More Key Findings from the 4Q20 Transport Customer Markets Report:

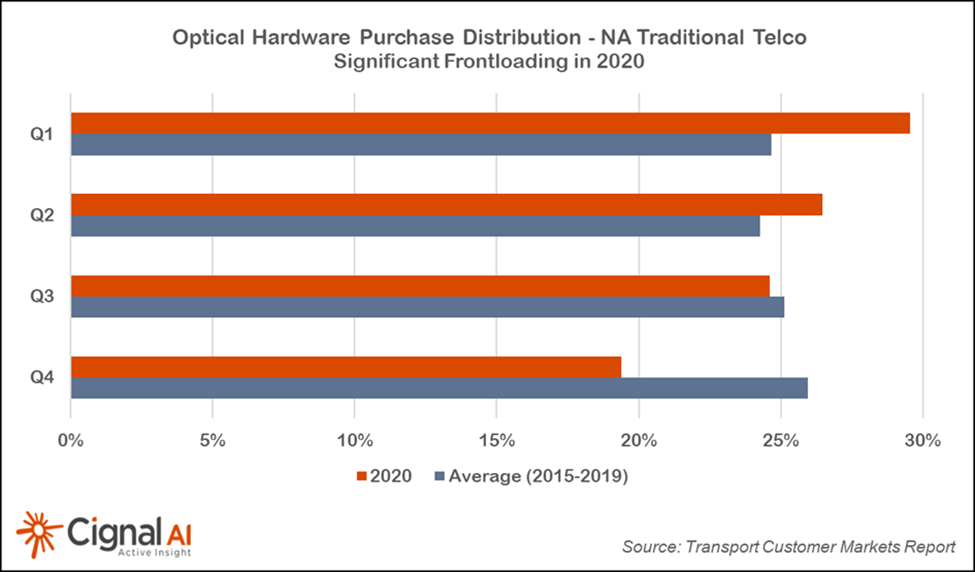

- Fourth Quarter spending on optical hardware by Cloud & Colo expanded dramatically in APAC but declined in EMEA and North America.

- Ciena lost some sales of optical transport equipment to Cloud operators but maintained market leadership in 2020. Huawei (due to growth in APAC), Nokia, and Infinera all gained share.

- Huawei maintained market share leadership for the year in both optical and packet transport equipment sales to Traditional Telcos. The company has not yet seen market share declines from growing political pressure in EMEA.

- Enterprise & Government spending on optical hardware was resilient for the year; defying expectations that it would decline due to COVID pressures.

- Transport markets should return to growth in the second half of 2021 as COVID restrictions are lifted, operational difficulties are resolved, and businesses resume normal operations. Strength will be led by Cloud & Colo operators, followed by Traditional Telco operators.

Separately, Cignal AI said on March 16th that Ciena’s revenue decline this quarter was steeper than forecast, but the company is poised to grow revenues based on the success of its WaveLogic 5e fifth generation coherent technology.

On March 2nd, Cignal AI said that Infinera originally expected its ICE6 technology to enter the market in the second half of 2020. The company’s current guidance now indicates a 2H21 arrival. Infinera reports a strong order pipeline, but has not specified exactly when the first ICE6 will ship for revenue.

About the Transport Customer Markets Report:

| The Cignal AI Transport Customer Markets Report tracks global optical and packet transport equipment spending by end-customer market type, including incumbent, wholesale, cloud and colocation, cable MSO and broadband, enterprise and government network operators. |

| The report includes historical market share and market size and five-year market size forecasts. Vendors examined: Adtran, ADVA, Alaxala, Ciena, Cisco, Ekinops, Ericsson, Fiberhome, Fujitsu, Fujitsu NC, Huawei, Infinera, Juniper Networks, Mitsubishi Electric, NEC, Nokia, Padtec, RAD, Tejas Networks, Ribbon Communications, Telco Systems, Xtera and ZTE. |

About Cignal AI:

| Cignal AI provides active and insightful market research for the networking component and equipment market and its end customers. Our work blends expertise from various disciplines to create a uniquely informed perspective on the evolution of networking communications. |

References:

https://cignal.ai/free-articles/

|

Reinhardt Krause of Investors Business Daily:

Cloud Computing: Amazon Leads In Data Center Spending:

Based on first-quarter earnings reports, 2021 is shaping up as another big year for cloud capital spending. But again, it’s still largely guesswork for analysts.

Take Amazon Web Services (AWS), the biggest provider of cloud computing services. Its March-quarter capital spending blew past estimates, jumping 78% to $12.1 billion from a year earlier.

Not all of that was cloud-related, though. Some of that went toward Amazon’s fulfillment centers, logistics and product distribution network.

Morgan Stanley analyst Katy Huberty addressed the issue in a recent note to clients:

“Estimates from (market researcher) Dell’Oro suggest that the three other major U.S. hyperscalers (Facebook (FB), Google and Microsoft) spend between 60% and 80% of total capex on (cloud computing) data centers and related infrastructure equipment, much higher than Amazon given its growing logistics and fulfillment spend,” Huberty said. “Quarterly capex trends for Amazon have become a less effective indicator of data center spend compared to the other three U.S. hyperscalers.”

