Month: May 2021

T-Mobile 5G hype vs Craig Moffett: “We’re not in the 5G era yet”

T-Mobile US reported total revenues of $19.8 billion and service revenues of $14.2 billion in the last quarter. T-Mobile’s gain of 1.2M post-paid net additions was solidly ahead of Wall Street consensus of 1.0M, and was similar to last year’s pro forma gain of 1.3M. The company added 773K post-paid phone subscribers, dramatically better than last year’s pro-forma gain of just 104K, and blowing away consensus of 475K.

T-Mobile’s 773,000 postpaid phone customer additions during the first quarter handily beat AT&T’s 536,000 and Verizon’s loss of 178,000 customers, according to Walter Piecyk, a financial analyst at LightShed Partners. They continue to take market share. Their annual post-paid subscriber growth rate of 3.9% marks a sharp acceleration from the 2.7% growth rate reported last quarter.

T-Mobile has already migrated 20% of Sprint’s customers, and 50% of Sprint’s traffic (a doubling from

last quarter), to the much more robust T-Mobile network. The vast majority of Sprint customers

are already enjoying service benefits from access (even with legacy handsets) to T-Mobile’s

lower frequency spectrum bands.

T-Mobile: America’s Largest, Fastest and Most Reliable 5G Network Extends its Lead

- Extended Range 5G covers 295 million people across 1.6 million square miles, 4x more than Verizon and 2x more than AT&T

- Ultra Capacity 5G covers 140 million people and on track to cover 200 million people nationwide by the end of 2021

- Majority of independent third-party network benchmarking reports show T-Mobile as the clear leader in 5G speed and availability

- Network perception catching up to reality with a nearly 120 percent increase in consumers who view T-Mobile as “The 5G Company” since Q3 2019

Image Credit: T-Mobile

……………………………………………………………………………………………………………………………………………….

On the company’s earnings call, T-Mobile US CEO Mike Sievert said that “discerning customers” are choosing T-Mobile’s new Magenta Max pricing plan, which offers few limits in the amount of 5G data that customers can consume. T-Mobile’s new Magenta Max customers consume 40% more data than its other 5G customers, and fully 70% more data than T-Mobile’s average 4G LTE customers.

“The take rate has just been amazing,” T-Mobile CFO Peter Osvaldik said of Magenta Max. “There are premium customers that are attracted to this premium network.”

“We’ve never been able to outrun the insatiable demand that customers have,” Sievert said of Internet service providers in general. “So when you provide the industry’s only true, unlimited plan, they do what they do, they use it up.”

According to Sievert, that indicates that T-Mobile’s 5G network will be a big winner. “We’re really starting to pull away from the pack. T-Mobile is positioned to maintain our 5G leadership for the duration of the 5G era.”

In a great example of braggadocio, Sievert said:

“We have again demonstrated that our unique winning formula and balanced approach enables us to grow share while delivering strong financial results. In our increasingly connected world, we recognize our role as stewards of this profitable company and industry, while continuing to use our Un-carrier DNA to bring change to wireless and broadband alike, to disrupt the status quo and ultimately benefit customers. And this quarter was no exception.”

T-Mobile said it now covers fully 140 million people with its 2.5GHz network, which it calls “ultra capacity.” By the end of this year, the company said that number will increase to 200 million people. Meantime, speeds available on that network will rise from an average of 300 Mbit/s today to up to 400 Mbit/s by the end of this year, the operator said. 5G speeds will continue to rise after that, according to T-Mobile’s network chief Neville Ray. “2022 is going to be even better,” he said.

Analyst Craig Moffett (who participated in the earnings call) put somewhat of a damper on all that 5G hype by stating: “But we’re not in the 5G era yet. We’re not even a year into the first generation of 5G iPhones. Less than 10% of Americans have 5G-enabled phones, and half of those probably only got a new phone because they needed a replacement. 5G isn’t really driving handset selection, or service provider selection, yet.”

“That T-Mobile continues to take share even in the twilight of the LTE era is reassuring. In a world of roughly comparable networks, they are competing on the basis of price alone… and they are taking share rapidly. In 5G, they will compete not only on the basis of the industry’s lowest prices, but also the industry’s best network. As we’ve said before, T-Mobile’s ‘worst to first’ story is a generational one. Networks don’t achieve advantage overnight, and they don’t lose it overnight, either. Ten and twenty-year cycles in telecom aren’t unusual.”

