Germany’s Contentious 5G Auction May Squeeze Telcos

Germany’s auction of 5G frequencies, now into its 10th week, has drawn 6 billion euros ($6.7 billion) in bids so far. That amount raised in a record 405 auction rounds for the 41 blocks on offer is more than experts thought companies would spend all together for all rounds. The duration of this auction has no precedent in Germany, with country’s 4G auction in 2010 lasting for 224 rounds.

German telco market leader Deutsche Telekom has complained that the regulator has forced up prices by offering too little spectrum. Deutsche Telekom leads in 13 of the blocks, with competitor Vodafone ahead in 12 and Telefonica Deutschland in eight, according to auction results published by the Federal Network Agency (BNetzA).

Source: Deutsche Telekom

……………………………………………………………………………………………………

New entrant 1&1 Drillisch, a ‘virtual’ mobile player controlled by United Internet, leads in eight blocks, as billionaire CEO Ralf Dommermuth pursues his dream of becoming Germany’s fourth operator.

Drillisch, and United Internet, have slashed their dividend payouts to conserve cash so that they can stay in the game.

As the telecom industry prepares for the costly rollout of new 5G networks, with little prospect of any immediate revenue growth from new 5G services, the spectrum bill is a further squeeze. And while bidding has recently slowed, the contest is not yet over.

Industry leaders say that inflated auction costs would undermine their ability to invest the billions needed to build 5G networks – as happened in a pricey spectrum auction in Italy last year.

………………………………………………………………………………………………………….

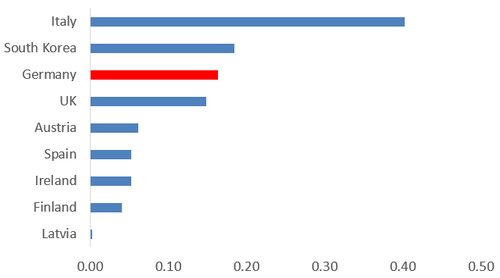

German telcos appear to be grasping expensively for a small amount of spectrum in the 3.6GHz range, the “mid-band” that looks optimal for the delivery of 5G services. The fight would have been less damaging and drawn-out had German regulators put more of these airwaves up for sale, according to Timotheus Höttges, the head of Deutsche Telekom. Instead, they chose to hold back 100MHz for industrial and local settings, such as German factories, leaving 300MHz to the telcos. Supply constraints have driven up the bids.

Competition has been especially fierce because of 1&1 Drillisch. Having previously bought network capacity from Telefónica, and functioned as a mobile virtual network operator, the broadband company is now determined to build a fourth mobile network using spectrum it picks up in the auction. After round 406, 1&1 Drillisch accounted for more than €1.1 billion ($1.2 billion) of the amount bid. Since the auction began, its share price has lost a quarter of its value as investors worry about the consequences of spending so much.

Outside Italy, Germany now values the mid-band at a higher level than any other European country that has licensed 5G spectrum. Were the auction to finish now, German telcos would pay about $0.16 per megahertz per head of population (per MHz pop, a common way of valuing spectrum) for 3.6GHz licenses. That edges Germany ahead of the UK, which raised about $0.15 (at current exchange rates) per MHz pop during a 3.4GHz auction in 2018. Spanish companies last year paid just €0.05 during a 3.6-3.8GHz auction (although this calculation does not consider usage fees they are also charged). Finland’s mid-band sale in October raised as little as $0.04.

However, the German auction is nowhere near Italy on this measure, and it will not even get close. After slapping just 200MHz of mid-band spectrum on the table, and slicing it like a badly cut pizza into uneven segments, Italian regulators made off with around $0.40 per MHz pop. The auction “winners” are now choking on their rewards. Telecom Italia and Vodafone, which landed the biggest mid-band concessions, are busy slashing jobs and pooling assets to ensure 5G rollout is affordable.

German telecom regulator Jochen Homann, the president of the Bundesnetzagentur, is said to have argued that bidders knew the conditions of the auction before it started and will have prepared accordingly. Yet analysts thought a spectrum sale would raise between €3 billion ($3.4 billion) and €5 billion ($5.6 billion), an upper limit the auction has now breached.

Light Reading says German authorities may still have cause to worry. While the country’s operators are in healthier shape than Italy’s, a large spectrum bill risks slowing down the pace of 5G rollout and jeopardizing national ambitions. With its large manufacturing sector, Germany is hopeful that 5G will support Industrie 4.0, a government initiative to bring communications technologies into factories and the workplace. The productivity boost this promises may be critical if Germany is to remain competitive with the US, China and other fast-developing Asian countries.

In the U.S., the FCC auctioned off 24GHz high-band spectrum in March 2019, with the announcement of more spectrum sales expected in the coming months. The U.S. has yet to allocate any mid-band spectrum.

References:

…………………………………………………………………………………………………………….

Related: World leaders in 5G:

VSG: 2018 U.S. Carrier Managed SD-WAN LEADERBOARD

Vertical Systems Group defines a managed SD-WAN service as a carrier-grade network offering for enterprise and business customers, which is managed by a network operator, and delivered over a software-defined network (SDN) service architecture that has separate control (overlay) and data (underlay) planes.

![]()

SD-WAN is one of three managed VPN segments that Vertical Systems tracks, along with MPLS and site-to-site VPNs. The top-five carrier managed SD-WAN companies are also leading providers of dedicated IP VPN services, which included landline and satellite connectivity.

