Analysis: Nokia’s strong growth in Optical Networks and AI network infrastructure

Executive Summary:

While Nokia’s first-quarter profitability improved across all reported metrics, year-over-year comparisons were significantly affected by a €120 million ($140 million) non-recurring charge recorded in the Mobile Networks business in the prior-year period. On a comparable basis, net profit increased 93% to approximately €295 million ($345 million). Despite ongoing cost restructuring initiatives, the company’s comparable operating margin remained at 6.2%, well below the ~11% levels observed in the corresponding quarters of 2021 and 2022, indicating continued margin compression relative to earlier cycle peaks.

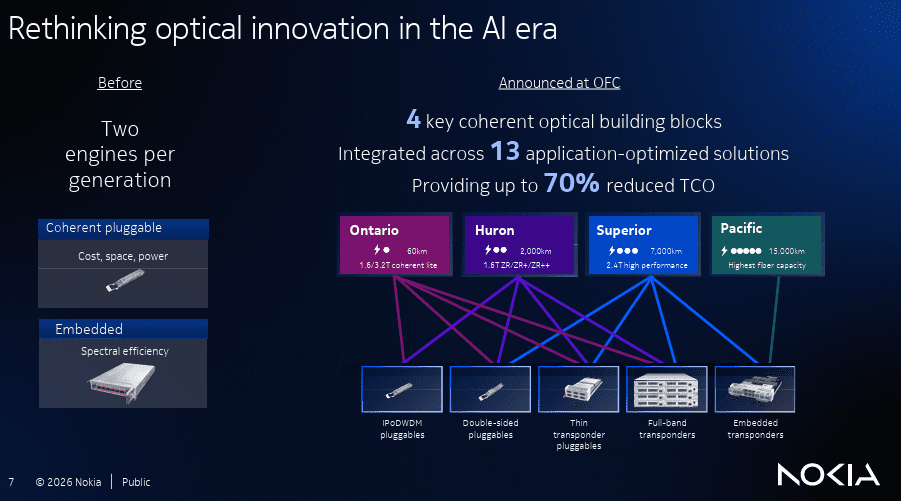

Optical networking has emerged as Nokia’s primary growth engine, significantly outpacing the company’s overall performance. At the group level, Nokia reported first-quarter comparable revenue growth of 3% year-over-year (4% in constant currency) to €4.5 billion ($5.3 billion). The acquisition of Infinera, which was completed in March last year, surely helped. As did massive investments by AI data center companies because Nokia’s optical gear is used for both intra and inter data center connectivity.

The company said Thursday that first-quarter sales of optical network infrastructure rose 12% on year, driven by demand from AI and cloud customers in the Americas. It booked 1 billion euros ($1.17 billion) of orders from AI & Cloud customers in the quarter and now sees overall sales in the network infrastructure business growing 12%-14% this year, having previously expected 6%-8%. The company had previously announced it was investing in additional manufacturing capacity to support growth and maximize the opportunity in this accelerating market.

