Ciena

VIAVI: 5G Service Now Reaches 1,662 Cities in 65 Countries

VIAVI today released new research demonstrating the accelerating pace at which 5G is growing, with coverage extending to an additional four countries and 301 cities worldwide since the beginning of this year. The new total — 1,662 cities across 65 countries — represents an increase of more than 20 percent during 2021 to date, according to the latest edition of the VIAVI report “The State of 5G,” now in its fifth year.

The top three countries that have the most cities with 5G coverage are China at 376, the United States at 284, and the Philippines with 95, overtaking South Korea which is now in fourth position with 85 cities. The APAC region remains in the lead with 641 cities, closely followed by EMEA at 623. The Americas region lags behind at 398 cities.

With the launch of commercial 5G services in four additional countries — Cyprus, Peru, Russia and Uzbekistan — well over a third of the world’s countries now have at least one live 5G network. However, the quality and speed of connectivity can vary significantly from region to region depending on available spectrum.

“Although we are seeing a significant jump in the number of networks being rolled out, not all 5G technologies are created equal,” said Sameh Yamany, Chief Technology Officer, VIAVI. “Networks operating in lower, mid and upper band frequencies perform very differently in terms of reach and throughput, increasing the importance of network assurance and optimization to consistently fulfill the promise of 5G.”

The latest edition of The State of 5G report is available here. The data was compiled from publicly available sources for information purposes only, as part of the VIAVI practice of tracking trends to enable cutting-edge technology development that allows communications service providers to command the 5G network.

This week during the Mobile World Congress in Barcelona, VIAVI is contributing to a demonstration of eMBB end-to-end testing with Rohde & Schwarz (Hall 3, Stand 3K30). VIAVI also will participate in a live panel discussion during the O-RAN ALLIANCE Industry Summit on June 29 to discuss the latest industry updates on the progress of O-RAN, and will showcase new virtual demos related to near-real-time RIC testing and deployment of an O-CU tester on edge infrastructure in the O-RAN Virtual Exhibition.

About VIAVI

VIAVI is a global provider of network test, monitoring and assurance solutions for communications service providers, enterprises, network equipment manufacturers, government and avionics. We help these customers harness the power of instruments, automation, intelligence and virtualization to Command the network. VIAVI is also a leader in light management solutions for 3D sensing, anti-counterfeiting, consumer electronics, industrial, automotive, and defense applications. Learn more about VIAVI at www.viavisolutions.com. Follow us on VIAVI Perspectives, LinkedIn, Twitter, YouTube and Facebook.

……………………………………………………………………………………………………………………………………………………………………………….

Only 19% of US business professionals claim to understand the benefits of 5G, according to a survey by Ciena, conducted in partnership with research firm Dynata. The survey found that there is an opportunity for telcos and the wider industry to better educate consumers on the full benefits that 5G can deliver, with:

- 41% of working professionals saying they only know a little bit about the benefits of 5G

- 32% of working professionals stating they have heard of 5G, but don’t understand what it is

- 8% of working professionals never having heard of 5G

Today, the main benefit that U.S. professionals associate with 5G is ‘faster access speeds’, which was cited by 61% of respondents. By contrast, only 6% of respondents considered ‘reduced latency (lag)’ to be a major benefit. Furthermore, only 18% of respondents said that they consider ‘more reliable connectivity’ to be a major benefit; and only 16% recognized ‘better wireless coverage’ as a major benefit. This illustrates a significant knowledge gap relating to 5G, both in terms of what it can deliver, and the terminology used to communicate the benefits.

Steve Alexander, Senior Vice President and Chief Technology Officer at Ciena, said: “5G is much more than just a faster wireless technology. 5G enables constant connectivity for people, machines and devices and is the infrastructure that the Internet of Things will rely on to create the cloud experience that we all need in our increasingly digital world. Yet, most professionals surveyed admit they don’t completely understand the broader benefits of 5G.”

“Fortunately, the data also highlighted the demand for 5G services, which could be leveraged – and indeed, driven – by providers effectively communicating the benefits and delivering the services users want, both humans and machines.”

