Optical Network Equipment Market

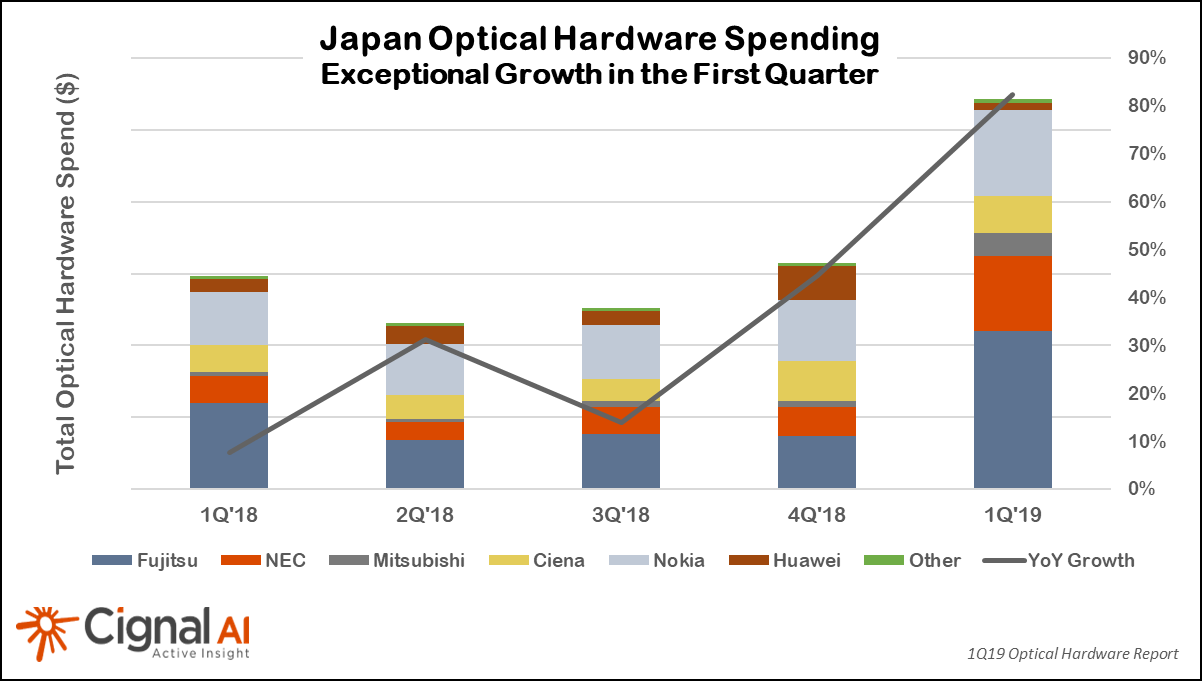

Cignal AI: Japan’s Optical Hardware Growth Soars in 1Q2019; North America Remains Weak

by Scott Wilkinson and Andrew Schmitt of Cignal AI (edited by Alan J Weissberger)

Metro Bandwidth Growth Outpaces Long Haul; North America Remains Weak

Japan continued its recent hot streak as 1Q2019 marked the fourth quarter in a row of growth with an extraordinary 82% increase, according to the most recent (1Q2019) Optical Hardware Report from research firm Cignal AI. Japan registered an extraordinary 82% year-over-year increase in optical networking hardware sales in the first quarter of 2019. Prime beneficiaries were domestic suppliers NEC, Mitsubishi and Fujitsu along with Ciena and Nokia, all of which posted significant gains during the quarter.

“The exceptional optical market growth in Japan is the story to watch for 2019,” said Scott Wilkinson, Lead Analyst for Optical Hardware at Cignal AI. “Network operators have begun significant network rebuilds and expansions, and domestic as well as non-Japanese vendors continue to grow sales in the region at remarkable rates.”

North American growth continued to disappoint as slow optical hardware spending among traditional telco operators obscured growth in sales to cloud and colo operators (e.g. multi-tenant data centers).

Additional key findings in the 1Q19 Optical Hardware Report:

- Metro Bandwidth Outpaces Long Haul – While long haul spending grew at a higher rate than metro, analysis reveals that metro bandwidth is growing more rapidly.

- Growth in China Decelerates – Growth in China moderated into the single-digits during 1Q19, as 2018’s high spending by Chinese carriers could not continue indefinitely.

- EMEA Posted Solid Gains – Both metro and long haul spending grew during the quarter, with growth led by both traditional and cloud & colo operators.