VSG Research Highlights:

SD-WAN is one of the three Managed VPN segments that Vertical tracks, along with MPLS and Site-to-Site VPNs. Service migration analysis shows that the majority of Carrier Managed SD-WAN service installations to date are hybrid configurations that include partial conversions of existing Site-to-Site and MPLS networks.

- The top five Carrier Managed SD-WAN companies are also the leading providers of Dedicated IP VPN services, including landline and satellite connectivity.

- A number of SDN-based technologies are utilized to deliver Carrier Managed SD-WAN services. The fourteen LEADERBOARD and Challenge Tier providers use products from the following companies (in alphabetical order): Cisco/Viptela, Silver Peak, Versa, and VMware/VeloCloud, or employ their own internally developed technologies. Several SD-WAN service providers offer multiple solutions.

The 14 leaderboard and challenge tier providers used SD-WAN technologies from Cisco/Viptela, Silver Peak, Versa Networks and VMware/VeloCoud or deploy their own internally developed technologies. Several SD-WAN service providers, such as AT&T, Verizon and CenturyLink, have multiple SD-WAN offerings.

https://www.verticalsystems.com/2019/05/21/2018-sd-wan-us-leaderboard/

New Report: 5G deployments to drive new business opportunities and revenue growth

Mobile service providers anticipate significant new revenue opportunities from the coming deployment of high-speed 5G networks and a host of new IoT-driven use cases.

According to a new survey conducted by the Business Performance Innovation (BPI) Network, in partnership with A10 networks, cellcos also believe much-improved security will be essential to realizing that potential.

The new study report, “Securing the Future of a Smart World,” demonstrates that carriers are moving decisively toward 5G commercialization and that security is a top concern. You can download the free report here. A few highlights:

- 67% will deploy their first commercial 5G networks within 18 months and another 20% within two years

- 94% expect growth in network traffic, connected devices and mission- critical IoT use cases to significantly increase security and reliability concerns for 5G networks

- 79% say 5G is a consideration in current security investments

“Mobile carriers anticipate significant revenue opportunities and exciting new use cases as they move forward with their 5G deployments. However, the industry also recognizes that 5G will dramatically raise the stakes for ensuring the security and reliability of these networks,” said Gunter Reiss, vice president of A10 Networks.

“New mission-critical applications like autonomous vehicles, smart cities, and remote patient monitoring will make network reliability vital to the safety and security of people and businesses. Meanwhile, dramatic increases in traffic rates and connected devices will significantly expand the attack surface and scale for cyber criminals.”

Operators still have a significant amount of work ahead to fortify their networks for the coming of 5G. For example, while more than 80% of mobile operator respondents say they will need to upgrade Gi/SGi firewalls at the core of their networks, only 11% have completed the implementation of new Gi/SGi firewalls.

Realizing the potential of full-scale 5G networks requires major investments by carriers—and payback on that spend is a crucial issue for the telecommunications industry. Operators see significant opportunities to increase revenues and innovate new business models.

The top-three benefits derived from 5G

- 67% – Overall growth in the mobile market

- 59% – Better customer service and satisfaction

- 43% – The creation of new 5G-enabled business models

Top drivers for 5G

- 61% – Smart cities

- 48% – Industrial automation and smart manufacturing

- 39% – High-speed connectivity

- 35% – Connected vehicles

- 37% – Fixed wireless

Assessing 5G security needs

Chief among security concerns are core network security and DDoS protection.

- 63% – Advanced DDoS protection the most important security capability needed for 5G networks.

- 98% of respondents said core network security was either very important (72%) or important (26%) in 5G build-outs.

- 79% have or will upgrade their Gi/SGi firewalls

- 73% have or will upgrade their GTP firewall

“Operators overwhelmingly understand the importance of upgrading security in a more connected and smart world,” continued Reiss.

“Now it’s time to take decisive action. Carriers need to move ahead aggressively with their plans to upgrade legacy DDoS protection and consolidate security services at the core and edge of their networks to address the growing concerns. A10 Networks 5G security solutions including Gi/SGi firewall, GTP firewall and AI-based DDoS protection enable operators to secure and scale their networks now and protect against the massive cyber threat coming with 5G.”

References:

https://www.mysecuritymarketplace.com/product/securing-the-future-of-a-smart-world/

2019 IoT World: Market Research from Ovum & Heavy Reading; LPWAN Market to be >$65 billion by 2025

I. IoT World May 14, 2019 presentation by Alexandra Rehak, Practice Leader IoT, Ovum and Steve Bell, Sr. Analyst, Heavy Reading.

Edited by Alan J Weissberger

Ovum Forecasts:

- IoT devices will grow to 21.5bn by 2023, while revenue will nearly double to $860bn.

- Key trends driving IoT evolution in 2019: enabling technologies, new business models, (industry) verticalization, big data & analytics, new tools, e.g. AI/ML.

- Drivers for IoT deployment still focus on efficiency and customer

experience, but many enterprises are looking for new revenue. Top 4 IoT drivers are to improve: operation efficiency, customer engagement & experience, strategic decision making based on actionable insights, new revenue streams from value added products/services. - The biggest enterprise IoT challenge is data – how to secure it, how

to derive analytics value from it, how to integrate it. Top 3 barriers to enterprise IoT deployment: data security & privacy (has been top concern for last 10+ years), data analytics skills/data scientists, difficult to integrate with existing IT (and likely OT too), complexity of technical implementation (and systems integration).

