Data Center Network Equipment

CoreSite Enables 50G Multi-cloud Networking with Enhanced Virtual Connections to Oracle Cloud Infrastructure FastConnect

Note 1. CoreSite is a subsidiary of American Tower Corporation and a member of Oracle PartnerNetwork (OPN).

Note 2. Oracle FastConnect enables customers to bypass the public internet and connect directly to Oracle Cloud Infrastructure and other Oracle Cloud services. With connectivity available at CoreSite’s data centers, FastConnect provides a flexible, economical private connection to higher bandwidth options for your hybrid cloud architecture. Oracle FastConnect is accessible at CoreSite’s data center facilities in Northern Virginia and Los Angeles through direct fiber connectivity. FastConnect is also available via the CoreSite Open Cloud Exchange® in seven CoreSite markets, including Los Angeles, Silicon Valley, Denver, Chicago, New York, Boston and Northern Virginia.

The integration of Oracle FastConnect and the CoreSite Open Cloud Exchange offers on-demand, virtual connectivity and access to best in class, end-to-end, fully redundant connection architecture.

Image Credit: CoreSite

…………………………………………………………………………………………………………………………………………………………………………………………………………..

The connectivity of FastConnect and the OCX can offer customers deploying artificial intelligence (AI) and data-intensive applications the ability to transfer large datasets securely and rapidly from their network edge to machine learning (ML) models and big data platforms running on OCI. With the launch of the new OCX capabilities to FastConnect, businesses can gain greater flexibility to provision on-demand, secure bandwidth to OCI with virtual connections of up to 50 Gbps.

With OCI, customers benefit from best-in-class security, consistent high performance, simple predictable pricing, and the tools and expertise needed to bring enterprise workloads to cloud quickly and efficiently. In addition, OCI’s distributed cloud offers multicloud, hybrid cloud, public cloud, and dedicated cloud options to help customers harness the benefits of cloud with greater control over data residency, locality, and authority, even across multiple clouds. As a result, customers can bring enterprise workloads to the cloud quickly and efficiently while meeting the strictest regulatory compliance requirements.

“The digital world requires faster connections to deploy complex, data-intense workloads. The simplified process offered through the Open Cloud Exchange enables businesses to rapidly scale network capacity between the enterprise edge and cloud providers,” said Juan Font, President and CEO of CoreSite, and SVP of U.S. Tower. “These enhanced, faster connections with FastConnect can provide businesses with a competitive advantage by ensuring near-seamless and reliable data transfers at massive scale for real-time analysis and rapid data processing.”

OCI’s extensive network of more than 90 FastConnect global and regional partners offer customers dedicated connectivity to Oracle Cloud Regions and OCI services – providing customers with the best options anywhere in the world. OCI is a deep and broad platform of cloud infrastructure services that enables customers to build and run a wide range of applications in a scalable, secure, highly available, and high-performance environment. From application development and business analytics to data management, integration, security, AI, and infrastructure services including Kubernetes and VMware, OCI delivers unmatched security, performance, and cost savings.

The new Open Cloud Exchange capabilities on FastConnect will be available in Q4 2023.

Related Resources:

- Watch What is The Open Cloud Exchange® and How Can It Simplify and Automate Your Cloud Connectivity?

- Open Cloud Exchange® Solution Brochure

- Trust CoreSite Data Centers to Enable Your AI Strategy

- Why businesses partner with CoreSite

About CoreSite:

CoreSite, an American Tower company (NYSE: AMT), provides hybrid IT solutions that empower enterprises, cloud, network, and IT service providers to monetize and future-proof their digital business. Our highly interconnected data center campuses offer a native digital supply chain featuring direct cloud onramps to enable our customers to build customized hybrid IT infrastructure and accelerate digital transformation. For more than 20 years, CoreSite’s team of technical experts has partnered with customers to optimize operations, elevate customer experience, dynamically scale, and leverage data to gain competitive edge. For more information, visit CoreSite.com and follow us on LinkedIn and Twitter.

References:

IEEE Santa Clara Valley (SCV) Lecture and Tour of CoreSite Multi-Tenant Data Center

https://www.coresite.com/cloud-networking/oracle-fastconnect

Using a distributed synchronized fabric for parallel computing workloads- Part I

by Run Almog Head of Product Strategy, Drivenets (edited by Alan J Weissberger)

Introduction:

Different networking attributes are needed for different use cases. Endpoints can be the source of a service provided via the internet or can also be a handheld device streaming a live video from anywhere on the planet. In between endpoints we have network vertices that handle this continuous and ever-growing traffic flow onto its destination as well as handle the knowhow of the network’s whereabouts, apply service level assurance, handle interruptions and failures and a wide range of additional attributes that eventually enable network service to operate.

This two part article will focus on a use case of running artificial intelligence (AI) and/or high-performance computing (HPC) applications with the resulting networking aspects described. The HPC industry is now integrating AI and HPC, improving support for AI use cases. HPC has been successfully used to run large-scale AI models in fields like cosmic theory, astrophysics, high-energy physics, and data management for unstructured data sets.

In this Part I article, we examine: HPC/AI workloads, disaggregation in data centers, role of the Open Compute Project, telco data center networking, AI clusters and AI networking.

HPC/AI Workloads, High Performance Compute Servers, Networking:

HPC/AI workloads are applications that run over an array of high performance compute servers. Those servers typically host a dedicated computation engine like GPU/FPGA/accelerator in addition to a high performance CPU, which by itself can act as a compute engine, and some storage capacity, typically a high-speed SSD. The HPC/AI application running on such servers is not running on a specific server but on multiple servers simultaneously. This can range from a few servers or even a single machine to thousands of machines all operating in synch and running the same application which is distributed amongst them.

The interconnect (networking) between these computation machines need to allow any to any connectivity between all machines running the same application as well as cater for different traffic patterns which are associated with the type of application running as well as stages of the application’s run. An interconnect solution for HPC/AI would resultingly be different than a network built to serve connectivity to residential households or a mobile network as well as be different than a network built to serve an array of servers purposed to answers queries from multiple users as a typical data center structure would be used for.

Disaggregation in Data Centers (DCs):

Disaggregation has been successfully used as a solution for solving challenges in cloud resident data centers. The Open Compute Project (OCP) has generated open source hardware and software for this purpose. The OCP community includes hyperscale data center operators and industry players, telcos, colocation providers and enterprise IT users, working with vendors to develop and commercialize open innovations that, when embedded in product are deployed from the cloud to the edge.

High-performance computing (HPC) is a term used to describe computer systems capable of performing complex calculations at exceptionally high speeds. HPC systems are often used for scientific research, engineering simulations and modeling, and data analytics. The term high performance refers to both speed and efficiency. HPC systems are designed for tasks that require large amounts of computational power so that they can perform these tasks more quickly than other types of computers. They also consume less energy than traditional computers, making them better suited for use in remote locations or environments with limited access to electricity.

HPC clusters commonly run batch calculations. At the heart of an HPC cluster is a scheduler used to keep track of available resources. This allows for efficient allocation of job requests across different compute resources (CPUs and GPUs) over high-speed networks. Several HPC clusters have integrated Artificial Intelligence (AI).

While hyperscale, cloud resident data centers and HPC/AI clusters have a lot of similarities between them, the solution used in hyperscale data centers is falling short when trying to address the additional complexity imposed by the HPC/AI workloads.

Large data center implementations may scale to thousands of connected compute servers. Those servers are used for an array of different application and traffic patterns shift between east/west (inside the data center) and north/south (in and out of the data center). This variety boils down to the fact that every such application handles itself so the network does not need to cover guarantee delivery of packets to and from application endpoints, these issues are solved with standard based retransmission or buffering of traffic to prevent traffic loss.