Alexander at Ciena concluded: “People understand 5G will have an impact for closing the digital divide and providing a boost to major industries across the US. However, alongside delivering the scalable, intelligent, and adaptive infrastructures necessary to enable 5G, service providers and their trusted technology partners like Ciena must take steps to help close the knowledge gap.”

Notes To Editors

The survey was carried out by Dynata on behalf of Ciena, from April 13-23 2021 and included a representative sample of 1908 business professionals across the United States.

Ciena demo’s 45 wavelengths @400G; Joins Google’s Cloud’s 5G/Edge ISV Program

During OFC 2021 last week, Ciena and Lumenisity Ltd. said that they had partnered to demonstrate transmission of 45 wavelengths, each at 400G, over 1,000 km of hollowcore fiber cable.

The demonstration paired Lumenisity’s CoreSmart hollowcore cable with Ciena’s WaveLogic 5 Extreme and Nano coherent optical engines, with the transmission occurring in a recirculating loop. The companies say their work indicates that hollowcore fiber cable can be used for high-bandwidth, long-reach applications such as data center interconnect (DCI) in addition to edge and 5G xHaul applications Lumenisity had previously cited (see “Lumenisity, BT drive 400ZR DWDM transmission over hollowcore fiber“ and “BT testing hollowcore fiber for 5G support”).

Lumenisty said that it has been working over the past six months with ecosystem partners to test the CoreSmart low-latency hollowcore cable in its System Lab in Romsey, UK (see “Startup Lumenisity unveils hollowcore fiber cables for DWDM applications, new funding” for more on Lumenisity’s fiber). Ciena participated in at least some of those exercises, including a second trial in which the two companies achieved a capacity of 38.4 Tbps with 48x800G channels over greater than 20 km without in line amplification using the current generation of CoreSmart. Lumenisity says the next generation of CoreSmart will be able to extend reach in such an application to between 50-100 km with no inline amplification when paired with the WaveLogic 5 Extreme.

“The results obtained both internally and with Ciena commercial WaveLogic 5 systems show further evidence that we are bringing our world-class hollowcore fiber cable technology to market at an accelerating rate for multiple high-capacity applications, that solve real world latency issues for our customers,” commented Tony Pearson, business development director at Lumenisity.

“System characterization results of WaveLogic 5 Extreme programmable 800G and WaveLogic 5 Nano 400ZR coherent pluggables running over CoreSmart show promising results with hollowcore fiber now proven to preserve high-capacity while materially reducing latency,” added Steve Alexander, senior vice president and CTO of Ciena. “We are proud to be at the forefront of this breakthrough technological achievement where we can enable a 50% increase in reach for latency-sensitive data center interconnects.”

…………………………………………………………………………………………………………………………………….

Separately, CTO Alexander wrote a blog titled, “Ciena has joined Google Cloud’s 5G/Edge ISV Program to help enterprises accelerate migration of their IT resources to the cloud“

Here’s an excerpt:

To facilitate the migration of enterprise IT workloads to the cloud, there is a requirement for higher speed connections from the enterprise edge to cloud provider that are scalable with enhanced security to best protect critical business data. Shared IP network connections to the cloud are acceptable for lower speed (10Gb/s) connections and below. However, when secure, higher speed connections are required to the cloud, connectivity via the IP network can become overly complex, expensive, and inefficient when compared to the optical network (Optical Fast Lane) that can provide a more efficient, cost-effective, and secure option for enterprises needing to reduce their workload migration times to support their evolving business objectives.

For the multi-cloud market to succeed, it must reduce the friction for enterprises to migrate their workloads to a cloud provider, as well as between cloud providers – on demand. This is analogous to the days when you had a mobile plan with one carrier, and to switch to another carrier, you had to switch mobile numbers, which was too complex for most customers, so they stuck with their existing carrier. Only when consumers could keep their phone number when they switched carriers (through Local Number Portability), did it make the mobile market truly competitive leading to improved choice, pricing, and innovation. This is what we’re trying to achieve in the multi-cloud market.

Google Cloud is one of the leading cloud providers in the market that embraces an architecture that enables their enterprise customers to gracefully migrate their workloads to Google Cloud via an Optical Fast Lane that enables Enterprise to develop and leverage the Google Cloud for new and innovative applications. Ciena is excited to be a key player in this program and in addressing this opportunity in the industry. This builds off Ciena’s long standing relationship with Google and other Cloud Providers serving both private and managed high-capacity optical transport networks – principally dominated by subsea, long-haul, metro and DCI connectivity.

