AT&T, Verizon, Spectrum Enterprise lead in fiber lit business connections; M&A in 2017

Vertical Systems Group (VSG) ranked the leading providers of on-net fiber business connections as of the end of 2016. The research group said that retail and wholesale fiber providers with 10,000 or more on-net fiber-lit commercial buildings in the U.S. qualify for this new benchmark.

VSG’s 2016 U.S. Fiber Lit Buildings LEADERBOARD list includes a mixture of traditional telcos, cable providers and a competitive carrier: AT&T, Verizon, Spectrum Enterprise were the top three followed by CenturyLink, Comcast, Level 3, Cox, Lightower Fiber Networks, Zayo, Altice USA and Frontier.

The Challenge Tier of fiber providers includes companies with lit fiber connections to between 2,000 and 9,999 U.S. commercial buildings. Seventeen companies qualified for the 2016 Fiber Lit Buildings Challenge Tier as follows (in alphabetical order): Cincinnati Bell, Cleareon, Cogent, Consolidated Communications, Electric Lightwave, Fairpoint, FiberLight, FiberNet Direct, FirstLight, IFN, Lumos, Southern Light, Sunesys, Unite Private Networks, Uniti Fiber, Windstream and XO.

………………………………………………………………………………………………………..

Rosemary Cochran, principal at Vertical Systems Group, said the criteria for the leader board list was for network service providers to have fiber installed and fiber transport equipment ready to serve business customers.

“This is commercial buildings and data centers that have fiber in place and there is active service equipment that enables provisioning of commercial services,” Cochran said. “We’re not counting residential fiber or standalone cell towers.”

Cochran added that VSG is not counting near-net buildings where service providers may be passing buildings with fiber but have not connected them yet. “It is either lit or not lit,” she said.

“On-net fiber lit buildings are valued strategic assets that give retail and wholesale providers a competitive edge in profitably delivering services to business customers. A major benefit of a fiber lit building is ready connectivity with provisioning through service orchestration, without the construction cost and extensive lead time required to light a building,” Cochran added.

………………………………………………………………………………………………………

Acquisitions of Fiber Providers happening this year:

“These dynamics are driving this year’s acquisitions among fiber providers that will significantly impact the U.S. fiber landscape. Eighteen of the twenty-eight Fiber LEADERBOARD and Challenge Tier companies have fiber-related transactions just completed or pending.”

One of the largest out of this group is CenturyLink’s pending deal for Level 3, one that will enhance the telco’s on-net fiber footprint.

CenturyLink’s Level 3 acquisition will increase its reach by nearly 75% to approximately 75,000, including 10,000 buildings in EMEA and Latin America, giving the telco a larger footprint to deliver Ethernet and software-defined services.

Some of the other acquisitions that will alter the on-net fiber profile will be Verizon’s recently completed purchase of XO Communications and Crown Castle’s pending acquisition of Lightower.

By purchasing XO, Verizon gained metro fiber networks in 40 major U.S. markets with over 4,000 on-net buildings and 1.2 million fiber miles.

Cochran said that since a number of these deals have not been completed it remains unclear as to what effect they will have.

Crown Castle, which will gain an additional 22,000 buildings, stands out from the crowd since the service provider has been operating the fiber providers it has bought as separate companies.

However, other pending acquisitions being made by Consolidated Communications, Cincinnati Bell and newer players like Uniti Fiber will have an effect.

Consolidated Communications, which will announce its second-quarter earnings tomorrow, recently completed its acquisition of FairPoint. By acquiring FairPoint, Consolidated immediately established itself as the ninth largest fiber player with a presence in 24 states and 8,000 on-net buildings. This greater density will enable Consolidated to pursue more dark fiber and lit Ethernet service opportunities with a larger mix of business and wholesale customers.

“Out of the companies on the leader board, 18 of them either already completed acquisitions or some are pending,” Cochran said. “Because a lot of deals happened in July with some that are pending such CenturyLink/Level 3, they are not reflected here.”

………………………………………………………………………………………………………..

Strategic importance of Fiber Assets to deliver business services:

Regardless of when these deals are completed, Cochran added that they show how having a large arsenal of fiber is important to compete for business services.

“There’s a lot that happened in the first half of this year and that’s going to shake things up,” Cochran said. “Just the fact that you have more than half of these companies involved in some kind of transaction shows the value of fiber.”

On the fiber leaderboard, 7 service providers have an ongoing spot on VSG’s Carrier Ethernet Leaderboard report. These providers include: AT&T, Verizon,Spectrum Enterprise, CenturyLink, Comcast, Level 3, and Cox.

Cochran noted that the presence of fiber has coincided with the growth of Ethernet in the domestic U.S. market.

“Fiber-based Ethernet is the most widely deployed technology,” Cochran said. “As those upgrades take place, one of the drivers is trying to get more bandwidth so there’s a correlation between higher bandwidth services and having that fiber in the building.”

“Wholesale services are also a big driver, which becomes a question of service provisioning. The work that’s being done at the MEF on inter-carrier provisioning and service orchestration across carriers to automate it with standard APIs would help to accelerate new services,” she added.

………………………………………………………………………………………………..

Other Fiber Providers:

All other fiber providers with fewer than 2,000 U.S. commercial fiber lit buildings are in the Market Players tier. The 2016 Market Players tier includes more than two hundred metro, regional and other fiber providers, including the following companies (in alphabetical order): Alpheus, Axia, Birch, C Spire, Centracom, Conterra, DQE Communications, EarthLink Business, Fatbeam, Global Capacity, GTT, Hawaiian Telecom, Hibernia, Hunter Communications, Independents Fiber Network, Infostructure, Logix Communications, LS Networks, Mediacom, Monmouth Telecom, Orca Communications, Pilot Fiber, PS Lightwave, Shentel, Silver Star Telecom, Sovernet, Spirit/Palmettonet, Syringa, TDS Telecom, TPX Communications, U.S. Signal, Veracity, Wilcon, WOW and others.

References:

https://www.verticalsystems.com/vsglb/u-s-fiber-lit-buildings-leaderboard/

AT&T, Verizon, Spectrum Enterprise lead in fiber lit business connections; M&A in 2017

Vertical Systems Group (VSG) ranked the leading providers of on-net fiber business connections as of the end of 2016. The research group said that retail and wholesale fiber providers with 10,000 or more on-net fiber-lit commercial buildings in the U.S. qualify for this new benchmark.

VSG’s 2016 U.S. Fiber Lit Buildings LEADERBOARD list includes a mixture of traditional telcos, cable providers and a competitive carrier: AT&T, Verizon, Spectrum Enterprise were the top three followed by CenturyLink, Comcast, Level 3, Cox, Lightower Fiber Networks, Zayo, Altice USA and Frontier.

