Uncategorized

Barclays: Expect slower growth for cable companies Comcast and Charter; AT&T to benefit

Investors should expect slower growth ahead for cable companies Comcast and Charter Communications, according to Barclays. Analyst Kannan Venkateshwar downgraded shares of Comcast to equal weight, and shares of Spectrum parent company Charter to underweight, pointing to dwindling subscriber numbers.Barclay’s noted dwindling subscriber numbers for the two companies.

A key source of concern among cable investors is the presence of emerging competition in the market for internet services, as wireless companies push forward with fiber and fixed-wireless-access offerings. While Comcast’s and Charter’s management teams made some acknowledgment of the competitive landscape on their earnings calls, they maintained that the biggest factor driving recent performance was that people have been moving homes in smaller numbers than before.

Venkateshwar didn’t seem sold on the cable companies’ explanations. “While cable has gained share vs DSL over time and therefore lower moves would impact growth rates, it is mathematically impossible to get to negative growth as seen last quarter, purely on account of lower move activity,” he wrote. “In addition, the decline in move activity is not new and has been going on for years and tends to worsen during recessions.”

He added that even if move rates were to improve, “there are new elements that are likely to reduce cable’s share of gross adds” — namely the emerging competitive dynamics.

“Charter’s management almost seems in denial of competition in talking down its impact, but if TMUS does grow fixed wireless access (FWA) to the full extent of its guidance range (~500k+/quarter), TMUS alone would be bigger than Altice by the end of next year,” Venkateshwar continued. “It is tough to see this not impacting cable structurally when cable net adds overall have been ~3mm in normal years and TMUS and VZ alone could add 2-2.5mm FWA subs a year.”

Venkateshwar isn’t sure that FWA represents “a viable solution for telecom operators long term” given capacity requirements, but said that for the moment, T-Mobile US Inc.and Verizon Communications Inc. have “low marginal costs due to excess spectrum.”

“Consequently, even if FWA proves unviable long term, it could still be a significant headwind for cable over the next 2-3 years,” he wrote.

Additionally, with the help of government funding, more people could move from DSL over to fiber, which would benefit AT&T which has been laser focused on growing its fiber footprint.

Venkateshwar acknowledged that one criticism of his analysis may be that he isn’t giving the cable companies enough credit for growing their own footprints, but he doesn’t see much correlation between footprint expansion and broadband growth rates for Comcast, Charter, and Altice USA Inc. when looking at the past five years. Accordingly, he expects the companies could get even less marginal benefit in a world with growing competition.

“Overall, these factors imply that the largest cable companies, Comcast and Charter, are likely past peak growth and the debate therefore boils down to the degree of downside to broadband net adds going forward,” he wrote. Venkateshwar said that his analyst suggests “cable providers could be at flat growth next year and potentially negative thereafter unless their pace of footprint expansion and marginal penetration of this expanded base accelerates.”

He noted that the companies have been growing wireless subscribers, though he has questions about the long-term economic potential of their wireless involvement. As it stands, Charter and Comcast have a mobile virtual network operator (MVNO) arrangement with Verizon that allows the companies to leverage Verizon’s network.

This strategy makes sense to test out the market and launch a service, but to anchor long-term strategic pivot of the scale that cable companies are attempting on someone else’s network is not viable in our view,” he wrote. “If cable companies continue to face challenges in broadband, which we think is likely, they may have little choice but to invest in more extensive wireless infrastructure in some form to extract the benefit of scale in wireless.”

References:

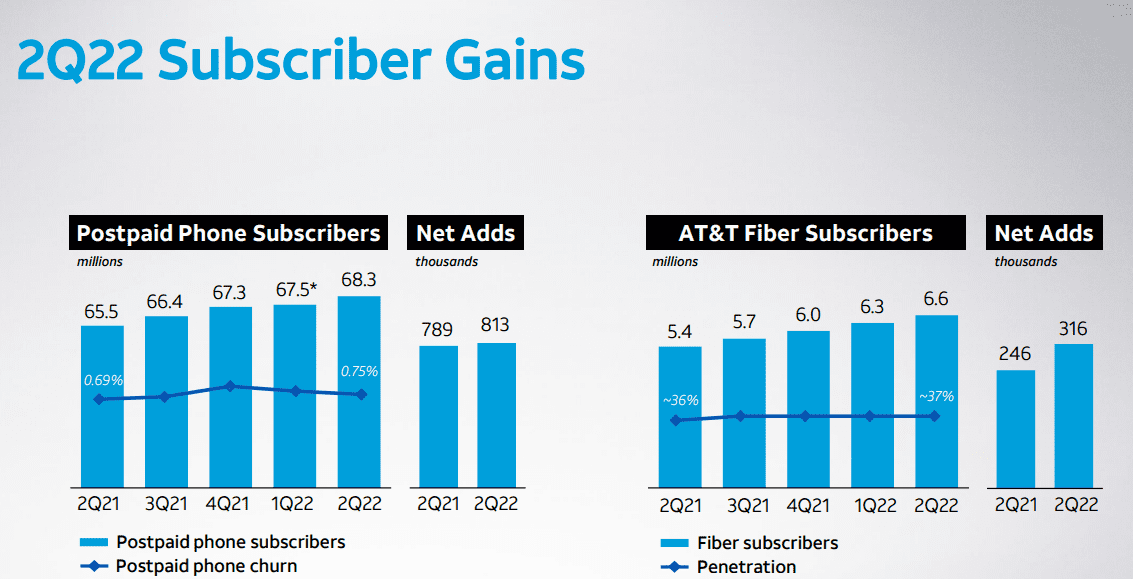

AT&T added 813K mobile postpaid subscribers & >300K net fiber subs during 2Q-2022

