains. Benefiting from forward-looking planning and effective execution, we expanded 5G+X, where “X” stands for the wider application of 5G, in applications that have been adopted by a plethora of industry sectors, as well as the mass market. For the latter, we launched exclusive plans for 5G customers and feature services such as ultra-high definition videos, cloud-based games and full-screen video connecting tones. As of the end of February 2020, our 5G plans attracted 15.40 million package customers – maintaining an industry-leading position.

In terms of vertical sector, China Mobile explored the possibility of combining 5G with AICDE capabilities, extending collaboration in the industry and deep-diving into classic manufacturing scenarios to develop our leadership in 5G smart manufacturing, 5G remote medical services and 5G automated mining, among other sectors. A total of 50 group-level demo application projects were implemented.

Looking ahead, 5G presents infinite possibilities. China Mobile will continue to take a systematic approach to planning and steadily implementing our “5G+” initiatives. The company will speed up technology, network, application, operations and ecosystem upgrades, accelerate industry transformation by converging technologies, integrate data to strengthen information transmission in society, and introduce digitized management to build the foundation for digital society development. By doing so, China Mobile will seek more extensive 5G deployment, covering more sectors and creating greater efficiency and social value.

…………………………………………………………………………………………….

References:

https://www.chinamobileltd.com/en/file/view.php?id=226450

https://www.chinatechnews.com/2020/03/19/26442-china-mobile-net-profit-down-9-5-in-2019

https://www.lightreading.com/asia/china-mobile-reports-154m-5g-customers/d/d-id/758329?

Telefónica and partners pursue development of 4G/5G Open RAN technology

Telefónica has announced an agreement to develop 4G and 5G Open RAN technology with partner companies Altiostar, Gigatera Communications, Intel, Supermicro and Xilinx. The Spain based pan European network operator also said it intends to launch vendor-neutral 4G and 5G Open RAN trials in UK, Germany, Spain and Brazil this year.

Telefonica said this latest collaboration comprises the necessary design and developments, integration efforts, operational procedures and testing activities required to deploy Open RAN in its networks. The Spanish network operator says this is part of its continuing efforts to lead network transformation towards 5G and that the collaboration would progress the design, development, optimisation, testing and industrialisation of Open RAN technologies across its footprint this year.

The collaboration focuses on the distributed units (DUs) and remote radio units (RRUs). The DUs implement part of the baseband radio functions using the FlexRAN software reference platform and servers based on the Intel Xeon processor. The RRUs connect through open interfaces, based on O-RAN Alliance’s fronthaul specification, and software that manages the connectivity in an open cloud RAN architecture.

Telefonica said DUs and RRUs will be designed with 5G-ready capabilities, meaning they can work in either 4G or 5G mode by means of a remote software upgrade. It will be testing the 4G and 5G hardware and software components in the lab and in the field this year, integrating an Open RAN model as part of its UNICA Next virtualization program.

……………………………………………………………………………………………….

The premise is that Open RAN will be cheaper as it encourages more suppliers into the market, especially in terms of the baseband hardware where economies of scale from using standard IT can be deployed.

A cloudified open radio access architecture can also enable faster software innovation and advanced features like network automation, self-optimization of radio resources and coordination of radio access nodes.

The main goal of the trial is to define precisely the hardware and software components in 4G and 5G to guarantee seamless interoperability. This includes:

• Testing the complete solution in the lab and in the field,

• Integrating the Open RAN model as part of the end-to-end virtualisation program (UNICA Next),

• Maturing the operational model, and

• Demonstrating new services and automation capabilities as offered by the Open RAN model.

The DUs and RRUs are designed with 5G-ready capabilities and so can work in 4G or 5G mode by means of a remote software upgrade.

…………………………………………………………………………………………………………

The OpenRAN trial also supports exposure to third-party, multi-access edge computing (MEC) applications through open Application Programming Interfaces (APIs), and integration with the virtualisation activities in the core and transport networks. Open interfaces also mean that operators can upgrade specific parts of the network without impacting others.

Telefónica describes this openness to third-party MEC applications as “the cornerstone” to bringing added-value to the customers by enabling a variety of rich 5G services, like virtual and augmented reality, online gaming, connected car, the industrial internet of things (IoT) and more.

Edge-computing applications running in the telco cloud can benefit from the strong capillarity of the access network, so services can be tailored instantly to match the users’ needs and the status of the live network.

……………………………………………………………………………………………..