- CALA Continues Lackluster Performance –Q1 showed no improvement for the region. Relief may be coming, as vendors believe major carriers in the region will return to spending later this year.

Cignal AI’s Optical Hardware Report is issued each quarter and examines optical equipment revenue across all regions and equipment types. The analysis is based on financial results, independent research, and guidance from individual equipment companies. Forecasts are based on overall spending trends for equipment types within the regions.

……………………………………………………………………………………………………………………………………………………………………………………………………..

Cignal AI’s interactive Optical Hardware Superdashboard is available to clients of the Optical Hardware Report and provides up-to-date market data for real-time visibility on individual vendors’ results. Users can manipulate data online and see information in a variety of useful ways.

The Cignal AI Optical Hardware Report is published quarterly and includes market share and forecasts for optical transport hardware used in optical networks worldwide. In addition to the interactive tracker, the analysis includes an Excel database as well as PDF and PowerPoint summaries. Subscribers to the Optical Hardware Report also have access to Active Insight, Cignal AI’s real-time news service on current market events.

The report examines revenue for metro WDM, long-haul WDM and submarine (SLTE) equipment in six global regions and includes detailed port shipments by speed. Vendors in the report include Adtran, ADVA, Ciena, Cisco, ECI, Ekinops, Fiberhome, Fujitsu, Huawei, Infinera, Mitsubishi Electric, NEC, Nokia, Padtec, Tejas, Xtera, and ZTE.

Full report details, as well as articles and presentations, are available on the Cignal AI website.

About Cignal AI

Cignal AI provides active and insightful market research for the networking component and equipment market and the market’s end customers. Our work blends expertise from a variety of disciplines to create a uniquely informed perspective on the evolution of networking communications.

Cignal AI: Record Spending on Cloud Operator Optical Networks Drives Growth in 2018

Cignal AI: Record Spending on Cloud Operator Optical Networks Drives Growth in 2018

|

|

|

Cignal AI: Long-Haul WDM Deployment Growth Sets Stage for Increased Spending in 2019

|

|

|

OFC 2019: Importance of Software and 5G Related Sessions

As optical networking evolves, industry changes emphasize the increasing importance of software in optical communications. Today’s software research extends beyond SDN/NFV to address control and optimization of transmission systems, network planning, and device design, and OFC’s Demo Zone picks up on this trend.

“OFC allows to us explore the latest software developments and discuss emerging trends,” said Laurent Schares, IBM Research, USA, an OFC 2019 general chair. “Now is the time to address operational strategies, use cases and field deployments — and demonstrations drive that point home.”

OFC 2019 expanded this year’s Demo Zone to reflect industry evolution. The Demo Zone will feature live demonstrations of key software functions and tools for optical communication devices, systems and networks. From AI engine cooperation to an open dis-aggregated transport network and beyond, the OFC Demo Zone addresses topics of coordination and collaboration between systems and organizations. These proof-of-concept and research demonstrations offer an opportunity for small group, interactive dialogue, featuring real-time exchanges between attendees and presenters.

………………………………………………………………………………………………………………………………………..

5G related symposia at OFC 2019:

5G Trials, Pilots, and Demonstrations, Monday, 4 March, 08:00 – 16:00

Organizers: Thomas Pfeiffer, Nokia Bell Labs, Germany; Jun Terada, NTT, Japan; Shan Wey, ZTE, USA

The fifth generation mobile networks (5G) have promised to transform mobile broadband services through a new network architecture that will enable significantly faster access speed, ultra-reliable low latency communications, and massive machine-to-machine communications, not only for mission critical applications but for everyone everywhere. As the industry is progressing towards 5G standards and 5G capable technologies, the deployment of 5G networks is about to become reality as evidenced by the flood of new product announcements and field trial reports by network operators.

This symposium is intended to update the OFC community about the latest progress of 5G trials, pilots, and demonstrations. Use case scenarios involving a wide range of relevant vertical sectors, e.g., mobile broadband access, connected transport, digital health, smart cities/venues, creative media, will be discussed. By reporting on recent progress, we hope to highlight the role of photonic technologies in delivering 5G network solutions and further inspire and challenge the photonics industry to advance developments targeting the future mobile communication networks.

The symposium is divided into three sessions. The first session will focus on 5G requirements and how major system vendors will realize x-haul transport over optical systems. The second session will provide insight into the perspectives and first experiences of leading telecom network operators and industrial players using 5G technologies. The third session finally will showcase future applications and field trials related to public sector initiatives.