An HPC/AI workload on the other hand, is measured by how fast a job is completed and is interfacing to machines so latency and accuracy are becoming more of a critical factor. A delayed packet or a packet being lost, with or without the resulting retransmission of that packet, drags a huge impact on the application’s measured performance. In HPC/AI world, this is the responsibility of the interconnect to make sure this mishaps do not happen while the application simply “assumes” that it is getting all the information “on-time” and “in-synch” with all the other endpoints it shares the workload with.

–>More about how Data centers use disaggregation and how it benefits HPC/AI in the second part of this article (Part II).

Telco Data Center Networking:

Telco data centers/central offices are traditionally less supportive of deploying disaggregated solutions than hyper scale, cloud resident data centers. They are characterized by large monolithic, chassis based and vertically integrated routers. Every such router is well-structured and in fact a scheduled machine built to carry packets between every group of ports is a constant latency and without losing any packet. A chassis based router would potentially pose a valid solution for HPC/AI workloads if it could be built with scale of thousands of ports and be distributed throughout a warehouse with ~100 racks filled with servers.

However, some tier 1 telcos, like AT&T, use disaggregated core routing via white box switch/routers and DriveNets Network Cloud (DNOS) software. AT&T’s open disaggregated core routing platform was carrying 52% of the network operators traffic at the end of 2022, according to Mike Satterlee, VP of AT&T’s Network Core Infrastructure Services. The company says it is now exploring a path to scale the system to 500Tbps and then expand to 900Tbps.

“Being entrusted with AT&T’s core network traffic – and delivering on our performance, reliability and service availability commitments to AT&T– demonstrates our solution’s strengths in meeting the needs of the most demanding service providers in the world,” said Ido Susan, DriveNets founder and CEO. “We look forward to continuing our work with AT&T as they continue to scale their next-gen networks.”

Satterlee said AT&T is running a nearly identical architecture in its core and edge environments, though the edge system runs Cisco’s disaggregates software. Cisco and DriveNets have been active parts of AT&T’s disaggregation process, though DriveNets’ earlier push provided it with more maturity compared to Cisco.

“DriveNets really came in as a disruptor in the space,” Satterlee said. “They don’t sell hardware platforms. They are a software-based company and they were really the first to do this right.”

AT&T began running some of its network backbone on DriveNets core routing software beginning in September 2020. The vendor at that time said it expected to be supporting all of AT&T’s traffic through its system by the end of 2022.

Attributes of an AI Cluster:

Artificial intelligence is a general term that indicates the ability of computers to run logic which assimilates the thinking patterns of a biological brain. The fact is that humanity has yet to understand “how” a biological brain behaves, how are memories stored and accessed, how come different people have different capacities and/or memory malfunction, how are conclusions being deduced and how come they are different between individuals and how are actions decided in split second decisions. All this and more are being observed by science but not really understood to a level where it can be related to an explicit cause.

With evolution of compute capacity, the ability to create a computing function that can factor in large data sets was created and the field of AI focuses on identifying such data sets and their resulting outcome to educate the compute function with as many conclusion points as possible. The compute function is then required to identify patterns within these data sets to predict the outcome of new data sets which it did not encounter before. Not the most accurate description of what AI is (it is a lot more than this) but it is sufficient to explain why are networks built to run AI workloads different than regular data center networks as mentioned earlier.

Some example attributes of AI networking are listed here:

- Parallel computing – AI workloads are a unified infrastructure of multiple machines running the same application and same computation task

- Size – size of such task can reach thousands of compute engines (e.g., GPU, CPU, FPGA, Etc.)

- Job types – different tasks vary in their size, duration of the run, the size and number of data sets it needs to consider, type of answer it needs to generate, etc. this as well as the different language used to code the application and the type of hardware it runs on contributes to a growing variance of traffic patterns within a network built for running AI workloads

- Latency & Jitter – some AI workloads are resulting a response which is anticipated by a user. The job completion time is a key factor for user experience in such cases which makes latency an important factor. However, since such parallel workloads run over multiple machines, the latency is dictated by the slowest machine to respond. This means that while latency is important, jitter (or latency variation) is in fact as much a contributor to achieve the required job completion time

- Lossless – following on the previous point, a response arriving late is delaying the entire application. Whereas in a traditional data center, a message dropped will result in retransmission (which is often not even noticed), in an AI workload, a dropped message means that the entire computation is either wrong or stuck. It is for this reason that AI running networks requires lossless behavior of the network. IP networks are lossy by nature so for an IP network to behave as lossless, certain additions need to be applied. This will be discussed in. follow up to this paper.

- Bandwidth – large data sets are large. High bandwidth of traffic needs to run in and out of servers for the application to feed on. AI or other high performance computing functions are reaching interface speeds of 400Gbps per every compute engine in modern deployments.

The narrowed down conclusion from these attributes is that a network purposed to run AI workloads differs from a traditional data center network in that it needs to operate “in-synch.

There are several such “in-synch” solutions available. The main options are: Chassis based solutions, Standalone Ethernet solutions, and proprietary locked solutions.–>These will be briefly described to their key advantages and deficiencies in our part II article.

Conclusions:

There are a few differences between AI and HPC workloads and how this translates to the interconnect used to build such massive computation machines.

While the HPC market finds proprietary implementations of interconnect solutions acceptable for building secluded supercomputers for specific uses, the AI market requires solutions that allow more flexibility in their deployment and vendor selection.

AI workloads have greater variance of consumers of outputs from the compute cluster which puts job completion time as the primary metric for measuring the efficiency of the interconnect. However, unlike HPC where faster is always better, some AI consumers will only detect improvements up to a certain level which gives interconnect jitter a higher impact than latency.

Traditional solutions provide reasonable solutions up to the scale of a single machine (either standalone or chassis) but fail to scale beyond a single interconnect machine and keep the required performance to satisfy the running workloads. Further conclusions and merits of the possible solutions will be discussed in a follow up article.

………………………………………………………………………………………………………………………………………………………………………………..

About DriveNets:

DriveNets is a fast-growing software company that builds networks like clouds. It offers communications service providers and cloud providers a radical new way to build networks, detaching network growth from network cost and increasing network profitability.

DriveNets Network Cloud uniquely supports the complete virtualization of network and compute resources, enabling communication service providers and cloud providers to meet increasing service demands much more efficiently than with today’s monolithic routers. DriveNets’ software runs over standard white-box hardware and can easily scale network capacity by adding additional white boxes into physical network clusters. This unique disaggregated network model enables the physical infrastructure to operate as a shared resource that supports multiple networks and services. This network design also allows faster service innovation at the network edge, supporting multiple service payloads, including latency-sensitive ones, over a single physical network edge.

References:

https://drivenets.com/resources/events/nfdsp1-drivenets-network-cloud-and-serviceagility/

https://www.run.ai/guides/hpc-clusters/hpc-and-ai

https://drivenets.com/news-and-events/press-release/drivenets-network-cloud-now-carries-more-than-52-of-atts-core-production-traffic/

https://techblog.comsoc.org/2023/01/27/att-highlights-5g-mid-band-spectrum-att-fiber-gigapower-joint-venture-with-blackrock-disaggregation-traffic-milestone/

AT&T Deploys Dis-Aggregated Core Router White Box with DriveNets Network Cloud software

DriveNets Network Cloud: Fully disaggregated software solution that runs on white boxes

Equinix to deploy Nokia’s IP/MPLS network infrastructure for its global data center interconnection services

Today, Nokia announced that Equinix will deploy a new Nokia IP/MPLS network infrastructure to support its global interconnection services. As one of the largest data center and colocation providers, Equinix currently runs services on multiple networks from multiple vendors. With the new network, Equinix will be able to consolidate into one, efficient web-scale infrastructure to provide FP4-powered connectivity to all data centers – laying the groundwork for customers to deploy 5G networks and services.

Muhammad Durrani, Director of IP Architecture for Equinix, said, “We see tremendous opportunity in providing our customers with 5G services, but this poses special demands for our network, from ultra-low latency to ultra broadband performance, all with business- and mission-critical reliability. Nokia’s end-to-end router portfolio will provide us with the highly dynamic and programmable network fabric we need, and we are pleased to have the support of the Nokia team every step of the way.”