Quotes:

Enrique Blanco, Telefónica’s CTIO: “Once again, Telefónica is leading the transformation towards having the best-in-class networks in our Operations with our customers as key pillars. Open RAN is a fundamental piece for that purpose while widening the ecosystem.”

“Telefónica is known for its leading-edge network and has been championing open vRAN implementations to bring greater network service agility and flexibility,” said Pierre Kahhale, Altiostar Vice President of Field Operations. “By bringing together the best-of-breed innovation, Telefonica is looking to achieve this vision into their network. We look forward to supporting this transformation of Telefonica’s network.”

Heavy Reading principal analyst Gabriel Brown: “Up to now, the open RAN action has been all about 4G. In 5G, the major integrated systems vendors [Ericsson, Huawei, Nokia, Samsung, ZTE] have been supplying their state-of-the-art systems to the market for about 18 months,” creating a big gap between what is available from them and what can be sourced from the open RAN community, says the analyst. “This move by Telefónica could help to stop that gap getting too much wider.”

“Gigatera Communications and Telefonica has been actively working to ensure state of the art technologies are being deployed. We truly value our partnership as we engage and revolutionize the industry.”, Daniel Kim, President.

“Open RAN offers a way for service providers to enhance customer experiences and enable new revenue-generating applications,” said Dan Rodriguez, vice president and general manager of Intel’s Network Platforms Group. “We are collaborating closely with Telefonica and the broader ecosystem, and also participating in initiatives like the O-RAN Alliance, to help accelerate innovation in the industry.”

“Supermicro is excited to partner with Telefónica, a premier telecommunications provider, to deliver server-class 5G solutions based on Open RAN architecture,”, Charles Liang, president and CEO of Supermicro. “Working closely with Telefónica on the deployment of 5G in the significant EMEA region, Supermicro’s history of rapid time-to-market for advanced, high-performance, resource-saving solutions is a key component for the successful implementation of next-generation applications, especially as x86 compute designs migrate to the telco market.”

“Xilinx is excited to collaborate with the disruptive mobile operator Telefónica as it leads the move to O-RAN” said Liam Madden, executive vice president and general manager, Wired and Wireless Group, Xilinx. “Our adaptable technology supports multiple standards, multiple bands and multiple sub-networks, providing Telefónica with a unique and flexible platform for radio, fronthaul, and acceleration for 4G and 5G networks.”

………………………………………………………………………………………………..

References:

https://www.mobileeurope.co.uk/press-wire/telefonica-partners-to-launch-4g-and-5g-open-ran-trials

https://www.totaltele.com/505252/Telefonica-rallies-a-posse-of-Open-RAN-vendors-to-take-on-5G

https://telecominfraproject.com/openran/

https://www.lightreading.com/4g-3g-wifi/telefonica-takes-open-ran-into-5g-territory/d/d-id/758293?

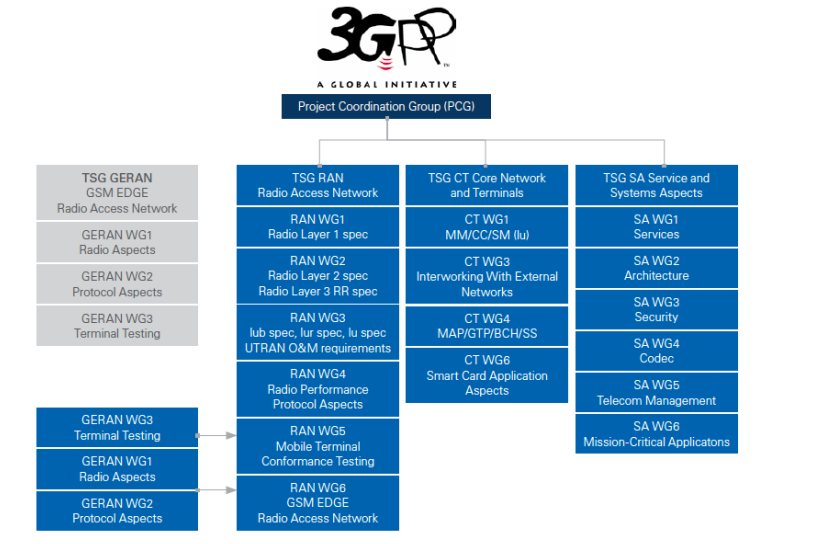

Strategy Analytics: Huawei 1st among top 5 contributors to 3GPP 5G specs

Even though there are more than 600 member companies participating in 3GPP, their 5G specification process is actually led by only a few leading telecom companies. New research from Strategy Analytics analyzes the contributions to 3GPP 5G specifications (Release 15 and Release 16) and finds that 13 companies contributed more than 78% 5G related papers and led 77% of the 5G related Work Items and Study Items.