Ciena is also a major supplier to Communication Service Providers (CSPs) and MSOs – serving all segments of the network – including high-speed access connectivity for Enterprises as well as cell-site routing and backhaul. In partnership with CSPs, Google Cloud is helping customers leverage their edge real-estate assets to facilitate low latency connectivity to Google Cloud and reduce the friction required for enterprises to improve their mean time to the cloud for their data and workloads.

………………………………………………………………………………………………………………….

References:

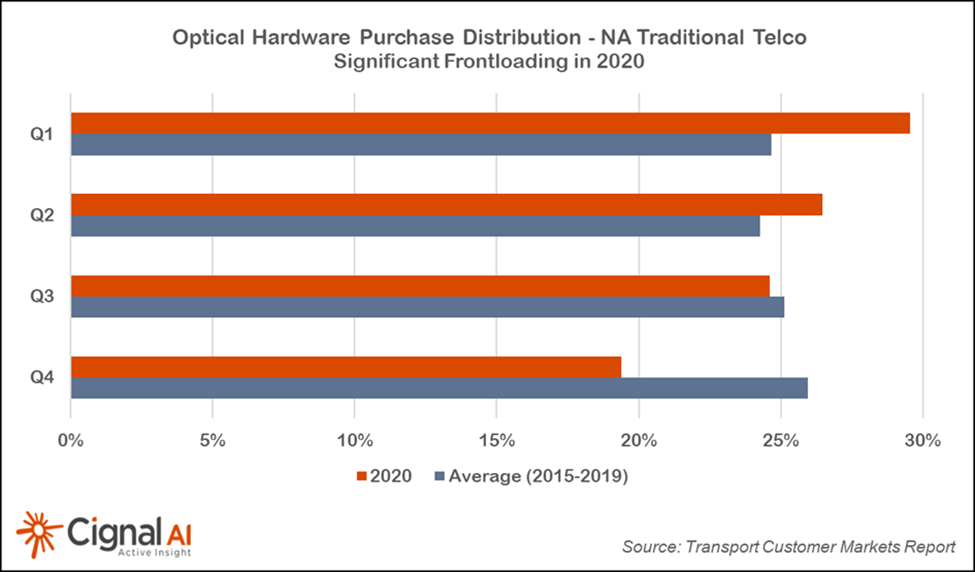

North American Cloud and Traditional Telco CapEx Drops in 4th Quarter 2020

Subhead: Exceptional 4Q Cloud & Colo Operator Spending in APAC

|

||||

|

||||

More Key Findings from the 4Q20 Transport Customer Markets Report:

Separately, Cignal AI said on March 16th that Ciena’s revenue decline this quarter was steeper than forecast, but the company is poised to grow revenues based on the success of its WaveLogic 5e fifth generation coherent technology. On March 2nd, Cignal AI said that Infinera originally expected its ICE6 technology to enter the market in the second half of 2020. The company’s current guidance now indicates a 2H21 arrival. Infinera reports a strong order pipeline, but has not specified exactly when the first ICE6 will ship for revenue. About the Transport Customer Markets Report:

About Cignal AI:

References:https://cignal.ai/opteq-hw-dashboard/https://cignal.ai/free-articles/

|

LG U+ first to deploy 600G backbone network in Korea with Ciena’s ROADM equipment

South Korea network operator LG U+ today announced it is the first carrier in South Korea to deploy 600Gb/sec on a single wavelength for long haul, using Ciena’s WaveLogic 5 technology. LG U+ made this upgrade to support remote experiences.

The company will establish a ROADM (Re-configurable Optical Add-Drop Multiplexer) backbone network to strengthen the competitiveness of business. LG U+’s newly constructed and dedicated nationwide ROADM backbone network will satisfy the needs of customers and preemptively respond to increased traffic following the introduction of the remote era. For this network transformation, LG U+ has selected Ciena’s WaveLogic 5 Extreme and WaveLogic Ai coherent optical solutions.