Enabling Technologies:

1. LPWAN will be a key enabler for cheaper, massive scale IoT

connectivity – and 2019 will be the year it finally takes off (Alan has heard that for several years now! However, NB-IoT and LoRa are growing very quickly in 2019.)

• <$1 per month connectivity

• <$10 modules

• Low bandwidth, long battery life, extended coverage characteristics

• Use cases: smart cities, consumer IoT, asset monitoring, environmental monitoring

• NB-IoT, LTE-M, LoRa, Sigfox are the big four LP WANs

2. 5G enables enhanced IoT digital capabilities:

▪ High bandwidth services – eg UHD video

▪ Critical applications, which require low latency – e.g., autonomous driving, industrial applications (3GPP Release 16 and IMT 2020 approved standard)

▪ High bandwidth, low latency services – e.g., augmented reality

▪ Information intensive routines, which require low latency performance– eg smart advertising, True AI (is what we have today fake AI?)

▪ Services that can – but don’t readily – work over 4G, e.g., mobile video conferencing

3. Edge and the IoT opportunity:

Virtualized services (including gateways and vCPE), FOG nodes, life cycle management, linking silos (systems and data), many different applications, data analytics, AI/ML/DL, threat intelligence, device management services, security credential management.

4. Blockchain is still early-stage as an IoT enabler, but promising use

cases are emerging

- Authentication of devices joining IoT network

- Supply chain management and verification

- Smart grid microcontracts

- Autonomous vehicles

Blockchain will not suit all IoT security and contract requirements. That’s because it’s: Complex, heavy processing load, not yet fully commercialized, private blockchain space is fragmented, need for supporting regulatory/legal frameworks Autonomous vehicles.

………………………………………………………………………………………………………….

Industrial IoT (IIoT):

It’s becoming a core focus for the market – and an important testbed for 5G. Requires ultra reliable and very low latency.

IIoT is moving beyond efficiency gains:

• IIoT will grow in importance in 2019

• Drivers: efficiency and margins, competitive positioning, ‘job lots of one’

• Challenges: IT/OT integration, security, traditional business models

• Applications: simple asset tracking/monitoring to complex propositions (predictive maintenance, digital twin, robotics, autonomy)

• IoT, 5G, and AI form virtuous circle for industrial sector and factory

campuses

• Private LTE as another enabler (Steve Bell of Heavy Reading was very optimistic on this during the Thursday morning, May 17th round table discussion on 5G and LTE for IoT). So is this author!

……………………………………………………………………………………………………..

IoT value chain: evolution from ‘platform providers’ to ‘end-to-end

solution providers,’ simplifying the buying process. An end-to-end solution requires: sensors/devices/hardware, connectivity, platform (connectivity and device control/management), applications, analytics, integration.

Value chain evolution is also driving IoT business model innovation, for both enterprises and providers. For connectivity, this includes: flat rate IoT connectivity pricing (e.g. $5 per year), bundled IoT device connectivity, alternative IoT connectivity providers (e.g. Sigfox, Zigbee mesh, BT mesh, etc), private LTE (licensed frequencies so not contention for bandwidth as with WiFi).

…………………………………………………………………………………………………….

Summary and Recommendations:

- Enabling IoT technologies: 5G, LPWAN, edge, blockchain – developing

quickly – but shouldn’t be seen in isolation. - IoT data usage & security: Focus of customer concern – stronger support,

simpler tools needed to deliver value through analytics, eventually AI. - Vertical strategies: Industries face significant disruption – understand

how IoT will help your customer to transform and address these shifts. - New IoT business models: increasingly sophisticated – end customers

very interested, but need help to understand them, manage risk.

……………………………………………………………………………………………………………

II. LPWAN Market Forecast from Global Market Insights, Inc.

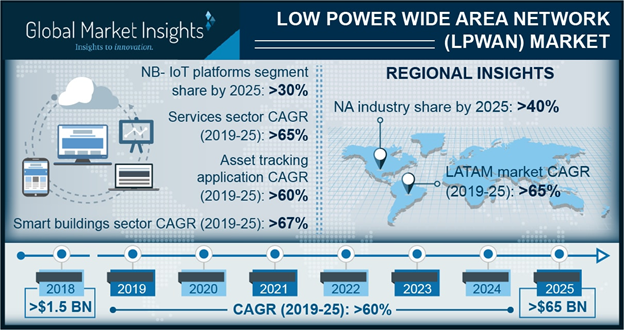

The LPWAN market is set to grow from its current market value of more than $1.5 billion (€1.3 billion) to over $65 billion (€58.2 billion) by 2025, according to a new research report by Global Market Insights, Inc.

Low power wide area network market growth is driven by the growing deployment of LPWA technologies, including LoRa, NB-IoT, and LTE-M, offering a wide range of connectivity options to enterprises. These technologies provide broader network coverage and better battery life to connect various devices. LPWAN networks are becoming very popular among enterprises to support various IoT use cases for verticals including healthcare, manufacturing, agriculture, logistics, and utilities.

For instance, the rising penetration of Industrial IoT (IIoT) in the manufacturing industry has increased the demand for LPWA technologies, particularly NB-IoT and LTE-M, to enable reliable machine-to-machine communication. Industrial IoT connections are expected to increase nearly five times between 2016 and 2025, from 2.4 billion to around 14 billion connections.

By deploying LPWAN connections, manufacturing companies can increase their operational efficiencies to drive high productivity. Another factor fuelling the LPWAN market growth is increasing investments by companies in LPWAN technologies. For instance, in June 2017, Cisco contributed to a US$ 75 million Series D funding round for Actility, a LPWAN startup. Cisco’s investments in Actility enabled it to accelerate the development of IoT solutions.