The Strategy Analytics report “Who Are the Leading Players in 5G Standardization? An Assessment for 3GPP 5G Activities” is available to clients and registered guests here . The report assesses the 13 leading companies’ contributions to 3GPP 5G standards for the period of Releases 15 and 16 so far, based on the following criteria:

- Volume of 5G related papers, including submitted papers, approved/agreed papers and the ratio of approved/agreed papers to total submissions in all Technical Specification Groups (TSGs) and Working Groups (WGs)

- Chairmanship positions, i.e. Chairman and Vice Chairmen for all TSGs and WGs

- Rapporteurs of 5G related Work Items (WIs) / Study Items (SIs) in all TSGs and WGs

The results indicate that the top 5 companies in 3GPP 5G specification activities are Huawei, Ericsson, Nokia, Qualcomm and China Mobile.

Guang Yang , Director at Strategy Analytics, noted, “3GPP plays the central role in the ecosystem of global 5G standardization. By analyzing the contributions of industry players to 3GPP 5G standards, we can get an idea of different companies’ positions in 5G innovation as well as their influence in the global mobile industry. So we looked at 3GPP organization and work procedures to assess each company’s influence from multiple aspects.”

Sue Rudd , Director Networks and Service Platforms service, added, “According to our assessment, leading infrastructure vendors – Huawei , Ericsson and Nokia – made more significant contributions to 5G standards than other studied companies. Huawei leads in terms of overall contributions to the end-to-end 5G standards, while Ericsson leads in TSG/WG chairmanship and Nokia in approved/agreed ratio of 5G contribution papers .”

Phil Kendall , Executive Director at Strategy Analytics, added, “It is important to remember that the true nature of the standardization process is actually one of industry collaboration rather than competition. 3GPP standardization continues to be a dynamic process. It is expected that emerging players and new market requirements will increasingly impact priorities for 3GPP Release 17 standards.”