Session 1 – 5G Trials: Vendor’s Perspective

Monday, 4 March, 08:00 – 10:00

Francis Dominique, Nokia, USA

Requirements of 5G Radio Netwoks on Optical X-haul Transport

The high data rate and very low latency applications supported by 5G require an appropriate transport network to meet the requirements of these applications. This paper provides an insight to the requirements imposed by 5G radio access networks (RAN) on front/midhaul transport.

Li Mo, ZTE, China

ZTE’s 5G Trials

Stefano Stracca, Ericsson, Italy

Network Convergence in 5G Transport

Soundarakumar Masilamani, C-DOT, India

5G Rural Strategy in India

Session 2 – 5G Trials: Network Operators’ and Vertical Industries’ Perspective

Monday, 4 March, 10:30 – 12:30

Kent McCammon, AT&T, USA

Recent Progress of AT&T’s 5G Trials

Yukihiko Okumura, NTT DoCoMo, Japan

5G Trials in Japan

Walid Mathlouthi, Google, USA

Regulatory Aspects for 5G to Enable New Business Models

Yuji Inoue, Toyota InfoTechnology Center, Japan

Industry 4.0

Session 3 – 5G Trials: Public Sector Initiatives

Monday, 4 March, 14:00 – 16:00

Dimitra Simeonidou, University of Bristol, UK

Test Bed and Trials for 5G Content Delivery in England

Harald Haas, University of Edinburgh, UK

5G Rural Trials in Scotland

Dan Kilper, COSMOS-PAWR, USA

COSMOS: An Advanced Optical and Wireless Networking Testbed in NYC

Moises Ribeiro, Universidade Federal do Espírito Santo, Brazil

5G Research and Testbeds in Brazil

https://www.ofcconference.org/en-us/home/program-speakers/symposia/

IHS Markit: Ciena tops the list of optical equipment vendors + Cignal AI’s OFC Preview

By Heidi Adams, executive director, network infrastructure, IHS Markit

Each year IHS Markit surveys service providers, in order to find out which companies they view as the leaders of the optical equipment market. The survey also explores their perceptions of vendors in key decision metrics, like pricing, total cost of ownership, technology innovation, research-and-development (R&D) investment, and product reliability.

Following are some of the key findings from this year’s survey:

Optical equipment vendor leaders:

In brand awareness, respondents perceive Ciena, Huawei, and Nokia as the overall leaders for optical transmission and switching equipment in 2018, with no change in the rankings from last year. These results are well aligned with positioning in the global optical network hardware market in the first three quarters of 2018, where Huawei, Ciena, and Nokia were ranked as the top three vendors by market share in this period.

Ciena was the most cited leader in optical DCI, with Huawei and Infinera tied for second place. Ciena also made significant strides this year in market perception for leadership in optical disaggregation, rising from third position in our 2017 survey to first-ranked position in 2018. Coriant (now Infinera), Huawei and Nokia all tied for second place.

Purchasing criteria:

IHS Markit survey respondents were also asked to identify the leaders in purchasing criteria, including pricing, technology innovation, product reliability, service and support and investment in research and development. The top three vendor selection criteria for optical equipment purchasing decisions in 2018 were, as follows:

- Product reliability

- Pricing

- Total cost of ownership

Ciena was the leader in 2018 for service provider perception of vendor leadership in product reliability, technology innovation, management software, and investment in research and development. Huawei topped the list for service provider perception of vendor leadership in pricing, total cost of ownership, solution breadth, and financial stability. Nokia was perceived as the leader in service and support for optical networks.

Optical Equipment Vendor Leadership Service Provider Survey – 2018

This survey explores how service providers evaluate and select optical transmission and switching equipment suppliers. It covers vendors installed and under evaluation and service provider opinions of vendors, including on key vendor selection criteria.