“T-Mobile’s brand, and its network, have been ascendant for years. But they have, up to now, achieved only parity. Their path to network superiority is potentially even longer, and, we suspect, even brighter.”

T-Mobile continues to increase market share even in the twilight of the LTE era is reassuring. In a

world of roughly comparable networks, they are competing on the basis of price alone… and they

are taking share rapidly. In 5G, they will compete not only on the basis of the industry’s lowest prices, but also the industry’s best network.

……………………………………………………………………………………………………………………………………….

References:

https://www.t-mobile.com/news/business/t-mobile-reports-strong-first-quarter-2021-results

https://www.lightreading.com/5g/does-5g-make-difference-t-mobile-says-yes/d/d-id/769256?

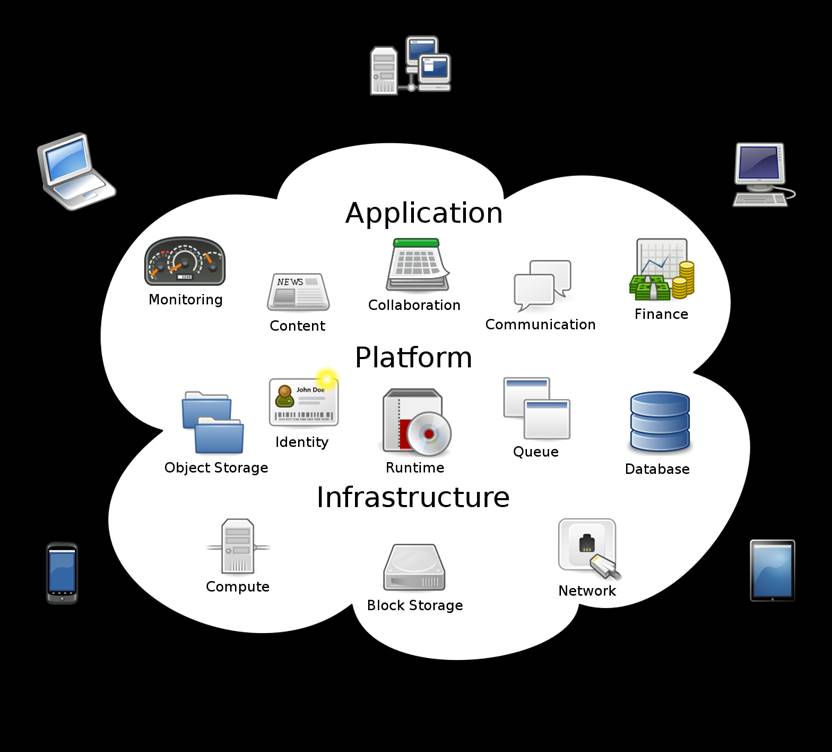

Gartner: Global public cloud spending to reach $332.3 billion in 2021; 23.1% YoY increase

According to Gartner, global public cloud spending is forecast to reach $332.3 billion in 2021, increasing by 23.1% from $270 billion in 2020. Growth in cloud spending can be attributed to increased adoption in technologies such as virtualization, edge computing and containerization.

“The events of last year allowed CIOs to overcome any reluctance of moving mission critical workloads from on-premises to the cloud,” said Sid Nag, research vice president at Gartner. “Even absent the pandemic there would still be a loss of appetite for data centers.

Table 1. Worldwide Public Cloud Services End-User Spending Forecast (Millions of U.S. Dollars)

| 2020 | 2021 | 2022 | |

| Cloud Business Process Services (BPaaS) | 46,131 | 50,165 | 53,121 |

| Cloud Application Infrastructure Services (PaaS) | 46,335 | 59,451 | 71,525 |

| Cloud Application Services (SaaS) | 102,798 | 122,633 | 145,377 |

| Cloud Management and Security Services | 14,323 | 16,029 | 18,006 |

| Cloud System Infrastructure Services (IaaS) | 59,225 | 82,023 | 106,800 |

| Desktop as a Service (DaaS) | 1,220 | 2,046 | 2,667 |

| Total Market | 270,033 | 332,349 | 397,496 |

BPaaS = business process as a service; IaaS = infrastructure as a service; PaaS = platform as a service; SaaS = software as a service Note: Totals may not add up due to rounding.