Sung-cheol Koo who’s in charge of LG U+’s wired business said, “Amid the expansion of cloud services such as telecommuting, video conferencing and remote classes, we are building a new backbone network that can accommodate the needs of various corporate customers. With a flexible and stable transmission network, we expect that companies can provide a higher level of service.”

LG U+ also applied the Optical Time Domain Reflectometer (OTDR) technology, which measures the loss of optical lines, disconnection points, and distances across the entire section of the new backbone network. By intuitively monitoring the condition of the line in real time, it is possible to shorten the response time in case of a failure.

With rapidly increasing traffic, Ciena will enable LG U+ to transmit single-carrier 600G wavelengths over the new flexible grid backbone that has six times the network capacity compared to the existing network. The new backbone network will provide enhanced availability through low-latency, multiple route diversity and direct connections between large cities without the need for regeneration.

LG U+ is in the process of implementing a major capacity upgrade, including multi-terabits of additional capacity, to accommodate large-capacity customers and enable stable traffic management. By applying OTDR (Optical Time Domain Reflectometer) technology to all sections of the backbone network, real-time and intuitive line condition monitoring is possible to shorten troubleshooting time and enable smooth network management and operations.

In addition, Ciena’s 6500 ROADM equipment can reliably configure DR (Disaster Recovery) line services to public government, financial institutions and compute centers of large enterprises through third party interworking certification. LG U+ can also provide a dedicated line service with enhanced security through optical transport encryption.

In addition, Ciena’s 6500 ROADM equipment can reliably configure DR (Disaster Recovery) line services to public government, financial institutions and compute centers of large enterprises through third party interworking certification. LG U+ can also provide a dedicated line service with enhanced security through optical transport encryption.

LGU+ will be using Ciena’s Manage, Control and Plan (MCP) SDN controller to be able to automate service delivery via next-generation OPEN APIs to improve customer experience and increase operational efficiencies.

References:

https://www.ciena.com/about/newsroom/press-releases/lg-u-builds-new-nationwide-backbone-network.html

Ciena and TELUS demo 800Gbps fiber optic transmission over 970km link from Toronto to Quebec City; Ciena Earnings & Guidance

Ciena claims to have achieved a worldwide transmission record of 800 Gbps with TELUS, over a record-breaking 971.2km distance. Teams from both organizations worked together and turned up an 800G wavelength from Toronto to Quebec City.

TELUS is one of the early 800 Gbps technology adopters who is in the process of augmenting their network with Ciena’s WaveLogic5 Extreme (WL5e). TELUS will be standardizing WaveLogic 5 Extreme for deployment in the near future. Part of the standardization activities include testing the full capabilities of the product to plan end user service offerings.

TELUS supports 15.3 million customer connections spanning wireless, data, IP, voice, television, entertainment, video and security. The TELUS network extends 6,000 km from Victoria, British Columbia to Halifax, Nova Scotia. Designed with the future in mind, TELUS’s next generation optical network consists of a state-of-the-art, colorless, directionless, contentionless, flexible grid (CDC-F) ROADM architecture with Layer 0 Control Plane, designed to support reliable, fast turn-up and re-route of unpredictable bandwidth demands across the network. Furthermore, it is ready to support new innovations in optical technologies as they become available, including the ability to carry optical channels of any spectrum size across the fiber. This fully flexible, intelligent photonic infrastructure allows for the simple addition of WL5e wavelengths and with that, access to significant cost, footprint, and power benefits.

“TELUS prides itself on having one of the world’s fastest networks and using industry-leading technology to deliver the best experience for our customers across Canada. Our collaboration with Ciena on breaking transmission records is an exciting innovation that speaks to both teams track records of success,” said Ken Nowakowski, Director Planning and Engineering, Transport and IP Infrastructure Development and Operations at TELUS.

Testing continues at TELUS, with planned deployment of WL5e in the coming months. Does this mean 800G will be deployed across long haul links? This is not a yes or no response, but 800G will be deployed where it makes sense in the TELUS network. As has always been the case, the line rate capacity that will be deployed depends on specific link characteristics, number of channels and desired reserved margin by the operator.