Amazon: Cloud Revenue Grows 30% In 2020

But for all of 2020, Amazon’s capital spending boomed 138% to more than $40.1 billion, said a Bank of America report. Google’s overall capital spending dipped 5% to $22.3 billion while Microsoft’s total capital spending rose 30% to $17.6 billion, said BofA.

The three biggest cloud computing services continue to gain share vs. rivals such as IBM (IBM) and Oracle (ORCL), analysts say. But whether they’re making significant profit — or any profit at all — based on what they spend is unclear.

AWS cloud revenue rose 30% to $45.4 billion in 2020. Microsoft’s Azure cloud business climbed 50% to $24.7 billion. Google’s cloud revenue, including Workspace office software, rose 46% to $13.1 billion. To stay on top, the cloud titans aim to make sure they can meet growing customer demand.

Their customers rent computer processing power and data storage by the hour, week or month.

Another Set Of Cloud Titans:

Bank of America has its own group of cloud computing titans that includes China’s Alibaba Group (BABA), Baidu (BIDU) and Tencent Holdings (TCEHY) as well as Microsoft, Google, Facebook and Amazon stock.

It forecasts that 2021 cloud capital spending by those seven companies will rise 20% to $128.3 billion vs. 37% growth in 2020.

Dell’Oro, in a March 17 press release, forecast that “hyperscale,” cloud data center capital spending will rise 20% in 2021. However, Dell ‘Oro didn’t provide a dollar figure or list the companies involved in the forecast. Dell’Oro did not respond to an email requesting more information.

https://www.investors.com/news/technology/cloud-computing-are-spending-but-how-much/

The importance of ‘cloudification’

There is an estimated £3.35 trillion in value to be unlocked across enterprise use-cases over the next five years, across finance, manufacturing and retail, to name but a few. The ‘cloudification’ of networks will play a key role for telcos looking to access these new revenue streams. ‘Cloudification’, or the ‘telco cloud’, is defined as “a software-defined, highly resilient cloud infrastructure that allows telcos to add services more quickly, respond faster to changes in demand, and centrally manage their resources more efficiently.” The telco cloud means a shift from providing network functions, to providing a platform that enterprises can build and innovate on.

As the needs of a diverse range of customers rapidly evolve, so too must the telcos themselves – deploying software at a matching pace. The cloudification of the network is helping to make the scalability of applications easier, opening the door to new services and helping deliver innovation to enterprise customers at the rate they now expect.

However, it’s important to remember that real cloudification is about far more than simply transferring network functions from proprietary hardware to software running on commercial, off-the-shelf, hardware in the same locations. It is about opening the network architecture to facilitate diversity, from network-in-a-box to networks running entirely in the public cloud – and every combination in between. The advantages of an open approach are vast, and the momentum behind merging telco and IT operations is growing.

https://telecoms.com/opinion/for-5g-to-succeed-telcos-must-adopt-a-software-mindset/

July 30, 2021 UPDATE:

Global spending on cloud infrastructure services totaled USD 42-47 billion in the second quarter of 2021, according to two of the latest research reports from Canalys and Synergy. That’s a rise of 36-39% from the same period a year earlier.

The industry attracted spending of 47 billion in the period, up 36 percent from a year earlier and USD 5 billion higher than the previous quarter, thanks to workload migration and the acceleration of cloud native application development, a study by Canalys showed.

The pandemic and, more recently, extreme weather events have raised concerns over the long-term disruption from environmental risks, boosting the importance of cloud services, the researchers found.

The top three cloud service providers attracted 61 percent of total spending in the second quarter, led by Amazon Web Services (AWS) whose income rose 37 percent year on year and had a 31 percent market share, Canalys researchers estimated.

Microsoft Azure was the second largest cloud service provider, with a 22 percent market share, and its income grew 51 percent year on year while Google was third with an 8 percent market share and with a 66 percent annual rise in income over the quarter.

According to data from Synergy Research Group, meanwhile, second-quarter enterprise spending on cloud infrastructure services totaled USD 42 billion, up USD 2.7 billion quarter on quarter and 39 percent higher than the year-earlier period, marking the fourth successive quarter of year-on-year growth.

According to Synergy Research’s calculations, Amazon re-established its strong lead in the second quarter with a 33 percent share of the cloud market, thanks to sequential growth of 10 percent. Microsoft and Google accounted for another 30 percent of the market. Synergy added, and the next 20 cloud providers combined had a 28 percent market share.

Among the companies chasing the top three, those with above average growth rates include Alibaba and four other leading Chinese cloud providers, Synergy said.

https://www.telecompaper.com/news/global-cloud-infrastructure-industry-worth-usd-42-47-bln-in-q2-research–1392136