“We’re pleased to see Nokia getting into the data center networking space and applying the same rigor to developing a next-generation open and easily extendible data center network operating system while leveraging its IP routing stack that has been proven in networks globally. It provides a platform that network operations teams can easily adapt and build applications on, giving them the control they need to move fast.”

Sri Reddy, Co-President of IP/Optical Networks, Nokia, said, “We are working closely with Equinix to help advance its network and facilitate the transformation and delivery of 5G services. Our end-to-end portfolio was designed precisely to support this industrial transformation with a highly flexible, scalable and programmable network fabric that will be the ideal platform for 5G in the future. It is exciting to work with Equinix to help deliver this to its customers around the world.”

With an end-to-end portfolio, including the Nokia FP4-powered routing family, Nokia is working in partnership with operators to deliver real 5G. The FP4 chipset is the industry’s leading network processor for high-performance routing, setting the bar for density and scale. Paired with Nokia’s Service Router Operating System (SR OS) software, it will enable Equinix to offer additional capabilities driven by routing technologies such as Ethernet VPNs (EVPNs) and segment routing (SR).

Image Credit: Nokia

……………………………………………………………………………………………………………………………………………………………………………….

This latest deal comes just two weeks after Equinix said it will host Nokia’s Worldwide IoT Network Grid (WING) service on its data centers. WING is an Infrastructure-as-a-Service offering that provides low-latency and global reach to businesses, hastening their deployment of IoT and utilizing solutions offered by the Edge and cloud.

Equinix operates more than 210 data centers across 55 markets. It is unclear which of these data centers will first offer Nokia’s services and when WING will be available to customers.

“Nokia needed access to multiple markets and ecosystems to connect to NSPs and enterprises who want a play in the IoT space,” said Jim Poole, VP at Equinix. “By directly connecting to Nokia WING, mobile network operators can capture business value across IoT, AI, and security, with a connectivity strategy to support business transformation.”

References:

…………………………………………………………………………………………………………………………………………………………..

About Nokia:

We create the technology to connect the world. Only Nokia offers a comprehensive portfolio of network equipment, software, services and licensing opportunities across the globe. With our commitment to innovation, driven by the award-winning Nokia Bell Labs, we are a leader in the development and deployment of 5G networks.

Our communications service provider customers support more than 6.4 billion subscriptions with our radio networks, and our enterprise customers have deployed over 1,300 industrial networks worldwide. Adhering to the highest ethical standards, we transform how people live, work and communicate. For our latest updates, please visit us online www.nokia.com and follow us on Twitter @nokia.

Resources:

- Webpage: Nokia 7750 SR-s

- Webpage: Nokia FP4 silicon

- Webpage: Nokia Service Router Operating System (SR OS)

- Webpage: Nokia Network Services Platform

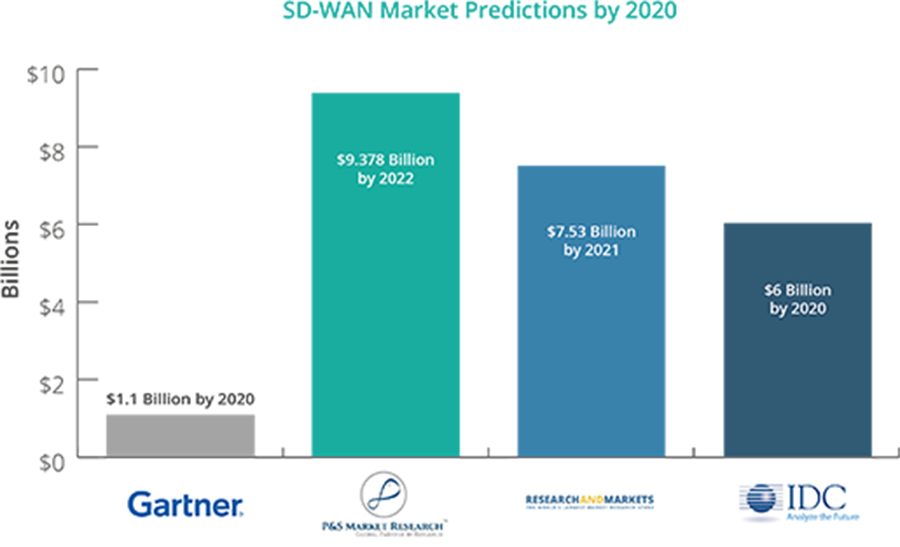

Dell’Oro: Data Center Switch market declined 9% YoY; SD-WAN market increased at slower rate than in 2019

Market research firm Dell’Oro Group reported today that the worldwide Data Center Switch market recorded its first decline in nine years, dropping 9 percent year-over-year in the first quarter. 1Q 2020 revenue level was also the lowest in three years. The softness was broad-based across all major branded vendors, except Juniper Networks and white box vendors. Revenue from white box vendors was propelled mainly by strong demand from Google and Amazon.

“The COVID-19 pandemic has created some positive impact on the market as some customers pulled in orders in anticipation of supply shortage and elongated lead times,” said Sameh Boujelbene, Senior Director at Dell’Oro Group. “Yet this upside dynamic was more than offset by the pandemic’s more pronounced negative impact on customer demand as they paused purchases due to macro-economic uncertainties. Supply constraints were not major headwinds during the first quarter but expected to become more apparent in the next quarter,” added Boujelbene.

Additional highlights from the 1Q 2020 Ethernet Switch – Data Center Report:

- The revenue decline was broad-based across all regions but was less pronounced in North America.

- We expect revenue in the market to decline high single-digit in 2020, despite some pockets of strength from certain segments.

The Dell’Oro Group Ethernet Switch – Data Center Quarterly Report offers a detailed view of the market, including Ethernet switches for server access, server aggregation, and data center core. (Software is addressed separately.) The report contains in-depth market and vendor-level information on manufacturers’ revenue; ports shipped; average selling prices for both Modular and Fixed Managed and Unmanaged Ethernet Switches (1000 Mbps,10, 25, 40, 50, 100, 200, and 400 GE); and regional breakouts. To purchase these reports, please contact us by email at [email protected].

…………………………………………………………………………………………………………………………………………………

Separately, Dell’Oro Group reported that the market for software-defined (SD)-WAN equipment increased by 24% in the first quarter (year-to-year), which was significantly below the 64% growth seen in 2019. Citing supply chain issues created by the coronavirus pandemic, the market research firm’s Shin Umeda predicted the market will post double-digit growth in 2020 despite “macroeconomic uncertainty.”

- Supply chain disruptions accounted for the majority of the Service Provider (SP) Router and CES Switch market decline in 1Q 2020.

- The SP Router and CES market in China showed a modest decline in 1Q 2020, but upgrades for 5G infrastructure are expected to drive strong demand over the rest of 2020.

Omdia: High-speed data-center Ethernet adapter market at $1.7 billion in 2019

Executive Summary:

The market for Ethernet adapters with speeds of 25 gigabits (25GE) and faster deployed by enterprises, cloud service providers and telecommunication network providers at data centers topped $1 billion for the first time in 2019, according to Omdia.

The total Ethernet adapter market size stood at $1.7 billion for the year. This result was in line with Omdia’s long term server and storage connectivity forecast. Factors driving that forecast include the growth in data sets, such as those computed by analytics algorithms looking for patterns, and the adoption of new software technologies like AI and ML which must examine large data sets to be effective, driving larger movement of data.

“Server virtualization and containerization reached new highs in 2019 and drove up server utilization. This increased server connectivity bandwidth requirements, and the need for higher speed Ethernet adapters” said Vlad Galabov, principal analyst for data center IT, at Omdia. “The popularization of data-intensive workloads, like analytics and AI, were also strong drivers for higher speed adapters in 2019”

25GE Ethernet adapters represented more than 25 percent of total data-center Ethernet adapter ports and revenue in 2019, as reported by Omdia’s Ethernet Network Adapter Equipment Market Tracker. Omdia also found that the price per each 25GE port is continued to decline. A single 25GE port cost an average of $81 in 2019, a decrease of $9 from 2018.

