fiber optics

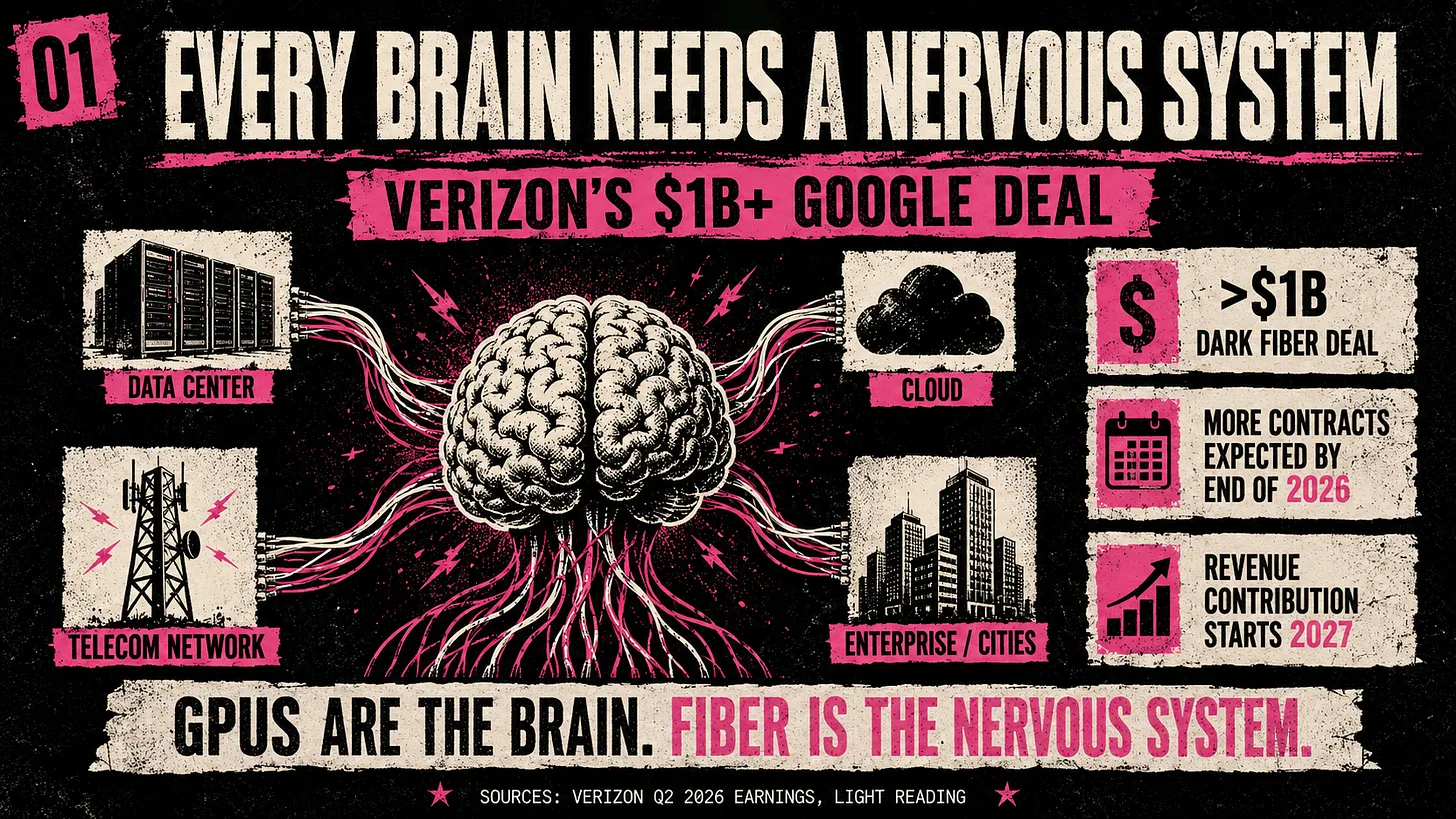

Verizon’s $1 Billion Google Dark Fiber Deal Highlights Importance of Optical Networks

Executive Summary:

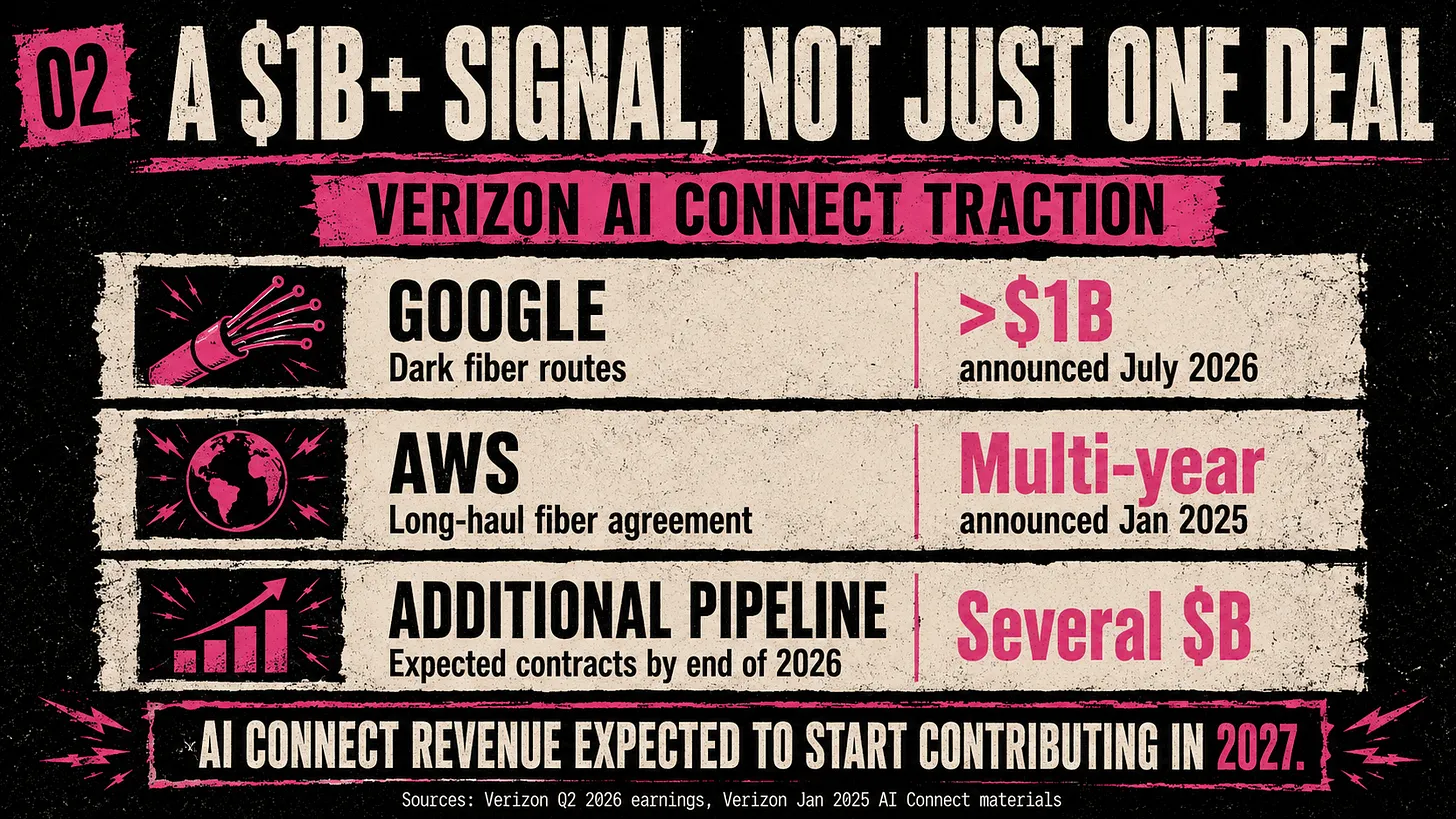

Verizon CEO Dan Schulman said on Friday the company had secured a more-than-$1 billion dark fiber agreement with Google. It underscores how hyperscale AI growth is elevating dark fiber, route diversity, and high-capacity optical engineering into core industry priorities and is evidence that the network layer is becoming a central enabler of AI-scale computing. The deal, disclosed during Verizon’s Q2 2026 earnings call, is intended to connect Google data centers and support the transport demands of AI workloads.

“We have other deals that we expect to announce by year end that taken together are expected to be worth multiple billions of dollars in revenue over the next several years,” Schulman said on Verizon’s post-earnings call.