The Challenge Tier of fiber providers includes companies with lit fiber connections to between 2,000 and 9,999 U.S. commercial buildings. Seventeen companies qualified for the 2016 Fiber Lit Buildings Challenge Tier as follows (in alphabetical order): Cincinnati Bell, Cleareon, Cogent, Consolidated Communications, Electric Lightwave, Fairpoint, FiberLight, FiberNet Direct, FirstLight, IFN, Lumos, Southern Light, Sunesys, Unite Private Networks, Uniti Fiber, Windstream and XO.

………………………………………………………………………………………………………..

Rosemary Cochran, principal at Vertical Systems Group, said the criteria for the leader board list was for network service providers to have fiber installed and fiber transport equipment ready to serve business customers.

“This is commercial buildings and data centers that have fiber in place and there is active service equipment that enables provisioning of commercial services,” Cochran said. “We’re not counting residential fiber or standalone cell towers.”

Cochran added that VSG is not counting near-net buildings where service providers may be passing buildings with fiber but have not connected them yet. “It is either lit or not lit,” she said.

“On-net fiber lit buildings are valued strategic assets that give retail and wholesale providers a competitive edge in profitably delivering services to business customers. A major benefit of a fiber lit building is ready connectivity with provisioning through service orchestration, without the construction cost and extensive lead time required to light a building,” Cochran added.

………………………………………………………………………………………………………

Acquisitions of Fiber Providers happening this year:

“These dynamics are driving this year’s acquisitions among fiber providers that will significantly impact the U.S. fiber landscape. Eighteen of the twenty-eight Fiber LEADERBOARD and Challenge Tier companies have fiber-related transactions just completed or pending.”

One of the largest out of this group is CenturyLink’s pending deal for Level 3, one that will enhance the telco’s on-net fiber footprint.

CenturyLink’s Level 3 acquisition will increase its reach by nearly 75% to approximately 75,000, including 10,000 buildings in EMEA and Latin America, giving the telco a larger footprint to deliver Ethernet and software-defined services.

Some of the other acquisitions that will alter the on-net fiber profile will be Verizon’s recently completed purchase of XO Communications and Crown Castle’s pending acquisition of Lightower.

By purchasing XO, Verizon gained metro fiber networks in 40 major U.S. markets with over 4,000 on-net buildings and 1.2 million fiber miles.

Cochran said that since a number of these deals have not been completed it remains unclear as to what effect they will have.

Crown Castle, which will gain an additional 22,000 buildings, stands out from the crowd since the service provider has been operating the fiber providers it has bought as separate companies.

However, other pending acquisitions being made by Consolidated Communications, Cincinnati Bell and newer players like Uniti Fiber will have an effect.

Consolidated Communications, which will announce its second-quarter earnings tomorrow, recently completed its acquisition of FairPoint. By acquiring FairPoint, Consolidated immediately established itself as the ninth largest fiber player with a presence in 24 states and 8,000 on-net buildings. This greater density will enable Consolidated to pursue more dark fiber and lit Ethernet service opportunities with a larger mix of business and wholesale customers.

“Out of the companies on the leader board, 18 of them either already completed acquisitions or some are pending,” Cochran said. “Because a lot of deals happened in July with some that are pending such CenturyLink/Level 3, they are not reflected here.”

………………………………………………………………………………………………………..

Strategic importance of Fiber Assets to deliver business services:

Regardless of when these deals are completed, Cochran added that they show how having a large arsenal of fiber is important to compete for business services.

“There’s a lot that happened in the first half of this year and that’s going to shake things up,” Cochran said. “Just the fact that you have more than half of these companies involved in some kind of transaction shows the value of fiber.”

On the fiber leaderboard, 7 service providers have an ongoing spot on VSG’s Carrier Ethernet Leaderboard report. These providers include: AT&T, Verizon,Spectrum Enterprise, CenturyLink, Comcast, Level 3, and Cox.

Cochran noted that the presence of fiber has coincided with the growth of Ethernet in the domestic U.S. market.

“Fiber-based Ethernet is the most widely deployed technology,” Cochran said. “As those upgrades take place, one of the drivers is trying to get more bandwidth so there’s a correlation between higher bandwidth services and having that fiber in the building.”

“Wholesale services are also a big driver, which becomes a question of service provisioning. The work that’s being done at the MEF on inter-carrier provisioning and service orchestration across carriers to automate it with standard APIs would help to accelerate new services,” she added.

………………………………………………………………………………………………..

Other Fiber Providers:

All other fiber providers with fewer than 2,000 U.S. commercial fiber lit buildings are in the Market Players tier. The 2016 Market Players tier includes more than two hundred metro, regional and other fiber providers, including the following companies (in alphabetical order): Alpheus, Axia, Birch, C Spire, Centracom, Conterra, DQE Communications, EarthLink Business, Fatbeam, Global Capacity, GTT, Hawaiian Telecom, Hibernia, Hunter Communications, Independents Fiber Network, Infostructure, Logix Communications, LS Networks, Mediacom, Monmouth Telecom, Orca Communications, Pilot Fiber, PS Lightwave, Shentel, Silver Star Telecom, Sovernet, Spirit/Palmettonet, Syringa, TDS Telecom, TPX Communications, U.S. Signal, Veracity, Wilcon, WOW and others.

References:

https://www.verticalsystems.com/vsglb/u-s-fiber-lit-buildings-leaderboard/

Comment & Analysis of Century Link’s 2nd Quarter results

broadband units. Consumer legacy revenue declined 8.8% Y/Y – lower access lines.

in employee-related expenses.

“We are confident our continued investment in high-quality, high-bandwidth broadband network infrastructure positions Century Link well for long-term growth,” said Glen F. Post, III, Century Link chief executive officer and president.

“Enterprise demand for high-bandwidth data services remains strong and, while consumer broadband units were weaker than expected, we are encouraged by the higher-value customers our improved offerings are attracting. We accelerated our capital investment in high-bandwidth services and broadband infrastructure during the second quarter, which we believe better positions us to increase revenues in the second half of 2017 and beyond. We anticipate second half and full year 2017 capital expenditures of approximately $1 billion and $2.6 billion, respectively.