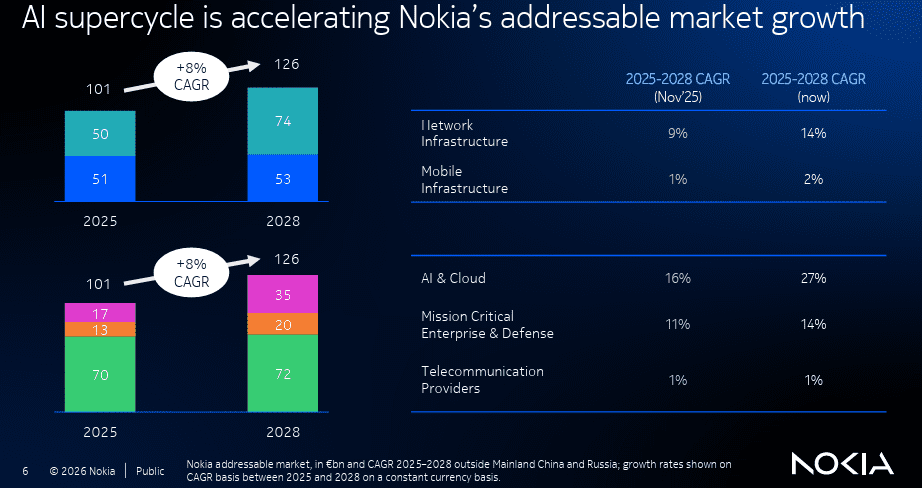

When Nokia held its capital markets day last November, the company expecting hyperscalers to invest about $540 billion in total capital expenditure this year. That number has now been raised to more than $700 billion, Nokia CEO Justin Hotard told reporters. As part of that flows into Nokia’s order book, first-quarter optical sales grew 56% year-over-year, to €821 million (US$959 million).

Image Credits: NOKIA

……………………………………………………………………………………………………………………………………………………………………………………………………….

Performance across segments remains uneven. Key drags included the fixed broadband segment within Network Infrastructure (NI)—which also encompasses optical—as well as the Mobile Networks (MN) radio access business. Despite these headwinds, CEO Justin Hotard is positioning NI, particularly its optical and IP routing units, as the core drivers of near-term growth. The company has raised its full-year NI growth outlook to 12–14%, up from the 6–8% range communicated in January, reflecting stronger momentum in high-capacity transport and IP networking demand.

Nokia is also guiding for full-year comparable operating profit in the range of €2.0–2.5 billion ($2.3–2.9 billion). At the midpoint, this would represent approximately 11% year-over-year growth relative to 2025, indicating improving operational leverage as higher-growth segments scale. The strongest momentum remains in optical and IP networking, while the legacy radio access business is still working through margin pressure, mix shifts, and the higher capital intensity of next-generation RAN evolution.

Within this context, the Mobile Infrastructure (MI) segment remains the principal source of performance uncertainty. Following internal reorganization, the “radio networks” unit—comprising the majority of the former Mobile Networks business—accounts for 63% of MI revenue. While constant-currency performance was broadly stable, reported radio networks revenue declined 5% year-over-year to €1.58 billion ($1.85 billion), contributing to a 3% decline in total MI revenue to approximately €2.5 billion.

Segment-level profitability metrics require careful normalization. MI reported operating profit of €222 million ($259 million), representing a 68% year-over-year increase. However, adjusting for the absence of the prior-year €120 million charge, operating profit would have declined by approximately 12%. On a normalized basis, operating margin would have decreased from ~9.8% to ~8.9%, rather than increasing from the reported 5.1%, indicating underlying margin pressure in the radio access portfolio.

Additional analytical complexity arises from the inclusion of Nokia Technologies within MI reporting. This licensing-driven business has historically exhibited operating margins exceeding 70%. Assuming a comparable margin profile in the current quarter, its implied operating contribution (~€270 million / $316 million) exceeds the total reported MI operating profit. This suggests that the combined radio networks and associated software activities may be operating at or near breakeven when disaggregated from licensing revenues, highlighting the importance of segment-level transparency in assessing the underlying economic performance of Nokia’s RAN portfolio.

A restructuring program, initiated under Pekka Lundmark and continued by CEO Justin Hotard, is designed to deliver approximately €1.2 billion ($1.4 billion) in annualized cost savings by the end of 2026. This is primarily driven by a planned reduction of approximately 14,000 positions from a September 2023 baseline of ~84,000 employees (excluding subsequently divested businesses). As of year-end 2025, Nokia reported 74,100 employees, excluding Infinera, implying that the majority of targeted reductions have been completed and that approximately 4,000 additional reductions remain. Management has indicated that future efficiency gains are expected to be incremental rather than driven by further large-scale restructuring.

…………………………………………………………………………………………………………………………………………………………………………………………

Analysis:

From a systems perspective, the key signal is that transport and aggregation layers are gaining strategic weight relative to the traditional macro-RAN hardware layer. Optical growth reflects the continued densification of metro and backbone networks, driven by higher east-west traffic, AI and cloud interconnect demand, and the need for lower-latency transport to support distributed radio and edge workloads. That makes optical and IP less of a “supporting cast” and more of the enabling fabric for cloudified telecom architectures.