From a telecom perspective, the significance lies in the shift from best-effort connectivity toward engineered optical infrastructure with explicit performance objectives. As hyperscalers expand distributed AI training and inference, the requirements for capacity, latency, route diversity, and operational control increasingly favor dark fiber over shared transport models.blogs.cisco+2

Why This Matters for Network Architecture:

Dark fiber gives the customer direct control over the optical layer, enabling custom design choices for line rates, protection schemes, and traffic engineering. That flexibility is especially relevant for large data-center interconnect environments, where traffic growth can quickly outpace conventional managed services.blogs.cisco+1

The Verizon-Google transaction also reinforces the role of long-haul and metro fiber as strategic infrastructure rather than commodity bandwidth. In practice, this places greater emphasis on fiber route resilience, diverse path design, and the ability to scale toward higher-capacity optical systems as AI clusters expand.blogs.cisco+1

Standards and Industry Implications:

While the deal itself is commercial, its implications touch several standards-adjacent concerns that are increasingly important to operators and vendors. These include high-capacity optical transport, inter-domain coordination, deterministic latency for distributed workloads, and the operational models needed to support AI-driven traffic growth.blogs.cisco+1

For IEEE ComSoc readers, the broader signal is that future network evolution may be shaped as much by AI infrastructure economics as by traditional access or mobility growth. The value proposition is moving toward fiber-based transport layers that can support hyperscale interconnect, cloud adjacency, and resilient backhaul for distributed computing environments.benton+1

Conclusions:

Verizon’s reported dark fiber deal with Google suggests that optical connectivity is no longer a passive enabler but a competitive differentiator in the data-center supply chain. It highlights a broader shift in network economics: AI growth is elevating fiber infrastructure from a supporting asset to a strategic enabler. For carriers, the message is clear — the winners in the AI era may be those that can pair scale, route control, and transport engineering with the capacity demands of hyperscale cloud buildouts.

Text & Images from Sebastian Barros:

Verizon’s billion dollar agreement with Google shows that the AI infrastructure boom is moving beyond chips, data centers and electricity. The next constraint is connecting everything together. Verizon will use existing fiber where possible and construct new routes where necessary. It can provide either dark fiber or managed, lit capacity, depending on what the customer wants.

Google already operates one of the most advanced private networks in the world. Its infrastructure spans more than two million miles of lit fiber, 33 subsea cable investments, more than 200 network edge locations, and thousands of content delivery sites. Yet Google still needs Verizon to provide additional routes.

The (hyperscaler) companies building the largest AI brains cannot build every nerve themselves, as the pace is too fast. The telco opportunity begins when data needs to leave the campus.

Models must be copied between regions; training datasets must be moved from storage locations to computing clusters; companies need private connections to cloud platforms; AI applications must retrieve enterprise information stored across different data centers. Inference results must reach factories, vehicles, hospitals, stores, offices, and consumers.

AI therefore requires two different networks. The first connects processors inside the brain. The second connects different brains with the outside world, and Telcos have a much stronger position in the second.

References:

https://sebastianbarros.substack.com/p/every-brain-needs-a-nervous-system

Verizon to build new, long-haul, high-capacity fiber pathways to connect AWS data centers

Hyper Scale Mega Data Centers: Time is NOW for Fiber Optics to the Compute Server

S&P Global Market Intelligence Surveys: Fiber Deployments in U.S. and Europe + AI Infrastructure Causes Market Shift

Amazon and Corning in Multi-Billion-Dollar Fiber Infrastructure Deal in North Carolina

2026 Fiber Connect Keynote: “The Future of Fiber Optics: AI and the Quantum”

Big Fiber’s $250M financing deal to buildout dark fiber routes for AI Data Center expansion

S&P Global Market Intelligence Surveys: Fiber Deployments in U.S. and Europe + AI Infrastructure Causes Market Shift

S&P’s Global Market Intelligence most recent survey showed that 87% of telecom providers in North America and Europe were deploying fiber optics last year, about the same as 2024. That’s according to the firm’s Erik Keith during a webinar hosted June 17th by the Fiber Broadband Association and its president, Gary Bolton. Among the 104 telecom operators surveyed globally, nearly nine out of ten are already using fiber as part of their broadband strategy. On the cable side, more than two-thirds of operators have either deployed fiber-to-the-home or plan to do so.

The Fiber Broadband Association says, “FTTH technology is clearly the “end game” solution for wireline broadband access services, however, the speed and scope of operator migration to full-fiber networks varies widely, depending on factors such as operator roadmaps and competitive landscape conditions.”

- Pervasive Adoption: Among the 104 telecom operators surveyed globally, 87% in North America and Europe utilize or are actively deploying fiber.

- FTTH Dominance: Fiber-to-the-home (FTTH) is widely regarded as the ultimate end-game for wireline broadband, though legacy copper and fixed wireless networks remain a part of some operators’ transition strategies.

- Cable Operator Progress: On the cable side, more than two-thirds of providers have already deployed FTTH or plan to do so as competition intensifies. More than two-thirds of surveyed cable operators have either deployed FTTH or plan to do so in the near future.

- Growing Cable Competition: Fiber overlap now extends across an estimated 75% of the U.S. cable footprint. Because of this, traditional cable operators are experiencing continued broadband subscriber losses and are actively revising their pricing and bundling strategies.

- High Consumer Satisfaction: Consumer surveys show that gigabit-tier fiber subscribers report the highest overall satisfaction rates, while fiber providers—including Verizon, Breezeline, and Frontier—claim the three lowest monthly churn rates in the U.S.

- AI as a Fiber Catalyst: Fiber is increasingly viewed as a dual-use asset capable of supporting both residential users and hyperscalers, as surging artificial intelligence (AI) demands require advanced, high-capacity infrastructure.

……………………………………………………………………………………………………………….

A different S&P Global Market Intelligence report argues that AI infrastructure demand is becoming linked to a larger market shift: constrained energy supply, higher expected earnings for producers and a growing premium for companies that control scarce capacity. For telecom and technology markets, the report adds another layer to the AI infrastructure conversation. The AI buildout is often discussed in terms of chips, models, cloud platforms and data centers. S&P Global Market Intelligence’s analysis suggests the conversation also needs to include energy supply, regional exposure, capex efficiency and the market value of scarce capacity.

……………………………………………………………………………………………………………….

References:

https://www.benton.org/headlines/fiber-breakfast-week-24-fiber-technology-trends

2026 Fiber Connect Keynote: “The Future of Fiber Optics: AI and the Quantum”

Analysis: Fiber Broadband Association (FBA) whitepaper: Upgrading MSO Networks to Fiber to the Home (FTTH): A Technical Perspective

Fiber Broadband Association Middle Mile WG: how to use “Digital Infrastructure Networks” for coordinated fiber backbone investments

Analysis: AT&T 1Q-2026 results: increased fiber penetration, FWA momentum, D2D deals, and mobile/home internet bundles

Fiber Optic Boost: Corning and Meta in multiyear $6 billion deal to accelerate U.S data center buildout

Fiber Optic Networks & Subsea Cable Systems as the foundation for AI and Cloud services

How will fiber and equipment vendors meet the increased demand for fiber optics in 2026 due to AI data center buildouts?

Automating Fiber Testing in the Last Mile: An Experiment from the Field

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

EdgeCore Digital Infrastructure and Zayo bring fiber connectivity to Santa Clara data center

Fiber Connect 2023: Telcos vs Cablecos; fiber symmetric speeds vs. DOCSIS 4.0?

Amazon and Corning in Multi-Billion-Dollar Fiber Infrastructure Deal in North Carolina

Introduction:

The surge in optical fiber demand is intensifying as hyperscale cloud providers accelerate infrastructure buildouts to support AI-driven workloads and high-density data center interconnect (DCI). Corning [1.] today announced a multi‑billion‑dollar investment from Amazon to expand fiber manufacturing capacity in North Carolina—incremental to its previously announced $10 billion regional cloud infrastructure expansion—reflects a broader structural shift in how optical supply chains are being secured and scaled.

Note 1. Corning’s fiber-optic infrastructure uses highly pure strands of optical glass thinner than a human hair to transmit massive amounts of data as pulses of light. These networks serve as the backbone for modern communications, connecting everything from rural broadband rollouts to hyperscale data centers driving generative AI. In hyperscale cloud and AI data centers, Corning provides high-density optical hardware and cables, such as their GlassWorks AI™ solutions. These large setups feature massive fiber-optic trunk cables containing hundreds to thousands of individual fibers bundled together to link powerful processors and servers. For outdoor networks running underground or on utility poles, you will see ruggedized cables protected by thick jackets and aramid yarn. These cables are designed to withstand weather, crushing, and extreme temperatures.

Corning’s structured cable solutions for internal data center connectivity. Image Credit: Corning

…………………………………………………………………………………………………………………………………………………………………………………….

This trend is not isolated. Hyperscalers including Meta, Microsoft, and wireline network operator Lumen are proactively entering long-term supply and co-investment agreements with fiber and cable manufacturers, effectively reshaping the upstream optical ecosystem.

Recent Fiber Supply Agreements with Corning:

-

May 2026: NVIDIA committed $500 million to Corning to support construction of three new optical manufacturing facilities in North Carolina and Texas. This investment is expected to increase Corning’s U.S.-based optical connectivity manufacturing capacity by approximately 10× and expand domestic fiber production by over 50%, targeting AI cluster interconnect requirements characterized by high fiber count and low-latency links aligned with IEEE 802.3 Ethernet and emerging co-packaged optics ecosystems.

-

January 2026: Meta finalized a $6 billion agreement with Corning to secure fiber supply for large-scale data center fabrics. These fabrics increasingly rely on high-fiber-density architectures consistent with leaf-spine topologies and standards such as IEEE 802.3bs/ck (400G/800G Ethernet), as well as parallel single-mode fiber (PSM) and wavelength-division multiplexing (WDM) approaches defined in ITU-T G.694.x.