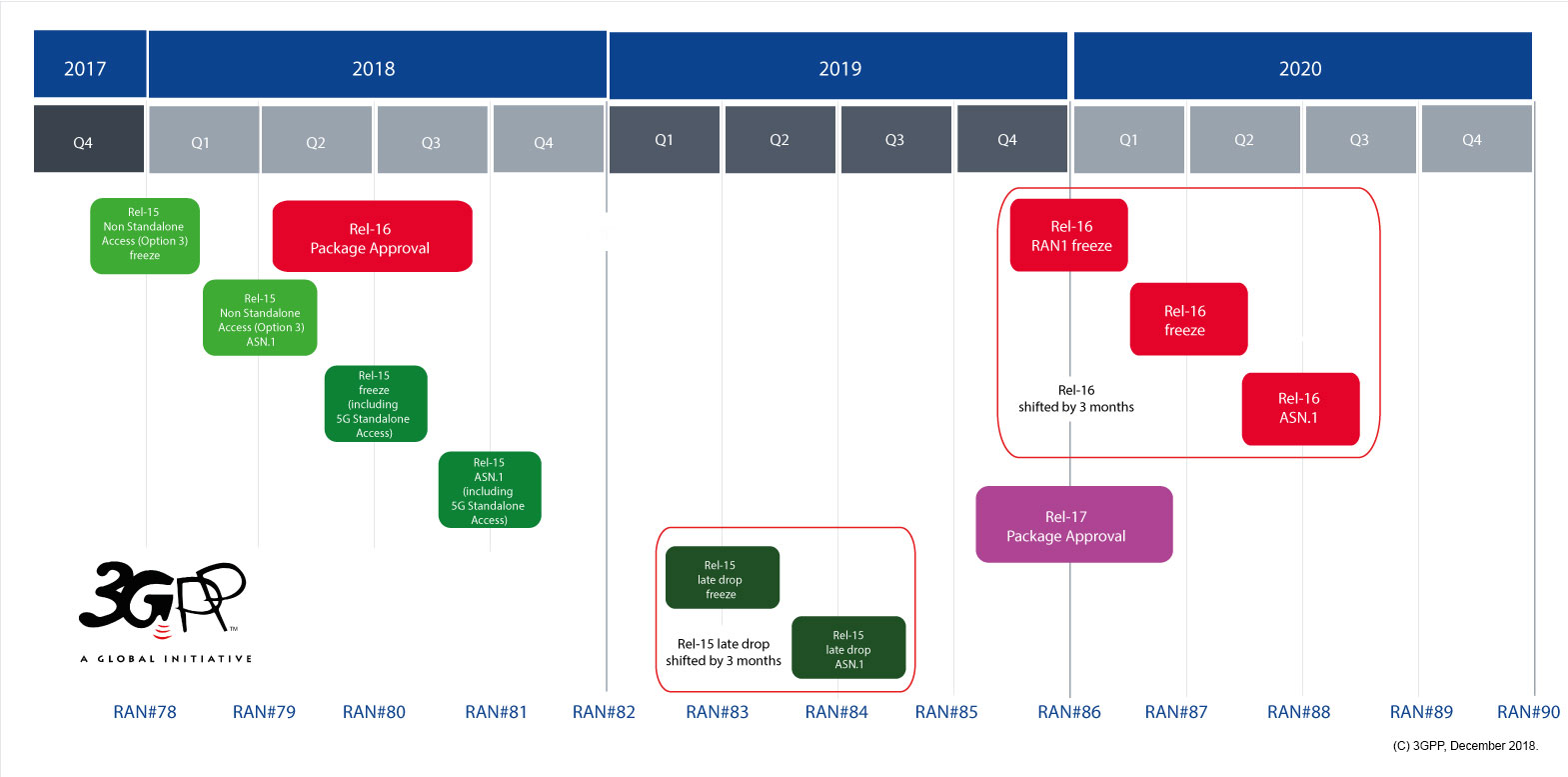

3GPP Timeline:

……………………………………………………………………………………………………

Mike Dano of Lightreading says “Huawei being the biggest contributor to the 3GPP’s 5G specs will undoubtedly worry U.S. lawmakers and regulators, who for years have argued the company poses a security threat to the nation. Huawei denies those allegations.”

“We must have a vocal presence at the standards bodies that are defining the rules for 5G. We have been woefully absent and need to make participation a priority,” wrote Mike Rogers in a recent opinion column. Rogers is a former US representative who co-authored the 2012 US government report initially outlining the security threats posed by Chinese equipment vendors like Huawei and ZTE.

“We need to work with our allies to staunch the spread of Huawei and other Chinese companies owned by the state. We need to better communicate what Chinese dominance of 5G means. This is something we have not successfully done, as shown by Britain deciding to allow Huawei into certain elements of the 5G network,” Rogers added.

Rogers now chairs the “5G Action Now” 501(c)4 advocacy organization, which has been working with the now-disbanded C-Band Alliance to speed up the C-Band spectrum auction in the US for 5G.

Indeed, legislation introduced early this year would require the Trump administration to develop a strategy to “promote United States leadership at international standards-setting bodies for equipment, systems, software, and virtually-defined networks relevant to 5th and future generation mobile telecommunications systems and infrastructure, taking into account the different processes followed by the various international standard-setting bodies.” That legislation passed the House and is now headed to the Senate.

Companies’ 3GPP contributions to the 5G specs [1.] don’t necessarily translate into revenues. For that, companies must patent their inventions.

Note 1. 3GPP specs vs 5G standards:

3GPP 5G specs in Release 15 and 16 have and will continue to be input to ITU-R WP 5D, but only some of those contributions will be in IMT 2020 which is currently restricted to the Radio Interface Technologies (RITs) or sets of RITs (SRITs). Other essential 5G specs like signaling, 5G packet core, 5G network management, etc will be standardized by SDOs (like ETSI) but the real work is done in 3GPP. Also note that IMT 2020 will have several NON 3GPP RITs from ETSI/DECT Forum and India (TSDSI).

…………………………………………………………………………………………………….

According to one study, Huawei leads in that respect also. IPlytics recently reported that the Chinese firm has far and away the most “declared 5G families” of patents, and the most filed since 2012.

However, it’s worth noting that UK law firm Bird & Bird argues that the reliance on such patent calculations isn’t very insightful, and that different methodologies yield different results.