“We achieved our expected adjusted EBITDA for the quarter as our employees did a great job managing costs, while core revenues were below our expectations primarily due to the decline in legacy revenues and the decline in broadband units being higher than anticipated. We continue to make good progress in obtaining the necessary approvals for the pending Level 3 acquisition, having received clearance in 23 of 25 required states and territories. Integration planning is progressing well and we continue to anticipate completing the acquisition by the end of September 2017. We remain excited about the value we believe this transaction will create for our customers, our shareholders and our employees,” concluded Mr. Post.

……………………………………………………………………………………….

Century Link’s presentation – 2ndQ 2017 Highlights & Trends:

1. Strategic services:

◦ Enterprise high-bandwidth data – solid growth in MPLS revenue offset by decline in Ethernet revenue; grew 5% Y/Y on a normalized basis

◦ IT & Managed services – continued growth in IT Services along with stabilization of managed hosting revenue

◦ Enterprise other strategic – ~$100 million Y/Y and Q/Q decline due to Colo-cation sale

◦ Consumer broadband – fewer subscribers Y/Y

◦ Consumer video – impact of satellite video contract restructuring

2. Acquisition of Level 3 Communications:

◦ Continued good progress in obtaining necessary approvals; received shareholder

approval and regulatory approvals/clearances in 23 states or territories, with 2 states

remaining

◦ Integration planning process continues to go well; remain confident with cash synergy target of $975 million

◦ Named combined company senior leadership team, effective at close; overall

organization design progressing well

◦ Continue to anticipate closing by end of September 2017

Forward Guidance:

Based on first half 2017 results and current expectations for the remainder of the year, Century Link anticipates coming in slightly below its full-year 2017 revenue and adjusted diluted EPS guidance, primarily driven by higher legacy revenue declines and lower consumer broadband revenue growth than anticipated. The company continues to expect adjusted EBITDA and adjusted free cash flow to be near the lower end of prior guidance.

Century Link is not providing updated guidance ranges for full-year 2017 due to the pending acquisition of Level 3, currently anticipated to be completed by the end of third quarter of 2017, and the expected consolidation of results for the combined companies in fourth quarter 2017.

Earnings Call:

The call will be accessible for replay through August 9, 2017, by dialing 855-859-2056. Investors can also listen to Century Link’s earnings conference call and webcast replay by accessing the Investor Relations portion of the company’s website at www.centurylink.com through August 24, 2017. Here are a few highlights:

First, we continue to outperform MPLS market growth projections forecasted by leading industry analysts. In second quarter, we had nearly 2,000 MPLS customers. This performance was driven in particular by our SMB customers, where we are seeing improved install intervals of nearly 20%, which should help accelerate our revenue recognition as we move into the third and fourth quarters of this year. Next, we launched a number of new products and – we’ve launched a number of new products in the past few months including our CenturyLink Ethernet service.

We’ve also had three simplified bundles of SD-WAN plus network packages. We rolled out a competitively priced cloud-enabled small business VoIP offering. And we rolled out a new comprehensive managed Enterprise offering that is an end-to-end solution that includes WiFi management, network management, video surveillance, security and mobility management, all from a single interface. Also we have increased focus on customer retention and we are seeing lower credits and adjustments as a result.

In addition, CenturyLink continues to be one of the leaders in network virtualization through the deployment of software-defined networking and network virtualization capabilities. Based on initial results, we expect these services to create significant value in the months ahead. Also the continuous onslaught of new security threats, such as WannaCry has brought greater interest in and sales of our strong network and cyber security capabilities, as we believe CenturyLink is growing in recognition as a leading provider of security services that are so important to our Enterprise customers.

And lastly, based on third-party research support, U.S. Enterprise high-bandwidth data services are forecast to grow at mid-single-digit compounded annual growth rates through 2021, and U.S. Enterprise Managed Network Services are forecast to grow at mid to upper single-digit compounded annual growth rates through 2021. Now this forecast gives even more confidence in the opportunity to continue to grow Enterprise business in the months ahead.

Second, our IT services revenue, which is primarily driven by IT consulting, cyber security, IT service management and big data and analytics, is growing. And our managed hosting business also showed a solid turnaround this quarter. The team overcame the market confusion and sales disruption created by the colocation sale and grew cloud revenue, especially driven or aided by our Cloud Application Manager suite.

Next as expected, we had a seasonally challenging quarter from consumer broadband subscribers approximately 65,000 residential subscriber loss was higher than anticipated. This was driven to a great degree of our stronger cable competition, particularly 1 gig offerings in some of our key markets, coupled with aggressive pricing. Over the past year, we have made a pivot towards higher-quality, more profitable consumer broadband sales by removing several low-priced promotional offers and increased credit standards.

……………………………………………………………………………………………….

References:

http://ir.centurylink.com/Cache/1500102071.PDF?O=PDF&T=&Y=&D=&FID=1500102071&iid=4057179

http://ir.centurylink.com/Cache/1500102077.PDF?O=PDF&T=&Y=&D=&FID=1500102077&iid=4057179

http://services.choruscall.com/links/ctl170802.html

http://www.centurylink.com/business/enterprise/cloud/public-cloud.html

https://techblog.comsoc.org/2017/05/24/centurylinklevel-3-says-its-fiber-assets-will-attract-smbs/

J.D. Power: SMB a Growth Opportunity; Telecom ARPU Falling in Every Region

Comment & Analysis of Century Link’s 2nd Quarter results

broadband units. Consumer legacy revenue declined 8.8% Y/Y – lower access lines.

in employee-related expenses.

“We are confident our continued investment in high-quality, high-bandwidth broadband network infrastructure positions Century Link well for long-term growth,” said Glen F. Post, III, Century Link chief executive officer and president.

“Enterprise demand for high-bandwidth data services remains strong and, while consumer broadband units were weaker than expected, we are encouraged by the higher-value customers our improved offerings are attracting. We accelerated our capital investment in high-bandwidth services and broadband infrastructure during the second quarter, which we believe better positions us to increase revenues in the second half of 2017 and beyond. We anticipate second half and full year 2017 capital expenditures of approximately $1 billion and $2.6 billion, respectively.

“We achieved our expected adjusted EBITDA for the quarter as our employees did a great job managing costs, while core revenues were below our expectations primarily due to the decline in legacy revenues and the decline in broadband units being higher than anticipated. We continue to make good progress in obtaining the necessary approvals for the pending Level 3 acquisition, having received clearance in 23 of 25 required states and territories. Integration planning is progressing well and we continue to anticipate completing the acquisition by the end of September 2017. We remain excited about the value we believe this transaction will create for our customers, our shareholders and our employees,” concluded Mr. Post.

……………………………………………………………………………………….