The LPWAN platforms held a major market share of over 70% in 2018 owing to the deployment of various platforms, including NB-IoT, LoRaWAN, Sigfox, and LTE-M. Massive IoT deployments in various industry verticals, including utilities, manufacturing, transportation, and healthcare, has increased the demand for LPWAN platforms to support connected devices requiring low power consumption, long range, and low costs. Among all the platforms, LoRaWAN platforms held the highest market share of over 50% in 2018 as they use unlicensed spectrum and are best suited for applications that generate low traffic and require low-cost sensors.

In the services segment, the managed services segment is expected to hold low power wide area network market share of around over 30% in 2025. Managed services enable organisations to accelerate the deployment of LPWAN and reduce the time & expenses spent on training the IT staff. The on-premise deployment model is expected to grow at a CAGR of over 50% over the projected timeline. The demand for this deployment model will increase as it enables organisations to build & manage their own LPWAN for IoT-based applications.

References:

Ovum’s latest video on IoT with Alexandra Rehak: https://ovum.informa.com/products-and-services/research-services/internet-of-things

https://www.gminsights.com/industry-analysis/low-power-wide-area-network-lpwan-market

Verizon Shows Benefits of “5G” for First Responders; 5G Fast Facts

Verizon gave first responders a look at 5G networks in action this week. Firefighters and police saw demonstrations of technology at a Verizon, New York city event. “You’re able to speed up,” Former New York Police Commissioner Bill Bratton said in a speech to first responders on Monday.

Augmented reality could give firefighters greater visibility and smart lighting on streets could help police more quickly track gunshots, among other potential advances.

5G Fast Facts:

- Verizon has launched its mobile 5G network in parts of Chicago and Minneapolis, and you can see the first Verizon 5G speed test results. The first compatible phone is the Moto Z3, which isn’t 5G-capable out of the box but can be retrofitted with 5G connectivity with a 5G Moto Mod you can order now.

- Samsung just released the $1,299 Galaxy S10 5Gflagship on Verizon’s 5G network. The device sports a 6.7-inch display and six camera lenses, including two with depth-sensing time-of-flight sensors for improved augmented reality experiences. We tested the S10 5G on Verizon in Chicago to take advantage of 5G speeds, and while the phone occasionally cleared 1 Gbps, our average downloads were 700 Mbps. However, the phone is markedly faster than an LTE Galaxy S10.

- LG is releasing a 5G phone of its own, the LG V50 ThinQ 5G, and it will debut on Sprint’s network for $1,152 on May 31. Sprint is currently taking preorders, but has not yet announced when its network will go live. Sprint is also selling a $600 5G hub from HTC, which will give LTE devices in your home 5G speeds when in Wi-Fi range of the hub.

- Sprint has announced a May launch for its 5G network in a handful of cities. AT&T is taking heat took heat for its 5G Evolution logo, which looks a lot like 5G, with speeds closer to 4G. T-Mobile is eyeing the second half of the year for its 5G push.

- Apple will reportedly wait until 2020 to release a 5G smartphone. The company participates in ITU-R WP 5D which is standardizing IMT 2020 Radio Interface Technologies (RITs).

- Qualcomm has said that 20 operators around the world will roll out 5G in 2019, including all major US carriers. Twenty device makers have committed to using Qualcomm’s 5G components in their devices.

High Altitude Platform System (HAPS): U.S. Proposal for frequency range 24.25-25.25 GHz

The following is a U.S. contribution to the World Radio-communication Conference (WRC-19) Sharm el-Sheikh, Egypt, 28 Oct – 22 Nov 2019:

ITU Radio Regulations defines a high-altitude platform station (HAPS) as “a station on an object at an altitude of 20 to 50 km and at a specified, nominal, fixed point relative to the Earth.”

Agenda item 1.14 was adopted by WRC-15 to consider, in accordance with Resolution 160 (WRC-15), regulatory actions that can facilitate deployment of HAPS for broadband applications. Resolution 160 resolves to invite the ITU-R to study additional spectrum needs of HAPS, examining the suitability of existing HAPS designations, and conducting sharing and compatibility studies for additional designations in existing fixed service allocations in the 38‑39.5 GHz band, on a global basis, and in bands already allocated to the fixed service in the 21.4‑22 GHz and 24.25-27.5 GHz bands in Region 2 exclusively.

Advances in aeronautics and transmission technologies have significantly improved the capabilities of HAPS to provide effective connectivity solutions and meet the growing demand for high capacity broadband networks, particularly in currently underserved areas. Recently conducted full-scale test flights have shown that solar-powered platforms in the upper-atmosphere can now be used to carry payloads that offer reliable and cost-effective connectivity, and a growing number of applications for the new generation of HAPS are being developed. The technology appears particularly well suited to complementing terrestrial networks by providing backhaul. A number of advantages of the new generation of HAPS are foreseen:

- Reach: HAPS platforms may operate at around 20 km above ground, which reduces their vulnerability to weather conditions that may affect service, provides large coverage areas and helps mitigate interference caused by physical obstacles.

- Geographical reach: HAPS that use the architecture of solar platforms can also provide connectivity where it is impossible to deploy terrestrial infrastructure: remote sites on land or sea.

- Wide-area coverage: Depending on the operational scenario, a single platform is capable of providing footprints on the order of up to 100 km in diameter, and recent technological advances in the development of optical inter-HAPS links now support the deployment of multiple linked HAPS, in fleets that can provide greater coverage within a country as needed.