AT&T remains committed to investing in its network operations, including a focus on its 5G and fiber-optic related assets. AT&T gained 813,000 mobile postpaid subscribers during the quarter that ended in June, more than doubling analyst predictions and raising its wireless revenue forecast for 2022.

AT&T posted flat results for its now dominate communications segment, which includes its 5G wireless, wireline, and fiber operations. Segment revenues increased 2% year over year to $28.7 billion. However, increased costs and a loss of wireline customers dropped segment operating income by 2.1% to $7.2 billion.

AT&T CEO John Stankey said on today’s earnings call:

“In Fiber, we continue to invest in building out a premium network, drive a great build velocity and deliver on our stated expectations for accelerated customer growth through improved penetration rates. We’re finding success in serving more customers in new and existing markets with what we believe is the best wired Internet offering available. This is evidenced by our more than 300,000 second quarter AT&T Fiber net adds, marking our 10th straight quarter with more than 200,000 Fiber net adds.

The strength and value of the AT&T Fiber experience is enabling us to increase share in our Fiber footprint and convert more IP broadband Internet subscribers to Fiber subscribers. Ultimately, our Fiber strategy is a sustainable and long-term technology play that will support key macro trends.

We expect to see a continuation of favorable ARPU trends as we expand the availability of what we believe is a best-in-class network with a multi-decade lifespan. So I’m very pleased with the strong customer growth we’re seeing.

Our success only reinforces the improved value proposition we’re providing, and we expect our investment in top-tier technology to translate into strong resiliency for our services for years to come.

Over the last eight quarters, we’ve achieved an industry-best six million postpaid phone net adds while adding nearly 2.3 million AT&T Fiber customers, increasing our Fiber subscriber base by more than 50%. I’m also very proud with the progress our teams have made in rapidly expanding our 5G and fiber footprints.

I’m pleased to say that we’ve achieved our target of covering 70 million mid-band POPs 2 quarters ahead of our year-end target, and are now on track to approach 100 million mid-band POPs by the end of this year.”

……………………………………………………………………………………………………………………………………………..

AT&T reduced its free cash flow expectations (FCF), saying that customers were paying bills later than usual due to economic stress. AT&T said it now expects 2022 free cash flow of $14 billion. About $1 billion of the difference was tied to the “timing of customer collections.”

The gloomier FCF outlook overshadowed second-quarter results that topped estimates for profit and wireless subscriber growth.

…………………………………………………………………………………………………………………………………

AT&T CFO Pascal Desroches told investors that AT&T was bracing for a delay in consumers paying their bills due to surging recession concerns. He explained that “it’s taking about two more days than last year to collect customer receivables,” which resulted in a $1 billion impact in Q2, and that AT&T had around $130 million in higher bad debt expense.

“While bad debt is now slightly higher than pre-pandemic levels, it is being offset by better than expected customer revenue growth,” Desroches said, citing recent price increases.

Desroches also warned that AT&T was cutting its full-year free-cash-flow guidance from $16 billion down to $14 billion due to ongoing economic and recession uncertainty. That cut looked modest next to the carrier only posting $4 billion in free cash flow for the first half of the year, which was well below expectations.

The executive explained that AT&T had front-loaded its $24 billion in full-year capex due to its mid-band 5G and fiber deployments. This will lessen second-half spend needs, though AT&T remains committed to spending another $24 billion on capex in 2023.

“It underscores the importance of transitioning to our own operating connectivity services as well as rolling 5G and fiber integrated solutions,” Desroches said of its capex push. “In fact, our connectivity services revenue growth continues to accelerate as we are up nearly 15% year over year. Both areas, business 5G and fiber, continue to perform well.”

AT&T has previously stated that its ability to tie together its 5G and fiber networks allow it to better support enterprise SD-WAN, secure access service edge (SASE), and security needs. The carrier has struck a number of deals with vendors like Cisco, Fortinet, and Palo Alto Networks to power these SD-WAN, SASE, and security initiatives.

“As people migrate away from VPN and we have a more dense fiber base, we’re selling more fundamental underlying transport, frankly, at higher speeds and therefore higher connection values in that segment of the market, and that’s where our future is,” added AT&T CEO John Stankey on the Q2 call.

Analyst Craig Moffett Comments:

To be sure, AT&T’s results in Mobility haven’t been bad. They’ve walked a tightrope of heavy promotions in return for good-enough subscriber growth, and, up to now. On the back

of those passably good results in Mobility, the company has (arguably) provided at least some degree of confidence that they can sustain their new, lowered, dividend.