Century Link’s presentation – 2ndQ 2017 Highlights & Trends:

1. Strategic services:

◦ Enterprise high-bandwidth data – solid growth in MPLS revenue offset by decline in Ethernet revenue; grew 5% Y/Y on a normalized basis

◦ IT & Managed services – continued growth in IT Services along with stabilization of managed hosting revenue

◦ Enterprise other strategic – ~$100 million Y/Y and Q/Q decline due to Colo-cation sale

◦ Consumer broadband – fewer subscribers Y/Y

◦ Consumer video – impact of satellite video contract restructuring

2. Acquisition of Level 3 Communications:

◦ Continued good progress in obtaining necessary approvals; received shareholder

approval and regulatory approvals/clearances in 23 states or territories, with 2 states

remaining

◦ Integration planning process continues to go well; remain confident with cash synergy target of $975 million

◦ Named combined company senior leadership team, effective at close; overall

organization design progressing well

◦ Continue to anticipate closing by end of September 2017

Forward Guidance:

Based on first half 2017 results and current expectations for the remainder of the year, Century Link anticipates coming in slightly below its full-year 2017 revenue and adjusted diluted EPS guidance, primarily driven by higher legacy revenue declines and lower consumer broadband revenue growth than anticipated. The company continues to expect adjusted EBITDA and adjusted free cash flow to be near the lower end of prior guidance.

Century Link is not providing updated guidance ranges for full-year 2017 due to the pending acquisition of Level 3, currently anticipated to be completed by the end of third quarter of 2017, and the expected consolidation of results for the combined companies in fourth quarter 2017.

Earnings Call:

The call will be accessible for replay through August 9, 2017, by dialing 855-859-2056. Investors can also listen to Century Link’s earnings conference call and webcast replay by accessing the Investor Relations portion of the company’s website at www.centurylink.com through August 24, 2017. Here are a few highlights:

First, we continue to outperform MPLS market growth projections forecasted by leading industry analysts. In second quarter, we had nearly 2,000 MPLS customers. This performance was driven in particular by our SMB customers, where we are seeing improved install intervals of nearly 20%, which should help accelerate our revenue recognition as we move into the third and fourth quarters of this year. Next, we launched a number of new products and – we’ve launched a number of new products in the past few months including our CenturyLink Ethernet service.

We’ve also had three simplified bundles of SD-WAN plus network packages. We rolled out a competitively priced cloud-enabled small business VoIP offering. And we rolled out a new comprehensive managed Enterprise offering that is an end-to-end solution that includes WiFi management, network management, video surveillance, security and mobility management, all from a single interface. Also we have increased focus on customer retention and we are seeing lower credits and adjustments as a result.

In addition, CenturyLink continues to be one of the leaders in network virtualization through the deployment of software-defined networking and network virtualization capabilities. Based on initial results, we expect these services to create significant value in the months ahead. Also the continuous onslaught of new security threats, such as WannaCry has brought greater interest in and sales of our strong network and cyber security capabilities, as we believe CenturyLink is growing in recognition as a leading provider of security services that are so important to our Enterprise customers.

And lastly, based on third-party research support, U.S. Enterprise high-bandwidth data services are forecast to grow at mid-single-digit compounded annual growth rates through 2021, and U.S. Enterprise Managed Network Services are forecast to grow at mid to upper single-digit compounded annual growth rates through 2021. Now this forecast gives even more confidence in the opportunity to continue to grow Enterprise business in the months ahead.

Second, our IT services revenue, which is primarily driven by IT consulting, cyber security, IT service management and big data and analytics, is growing. And our managed hosting business also showed a solid turnaround this quarter. The team overcame the market confusion and sales disruption created by the colocation sale and grew cloud revenue, especially driven or aided by our Cloud Application Manager suite.

Next as expected, we had a seasonally challenging quarter from consumer broadband subscribers approximately 65,000 residential subscriber loss was higher than anticipated. This was driven to a great degree of our stronger cable competition, particularly 1 gig offerings in some of our key markets, coupled with aggressive pricing. Over the past year, we have made a pivot towards higher-quality, more profitable consumer broadband sales by removing several low-priced promotional offers and increased credit standards.

……………………………………………………………………………………………….

References:

http://ir.centurylink.com/Cache/1500102071.PDF?O=PDF&T=&Y=&D=&FID=1500102071&iid=4057179

http://ir.centurylink.com/Cache/1500102077.PDF?O=PDF&T=&Y=&D=&FID=1500102077&iid=4057179

http://services.choruscall.com/links/ctl170802.html

http://www.centurylink.com/business/enterprise/cloud/public-cloud.html

https://techblog.comsoc.org/2017/05/24/centurylinklevel-3-says-its-fiber-assets-will-attract-smbs/

J.D. Power: SMB a Growth Opportunity; Telecom ARPU Falling in Every Region

Sprint Reports 1st Net Income in 3 years; CEO Says Merger Decision Coming Soon

As we’ve previously reported, Sprint is exploring various M &A options, including a merger with rival wireless carrier T-Mobile US Inc as well as a tie-up with cableco/ MSO Charter Communications Inc. Japan’s SoftBank Group Corp owns approximately 80% of the company.

“We’ve had sufficient conversations with several parties and soon we’re going to start making decisions,” Sprint CEO Marcelo Claure said on a conference call Tuesday (see Reference 1. below for the replay) after the company reported results for the three months ending June 30. The company achieved net income of $206 million, compared to a loss of $302 million one year earlier. This was the first time in three years Sprint did not have a loss for any quarter. However, the positive net income was achieved via cost cutting. Sprint reported almost $370 million of combined year-over-year reductions in cost of services and selling, general and administrative expenses.

Sprint is in the middle of a turnaround plan and has sought to strengthen its balance sheet to compete in a saturated market for wireless service. Although Sprint has cut costs, analysts have said the company is highly leveraged. While its customer base has expanded under Mr. Claure, growth has been driven by heavy discounting. It recently offered free wireless service (including unlimited data) for one year to new subscribers. Sprint’s CEO had previously hinted that the #4 U.S. wireless carrier doesn’t have the necessary funds to invest in 5G infrastructure, which gives more impetus to some type of M&A deal if Sprint is to survive.

A person familiar with the matter told Reuters that SoftBank CEO Masayoshi Son is considering making an acquisition offer for the cable company to combine it with Sprint as early as the end of August. The deal would entail SoftBank buying the Sprint shares it does not already own, the Reuters source said.

“The talks with T-Mobile have been encouraging, the talks with other partners have been encouraging,” Mr. Claure said. “Everybody has shown a high level of interest in evaluating Sprint as a potential merger partner,” he added.