- Low cost and environmental aspects: The cost of operating stratospheric platforms is projected to be lower than other connectivity solutions depending on geographical area, while mass production of the aircraft will significantly lower upfront capital expenditure for deployment. HAPS can run exclusively on solar power for long periods, connecting people with almost no environmental impact.

- Rapid deployment and flexibility: It may be possible to deploy HAPS services without long lead times and it is relatively simple to return solar platforms to the ground for maintenance or payload reconfiguration.

The ITU-R conducted sharing and compatibility studies to assess coexistence between HAPS and incumbent and proposed systems and services (including issues of overlap with WRC-19 agenda items 1.6 and 1.13). Associated regulatory provisions are proposed below based on the results of sharing studies.

Proposal

For the frequency range 24.25-25.25 GHz in Region 2, the USA proposes “no change” (NOC) to the Radio Regulations, as Resolution 160 (WRC-15) calls for identifications for HAPS in frequency bands already allocated to the fixed service on a primary basis. In Region 2, the bands in this frequency range are not already allocated to the fixed service. No studies have been conducted in the ITU-R to assess the sharing and compatibility of adding a new fixed service allocation to the 24.25-25.25 GHz band in Region 2. As a frequency band cannot be designated for fixed service HAPS use without a fixed service allocation, no change is proposed under agenda item 1.14. This proposal is aligned with Method 4A of the CPM Report to WRC-19.

…………………………………………………………………………………………………………………………………………………………………………………………………….

Table of Frequency Allocations

| Allocation to services | ||

| Region 1 | Region 2 | Region 3 |

| 24.25-24.45

FIXED |

24.25-24.45

RADIONAVIGATION |

24.25-24.45

RADIONAVIGATION FIXED MOBILE |

| 24.45-24.65

FIXED INTER-SATELLITE |

24.45-24.65

INTER-SATELLITE RADIONAVIGATION |

24.45-24.65

FIXED INTER-SATELLITE MOBILE RADIONAVIGATION |

| 5.533 | 5.533 | |

| 24.65-24.75

FIXED FIXED-SATELLITE INTER-SATELLITE |

24.65-24.75

INTER-SATELLITE RADIOLOCATION- |

24.65-24.75

FIXED FIXED-SATELLITE INTER-SATELLITE MOBILE |

| 5.533 | ||

Reasons: Resolution 160 (WRC-15) calls for identifications for HAPS in frequency bands already allocated to the fixed service on a primary basis. In Region 2, for the frequency range 24.25-25.25 GHz, the bands in this frequency range are not allocated to the fixed service.

| Allocation to services | ||

| Region 1 | Region 2 | Region 3 |

| 24.75-25.25

FIXED FIXED-SATELLITE |

24.75-25.25

FIXED-SATELLITE |

24.75-25.25

FIXED FIXED-SATELLITE MOBILE |

Reasons: Resolution 160 (WRC-15) calls for identifications for HAPS in frequency bands already allocated to the fixed service on a primary basis. In Region 2, for the frequency range 24.25-25.25 GHz, the bands in this frequency range are not allocated to the fixed service.

Tech Mahindra: India Needs to Begin 5G Spectrum Auction Now!

Manish Vyas, President of Communications Business and Chief Executive Officer of Network Services, of Tech Mahindra said the India Department of Telecom needs to commence the auction of 5G spectrum now. He noted that regulators in some countries have already formulated policies and initiated spectrum auctions for the 5G roll out in their respective nations.

Vyas said 4G is yet to touch all parts of India and that needs to happens on a massive scale. Yet there are some “definite green-shoots” of 5G trials.

More than technology, the bigger impediment could be the India regulatory body’s policy on 5G spectrum. The experimental license by DoT will need modifications, and till that happens, the sector is in for a “waiting game” he said.

“US, Australia, Italy, Switzerland, Saudi Arabia and more (have started 5G spectrum auctions). Spectrum is the life blood of any wireless network. For 5G, globally regulators have been licensing mid-band (3.5GHz) and in some countries mmWave (millimeter Wave) spectrum bands as well.

For 5G to be rolled out in India, the first necessary step is for the regulator to auction the 5G spectrum. Everything else will be gated on spectrum,” he wrote in an email to the Economic Times of India.

Vodafone Idea recently said the auction of 5G spectrum should not be held before 2020 as the industry needs time to develop India-specific use cases for the next-generation technology.

A DoT official in December last year said the government expects to complete processes for 5G spectrum auction by August, 2019.

…………………………………………………………………………………………………..

Tech Mahindra established a strategic partnership with Intel on a wide range of topics spanning across Virtualization of RAN (radio access network) , Cloud native 5G Core and on Edge Computing, Vyas said.

“Intel brings best in class technology for 5G infrastructure and will form the foundation of 5G networks.

We are collaborating with Intel to maximise the benefits of their technology for 5G networks and we are also working on developing 5G use cases for specific industry verticals in the CoE,” he said.

A panel set up to recommend the scope of 5G trials in the country has submitted its report to the Department of Telecom (DoT), a source said.

The DoT-constituted committee chaired by IIT Kanpur Director Abhay Karandikar was tasked to give recommendations on the scope of trials, as well as size, quantum, pricing and other aspects for offering experimental/trial spectrum for 5G and other trials.

A DoT source privy to the development said that the report was submitted recently and is currently being examined, but did not divulge details.