Source: Gartner (April 2021)

As organizations mobilize for a massive global effort to produce and distribute COVID-19 vaccinations, SaaS based applications that enable essential tasks such as automation and supply chain is critical. Such applications continue to demonstrate reliability in scaling vaccine management, which in turn will help CIOs further validate the ongoing shift to cloud.

“It’s important to note that the usage and adoption of cloud that served enterprises well during the ongoing crisis will not look the same in the coming years,” said Mr. Nag. “It will further evolve from serving pedestrian use cases such as infrastructure and application migration, to those that combine cloud with technologies such as artificial intelligence, the Internet of Things, 5G and more.

“In other words, cloud will serve as the glue between many other technologies that CIOs want to use more of, allowing them to leapfrog into the next century as they address more complex and emerging use cases. It will be a disruptive market, to say the least.”

Cloud Computing Fuels Revenues and Profits for Big 3 Cloud Companies:

Amazon’s market-leading AWS cloud business grew revenue 32% in the first quarter, a faster pace than analysts had expected and accelerating from 28% growth in the fourth quarter. Microsoft’s revenue has skyrocketed since it invested billions of dollars to build a massive, interconnected cloud computing platform. Revenues for its Azure cloud offering were up 50% in the quarter. Meanwhile, revenues at Google’s Cloud business grew 46% this past quarter. However, Google continues to be a distant third to Amazon and Microsoft in the cloud business.

All three cloud providers are making a big push into edge computing and 5G “cloud native” core networks. That effectively makes them leaders in those new tech markets, with the traditional network providers playing a subservient role. For example, Dish Network will build its 5G core network using the AWS cloud infrastructure and services.

These big three cloud businesses are in reality massive cloud (i.e. Internet) resident data centers with high-speed interconnections (Data Center Interconnects). There’s no reason to think growth will slow any time soon. Were they stand-alone businesses, they would be the three largest enterprise-software entities in the world. And they design their own compute servers, making them the world’s largest global computer companies too!

………………………………………………………………………………………………………………………………………………….

While cloud services boomed in the past year, Gartner suggests that spending on cloud might take a different note in 2021 and 2022 as enterprises shift away from infrastructure and application migration towards advanced applications integrating AI and IoT and 5G.

In the first quarter of 2021, research and analytics firm Canalys reported that global cloud services infrastructure spending grew to $41.8 billion to represent a 35% year-on-year increment and 5% quarter-on-quarter growth.

References:

Curmudgeon/Sperandeo: Technology Fab Five Biggest Winners from Covid-19 Pandemic

Vodafone and Google Cloud to Develop Integrated Data Platform

Vodafone and Google Cloud today announced a new, six-year strategic partnership to drive the use of reliable and secure data analytics, insights, and learnings to support the introduction of new digital products and services for Vodafone customers simultaneously worldwide.

In a significant expansion of their existing agreement, Vodafone and Google Cloud will jointly build a powerful new integrated data platform with the added capability of processing and moving huge volumes of data globally from multiple systems into the cloud.

The platform, called ‘Nucleus‘, will house a new system – ‘Dynamo‘ – which will drive data throughout Vodafone to enable it to more quickly offer its customers new, personalized products and services across multiple markets. Dynamo will allow Vodafone to tailor new connectivity services for homes and businesses through the release of smart network features, such as providing a sudden broadband speed boost.

Capable of processing around 50 terabytes of data per day, equivalent to 25,000 hours of HD film (and growing), both Nucleus and Dynamo, which are industry firsts, are being built in-house by Vodafone and Google Cloud specialist teams. Up to 1,000 employees of both companies located in Spain, the UK, and the United States are collaborating on the project.

Vodafone has already identified more than 700 use-cases to deliver new products and services quickly across Vodafone’s markets, support fact-based decision-making, reduce costs, remove duplication of data sources, and simplify and centralize operations. The speed and ease with which Vodafone’s operating companies in multiple countries can access its data analytics, intelligence, and machine-learning capabilities will also be vastly improved.

By generating more detailed insight and data-driven analysis across the organization and with its partners, Vodafone customers around the world can have a better and more enriched experience. Some of the key benefits include:

- Enhancing Vodafone’s mobile, fixed, and TV content and connectivity services through the instantaneous availability of highly personalized rewards, content, and applications. For example, a consumer might receive a sudden broadband speed boost based on personalized individual needs.