Despite representing a small portion of the market, 100GE Ethernet adapters are increasingly deployed by cloud service providers and enterprises running high-performance computing clusters. Shipments and revenue for 100GE Ethernet adapter ports both grew by more than 60 percent in 2019. Each 100GE adapter port is also becoming more affordable. In 2019, an individual 100GE Ethernet adapter port cost $321 on average, a decrease of $34 from 2018.

“Cloud service providers (CSPs) are leading the transition to faster networks as they run multi-tenant servers with a large number of virtual machines and/or containers per server. This is driving high traffic and bandwidth needs,” Galabov said. “Omdia expects telcos to invest more in higher speeds going forward—including 100GE—driven by network function virtualization (NFV) and increased bandwidth requirements from HD video, social media, AR/VR and expanded IoT use cases.”

The Ethernet outlook:

Omdia expects Ethernet adapter revenue to grow 21 percent on average each year through 2024. Despite the COVID-19 lockdown, the Ethernet adapter market is set to remain close to this growth curve in 2020.

Ethernet adapters that can provide complete on-card processing of network, storage or memory protocols, data-plane offload or that can offload server memory access will account for half of the total market revenue in 2020, or $1.1 billion. Ethernet adapters that have an onboard field customizable processor such as a field-programmable gate array (FPGA) or system on chip (SoC), will account for slightly more than than a quarter of 2020 adapter revenue, totaling $557 million. Adapters that only provide Ethernet connectivity will make up a minority share of the market, at just $475 million.

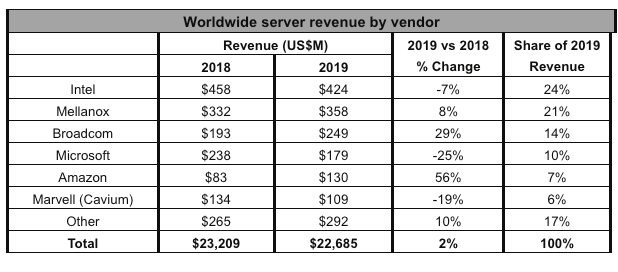

Intel maintains lead:

Looking at semiconductor vendor market share, Intel held 24 percent of the 2019 Ethernet adapter market, shipping adapters worth $424 million in 2019. This represents a 2.5-point decrease from 2018 that Omdia attributes to the aging Intel Ethernet adapter portfolio which consists primarily of 1GE and 10GE adapters with Ethernet connectivity only. Intel indicated it will introduce adapters with offload functionality in 2020 that will help it remain competitive in the market.

Mellanox (now part of NVIDIA) captured 21 percent of the 2019 Ethernet adapter market, a 1-point increase compared to 2018. The vendor reported strong growth of its 25GE and 100GE offload adapters driven by strong cloud service provider demand and growing demand among enterprises for 25GE networking.

Broadcom was the third largest Ethernet adapter vendor in 2019, commanding a 14 percent share of the market, an increase of 3 points from 2018. Broadcom’s revenue growth was driven by strong demand for high-speed offload and programmable adapters at hyperscale CSPs.

In 2019, Microsoft and Amazon continued to adopt in-house-developed Ethernet adapters. Given their large scale and the high value of their high-speed offload and programmable adapters, the companies cumulatively deployed Ethernet adapters worth over $300 million. This made them the fourth and fifth largest makers of Ethernet adapters in 2019. As both service providers deploy 100GE adapters in larger numbers in 2020, they’re set to remain key trendsetters in the market.

Amazon AWS and Microsoft Azure continued to use in-house-developed Ethernet adapters. Given their large scale and the high value of their high-speed offload and programmable adapters, the companies cumulatively deployed Ethernet adapters worth over $300 million, according to Omdia. This made Microsoft and Amazon, respectively, the fourth and fifth largest makers of Ethernet adapters in 2019. As both service providers deploy 100GE adapters in larger numbers in 2020, Omdia expects them to continue to be key trendsetters in the market going forward.

About Omdia:

Omdia is a global technology research powerhouse, established following the merger of the research division of Informa Tech (Ovum, Heavy Reading and Tractica) and the acquired IHS Markit technology research portfolio*.

We combine the expertise of over 400 analysts across the entire technology spectrum, analyzing 150 markets publishing 3,000 research solutions, reaching over 14,000 subscribers, and covering thousands of technology, media & telecommunications companies.

Our exhaustive intelligence and deep technology expertise allow us to uncover actionable insights that help our customers connect the dots in today’s constantly evolving technology environment and empower them to improve their businesses – today and tomorrow.

………………………………………………………………………………………………………………………………………………..

Omdia is a registered trademark of Informa PLC and/or its affiliates. All other company and product names may be trademarks of their respective owners. Informa PLC registered in England & Wales with number 8860726, registered office and head office 5 Howick Place, London, SW1P 1WG, UK. Copyright © 2020 Omdia. All rights reserved.

*The majority of IHS Markit technology research products and solutions were acquired by Informa in August 2019 and are now part of Omdia.

TMR: Data Center Networking Market sees shift to user-centric & data-oriented business + CoreSite DC Tour

TMR Press Release edited by Alan J Weissberger followed by Coresite Data Center Talk & Tour for IEEE ComSocSCV and Power Electronics members

TMR Executive Summary and Forecast:

The global data center networking market is expected to emerge as highly competitive due to rising demand for networking components.

The major players operating in the global data center networking market include Hewlett Packard Enterprise, Cisco Systems, Inc., Arista Networks, Microsoft Corporation, and Juniper Networks. The key players are also indulging into business strategies such as mergers and acquisitions to improve their existing technologies. Those vendors are investing heavily in the research and development activities to sustain their lead in the market. Besides, these firms aim to improve their product portfolio in order to expand their global reach and get an edge over their competitors globally.

The global data center networking market is likely to pick up a high momentum since the firms are rapidly shifting to a more user-centric and data-oriented business. According to a recent report by Transparency Market Research (TMR), the global data center networking market is expected to project a steady CAGR of 15.5% within the forecast period from 2017 to 2025. In 2016, the global market was valued around worth US$63.05 bn, which is projected to reach around a valuation of US$228.40 bn by 2025.

On the basis of component, the global data center networking market is segmented into services, software, and hardware. Among these, the hardware segment led the market in 2016 with around 52.0% of share of data center networking market, as per the revenue. Nevertheless, projecting a greater CAGR than other segments, software segment is as well foreseen to emerge as the key segment contributing to the market growth. Geographically, North America was estimated to lead the global market in 2016. Nevertheless, Asia Pacific is likely to register the leading CAGR of 17.3% within the forecast period from 2017 to 2025.

Rising Demand for Networking Solutions to Propel Growth in Market

Increased demand for networking solutions has initiated a need for firms to change data center as a collective automated resource centers, which provide better flexibility to shift workload from any cloud so as to improve the operational efficiency.

Rising number of internet users across the globe require high-speed interface. Companies are highly dependent on the data centers in terms of efficiency to decrease the operational cost and improve the productivity.

Nevertheless, virtualization and rising demand for end-use gadgets are the major restrictions likely to hamper growth in the data center networking market in the coming years. Rising usage of mobile devices and cloud services also is hindering the steady strides in the data center networking market.

Popularity of Big Data to Add to Market Development in Future:

Rising popularity of big data and cloud services from the industry as well as consumer is anticipated to fuel the development in the global data center networking market. Advantages such as low operational costs, flexibility, better security and safety, and improved performance are likely to proliferate the market growth.

Disaster recovery and business continuity has resulted in simplification of data center networking by saving both money and time for companies. Financial advantages along with technology is likely to augur the demand in data center networking and cloud computing.