Meanwhile, they’ve promised faster capital spending on fiber deployment in their Consumer Wireline segment, something they have promised will result in at least positive longer-term growth in a segment that accounts for about 10% of revenues. (They’ve largely been silent about their much larger Business Wireline segment, which is shrinking badly and still getting worse).

AT&T’s consolidated growth prospects rest entirely on their Mobility segment. Their Business Wireline segment, which represents nearly 20% of revenues, is shrinking by high single digits, while their Consumer Wireline segment is at best marginally better than flat. Their Mobility segment has maintained modest service revenue growth through a mix of relatively rapid subscriber growth, offset by shrinking ARPU. Mobility is AT&T’s largest and most important business, accounting for two-thirds of consolidated pro forma revenues.

Subscriber growth trends remain very strong:

• AT&T added 1.06M post-paid subscribers, much better than the Street consensus expectation of 804K, in line with last year’s 1.16M.

• Better still, they added 813K post-paid phone subscribers on an as-reported basis, and with migrations (for comparability to the reporting of the other carriers), would have been a still-impressive 793K. Reported post-paid phone net additions were much better than consensus of 562K, and better than last year’s 789K.

• Pre-paid net additions of 231K also beat Street consensus of 131K, but were down from last year’s 297K gain.

We won’t know the industry’s growth rate until everyone else has reported, but it seems clear that AT&T is gaining unit market share. At their heart of their subscriber gain story is low churn. AT&T’s “best deals for all” promotion continues to keep churn very low.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

According to Seeking Alpha, six analysts rate AT&T stock (“T”) a Strong Buy, while seven have a Buy rating on the stock. 15 analyst rate “T” as a Hold, while there are 0 Sell recommendations.

References:

https://investors.att.com/financial-reports/quarterly-earnings/2022

More KPN customers use fiber vs copper for broadband services in Nederlands

Dutch network operator KPN announced a new milestone on its fixed network: more customers are using fiber services than the old copper infrastructure for the first time. The disclosure was made in an internal announcement obtained by Telecompaper. KPN is seeing a steady increase in fiber orders in its consumer/residential market. The company said around 65% of orders are fiber and 35% for services on copper lines (DSL or POTs).

According to the Q1 Dutch Consumer Broadband report [1.], KPN had roughly the same number of residential DSL and fiber subscribers at the end of March, with just over 1.3 million lines each. While it has been adding fiber optic subscribers steadily each quarter, DSL losses remain slightly greater when including its second brand. The total consumer fixed broadband base has been flat (0% growth) over the past year.

Note 1. This Telecompaper report analyses developments in the first quarter of 2022 in the Dutch market for broadband internet access, focusing on consumer connections. The report further includes data on developments, fixed market revenues and broadband revenues. The findings are compared with results from previous periods. The analysis is based on Telecompaper’s continuous research into the development of the Dutch broadband communication services market. The focus is on cable network operators (Ziggo, Delta, Caiway), DSL providers (KPN, T-Mobile, Tele2, Online.nl, Budget Thuis) and FTTH providers (including KPN, T-Mobile, Caiway, Delta, Tele2, Online.nl, Budget Thuis).

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Babak Fouladi, KPN’s Chief Technology & Digital Officer and member of the Board of Management, spoke at the Telecom Insights 2022 conference in May. He said:

“Telecom networks are essential and vital, and we do not only literally ensure that the world remains connected to everything and everyone. Our networks also support massive digitization, essential in crisis situations since online access is often the only door to the outside world and contact with others. Our networks enable people to work from home, study online or continue doing business. In addition, the digital infrastructure contributes to the global economy and to keeping healthcare and education affordable. And our infrastructure makes a structural contribution to reducing CO2 emissions, the use of fossil fuels and cleaner air. Digitization is more and more important as accelerator for sustainability.”

He concluded his speech with an appeal to the Dutch telecom sector: “Let’s make the Netherlands the best connected country in the world! Let’s make it happen, together.”

![]()

References:

https://www.overons.kpn/nieuws/en/lets-make-the-netherlands-the-best-connected-country-in-the-world/

Swisscom tests 50G PON technology on a live network

State-owned network provider Swisscom has begun testing 50G PON technology in the live network of an unnamed Swiss municipality, after putting it through its paces in a laboratory in 2020 – the first telco in the world to do so, it claims. Swisscom believes 50G PON will lead to increased flexibility for its business customers, facilitating, for example, additional security features.

Swisscom claims that “50G-PON will lead to a new kind of flexibility in high-speed connectivity, chiefly for business customers, paving the way for additional security service features or connection service attributes. For example, the technology significantly reduces latency compared to today’s standards, and guaranteed transmission speeds can be defined by network slicing (NOTE: network slicing requires a 5G SA Core network and is not intended for fiber optics networks). These are just a few examples that, thanks to 50G-PON, can be included in considerations for new products and services aligned to business customer requirements in the coming years.”