…………………………………………………………………………………………………………………………………………………

Cignal AI on OFC 2019–

400ZR Steals the Show:

No single topic at OFC will command as much attention as 400ZR, which is based on fourth-generation coherent technology and an OIF standard for coherent short reach DCI applications. Product development is well underway with over a dozen component and equipment companies spending in excess of $300M in this effort. The market for short reach coherent extends well beyond the DCI needs of Microsoft and Google. Derivatives (known as ZR+ or ZR plus) are emerging which are designed to meet the broader needs of network operators everywhere. ZR is the first coherent technology that will be both standardized and pluggable, and the emergence of ZR products will shake up the optical equipment landscape. One major impact is that 10G WDM will become obsolete in its only remaining stronghold- the edge of the optical network. The greater question is what role standalone optical hardware will play in the network as the performance and interoperability of coherent pluggables improve. Expect a cascade of activity at OFC from component and equipment companies as they uncover their ZR plans and demonstrate the latest optical engines, and some bombshell announcements and partnerships from the leaders in this space – Inphi, Acacia, Ciena, Cisco, Huawei, Nokia, and NTT Electronics.

While fourth-generation 400G products have been announced at OFC already for the last two years, 2019 is the year that these products start deploying for revenue. Starting in early 2019, third generation solutions from Acacia (via multiple hardware vendors), Nokia, Huawei, Fujitsu, and Infinera will join Ciena in live network deployments. Now that 400G is deployed, there will be multiple roadmap announcements at OFC seeking to leapfrog 400G and propose the next generation of coherent optical speeds. 600G is a given, but there will be 800G and perhaps 1Tbps announcements as well. Components suppliers and equipment manufacturers will show roadmaps to higher speed sixthgeneration coherent optical components in preparation for a 2020 introduction.

We expect Infinera to disclose more detail on its ICE6 R&D efforts and would not be surprised to hear Ciena talk about a successor to the Wavelogic AI now that competitive products are arriving in the market.

Disaggregation Continues, with Many Definitions:

The disaggregation trend will continue to gain strength at OFC, but the definition will continue to change. Whereas the original concept was complete separation of switching transponders, ROADMs, and perhaps even components into separately manageable elements, now new solutions are starting to look more like traditional optical equipment. Compact modular systems, which are the most visible components of a disaggregation strategy, have moved from monolithic transponder or open line systems to more complex devices that can include switching and multiple functions in the same shelf. Some systems now even have modularity via cards (although they are called “sleds” rather than “cards”), making them look more like traditional systems in everything but physical dimensions. Several large operators are skeptical about disaggregation, while several others agree with the concept but consider current solutions too difficult to manage. Regardless, the industry-wide shift to disaggregation will accelerate as implementation becomes easier and better attuned to the needs of a wider variety of customers. General availability and customer announcements for 2019 are expected from several vendors, including ADVA, Cisco, Coriant, Fujitsu, and Nokia. In addition to the compact modular announcements,

Cignal AI Raises Forecast for Asia Optical Hardware Market while NA declined for 8th consecutive quarter

|

|

|

Optical Vendor Summary Reports

A new feature of the Optical Hardware Report this quarter are Optical Vendor Summary Reports which examine in depth the most recent quarterly results and items of interest about vendors in the optical market. Reports this quarter cover ADVA, Ciena, Fujitsu, Huawei, Infinera/Coriant and Nokia.

About the Optical Hardware Report

The Cignal AI Optical Hardware Report is published quarterly and includes market share and forecasts for optical transport hardware used in optical networks worldwide. The analysis includes an Excel database as well as PDF and PowerPoint summaries. Subscribers to the Optical Hardware Report also have access to Cignal AI’s real-time news briefs on current market events, Active Insight.

The report examines revenue for metro WDM, long-haul WDM and submarine (SLTE) equipment in six global regions and includes detailed port shipments by speed. Vendors in the report include Adtran, ADVA, Ciena, Cisco, Coriant, ECI, Ekinops, Fiberhome, Fujitsu, Huawei, Infinera, Juniper Networks, Mitsubishi Electric, MRV, NEC, Nokia, Padtec, Tejas, Xtera and ZTE.

Full report details, as well as articles and presentations, are available on the Cignal AI website.

IHS Markit: Data Center Interconnect (DCI) is Fastest-growing Application for Optical Networking

A significant driver for innovation in the optical market, data center interconnect (DCI) is the fastest-growing application for optical networking equipment, according to a new study from business information provider IHS Markit. Eighty-six percent of service providers polled for the Optical Network Applications Survey have plans to support DCI applications in their networks.

“Data center interconnect is enjoying a meteoric rise as the hottest segment in the optical networking applications space,” said Heidi Adams, senior research director for transport networks at IHS Markit. “Service providers are becoming increasingly invested in the DCI market, both for providing interconnect between their own data centers and for offering DCI services to internet content providers and enterprises. We estimate that service providers will account for around half of all DCI equipment spending in 2018.”