Companies are highly focused on data center solution providers to perform efficiently and effectively, with better productivity, high profit, and decreased prices. These goals require high-end networking technologies and upgraded performance server. It also needs a proper integration between simplified networking framework and server to reach the optimum level of performance.

The study presented here is based on a report by Transparency Market Research (TMR) titled “Data Center Networking Market (Component Type – Hardware, Software, and Services; Industry Vertical – Telecommunications, Government, Retail, Media and Entertainment, BFSI, Healthcare, and Education) – Global Industry Analysis, Size, Share, Growth, Trends and Forecast 2017 – 2025.”

Get PDF Brochure at:

https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=21257

Request PDF Sample of Data Center Networking Market:

https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=21257

About TMR:

Transparency Market Research is a next-generation market intelligence provider, offering fact-based solutions to business leaders, consultants, and strategy professionals.

Our reports are single-point solutions for businesses to grow, evolve, and mature. Our real-time data collection methods along with ability to track more than one million high growth niche products are aligned with your aims. The detailed and proprietary statistical models used by our analysts offer insights for making right decision in the shortest span of time. For organizations that require specific but comprehensive information we offer customized solutions through adhoc reports. These requests are delivered with the perfect combination of right sense of fact-oriented problem solving methodologies and leveraging existing data repositories.

TMR believes that unison of solutions for clients-specific problems with right methodology of research is the key to help enterprises reach right decision.”

Contact

Mr. Rohit Bhisey

Transparency Market Research

State Tower

90 State Street,

Suite 700,

Albany, NY – 12207

United States

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Email: [email protected]

Website: https://www.transparencymarketresearch.com

Research Blog: http://www.europlat.org/

Press Release:

………………………………………………………………………………………………………..

Coresite Data Center Tour:

On May 23, 2019, IEEE ComSocSCV and IEEE Power Electronics members were treated to a superb talk and tour of the Coresite Multi-Tenant Data Center (MTDC) in Santa Clara, CA.

CoreSite is a Multi-Tenant Data Center owner that competes with Equinix. CoreSite offers the following types of Network Access for their MTDC colocation customers:

•Direct Access to Tier-1 and Eyeball Networks

•Access to Broad Range of Network Services (Transit/Transport/Dark Fiber)

•Direct Access to Public Clouds (Amazon, Microsoft, Google, etc)

•Direct Access to Optical Ethernet Fabrics

………………………………………………………….

CoreSite also provides POWER distribution and backup on power failures:

•Standby Generators

•Large Scale UPS

•Resilient Design

•Power Quality

•A/B Power Delivery

•99.999% Uptime

….and PHYSICAL SECURITY:

•24/7 OnSite Security Personnel

•Dual-Authentication Access

•IP DVR for All Facility Areas

•Perimeter Security

•Equipment Check-In/Out Process

•Access-Control Policies (Badge Deactivation, etc)

……………………………………………………………………………………………………..

There are 28 network operators and cloud service providers that have brought fiber into the CoreSite Santa Clara MTDC campus. The purpose of that is to enable customers to share fiber network/cloud access at a much higher speed and lower cost than would otherwise be realized via premises-based network/cloud access.

While the names of the network and cloud service providers could not be disclosed, network providers included: Verizon, AT&T, Century Link, Zayo. In addition, AWS Direct Connect, Microsoft Azure ExpressRoute, Alibaba Cloud, Google Cloud interconnection and other unnamed cloud providers were said to have provided direct fiber to cloud connectivity for CoreSite’s Santa Clara MTDC customers.

Here’s how network connectivity is achieved within and outside the CoreSite MTDC:

The SMF or MMF from each customer’s colocation cage is physically routed (under the floor) to a fiber wiring cross-connect/patch panel maintained by Coresite. The output fibers are then routed to a private room where the network/cloud providers maintain their own fiber optic gear (fiber optic multiplexers/switches, DWDM transponders and other fiber transmission equipment) which connect to the outside plant fiber optic cable(s) for each network/cloud services provider.

The outside plant fiber fault detection and restoration are done by each network/cloud provider- either via a mesh topology fiber optic network or 1:1 or N:1 hot standby. Coresite’s responsibility ends when it delivers the fiber to the provider cages. They do, however, have network engineers that are responsible for maintenance and trouble shooting in the DC when necessary.

Instead of using private lines or private IP connections, CoreSite offers an Interconnect Gateway-SM provides their enterprise customers a dedicated, high-performance interconnection solution between their cloud and network service providers, while establishing a flexible IT architecture that allows them to adapt to market demands and rapidly evolving technologies.

CoreSite’s gateway directly integrates enterprises’ WAN architecture into CoreSite’s native cloud and carrier ecosystem using high-speed fiber and virtual interconnections. This solution includes:

-Private network connectivity to the CoreSite data center

-Dedicated cabinets and network hardware for routing, switching, and security

-Direct fiber and virtual interconnections to cloud and network providers

-Technical integration, 24/7/365 monitoring and management from a certified CoreSite Solution Partner

-Industry-leading SLA

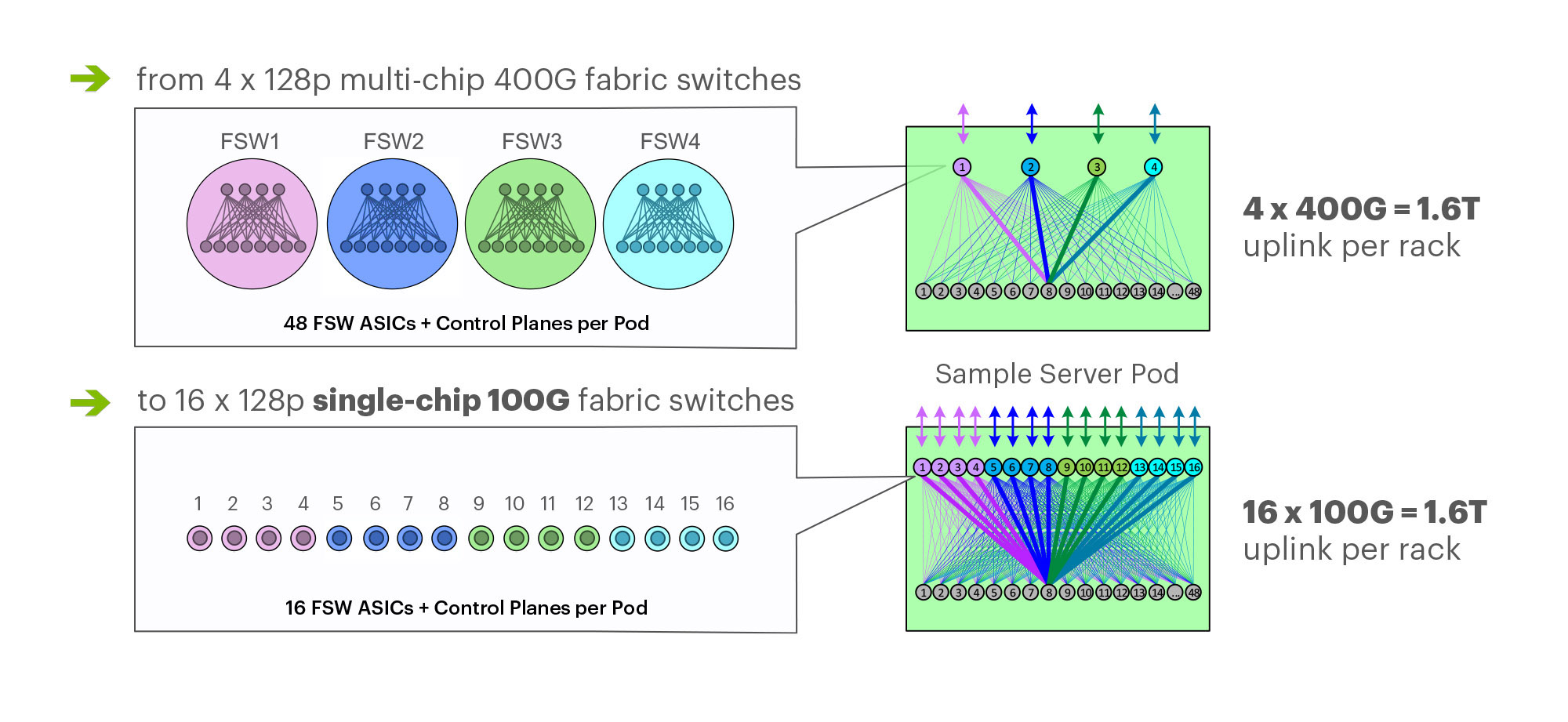

Facebook’s F16 achieves 400G effective intra DC speeds using 100GE fabric switches and 100G optics, Other Hyperscalers?