Swisscom plans to introduce the technology by 2025 at the latest. PON technologies can be used in both point-to-point and point-to-multipoint networks. The passive splitter is placed in a point-to-point network rather than in the cable conduit at the control center.

References:

https://www.swisscom.ch/en/about/news/2022/07/11-neuster-glasfasertechnologie.html

https://www.swisscom.ch/en/about/network.html

Review of SideTrak Solo 17.3 inch portable monitor

This SideTrak Solo portable 17.3 inch monitor works great!

It was easy to set-up via Windows 10 laptop- plugged in HDMI cable for the audio/video and USB cable for power feeding from PC to monitor. Then changed Display settings to dual display from mirrored display in order to get 2 separate screens.

After set-up, you can drag a webpage from 1 screen to another which is very useful if you are doing research work or want to watch a video on 1 screen while working on the other screen.

The image clarity is better than on my new ACER laptop which was a pleasant surprise. You can adjust the volume UP or DOWN via the top & bottom buttons on the lower right side of the display. The stand is very stable so it’s easy to move the monitor.

Because it’s portable, you can take it along with your laptop to do work or watch videos away from home/on the road.

All in all, I’m very satisfied with this product!

References:

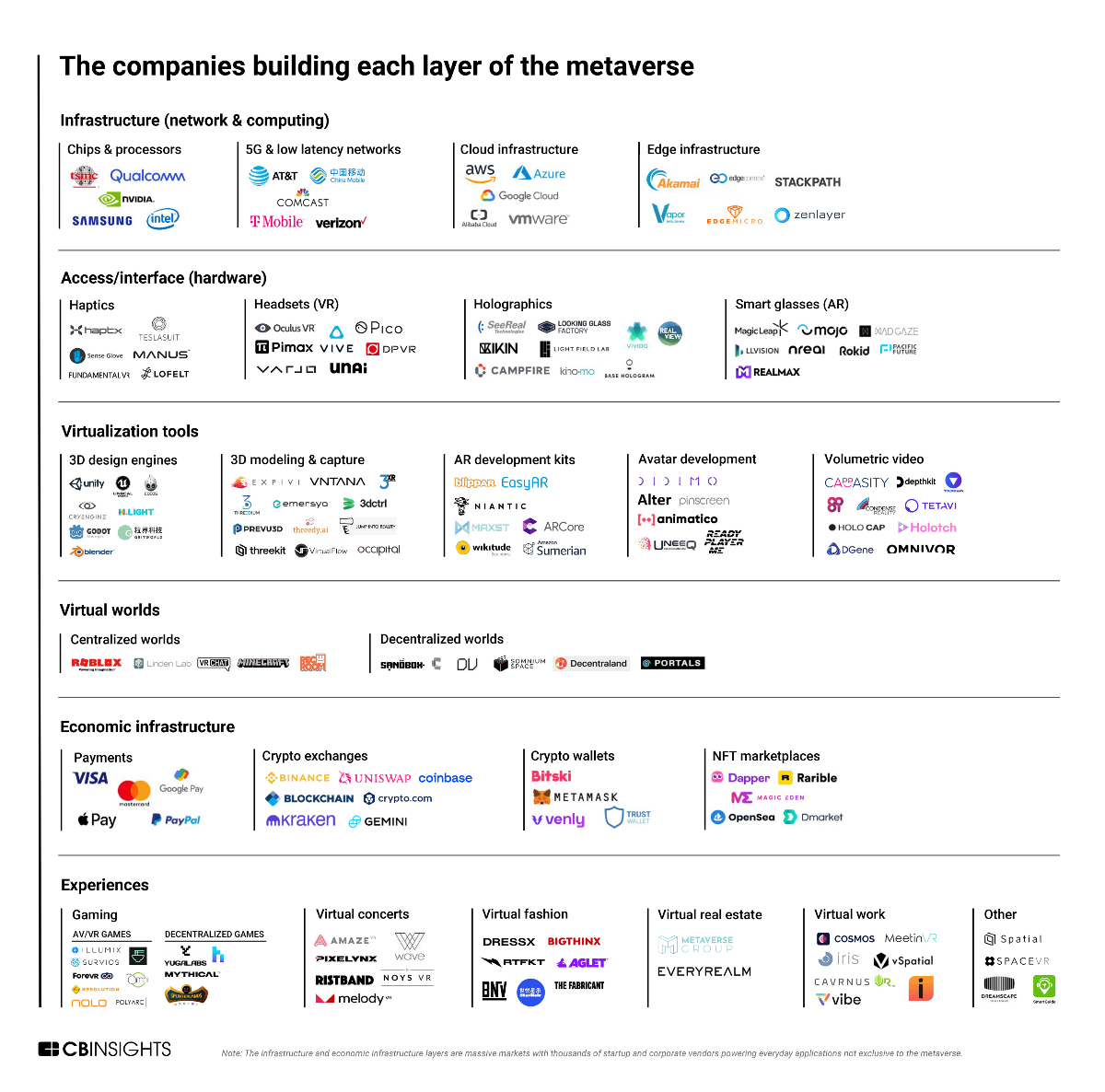

CB Insights: The Metaverse Explained & Companies Making it Happen

The metaverse could be tech’s next trillion-dollar opportunity, according to Mark Zuckerberg of Facebook/Meta Platforms. The business world is obsessed with “the metaverse”: the concept of shared worlds driven by virtual products and digital experiences that are highly immersive and interactive.