The Wall Street Journal reported (on line subscription required) that the offer being considered by Sprint’s chairman and SoftBank founder, Masayoshi Son, would be to form a new publicly traded entity that would use SoftBank money to buyout shareholders of both Sprint and Charter at a premium. The transaction would be funded with roughly half cash and half stock. The deal would result in SoftBank controlling the combined company.

SoftBank has already lined up financing from at least three banks to fund the deal, according to people familiar with the matter. One of them cautioned that it could still take several weeks or more to reach an agreement with either company.

Mr. Claure said a deal with T-Mobile might be the preferred option, but it would be tougher to get past antitrust regulators in Washington. Sprint and T-Mobile held merger talks in 2014 but backed down in the face of regulator opposition.

“If you were to merge with another wireless carrier, the synergies are enormous. I mean, this is a scale business, and today you need to operate two competing networks to offer the same service, having half the amount of customers that AT&T and Verizon have,” Mr. Claure said.

A Charter deal poses its own hurdles, particularly since the company said Sunday that it isn’t interested in buying Sprint. Mr. Claure said Tuesday that Sprint didn’t offer to sell itself, so he was “surprised to see Charter’s announcement.”

Were Sprint to go it alone, the results it reported on August 1st show it has a rough road ahead. The carrier drew praise from analysts for posting its first quarterly profit in three years—$206 million compared with a loss of $302 million a year ago—but revenue fell 4.5% to $8.2 billion and it added fewer customers than rivals. While Sprint started investing more money in network improvements, its quarterly profit came primarily from cost-cutting.

The company said it had 88,000 postpaid phone additions during the quarter, the eighth consecutive period of expansion. However, the pace of growth has slowed from a year ago when the company reported 173,000 postpaid additions. Overall, it still suffered a net loss of 39,000 postpaid subscribers (a figure that includes things like tablets and smartwatches.)

Mr. Claure said Sprint will be fine without a deal, but “doing a strategic transaction will always be significantly better than having a stand-alone entity.”

……………………………………………………………………………………………………

“The obvious risk in so openly courting one potential suitor after another is that Sprint will increasingly be viewed as damaged goods,” said analyst Craig Moffet in a research note to clients. “Like an unsold house that has sat too long on the market, an asset that has been shopped too often without success takes on an air of taint.”

……………………………………………………………………………….

References:

1. Sprint’s earning call webcast- available on demand requires registration at:

2. Sprint Reports Net Income for the First Time in Three Years with 1st Quarter of Fiscal 2017:

3. Earnings Results Presentation:

http://s21.q4cdn.com/487940486/files/doc_financials/quarterly/2017/q1/02_Q1FY17-Slides_Final.pdf

BT offers to spend up to £600M on rural broadband in the UK

BT has offered to spend up to £600M to connect the final 1M homes and businesses in rural areas of Britain to a broadband connection suitable for most needs. The telecom company said every home and business in the UK would have a broadband speed of at least 10 megabits per second (Mbits/s), fast enough to stream movies, video conference and browse the web.

Broadband endpoints will either be connected via the Openreach network through fiber-optic cables, a network of copper lines via xDSL, or through the fixed broadband wireless system, where connections use radio and, in some cases, satellite signals.

BT’s plan is for 99% of the UK population to be able to obtain a broadband service of at least 10 Mbit/s by 2020. That speed meets the needs of a typical household, according to UK regulatory authority Ofcom, but is less than the 2015 FCC broadband speed minimum of 25M bit/s (downstream).

About 93% of the UK population can already access a service of at least 24 Mbit/s, according to the UK government, but there has been concern about a growing “digital divide” as rural communities miss out on the broadband revolution.

The government said it was weighing BT’s proposal against a regulatory approach. “We warmly welcome BT’s offer and now will look at whether this or a regulatory approach works better for homes and businesses,” said Culture Secretary Karen Bradley in a weekend statement. “Whichever of the two approaches we go with in the end, the driving force behind our decision making will be making sure we get the best deal for consumers.”

Actual network construction is not due to finish until late 2021 or 2022, because of work on the rollout of fixed network technologies.

The UK government said rollout would take longer under a regulatory approach but highlighted the pricing implications of BT’s plan for rivals and broadband consumers.

“It is also proposed that BT would fund this investment and recover its costs through the charges for products providing access to its local access networks,” it said. “The approach to recovering these costs will be considered in Ofcom’s current wholesale local access review.”

Gavin Patterson, CEO of BT, said:“ We are pleased to make a voluntary offer to deliver the Government’s goal for universal broadband access at minimum speeds of 10Mbps. This would involve an estimated investment of £450m — £600m depending on the final technology solution.”

At the top end of this range, the investment would equal about 2.5% of BT’s revenues in its last fiscal year (to end-March 2017) and about 17% of overall capital expenditure across the Group.

BT said it would look to recover the cost of its investment by leasing the rural networks to its rivals. The offer will also be reflected in Ofcom’s current review of how to regulate the market for super fast, fiber-based networks of the future.

Capex soared by about £3.5 billion ($4.6 billion) at BT last year, largely because of spending on broadband roll outs. BT is planning several major investments in the coming years: it plans to extend all-fiber networks to around 2 million UK premises by 2020, and connect another 10 million homes and businesses to a xDSL technology called G.fast, which boosts connectivity speeds over last-mile copper loops. (See BT to Cover 2M Homes With FTTP in $8.7B Plan.)

Earlier this month, BT CEO Patterson said he was considering the viability of a much more ambitious fiber roll out that would benefit around 10 million premises by 2025. (See BT Rejigs Consumer Biz as Profits Hit by £225M Italy Payout.)

He has also indicated that BT will participate in an upcoming auction of airwaves that could be used to support new 5G services. Operators made crippling payments for spectrum licenses during previous auctions, although experts do not expect a 5G auction to generate a similar windfall.

References:

https://www.ft.com/content/a4ba67a4-73b0-11e7-aca6-c6bd07df1a3c

http://www.itproportal.com/news/bt-unveils-600m-scheme-to-bring-broadband-to-every-rural-uk-home/

TBR Analysis of Verizon’s 2nd Quarter Results + Earnings Call Remarks

Unlimited data boosts Verizon’s phone net additions though wireless margins continue to diminish

by Steve Vachon, TBR Analyst

In 2Q17 Verizon was able to report consolidated year-to-year revenue growth (+0.1%, on a historical, non-adjusted basis) for the first quarter since 1Q16, but this was mainly due to $693 million in revenue generated from acquisitions that have closed in the past year, including Fleetmatics, Telogis and, most recently, Yahoo, which closed on June 13, 2017.