On March 14th at the 2019 OCP Summit, Omar Baldonado of Facebook (FB) announced a next-generation intra -data center (DC) fabric/topology called the F16. It has 4x the capacity of their previous DC fabric design using the same Ethernet switch ASIC and 100GE optics. FB engineers developed the F16 using mature, readily available 100G 100G CWDM4-OCP optics (contributed by FB to OCP in early 2017), which in essence gives their data centers the same desired 4x aggregate capacity increase as 400G optical link speeds, but using 100G optics and 100GE switching.

F16 is based on the same Broadcom ASIC that was the candidate for a 4x-faster 400G fabric design – Tomahawk 3 (TH3). But FB uses it differently: Instead of four multichip-based planes with 400G link speeds (radix-32 building blocks), FB uses the Broadcom TH3 ASIC to create 16 single-chip-based planes with 100G link speeds (optimal radix-128 blocks). Note that 400G optical components are not easy to buy inexpensively at Facebook’s large volumes. 400G ASICs and optics would also consume a lot more power, and power is a precious resource within any data center building. Therefore, FB built the F16 fabric out of 16 128-port 100G switches, achieving the same bandwidth as four 128-port 400G switches would.

Below are some of the primary features of the F16 (also see two illustrations below):

-Each rack is connected to 16 separate planes. With FB Wedge 100S as the top-of-rack (TOR) switch, there is 1.6T uplink bandwidth capacity and 1.6T down to the servers.

-The planes above the rack comprise sixteen 128-port 100G fabric switches (as opposed to four 128-port 400G fabric switches).

-As a new uniform building block for all infrastructure tiers of fabric, FB created a 128-port 100G fabric switch, called Minipack – a flexible, single ASIC design that uses half the power and half the space of Backpack.

-Furthermore, a single-chip system allows for easier management and operations.

Facebook F16 data center network topology

Facebook F16 data center network topology

………………………………………………………………………………………………………………………………………………………………………………………………..

Multichip 400G b/sec pod fabric switch topology vs. FBs single chip (Broadcom ASIC) F16 at 100G b/sec

…………………………………………………………………………………………………………………………………………………………………………………………………..

In addition to Minipack (built by Edgecore Networks), FB also jointly developed Arista Networks’ 7368X4 switch. FB is contributing both Minipack and the Arista 7368X4 to OCP. Both switches run FBOSS – the software that binds together all FB data centers. Of course the Arista 7368X4 will also run that company’s EOS network operating system.

F16 was said to be more scalable and simpler to operate and evolve, so FB says their DCs are better equipped to handle increased intra-DC throughput for the next few years, the company said in a blog post. “We deploy early and often,” Baldonado said during his OCP 2019 session (video below). “The FB teams came together to rethink the DC network, hardware and software. The components of the new DC are F16 and HGRID as the network topology, Minipak as the new modular switch, and FBOSS software which unifies them.”

This author was very impressed with Baldonado’s presentation- excellent content and flawless delivery of the information with insights and motivation for FBs DC design methodology and testing!

References:

https://code.fb.com/data-center-engineering/f16-minipack/

………………………………………………………………………………………………………………………………….

Other Hyperscale Cloud Providers move to 400GE in their DCs?

Large hyperscale cloud providers initially championed 400 Gigabit Ethernet because of their endless thirst for networking bandwidth. Like so many other technologies that start at the highest end with the most demanding customers, the technology will eventually find its way into regular enterprise data centers. However, we’ve not seen any public announcement that it’s been deployed yet, despite its potential and promise!

Some large changes in IT and OT are driving the need to consider 400 GbE infrastructure:

- Servers are more packed in than ever. Whether it is hyper-converged, blade, modular or even just dense rack servers, the density is increasing. And every server features dual 10 Gb network interface cards or even 25 Gb.

- Network storage is moving away from Fibre Channel and toward Ethernet, increasing the demand for high-bandwidth Ethernet capabilities.

- The increase in private cloud applications and virtual desktop infrastructure puts additional demands on networks as more compute is happening at the server level instead of at the distributed endpoints.

- IoT and massive data accumulation at the edge are increasing bandwidth requirements for the network.

400 GbE can be split via a multiplexer into smaller increments with the most popular options being 2 x 200 Gb, 4 x 100 Gb or 8 x 50 Gb. At the aggregation layer, these new higher-speed connections begin to increase in bandwidth per port, we will see a reduction in port density and more simplified cabling requirements.

Yet despite these advantages, none of the U.S. based hyperscalers have announced they have deployed 400GE within their DC networks as a backbone or to connect leaf-spine fabrics. We suspect they all are using 400G for Data Center Interconnect, but don’t know what optics are used or if it’s Ethernet or OTN framing and OAM.

…………………………………………………………………………………………………………………………………………………………………….

In February, Google said it plans to spend $13 billion in 2019 to expand its data center and office footprint in the U.S. The investments include expanding the company’s presence in 14 states. The dollar figure surpasses the $9 billion the company spent on such facilities in the U.S. last year.

In the blog post, CEO Sundar Pichai wrote that Google will build new data centers or expand existing facilities in Nebraska, Nevada, Ohio, Oklahoma, South Carolina, Tennessee, Texas, and Virginia. The company will establish or expand offices in California (the Westside Pavillion and the Spruce Goose Hangar), Chicago, Massachusetts, New York (the Google Hudson Square campus), Texas, Virginia, Washington, and Wisconsin. Pichai predicts the activity will create more than 10,000 new construction jobs in Nebraska, Nevada, Ohio, Texas, Oklahoma, South Carolina, and Virginia. The expansion plans will put Google facilities in 24 states, including data centers in 13 communities. Yet there is no mention of what data networking technology or speed the company will use in its expanded DCs.

I believe Google is still designing all their own IT hardware (compute servers, storage equipment, switch/routers, Data Center Interconnect gear other than the PHY layer transponders). They announced design of many AI processor chips that presumably go into their IT equipment which they use internally but don’t sell to anyone else. So they don’t appear to be using any OCP specified open source hardware. That’s in harmony with Amazon AWS, but in contrast to Microsoft Azure which actively participates in OCP with its open sourced SONIC now running on over 68 different hardware platforms.

It’s no secret that Google has built its own Internet infrastructure since 2004 from commodity components, resulting in nimble, software-defined data centers. The resulting hierarchical mesh design is standard across all its data centers. The hardware is dominated by Google-designed custom servers and Jupiter, the switch Google introduced in 2012. With its economies of scale, Google contracts directly with manufactures to get the best deals.Google’s servers and networking software run a hardened version of the Linux open source operating system. Individual programs have been written in-house.

IHS Markit: Service Provider Data Center Growth Accelerates + Gartner on DC Networking Market Drivers

Service Provider Data Center Growth Accelerates, by Cliff Grossner, Ph.D., IHS Markit

Service providers are investing in their data centers (DCs) to improve scalability, deploy applications rapidly, enable automation, and harden security, according to the Data Center Strategies and Leadership Global Service Provider Survey from IHS Markit. Respondents are considering taking advantage of new options from server vendors such as ARM-based servers and parallel compute co-processors, allowing them to better match servers to their workloads. The workloads most deployed by service provider respondents were IT applications (including financial and on-line transaction processing), followed by ERP and generic VMs on VMware ESXi and Microsoft Hyper-V. Speed and support for network protocol virtualization and SDN are top service provider DC network requirements.