-

September 2025: Microsoft entered a manufacturing agreement with Corning and Heraeus focused on hollow-core fiber (HCF), a technology aligned with ITU-T G.650 characterization frameworks. HCF offers lower latency (reduced group index) and improved performance for latency-sensitive AI workloads and inter-data center transport.

-

August 2024: Corning and Lumen established a supply agreement for next-generation fiber optic cable to support AI-driven traffic growth. This aligns with ITU-T G.652.D and G.657 fiber standards for bend-insensitive and high-capacity terrestrial deployments, as well as evolving requirements for high-count ribbon fiber cables in dense metro and campus environments.

Structural Implications for the Optical Supply Chain:

Hyperscalers are transitioning from passive consumers of optical components to active participants in manufacturing scale-up, including:

-

Anchor tenancy models: As seen with Meta’s backing of Corning’s North Carolina facility, hyperscalers are underwriting capacity expansion, effectively securing preferential access to supply.

-

Vertical influence: Direct investments and long-term offtake agreements allow hyperscalers to influence fiber specifications, manufacturing roadmaps, and deployment architectures (e.g., optimized fiber types for short-reach vs. long-haul DCI).

-

Workforce development: Amazon and Corning’s collaboration with Catawba Valley Community College to expand fiber technician training reflects a strategic effort to address labor constraints in optical manufacturing and deployment, reinforcing domestic supply chain resilience.

Implications for Telecom Operators:

These developments introduce non-trivial risks and strategic considerations for telecom operators:

-

Supply prioritization: Hyperscaler-backed agreements may shift allocation dynamics, potentially constraining availability for traditional telecom buyers during periods of tight supply.

-

Pricing pressure: Long-term, high-volume contracts could influence pricing benchmarks, potentially disadvantaging operators without comparable scale or capital flexibility.

-

BEAD timing mismatch: U.S. operators anticipating fiber expansion funded by BEAD (Broadband Equity, Access, and Deployment) may face supply bottlenecks if hyperscaler demand absorbs near-term manufacturing output.

-

Architectural divergence: Hyperscaler-driven requirements—optimized for short-reach, ultra-high-capacity intra-data-center and DCI links—may skew innovation toward their use cases, potentially misaligning with traditional access network needs governed by ITU-T G.984 (GPON), G.9807 (XGS-PON), and emerging 25G/50G PON standards.

A useful analogy is the semiconductor industry, where hyperscaler influence has already reshaped foundry capacity allocation and advanced node prioritization. A similar dynamic is now emerging in optical fiber and connectivity, with hyperscalers effectively acting as quasi-industrial planners for next-generation optical infrastructure.

Quotes:

“Amazon’s investments in North Carolina have created more than 26,000 jobs across the state. This multibillion-dollar agreement with Corning continues that commitment, channeling investment into American manufacturing and creating 1,000 new jobs at their facilities near our data centers,” said Matt Garman, CEO of AWS. “We’re also partnering to train North Carolinians for highly skilled roles in fiber optics and fusion splicing. These long-term investments create long-term careers and real opportunity in the communities where we operate.”

“This agreement with Amazon represents a significant milestone for Corning and for American manufacturing,” said Wendell Weeks, chairman, CEO, and president of Corning. “For 175 years, Corning has pioneered the technologies that connect people and transform industries. Amazon’s investment will help us expand production, create 1,000 new advanced manufacturing jobs at our facilities, and lead the way toward building a resilient U.S. manufacturing base.”

Clearfield CEO Cheri Beranek told Fierce Network at Fiber Connect that supply chain issues are re-emerging, particularly around high-count fiber. “There’s absolutely a shortage of ribbon fiber,” she said, referring to a conversation with Hawaii Telecom, a Clearfield customer. “The high count for the ribbon fiber … everything over 432 is tough to get,” she said. “The fiber companies want to tell you that there’s enough American‑made fiber… but there can’t be.”

“In talking to fiber optic suppliers, they all say one thing, ‘It’s nice to finally be the cool kid on the block.’ Hyperscalers are finally realizing that they not only need compute, storage, chips, power, water and real estate, they also need fiber optic connectivity,” said Fierce Network’s Chief Analyst Linda Hardesty.

The net effect is a tightening coupling between AI infrastructure demand and optical supply chain strategy—one that telecom operators will need to actively manage through procurement strategy, vendor diversification, and potentially deeper participation in supply-side partnerships.

End Note:

Amazon’s long-term commitment to North Carolina goes beyond direct investments and jobs created in the state. Through workforce development, Career Choice, and upskilling programs, Amazon has already provided practical training for nearly 7,000 people in North Carolina, helping to open new pathways for higher-paying jobs and fulfilling careers.

In the last decade, Amazon has contributed more than $72 million to charities and organizations supporting local needs across North Carolina, with $10 million provided in 2025 alone to 26 local community partners. This includes contributions like $1.5 million to enhance public safety services for southeastern Hamlet and surrounding Richmond County communities by funding a new fire substation that is expected to lower emergency response times and homeowner insurance premiums.

References:

https://www.corning.com/data-center/au/en/home/applications/enterprise-private-data-center.html

https://www.aboutamazon.com/news/company-news/amazon-corning-fiber-optics-1000-jobs-north-carolina

Fiber Optic Boost: Corning and Meta in multiyear $6 billion deal to accelerate U.S data center buildout

Corning to Build New Fiber Optic Plant in Phoenix, AZ for AT&T Fiber Network Expansion

Calix and Corning Weigh In: When Will Broadband Wireline Spending Increase?

Verizon-Corning $1.05B fiber deal part of larger build-out or buy program

Goldman Sachs report: Optical Networking is the next mega trend in AI infrastructure

Goldman Sachs analysts forecast a $154billion opportunity in optical networking driven by skyrocketing capacity demands from hyperscale cloud and AI workloads. Carriers and vendors are integrating 10GbE edge networking and AI-RAN (Artificial Intelligence Radio Access Network) trials on live 5G networks.

Goldman argues that AI infrastructure is creating a networking bottleneck phase, where optical interconnects become essential to connect more chips, keep latency low, and let AI clusters scale efficiently. The total optical networking market forecast 9x increase to $154 billion is due to both scale-up and scale-out AI data center architectures grow.

AI compute gains are no longer just about faster GPU and HBM chips; they depend on moving data fast enough between chips, racks, and super-nodes. Goldman Sachs emphasizes that networking now “unlocks computing capability” by enabling seamless exchange across multiple AI chips, which is exactly where copper-based links start to fall short. That makes fiber-optic connectivity, pluggable optics, and co-packaged optics central to the next phase of AI build-out. The report splits opportunity across scale-up and scale-out networking, plus component categories such as copper cables, pluggable optical modules, CPO, and PCB midplanes.

External coverage of this report says Goldman Sachs sees scale-up as the larger pool, about $106 billion or 69% of the $154 billion TAM, while CPO could represent about $91 billion or 59% of the total, assuming 29% penetration in scale-out networking. In practical terms, the report is signaling that the highest-value optical opportunity sits inside tightly coupled AI systems, not just in long-haul or metro transport.

………………………………………………………………………………………………………………………………………………………………………………………….

Goldman projects the following:

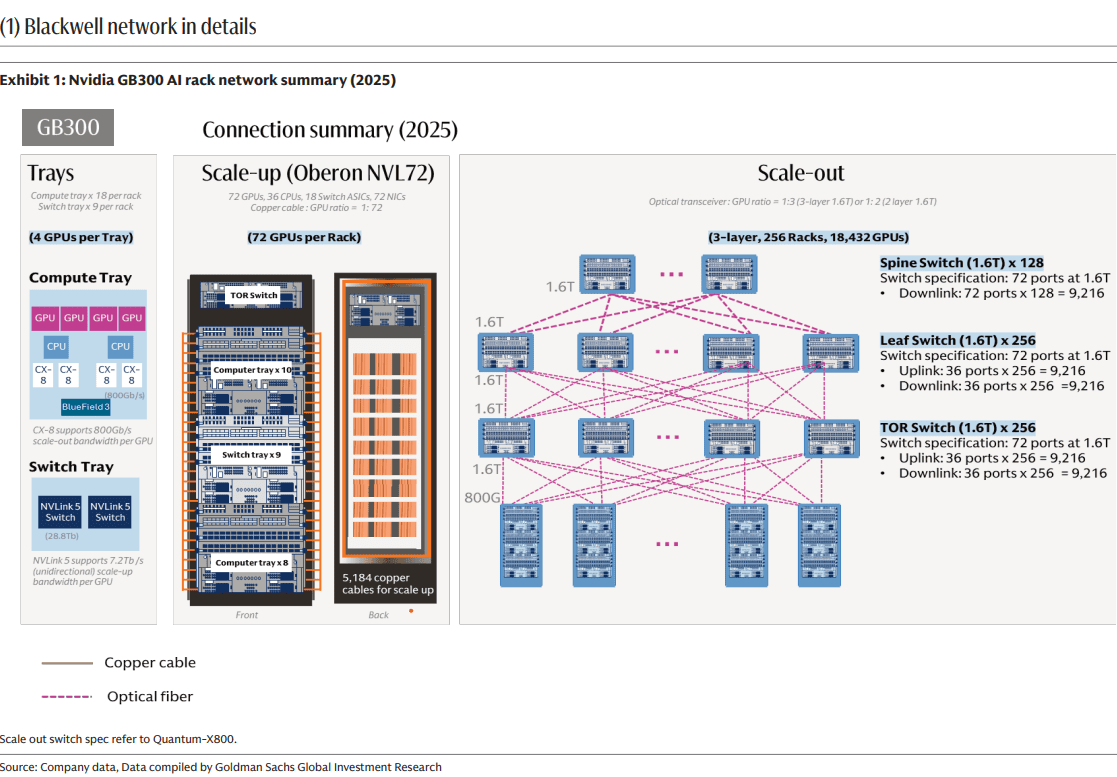

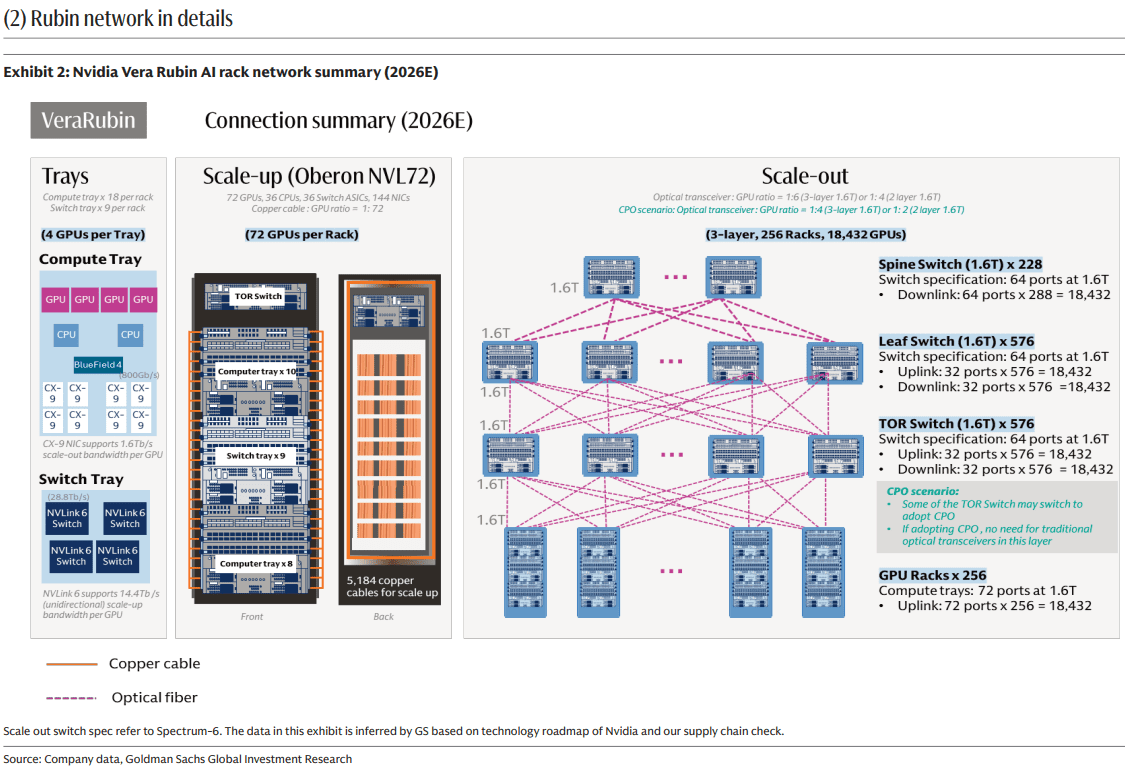

- Dollar content increase by 16x / 45x in Scale Out / Scale Up per computing unit from GB300 NVL72 (per computing unit means 72 GPUs per rack to reach NVL72) to Rubin Ultra NVL576 (per computing unit means 72 GPUs per rack, and 8 racks together to reach NVL576), with opportunities across pluggable optical modules, optical engines in CPO, copper cables, and PCB midplanes.

- A 13x larger addressable market for optical modules / optical engines expanding from scale out (e.g. GB300 NVL72) to scale up (e.g. Nvidia Rubin Ultra [1.] NVL576 level 2 scale up via CPO) per computing unit. n

- A 10x larger value market for pluggable optical modules in scale out per computing unit from GB300 NVL72 to Rubin Ultra NVL576, even with a 29% CPO penetration rate. The numbers of pluggable optical module (1.6T equivalent) per computing unit would increase from 216 units in GB300 NVL72 to 2.5k units in Rubin Ultra NVL576.

Note 1. Nvidia Rubin Ultra is a flagship, next-generation AI and high-performance computing (HPC) processor succeeding the standard Rubin architecture. Scheduled to debut in late 2027, it utilizes massive multi-die chiplet designs and unprecedented memory configurations to power the next wave of generative and agentic AI.

………………………………………………………………………………………………………………………………………………………………………….

Market Forecasts:

The investment bank expects the aggregate dollar content per computing unit across scale up and scale out to increase by 29x from US$315k in GB300 NVL72 to US$9.4bn in Rubin Ultra NVL576, and assuming the numbers of racks through the full product cycle are 48k racks for GB300 NVL72, and 16.5k computing units for Rubin Ultra NVL576, the aggregate value TAM across scale up and scale out would increase by 9x from US$15bn in GB300 NVL72 (mainly in 2026) to US$154bn in Rubin Ultra NVL576 (mainly in 2028).

Among the US$154bn value TAM, 69% goes to scale up, or US$106bn, and CPO contributes US$91bn, or 59% of the US$154bn value TAM, assuming CPO at 29% penetration rate in scale out.

For network architects, the important takeaway is that AI clusters are becoming optics-heavy at more layers of the network stack, not just at the edge of the rack. The likely winners are suppliers that can reduce power, improve density, and simplify packaging for very high-bandwidth links, especially around CPO and advanced pluggables. This is less a story about traditional telecom optics and more about datacenter interconnects optimized for GPU fabrics and AI training/inference throughput.

The most consistently cited “top beneficiaries” are Coherent, Lumentum, and Fabrinet. These companies sit close to the core optical component modules and manufacturing layers that scale with higher AI interconnect demand. That makes them the most straightforward proxies for the forecasted optics expansion. The report’s thesis favors companies with strong exposure to high-end optical transport, coherent optics, and data-center interconnect rather than the broader optical networking/PON equipment companies like Ciena, Nokia/Infinera, Cisco/Acacia, ADVA, or Calix.

Conclusions:

Strategically, Goldman Sachs maintains that optical networking is no longer a niche enabling layer; it is becoming a core enabler of AI capex scaling. That shifts investor attention toward optical component vendors, silicon photonics, transceiver suppliers, and adjacent packaging ecosystems. The report’s core message is simple: as AI clusters grow, the network fabric becomes a first-order constraint, and optics are the most likely answer.

References:

2026 Fiber Connect Keynote: “The Future of Fiber Optics: AI and the Quantum”

How will fiber and equipment vendors meet the increased demand for fiber optics in 2026 due to AI data center buildouts?

Big Fiber’s $250M financing deal to buildout dark fiber routes for AI Data Center expansion

Analysis: Fiber Broadband Association (FBA) whitepaper: Upgrading MSO Networks to Fiber to the Home (FTTH): A Technical Perspective

Fiber Optic Boost: Corning and Meta in multiyear $6 billion deal to accelerate U.S data center buildout

Fiber Optic Networks & Subsea Cable Systems as the foundation for AI and Cloud services

AI infrastructure investments drive demand for Ciena’s products including 800G coherent optics

DriveNets and Ciena Complete Joint Testing of 400G ZR/ZR+ optics for Network Cloud Platform

2026 Fiber Connect Keynote: “The Future of Fiber Optics: AI and the Quantum”

Dr. Michio Kaku’s 2026 Fiber Connect keynote, “The Future of Fiber Optics: AI and the Quantum,” kicked off the inaugural AI & Emerging Technology Infrastructure Summit on Wednesday, May 20,2026.

As a theoretical physicist and futurist, Dr. Kaku delivered a high-altitude roadmap framing fiber optic networks not merely as faster telecom pipes, but as the mandatory foundation for a world defined by concurrent, multi-cloud AI infrastructure and quantum mechanics.

Kaku described the convergence of AI, quantum computing, and fiber infrastructure as a critical shift toward an AI-native, quantum-enabled internet essential for national competitiveness. Kaku emphasized that fiber optics are necessary to facilitate “quantum AI” by handling high-density, low-latency data movement, moving beyond traditional networking to support exponential computing advancements.

Key Takeaways:

- Fiber as the Foundation for AI: Dr. Kaku explained that massive data sets and hyperscale AI computations cannot run efficiently over wireless or legacy networks. Fiber’s near-limitless bandwidth and sub-millisecond latency are required to process these workloads in real-time.

- The Quantum Computing Leap: He detailed how quantum networks—which compute at the atomic level—will redefine security and processing power. He emphasized that quantum data requires the stability, security, and bandwidth that only fiber optics can provide.

- National Competitiveness: Dr. Kaku framed fiber broadband as a strategic national asset. He argued that a region’s ability to evolve into an AI-native economy depends directly on robust fiber infrastructure to secure future healthcare, financial, and climate innovations.

- The “Thinking Economy”: He projected that networks are evolving to do more than just transport data. They will increasingly support “thinking economies” where intelligence moves instantly between edge computing centers, end-points, and the cloud.