The optical data center equipment market reached $1.4 billion in sales in the first half of 2018, posting 19 percent year-over-year growth, according to IHS Markit. A key driver of the market is the compact DCI sub segment, which notched a 173 percent growth rate during this same time period.

“‘Compact’ DCI equipment is designed to fit within a data center environment from the form factor, power consumption and operational perspectives,” Adams said. “It’s optimized to meet the requirements of internet content providers like Google, AWS, Facebook, Microsoft and Apple.”

The top three vendors in the compact DCI sub segment are Ciena, Infinera and Cisco, who collectively account for three-quarters of the market.

Additional DCI highlights

- Cost per port is the leading criterion among survey respondents for the selection of equipment for DCI applications.

- 100G is the main currency for line-side DCI interfaces in 2018, declining in favor of 400G by 2021.

- IHS Markit forecasts the total DCI market to grow at a 15 percent compound annual growth rate (CAGR) from 2017 to 2022, representing a higher rate of growth than the overall WDM market.

Optical Network Applications Service Provider Survey – 2018

This survey analyzes the trends and assesses the needs of service providers using emerging optical networking architectures. It covers data center interconnect, packet-optical equipment and software-defined networking for transport networks. For the survey, IHS Markit interviewed 22 service providers who have deployed packet-optical transport, optical DCI and/or transport SDNs or will do so in the future.

DCI, Packet-Optical & OTN Equipment Market Tracker

This biannual report provides worldwide and regional vendor market share, market size, forecasts through 2022, analysis and trends for data center interconnect equipment, packet-optical transport systems, and OTN transport and switching hardware.

Reference:

https://www.ciena.com/insights/what-is/What-is-DCI.html

Cignal AI: Record Cloud and Colo Optical Hardware Spending in 2Q18

by Andres Schmitt

Ciena Leads Sales to North American Cloud/Colo Operators; Huawei Sees Strong Demand from Chinese Cloud Giants

|

|

|

Cignal AI: Compact Modular Optical Equipment Market to hit $1 Billion in 2018

|

|

|

IHS Markit & Cignal AI: Global Optical Equipment Market Down but EMEA Up

By Heidi Adams, senior research director, transport networks, IHS Markit

Highlights

- In the second quarter of 2018 (Q2 2018), global optical network hardware revenue totaled $3.5 billion, decreasing 7 percent on a year-over-year basis.

- The global Q2 2018 optical equipment market net of China was down 3 percent year over year. China itself declined 17 percent year over year.

- Wavelength division multiplexing (WDM) revenue totaled $3.3 billion in Q2 2018, up 9 percent quarter over quarter, but down 6 percent from a year ago.

- Huawei remained the overall optical equipment market leader in Q2 2018, increasing its market share to a new high of 36 percent. Ciena moved into the number-two position, and Nokia dropped to third.

Our analysis

The optical equipment market continued to struggle in Q2 2018 due to the following factors:

- Lower spending in China; ZTE shuttered major operations for most of the quarter

- A big drop in submarine line terminal equipment (SLTE) spending

- A slowdown in long-haul spending by tier-1 operators in North America

Even a healthy internet content provider (ICP) segment has not been enough to offset the spending declines of the major operators in North America. Europe, the Middle East and Africa (EMEA) remained flat year over year. The Caribbean and Latin America (CALA) saw sequential growth, but the region continued its overall year-over-year downward trend of diminishing network infrastructure investment. Meanwhile, in Asia Pacific, India remains very strong for optical spending and Japan is emerging as an area of renewed investment.

The WDM equipment segment increased sequentially but declined on a year-over-year basis – as did the metro and long-haul WDM sub segments. IHS Markit continues to view the metro WDM sub segment as the main growth vector for the market through at least 2022. Subsea-related optical equipment investment continues to be project driven and highly variable, with second quarter SLTE at half the level seen in the same period last year.

Looking ahead, IHS Markit forecasts a positive optical equipment market compound annual growth rate (CAGR) of 4 percent from 2017 through 2022.

Optical Network Hardware Market Tracker – Q2 2018

This report tracks the global market for metro and long-haul WDM and SONET/SDH equipment and SONET/SDH and WDM ports. It provides market size, market share, forecasts through 2022, analysis and trends.

………………………………………………………………………………………………………………………………………………………………………

Cignal AI Reports 2Q18 EMEA Optical Spending Offset Weakness in North America

by Andrew Schmitt, Founder – Cignal AI

|

|

|