Some industry representatives had earlier informed the committee, during the past deliberations, that the various stages involved in the process of experimentation and trials such as import and release of equipment, logistic clearance, installation and commission of equipment, network integration, interoperability checking, and testing of applications require longer duration and that the existing validity of three months is very short and needs to be increased.

The National Digital Communications Policy 2018 outlines a mission to ‘propel India’ by enabling next generation technologies and services through investments, innovation and IPR generation.

In this regard, it underlines the need to harness the power of emerging digital technologies, including 5G, Artificial Intelligence, Internet of Things, Cloud and Big Data to enable provision of future-ready products and services.

Berg Insight: China driving global cellular IoT adoption via NB-IoT; 5G-IoT coming in late 2020

A new report from the IoT analyst firm Berg Insight estimates that the global number of cellular IoT (e.g. NB-IoT, LTE-M, LTE, 2G, 3G, etc) subscribers increased by 70 percent during 2018 to reach 1.2 billion. IoT growth was driven by “exceptional adoption” in China.

The market research firm forecasts that there will be 9 billion IoT devices connected to cellular networks worldwide by 2023.

China, which accounted for 63% of the global installed base in 2018, is expected to continue to be the key driver for IoT adoption, as the Chinese government is actively driving adoption as a tool for achieving domestic and economic policy goals.

“China is deploying cellular IoT technology at a monumental scale”, said Tobias Ryberg, principal analyst and author of the report.

According to data from the Chinese mobile operators, the installed base in the country increased by 124% year-on-year to reach 767 million at the end of 2018.

China has overtaken Europe and North America in penetration rate with 54.7 IoT connections per 100 inhabitants, Ryberg said.

He said the role of the government is the main explanation for why China is ahead of the rest of the world in the adoption of IoT.

“The most distinctive characteristic of the Chinese IoT market is however the way that the government is systematically using new technology to implement its vision for urban life in the 21st century,” Ryberg said.

“At the same time the private sector also implements IoT technology to improve efficiency and drive innovation.”

China has witnessed widespread adoption of connected cars, fleet management, smart metering, asset monitoring and as well as new consumer services like bike sharing.

The report also analyses the IoT business KPIs (Key Performance Indicators) released by mobile operators in different parts of the world and found significant regional differences.

While China has the world’s highest IoT penetration rate, Europe seems is doing better job in terms of monetizing the IoT business.

According to the report, the monthly ARPU for cellular IoT connectivity services in China was only €0.22 ($0.25), compared to € 0.70 in Europe.

Global revenues from cellular IoT connectivity services increased by 19% in 2018 to reach €6.7 billion. The ten largest players had a combined revenue share of around 80%.

………………………………………………………………………………………………………………….

Editor’s Note: The most popular cellular IoT network in China is NB-IoT. China Telecom Offers NB–IoT Nationwide. ChinaTelecom has built the world’s largest NB–IoT network so far by upgrading 310,000 base stations acrossChina to support NB–IoT. … It is using the 800MHz spectrum band, which is being refarmed for 4G in China and enables good in-building penetration and very wide coverage.

A GSMA case study illustrates how China Mobile, China Telecom and China Unicom enable consumers and businesses to benefit from better services using NB-IoT, while opening up new business models for mobile operators and their partners.

Supporting extensive coverage and low power consumption, NB-IoT is making it feasible to securely remotely monitor and control very large volumes of everyday devices, appliance, machines and vehicles. Both consumers and businesses in China are now benefiting from greater convenience, better reliability, and improved safety and security.

Above image courtesy of GSMA

……………………………………………………………………………………………………………………………….

In a separate report, Berg Insight says 5G will reach the IoT market in late 2020.

The first 5G cellular IoT modules will become available to developers this year, enabling early adopters to create the first IoT devices based on the standard. Based on the experience of previous introductions of new standards, 5G will however not be an instant hit. By 2023, Berg Insight forecasts that 5G will account for just under 3 percent of the total installed base of cellular IoT devices.

“5G still has some way to go before it can become a mainstream technology for cellular IoT”, says Tobias Ryberg, Principal Analyst and author of the report.

“Just like 4G when it was first introduced, the initial version of 5G is mostly about improving network performance and data capacity. This is only relevant for a smaller subset of high-bandwidth cellular IoT applications like connected cars, security cameras and industrial routers. The real commercial breakthrough will not happen until the massive machine type communication (mMTC) use case has been implemented in the standard.”

mMTC is intended as an evolution of the LTE-M/NB-IoT enhancements to the 4G standard. Since NB-IoT has only just started to appear in commercial products, there is no immediate demand for a successor. Over time, fifth generation mobile networks will however become necessary to cope with the expected exponential growth of IoT connections and data traffic. The report identifies homeland security as an area where 5G cellular IoT can have a major impact already in the early 2020s.

“5G enables the deployment of high-density networks of AI-supported security cameras to monitor anything form security-classified facilities to national borders or entire cities”, says Mr. Ryberg.

“How this technology is used and by whom is likely to become one of the most controversial issues in the next decade.”

……………………………………………………………………………………………………………..

References:

http://www.berginsight.com/News.aspx?m_m=6&s_m=1

https://www.gsma.com/iot/nbiot-iot-commercial-case-study-china/

https://www.telecomasia.net/content/berg-insight-china-driving-global-cellular-iot-adoption

WDM-PON to Enable 5G+FTTH Converged Gigaband Access

SOURCE: ZTE

Introduction:

5G networks will be distinctly different then 4G-LTE networks, even though all so called “5G” pre-standard deployments use 3GPP Rel 15 5G-NR NSA (Non Stand Alone) for the data plane, with a heavy LTE anchor for: signaling, network management and mobile packet core (EVC). ITU-R will specify the radio related standards for 5G, while ITU-T will standardize the non radio aspects, as reported NUMEROUS times on this techblog website.