The presentation and subsequent fireside chat with quantum computing firm IonQ offered several critical technological dimensions and actionable industry analysis:

The Physics of the “AI Triad” (Compute, Quantum, & Photonics):

Kaku mapped out how classical silicon-based computing is approaching its physical limits (thermodynamics and transistor gating). He explained that the future relies on a three-pronged convergence:

-

- AI Models: The brain processing the logic.

- Quantum Computing: The hyper-accelerator solving atomic, chemical, and multi-variable optimization issues.

- Optical Fiber: The unified nervous system. Quantum and distributed AI workloads cannot scale on traditional copper networks because they require absolute determinism, zero-jitter latency, and near-limitless bandwidth.

Upgrading to a Quantum-Ready Internet:

Drawing from themes in his book Quantum Supremacy, Kaku noted that the move toward a quantum-enabled web alters the physical network topology. Operators must plan for physical security layers (like Quantum Key Distribution) and data transmission methods that preserve quantum entanglement across distances.

–>Fiber is the only media capable of transporting light photons over vast geographies without disrupting these states.

The Power and Cooling Crisis:

A significant focus of the analysis was the staggering energy footprint of next-generation AI factories and hyper-scale data centers. Kaku noted that moving data electronically creates heat resistance. Shifting toward all-optical (photonic) networks and in-rack fiber interconnects removes electronic bottlenecks, drastically reducing the power required to pass massive datasets between distributed data centers

Strategic Implications for Network Operators:

During the fireside chat, the discussion moved from theoretical physics to immediate business strategy and tactics:

-

- National Competitiveness: Bandwidth, latency, and optical infrastructure are the new benchmarks for a country’s economic power.

- Capacity Planning: Network planners must shift from estimating consumer download speeds to calculating the throughput required for real-time, stateful AI agents and machine learning inference workloads operating at the network edge.

FBA Panel and Summit Sessions:

Following Kaku’s opening address, the Fiber Broadband Association (FBA) hosted deep-dive industry panels that put these physics concepts into operator terms:

- The Open Compute Project (OCP): Discussed open-source hardware standards for in-rack photonics to support massive AI clustering.

- Multi-Data-Center Architectures: Network engineers mapped out how dense dark fiber rings are being laid to link secondary edge facilities, allowing enterprises to run heavy inference closer to end-users without overwhelming backbone networks.

- AI data center speed and power requirements are transitioning towards 800 Gbps–1.6 Tbps node-to-node networking and gigawatt-scale power to handle distributed generative AI workloads.

- High rack densities up to 240 kW require advanced liquid or immersion cooling, with optical technologies being introduced to reduce heat generation.

…………………………………………………………………………………………………………………………………..

References:

https://fiberconnect.fiberbroadband.org/about/whats-new/

Analysis: Fiber Broadband Association (FBA) whitepaper: Upgrading MSO Networks to Fiber to the Home (FTTH): A Technical Perspective

Fiber Broadband Association Middle Mile WG: how to use “Digital Infrastructure Networks” for coordinated fiber backbone investments

Analysis: AT&T 1Q-2026 results: increased fiber penetration, FWA momentum, D2D deals, and mobile/home internet bundles

Fiber Optic Boost: Corning and Meta in multiyear $6 billion deal to accelerate U.S data center buildout

Fiber Optic Networks & Subsea Cable Systems as the foundation for AI and Cloud services

How will fiber and equipment vendors meet the increased demand for fiber optics in 2026 due to AI data center buildouts?

Automating Fiber Testing in the Last Mile: An Experiment from the Field

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

Big Fiber’s $250M financing deal to buildout dark fiber routes for AI Data Center expansion

Executive Summary:

Big Fiber [1.] has secured $250 million in financing from Stonepeak and Caisse de dépôt et placement du Québec (CDPQ) to expand its dark fiber footprint and increase network capacity in response to accelerating hyperscaler and large-scale data center investments in AI-driven workloads.

Note 1. Sunnyvale, CA headquartered Big Fiber was previously known as Bandwidth IG, which was originally established in 2019 as a telecom and dark-fiber infrastructure company. The rebrand to BIG Fiber was announced on May 1, 2025 when the company described it as a shift to better reflect its focus on privately owned, newly constructed dark fiber networks. The company has built privately owned metro dark fiber networks from its inception, primarily in the SF Bay Area and the Greater Portland, OR and Atlanta, GA areas.

BIG Fiber structures its dark fiber portfolio around high‑strand‑count, single‑mode, low‑loss fiber deployed in purpose‑built, underground metro and regional routes, rather than a carrier‑specific “technology” stack of its own. The company’s public materials emphasize:

-

Single‑mode fiber (SMF) for metro and long‑haul connectivity, consistent with standard dark‑fiber infrastructure designed for multi‑wavelength and DWDM‑based upgrades.

-

High‑density, high‑fiber‑count cables in metro corridors (often hundreds of strands) to support dense data‑center and interconnect demand, which is typical of “new‑build” dark‑fiber operators entering AI‑and‑cloud‑centric markets.

-

Point‑to‑point and ring‑style topologies engineered for extreme route diversity (tri‑/quad‑versity) and low latency, rather than a legacy long‑haul backbone that relies on older fiber types or managed wavelengths.

To complement Big Fiber’s dark‑fiber infrastructure; the customer provides the optical PHY layer (e.g., coherent DWDM, 400ZR/ZR+, or other high‑speed optics), which is how dark‑fiber providers typically position their offerings.

–>More about Big Fiber at the end of this article from the company itself.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Proceeds of the facility will be used to refinance existing debt, provide new capital and facilitate the necessary headroom for major fiber optic network expansions already underway. This includes a significant multi-market buildout in Greater Atlanta, adding over 205 route miles and 165,000 fiber miles to BIG Fiber’s existing market-leading footprint.

“Our partnership with Stonepeak Credit and La Caisse marks a pivotal moment in our mission to empower our customers with highly scalable and purpose-built dark fiber solutions,” said Bruce Garrison, CEO of BIG Fiber. “This financing ensures we have the scale to stay ahead of the escalating demand for modernized infrastructure enabling the AI ecosystem and the necessary digital highways for decades to come.”

“BIG Fiber’s infrastructure delivers critical bandwidth to meet the insatiable demand for both data and compute capacity across its key markets,” said Arun Varanasi, Managing Director at Stonepeak Credit. “We are proud to partner with Columbia Capital, SDC Capital Partners, and La Caisse to support the company’s next leg of growth as it positions itself as one of the preeminent dark fiber operators in the country.”

“BIG Fiber is well positioned to meet the growing connectivity needs of enterprises and data centers seeking new, high-quality infrastructure options,” said Jérôme Marquis, Managing Director and Head of Private Credit at La Caisse. “Its resilient business model, underpinned by long-term contracts and strong structural demand, positions the company well for growth. Together with Stonepeak Credit, we’re providing a tailored financing solution that supports the continued buildout of essential digital infrastructure.”

The latest expansion will bring BIG Fiber’s Atlanta and San Francisco Bay Area network capacity to 850 route miles and over 3 million fiber miles. Projects are currently under construction or contract, with phased Ready for Service (RFS) dates expected in early 2027.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………

According to Big Fiber Chief Commercial Officer Patton Lochridge, demand signals are particularly strong in key U.S. metros including the San Francisco Bay Area, Hillsboro, and Atlanta, where new fiber routes are being deployed to support AI-centric data center expansion. “We’re seeing customers require extreme route diversity, often moving toward triversity or quadversity networks to connect metro assets and long-haul routes,” Lochridge said. He added that inference workloads are increasing the demand for dense metro connectivity: “Traditional telecommunications networks are often too congested or lack the latency and loss tolerances required for stringent AI workloads, making purpose-built metro fiber essential.” Lochridge indicated that the majority of the new capital will be directed toward greenfield build-outs and targeted overbuilds of “exhausted legacy telecommunications corridors that need more scale.”

Industry analysts highlight a parallel geographic shift in AI infrastructure deployment. Sterling Perrin, senior principal analyst for optical networks and transport at Omdia, noted that AI campuses are expanding beyond traditional connectivity hubs such as Ashburn, Dallas, and Northern California into power-advantaged regions including West Texas, Ohio, Tennessee, Louisiana, and Georgia. “They all require massive fiber optic connectivity,” Perrin said.

Power availability is emerging as a primary constraint shaping network topology. Ron Westfall, vice president and analyst at HyperFrame Research, emphasized that grid limitations are driving hyperscalers toward distributed AI campus architectures interconnected via metro and long-haul dark fiber. “Power grid constraints have forced a material shift toward metro and long-haul dark fiber infrastructure to stitch together distributed regional data center campuses,” Westfall said. “Because this relentless GPU-to-GPU communication demands near-zero latency and unprecedented bandwidth, infrastructure planners are prioritizing the deployment of ultra-high-strand dark fiber corridors that directly link distributed, power-rich data centers.”

AI Workloads Reshape Optical Demand:

AI-driven traffic growth is now materially impacting the optical supply chain. In its April 2026 post-OFC analysis, CRU Group reported that AI-related data center demand “has overtaken traditional telecom as the primary growth engine for optical [fiber] and cable,” contributing to tightening supply conditions for high-fiber-count cables and upstream preform materials.