Ciena 6500 shelves with WaveLogic 5 Extreme

The real news here is the resulting long-term benefits of the WL5e network upgrade for both TELUS and their end users. TELUS can continue to provide high quality, high speed connectivity to their end users – such as teleworker videoconferencing, multi-player interactive gaming, Internet access for low income families, and even live-streaming the Stanley Cup playoffs – while more efficiently using bandwidth resources and evolving to a greener network.

……………………………………………………………………………………………………………………………………………………………………………………….

Separately, Ciena announced earnings today. For the fiscal third quarter ended Aug. 1, Ciena (ticker: CIEN) reported revenue of $876.7 million, up 1.7% from a year earlier, and ahead of the Wall Street analyst consensus at $971.8 million. Non-GAAP profit was $1.06 a share, nicely above the Street consensus at 83 cents.

“Operating conditions have complicated and extended the time required to deploy and activate new equipment and services with many of our large and long-standing international customers,” the company said in a presentation prepared for its earnings call with analysts on Thursday. “Conditions have made it more challenging to ramp up and operationalize some of our newer international deals and customer wins on their original timelines.”

Ciena also said “customer uncertainty around broader economic conditions is driving more cautious spending behaviors.” It said “longer term fundamental drivers—increasing network traffic, demand for bandwidth and adoption of cloud architectures—remain strong.” Ciena CEO Gary Smith said Covid-19-related market dynamics were likely to adversely impact revenue “for a few quarters.”

Here are a few data points from the company’s earnings presentation:

- Non-telco represented 43% of total revenue

- Direct web-scale contributed 25% of total revenue

- MSO’s contributed 9% of total revenue

- Americas revenue up 9% YoY

- TTM Adjusted R&D investment was $518M

- 535 100G+ total customers, which includes 37 new wins on WaveLogic Ai and 27 new wins on WaveLogic 5e in Q3-2020

- Shipped WL 5 Extreme to almost 40 customers, and the technology is live and carrying traffic in several networks

……………………………………………………………………………………………………………………………………………………………………………………………………..

Overview of Ciena’s Technology Portfolio:

PROGRAMMABLE INFRASTRUCTURE:

Converged Packet-Optical Networking: Software-defined platforms, featuring Ciena’s award-winning WaveLogic™ Photonics and agnostic packet/OTN switching, designed to maximize scale, flexibility and openness. Optimizes network performance from the access edge, along the backbone, and across ocean floors.

Packet Networking: Purpose-built platforms hosting a common Service-Aware Operating System that are the building blocks for low-touch, high-velocity Ethernet/MPLS/IP access to metro networks.

SOFTWARE CONTROL AND AUTOMATION:

Open software that includes Blue Planet® multi-domain orchestration, inventory, and route optimization to support the broadest range of closed-loop automation use cases across multi-layer, multi-vendor networks, as well as Ciena’s Manage, Control and Plan (MCP) domain controller for bringing software-defined programmability to next-gen Ciena networks.

ANALYTICS AND INTELLIGENCE:

Blue Planet Unified Assurance and Analytics: An open suite of software products that unifies multilayer, multi-domain assurance with AI-powered analytics to provide unprecedented insights that help transform and simplify business operations for network providers.

INNOVATION AND THE ADAPTIVE NETWORK:

▪ WaveLogic™ roadmap extends beyond 400G and with multiple form factors

▪ Adaptive IP™ capabilities for Packet Networking to address fiber densification (5G & Fiber Deep)

▪ Blue Planet® Intelligent Automation Portfolio and closed-loop automation capability strengthened with recent acquisition of Centina

References:

Century Link selected by Internet2 for Advanced Optical Fiber & Professional Services

Internet2, a non-profit, member-driven advanced technology community, selected CenturyLink to provide the fiber network and related professional services for the technology community’s network infrastructure. Contractual fiber-use agreements extend through at least 2042.

The forthcoming Internet2 network will use the company’s low-loss optical fiber for the majority of its footprint. CenturyLink’s optical fiber is ITU-T G.652.D compliant and designed to be optimized for high bit rate coherent systems using advanced modulation schemes supporting 100G and above. Internet2 also chose CenturyLink to provide the professional services to migrate to the new platform, which will be equipped with a flex-grid open-line system from Ciena.