Several market research firms forecast that 5G base stations installed in China will be two to three times as many as 4G- LTE base stations. GSMA forecasts that from launch in 2020, Chinese 5G connections will scale rapidly over time, to reach 428 million by 2025. Beyond this date, further growth will be determined by incremental network rollout (and the ability of operators to earn ROI), and the price point at which 5G devices are available.

……………………………………………………………………………………………………………

Definitions: C-RAN, DUs, and AAUs:

The Centralized Radio Access Network (C-RAN) mode where the Distributed Units (DUs) for many Active Antenna Units (AAUs) are placed at a centralized location significantly increases the fronthaul distance between DUs and AAUs. If all DU-AAU connections are through fiber, the amount of fiber required will rise by 10-fold. That entails heavy civil works and enormous investments.

25Gbps WDM-PON is Ideal for 5G Fronthaul:

WDM-PON is a passive optical networking technology that can be used to address the fiber deployment challenges. A WDM-PON design can be used to separate optical-network units (ONUs) into several virtual point-to-point connections over the same physical infrastructure, a feature that enables efficient use of fiber compared to point-to-point direct fiber connection and offers lower latency than TDM-based technologies. A notable benefit of this technology is high bandwidth, low latency, and fiber savings. 5G fronthaul based on 25Gbps WDM-PON technology has the following technical advantages:

- Support for CPRI and eCPRI standards as well as 4G/5G hybrid networking.

- 25Gbps high bandwidth per wavelength, which can smoothly evolve to 50Gbps in the future.

- Up to 20 pairs of wavelengths on a single trunk fiber.

- Colorless ONU technology allows flexible wavelength allocation and wavelength routing.

- In the future, a colorless Small Form-Factor Pluggable (SFP) ONU can be directly inserted into the AAU for easy installation.

- The Arrayed Waveguide Grating (AWG) incurs a power loss of about 5.5 dBm, which is lower than that of the optical splitter.

5G+FTTH Converged Gigaband Access Solution

WDM-PON is a key innovation that enables 5G+FTTH converged gigaband access. Compared with direct fiber connections between DU and AAU, the WDM-PON based fronthaul mode saves trunk fibers by more than 90 percent (shown as Figure 1). Another advantage of WDM- PON is that wavelengths can be flexibly allocated and resources can be remotely, centrally managed.

WDM PON enriches and perfects 5G fronthaul technology, giving operators more options by allowing for 5G+FTTH converged gigaband access in dense urban areas.

Based on the above principles, ZTE and China Telecom jointly launched the 5G+FTTH Converged Gigaband Access solution. The solution has unique advantages in trunk fiber, equipment space and power savings. Specifically, it:

- Cuts 95 percent trunk fiber by allowing up to 20 AAUs to share the same trunk fiber.

- Saves 10 percent power and shrinks space through OLT reuse.

- Reduces overall investments by 50 percent.

In addition to the high-density WDM-PON cards, the OLT also innovatively provides TDM-like channels to ensure a processing latency of less than 7µs in the OLT. If the distance between OLT and ONU is 5 kilometers, a transmission latency of 25µs will ensue over the fiber. Consequently, the total end-to-end latency is less than 32μs, which is 68 percent lower than the 5G URLLC requirements. The TDM-like channel handles traffic sent from 5G AAUs in real time without the queuing, buffering, forwarding, routing and searching processes. The resulting low-latency forwarding meets the stringent latency requirements of 5G fronthaul for URLLC applications.

Industry’s First WDM-PON for 5G Fronthaul Validation:

In December 2018, ZTE and the Technology Innovation Department and Optical Access Research Department of China Telecom jointly completed the industry’s first validation of Nx25Gbps WDM-PON for 5G fronthaul on the live network of China Telecom Suzhou Branch. The validation demonstrated that 25Gbps WDM-PON could carry 5G fronthaul services stably and transparently, with the data rate and end-to-end latency equal to those in a point-to-point direct fiber connection.

Achievements in WDM-PON Standards and Technologies:

ZTE and China Telecom collaborate to actively participate in the standardization of WDM-PON. The collaboration has produced numerous achievements including:

- Editor of “ITU-T G.Sup66 : 5G wireless fronthaul requirements in a passive optical network context” in October 2018.

- Submitted five proposals to the ITU-T, applied for 23 patents and released two papers.

3) Co-led the formulation of the “Nx25Gbps WDM-PON for 5G Mobile Fronthaul” series standards of China Communications Standards Association (CCSA).

4) Formulated the industry’s first enterprise standard on Nx25Gbps WDM-PON management channels for China Telecom.

5) Proposed the concept of SFP ONUs, which has been accepted by CCSA and is being incorporated into its standards.

Besides the achievements in WDM-PON standards, ZTE has also made breakthroughs in key WDM-PON technologies, including:

1) Developed 25Gbps WDM-PON optical modules with low cost, low power consumption, and high transmission power.

2) Developed the technology of ultra-low latency forwarding of CPRI/eCPRI traffic based on cell switching.