We already have virtual worlds featuring live concerts and online games where players spend hundreds of hours — but metaverse enthusiasts see a future where entire societies thrive in an online realm inhabited by avatars of real people.

While the space is still in early days, the longer-term implications may not be trivial. Some users — especially younger ones — may eventually earn, spend, and invest most of their money in digital worlds. The metaverse could represent a $1T market by the end of the decade, according to CB Insights’ Industry Analyst Consensus.

The metaverse is a vision, not a specific technology. For enterprises, this ambiguity can make it challenging to figure out how to tap into the emerging trends the metaverse represents. Below are the companies making it a reality:

The metaverse requires compute and processing infrastructure that can support both big data flows and low latency. Tech emerging within categories such as chips & processors, 5G, cloud infrastructure, and edge infrastructure, will prove vital to creating a seamless, lag-free experience in the metaverse.

Chips & processors: Advancements in this space will support the intense computing and processing requirements of metaverse applications.

New metaverse-focused hardware — e.g., virtual reality (VR) headsets and augmented reality (AR) glasses — is being designed to support intense workloads related to high-fidelity graphics and artificial intelligence (AI) on smaller, lightweight devices. Qualcomm chips stand out in this arena — the tech giant claims its Snapdragon chips have been used in over 50 AR/VR devices, including popular VR headsets like Meta’s Oculus and HTC Vive. Qualcomm also recently announced the launch of its $100M Snapdragon Metaverse Fund, which will invest in the extended reality (XR) space.

Additionally, Intel claims that the metaverse will necessitate a 1000x increase in computational efficiency, including advancements in 5G and hybrid edge-cloud infrastructures. That said, new chips will also be required to power these critical low latency computing networks. In February 2022, the semiconductor company released details on new chips that will support high-power data centers and 5G networks.

5G & low latency networks: 5G wireless tech will power high-resolution metaverse applications — such as immersive worlds or gaming — by supporting reliable, flexible, and low latency networks for connected devices.

As of 2022, each of the leading telecom companies in the US offers a 5G network. Some are experimenting with 5G in gaming and AR/VR. For example, in April 2021, Verizon partnered with VR startup Dreamscape Immersive to build immersive learning and training applications on Verizon’s 5G network. Three months later, AT&T partnered with Meta’s Reality Labs to show how 5G could be utilized to generate more seamless augmented reality experiences.

Cloud infrastructure: Cloud infrastructure will enable metaverse companies, especially those hosting virtual worlds and experiences, to store and parse through the vast amounts of data they generate.

In 2018, Epic Games‘ Fortnite generated 5 petabytes of data per month (that’s equivalent to 2.5T pages of standard text). In order to store and make sense of this data, Fortnite runs almost entirely on Amazon Web Services (AWS), where it uses cloud computing to aggregate and analyze information from its otherwise unwieldy data stream.

Advancements in this space will also help people access the metaverse on devices that lack sufficient processing power for applications like high-res graphics and AI — cloud computing allows experiences to be processed on a remote server and then streamed to a device, such as a PC, VR headset, or phone. While this back-and-forth communication with an external server can lag, related developments in edge computing and 5G will help to reduce latency.

Edge infrastructure: Edge computing will be used for metaverse applications that depend on real-time responses, such as AR/VR and gaming.

Edge computing enables data from low-power devices to be processed closer to where it is created — i.e., at “the edge.” This can be particularly helpful when it comes to situations that require information to be processed in real time — such as utilizing hand-tracking sensors on a VR headset or processing commands during competitive gaming. In fact, edge infrastructure companies like Stackpath and Zenlayer list gaming and virtual reality among their main focus areas.

Edge processing is heavily interrelated with cloud computing. While cloud infrastructure handles workloads that do not require minimal latency, such as loading out-of-sight objects in a game, edge infrastructure handles inputs that need a very quick response, like player movements. Some companies develop blended offerings. For example, Akamai offers edge-cloud hybrid services to a number of high-profile gaming companies, including Roblox and unicorn Riot Games.

Access/interface (hardware)

This layer includes hardware devices that allow people to experience the metaverse. While this category encompasses connected devices like mobile phones, PCs, and gaming consoles, it is predominantly centered around emerging technologies designed to enhance immersion in a virtual setting.

Haptics: Haptic startups are developing technology to bring the sense of touch into virtual worlds.

Some startups, such as HaptX and Sense Glove, are developing gloves that grant virtual objects tangibility. Bridging micro-vibrations, pneumatic systems for force resistance, and motion tracking, this technology can give the impression that digital objects have texture, stiffness, and weight.

In the future, haptic technology may extend well beyond a person’s hands. Scotland-based Teslasuit is developing complete bodysuits to provide whole-body haptic feedback and climate control in virtual environments.