………………………………………………………………………………………………

References:

Cignal AI: Optical Network Equipment Sales +25% in 4Q2019 + 650 Group

Cignal AI:

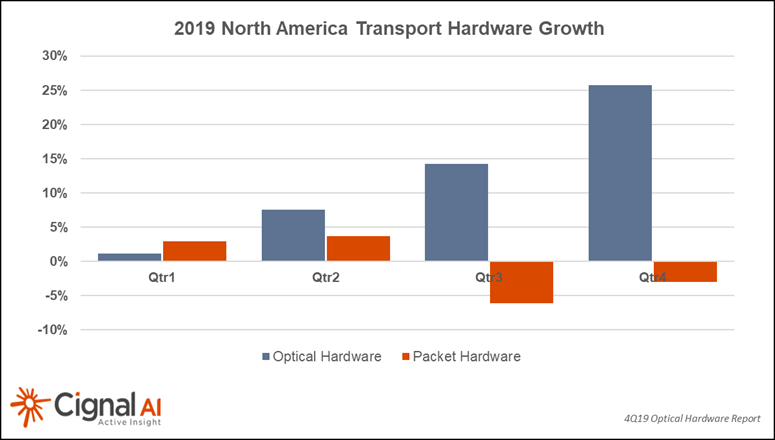

Recent optical network equipment sales in North America were quite encouraging – up more than 25% for 4Q19 and 10% for all of 2019, according to the most recent Transport Hardware Report.

“After three years of North American spending declines as operators focused capex on wireless and access, optical hardware sales in the region revived and grew at a healthy pace for 2019, while packet hardware sales remained flat,” said Scott Wilkinson, Lead Analyst at Cignal AI. “Market leaders Ciena, Infinera, and Cisco all achieved optical sales growth exceeding 25% in 2019.”

Manufacturing at Huawei in Dongguan appears to be close to resuming normal levels of operation, although installation activity underway in China is still not clear. Ciena indicated a revenue impact of $30M during an earnings call in early March. It’s unclear right now what the ultimate impact will be; time will tell. We will revisit projections in April with the hope that events will be more certain at that time.

OFC was severely impacted when almost all major exhibitors pulled out of the show as health concerns mounted. The organizers did an admirable job of salvaging the technical sessions via Zoom teleconference.

Cignal AI will deliver a wrap-up report summarizing many of the important announcements that companies intended to make during the show. Look for it in the coming weeks, and if you have important news or perspective to share – contact us!

……………………………………………………………………………………………

Separately, a newly released report by 650 Group states that the Optical Transport Network market revenues increased 5% Y/Y in 4Q19. Revenues in four of the six geographic theatres experienced year over year growth, with North America having been the most robust.

“For the full year 2019, the top five Hyperscalers experienced the most growth out of any customer segment we track and has consistently been a top-performing customer segment in recent years,” said Chris DePuy, Technology Analyst and Founder at 650 Group. “Top vendors in the market are expecting their 800 Gbps optical transport technology to contribute to revenues towards the end of this year, 2020. We expect that optical transport systems companies that ship this new technology early will be well-positioned to take on the potential substitution threat of optical modules on switches and routers in the coming years.”

The forecast section of this report has been updated to reflect changes in both demand and supply related to health fears that have emerged in 1Q20. The report also reflects quantitative Data Center Interconnect (DCI) deployment scenarios across long-haul, metro, cloud, colocation, and telecom service providers.

For more information about the report, contact:

[email protected] or www.650group.com

Gartner: Top 10 Trends for Communications Service Providers (CSPs) in 2020

Key Findings:

-

Compared with previous cellular generations, the multilayered architecture of 5G creates opportunities for CSPs to expand beyond connectivity-centric solutions. However, disaggregation also allows new entrants to join incumbent CSPs in the 5G ecosystem.

-

Increasingly, network-based CSPs are exploring options to spin off network-related infrastructure into a separate entity, thereby unlocking funds needed for network upgrades and expansion while still meeting shareholder dividend commitments.

-

As live streaming of TV, games and e-sports enters the mainstream, the need to reduce latency and lower cost is driving hyperscale cloud providers, device manufacturers and developers to expand their influence out to the edge of CSPs’ networks.

-

Data, analytics and artificial intelligence (AI) now play an expansive and critical role in generating new business value, lowering costs and improving customer advocacy.

-

Cloud-native CSPs are emerging as aggressive challengers, and leading incumbent CSPs are expanding on efforts to virtualize their networks and adopt cloud-native capabilities.

Recommendations:

-

Pursue new capabilities and partnerships for 5G and streaming content by investigating how ecosystem approaches could be employed to meet business strategy goals.

-

Accelerate migration to cloud-native capabilities by appointing leaders who understand the business and technical implications that will arise.

-

Facilitate organizational alignment to become data-driven by establishing executive-level accountability and cross-functional oversight for data intelligence activities.

-

Maintain free cash flow from traditional telecommunications services by adopting automation, analytics and AI to improve operational efficiency and drive down costs.