Summary and Prospects:

25Gbps WDM-PON is ideal for 5G fronthaul. It is a key innovation to enable 5G+FTTH converged gigaband access in an economical way. ZTE is currently extending WDM-PON based fronthaul from outdoor AAUs to a 5G indoor distribution system. When indoor 5G fronthaul is combined with the Passive Optical LAN (POL), 5G+FTTO (Fiber To The Office) converged dual-gigabit rates can be achieved in industrial parks.

References:

https://www.gsmaintelligence.com/research/?file=67a750f6114580b86045a6a0f9587ea0&download

AT&T FirstNet Makes Great Progress; Deal with Mutualink increases Inter-operability

FirstNet is a dedicated LTE network for public safety users, which passed 600,000 “connections” earlier this month. It has been built by AT&T and has has engagements with more than 7,000 public safety agencies.

FirstNet is built in public-private partnership with the First Responder Network Authority (FirstNet Authority). This helps to ensure that the FirstNet communications platform and service offerings meet the short- and long-term needs of the public safety community.

FirstNet is improving communications to allow for improved response times and outcomes for first responders from coast-to-coast, in rural and urban areas, inland and on boarders – leading to safer, and more secure communities. It provides innovation and dedicated capacity so public safety can take advantage of advanced technologies, tools and services during emergencies, such as:

- Applications that allow first responders to reliably share videos, text messages, photos and other information during incidents in near real-time

- Devices configured to meet the focused needs of public safety

- Improved location services to help with mapping capabilities during rescue and recovery operations

- Deployables available for planned and unplanned emergency events

……………………………………………………………………………………………………………………………….

Speaking this past week at the MoffettNathanson’s 6th Annual Media & Communications Summit in New York City, AT&T Senior Executive Vice President and Chief Financial Officer John Stephens discussed how the carrier’s deployment of FirstNet is progressing rapidly and laying the groundwork for 5G.

According to AT&T, FirstNet is 25% faster than any domestic commercial network. That claim is based on Ookla test data covering average download speeds in Q1 2019.

The FirstNet build-out is instrumental to AT&T 5G deployment plans, Stephens said. “The FirstNet contract, which is enabling us to go through a process from an LTE to evolve into a 5G network, is really working. We’re getting dramatic speed uptakes. If you look at the two fastest networks in the United States right now, they’re both ours…That’s what’s driving the business. That’ll drive innovation, that’ll drive opportunity.”

As AT&T upgrades its cell sites to deploy Band 14 [1] for FirstNet, crews are upgrading other equipment to support the 5G New Radio specification. Stephens said the operator is working toward “national coverage of 5G” by the “middle of the next year.”

Note 1. Band 14 is the spectrum licensed to the First Responder Network Authority (FirstNet) to create a nationwide public-safety wireless broadband network. Band 14represents 20 MHz of highly desirable spectrum in the 700 MHz band that provides good propagation in urban and rural areas and decent penetration into buildings.

……………………………………………………………………………………………………………………………..

This week, AT&T announced it would resell Mutualink to enhance interoperable communications for public safety. This new relationship will allow AT&T to bring Mutualink’s Interoperable Response and Preparedness Platform (IRAPP) to first responders and supporting agencies using services provided over FirstNet public safety communications platform.

Mutualink states on their website: “This network is the largest nationwide network of public safety agencies, critical infrastructure, schools and private enterprise security. The IRAPP is transport agnostic, device agnostic and media agnostic. It leverages your current communications assets and incorporates new devices as needed. Connect to the IRAPP network via public or private LTE, satellite or terrestrial broadband.”

“FirstNet brings public safety one, nationwide platform for consistent, reliable communications across agencies and jurisdictions,” said Chris Sambar, senior vice president, FirstNet Program at AT&T. “As apps and mobile data increasingly become critical components of the public safety response, we want to help make sure the flow of information that FirstNet provides remains seamless. Our agreement with Mutualink aims to do just that, taking the interoperability that FirstNet provides to the next level.”

FirstNet already facilitates multi-agency communications to aid in incident response and resolution. The agreement with Mutualink builds upon this, expanding the reach, reliability and capability of FirstNet services today. FirstNet subscribers can use the Mutualink IRAPP solution to enhance their ability to easily and quickly communicate across systems and applications, sharing voice, data, video and more in a highly secure environment.

By bringing the Mutualink solution to the FirstNet platform, first responders using Mutualink’s IRAPP will be able to simultaneously take advantage of key FirstNet capabilities – like First Priority™, which enables priority and, for first responders, preemption.

“Adding Mutualink’s Interoperable Response and Preparedness Platform to the FirstNet communications platform will increase the level of interoperability for public safety, especially with respect to on-demand cross-agency interoperability. Our solution enables highly secure sharing of video and data across systems and integration with smart sensor and IoT systems,” Mark Hatten, chief executive officer and chairman, Mutualink. “This will help FirstNet subscribers scale up their access to emerging information as the situation unfolds, creating a common operating picture for all involved.”

……………………………………………………………………………………………………………………….

“FirstNet is helping first responders solve long-standing interoperability challenges and arming them with the information they need to coordinate action plans and make critical decisions. We’re pleased to see AT&T form innovative collaborations that will help foster a new era of situational awareness for public safety,” said FirstNet Authority Acting CEO Edward Parkinson.

………………………………………………………………………………………………………………………

References:

https://www.firstnet.gov/network

https://about.att.com/story/2019/att_and_mutualink.html

https://mutualink.net/our-solution/

http://mutualink.net/wp-content/uploads/2017/03/1-National-Vision-White-Paper-3-17-17.pdf

https://www.rcrwireless.com/20190516/5g/att-5g-national-coverage