- Increasing the number of smart network services in its Google Cloud footprint from eight markets to the entire Vodafone footprint. This allows Vodafone to precisely match network roll-out to consumer demand, increase capacity at critical times, and use machine learning to predict, detect, and fix issues before customers are aware of them.

- Empowering data scientists to collaborate on key environmental and health issues in 11 countries using automated machine learning tools. Vodafone is already assisting governments and aid organisations, upon their request, with secure, anonymised, and aggregated movement data to tackle COVID-19. This partnership will further improve Vodafone’s ability to provide deeper insights, in accordance with local laws and regulations, into the spread of disease through intelligent analytics across a wider geographical area.

- Providing a complete digital replica of many of Vodafone’s internal support functions using artificial intelligence and advanced analytics. Called a digital twin, it enables analytic models on Google Cloud to improve response times to enquiries and predict future demand. The system will also support a digital twin of Vodafone’s vast digital infrastructure worldwide.

- In addition, Vodafone will re-platform its entire SAP environment to Google Cloud, including the migration of its core SAP workloads and key corporate SAP modules such as SAP Central Finance.

Johan Wibergh, Chief Technology Officer for Vodafone, said: “Vodafone is building a powerful foundation for a digital future. We have vast amounts of data which, when securely processed and made available across our footprint using the collective power of Vodafone and Google Cloud’s engineering expertise, will transform our services, to our customers and governments, and the societies where they live and serve.”

Thomas Kurian, CEO at Google Cloud, commented: “Telecommunications firms are increasingly differentiating their customer experiences through the use of data and analytics, and this has never been more important than during the current pandemic. We are thrilled to be selected as Vodafone’s global strategic cloud partner for analytics and SAP, and to co-innovate on new products that will accelerate the industry’s digital transformation.”

Revenues at Google’s Cloud business grew 46% this past quarter. However, Google continues to be a distant third to Amazon and Microsoft in the cloud business.

Technical Notes:

All data generated by Vodafone in the markets in which it operates is stored and processed in the required Google Cloud facilities as per local jurisdiction requirements and in accordance with local laws and regulations. Customer permissions and Vodafone’s own rigorous security and privacy by design processes also apply.

On the back of their collaborative work, Vodafone and Google Cloud will also explore opportunities to provide consultancy services, offered either jointly or independently, to other multi-national organizations and businesses.

The platform is being built using the latest hybrid cloud technologies from Google Cloud to facilitate the rapid standardization and movement of data in both Vodafone’s physical data centers and onto Google Cloud. Dynamo will direct all of Vodafone’s worldwide data, extracting, encrypting, and anonymizing the data from source to cloud and back again, enabling intelligent data analysis and generating efficiencies and insight.

References:

https://cloud.google.com/press-releases/2021/0503/vodafone-google-cloud (video)

Strand Consult: The 10 Parameters of Open RAN; AT&T memo to FCC

Strand Consult is attempting to determine if, when, and how Open RAN (TIP project) and O-RAN (Alliance) will replace conventional RAN on a 1:1 basis without compromising the network quality, security, energy efficiency, and other important factors. Mobile operators have little ability to raise price, so operators must compete on network quality, coverage, and other factors. Here are few things to keep in mind.

In general, mobile ARPU is falling. In many countries, operators are trying to shift the focus away from price by competing on innovation and quality. For example, US mobile operators compete on the quality and coverage of their 4G and 5G networks. Mobile operators are focused on rolling out technology quickly, maintaining customer satisfaction, and ensuring quality of experience and other key performance indicators (KPIs). Chief technology officers, network managers, and other technical staff are laser focused on these KPIs and are loath to make changes to which would negatively impact these indicators.

In general, Strand Consult observes that what public affairs officials say about OpenRAN differs significantly from what network managers say.

Strand Consult’s 10 parameters to evaluate OpenRAN:

Strand Consult’s investigation has been guided by 10 parameters or questions to determine the value of OpenRAN. Here is what we’ve learned.