Discussion:

Among the topics Gartner has observed as top of mind for CSPs include network virtualization and artificial intelligence. These are embellished in sections Becoming Data-Driven Becomes Critical and Cloud-Native as a Network Foundation, which explain the imperative needed to address what are becoming foundational capabilities. AI Enters the Workforce addresses the people context of AI, and how the move to automated provisioning and operations can, in the midterm, lead to augmentation, rather than wholesale replacement.

In the consumer market, digital content is well and truly dominating the strategy agenda. Livestreaming of TV, games, e-sports and other digital content is now mainstream. The need to improve performance and lower cost is driving the ecosystem of hyper-scale cloud providers, device manufacturers and developers to expand its influence into what was previously the exclusive domain of network-based CSPs.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

5G Assessment:

5G is viewed by mobile-network-based CSPs as a significant opportunity for growth, particularly in B2B. It also presents a challenge in terms of the level of investment required for coverage and capacity demands. At the same time, digital ecosystems are increasingly dominating the way industries function and, subsequently, how technology solutions are defined. This presents compelling opportunities for competitive market entrants looking to exploit opportunities to reinvent processes and define new operating models for industries.

-

Compared with previous cellular generations, the multilayered architecture of 5G (network plus software and services) creates opportunities for CSPs to expand beyond connectivity-centric solutions. However, disaggregation also allows new entrants to join incumbents in the 5G ecosystem.

-

CSPs aspire to derive value from 5G through enterprise solutions that expand the mobile ecosystem to new industries, enabling opportunities to participate in concepts such as factory of the future, autonomous transportation, remote healthcare, agriculture, digitized logistics and retail.

-

CSPs have found it difficult to identify strong monetization and operation efficiency opportunities for enterprise 5G, partly because of a lack of insight into key vertical markets.

5G improves drastically on previous generations of mobile cellular connectivity (3G and 4G), with peak data speeds of up to 20 Gbps, much higher network capacity and significantly lower latency. As such, 5G-capable handsets and smart devices will give rise to new experiences for consumers, such as gaming, esports, content streaming and virtual reality (VR), to name a few.

However, for CSPs, the enterprise segment will be key to monetizing higher-margin opportunities. To be successful, it will require a significant shift from 3G or 4G, where the focus was on delivering horizontal product and service offerings related to connectivity. By taking a platform approach to 5G, CSPs can potentially unlock new value through delivering industry-specific solutions.

The software-centric approach of disaggregating hardware and software (e.g. Open RAN) creates opportunities for new providers to offer solutions or services in the 5G ecosystem. It will enable enterprises to procure services from multiple providers in the ecosystem, enabling service flexibility and diversity, rather than being locked in with a single CSP.

The concept of 5G as a platform leverages a broad range of capabilities (beyond those related to connectivity, such as edge computing and network slicing). It also encompasses the use of data analytics, AI and machine learning, data aggregation, and service orchestration. Security will play an important role. Thus, the concept of 5G as a platform includes horizontal capabilities (common across industries) and vertical capabilities (specific to industries) that can enable CSPs to participate in emerging digital ecosystems.

Since the technology specifics of 5G are still a work in progress, there will be shifts in product or service offerings. Technology alliances and partnerships between diverse stakeholders are likely to arise. Such a nebulous market can be confusing for enterprises and participants, especially in the context of evolving standards.

An industry-platform-centric approach to 5G has the potential to enhance a CSP’s ability to deliver better business outcomes to their enterprise customers. However, new operating practices are required. The isolationist nature of processes, systems and methodologies within the network and IT will also need to be addressed (see “Unlocking the Value of Network and IT Fusion in CSPs”).

Most CSPs have begun implementing some of the foundational capabilities for treating 5G as a platform, such as software-defined networking and network function virtualization (NFV). These provide for the ability to divide services into smaller, software-driven functions, which allows businesses, operators and cloud providers to deploy and configure these services in a more-flexible manner. But again, these solutions and networks often lack interoperability.

Although it’s still early days for the 5G private network opportunity, regulators and standards bodies are beginning to put initiatives in place targeting this opportunity. CSPs have the potential to deliver turnkey network solutions into the industrial space. Equipment vendors would also have the option to do this directly.

Telenor deploys first commercial 5G network in Norway

On March 13th, Telenor Norway announced the commercial launch of a 5G network in nine towns and cities in Norway, following a 5G trial that began in Kongsberg in November 2018. Ericsson is Telenor’s 5G base station supplier.