Verizon’s core businesses continue to feel the weight of pricing pressures and market saturation within the mobility, video and business services markets. These trends are exemplified by wireless revenue remaining in decline (-1.9% year-to-year) despite the recent launch of unlimited data, competition from over the top (OTT) preventing Fios video subscriber additions and growth within Verizon’s new Business Markets unit being largely contingent on the XO Communications acquisition.

The launch of Verizon’s unlimited data plans in February boosted postpaid phone net additions, totaling 358,000 in 2Q17 compared to 86,000 in 2Q16, as more customers are shifting to unlimited data for its convenience and to support increasing mobile video usage. TBR believes the price point of Verizon’s unlimited plans is also benefiting subscriber growth while minimizing average revenue per user (ARPU) declines as they strike a happy medium, starting at a lower price point than AT&T’s Unlimited Plus program, competing on-par with multiline T-Mobile One Plus plans without yielding to the overly aggressive pricing of Sprint’s Unlimited Freedom promotions.

Maintaining sufficient LTE capacity is critical as the carrier is continuing to rely on its reputation of providing superior network coverage as its primary differentiator to attract unlimited data coverage. TBR believes Verizon is well-positioned to sustain its unlimited data strategy long term as currently only 50% of its spectrum is being used for LTE and the company can continue to add network capacity via small cells, deploying AWS-3 licenses and refarming 3G licenses for LTE. However, Verizon’s network distinctions are becoming less pronounced as competitors continue to densify their networks and move towards 1Gbps data speeds by implementing LTE-Advanced technologies, which will require Verizon to implement new differentiators to stand out in the unlimited data market.

Despite the success of Verizon’s unlimited data plans, wireless EBITDA margins fell for the third-consecutive quarter in 2Q17, declining 170 basis points year-to-year to 45.8%. Verizon’s diminishing wireless (profit) margins are in part due to the carrier’s shift to a non-subsidy device pricing model as decreased equipment subsidies are failing to offset service revenue declines stemming from lower-priced wireless plans offered under this model. Postpaid ARPU is also being limited by Verizon Plan features including Carryover Data and Safety Mode that are helping tiered data customers conserve data usage. Conversely, TBR anticipates the adoption of unlimited data plans will mainly have a stabilizing effect on postpaid phone ARPU over the next year as migrations from customers on less expensive plans will be offset by the cost savings heavy overage customers will realize by transitioning to unlimited data.

Highlights of Verizon’s Earnings Call Transcript:

Matthew D. Ellis – Verizon Communications, Inc.

We had a strong quarter of execution. First, we invested in our 4G network leadership position, resulting in a sweep of third-party network performance surveys for the first half of 2017, while prepositioning for 5G services. Second, we delivered solid wireless operational performance and financial results in a competitive environment with an increase in both postpaid and prepaid accounts. Third, we successfully completed the acquisition of Yahoo’s operating assets to scale our media business.

Network leadership is the central element of our strategy, and we are continually investing in our network to extend our leadership in 4G capacity growth with densification using small cells, which includes expanding our fiber capabilities. As we prepare for the network of the future, we announced the acquisition of Straight Path for $3.1 billion, which we expect will close by the end of first quarter 2018. Straight Path complements our spectrum portfolio and positions us to lead and further drive 5G technology and its ecosystem. We have begun the pre-commercial fixed wireless trials in eight out of the 11 markets and have our first batch of customers on this technology. As we have previously highlighted, we will have trial results later in the year, and I look forward to sharing them with you.

We had a strong quarter, adding and retaining wireless customers as the momentum from the launch of our unlimited plans was sustained throughout the quarter. We delivered a strong wireless operational performance that reflects customer demand for our high-quality network in a highly competitive market. Finally, we completed the acquisition of Yahoo’s operating assets and immediately began executing on integration plans that we’ve been working on for over a year. We are confident in the execution of our strategy, which we expect to drive profitable growth, generate strong cash flows, and return long-term value to our shareholders.

Total wireline revenue on a reported basis grew 1.2%, including the recently acquired XO operations. On an organic basis, wireline segment revenue decreased 2.8% compared to a decline of 3.2% last quarter. This shift in the wireline revenue trend towards fiber is growing. Organically, fiber based products grew more than 3%, which supports our plans to further invest in fiber. Our emphasis on delivering value to all business customers, from the very small to the large enterprise, was recognized recently in a leading third-party study. More importantly, we won the large enterprise business award for the second consecutive year in the same study.

Consumer markets revenue increased 0.6%, driven by Fios Internet activity. Consumer Fios revenue growth of 4.1% was consistent with the past several quarters. During the quarter, we launched Fios Gigabit Connection in certain markets, which offers symmetrical speeds of up to 1 gigabit per second. In Fios Internet, we added 49,000 customers. Fios Video results were pressured due to softer secular demand for traditional linear video, given growth in the over-the-top offerings, as well as competitive promotional activity. Fios Video losses were 15,000 in the quarter. For the second quarter, Enterprise Solutions revenue fell 4.1% on an organic basis, which was due to persistent trends in our legacy products and pricing compression in the marketplace. On a constant-currency basis, revenue was down 3.5%.

Partner Solutions revenue declined 6.8% on an organic basis, while the revenue mix towards fiber has been trending higher. Within business markets, fiber revenue is expanding, driven by Fios broadband demand, offset by continued pressure in legacy products. On an organic basis, revenue declined 4.9% and improved slightly sequentially.

On a comparable basis, the second quarter wireline EBITDA margin was 20.8%, compared to 13.3%, which included the work stoppage, last year. Sequentially, wireline EBITDA margin was down 120 basis points, primarily due to lower revenue from Enterprise Solutions and Partner Solutions and an increase in operating expense as a result of leasing data center space related to the sale to Equinix.

…………………………………………………….

Commentary from Fierce Wireless:

Whether Verizon can maintain its network edge in an era of unlimited data is unclear, however. Recent data from Ookla indicates that the networks of both Verizon and AT&T have suffered as traffic has ramped up in recent months, as T-Mobile recently pointed out. So Verizon must continue to move quickly to meet the ever-increasing demands of consumers as mobile data traffic soars.

“Subscriber trends recovered sharply this quarter; however, this is partly due to an aggressive push behind unlimited that we don’t think is sustainable for Verizon,” New Street Research analysts said in a note to investors. “They have the least capacity per sub of all the carriers, and their network performance is already deteriorating both in absolute terms and relative to peers. Verizon is also paying for improved subscriber trends with ARPU and service revenue pressure. The recovery in subs is also partly due to record low churn across the industry in general, which we suspect will reverse later in the year with the new iPhone launch.”