Headsets (VR): These companies are developing VR goggles — currently considered the main entry point to metaverse applications. These devices provide visual and audio content to users to immerse them in a digital setting.

One of the most popular VR headsets is Meta’s Oculus, which saw a surge in consumer interest during the 2021 holiday season.

Startups have followed suit. Varjo, for example, uses lidar and computer vision to bring depth perception, eye-tracking, and hand-tracking to its VR headsets.

Holographics: These companies use light diffraction technology to project 3D objects into physical spaces. These holograms, like augmented reality, bring digital experiences into the physical world.

While holographic technology is still in its early stages, it has the potential to be applied to a wide range of use cases, from hologram-led set design and performances to product design and medicine. Base Hologram is using the tech to bring popular artists like Whitney Houston and Buddy Holly back to the stage, while Israel-based RealView Imaging renders holograms of a patient’s internal organs to help with surgical planning.

The technology has a long way to go before it sees widespread success, but companies currently working in the space have given us an idea of what to expect down the road.

Smart glasses (AR): Companies here are developing glasses or contact lenses with AR capabilities.

While not all applications of AR glasses are directly related to the metaverse — for example, AR tools designed exclusively to help engineers fix refrigerators do not revolve around shared experiences — the companies featured in this category are setting the foundation for a bridge between physical and virtual worlds.

As AR gains popularity, particularly for social purposes, the tech will evolve into a tool that more effectively blends virtual and real-world elements — such as interacting with someone’s metaverse avatar at an event — further blurring the line between consumers’ online and offline identities.

Currently, China-based Nreal is developing AR glasses equipped with web browsing and video streaming capabilities for the everyday consumer. Others, like Magic Leap, are developing AR headsets for enterprise use cases.

5G Emerge: ESA & European Broadcast Union agreement for satellite enabled 5G media market

Recently, the European Space Agency (ESA) announced that it will seek to boost the satellite-enabled 5G media market. The ESA signed an agreement to work with the European Broadcast Union – an alliance of public service media organizations – that will enable Europe to gain a lead in media content delivery as well as maintaining its technical autonomy.

The agreement – called 5G Emerge – is a partnership between ESA and the European Broadcast Union, plus 20 companies from Italy, Luxembourg, the Netherlands, Norway, Sweden and Switzerland. Under the agreement, the partners will define, develop and validate an integrated satellite and terrestrial system which will leverage on the structural advantages of satellite-based infrastructures combined with the flexibility of 5G and beyond 5G technologies to reach anyone, anywhere.

The media industry has been quick to embrace 5G technologies, which offer ultra-high-quality videos as well as extra fast games with very low lag times. Telecommunications satellites will play a crucial role in enabling the seamless and ubiquitous connectivity on which 5G and 6G networks rely.

Under the 5G Emerge agreement, the partners will define, develop and validate an integrated satellite and terrestrial system based on open standards [1.] to efficiently deliver high-quality content distribution services. The system will leverage on the structural advantages of satellite-base infrastructures combined with the flexibility of 5G and beyond 5G technologies to reach anyone and anywhere.

Note 1. There are no ITU-R standard or 3GPP approved specs on 5G Satellite RANs- only terrestrial.

The agreement was signed between Antonio Arcidiacono, Director of Technology and Innovation at the European Broadcast Union, Jean-Pierre Choffray of satellite operator SES, Matteo Ainardi of consultants Arthur D Little and Elodie Viau, Director of Telecommunications and Integrated Applications at ESA.

Antonio Arcidiacono said: “Together we will build a solution that combines all satellite and terrestrial IP-based network infrastructures, guaranteeing sustainability and quality of service. It also guarantees that the network will cover 100% of the population, no matter where they are located. This is a critical requirement for public service media organisations.”

Elodie Viau said: “It is crucial for Europe to protect and enhance its autonomy when it comes to media and communications infrastructure. The 5G-Emerge project will support the digital transformation of European society, enabling new applications and services.”

References:

T-Mobile US achieves speeds over 3 Gbps using 5G Carrier Aggregation on its 5G SA network

T-Mobile US said it was able to aggregate three channels of mid-band 5G spectrum, reaching speeds over 3 Gbps on its standalone 5G network. It’s the first time the test has ever been done with a commercial device, here the Samsung Galaxy S22 powered by Snapdragon 8 Gen 1 Mobile Platform with Snapdragon X65 Modem-RF System), on a live production network, the company said.

5G Carrier Aggregation (New Radio or NR CA) allows T-Mobile to combine multiple 5G channels (or carriers) to deliver greater speed and performance. In this test, the carrier merged three 5G channels – two channels of 2.5 GHz Ultra Capacity 5G and one channel of 1900 MHz spectrum – creating an effective 210 MHz 5G channel.

The achievement is only possible with standalone 5G architecture (SA) and is just the latest in a series of important SA 5G milestones for T-Mobile. The carrier said it was the first in the world to launch a nationwide SA 5G network nearly two years ago. The carrier began lighting up Voice over 5G (VoNR) this month so that all services can run on 5G. By removing the need for an underlying LTE network and 4G core, 5G will be able to reach its true future potential with incredibly fast speeds, real-time responsiveness and massive connectivity, the company mentioned.