“Traditional methods for network provisioning to provide users with a quality experience, such as statically assigned priorities (QoS) in the DC network, are no longer effective. The DC network must be able to recognize individual application traffic flows and rapidly adjust priority to match the dynamic nature of application traffic in a resource-constrained world. New requirements for applications delivered on demand, coupled with the introduction of virtualization and DC orchestration technology, has kicked off an unprecedented transformation that began on servers and is now reaching into the DC network and storage,” said Cliff Grossner Ph.D., senior research director and advisor for cloud and data center at IHS Markit , a world leader in critical information, analytics and solutions.

“Physical networks will always be needed in the DC to provide the foundation for the high-performance connectivity demanded of today’s applications. Cisco, Juniper, Huawei, Arista, and H3C were identified as the top five DC Ethernet switch vendors by service provider respondents ranking the top three vendors in each of eight selection criteria. These Ethernet switch providers have a long history as hardware vendors. When selecting a vendor, respondents are heavily weighing factors such as product reliability, service and support, pricing model, and security,” said Grossner.

More Service Provider Data Center Strategies Highlights:

· Respondents indicate they expect a 1.5x increase in the average number of physical servers in their DCs by 2019.

· Top DC investment drivers are scalability (a driver for 93% of respondents), rapid application deployment (87%), automation (73%), and security (73%).

· On average 90% of servers are expected to be running hypervisors or containers by 2019, up from 74% today.

· Top DC fabric features are high speed and support for network virtualization protocols (80% of respondents each), and SDN (73%).

· 100% of respondents intend to increase investment in SSD, 80% in software defined storage, and 67% in NAS.

· The workloads most deployed by respondents were generic IT applications (53% of respondents), followed by ERP and generic VMs (20%).

· Cisco and Juniper are tied for leadership with on average 58% of respondents placing them in the top three across eight categories. Huawei is #3 (38%), Arista is #4 (28%), and H3C is #5 (18%).

Data Center Network Research Synopsis:

The IHS Markit Data Center Networks Intelligence Service provides quarterly worldwide and regional market size, vendor market share, forecasts through 2022, analysis and trends for (1) data center Ethernet switches by category [purpose-built, bare metal, blade, and general purpose], port speed [1/10/25/40/50/100/200/400GE] and market segment [enterprise, telco and cloud service provider], (2) application delivery controllers by category [hardware-based appliance, virtual appliance], and (3) software-defined WAN (SD-WAN) [appliances and control and management software], (4) FC SAN switches by type [chassis, fixed], and (5) FC SAN HBAs. Vendors tracked include A10, ALE, Arista, Array Networks, Aryaka, Barracuda, Cisco, Citrix, CloudGenix, CradlePoint, Dell, F5, FatPipe, HPE, Huawei, Hughes, InfoVista, Juniper, KEMP, Nokia (Nuage), Radware, Riverbed, Silver Peak, Talari, TELoIP, VMware, ZTE and others.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

The following information was collected by Alan J Weissberger from various subscription only websites:

Gartner Group says the data center networking market is primarily driven by three factors:

- Refresh of existing data center networking equipment that is at its technological or support limits

- The expansion of capacity (i.e., physical buildouts) within existing locations

- The desire to increase agility and automation to an existing data center

Data center networking solutions are characterized by the following elements:

- Physical interfaces: Physical interfaces to plug-in devices are a very common component of products in this market. 10G is now the most common interface speed we see in enterprise data center proposals. However, we are also rapidly seeing the introduction of new Ethernet connectivity options at higher speeds (25 GbE, 50 GbE and 100 GbE). Interface performance is rarely an issue for new implementations, and speeds and feeds are less relevant as buying criteria for the majority of enterprise clients, when compared to automation and ease of operations (see “40G Is Dead — Embrace 100G in Your Data Center!” ).

- Physical topology and switches: The spine-and-leaf (folded Clos) topology is the most common physical network design, proposed by most vendors. It has replaced the historical three-tier design (access, aggregation, core). The reduction in physical switching tiers is better-suited to support the massive east-west traffic flows created by new application architectures (see “Building Data Center Networks in the Digital Business Era” and “Simplify Your Data Center Network to Improve Performance and Decrease Costs” ). Vendors deliver a variety of physical form factors for their switches, including fixed-form factor and modular or chassis-based switches. In addition, this includes software-based switches such as virtual switches that reside inside of physical virtualized servers.

- Switching/infrastructure management: Ethernet fabric provides management for a collection of switches as a single construct, and programmable fabrics include an API. Fabrics are commonly adopted as logical control planes for spine-and-leaf designs, replacing legacy protocols like Spanning Tree Protocol (STP) and enabling better utilization of all the available paths. Fabrics automate several tasks affiliated with managing a data center switching infrastructure, including autodiscovery of switches, autoconfiguration of switches, etc. (see “Innovation Insight for Ethernet Switching Fabric” ).

- Automation and orchestration: Automation and orchestration are increasingly important to buyers in this market, because enterprises want to improve speed to deliver data center network infrastructure to business, including on-demand capability. This includes support and integration with popular automation tools (such as Ansible, Chef and Puppet), integration with broader platforms like VMware vRA, inclusion of published/open APIs, as well as support for scripting tools like Python (see “Building Data Center Networks in the Digital Business Era” ).

- Network overlays: Network overlays create a logical topology abstracted from the underlying physical topology. We see overlay tunneling protocols like VXLAN used with virtual switches to provide Layer 2 connectivity on top of scalable Layer 3 spine-and-leaf designs, enabling support of multiple tenants and more granular network partitioning (microsegmentation), to increase security within the data center. Overlay products also typically provide an API to enable programmability and integration with orchestration platforms.

- Public cloud extension/hybrid cloud: An emerging capability of data center products is the ability to provide visibility, troubleshooting, configuration and management for workloads that exist in a public cloud provider’s infrastructure. In this case, vendors are not providing the underlying physical infrastructure within the cloud provider network, but provide capability to manage that infrastructure in a consistent manner with on-premises/collocated workloads.

You can see user reviews for Data Center Networking vendors here.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

In a new report, HTF Market Intelligence says that the Global Data Center Colocation Market will Have Huge Growth by 2025.

The key players are highly focusing innovation in production technologies to improve efficiency and shelf life. The best long-term growth opportunities for this sector can be captured by ensuring ongoing process improvements and financial flexibility to invest in the optimal strategies. Company profile section of players such as NTT Communications Corporation, Dupont Fabros Technology, Inc., Digital Realty Trust, Inc., Cyxtera Technologies, Inc., Cyrusone Inc., Level 3 Communications Inc., Equinix, Inc., Global Switch, AT&T, Inc., Coresite Realty Corporation, China Telecom Corporation Limited, Verizon Enterprise Solutions, Inc., Interxion Holding NV, Internap Corporation & KDDI Corporation includes its basic information like legal name, website, headquarters, its market position, historical background and top 5 closest competitors by Market capitalization / revenue along with contact information. Each player/ manufacturer revenue figures, growth rate and gross profit margin is provided in easy to understand tabular format for past 5 years and a separate section on recent development like mergers, acquisition or any new product/service launch etc.

Browse the Full Report at: https://www.htfmarketreport.com/reports/1125877-global-data-center-colocation-market-6

IHS Markit: CSPs accelerate high speed Ethernet adapter adoption; Mellanox doubles switch sales

by Vladimir Galabov, senior analyst, IHS Markit

Summary:

High speed Ethernet adapter ports (25GE to 100GE) grew 45% in 1Q18, tripling compared to 1Q17, with cloud service provider (CSP) adoption accelerating the industry transition. 25GE represented a third of adapter ports shipped to CSPs in 1Q18, doubling compared to 4Q17. Telcos follow CSPs in their transition to higher networking speeds and while they are ramping 25GE adapters, they are still using predominantly 10GE adapters, while enterprises continue to opt for 1GE, according to the Data Center Ethernet Adapter Equipment report from IHS Markit.