TBR: AT&T Improves Profitability Despite Declining Revenues & Price Pressures

Below is TBR’s commentary on AT&T’s 2Q17 earnings. Contact Steve Vachon at +1 (603) 929-1166 or [email protected] for additional commentary.

For content reuse and media usage guidelines, please see TBR terms of use.

AT&T is improving its value proposition as competition within the mobile and video markets intensify

AT&T’s consolidated revenue fell 1.7% year-to-year to $39.8 billion in 2Q17 due to declines across all of the company’s core businesses, with the exception of its International division. AT&T’s profitability improved in the quarter, however, as operating margins rose 220 basis points year-to-year to 18.4%, aided by the company’s emphasis on non-subsidized wireless device plans.

Pricing pressures, smartphone saturation and stronger competition from OTT providers are creating obstacles for AT&T to grow its mobility and video businesses, which is spurring the carrier to become more reliant on bundles combining both services to improve its value proposition. Though TBR believes AT&T trailed all of its Tier 1 competitors in postpaid phone net additions in 2Q17, the launch of its unlimited data plans helped to mitigate declines as the carrier’s postpaid phone losses improved in the quarter to -89,000, compared to -180,000 in 2Q16.

In June AT&T Unlimited Choice customers gained the option to add DirecTV Now to their accounts for $10 per month, a benefit previously offered only to Unlimited Plus customers. TBR believes the move will boost wireless and DirecTV subscriber additions, but will come at the expense of limiting postpaid phone ARPU as customers now have less incentive to select AT&T Unlimited Plus plans, which have a starting price point that is $30 more expensive than Unlimited Choice plans.

AT&T is relying on the low price point and flexibility of DirecTV Now, which gained 152,000 customers in 2Q17, to help offset declines within its U-verse TV and DirecTV satellite businesses, which lost a combined 351,000 subscribers in the quarter. Though AT&T increased Video Entertainment revenue by 2.1% year-to-year in 2Q17, TBR believes sustaining revenue growth in the segment will be increasingly challenging as total video subscribers decrease and the company trades linear TV subscribers for lower ARPU DirecTV Now connections.

New features such as the inclusion of additional live local channels and upcoming 4K HDR and cloud DVR support provide added incentives to attract DirecTV Now customers, but addressing the platform’s streaming capacity is critical as recent service interruptions will drive some subscribers to switch to rivals such as SlingTV and Hulu Live.

AT&T deepens emphasis on the public sector and software-mediated network services to improve Business Solutions revenue

To improve Business Solutions revenue, which decreased 2.7% year-to-year in 2Q17 due primarily to lower legacy voice and data revenue, AT&T is targeting growth from government customers. In April AT&T announced it is consolidating its government and education operations, which generated about $15 billion in sales in 2016, into the new Global Public Sector division to improve cohesiveness and foster partnerships across agencies in different sectors. Additionally, AT&T will be able to provide first responders with more reliable connectivity through its collaboration with First Net, which has already attracted contracts from five states as of July.

AT&T will improve the profitability of Business Solutions long-term by adopting NFV and SDN technologies. Integrating open-source technologies and white box hardware will provide cost savings by enabling the carrier to become less dependent on more costly, proprietary infrastructure. Additionally, TBR expects the acquisition of Brocade’s Vyatta network operating system will enable AT&T to meet its goal of virtualizing 75% of its network by 2020.

In addition to cost savings, AT&T is creating revenue streams by introducing new software-mediated network services to its portfolio, including an upcoming SD-WAN service in collaboration with VeloCloud. However, AT&T will be disadvantaged by its relatively late entry into the SD-WAN market as competitors including Verizon and CenturyLink have already begun to cement leading positions within the segment.

…………………………………………………………………………………………………………

References:

http://edge.media-server.com/m/p/gz5k2iq4/lan/en (Recording of earnings call)

J.D. Power: SMB a Growth Opportunity; Telecom ARPU Falling in Every Region

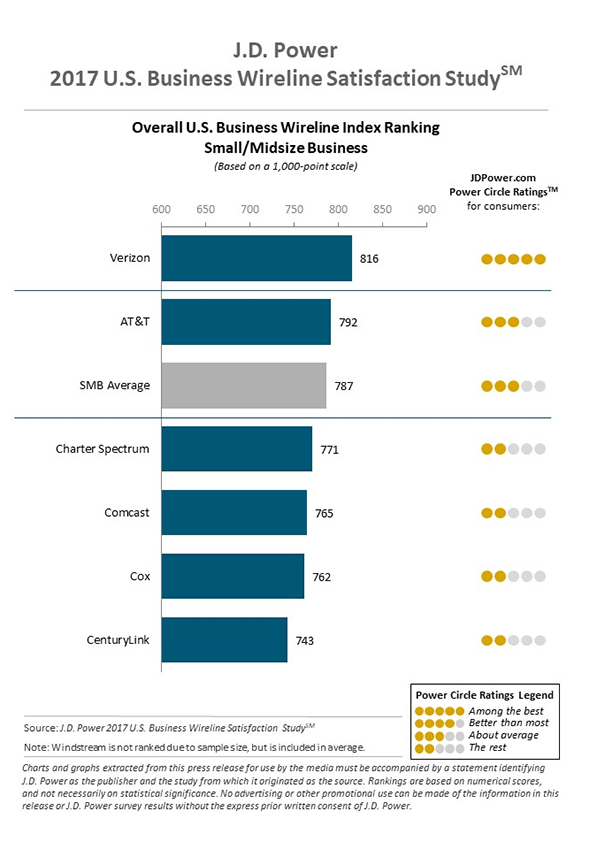

J.D. Power Report Highlights:

Enterprises with 500 or more employees are more likely to be satisfied with their telecom service, according to a report from J.D. Power, which sees the small- to medium-size business market as a growth opportunity for telcos. Medium-size businesses had an average satisfaction score of 787, J.D. Power said in a press release.

The J.D. Power report, which grades larger telecoms and cable companies, gives Verizon and AT&T the highest marks.

Verizon exceeded the average satisfaction level and topped the rankings for all three categories of businesses – small, mid-size and large. The company’s overall scores were 762, 816 and 821, respectively, for small, mid-size and large companies.

AT&T came in second place and exceeded the average score in the mid-size and large categories, with scores of 792 and 820, respectively. But Cox came in second among the smallest businesses, with a score of 744. AT&T followed at 730.

Cox was the only cableco to have a score above the average in any of the three categories. Among the telcos, CenturyLink also failed to have a score above the average in any category – a situation that company will want to address whenever its merger with Level 3 closes and the company becomes the most enterprise-focused of all the major service providers.