The RAN market is moving toward software-defined, cloud-native, and increasingly AI-assisted architectures, which raises the bar for vendor differentiation. Nokia has been emphasizing AI-RAN and anyRAN work with NVIDIA and operators including BT, NTT Docomo, T-Mobile, and others, positioning itself around AI-for-RAN, AI-on-RAN, and AI-and-RAN use cases. Architecturally, this suggests the company is trying to move beyond a pure radio-box supplier model toward a compute-centric platform strategy tied to 5G-Advanced and AI-native 6G.

This transition intensifies competition with vendors pursuing virtualized RAN, Open RAN, and multi-vendor disaggregation strategies. In that environment, the critical battleground shifts from integrated proprietary base stations to software portability, orchestration, open interfaces, cloud infrastructure integration, and accelerator support. For Nokia, the commercial challenge is that the economics of vRAN and AI-RAN depend not only on technical readiness, but also on whether operators can justify new compute and orchestration layers without eroding total cost of ownership.

The broader networking trend is convergence between mobile, optical, IP, and cloud infrastructure. The same traffic growth that pressures RAN capacity also increases demand for optical transport, IP routing, and security-aware automation across the transport and service layers. In that sense, Nokia’s segment mix highlights a wider industry direction: radio access is becoming only one part of a larger distributed compute and transport system, rather than the dominant center of gravity.

In conclusion, Nokia is benefiting as telecom architecture is becoming more horizontal and software-driven, while still facing friction in the vertically integrated legacy RAN model. Optical and IP are scaling nicely with increased high speed data center traffic; RAN is being redefined by cloud (vRAN), AI, and disaggregation; and the vendor that can best align silicon, software, orchestration, and transport will be better positioned for 5G-Advanced and early 6G/IMT 2030 transitions.

…………………………………………………………………………………………………………………………………………………………………………………………

References:

https://www.nokia.com/about-us/investors/results-reports/

Nokia in major pivot from traditional telecom to AI, cloud infrastructure, data center networking and 6G

Nokia’s AI Applications Study: “Physical AI” may require RAN redesign to support high‑volume, low‑latency uplink traffic

Nokia to showcase agentic AI network slicing; Ericsson partners with Ookla to measure 5G network slicing performance

Australia’s NBN and Nokia demonstrate multi-generation optical technologies concurrently over existing FTTP infrastructure

China’s telecom industry rapid growth in 2025 eludes Nokia and Ericsson as sales collapse

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

Indosat Ooredoo Hutchison, Nokia and Nvidia AI-RAN research center in Indonesia amongst telco skepticism

Nokia Bell Labs and KDDI Research partner for 6G energy efficiency and network resiliency

2 thoughts on “Analysis: Nokia’s strong growth in Optical Networks and AI network infrastructure”

Leave a Reply

Nokia’s significant pivot toward AI-driven data center and network infrastructure, resulted in a 49% surge in revenue from AI and cloud customers in Q1 2026. The Finland based company is becoming a pure-play AI infrastructure provider! For example, €1 billion in hyperscaler optical orders, a 54% spike in operating profit, and the stock up 9% today to a 16-year high.

Nokia is collaborating with NVIDIA, T-Mobile, SoftBank, and Indosat Ooredoo Hutchison to develop AI-native radio access networks (AI-RAN). Successful tests indicate that AI and RAN workloads can run on shared GPU infrastructure, improving efficiency. Nokia is seeing traction in its 7220 Interconnect Router (IXR) switches for data centers, which offer 1.6 Terabit Ethernet to meet AI workload demands.

Since their legacy mobile business is stagnant, the company is actively redirecting mobile investments to fund the plumbing of the intelligence AI grid, and the gambit is definitely working.

Nokia’s growth in optical networks and AI infrastructure is truly impressive. However, I wonder how their innovative solutions will impact smaller players in the AI & optical networking equipment market. A balanced ecosystem is crucial for driving true advancement.