- Whether OpenRAN is a technical standard. The O-RAN Alliance is a private organization that develops technical specifications for OpenRAN. It should not be confused with the OpenRAN Policy Coalition which is a public affairs organization. The O-RAN Alliance is not a standards development organization (SDO), but rather an industrial collaboration that builds solutions on top of 3GPP specifications. While industrial cooperation is important, there can be no mobile networks the 3rd Generation Partnership Project (3GPP), an umbrella term for many standards organizations which develop protocols for mobile telecommunications and define the technological inputs for cellular networks. Companies like Rakuten develop their own corporate and proprietary concepts for OpenRAN. These concepts that do not necessarily follow a particular standard (3GPP) or O-RAN Alliance specification.

- Whether OpenRAN can replace Chinese equipment. Some mobile operators have suggested that OpenRAN is the way to avoid Huawei and ZTE in mobile networks. However other Chinese companies are deeply involved with OpenRAN technical specifications, product roadmap, and strategy. One founding member of the O-RAN Alliance is China Mobile, a state-owned company and the world’s largest mobile operator with 950 million subscribers and 450,000 employees. The O-RAN Alliance has more than 40 Chinese member companies, many of which government-owned and military aligned (See Strand Consult’s research note 44 Chinese companies have joined the OpenRAN effort, a strategy to reduce Huawei’s presence in 5G). The Chinese members of 0-RAN Alliance outnumber the Europeans. China Mobile’s Chih-Lin has veto power over the organization. China Mobile leads or co lead 8 of the 9 O-RAN Alliance’s working groups either as chairman or vice-chairman.

- OpenRAN and 5G innovation. OpenRAN proponents claim it will have a revolutionary impact on 5G, however reports suggest that large scale deployment of OpenRAN won’t happen until 2025. This means that OpenRAN cannot replace existing RAN on a 1:1 basis today. The 5G networks rolled out today use the standards from 3GPP Release 15 with increased functionality forthcoming in Releases 16 and 17 within two years. There are more than 144 3GPP-5G commercial networks deployed but only one proprietary OpenRAN 5G network (Rakuten). If OpenRAN is to increase 5G innovation, it must evolve faster than 5G itself. Presently it is not on par with the 5G standards defined years ago. It is difficult to see how OpenRAN can catch up when the significant resources already supporting the 3GPP standards timeline.

- OpenRAN and 5G deployment. Today mobile operators are rolling out 5G at a faster than 4G and even fast than 3G. In practical terms, 5G networks already built in 2019 and 2020 and those to be built in 2021 and 2022 already have the standards roadmap in place. If OpenRAN can’t catch up by 2025, operators have only two choices, delay 5G until 2025 (when 6G will start to take root) or replace their 5G equipment in 4 to 5 years. OpenRAN may be too little, too late for 5G operators.

- OpenRAN and vendor diversity. OpenRAN proponents claim that it will create more competition in the network equipment market. The 5G network equipment vendor market has many vendors and segments. Omdia details more than a dozen full-service providers with additional providers in segments for antennas, basebands, remote radios, small cells, macro cells, phase shifters and so on. This idea that there are not many vendors for 5G equipment was likely created by Huawei to deter the security reviews and subsequent restrictions imposed on the military-aligned company. If anything, the restrictions on Huawei have helped to open the door to new equipment vendors which could not compete because of Huawei’s predatory pricing and anti-competitive tactics. For example, Samsung has quickly gained market share and is supply 5G rollouts in the US, Australia, and other countries.

- OpenRAN and network equipment cost. OpenRAN proponents suggest that it can lower the cost of network equipment. The cost competitiveness of OpenRAN versus RAN is not yet known. It may be that some OpenRAN providers can offer equipment more cheaply on some parameters, but the cost advantage may not be significant when considering all the costs such as supply, availability, energy consumption, security, warranty, network integration, equipment matching, new contracts and service level agreements etc. However, operators frequently reduce their number of vendors so that they can enjoy lower unit costs with volume purchasing, the company BUYIN is a great case. For an operator’s perspective, check out the comments from Neil McRae, Managing Director and Chief Architect at BT (Scroll to minute 51 minute in the video). McRae explains that when he took his job, he inherited a network portfolio with 50 vendors. He subsequently reduced it to 4 vendors and saved £1 billion in 3 years. He observed that too many vendors not only increased cost, it increased complexity. He is wary of notions of “open architectures” which require managing portfolios of 5-50 vendors. He noted that vendor reduction increased shareholder value and that he would pursue the same strategy again.