………………………………………………………………………………………………………

“We are happy to announce that we have chosen Ericsson to start building the future 5G radio network in Norway, and I am confident we now are perfectly positioned to be in the forefront of the country’s network modernisation. As the first mobile operator on 5G in Scandinavia, Telenor will ramp up the roll out of 5G to our customers in Norway in 2020. The full modernisation of the mobile network in Norway is an ambitious undertaking, and something we are excited to get started on,” says Petter-Børre Furberg, CEO of Telenor Norway.

………………………………………………………………………………………………………

There are 38 5G base stations in Trondheim- Norway’s tech capital. The other 5G locations are Elverum, Askvoll, Svalbard, Kvitfjell, Heroya, Froya, and limited developments in the centres of Bodo and of Oslo, with Fornebu airport also served. Telenor will extend 5G in Oslo and open 5G networks in Bergen, Stavanger and Sandnes during 2020. In 2021, the operator will upgrade almost 2,000 base stations, rising to 8,500 over the next four to five years (see below for details).

![]()

“Telenor is proud to be the first mobile operator to launch a commercial 5G network in Norway, as we have worked tirelessly to stay at the forefront of the 5G development,” said Sigve Brekke, President and CEO of Telenor Group. “By bringing Norway into a new technological age, today’s opening marks another milestone in Telenor’s 165-year-long history. We expect 5G to be the key driver of transformation in this decade, and we are very much looking forward to continuing the roll-out of 5G to our customers.”

“Norway has some of the world’s fastest mobile networks, and with 5G, they become faster and even more reliable,” said Linda Hofstad Helleland, Norway’s Minister of Regional Development and Digitalisation. “Given the current situation in Norway, we see how important the digital infrastructure is for those quarantined and those working from home. The new 5G network will provide better mobile coverage and gradually better access to broadband across the country, which will reduce the vulnerability of an increasingly digitised society.”

“This is a day we have been looking forward to for a long time,” said Petter-Børre Furberg, CEO of Telenor Norway. “We launched our first 5G pilot as early as 2018, and since then we have been experimenting and exploring, trying to learn as much as we possibly can. Today, we are not only opening our 5G network in the city of Trondheim, we are also opening the very first commercial 5G network in Norway. In addition, we are making 5G commercially available in all locations where we, until now, have been running tests. As of today, Telenor customers with a 5G device will at these locations be able to connect to the mobile network of the future.”

Telenor said it will upgrade 8,500 base stations over the next few years. It remains to be seen how much of that work will be able to be done over the next few months, due to the coranavirus clamp downs.

“We have worked hard to become the first mobile operator in Norway to open the 5G network, and are now fully focused on our continued plans. During 2021, we will upgrade close to 2,000 base stations, while a total of 8,500 base stations will be upgraded within the next four to five years,” Furberg concluded.

…………………………………………………………………………………………………..

Telenor Norway and 5G:

- Telenor opened Scandinavia’s first 5G pilot in Kongsberg on 8 November 2018.

- Telenor launched Scandinavia’s largest 5G pilot in Elverum on September 26, 2019. In addition, Telenor announced pilots in nine further locations across the country and conducted Norway’s first video call over 5G.

- Telenor launched the world’s northernmost 5G pilot on the Norwegian archipelago of Svalbard.

- Telenor’s 5G network was commercially launched on 13 March 2020. Telenor customers with a 5G device can now connect to the next generation mobile network in nine different locations in Norway.

- Telenor will start development of 5G in Oslo, Bergen, Stavanger and Sandnes. The new mobile network will open in these cities during 2020.

- Telenor builds 5G in Trondheim in collaboration with Ericsson.

References:

Analysis: Nokia and Marvell partnership to develop 5G RAN silicon technology + other Nokia moves

Nokia has teamed up with semiconductor company Marvell Technology Group Ltd to develop customized 5G radio access system-on-chip leveraging its ReefShark technology. The alliance underscores Nokia’s commitment to deliver cost-effective and automated 5G network operations, especially at a time when it is aiming to walk the extra mile to revive its faltering 5G business.

As part of the agreement, Marvell Technology’s multi-core Radio Access Technology applications will be incorporated in Nokia’s AirScale RAN product line with its 5G-backed ReefShark portfolio. Equipped with customized ARM-architecture-based processor chips, this potential breakthrough innovation aims to deliver a best-in-class customer experience with reduced power consumption and enhanced performance and capacity.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Tommi Uitto, President of Mobile Networks at Nokia, said:

“This important announcement highlights our continued commitment to expanding the variety and utilization of ReefShark chipsets in our portfolio. This ensures that our 5G solutions are equipped to deliver best-in-class performance to our customers. As service providers continue to evolve their 5G plans and support growing traffic and new vertical services, the infrastructure and components must evolve rapidly. Adopting the latest advancements in silicon technology is a critical step to better serve our customers’ needs.”