Despite this surge, the majority of AI traffic remains intra-data-center. Omdia estimates indicate that up to 90% of AI traffic does not exit the facility during GPU cluster operations. However, the emergence of distributed AI architectures is beginning to increase requirements for high-capacity inter-data-center interconnect (DCI).

At the Optica Executive Forum, Cisco SVP and Fellow Rakesh Chopra highlighted the scale differential between AI and conventional traffic profiles. As cited by Perrin, AI “scale-up” traffic within data centers can generate 504 times more traffic than traditional DCI flows, while “scale-out” traffic can produce 56 times DCI bandwidth requirements. “With AI training models at the limits of what can be processed within a data center, distributed AI clusters are inevitable,” Perrin said.

This architectural transition is reflected in NVIDIA’s AI factory designs, which decouple east-west GPU compute traffic from traditional north-south enterprise flows, leveraging low-latency leaf-spine topologies optimized for continuous GPU synchronization.

Westfall further noted that these evolving traffic patterns are fundamentally altering network design assumptions. Operators are increasingly optimizing for persistent machine-to-machine synchronization rather than burst-oriented enterprise traffic models.

Fiber as a Core AI Infrastructure Asset:

The Big Fiber’s latest financing aligns with broader trends in AI infrastructure investment, where capital is being deployed across integrated stacks including energy, land, connectivity, and compute infrastructure. Utilities are expanding transmission capacity, while developers are co-locating generation resources near emerging AI hubs.

Within this context, fiber infrastructure is being revalued based on its strategic proximity to power-rich data center clusters. “Infrastructure monetization is shifting away from historical metrics such as per-megabit pricing toward asset-level valuations built around proximity to power-rich data centers,” Westfall said.

If current deployment trajectories persist, the resulting topology will consist of a dense, high-capacity mesh of metro and long-haul fiber routes interconnecting geographically distributed, power-optimized AI campuses with hyperscale cloud and interconnection ecosystems.

………………………………………………………………………………………………………………………………

About BIG Fiber:

BIG Fiber is a metro dark fiber provider that offers high capacity, strategically placed, dark fiber networks to mission critical data centers, Hyperscalers and enterprises throughout the San Francisco Bay Area, Greater Portland and Greater Atlanta areas. BIG Fiber’s 100% underground network meets critical data needs for enterprises and data centers that require new, quality infrastructure options. BIG Fiber’s San Francisco Bay Area network offers more than 320 route miles and 65 data centers. The Greater Portland network has more than 20 route miles and 15 data centers, and the Greater Atlanta network has more than 550 route miles and 30 data centers. BIG Fiber was founded in 2019 and is headquartered in Sunnyvale, California. Visit www.bigfiber.com to learn more.

………………………………………………………………………………………………………………………………

References:

BIG Fiber Secures $250 Million Financing Led by Stonepeak Credit and La Caisse

Analysis: Fiber Broadband Association (FBA) whitepaper: Upgrading MSO Networks to Fiber to the Home (FTTH): A Technical Perspective

Fiber Broadband Association Middle Mile WG: how to use “Digital Infrastructure Networks” for coordinated fiber backbone investments

Analysis: AT&T 1Q-2026 results: increased fiber penetration, FWA momentum, D2D deals, and mobile/home internet bundles

Fiber Optic Boost: Corning and Meta in multiyear $6 billion deal to accelerate U.S data center buildout

Fiber Optic Networks & Subsea Cable Systems as the foundation for AI and Cloud services

How will fiber and equipment vendors meet the increased demand for fiber optics in 2026 due to AI data center buildouts?

Automating Fiber Testing in the Last Mile: An Experiment from the Field

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

Analysis: Fiber Broadband Association (FBA) whitepaper: Upgrading MSO Networks to Fiber to the Home (FTTH): A Technical Perspective

Executive Summary:

The Fiber Broadband Association (FBA) has published an economic and structural framework for Hybrid Fiber Coax (HFC)-to-Fiber to the Premises (FTTP) [1.] upgrades, viewing that as a ‘strategic imperative’ for cable network operators (MSOs). FBA’s The whitepaper white paper, “Upgrading MSO Networks to Fiber to the Home (FTTH): A Technical Perspective,“ positions fiber as the long-term architectural solution for cable access networks.

The whitepaper evaluates multiple migration paths—including full overbuilds, targeted deployments, and HFC/FTTP coexistence—alongside passive optical network (PON) options and operating models. Economically, the report estimates FTTP operating expenses to be approximately 50% lower than HFC, driven by the elimination of active outside plant components. It outlines deployment options ranging from incremental overlays to full HFC replacement, each with distinct cost-performance trade-offs.

Note 1. Fiber optic access networks (sometimes referred to as fiber-to-the-home—FTTH—or fiber-to-the-premises—FTTP) are built to connect homes and businesses to lightning fast Internet connections. The fiber optic cables that make up these networks are the fastest and most reliable broadband technology and are capable of delivering vastly higher bandwidth than traditional copper wires or wireless. All-fiber networks are directly connected from the central office all the way to a subscriber’s building. There is no other technology along the path except fiber optics.

Fiber optic cables are made up of thin strands of glass that carry information by transmitting pulses of light, which are usually created by lasers. The vibrations are turned on and off very quickly. A single fiber can carry multiple streams of information simultaneously over different wavelengths, or colors, of light, enabling more robust video, Internet, and voice services. Fiber cables are capable of transmitting multi-gigabit Internet speeds compared to the mere megabytes typical of copper connections.

Image Credit: Panther Media GmbH/Alamy Stock Photo

…………………………………………………………………………………………………………………………..

Divergent Cable Operator (MSO) Strategies:

In practice, MSO upgrade strategies remain highly variable, shaped by market competition, plant condition, density, and capital constraints. Most large operators now manage hybrid access portfolios spanning HFC, FTTP, and, in some cases, fixed wireless access (FWA).

Optimum Communications, for example, is deploying FTTP overlays in dense Northeastern markets while relying on DOCSIS 3.1 in rural areas where fiber economics are less favorable.

Comcast and Charter similarly pursue selective FTTP in greenfield and edge-out scenarios but continue to prioritize HFC evolution via DOCSIS 4.0. Both assert that upgraded HFC can deliver symmetrical multi-gigabit services at lower cost. Charter estimates upgrade costs at approximately $100 per home passed (excluding CPE), versus roughly $200 for Comcast. Both operators utilize virtualized CMTS platforms and distributed access architectures (DAA) to support converged HFC/FTTP operations and targeted fiber extensions.

Operational cost differences remain contested. Charter CEO Chris Winfrey characterized the delta as minimal—on the order of one to two dollars per passing—stating, “We’ll take that tradeoff any day.” This reinforces the view that large-scale HFC-to-FTTP overbuilds are unlikely among major incumbents in the near term.

HFC investment also continues. Comcast and Charter are deploying low-latency capabilities based on the IETF Low Latency Low Loss Scalable Throughput (L4S) standard, with Charter already launching in multiple U.S. markets.

Fiber-First Deployments:

Smaller operators are, in some cases, moving more decisively toward FTTP. MCTV, serving approximately 57,000 customers in Ohio and West Virginia, determined that FTTP and DOCSIS 3.1 were cost-comparable and opted for full fiber rebuilds. The operator now passes more than 80% of its footprint with FTTP and has decommissioned roughly two-thirds of its HFC power supplies.

Competitive and Technology Outlook:

The FBA identifies FTTP as the “primary driver” of recent cable subscriber losses, citing “structural limitations” of HFC in symmetry, latency, and scalability “that DOCSIS upgrades can partially address but not fully overcome.” Cable proponents dispute this, pointing to DOCSIS 4.0 and future enhancements.

However, competitive pressure is multi-dimensional. In addition to fiber, FWA is gaining traction, particularly in lower-speed tiers. As a result, operators are increasingly focused on pricing, service bundling, and customer experience, including converged broadband-mobile offerings, rather than peak speeds alone.

On the technology roadmap, CableLabs continues to extend DOCSIS, including exploration of an “operational annex” supporting spectrum up to 3 GHz and downstream rates around 25 Gbit/s, with longer-term targets of 6 GHz and 50 Gbit/s. At the same time, it is expanding work on PON, including coherent PON, reflecting a more access-technology-agnostic posture.

Migration Trajectory:

Some industry veterans align with the FBA’s long-term view. John Chapman has advocated a “fiber-first” strategy, citing projections that access networks may need to support up to 1 Tbit/s by 2040. Rather than abrupt transitions, this approach emphasizes phased migration from HFC to FTTP while leveraging existing infrastructure.

Quotes:

John Chapman, a DOCSIS pioneer and former long-time Cisco Systems engineering exec, suggested last year that the cable industry should adjust its thinking and take a “fiber-first” approach as historical trends indicate that broadband access networks will need to be capable of supporting speeds of 1 Tbit/s by 2040. Rather than doing a quick cutover, he thinks MSO’s should migrate from HFC to FTTP over an extended period. But they should get started now.

“The industry has reached an inflection point between the maturity of DOCSIS and the inevitability of fiber. It’s about coming up with a graceful, pragmatic solution to migrate, to transition from DOCSIS to fiber. And that migration’s going to take 20 years. But we need a strategy that accommodates the two,” he said. “It’s a cultural change.”