“We expect higher speeds (25GE+) to be most prevalent at CSPs out to 2022, driven by high traffic and bandwidth needs in large-scale data centers. By 2022 we expect all Ethernet adapter at CSP data centers to be 25GE and above. Tier 1 CSPs are currently opting for 100GE at ToR with 4x25GE breakout cables for server connectivity,” said Vladimir Galabov, senior analyst, IHS Markit. “Telcos will invest more in higher speeds, including 100GE out to 2022, driven by NFV and increased bandwidth requirements from HD video, social media, AR/VR, and expanded IoT use cases. By 2022 over two thirds of adapters shipped to telcos will be 25GE and above.”

CSP adoption of higher speeds drives data center Ethernet adapter capacity (measured in 1GE port equivalents) shipped to CSPs to hit 60% of total capacity by 2022 (up from 55% in 2017). Telco will reach 23% of adapter capacity shipped by 2022 (up from 15% in 2017) and enterprise will drop to 17% (down from 35% in 2017).

“Prices per 1GE ($/1GE) are lowest for CSPs as higher speed adapters result in better per gig economies. Large DC cloud environments with high compute utilization requirements continually tax their networking infrastructure, requiring CSPs to adopt high speeds at a fast rate,” Galabov said.

Additional data center Ethernet adapter equipment market highlights:

· Offload NIC revenue was up 6% QoQ and up 55% YoY, hitting $160M in 1Q18. Annual offload NIC revenue will grow at a 27% CAGR out to 2022.

· Programmable NIC revenue was down 5% QoQ and up 14% YoY, hitting $26M in 1Q18. Annual programmable NIC revenue will grow at a 58% CAGR out to 2022.

· Open compute Ethernet adapter form factor revenue was up 11% QoQ and up 56% YoY, hitting $54M in 1Q18. By 2022, 21% of all ports shipped will be open compute form factor.

· In 1Q18, Intel was #1 in revenue market share (34%), Mellanox was #2 (23%), and Broadcom was #3 (14%)

Data Center Compute Intelligence Service:

The quarterly IHS Markit “Data Center Compute Intelligence Service” provides analysis and trends for data center servers, including form factors, server profiles, market segments and servers by CPU type and co-processors. The report also includes information about Ethernet network adapters, including analysis by adapter speed, CPU offload, form factors, use cases and market segments. Other information includes analysis and trends of multi-tenant server software by type (e.g., server virtualization and container software), market segments and server attach rates. Vendors tracked in this Intelligence Service include Broadcom, Canonical, Cavium, Cisco, Cray, Dell EMC, Docker, HPE, IBM, Huawei, Inspur, Intel, Lenovo, Mellanox, Microsoft, Red Hat, Supermicro, SuSE, VMware, and White Box OEM (e.g., QCT and WiWynn).

………………………………………………………………………………………………………………………………………….

Mellanox Ethernet Switches for the Data Center:

In the Q1 2018 earnings call, Mellanox reported that its Ethernet switch product line revenue more than doubled year over year. Mellanox Spectrum Ethernet switches are getting strong traction in the data center market. The recent inclusion in the Gartner Magic Quadrant is yet another milestone. There are a few underlying market trends that is driving this strong adoption.

Network Disaggregation has gone mainstream

Mellanox Spectrum switches are based off its highly differentiated homegrown silicon technology. Mellanox disaggregates Ethernet switches by investing heavily in open source technology, software and partnerships. In fact, Mellanox is the only switch vendor that is part of the top-10 contributors to open source Linux. In addition to native Linux, Spectrum switches can run Cumulus Linux or Mellanox Onyx operating systems. Network disaggregation brings transparent pricing and provides customers a choice to build their infrastructure with the best silicon and best fit for purpose software that would meet their specific needs.

25/100GbE is the new 10/40GbE

25/100GbE infrastructure provides better RoI and the market is adopting these newer speeds at record pace. Mellanox Spectrum silicon outperforms other 25GbE switches in the market in terms of every standard switch attribute.

IHS Markit: On-premises Enterprise Data Center (DC) is alive and flourishing!

by Cliff Grossner, PhD, IHS Markit

Editor’s Note: Cliff and his IHS Markit team interviewed IT decision-makers in 151 North American organizations that operate data centers (DCs) and have at least 101 employees.

………………………………………………………………………………………………………………………………………………….

Summary:

While enterprise have been adopting cloud services for a number of years now, they are also continuing to make significant investments in their on-premises data center infrastructure. We are seeing a continuation of the enterprise DC growth phase signaled by last year’s respondents and confirmed by respondents to this study. Enterprises are transforming their on-premises DC to a cloud architecture, making the enterprise DC a first-class citizen as enterprises build their multi-clouds.

The on-premises DC is evolving with server diversity set to increase, the DC network moving to higher speeds, and increased software defined storage with solid state drive (SSD) adoption, according to the Data Center Strategies and Leadership North American Enterprise Survey

“Application architectures are evolving with the increased adoption of software containers and micro-services coupled with a Dev/Ops culture of rapid and frequent software builds. In addition, we see new technologies such as artificial intelligence (AI) and machine learning (ML) incorporated into applications. These applications consume network bandwidth in a very dynamic and unpredictable manner and make new demands on servers for increased parallel computation,” said Cliff Grossner Ph.D., senior research director and advisor for cloud and data center at IHS Markit (Nasdaq: INFO), a world leader in critical information, analytics and solutions.

“New software technologies are driving more diverse compute architectures. An example is the development of multi-tenant servers (VMs and software containers), which is requiring new features in CPU silicon to support these technologies. AI and ML have given rise to a market for specialized processors capable of high degrees of parallelism (such as GPGPUs and the Tensor Processing Unit from Google). We can only expect this trend to continue and new compute architectures emerging in response,” said Grossner.

More Data Center Strategies Highlights

· Respondents expect a greater than 2x increase in the average number of physical servers in their DCs by 2019.

· Top DC investment drivers are security and application performance (75% of respondents) and scalability (71%).

· 9% of servers are expected to be 1-socket by 2019, up from 3% now.

· 73% of servers are expected to be running hypervisors or containers by 2019, up from 70% now.

· Top DC fabric features are high speed (68% of respondents), automated VM movement (62%), and support for network virtualization protocols (62%).

· 53% of respondents intend to increase investment in software defined storage, 52% in NAS, and 42% in SSD.

· 30% of respondents indicated they are running general purpose IT applications, 22% are running productivity applications such as Microsoft Office, and 18% are running collaboration tools such as email, SharePoint, and unified communications in their data centers.

· Cisco, Dell, HPE, Juniper, and Huawei were identified as the top 5 DC Ethernet switch vendors by respondents ranking the top 3 vendors in each of 8 selection criteria.

Data Center Network Research Synopsis:

The IHS Markit Data Center Networks Intelligence Service provides quarterly worldwide and regional market size, vendor market share, forecasts through 2022, analysis and trends for (1) data center Ethernet switches by category [purpose-built, bare metal, blade, and general purpose], port speed [1/10/25/40/50/100/200/400GE] and market segment [enterprise, telco and cloud service provider], (2) application delivery controllers by category [hardware-based appliance, virtual appliance], and (3) software-defined WAN (SD-WAN) [appliances and control and management software], (4) FC SAN switches by type [chassis, fixed], and (5) FC SAN HBAs.

Vendors tracked include A10, ALE, Arista, Array Networks, Aryaka, Barracuda, Cisco, Citrix, CloudGenix, CradlePoint, Dell, F5, FatPipe, HPE, Huawei, Hughes, InfoVista, Juniper, KEMP, Nokia (Nuage), Radware, Riverbed, Silver Peak, Talari, TELoIP, VMware, ZTE and others.