J.D. Power attributes the higher satisfaction level of the larger businesses to several factors, including higher satisfaction levels with communication, cost of service and customer service. Those companies with an account representative assigned to their business have notably higher overall satisfaction, researchers noted – and larger companies are more likely to have account representatives assigned to them.

Service providers in general have been emphasizing the business market in recent years and that emphasis seems to be yielding positive results. Scores for all the categories of companies were higher than for a similar study that J.D. Power conducted in 2015. Scores for 2015 were 783 for large companies, 747 for mid-size companies and 715 for small companies.

The business market has been a particularly strong focus for cable companies, which do not have wireless businesses but do have modern fiber network infrastructure. The J.D. Power results suggest cable companies still have a way to go in gaining business customers’ loyalty and trust, however.

The J.D. Power results suggest opportunities for service providers that can excel at serving SMBs – and tier two service providers such as Windstream and Frontier have been focusing on that market for a long time. So was TW Telecom (which was acquired by Level 3, which is in turn being acquired by Century Link) and XO Communications which was acquired by Verizon.

Tier two telcos were not included in the J.D. Power report.

…………………………………………………………………………………………

Telecom ARPU Falling in Every Region

Closing Comment:

Perhaps, the negative growth in telecom is causing telcos to merge to acquire scale and to go into other businesses (like Orange investing in on-line banking instead of its core telecom business).

Fierce Telecom reported on July 24th:

CenturyLink, Frontier, Windstream suffer worst 3 quarters in history

CenturyLink, Frontier and Windstream have continued to see pressure over the past three quarters as shares at each of these companies dropped dramatically due to issues at each company.

“Shares in the wireline ILEC/RLEC space (CenturyLink, Frontier, Windstream) have endured the worst three consecutive quarters in industry history, with shares plummeting an average of -20% in 4Q16, -21% in 1Q17, and -24% in 2Q17 (we note another -5% in 3Q17 thus far), mostly from Frontier and Windstream as CenturyLink shares are being supported by the Level 3 acquisition,” Cowen said in a research note.

Overall, the three companies face the industry-wide challenge of balancing strategic service growth with ongoing legacy service declines and losing market share to cable operators.

Additionally, each of these companies has been dealing with specific headwinds in their businesses. Frontier has been challenged by integrating the properties it purchased from Verizon in California, Texas and Florida, while CenturyLink is dealing with a raft of lawsuits over alleged consumer fraud issues and Windstream is seeing declines in its legacy TDM-based wholesale business sector.

References:

http://www.jdpower.com/sites/default/files/2017108.pdf

AT&T: Latency sensitive, next-gen apps need Edge Computing & We’re All In!

AT&T strongly advocates the use of edge computing (EC) as a way to reinvent the telco network and cloud so as to make new services like augmented reality, virtual reality, and low latency “5G” applications practicable.

The company’s CTO wrote in a blog post that it is adding intelligence to its cell towers, central offices, and small cells that are at the “edge” of the cloud by outfitting them with high-end graphics processing chips and other general purpose computers. By doing so, it will reduce the distance that data has to travel to get processed, thereby reducing latency and boosting overall network performance.

“Edge computing fulfills the promise of the cloud to transcend the physical constraints of our mobile devices,” said Andre Fuetsch, president of AT&T Labs and CTO in a statement. “The capabilities of tomorrow’s “5G” are the missing link that will make edge computing possible.” That’s because many “5G” applications require low latency, especially for real time control of machinery and Internet connected devices (IoT).

AT&T said it will begin deploying edge computing out over the next few years starting with urban areas and expanding those over time. The company also said that MEC is an important element to the company’s network virtualization program. The company’s goal is to have 55 percent of its network virtualized by year-end with a longer term goal of having 75 percent of its network virtualized by 2020.

The above referenced AT&T blog post identified the challenge and solution for next-gen applications:

Here’s the challenge: Next-gen applications like autonomous cars and augmented reality/virtual reality (AR/VR) will demand massive amounts of near-real time computation.

For example, according to some third-party estimates, self-driving cars will generate as much as 3.6 terabytes of data per hour from the clusters of cameras and other sensors. Some functions like braking, turning and acceleration will likely always be managed by the computer systems in the cars themselves.

But what if we could offload some of the secondary systems to the cloud? These include things like updating and accessing detailed maps these cars will use to navigate.

Or consider AR/VR. The industry is moving to a model where those applications will come through your smartphone. But creating entirely virtual worlds or overlaying digital images and graphics on top of the real world in a convincing way also requires a lot of processing power. Even when phones can deliver that horsepower, the tradeoff is extremely short battery life.

Edge computing addresses those obstacles by moving the computation into the cloud in a way that feels seamless. It’s like having a wireless supercomputer follow you wherever you go.

………………………………………………………………………………………………………………………

AT&T said that it’s already deploying EC-capable services to enterprise customers today through AT&T FlexWareSM service. Customers can currently manage powerful network services through a standard tablet device. We expect to see more applications for EC in areas like public safety that will be enabled by the FirstNet wireless broadband network.

The company claims to be committed to deploying mobile 5G as soon as possible and are committed to edge computing. As AT&T rolls out EC over the next few years, dense urban areas will be their first targets, and they’ll expand from those over time.

In conclusion, AT&T stated “we’re all in- now (for edge computing)” as per these strong closing remarks:

AT&T Labs and AT&T Foundry innovation centers are at the heart of designing and testing edge computing. In February, the AT&T Foundry in Palo Alto, CA, released a white paper on the computing and networking challenges around AR/VR. We’ll put out a second white paper in the coming weeks. It will discuss how we can apply edge computing to enable mobile augmented and virtual reality technology in the ecosystem.

There’s no time to lose. We think edge computing will drive a wave of innovation unlike anything seen since the dawn of the internet itself. Stay tuned.

…………………………………………………………………………………………………………………………..

Other network operators have been touting multi-access edge computing (MEC) in conjunction with “5G” networks. Late last year, 5G Americas, a trade group representing several operators in North and South America (including AT&T), released a white paper about the growing interest in MEC and said that standards bodies like the 3GPP and ETSI are considering including MEC in the 5G standards development.

ETSI has formed the Multi-access Edge Computing Industry Specification Group (MEC ISG). Earlier this month, ETSI released its first package of standardized application programming interfaces (APIs) that will support MEC interoperability.

……………………………………………………………………….

References:

http://about.att.com/story/reinventing_the_cloud_through_edge_computing.html

https://www.wirelessweek.com/news/2017/07/t-turns-edge-computing-vr-other-5g-use-cases