“We believe the combination of the most advanced fiber from CenturyLink with the latest coherent transmission technologies from Ciena provides enormous opportunities to enable research and academic pursuits in the United States,” said Rob Vietzke, vice president of network services for Internet2, in a prepared statement.

“Whether it is tracking the origins of Neutrinos in the Antarctic, comparing gene sequences or studying the climate, this new optical network, with its ability to span very long distances at very high bandwidths [with] improved efficiency, is essential to providing the best research infrastructure for data-intensive science on the globe.”

Map of Internet2® Network Advanced Layer 1 Service, December 2019 (Source: CenturyLink) – Image courtesy of Matthew Wilson

……………………………………………………………………………………………………….

Internet2’s core infrastructure components include the nation’s largest and fastest research and education network. The network currently connects 321 U.S. universities, 60 government agencies, 43 regional and state education networks and through them supports more than 100,000 community anchor institutions, among others.

“One of America’s leading research and education organizations (Internet2) placed its trust in CenturyLink to upgrade its network to a high-speed, high-capacity, fiber-optic network that will support today’s leading-edge research projects,” said Sonia Ramsey, CenturyLink’s vice president for the state and local government and education market. “Internet2’s selection of CenturyLink recognizes the company’s long-standing relationship with the research and education community and our commitment to meet the community’s ever-increasing advanced technology needs,” she added.

CenturyLink recently overpulled a large portion of its national fiber footprint and also realigned amplifier spacing to create more efficient resources for optimized optical networks. Internet2 will migrate its segments to the new fiber on all available segments and continue to work with CenturyLink to migrate the remaining segments as their build-out continues.

With the low-loss optical fiber and the upgraded optronics kit, Internet2 will have the ability to reach anywhere on its domestic footprint with an unregenerated wavelength of up to 200G. Many high-use spans on Internet2’s Network will also support 400G and 800G wavelengths with existing technologies and higher bitrates are expected in the coming years as new DSP technology comes into production. Internet2 has been able to achieve unregenerated spans without employing Raman amplification, a reduction in complexity and improved efficiency both at installation and for ongoing operations.

…………………………………………………………………………………………………..

About Internet2:

Internet2® is a non-profit, member-driven advanced technology community founded by the nation’s leading higher education institutions in 1996. Internet2 serves 321 U.S. universities, 60 government agencies, 43 regional and state education networks and through them supports more than 100,000 community anchor institutions, over 1,000 InCommon participants, 56 leading corporations working with our community, and 70 national research and education network partners that represent more than 100 countries.

Internet2 delivers a diverse portfolio of technology solutions that leverages, integrates, and amplifies the strengths of its members and helps support their educational, research and community service missions. Internet2’s core infrastructure components include the nation’s largest and fastest research and education network that was built to deliver advanced, customized services that are accessed and secured by the community-developed trust and identity framework.

Internet2 offices are located in Ann Arbor, Mich.; Denver, Colo.; Washington, D.C.; and West Hartford, Conn. For more information, visit www.internet2.edu or follow @Internet2 on Twitter.

About CenturyLink:

CenturyLink is a technology leader delivering hybrid networking, cloud connectivity, and security solutions to customers around the world. Through its extensive global fiber network, CenturyLink provides secure and reliable services to meet the growing digital demands of businesses and consumers. CenturyLink strives to be the trusted connection to the networked world and is focused on delivering technology that enhances the customer experience. Learn more at http://news.centurylink.com/.

Media Contact

Sara Aly, Internet2

[email protected]

References:

IHS Markit: Ciena tops the list of optical equipment vendors + Cignal AI’s OFC Preview

By Heidi Adams, executive director, network infrastructure, IHS Markit

Each year IHS Markit surveys service providers, in order to find out which companies they view as the leaders of the optical equipment market. The survey also explores their perceptions of vendors in key decision metrics, like pricing, total cost of ownership, technology innovation, research-and-development (R&D) investment, and product reliability.

Following are some of the key findings from this year’s survey:

Optical equipment vendor leaders:

In brand awareness, respondents perceive Ciena, Huawei, and Nokia as the overall leaders for optical transmission and switching equipment in 2018, with no change in the rankings from last year. These results are well aligned with positioning in the global optical network hardware market in the first three quarters of 2018, where Huawei, Ciena, and Nokia were ranked as the top three vendors by market share in this period.