“5G networks need to support billions of devices and machines, and this massive increase in volume and scale means that existing infrastructure and components must evolve rapidly, adopting technologies and techniques to enable to deploy 5G networks quickly, added Uitto.”

(Image credit: Nokia)

………………………………………………………………………………………………………………………….

Other Nokia Initiatives:

- Nokia also agreed to a partnership with Intel on programs to accelerate its 5G development. Intel’s new Atom chip is targeted at base stations. Nokia will ship Intel Atom-powered variants of its 5G AirScale radio access technology. The company will also use Intel’s second generation Xeon scalable processor in its AirFrame data center kit, allowing for common architecture from the cloud to the edge of 5G networks.

- Nokia said it needed several partnerships to enable it support and achieve its goals for 5G.

- Nokia will acquire optical networking technology provider Elenion. Nokia said that adding Elenion will broaden its addressable market and unlock some cost benefits.

- Nokia took a $561 million R&D loan which was signed with the European Investment Bank (EIB) in August 2018, but was only disbursed last month. The loan has an average maturity of about five years after disbursement according to Reuters. A Nokia representative said the company would use the loan to further accelerate its research and development of 5G technology

……………………………………………………………………………………………………………………………………………………………………………

Analysis by Zacks Equity Research:

Nokia has long struggled to undertake additional investments related to its 5G powered ReefShark SoCs. These SoCs are best known to leverage a single computer chip to operate an entire system. Unfortunately, its inability to develop ReefShark portfolio has hindered its cost-efficiency feature, compromising its profitability to rivals like Ericsson ERIC, which spends hefty amounts on R&D. Dearth of resources and geared up 5G spending cycle have also put Nokia at the risk of losing out on upcoming commercial launches.

The latest collaboration comes as a savior for the Finnish company to cater new vertical markets especially in the face of burgeoning network traffic and dynamic 5G plans. Dubbed as a key partnership, it is expected to reduce Nokia’s technical disparities and address the complex requirements of 5G NSA, SA, NR specifications for future 5G network deployments.

Nokia’s gross margin was negatively impacted by a high cost level associated with its first generation 5G products, product mix and profitability challenges in China. Despite a 4.2% rise in revenues in third-quarter 2019, the performance was marred by pricing pressure in early 5G deals and temporary capital expenditure constraints in North America related to the proposed merger of T-Mobile US and Sprint. This was followed by its decision to suspend dividend payments and slash guidance for 2020. The company has also decided to retrench about 180 employees in order to trim operating costs.

It remains to be seen whether Nokia will be able to script a turnaround amid a challenging macroeconomic environment and geopolitical uncertainties.

……………………………………………………………………………………………………………………………………………………………………………

About Marvell:

Marvell first revolutionized the digital storage industry by moving information at speeds never thought possible. Today, that same breakthrough innovation remains at the heart of the company’s storage, processing, networking, security and connectivity solutions. With leading intellectual property and deep system-level knowledge, Marvell’s infrastructure semiconductor solutions continue to transform the enterprise, cloud, automotive, industrial, and consumer markets. To learn more, visit: https://www.marvell.com/

About Nokia:

We create the technology to connect the world. Only Nokia offers a comprehensive portfolio of network equipment, software, services and licensing opportunities across the globe. With our commitment to innovation, driven by the award-winning Nokia Bell Labs, we are a leader in the development and deployment of 5G networks.

Our communications service provider customers support more than 6.1 billion subscriptions with our radio networks, and our enterprise customers have deployed over 1,000 industrial networks worldwide. Adhering to the highest ethical standards, we transform how people live, work and communicate. For our latest updates, please visit us online www.nokia.com and follow us on Twitter @nokia.

Media Inquiries:

Nokia Communications

Phone: +358 10 448 4900

Email: [email protected]

Marvell Communications

Phone: +1 408 222 8966

Email: [email protected]

……………………………………………………………………………………………………………………………………………………………………………

References:

https://www.zacks.com/stock/news/797965/can-nokia-revive-its-5g-business-with-marvell-partnership

https://www.techradar.com/news/nokia-secures-5g-chip-partnerships-with-intel-and-marvell