Jay Rolls, a former Charter CTO and current CTO of BSP, a company that conducts due diligence on various types of broadband network transactions, also believes that cable operators should be weighing whether FTTP is the right move. His recent analysis suggests that the capital spend on a DOCSIS 4.0 overhaul is comparable to an FTTP rebuild.

“Every network and market is different, but the tipping point is fast arriving where overbuilding fiber makes as much financial sense as upgrading HFC, especially when you consider what comes next,” he said on a Light Reading podcast.

References:

Upgrading MSO Networks to Fiber to the Home (FTTH): A Technical Perspective

https://fiberconnect.fiberbroadband.org/

Fiber Broadband Association Middle Mile WG: how to use “Digital Infrastructure Networks” for coordinated fiber backbone investments

Analysis: AT&T 1Q-2026 results: increased fiber penetration, FWA momentum, D2D deals, and mobile/home internet bundles

Fiber Optic Boost: Corning and Meta in multiyear $6 billion deal to accelerate U.S data center buildout

Fiber Optic Networks & Subsea Cable Systems as the foundation for AI and Cloud services

How will fiber and equipment vendors meet the increased demand for fiber optics in 2026 due to AI data center buildouts?

Automating Fiber Testing in the Last Mile: An Experiment from the Field

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

T-Mobile expands FTTH footprint via 50-50 JVs with Oak Hill Capital and Wren House

T-Mobile US is expanding its fiber-to-the-home (FTTH) footprint by investing ~$2.7 billion in two new 50-50 joint ventures (JVs) with Oak Hill Capital ($2 billion for GoNetspeed and Greenlight Networks) and Wren House ($700 million for i3 Broadband). These partnerships aim to pass around 1.8 million homes, largely in the northeastern U.S., accelerating T-Mobile’s fixed broadband expansion alongside their 5G network. Those deals are expected to close in the first half of 2027. T-Mobile, which markets fiber services under the brand name “T-Fiber,” said the deals are part of a plan to serve 18 million to 19 million total broadband customers – including 3 million to 4 million fiber customers – by the end of 2030.

- GoNetspeed offers voice and broadband services to residential and business customers (including multiple-dwelling units, or MDUs) in parts of Alabama, Connecticut, Maine, Massachusetts, Missouri, New York, Pennsylvania and Vermont, with plans to light up networks in cities in New Jersey and Rhode Island. GoNetspeed sells a handful of fiber-fed broadband tiers up to 6 Gbit/s and offers DSL in some areas.

- Greenlight Networks, founded in 2011, supports speeds up to 10 Gbit/s for residential and business customers in New York (Rochester, Buffalo, Binghamton, Capital Region and Hudson Valley), Pennsylvania (Scranton, Wilkes-Barre and Lehigh Valley), and Baltimore, Maryland. It serves about 225,000 homes and nearly 10,000 small businesses.

- i3 Broadband serves parts of Illinois and Missouri with broadband and voice services.

T-Mobile said GoNetspeed and Greenlight are expected to pass a combined 1.3 million households by the end of 2026, with i3 Broadband expected to pass roughly 500,000 households by that time. As it is with T-Mobile’s prior fiber JVs, the service providers involved in this new pair of transactions will operate under wholesale models that enable T-Mobile to offer “simple” plans with no annual service contracts.

- Target: ~1.8 million new homes passed, primarily in the Northeast.

- Partners: Joint ventures with investment firms Oak Hill Capital and Wren House.

- Strategic Goal: Deepen fiber footprint to support a target of 18-19 million broadband customers by 2030, with 3-4 million on fiber.

- Starlink Business Backup: T-Mobile is introducing a Starlink-powered backup option to provide comprehensive, resilient connectivity for business customers, enhancing their “SuperBroadband” offerings.

- Broadband Strategy: This move follows earlier 2025 moves, including the joint venture with EQT to acquire Lumos and the takeover of Metronet, strengthening T-Mobile’s position as a major fiber competitor.

Image Credit: Panther Media GmbH/Alamy Stock Photo

……………………………………………………………………………………………………………………………………………………………

New Street Research analysts David Barden and Vikash Harlalka (via Light Reading) said GoNetspeed passed about 770,000 locations in June 2025, with 725,000 of them passed with fiber, and the rest passed by copper and hybrid fiber/coax (HFC). They also estimate that Greenlight passed about 330,000 locations and i3 Broadband passed roughly 370,000 with fiber as of June 2025. Combined, the three operators involved in the proposed T-Mobile JVs pass nearly 1.5 million total locations, including 1.4 million fiber locations, according to NSR.

Based on an assumption that each fiber network operator has achieved penetration levels of about 25%, New Street said this implies that the Oak Hill JV has about 275,000 customers while the Wren House JV has about 75,000. At that level, they said that means T-Mobile is paying about $725 million for customers from the Oak Hill JV and $250 million for customers from the Wren House JV. The New Street analysts said today’s announcement shows that T-Mobile continues to have interest in acquiring “pure-play fiber operators.” As such, they also believe that the odds of a reported T-Mobile-Uniti deal have dropped.

The analysts also believe that the new fiber-focused JVs will also lower the odds of a potential combination with a major US cable operators such as Charter Communications. “A larger fiber footprint also makes it more difficult to get a deal approved by regulators,” they explained.

……………………………………………………………………………………………………………………………………………………………..

Even with the two new JV’s, T-Mobile’s fiber footprint will still be dwarfed by those of AT&T and Verizon,

- AT&T is targeting a 60 million fiber-to-the-premises (FTTP) footprint by 2030, leveraging joint ventures to accelerate deployment.

- Verizon, following acquisitions of Frontier and Eaton Fiber, projects 32 million fiber passings by 2026, with plans to reach 40–50 million via further partnerships and inorganic growth. Verizon, which also struck a deal to acquire Eaton Fiber last fall, is on track to end 2026 with more than 32 million fiber passings. CEO Dan Schulman reiterated that Verizon plans to broaden its fiber footprint to 40 million-50 million “over the medium term,” but did not provide a more specific timeframe. “There’s no question that fiber is a key differentiator … against competitors that don’t have it,” Schulman said, noting that the attachment rate of Verizon mobile customers who also get broadband from Verizon is hovering at about 55%.

……………………………………………………………………………………………………………………………………………………………..

References:

https://www.lightreading.com/broadband/t-mobile-s-new-jvs-fixate-on-fiber

https://www.lightreading.com/broadband/verizon-surpasses-6m-fwa-subs-as-priority-shifts-to-fiber

T-Mobile US announces new broadband wireless and fiber targets, 5G-A with agentic AI and live voice call translation

Analysis: AT&T 1Q-2026 results: increased fiber penetration, FWA momentum, D2D deals, and mobile/home internet bundles

Evercore: T-Mobile’s fiber business to boost revenue and achieve 40% penetration rate after 2 years

T-Mobile & EQT Joint Venture (JV) to acquire Lumos and build out T-Mobile Fiber footprint

Highlights of 2025 Broadband Nation Expo: Comcast, T-Mobile keynotes + selected quotes

T-Mobile posts impressive wireless growth stats in 2Q-2024; fiber optic network acquisition binge to complement its FWA business

Fiber Broadband Association Middle Mile WG: how to use “Digital Infrastructure Networks” for coordinated fiber backbone investments

The Fiber Broadband Association (FBA) today released guidance from its Middle Mile Working Group (WG) which outlines how states can strengthen digital infrastructure through coordinated fiber backbone investment. Fiber is the foundation of AI, powering the high-capacity, low-latency, secure connectivity that links data centers, cloud infrastructure, and the communities that depend on them. To meet rising national demand, the U.S. must scale fiber deployment 2.3x by 2029. This goal requires accelerated infrastructure builds and strong coordination among states, utilities, and industry partners.

Digital Infrastructure Networks are strategic fiber optic systems that connect the core internet backbone to last-mile broadband providers. By strengthening these middle-mile connections, states can reduce the cost of broadband deployment, improve network resiliency, and expand connectivity to unserved and underserved communities.

“Middle-mile infrastructure is what allows broadband networks to scale,” said Sachin Gupta, Chair of the Middle Mile Working Group and Vice President of Business and Technology Strategies at Centranet. “When high-capacity fiber backbones are located closer to underserved communities, providers can extend last-mile networks more affordably, reach more locations, operate more efficiently, and better serve communities across the state.”

Among the recommendations:

- Coordinate infrastructure projects across agencies to streamline deployment and reduce unnecessary construction

- Implement “dig once” policies that install conduit or fiber whenever roads or utility corridors are opened for construction

- Leverage state-owned assets, including rights-of-way, existing fiber routes, and utility infrastructure

- Modernize permitting and coordination processes to accelerate broadband builds

FBA will further explore these strategies during two Middle Mile Working Group breakout sessions at Fiber Connect 2026, taking place Tuesday morning. The sessions include:

- Rural Collaboration, Infrastructure Planning, and Sustaining Affordable, High-Performance Middle Mile Broadband

- Unlocking New Middle Mile Opportunities for ISPs and Community Networks

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………

Technical Topology: The DWDM Advantage:

- Massive Spectral Efficiency: Multiplexing up to 96+ channels onto a single fiber, with each wavelength supporting 100G, 400G, or 800G data rates.