Ciena was the most cited leader in optical DCI, with Huawei and Infinera tied for second place. Ciena also made significant strides this year in market perception for leadership in optical disaggregation, rising from third position in our 2017 survey to first-ranked position in 2018. Coriant (now Infinera), Huawei and Nokia all tied for second place.

Purchasing criteria:

IHS Markit survey respondents were also asked to identify the leaders in purchasing criteria, including pricing, technology innovation, product reliability, service and support and investment in research and development. The top three vendor selection criteria for optical equipment purchasing decisions in 2018 were, as follows:

- Product reliability

- Pricing

- Total cost of ownership

Ciena was the leader in 2018 for service provider perception of vendor leadership in product reliability, technology innovation, management software, and investment in research and development. Huawei topped the list for service provider perception of vendor leadership in pricing, total cost of ownership, solution breadth, and financial stability. Nokia was perceived as the leader in service and support for optical networks.

Optical Equipment Vendor Leadership Service Provider Survey – 2018

This survey explores how service providers evaluate and select optical transmission and switching equipment suppliers. It covers vendors installed and under evaluation and service provider opinions of vendors, including on key vendor selection criteria.

…………………………………………………………………………………………………………………………………………………

Cignal AI on OFC 2019–

400ZR Steals the Show:

No single topic at OFC will command as much attention as 400ZR, which is based on fourth-generation coherent technology and an OIF standard for coherent short reach DCI applications. Product development is well underway with over a dozen component and equipment companies spending in excess of $300M in this effort. The market for short reach coherent extends well beyond the DCI needs of Microsoft and Google. Derivatives (known as ZR+ or ZR plus) are emerging which are designed to meet the broader needs of network operators everywhere. ZR is the first coherent technology that will be both standardized and pluggable, and the emergence of ZR products will shake up the optical equipment landscape. One major impact is that 10G WDM will become obsolete in its only remaining stronghold- the edge of the optical network. The greater question is what role standalone optical hardware will play in the network as the performance and interoperability of coherent pluggables improve. Expect a cascade of activity at OFC from component and equipment companies as they uncover their ZR plans and demonstrate the latest optical engines, and some bombshell announcements and partnerships from the leaders in this space – Inphi, Acacia, Ciena, Cisco, Huawei, Nokia, and NTT Electronics.

While fourth-generation 400G products have been announced at OFC already for the last two years, 2019 is the year that these products start deploying for revenue. Starting in early 2019, third generation solutions from Acacia (via multiple hardware vendors), Nokia, Huawei, Fujitsu, and Infinera will join Ciena in live network deployments. Now that 400G is deployed, there will be multiple roadmap announcements at OFC seeking to leapfrog 400G and propose the next generation of coherent optical speeds. 600G is a given, but there will be 800G and perhaps 1Tbps announcements as well. Components suppliers and equipment manufacturers will show roadmaps to higher speed sixthgeneration coherent optical components in preparation for a 2020 introduction.

We expect Infinera to disclose more detail on its ICE6 R&D efforts and would not be surprised to hear Ciena talk about a successor to the Wavelogic AI now that competitive products are arriving in the market.

Disaggregation Continues, with Many Definitions:

The disaggregation trend will continue to gain strength at OFC, but the definition will continue to change. Whereas the original concept was complete separation of switching transponders, ROADMs, and perhaps even components into separately manageable elements, now new solutions are starting to look more like traditional optical equipment. Compact modular systems, which are the most visible components of a disaggregation strategy, have moved from monolithic transponder or open line systems to more complex devices that can include switching and multiple functions in the same shelf. Some systems now even have modularity via cards (although they are called “sleds” rather than “cards”), making them look more like traditional systems in everything but physical dimensions. Several large operators are skeptical about disaggregation, while several others agree with the concept but consider current solutions too difficult to manage. Regardless, the industry-wide shift to disaggregation will accelerate as implementation becomes easier and better attuned to the needs of a wider variety of customers. General availability and customer announcements for 2019 are expected from several vendors, including ADVA, Cisco, Coriant, Fujitsu, and Nokia. In addition to the compact modular announcements,