- OpenRAN and security. OpenRAN proponents suggest that OpenRAN technology and the “unbundling” of 5G hardware and software is the means reduce reliance on Huawei and hence greater security. However, it is not clear how trading one known insecure Chinese vendor for 50 unknown Chinese vendors is the path to greater security. The issue of backdoors is omnipresent on all Chinese hardware given the country’s disposition and associated intelligence and surveillance policies. Moreover, it is not clear how security is improved when network owners must vet not one, but multiple new OpenRAN vendors. The time and cost to perform this review would seem to be multiplied by the number of vendors the operators takes on.

- OpenRAN and energy efficiency. Energy efficiency is an increasingly important issue for mobile operators which expect to compete on carbon reduction strategies. Naturally if OpenRAN could offer a greener solution, that would be an advantage. However, it is reported that many OpenRAN installation use the Intel X86 processor, which is less efficient than specialized RAN chips. If anything, energy consumption could increase if signals must traverse a multitude of mix and match components instead of a single end-to-end system designed with energy efficiency in mind. To reduce energy, Apple developed tits own processer as an alternative to Intel X86.

- OpenRAN and Rakuten. The media has promoted a supposed Rakuten success story with OpenRAN success. However, Rakuten is not offering open-source tools, but rather proprietary OpenRAN solution. It offers this through a freemium model in which free service is offered for a period, and operators pay down the line. Some companies have success with freemium and loss leader models, but typically they need scale.

- OpenRAN and the indigenous movement. OpenRAN has been promoted as a way to support domestic innovation like India or Brazil or what Germany’s Economic Minister calls for European-only actors in 5G. Curiously many of these calls are coupled with operator strategies to keep Huawei equipment in place because OpenRAN will not be ready for some years. Policymakers have also pursued subsidies and other financial incentives to support local OpenRAN startups which may design the equipment in their respective country but manufacture it in China. Unfortunately, production in China and with Chinese partners could compromise security, as the Supermicro case demonstrates.

Conclusion

The many problems that OpenRAN is purported to solve is impressive. In fact, I have to go back to 3G in 2000 to find the level of hype observed today with OpenRAN. Indeed, the Huawei problem is so serious that people are desperate for a solution. However, in the enthusiasm for the OpenRAN solution, too many want to look past the inconvenient reality that China is shaping much of the Open RAN future particularly through the O-RAN Alliance.

It is important to develop secure alternatives to Huawei, but this is not a reason to oversell OpenRAN. While it may be commendable to pursue the goals proffered by OpenRAN proponents, the actual impact of OpenRAN must be measured by real world facts and experience.

The questions remain how OpenRAN will affect the CAPEX and OPEX mobile operators in the short, medium and long term and whether operators will buy OpenRAN as a serious 1:1 alternative to standard RAN in Paris, London, Berlin, Madrid, New York, Sao Paulo and Copenhagen. It seems that OpenRAN is falling short of expectations.

Separately, AT&T told the FCC it plans to begin adding open RAN-compliant equipment into its network “within the next year.”

That puts AT&T on roughly the same timeframe as Verizon. Verizon’s SVP Adam Koeppe told Light Reading earlier this year that the operator’s 5G hardware vendors – Ericsson, Samsung and Nokia – will begin supplying open RAN-compliant equipment starting later this year. And he expects that the bulk of their equipment shipments to Verizon will comply with open RAN specifications by next year. AT&T told the FCC it expects to implement similar changes into its own network.

“The challenge for an operator shifting to any open network architecture, including but not limited to O-RAN, will be maintaining network reliability, integrity and performance for customers during the transition,” the operator wrote in a filing. “For our part, AT&T serves multiple customer groups, with varied and often complex, service requirements. As we introduce O-RAN into our network, our goal will be maintaining the same high level of performance at scale. We are actively working in this direction.”

References:

https://www.lightreading.com/open-ran/atandt-to-launch-open-ran-by-next-year/d/d-id/769199?

AT&T to FCC: Promoting the Deployment of 5G Open Radio ) Access Networks – GN Docket No. 21-63

https://ecfsapi.fcc.gov/file/1042871504579/AT%26T%20Comments%20to%20FCC%20NOI%20(04.28.21).pdf