NR CA is live in parts of T-Mobile’s network today, combining two 2.5 GHz 5G channels for greater speeds, performance and capacity. Customers with the Samsung Galaxy S22 will be among the first to experience a third 1900 MHz 5G channel later this year. This functionality will expand across the carrier’s network and to additional devices in the near future.

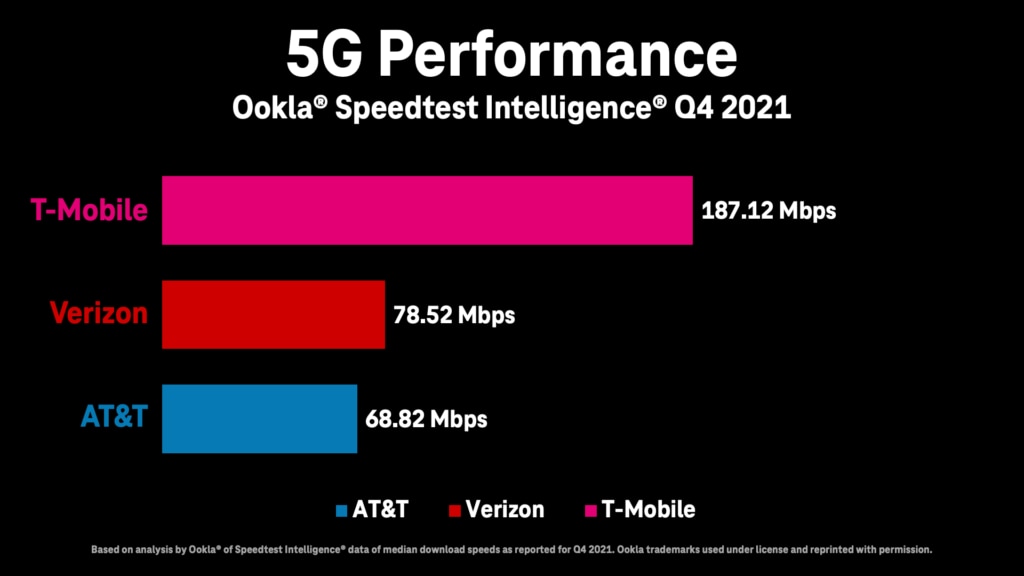

T-Mobile US was the first in the world to launch a nationwide SA 5G network nearly two years ago and has been driving toward a true 5G-only experience for customers ever since. Just this month the Un-carrier began deploying Voice over 5G (VoNR) so ALLvoice services can run on 5G. By removing the need for an underlying 4G LTE network and 4G core, 5G will be able to reach its true future potential with incredibly fast speeds, real-time responsiveness and massive connectivity. The carrier’s 5G network covers 315 million people across 1.8 million square miles. 225 million people nationwide are covered with super-fast Ultra Capacity 5G, and T-Mobile expects to cover 260 million in 2022 and 300 million next year. It also has the fastest 5G network, according to Ookla speed tests in Q4 2021:

Note that neither Verizon or AT&T have deployed 5G SA core networks with no future dates specified.

References:

AT&T CFO sees inflation as main threat, but profits and margins to expand in 2nd half 2022

At the Credit Suisse Communications Conference on Tuesday, AT&T CFO Pascal Desroches said Tuesday that inflation is the issue he is most concerned about, and one that he expects to continue “for the foreseeable future. It’s hard for me to envision that that’s not going to impact the consumer negatively,” Desroches said. “And that we and some others will see some pressure,” he added.

AT&T has already raised prices on some mobile service plans in order to combat the impacts of inflation. The CFO’s comments were made mere weeks after the telecom giant increased the pricing for certain older single-line individual plans by $6 per month or $12 a month for family plans.

Yet Desroches said the company may review its pricing again. AT&T is seeing the impacts of inflation across labor, supplies, energy and transport. Nonetheless, AT&T is expecting to see profit margins expand during the course of the second half of the year, as well as improved profit trends, Desroches added.

Desroches reiterated that AT&T has taken a disciplined approach to growth and investment and made the following points:

- The company continues to grow customer relationships in its strategic focus areas of 5G and fiber. Desroches said the company continues to see healthy consumer demand even with continued expectations that 2022 postpaid wireless industry demand is unlikely to replicate 2021 levels. AT&T continues to successfully attract high-value customers with its consistent, simple go-to-market strategy.

- Desroches remains comfortable that the company can deliver improving postpaid phone ARPU trends in 2022. He noted that postpaid phone ARPU could in fact edge up sequentially in the second quarter.

- Desroches also reiterated expectations for gradual improvement in year-over-year mobility EBITDA trends through the course of 2022. Following a more pronounced impact in the second quarter, the revenue and EBITDA impacts of the previously announced 3G network shutdown and the absence of approximately $100 million in CAF II and FirstNet related reimbursements are expected to be more than mitigated in the back half of year by organic service revenue growth and the lapping of 3G shutdown costs comparisons in the second half of 2021.