- Scalable Architecture: Capacity can be increased incrementally by lighting new wavelengths without forklift upgrades or additional trenching.

- Resilient Topologies:

- Ring Networks: Often preferred for regional backhaul, utilizing Optical Add/Drop Multiplexers (OADMs) to provide self-healing 1+1 protection and sub-50ms failover.

- Mesh Networks: The gold standard for reliability, offering multiple diverse paths to ensure uptime even during multiple fiber cuts.

- Long-Haul Performance: Utilizing Erbium-Doped Fiber Amplifiers (EDFAs) and Raman amplification to maintain signal integrity over spans exceeding 1,000 km without electronic regeneration.

References:

Learn more; fiberconnect.fiberbroadband.org. Learn more about FBA’s research here or subscribe to FBA’s Fiber Forward Weekly newsletter here to stay updated.

Digital Infrastructure Networks: Meeting the Broadband Challenge for State Governments

Australia’s NBN and Nokia demonstrate multi-generation optical technologies concurrently over existing FTTP infrastructure

Automating Fiber Testing in the Last Mile: An Experiment from the Field

U.S. fiber rollouts now pass ~52% of homes and businesses but are still far behind HFC

Highlights of FiberConnect 2024: PON-related products dominate

Fiber Broadband Association: 1.4M Fiber Miles Needed for 5G in Top 25 U.S. Metros

AT&T expands its fiber-optic network amid slowdown in mobile subscriber growth

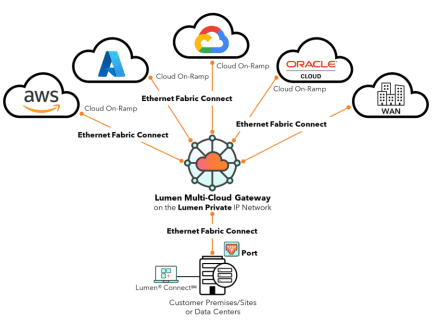

Lumen launches Multi-Cloud Gateway (MCGW) and expands metro fiber network after selling consumer FTTH business to AT&T

Lumen Technologies has announced a new Multi-Cloud Gateway (MCGW) and expanded its metro fiber optic network across 16 major U.S. markets, delivering up to 400G b/sec connectivity to support high-speed AI data processing. This initiative provides a software-defined, self-service platform for secure, private, and flexible connections between enterprise data centers and cloud providers.

Lumen says the new MCGW product and expanded fiber footprint will simplify how data moves across hybrid environments by bringing both centralized multi-cloud routing and high-capacity private metro connectivity. The result will be a more consistent, controllable networking foundation for AI and other modern workloads. This expansion is part of a broader strategy where Lumen plans to reach 58 million fiber miles by 2031 to meet the soaring demand for AI-ready infrastructure.

“Moving data across hybrid environments is a lot like managing air traffic – you need clear routes, predictable timing, and the ability to adjust when conditions change. Most legacy networks weren’t built for that level of coordination,” said Jim Fowler, Lumen chief technology and product officer. “With our expanded network fabric, Lumen gives enterprises a way to move data securely, effortlessly, and consistently across clouds, data centers, and edge locations, designed to reduce the complexity that hold AI-driven operations back.”

Multi-Cloud Gateway: Multi-Cloud Gateway (MCGW) is a core element of Lumen’s shift to cloud-based telecom. Built as a software-defined, self-service routing layer on Lumen’s global fiber network, MCGW provides private, high-capacity connectivity among enterprises, hyperscalers and emerging cloud platforms. It turns traditional telecom interconnection into a programmable cloud fabric, allowing customers to dynamically connect cloud-to-cloud and cloud-to-enterprise environments, optimize traffic for performance and cost, and support advanced use cases such as AI workload distribution and real-time data exchange. By unifying connectivity, routing and policy, MCGW is designed to reduce operational complexity, speed time to service and lower total cost of ownership.

Lumen Multi-Cloud Gateway:

Image credit: Lumen Technologies

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

Metro Ethernet & IP Services: Expanded high-capacity, dedicated connectivity across 16 U.S. markets, delivering up to 100Gbps between regional data centers, campuses, and edge locations and up to 400Gbps at key cloud data centers in those markets. This enables fast, secure movement of massive datasets for AI training, analytics, replication, and disaster recovery.

Recently upgraded markets include Northern Virginia; Atlanta; Chicago; Columbus; Dallas; Denver; Kansas City; Las Vegas; Los Angeles; Minneapolis; New York City; Phoenix; Portland; San Antonio; San Jose; and Seattle.

“AI is reshaping network design, pushing enterprises to move from experimentation to execution with architectures that reduce latency, cost variability, and operational complexity,” said Courtney Munroe, Vice President, Worldwide Telecommunications Research at IDC. “As workloads become more distributed and performance sensitive, organizations are rethinking how they connect edge sites, data centers, and multiple clouds, and Lumen’s network fabric shows how programmable networks can deliver more consistent data movement.”

The business impact is immediate and practical for industries scaling their AI ambitions:Financial Services: Keep risk, payments, and fraud workloads synchronized across multiple clouds with centralized policy control for lower latency and more predictable performance.

- Retail: Improve business agility by accelerating data movement across cloud and enterprise environments, so analytics keep pace with changing demand.

- Healthcare: Maintain data separation, support telehealth services, imaging and analytics, disaster recovery, and manage research workloads across institutions and resource centers.

- Manufacturing: Connect regional facilities and cloud environments to enable real-time analytics and predictive maintenance.

- Multi-Cloud Gateway (MCGW): Launched and available as of February 17, 2026, as a software-defined, self-service routing layer.

- Metro Network Expansion: Currently live across 16 major U.S. markets (including New York, Chicago, and Los Angeles), offering up to 400 Gbps at key cloud data centers.

- Internet On-Demand: Expanded in late 2025 to over 10 million new business locations, providing “cloud-like” connectivity scalability within minutes.

- Wavelength RapidRoutes: Available for deployment in just 20 business days, significantly faster than industry standard turn-up times.

- Microsoft: Chosen to expand Microsoft’s network capacity to support surging demand for Azure AI services. Microsoft utilizes Lumen’s Private Connectivity Fabric (PCF) for custom network architecture between data centers.

- Google Cloud: Partnered to modernize Network-as-a-Service (NaaS) offerings. This allows Lumen-managed SD-WAN and security services to be hosted directly in Google Cloud regions.

- Palantir Technologies: A multi-year alliance formed in October 2025 to combine Lumen’s connectivity fabric with Palantir’s Foundry and AI Platform (AIP), enabling enterprises to deploy AI faster in multi-cloud environments.

- Other Hyperscalers: Lumen has secured approximately $8.5 billion in private connectivity deals with companies including Amazon Web Services (AWS) and Meta to support their AI model training.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………

On February 2nd, Lumen announced that it completed the sale of its Mass Markets fiber-to-the-home business in 11 states, including Quantum Fiber, to AT&T for $5.75 billion in cash. The sale includes substantially all of the related consumer fiber access network and customer relationships in those 11 states, which serve more than 1 million fiber customers and reaches more than 4 million enabled fiber locations. The completed transaction is another strategic milestone in Lumen’s transformation into the leading enterprise digital networking services company built for the multi-cloud, AI-driven economy rather than for consumer fiber access.

As part of the completed transaction, Lumen will retain assets that will continue to serve as the foundation of its enterprise transformation, including all national, regional, state, and metro level fiber backbone network infrastructure, central offices and associated real estate. In addition, Lumen is retaining and caring for its copper-based consumer services, which continue to provide a strong ongoing financial contribution to Lumen. The enterprise and wholesale fiber customers will remain with Lumen in all geographies.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………

About Lumen Technologies:

Lumen is unleashing the world’s digital potential. We ignite business growth by connecting people, data, and applications – quickly, securely, and effortlessly. As the trusted network for AI, Lumen uses the scale of our network to help companies realize AI’s full potential. From metro connectivity to long-haul data transport to our edge cloud, security, managed service, and digital platform capabilities, we meet our customers’ needs today and as they build for tomorrow.

When networks shift from constraint to enabler, organizations can move faster, scale with confidence, and unlock greater innovation. To learn more about these products and availability timelines, visit Multi-Cloud Gateway and Connectivity Services.

……………………………………………………………………………………………………………………………………………………………………………………………

References:

https://assets.lumen.com/is/content/Lumen/lumen-multi-cloud-gateway-data-sheet

Lumen: “We’re Building the Backbone for the AI Economy” – NaaS platform to be available to more customers

Lumen deploys 400G on a routed optical network to meet AI & cloud bandwidth demands

Lumen and Ciena Transmit 1.2 Tbps Wavelength Service Across 3,050 Kilometers

Analysts weigh in: AT&T in talks to buy Lumen’s consumer fiber unit – Bloomberg

Lumen Technologies to connect Prometheus Hyperscale’s energy efficient AI data centers

Microsoft choses Lumen’s fiber based Private Connectivity Fabric℠ to expand Microsoft Cloud network capacity in the AI era

Lumen, Google and Microsoft create ExaSwitch™ – a new on-demand, optical networking ecosystem

ACSI report: AT&T, Lumen and Google Fiber top ranked in fiber network customer satisfaction