- AT&T’s fiber build progress continues with expectations to achieve 30+ million customer locations by 2025. Desroches noted that AT&T is acquiring new customers and seeing strong penetration rates thanks to a straightforward go-to-market approach.

- Desroches shared that the company continues to work with state and local government municipalities across the country to provide affordable broadband connectivity to low-income customers through the Affordable Connectivity Program. Over time, the company believes these efforts can help provide internet for all Americans and expand the total addressable market for broadband access. Additionally, Desroches indicated that any federal funding in support of the company’s fiber buildout would be deployed to expand its network to additional customer locations, representing potential upside above AT&T’s existing guidance.

- AT&T continues to work through its business wireline portfolio rationalization process and focus its efforts on core transport and connectivity solutions. Desroches noted that the company has yet to see a recovery in government sector demand trends which impacted the business during the first quarter.

- With regard to the macroeconomic environment, Desroches said that the company considered a higher-than-typical level of inflation when setting 2022 budget. The company’s recent pricing increases were a response to higher-than-expected inflation trends. Additionally, the company has opportunities to address the impacts of inflation with its ongoing cost savings initiative, which is expected to reach a run rate of $4+ billion by the end of this year.

- Desroches stated the company feels good about its financial flexibility, does not plan to issue any debt in the near-term and remains focused on its goal of achieving a net debt-to-adjusted EBITDA ratio in the 2.5x range by the end of 2023.

References:

https://about.att.com/story/2022/pascal-desroches-webcast-summary-june-14.html

https://www.barrons.com/articles/att-prices-inflation-51655220258

New broadcast TV standard ATSC 3.0 “Next Gen TV” to cover 82% of U.S. households by end of 2022

Pearl TV, a consortium of U.S. broadcasters operating more than 820 TV stations, said that it is making progress with hardware and software that wants to accelerate the rollout and adoption of ATSC 3.0, the new broadcast TV signaling standard that’s been branded as “NextGen TV.” ATSC 3.0 has been in the works for many years, but only now seems to be gaining a wide following.

Pearl TV has collaborated with Taiwan wireless telecom semiconductor company MediaTek on a reference design for smart TVs and other devices that support the new standard. On the software front, the consortium has formally introduced RUN3TV, a web-based platform that enables broadcasters to deliver interactive and on-demand apps and services over ATSC 3.0.

The new IP-based standard – which supports 4K video, enhanced audio and interactive apps – are expected to take center stage. Pearl TV’s members include Cox Media Group, the E.W. Scripps Company, Graham Media Group, Hearst Television, Nexstar Media Group, Gray Television, Sinclair Broadcast Group and Tegna.

Sinclair Broadcast Group and USSI Global said they will partner to offer the nation’s first commercial datacasting service using the NextGen Broadcast standard (ATSC 3.0). The pilot program will deliver local content, advertising, and data files to the rapidly growing Electric Vehicle Charging station market.

The ATSC 3.0 reference design – billed as the “FastTrack to NextGen TV” platform – includes a TV system-on-chip (SoC), ATSC 3.0 demodulators and a software stack. It will be pre-certified for compliance with the Consumer Technology Association’s (CTA’s) NextGen TV logo requirements, A3SA security (which uses IP-based encryption protocols, device certificates and rights management technology) and the RUN3TV application platform.

It’s hoped that the ATSC 3.0 reference design will open up the market for lower-cost ASTC 3.0-based TVs and drive more volume into the NextGen TV ecosystem. MediaTek already provides TV SoCs to about 90% of all TV brands, according to Pearl TV and MediaTek. The program stems from a partnership between them announced in January 2022. CTA expects NextGen TV sales to double this year, rise by 75% in 2023 and then double again in 2024.

About 70 TV models from Samsung, Sony and LG Electronics support ASTC 3.0 today, with Hisense on deck to build sets that utilize the new standard. More than 100 TV models are expected to support ATSC 3.0 by later this year, Anne Schelle, managing director of Pearl TV, recently told Light Reading.

The official launch of RUN3TV brings to market a web platform that supports interactive apps delivered via ATSC 3.0, such as targeted advertising, weather widgets, live sports scores, TV-based commerce and enhanced emergency alerts. It is arriving on the scene as the deployment of the new standard reaches about 60 markets.

Pearl TV is launching the RUN3TV platform through a subsidiary, ATSC 3.0 Framework Alliance LLC, with development partners that include Kineton, MadHive, IBM Weather, Freewheel (the Comcast-owned ad-tech company) and Google. Gray Television.

The E.W. Scripps Company, Graham Media, Tegna, Hearst and Howard University’s WHUT are among the platform’s early adopters.

“With NextGen TV and RUN3TV, broadcasters can now bring the OTA environment into the digital world,” Schelle said in a statement.

The reference design and interactive platform are coming together amid an ongoing expansion of ATSC 3.0. It’s expected that NextGen TV will cover about 82% of all U.S. households by the end of 2022. Large markets set for launches later this year include Boston, New York, Philadelphia, Chicago and Miami.

References: