AT&T tests “5G” transmission on mid band (sub 6GHz) and later low band (700MHz) spectrum

AT&T plans to test “5G” transmission equipment in the 4400 MHz to 5000 MHz band in Austin, Texas, having received an experimental license from the FCC.

The 4400MHz to 5000MHz band is known as the n79 band in 3GPP Release 15 “5G New Radio (NR)” specification [1.]. It is also part of the C-Band in the US.

Note 1. 3GPP completed Release 15 “5G NR” specifications in June 2018. Together with 3GPP final NR specifications in Release 16, they will be submitted for consideration as an IMT 2020 Radio Interface Technology (RIT) at a future ITU-R WP5D meeting. Release 16 is now scheduled for completion during the first half of 2020. It will (hopefully) specify ultra low latency, ultra high reliability operation in the data plane- an important use case for 5G/ IMT 2020.

…………………………………………………………………………………………………

AT&T is running mobile tests between the beginning of June and the beginning of September this year. AT&T says that those tests will operate “within 20 meters radius of base.”

“AT&T seeks to further validate system design and operation in the sub-6 GHz band for certain applications and use cases such as IAB (Integrated Access and Backhaul), LNC (LTE-NR Coexistence), V2X (Vehicle to vehicle/others), URLLC (Ultra-Reliable Low Latency Communication), mMTC (massive Machine Type Communications), and eMBB (enhanced Mobile BroadBand),” wrote AT&T’s David Wolter in the company’s application for the FCC license.

“We wouldn’t be able to share info beyond that in the license app,” an AT&T spokeswoman told Light Reading.

AT&T is scheduled to start its rollout of 5G on low-band spectrum next year, probably on the 700MHz band.

This week, the company announced a successful sub-6GHz spectrum transmission field test in in Plano, TX. However, the actual frequencies used were not disclosed.

After making our first data transfer over Sub-6GHz spectrum in the field this week, AT&T is a step closer to introducing 5G over sub-6 spectrum, with plans to offer nationwide 5G in the first half of 2020. This milestone connection was made in Plano, Texas using a Qualcomm Technologies smartphone form factor test device powered by a Qualcomm® Snapdragon™ 5G modem, RF transceiver and RF Front-End (RFFE) solution. Moving this connectivity from the Lab to the field marks significant progress toward our plans to offer 5G to customers across the country. We also remain on track to offer our first smartphone capable of accessing 5G over low-band spectrum as early as this year.

The mega telco and media giant is currently running some of its 5G networks in 21 cities on its 39GHz millimeter wave system for businesses and selected developers. Compared with low-band, these millimeter wave networks offer blazing speeds (1 Gbit/s), but much lower coverage ranges (1,000 to 2,000 feet). Hence, they will require many more small cells for any given geographical area.

AT&T plans to offer nationwide 5G running on low-band spectrum in the first half of 2020. The operator is expected to use 700MHz spectrum, alongside its FirstNet 4G 700MHz deployment, but could rely on other frequencies as well. AT&T has also been involved in discussions about using the C-Band, largely in the 3.7GHz to 4.2GHz ranges, for 5G.

………………………………………………………………………………………………………

Addendum: Frequency Bands for IMT 2020

SK Telecom Launches 5G AR and VR Services for eSports

SK Telecom today announced the launch of three 5G AR and VR services – ‘Jump AR’, ‘LCK* VR Live Broadcasting’ and ‘VR Replay’ – to offer a more realistic and immersive experience when watching eSports games.

‘Jump AR’ is an augmented reality service that teleports users to an eSports stadium, LoL Park, through their smartphone screens. When accessing the ‘Jump AR’ app, a ‘virtual portal’ to LoL Park in Seoul appears on the screen. If users take a few steps towards the virtual portal, they are transported to the virtual LoL Park.

By moving their smartphones around, users can get a 360-degree view of LoL Park’s interior, leave AR messages of support, watch greeting videos of players, and also read messages left by other eSports fans.

SK Telecom applied a hyper-immersive space platform and real-time tracking technology to allow users to freely navigate the virtual LoL Park. Users can also take fan selfies through 3D facial recognition and realistic AR rendering technologies.

LCK VR Live Broadcasting’ allows users to watch eSports players close-up through the 360-degree VR cameras installed in LoL Park while enjoying the cheers from actual audience in real time.

‘VR Replay’ is a new eSports video content that provides highlights from the perspective of characters in the game. By wearing VR headsets, users can watch 360-degree battle scenes from characters’ point of view. SK Telecom applied an advanced technology that combines separate scenes into a 360-degree video content.

The company provides ‘LCK VR Live Broadcasting’ and ‘VR Replay’ through ‘SKT-5GX’ section of ‘oksusu.’

The esports arena within the LoL Park, set up by Riot Games in Seoul, can seat 400 spectators, but tickets are frequently sold out early, the Korean telecom firm said, noting that its new AR and VR services will allow esports fans to enjoy games anywhere with smartphones if they fail to obtain tickets.

The Jump AR service offers users the experience of being teleported down to the esports arena, providing a 360-degree view.

The VR Replay offers highlight scenes of games from the perspective of game characters. Wearing a VR headset, users can enjoy an immersive viewing experience as if they are in the middle of the battlefield in the games.

The VR on-the-spot live broadcast enables users to watch players at close range through 360-degree VR cameras installed at the esports arena.

“With new 5G immersive technologies, SK Telecom has realized unprecedented eSports broadcasting services and content,” said Jeon Jin-soo, Vice President and Head of 5GX Service Business Division of SK Telecom. “We will continue to develop innovative 5G services to offer immersive experiences for customers.”

Models promote SK Telecom’s AR and VR services designed to offer more immersive viewing experiences for esports fans at LoL Park in Seoul in this photo provided by the mobile carrier, PHOTO Courtesy of SK Telecom

……………………………………………………………………………………………………

About SK Telecom

SK Telecom is the largest mobile operator in Korea with nearly 50 percent of the market share. As the pioneer of all generations of mobile networks, the company has commercialized the fifth generation (5G) network on December 1, 2018 and announced the first 5G smartphone subscribers on April 3, 2019. With its world’s best 5G, SK Telecom is set to realize the Age of Hyper-Innovation by transforming the way customers work, live and play.

Building on its strength in mobile services, the company is also creating unprecedented value in diverse ICT-related markets including media, security and commerce.

For more information, please contact [email protected] or [email protected].

Media Contact

Yong-jae Lee

SK Telecom Co., Ltd.

(822) 6100 3838

Irene Kim

SK Telecom Co., Ltd.

(822) 6100 3867

Ha-young Lee

BCW Korea

(822) 3782 6421

U.S. DoJ in ~$1B Telecom Services Deal With AT&T

Task Order valued at $984 [1.] million over 15 years to help improve mission performance

Note 1. The total value of the Task Order is estimated at $984 million over 15 years if all options are exercised.

…………………………………………………………………………….

AT&T is doing great in the public sector. FirstNet has received many accolades and is world class. On Monday, July 29th, the telecom and media giant announced the $984 million DoJ award as part of the General Services Administration’s $50 billion Enterprise Infrastructure Solutions (EIS), contract.

EIS is set to replace the current governmentwide telecom contract vehicles Networx and WITS-3, both of which will expire within the next three years. Agencies are expected to use that transition as an opportunity to fully modernize their communications infrastructure.

The Justice Department (DoJ) is the third U.S. federal agency to select a company to help modernize all its telecommunications services.

“Through this award, the DoJ will transition to a next-generation communications platform supporting more than 120,000 employees across more than 2,100 locations,” AT&T said in a press release. That work will include incorporating IP voice and other modern communications tools, as well as data and cloud security and other professional services.

“The AT&T solution will provide DoJ the flexibility and protections to meet their requirements as they aim to strike the right balance between needs to access cloud services from multiple providers and ensuring the access is highly secure,” the release states.

“The DOJ and its component organizations do the hard work of protecting the freedoms, rights and safety of all Americans,” said Stacy Schwartz, vice president, AT&T – Public Safety and FirstNet. “We are honored to provide a modern communications platform and capabilities to support the DOJ’s work for the next 15 years.”

The contract covers the entirety of the Justice Department, including 43 component offices and programs; the enterprise wide Joint Cloud Optimized Trusted Internet Connection Service, or JCOTS; and the law enforcement special communications network FirstNet.

The enterprise contract will be the only EIS award to come out of the Justice Department, the agency told Nextgov, though the FBI will be reissuing its separate solicitation “at a later date.”

AT&T is one of three vendors to complete the security review required before beginning work on an EIS contract, along with Verizon and CenturyLink. Six smaller vendors—BT Federal, CoreTech, Granite, Harris, MetTel and MicroTech—have yet to finish their security authorization work with GSA.

Two other agencies have made their EIS awards this summer: the Railroad Retirement Board, which also went with AT&T, and half of NASA’s requirement under a $10.5 million deal with CenturyLink.

Additionally, the DOJ solution includes access to the AT&T mobility network and FirstNet, the nationwide, dedicated communications platform purpose-built for public safety. FirstNet brings public safety a physically separate core network for enhanced security, priority and preemption, no speed limitations anywhere in the country, and Band 14 spectrum for their dedicated use. These services and AT&T’s global network offer DOJ and its component organizations access to highly secure and reliable connectivity, as well as vital communications capabilities when and where they are needed.

To learn more about AT&T Public Sector, go here.

…………………………………………………………………………………………….

References:

https://about.att.com/story/2019/department_of_justice.html

The Mouse that ROARED: Monaco Claims It’s Won the 5G Race!

Monaco Grand Prix inspired the country to win the 5G race, by Digital Trends

Editor’s Note:

With a population of less than 39,000 people, Monaco is a tiny independent city-state on France’s Mediterranean coastline known for its upscale casinos, yacht-lined harbor and prestigious Grand Prix motor race, which runs through Monaco’s streets once a year. Monte-Carlo, its major district, is home to an elegant belle-époque casino complex and ornate Salle Garnier opera house. It also has many luxurious hotels, boutiques, nightclubs and restaurants. I visited the country with my son in the summer of 2003 while attending an ITU standards meeting near Valbonne, France.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Monaco is the first fully 5G-connected country in the world. That means if you have a 5G phone, a 5G connection (and therefore super-fast download speeds) will accompany it anywhere in Monaco. It sounds small, but 5G is rolling out in small areas of select cities around the world, so at the moment it’s impossible to get a complete 5G experience outside of Monaco. What drove the country to adopt the next-gen network so quickly?

“It’s the Grand Prix that brings a sense of urgency to launching 5G in Monaco,” Martin Peronnet, CEO of Monaco Telecom, told Digital Trends in an interview at the company’s headquarters, less than two weeks after its 5G service went live.

Monaco is not your usual country as it’s not very big at all. It’s actually smaller than Central Park in New York, but it’s still home to almost 40,000 people and another 70,000 people come to Monaco to work each day — it’s one of the few places that has more jobs than residents.

While 5G will bring new opportunities to everyone there, it was the annual Formula One Grand Prix that shaped Monaco’s 5G endeavour. It launched on July 10 after two months of hard work — an incredibly fast turnaround — made possible by a vital partnership and meticulous planning. Monaco Telecom worked with Huawei to make its 5G network a reality, and it’s solely powered by the Chinese company’s network infrastructure.

“Monaco is sometimes the busiest place in the world, in terms of mobile usage, and that’s typically during the Grand Prix,” Peronnet said. “It’s really one of the most challenging events to cover with telecommunications. There is so much usage, and each year we continuously rework our network to serve the 50% more usage we get. We knew our 4G network would not be enough in two years time.”

Implementing a 5G network is not easy, but Monaco was prepared and has been at the forefront of some serious mobile tech breakthroughs already — key to 5G’s rollout.

“For the last four years, our strategy has been to be in the leading position for new technologies. We were the first to introduce 450Mbps speeds on 4G, and the first in the world to launch 1Gbps on 4G in 2017. We have done a lot of work to modernize the network,” Peronnet added.

This forethought is important, along with the introduction of tech like 4×4 MIMO (multiple-input multiple-output), and key to Monaco Telecom’s 5G launch going smoothly. Long trials were shunned and the focus was always on the commercial launch. Why the rush? Introducing 5G is essential to make sure everyone in Monaco during future Grand Prix will be able to enjoy a good connection. At least 200,000 people attend the Monaco Grand Prix weekend, and as you’d expect, photos and videos are constantly shared, and the level of activity is only going to increase.

The Grand Prix didn’t just dictate Monaco’s need for 5G — it even dictated when work on deploying the Huawei infrastructure and equipment could start. Astonishingly, work began just two months before the July 10 switch-on, and the final base station was installed only two days before that date.

“We couldn’t work on the network before the end of the 2019 Grand Prix,” Peronnet said. “Because it’s so busy, we cannot touch [the network]. In fact, each year we redesign it to make it Grand Prix-ready, and when it’s all over, it’s put back into its normal configuration.”

This tight time frame was oddly advantageous, because it allowed Monaco Telecom to use the newest Huawei equipment and the latest commercial versions of the 5G technology, which only came along in June. Martin admits all this wouldn’t have been possible in a country any bigger than Monaco. However, there are still 23 sites that needed to be equipped with 5G antennas, and six tons of hardware was used, some of which had to reach some challenging places.

For example, one base station is found on the side of a cliff and accessed by climbers, while another is hidden on top of the old town’s cathedral — which required a crane and serious negotiation with authorities to place. Another antenna is on the Monte Carlo Casino, which was problematic due to specific network interference issues. Remember, all this and a lot more was completed in two months.

To launch a full 5G network so fast required hard work, a strong partnership, and plenty of trust. Peronnet described Monaco Telecom as one of the smallest carriers in the world while pointing out its partner Huawei is one of the biggest mobile technology companies in the world. Yet the two teams worked well together.

“They’re very good on mobile; they’re very reliable, and they like challenges,” he said about Huawei.

Apparently, engineers in both Monaco and China didn’t sleep for a week during the final stages of the project — such was the drive to complete it. “It’s good to know you can rely on the company you need to achieve things with, and it gave us confidence,” he added.

He explained that using only one manufacturer’s equipment is important on a small network like Monaco Telecom, as multiple vendors complicate the process. My interview came on the same day the U.K. announced a continued delay in choosing providers for its own 5G network infrastructure and additionally stated concerns over the availability and reliability of Huawei technology due to the firm’s presence on the Entity List in the U.S.. Was this a concern for Monaco Telecom? “Not on 5G,” he said. “But we are concerned. We are a small country, and we can’t influence the world. Nobody really cares about the decisions Monaco is making, as it doesn’t have a consequence for the rest of the world. We are faced with this uncertainty, and in business you don’t like uncertainty.”

“The main issue isn’t about people spying, it’s about security breaches.” Monaco Telecom takes its network security seriously. Like the U.K., it has a security center that tests infrastructure equipment. “Security applies to all,” he said. “The main issue isn’t about people spying, it’s about security breaches. We’ve been working a lot with the government and Monaco’s security agency to try and define a fortress around our equipment, to monitor individually each piece. This applies not only to Huawei, but all.”

Peronnet was quick to add that Monaco is not breaking new ground using Huawei equipment, which puts security concerns into context. “We’re not making a choice that no-one else has,” he said. “Huawei is the number one network provider in Europe, and Monaco Telecom is not big enough to help it achieve that.”

The launch will make the 2020 race the first 5G Monaco Grand Prix. Does that mean there will be specific 5G-centric plans for the race? Peronnet believes it’s a little too early for that, but is open to doing something.

“If there are some use cases that make the race safer because of 5G, why not?” This would still need the Formula One Association and the Automobile Club of Monaco’s involvement. However, he sees greater advantages coming in 2021.

“By this time there will be roaming agreements between operators, so visitors will be able to roam on 5G,” he said. “The line-up of handsets will be much larger, and the costs will have dropped. The line-up of handsets will be much larger, and the costs will have dropped.” For these reasons, he expects 5G phones to take at least 10% of the traffic during the race weekend, which will also take load away from the 4G network, resulting in a better connected experience at the 2021 Monaco Grand Prix for everyone. How about the network itself? Increasing the density of coverage outside and advancing the indoor coverage is on the agenda.

The 5G network operates on the 3.5GHz bandwidth, making it difficult for the signal to penetrate buildings. “We still have a long way to go in order to provide great indoor coverage with 5G,” Peronnet said. “It will need specific hardware, which is coming, but not ready yet.”

How about the smartphones that receive the 5G signal? Currently, Monaco Telecom offers the Huawei Mate 20 X 5G and the Xiaomi Mi Mix 3 5G smartphones. However, while both are very good devices, Peronnet told me that Monaco adores the iPhone, and inhabitants may be waiting for Apple to enter the 5G race. foxconn china tariffs could make iphone more expensive manufacturing Apple “[It will be] huge. Decisive,” Peronnet said about the potential of a 5G iPhone.

“Monaco is 80% iPhone. When Apple releases a 5G iPhone, 5G in Monaco will skyrocket.” Apple is rumored to launch a 5G iPhone in 2020, so for now the line-up is Android only, but there are no current promotions running to convince people to adopt Android instead. Peronnet believes people should make their own choice, and that feeling at ease with their phone is more important than pushing them to make a switch. While Monaco has early adopters, they are not ones who are keen to test or deal with bugs. This emphasizes the importance of launching a reliable 5G network quickly.

Over the course of an afternoon, evening, and following morning I tested out Monaco Telecom’s 5G network on a Huawei Mate 20 X 5G. The experience displayed the promise we all expect from 5G, but has not always been evident in early tests elsewhere. The speeds were consistently impressive, ranging between 500Mbps to over 1Gbps, but what was most noticeable was the reliability and breadth of coverage.

I walked around Monaco’s main town, taking in the Monte Carlo Casino, the world-famous harbor which becomes the pit lane during the Grand Prix, and up the hill past La Rascasse and towards more residential areas, throughout which the 5G signal remained constant. Each test I performed along the way showed I was getting 5G, rather than 4G speeds with a 5G network indicator on the phone. Although I could only browse and view YouTube videos on the phone, rather than anything more complex, it was seamless, speedy, and a wonderful thing to use. The 5G signal struggled to work indoors, and my hotel only served 4G speeds, but a 5-minute walk saw 5G quickly return.

Not that 4G is a problem in Monaco, and the speeds I achieved still regularly reached 300Mbps. It’s a deeply impressive feat to have 5G coverage like this so quickly, in a challenging environment, and Monaco truly provides the first proper glimpse of the 5G world we have been teased with for several years.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

This article is posted at:

https://www.digitaltrends.com/mobile/5g-in-monaco-with-huawei-interview/

Justice Dept approves the “New T-Mobile” via Sprint merger; Dish Network becomes 4th U.S. wireless carrier with focus on 5G

The Justice Department approved T-Mobile US Inc. ’s merger with Sprint Corp. after the companies agreed to create a new wireless carrier by selling assets to satellite-TV provider Dish Network Corp. The federal approval for T-Mobile and Sprint caps a more than yearlong review of a combination that fell apart twice in the past five years over terms of the deal or fears that the Justice Department would object.

The landmark antitrust agreement seeks to address concerns that the combination of T-Mobile, the nation’s No. 3 carrier by subscribers, and No. 4 Sprint will drive up prices for consumers. It would leave more than 95% of American cellphone customers with the top three U.S. operators.

A deal brokered by the Justice Department will require Dish, which has been sitting on valuable airwaves, to build a 5G network for cellphone customers. To help it get started, T-Mobile will sell Sprint’s prepaid brands to Dish and give access to its network for seven years.

“The remedies set up Dish as a disruptive force in wireless” with the pieces needed for the company to have a cellphone service that is ready to go, Makan Delrahim, the Justice Department’s antitrust chief, said in a news conference.

Critics of the arrangement include a group of state attorneys general that broke with the Justice Department and have filed an antitrust lawsuit seeking to block the more than $26 billion merger. Five states that weren’t part of the lawsuit joined the federal government in the settlement announced Friday.

“Why scramble so much to create a fourth competitor when you already have one?” said Samuel Weinstein, an assistant law professor at the Cardozo School of Law at Yeshiva University who worked previously in the Justice Department’s antitrust unit.

The deal gives Dish Network, a satellite-TV provider, about nine million Sprint prepaid cellphone customers and additional wireless spectrum. Those subscribers, which mostly come from its Boost Mobile business, represent about one-fifth of Sprint’s customer base. Dish’s service, which could keep the Boost brand or take on a new name, would also be able to move from pay-as-you-go plans to postpaid service, which tends to be more profitable.

T-Mobile and Sprint must also give Dish access to at least 20,000 cell sites and hundreds of retail locations. The new T-Mobile must provide “robust access” to its network, the Justice Department said. Please see comments on Dish in the box below this article.

The union of T-Mobile and Sprint, years in the making, would create a wireless company surpassing 90 million U.S. customers, closing the gap with Verizon Communications Inc. and AT&T Inc., which each have roughly 100 million wireless customers. It also would fulfill a long-held goal of Japan’s SoftBank Group Corp., which owns most of Sprint, and Deutsche Telekom AG, which controls T-Mobile.

T-Mobile and Sprint currently use separate frequencies, often requiring different cell towers:

Under the merger:

- Dish rents capacity from the new T-Mobile, creating a new carrier to serve Boost Mobile customers and giving it time to build its own network.

- After seven years, Dish runs its own network using spectrum from its past acquisitions and its own equipment installed on fewer towers.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Federal Communications Commission Chairman Ajit Pai, who had previously backed the deal, said Friday the Justice Department settlement, coupled with T-Mobile and Sprint’s earlier commitments to deploy a nationwide 5G network, will preserve competition and advance U.S. leadership in rolling out next-generation networks.

In its agreement with the government, T-Mobile promised not to raise prices for three years and cover 97% of the U.S. population with 5G service in three years. T-Mobile has been adding millions of customers at the expense of its rivals, pushing unlimited data plans and lower prices than the incumbents. Sprint, despite owning valuable airwaves, has been shedding millions of subscribers and has struggled to be profitable.

T-Mobile surpassed Sprint to become the number three wireless carrier by subscribers and argued the acquisition of the smaller carrier’s airwaves would help speed its deployment of a 5G network so that it could better compete with Verizon and AT&T. U.S. carriers have been battling for customers in the $180 billion wireless voice-and-data market, where growth has slowed now that the companies have rolled out unlimited data plans and most Americans have upgraded to smartphones.

Letitia James, the New York attorney general, said the proposed merger would cause harm to consumers nationwide. “To be clear: The free market should be picking winners and losers, not the government, and not regulators,” she said during a call with reporters. Ms. James said Dish lacks the experience to operate a nationwide mobile network.

Mr. Delrahim said his office will share its settlement with the federal judge overseeing the states’ lawsuit. “Sometimes independent sovereigns do make independent determinations,” he said. A trial is expected later this year. On Friday, T-Mobile and Sprint extended the deadline to close their deal, from July 29 to Nov. 1.

The Justice Department stopped sharing information with the Democratic attorneys general after they decided to file their lawsuit in June without notifying their federal counterparts, Mr. Delrahim said. “That was their choice, not ours,” he said.

…………………………………………………………………………………………..

T-Mobile said it expects to close its Sprint purchase in the second half of this year despite the states’ lawsuit. Under the deal, Dish will pay $1.4 billion for the Sprint customer accounts, most of which come from its Boost prepaid brand, and $3.6 billion three years later to buy Sprint spectrum licenses in the 800-megahertz range, which can travel long distances and cover rural areas.

The new T-Mobile will have the option to lease back part of that spectrum for an additional two years after the airwaves sale closes. The companies have also agreed to negotiate for T-Mobile to lease Dish spectrum in the 600-megahertz range.

Dish is set to start its wireless life with a base of Sprint’s pay-as-you-go customers, though carriers often struggle to keep those so-called prepaid subscribers. More than 4% of Sprint’s prepaid customers choose to drop their service or are disconnected for nonpayment each month, according to company filings.

The deal creates a fake competitor, said Andrew Jay Schwartzman, a lecturer at Georgetown Law, adding that even if Dish builds out its own network it will take years. During that time, the three large carriers will be able to introduce 5G and lock in their subscriber bases, he said.

“Rather than having Sprint as a weak fourth competitor, the combined companies will now face an extremely weak fourth competitor,” Mr. Schwartzman said.

Sprint ended March with nearly $33 billion of net debt on its balance sheet. Even though it had more than 40 million customers, Sprint said during deal negotiations that it was in poor health and wouldn’t be able to launch nationwide 5G service without the merger.

Dish has argued it can build a better network by starting from scratch. Even before he pursued a deal with the Justice Department, Dish Chairman Charlie Ergen said his business could invest capital more efficiently without the burden of old equipment and software holding back its ambitions. Dish hasn’t made public the prices or structure of the wireless plans it will sell.

“These developments are the fulfillment of more than two decades’ worth of work and more than $21 billion in spectrum investments intended to transform Dish into a connectivity company,” Dish CEO Ergen said in a press release. “Taken together, these opportunities will set the stage for our entry as the nation’s fourth facilities-based wireless competitor and accelerate our work to launch the country’s first standalone 5G broadband network.”

Dish says:

The 800 MHz nationwide spectrum adds to Dish’s existing 600 MHz and 700 MHz low-band holdings. The low-band portfolio, well suited for wide geographic coverage and in-building penetration, complements Dish’s AWS-4 and AWS H Block mid-band offerings, which promise high data capacity potential with narrower operating range.

Dish has committed to new buildout schedules associated with the company’s 600 MHz, AWS-4, 700 MHz E Block and AWS H Block licenses. In addition, DISH has committed to deploy 5G Broadband Service utilizing those licenses.

Senior FCC officials said on a call with reporters that they are confident the new carrier under Dish will be viable because the wholesale deal it has struck with the new T-Mobile is more aggressive than any other such arrangement the carrier and Sprint currently have. Its terms give Dish the financial ability to compete in the prepaid market against T-Mobile’s Metro brand, they said. The settlement also included provisions designed to make sure Dish actually builds the promised infrastructure. Among other penalties, Dish agreed to pay the government up to $2.2 billion if it fails to meet its network expansion requirements.

Following the closing of T-Mobile’s merger with Sprint and subsequent integration into the New T-Mobile, DISH will have the option to take on leases for certain cell sites and retail locations that are decommissioned by the New T-Mobile for five years following the closing of the divestiture transaction, subject to any assignment restrictions. The companies have also committed to engage in good faith negotiations regarding the leasing of some or all of DISH’s 600 MHz spectrum to T-Mobile.

The completion of the T-Mobile and Sprint combination remains subject to remaining regulatory approvals and certain other customary closing conditions. T-Mobile and Sprint expect to receive final federal regulatory approval in Q3 2019 and currently anticipate that the merger will be permitted to close in the second half of 2019. Additional information can be found at www.NewTMobile.com.

………………………………………………………………………………………………………………………………………………………………………

Addendum from WSJ Editorial Board July 27, 2019 print edition:

The Justice Dept has rescued Dish Chairman Charlie Ergen from his bet of buying wireless spectrum but keeping it idle. Mr. Ergen loudly opposed the merger, and his reward was the chance to buy Sprint’s pre-paid customers at a bargain price and have access to 20,000 T-Mobile-Sprint cell sites and hundreds of retail locations. But Dish has no experience running a wireless network, and it will take years to build one even as the Big Three invest to gain an edge in 5G wireless…………………………………………………..

A strong third competitor will be good for consumers and 5G deployment in the U.S. The combined company should force Verizon and AT&T to focus on 5G rather than dabbling in content acquisitions like Time Warner. Three strong competitors are better than two.

………………………………………………………………………………….

FCC Comments:

“That’s a real significant win for U.S. leadership in 5G. It’s been my top priority. It’s been a big priority for the Trump administration. And by accelerating 5G build-out through this deal, 99% of Americans are going to see 5G faster,” FCC Commissioner Carr said.

In addition to the Justice Department, FCC Chairman Ajit Pai announced support for the more than $26 billion merger in May. The deal still faces a lawsuit from 13 state attorneys general and the District of Columbia that seeks to block it.

…………………………………………………………………………………..

References:

https://www.t-mobile.com/news/t-mobile-sprint-merger-doj-clearance

https://www.cnbc.com/2019/07/26/dish-network-finally-has-a-plan-for-a-new-wireless-network.html

https://techblog.comsoc.org/2018/08/03/dish-network-on-track-for-5g-build-out-phase1-is-nb-iot/

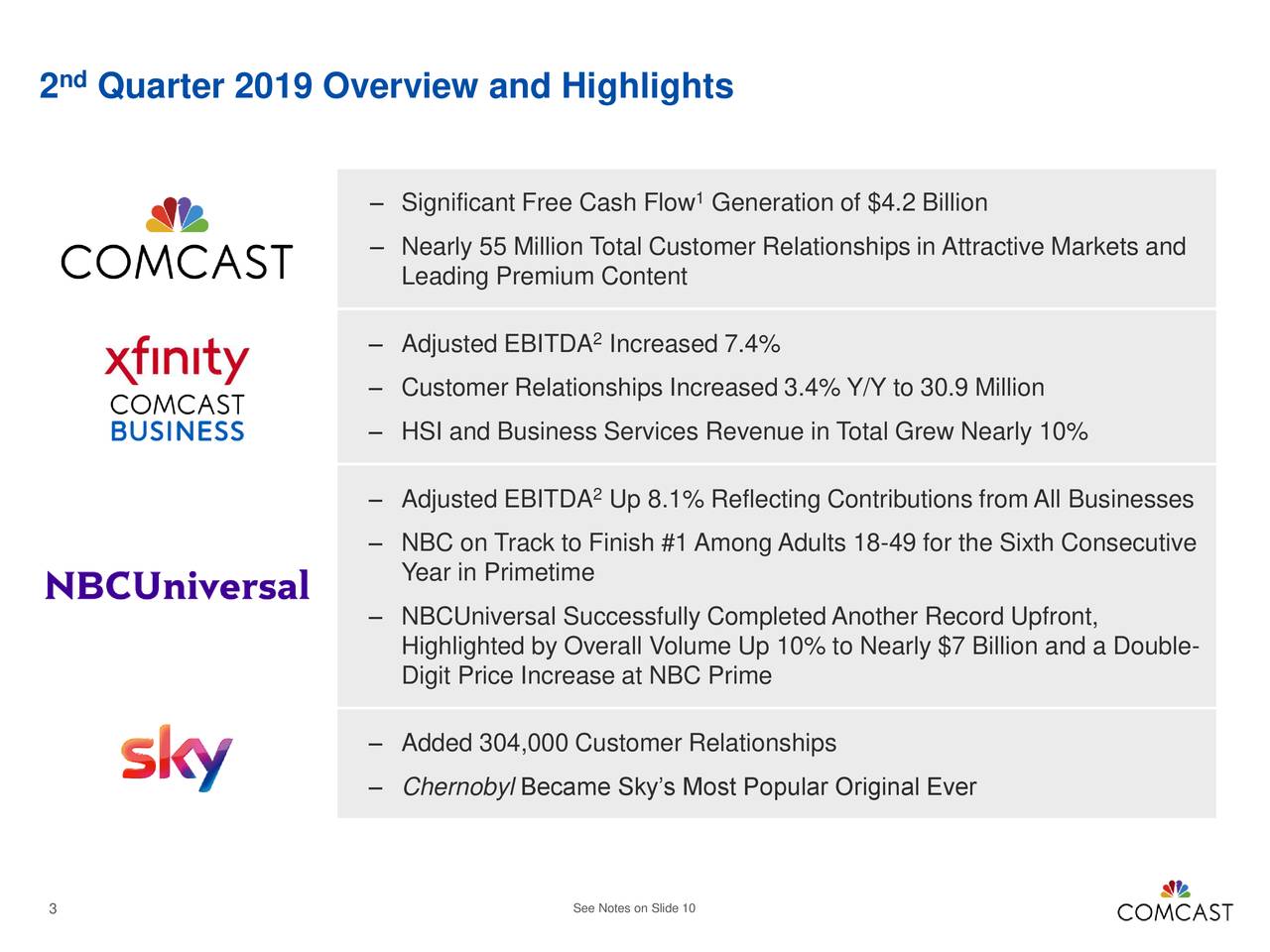

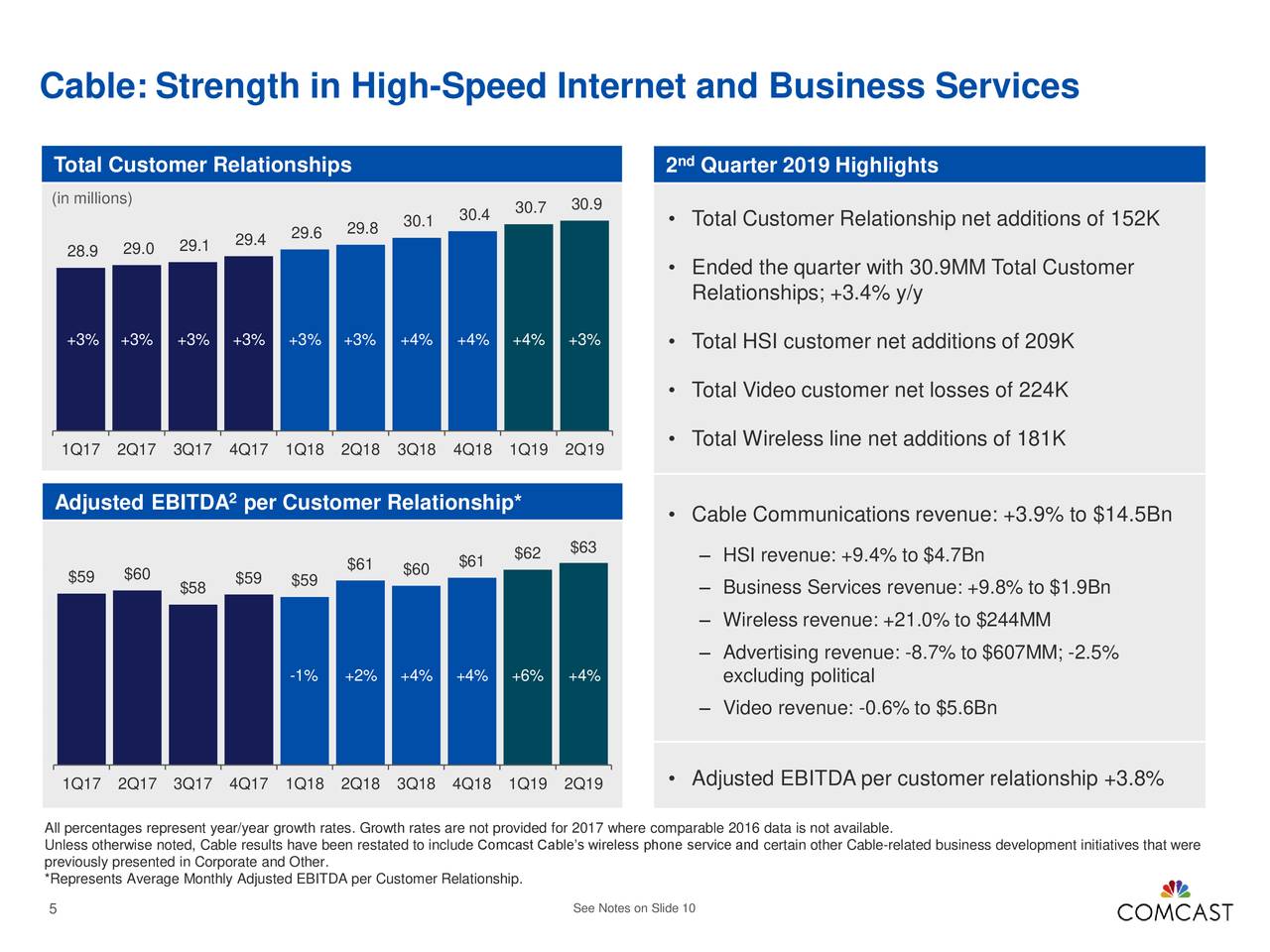

Comcast earnings beat with strong broadband subscriber growth; AT&T is still largest U.S. pay TV provider but bleeds video subs

Despite much higher video subscriber losses than in the past, Comcast generated healthy revenue and profit margin increases in Q2-2019, based on the strength of its performance in the broadband, wireless, business services and other sectors. Comcast, the largest cable and broadband provider in the U.S., reported steady revenue and subscriber gains nearly across the board on July 25th, with the glaring exception of its slumping Xfinity pay-TV business. It also racked up revenue gains in its NBC Universal cable networks, broadcast TV and theme park units, as well as customer revenue gains at its new Sky operation in Europe.

On the pay-TV side, Comcast suffered less collateral damage than most of its peers (e.g. AT&T Direct TV and Direct TV now bled subscribers in the most recent quarter – see Editor’s Note below). The cableco/MSO saw its video subscriber losses increase in the second quarter as cord-cutting by consumers accelerated. The company shed 224,000 video subs (209,000 residential and 15,000 business subs) during the quarter, far worse than its loss of 140,000 subs a year earlier. That reduced its total video base to 21.64 million, maintaining its status as the nation’s second-largest pay-TV provider behind AT&T. Despite these much heftier sub losses, Comcast’s video revenues declined just 0.6% on a year-over-year basis to $5.59 million, thanks to price hikes and subscriber tier upgrades. More importantly from the company’s perspective, video ARPU increased by 1.3%, as the operator, like a growing number of its peers, continues to shift its focus from low-margin to high-margin customers.

…………………………………………………………………………………………………………………………………………………………………………………………………………..

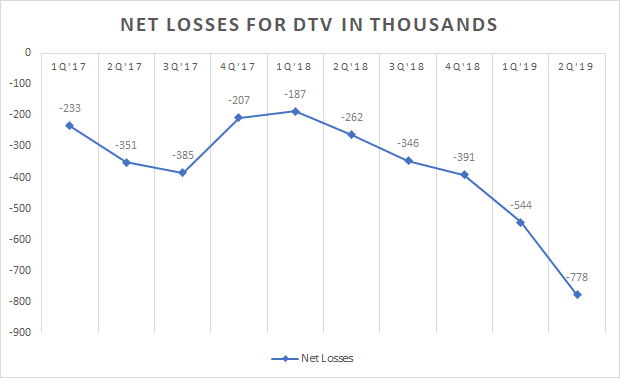

Editor’s Note: The second quarter is typically the worst of the year for pay-TV providers. For example, AT&T lost 778,000 premium TV subscribers in the second quarter, including DirecTV satellite and U-verse television customers – a sharp acceleration in subscriber losses from the 544,000 that cut the cord in Q1-2019. The total number of premium TV video connections fell to 22.9 million, its lowest total since June 30, 2017, when it stood at almost 25.2 million, an overall net loss of 2.3 million.

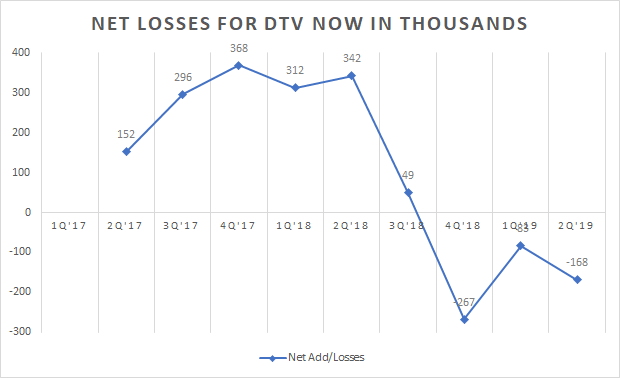

AT&T also lost 168,000 streaming DirecTV Now accounts and AT&T said it expects a similar level of video losses to continue in the current quarter. It’s somewhat surprising that AT&Ts video streaming offering is seeing a mass exodus with the number of subscribers peaking at 1.858 million in September 2018 to 1.34 million now, a decline of more than 500,000.

…………………………………………………………………………………………………………………………………………………………………………………………….

Comcast is by far the largest broadband provider in the U.S. (that’s right- ahead of AT&T, Verizon and CenturyLink). The cableco/MSO added 209,000 new broadband Internet subscribers (182,000 residential and 28,000 business) in the spring quarter, boosting its total broadband base to 27.8 million at the end of June. While that’s down markedly from its gain of 260,000 broadband subs a year earlier, the year-ago total marked the company’s best-ever broadband quarter. Comcast executives stressed that they’re well on their way to their 14th consecutive year of 1 million-plus broadband subscriber increases.

Broadband revenues surged 9.4% to $4.66 billion in the 2nd quarter, due to the impressive increase in broadband subscribers. Residential broadband ARPU (average revue per unit) rose by 4.2% year-over-year, as fewer bundling discounts and subscriber upgrades to higher-priced speed tiers lifted revenues even without price hikes.

“The ARPU is growing, broadband revenue is growing, and it’s margin accretive, so it’s helping the EBITDA growth,” said Comcast Cable President and CEO Dave Watson, in the cableco/MSO’s Q2 earnings call. “So overall, I think we have a solid pipeline for broadband innovation.”

…………………………………………………………………………………………………………………………………………………………………………….

On the wireless front, Comcast’s Xfinity Mobile service continued its steady, if slightly slower, ascent to profitability. The MSO added 181,000 mobile lines in Q2, raising its total to nearly 1.6 million lines. The strong mobile line gains were off from adds of 204,000 lines in the year-ago period but up from adds of 170,000 lines in Q1.

As a result, Comcast’s mobile revenues rose 21.0%, to $244 million. Operating cash flow from Comcast’s mobile business improved as well to $88 million, down substantially from a year earlier, as the new unit edges ever closer to profitability.

Speaking on the company’s earnings call Thursday morning July 25th, Comcast Senior EVP and CFO Mike Cavanagh said Xfinity Mobile is “already positively impacting [customer] retention and attracting new customers” to the company’s cable offerings. He predicted that the mobile unit will start producing positive economic results when penetration rates reach “the mid-to-high single digits.”

…………………………………………………………………………………………………………………………………………………………………………..

Similar to other large North American pay-TV providers that have reported Q2 earnings so far. “We’ll continue to emphasize our approach to this segment,” said Comcast Cable President and CEO Dave Watson. “We’re not going to chase the low end.”

Comcast officials still had no early results to share about Xfinity Flex, a new video streaming product for broadband-only customers that’s powered by the MSO’s cloud-based X1 platform (including the X1 voice-based navigation and search system) and integrated with OTT offerings like Netflix, Amazon Prime Video and YouTube. But executives said more information will come soon.

“It’s an important long-term product,” Watson said Flex on the company’s Q1 earnings call in April, noting it’s early use in a “targeted fashion” to build a broader video relationship with the operator’s broadband-only subs. “We think Internet-delivered video is a good thing for the cable business.”

Also on the streaming video front, Comcast executives revealed a bit more about the forthcoming OTT-delivered video service from the conglomerate’s NBCUniveral (NBCU) unit. Plans call for the OTTP offering, to be based on the existing Now TV platform of Comcast’s Sky service in Europe, to launch in April.

The new ad-supported service mainly will feature acquired movies and TV shows, rather than exclusive originals, at least at first, said NBCU CEO Steve Burke. Despite a market crowded with incumbents like Netflix and Amazon, as well as such new entrants as Disney, WarnerMedia and Apple, Burke is not worried, he said, in a statement.

“Our service is very different from Netflix,” said Burke. “We believe we’ve got some ideas that are innovative and don’t really want to share those until we get right close to launch, but we’re very pleased to have The Office and very optimistic about our streaming plans at this point.”

…………………………………………………………………………………………………………………………………………………………………………..

In a fresh research note issued after the earnings call this morning, Craig Moffett, a principal analyst at MoffettNathanson, gave an approving nod to this strategy:

“As cable operators stop chasing low-value video subscribers, their margins will rise with mix shift, their margins will improve further with improvement in video economics on those that remain; their margins will expand still further as broadband ARPU accelerates (fewer bundled discounts), and their margins will expand still further as their non-programming costs fall as a percentage of revenue. Almost predictably, Comcast raised its cable margin 2019 guidance yet again (now to ‘over’ 100 bps for the year, from previously ‘up to’).”

Comcast Business kept up its steady growth pace of the past decade and a half. With close to 2.4 million commercial “customer relationships,” the cableco boosted its business service take to $1.93 billion in the second quarter, up 9.8% from a year ago. As a result, the company is now on target to approach the $8 billion mark in annual business revenues this year.

References:

http://www.broadbandworldnews.com/author.asp?section_id=472&doc_id=753022&

https://www.cnbc.com/2019/07/25/comcast-q2-2019-earnings.html

https://www.cmcsa.com/financials/earnings

https://seekingalpha.com/article/4277488-t-mass-exodus-continues

IHS Markit: 5G subscribers in Asia and North America set to rise to 1.1 billion by 2023

by Elias Aravantinos, principal analyst, IHS Markit

Introduction:

The rollout of 5G technology will proceed at blistering pace, with the number of subscriptions in Asia and North America set to exceed 1 billion units by the technology’s fifth year of deployment, nearly triple the total for 4G during the same time period.

Starting from a negligible level this year, 5G subscribers in the Asia Pacific and North America regions will soar to 1.1 billion units by 2023. In contrast, 4G’s subscriber base in the two regions amounted to just 417 million units in 2014 five years after that technology’s initial deployment.

Several factors will contribute to 5G’s rapid rise, including the early availability of a large number of compatible devices.

“During 4G’s first year of launch, there were only three smartphones available to consumers that supported the standard,” said Elias Aravantinos, principal analyst at IHS Markit. “On the other hand, 5G boasts at least 20 smartphone designs available for release to the market this year. This demonstrates the high degree of market readiness for 5G, and its capability to attain high volumes more quickly than 4G.”

4G vs 5G subscriptions for 1st five years in North America and Asia

Asia moves to the 5G vanguard:

While North America initially will lead the world in terms of 5G installed base, the Asia-Pacific region will rise rapidly and surpass it in 2021. By 2023, Asia Pacific will have a 5G installed base of 785 million, dwarfing the 294 million total for North America.

“Asia Pacific is destined for 5G market domination thanks to the massive deployment of the technology in China and India,” Aravantinos said. “Led by deployment in these countries, 5G will reach its so-called ‘golden year” in 2023, when 5G will be present in most handsets.”

Handsets make early entrance:

A raft of 5G-enabled smartphones will be introduced or have already been rolled out in 2019. In North America and Asia, 5G phones on the market this year include the Motorola Moto Z3 with the 5G Moto Mod, the Samsung Galaxy S10 5G and the LG V50 5G. In Europe, 5G models will include the Xiaomi Mi Mix 3 5G, the Oppo Reno 5G, the OnePlus 7 Pro and the Huawei Mate 20 X and Mate X.

The future of 5G:

In addition to the ready availability of phones, 5G demand will be stimulated by its compelling capabilities. While today’s 4G phones often require data buffering that slows down performance, 5G smartphones will be able to perform such tasks instantaneously. With today’s 4G LTE service, downloading a high-definition movie might take 10 minutes, but with 5G technology this could take a matter of seconds. In practice, these faster speeds will allow for the seemingly instant transfer of data.

The lower latency of 5G will substantially reduce lag and help improve streaming applications like online gaming, video calling, and interactive live sports experiences, among others.

A comprehensive look at 5G

As network operators and smartphone makers across the globe race to deploy 5G, IHS Markit has launched “5G First Look,” a new service that provides insight into the world of 5G and how 5G networks perform. It includes 5G readiness benchmarks, 5G smartphone teardown analysis, and first-look results from comprehensive, scientific 5G network performance testing in South Korea, the United States, Switzerland and the United Kingdom—with more countries and regions added as 5G networks launch across the globe.

………………………………………………………………………………………………………………………………………………

Editor’s Note:

While IHS Markit says the rollout of 5G is proceeding at a “blistering pace,” it is all a publicity ploy based on 3GPP Rel 15 NR NSA with only enhanced mobile broadband in the data plane. The deployment of standardized 5G hasn’t started yet and won’t until late 2021 at the earliest!

We completely disagree with all of the above forecasts, simply because we really don’t know what the market will be for standardized 5G= IMT 2020 radio and non radio aspects. In our opinion, the key IMT 2020 deliverable will be ultra high reliability with ultra low latency (1 of the 3 agreed upon 5G use cases). That won’t be realized until 3GPP Release 16 has been completed or another RIT/SRIT proposal has been accepted, e.g. Nufront’s (which is different than RIT submitted from China which has advanced to next step).

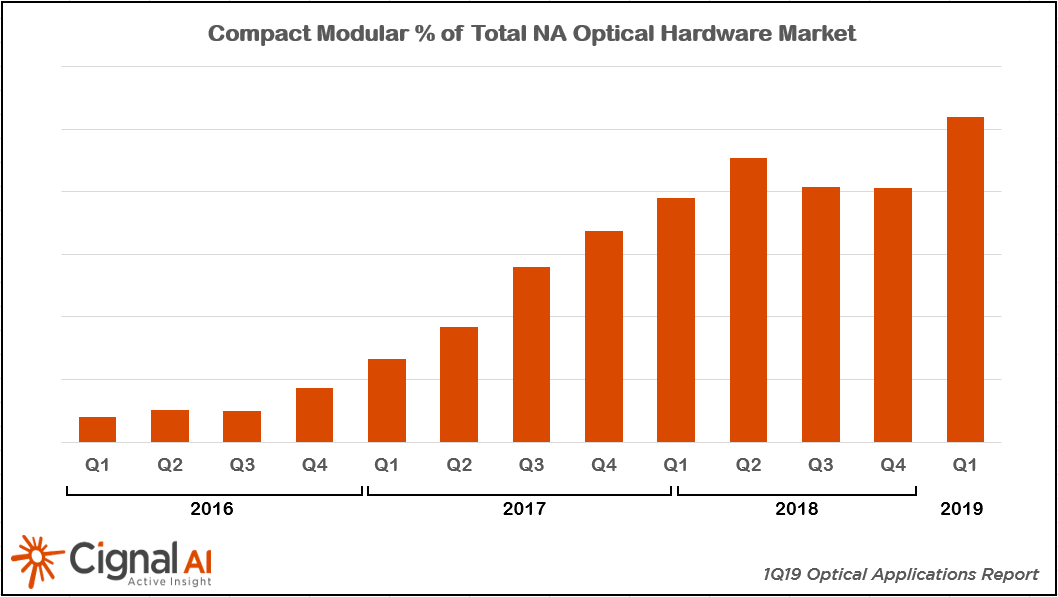

CignalAI: Cloud and Colo Optical Hardware Spending Increases by 50% in North America; Century Link’s impressive fiber buildout

by Cignal AI staff

Overview:

Cloud and colocation (colo) operator spending on optical communications hardware continued to spur market growth in the first quarter of 2019, according to the most recent Optical Customer Markets Report from research firm Cignal AI. Cloud and colo spending increased over 50% in North America, offsetting declines in other regions, with Ciena continuing to lead all sales to cloud operators.

In EMEA, traditional telco (incumbent and wholesale network operators) optical spending recovered and will grow by double digits during 2019. Spending growth by these operators is slowing in APAC as total spending reaches record highs. Huawei continues to lead this market in APAC, EMEA, and CALA, while Ciena leads in North America.

“Optical spending in North America continues to shift from traditional telco providers to the cloud and colo operators,” said Scott Wilkinson, Lead Analyst for Optical Hardware at Cignal AI. “Despite traditional telco operators accounting for most spending, the rapid growth in cloud spending combined with traditional operators now adopting cloud architectures has permanently changed supplier R&D priorities.”

The Cignal AI Optical Customer Markets Report is issued quarterly and quantifies optical equipment sales to five key customer markets: Incumbent, Wholesale, Cloud and Colo, Cable/MSO, and Enterprise and Government.

The latest report is now enhanced and includes optical equipment vendor market share for all customer markets as well as updated forecasts through 2023.

Additional findings in the 1Q19 Optical Customer Markets Report include:

- Ciena Waveserver Ai market share continues to increase as cloud & colo spending grows. New compact modular platforms targeted at this market are entering the market in 2Q19 with Cisco, Infinera, and Nokia among those expecting stronger sales in the next quarter.

- North American cable/MSO spending declined in the first quarter. However, moderate growth is still expected in 2019.

- Enterprise and Government spending shows pressure from consolidation and Cloud and Colo encroachment and isn’t expected to recover in the next two years.

About the Optical Customer Markets Report:

The Cignal AI Optical Customer Markets Report tracks optical equipment spending by end customer market type. It provides forecasts based on expected spending trends by regional basis. The report includes revenue-based market size and share for all end customer markets across all regions.

Vendors examined include Adtran, ADVA, Ciena, Cisco, ECI, Ekinops, Fiberhome, Fujitsu Networks, Huawei, Infinera, Juniper Networks, Mitsubishi Electric, MRV, NEC, Nokia, Padtec, TE Conn, Tejas Networks, Xtera and ZTE.

………………………………………………………………………………………….

About Cignal AI:

Cignal AI provides active and insightful market research for the networking component and equipment market and the market’s end customers. Our work blends expertise from a variety of disciplines to create a uniquely informed perspective on the evolution of networking communications.

To purchase the report contact: [email protected]

……………………………………………………………………………………………

July 25, 2019 Update-CignalAI comments on Cisco-Acacia:

Two weeks ago, Cisco announced it was acquiring Acacia, a move that could transform the company into a market leader in a new era of pluggable coherent optics and disaggregated networks. Cisco was already a growing customer for Acacia and was poised to be one of the leading consumers of Acacia’s AC1200 module that is now reaching the market. Between Cisco’s previous Luxtera acquisition for short-reach optical technology and its current addition of Acacia for long reach coherent, the company will have deep vertical integration.

| Compact modular optical hardware is being used in more network applications than ever before, driving up sales during the first quarter of 2019 as reported in the latest Optical Applications Report. Worldwide, compact modular hardware sales are tracking to exceed $1 billion in revenue this year. |

………………………………………………………………………………………………………..

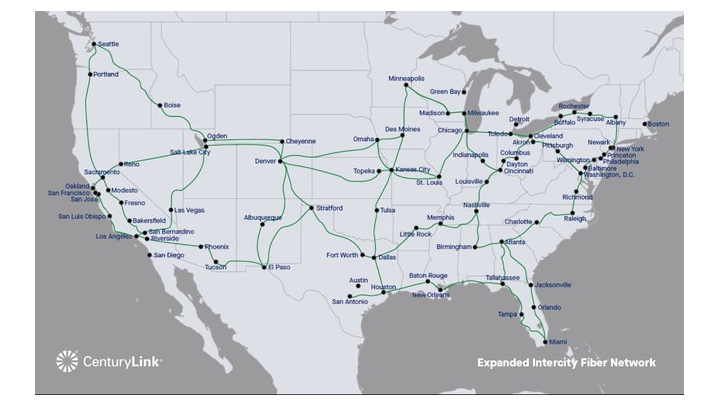

Separately, CenturyLink says it has completed the first of a two-phase build out that will see its fiber-optic networks in the U.S. and Europe grow by 4.7 million fiber miles. The new fiber infrastructure leverages ultra-low-loss fiber from Corning (NYSE: GLW) and will support businesses, government agencies, and other service providers who want access to fiber.

The first phase, completed in June, addressed CenturyLink’s U.S. requirements and connected more than 50 cities via 3.5 million new fiber miles. The European work, slated to finish in the first part of 2021, will see 1.2 million fiber miles installed. Both deployments leverage CenturyLink’s multi-conduit infrastructure, which the company says enables quick and economical fiber deploy and capacity expansion.

CenturyLink’s expanded fiber network connects more than 50 locations in the U.S. Image courtesy of Century Link

……………………………………………………………………………………………………

“Our newly built intercity fiber network, created with the latest optical technology, is another example of how our diverse fiber assets differentiate us from other network providers,” said Andrew Dugan, CenturyLink chief technology officer. “Our multi-conduit infrastructure has a significant amount of capacity for supporting the growing demand for fiber and will allow us to quickly and cost effectively deploy new fiber technology now and in the future. This uniquely positions CenturyLink to meet the needs of companies seeking highly reliable, low-latency network infrastructure designed to move massive amounts of data.”

CenturyLink was able to quickly and cost effectively complete the first phase of the project using multi-conduit infrastructure already in place. The company is currently selling routes to large enterprise companies and content providers in the U.S. and will work with customers to add additional routes as needed.

Key Facts:

- CenturyLink is creating an extensive 4.7-million fiber mile intercity fiber network across the U.S. and parts of Europe.

- The first phase, comprising 3.5 million fiber miles, was completed in June. An additional 1.2 million fiber miles will be added by early 2021.

- CenturyLink is currently selling fiber routes to large enterprise companies and content providers in the U.S.

- Multi-conduit infrastructure allows CenturyLink to quickly and economically deploy new fiber technology or add network capacity as needed.

- The investments in the first phase of the fiber upgrade are included in CenturyLink’s full year 2019 capital expenditure outlook.

- The expanded fiber network utilizes Corning’s SMF-28® ULL fiber and SMF-28® Ultra fiber, creating the largest ultra-low-loss fiber network in North America.

References:

http://news.centurylink.com/2019-07-23-CenturyLink-Expands-Fiber-Network-Across-U-S-and-Europe

Apple in advanced talks to buy Intel’s 5G modem business for $1 billion

The Wall Street Journal reported late yesterday that Apple is in advanced talks to buy Intel’s abandoned smartphone modem business for $1 billion, saying that a deal encompassing patents and staff could be announced as early as next week.

Intel announced this past April it was exiting the 5G (and 4G LTE) modem chip business earlier this year after Apple reached a surprise settlement with Qualcomm that would see Apple once again return to using Qualcomm’s modems in its phones. Intel CEO Bob Swan went on to clarify that Intel had abandoned the modem chip business directly because of the Apple settlement — without Apple as a customer, the company concluded that it “just didn’t see a path” forward.

The deal would give Apple access to engineering work and talent behind Intel’s years long push to develop modem chips for 4G LTE and the crucial next generation of wireless technology known as 5G, potentially saving years of development work. Apple has been working to develop chips to further differentiate its devices as smartphone sales plateau globally, squeezing the iPhone business that has long underpinned its profit. It has hired engineers, including some from Intel, and announced plans for an office of 1,200 employees in San Diego.

For Intel’s part, a deal would allow the company to shed a business that had been weighing on its bottom line: The smartphone operation had been losing about $1 billion annually, a person familiar with its performance has said, and has generally failed to live up to expectations. Though it would exit the smartphone business, Intel plans to continue to work on 5G technology for other connected devices.

Intel and Apple have been in off- and on-again talks for about a year. They broke down around the time Apple reached a multiyear supply agreement for modems with Intel rival Qualcomm Inc., The Wall Street Journal reported in April.

Intel had cast a wider net for buyers then and received expressions of interest from a number of parties, but the talks with Apple—long seen as the most-logical buyer—soon resumed.

Neither Intel or Apple sent a delegate to the recently completed ITU-R WP5D Technology Aspects WG meeting where IMT 2020 RIT/SRIT candidate technologies were progressed.

The Apple-Intel discussions began last summer, around the time former Intel Chief Executive Brian Krzanich resigned, people familiar with the matter have said. Mr. Krzanich championed the modem business and touted 5G technology as a significant future revenue stream. When Bob Swan was named to that job in January, analysts said the odds of a deal rose because his focus on cleaning up Intel would require addressing the losses in the modem business.

Intel is the latest Apple supplier to exit a business after the iPhone maker moved to develop components in-house. Late last year, Apple agreed to a $600 million deal to acquire 300 engineers and facilities from Dialog Semiconductor PLC as the company increasingly develops the battery-management chips Dialog had supplied.

Apple has been reluctant to cut big deals in the past, preferring to acquire about 15 to 20 small companies annually that have technology it can easily integrate. But with the slowdown in its iPhone business, the company has become more open to bigger deals. It has been spending its giant cash reserves on share buybacks and dividends (AKA financial engineering). But the iconic company still has a substantial war chest, with $113 billion of cash after debt as of March 30th. Its largest deal to date remains the $3 billion acquisition of Beats Electronics LLC in 2014.

Here’s a timeline of Intel’s rocky relationship with Apple for the iPhone:

- 2007 — 2016: Qualcomm was Apple’s go-to modem provider.

- 2016 — April 2019: Apple put its arm around Intel, hoping it could offer the same chips as Qualcomm for a lower price.

- April 16, 2019: Apple begrudgingly settled lawsuits with Qualcomm, and agreed to use its chips again for at least 6 years.

- Also April 16, 2019: Since Apple broke up with it, Intel announced it was done with smartphone modems.

Key Takeaways:

After the Apple / Qualcomm deal, Intel reportedly began searching for a buyer for its modem business. Apple makes a lot of sense as a buyer. Prior to Apple and Qualcomm settling, Intel became the sole third-party modem provider for the 2018 models of the iPhone. And Apple has long been Intel’s only major customer for modems — nearly every other major Android phone relies on either Qualcomm or in-house solutions.

If Apple is able to effectively use Intel’s patents, research, and engineers into a functioning 5G chip assembly line, Qualcomm will lose the power it has over the iPhone. If not, there won’t be any competition and Qualcomm will keep charging high prices for 5G chipsets. Qualcomm is the only chip company to date that is able to offer modem chips for 5G phones, so Apple has no choice but to work with them unless it acquires Intel’s 5G modem chip business.

Verizon Software-Defined Interconnect: Private IP network connectivity to Equinix global DC’s

Verizon today announced the launch of Software-Defined Interconnect (SDI), a solution that works with Equinix Cloud Exchange Fabric™ (ECX Fabric™), offering organizations with a Private IP network direct connectivity to 115 Equinix International Business Exchange™ (IBX ®) data centers (DC’s) around the globe within minutes.

Verizon claims its new Private IP service [1] provides a faster, more flexible alternative to traditional interconnectivity, which requires costly buildouts, long lead times, complex provisioning and often truck rolls: APIs are used to automate connections and, often, reduce costs, boasts Verizon. The telco said in a press release:

SDI addresses the longstanding challenges associated with connecting premises networks to colocation data centers. To do this over traditional infrastructure requires costly build-outs, long lead times and complex provisioning. The SDI solution leverages an automated Application Program Interface (API) to quickly and simply integrate pre-provisioned Verizon Private IP bandwidth via ECX Fabric, while eliminating the need for dedicated physical connectivity. The result is to make secure colocation and interconnection faster and easier for customers to implement, often at a significantly lower cost.

Note 1. Private IP is an MPLS-based VPN service that provides a simple network designed to grow with your business and help you consolidate your applications into a single network infrastructure. It gives you dedicated, secure connectivity that helps you adapt to changing demands, so you can deliver a better experience for customers, employees and partners.

Private IP uses Layer 3 networking to connect locations virtually rather than physically. That means you can exchange data among many different sites using Permanent Virtual Connections through a single physical port. Our MPLS-based VPN solution combines the flexibility of IP with the security and reliability of proven network technologies.

……………………………………………………………………………………………………………

“SDI is an addition to our best-in-class software-defined suite of services that can deliver performance ‘at the edge’ and support real-time interactions for our customers,” said Vickie Lonker, vice president of product management and development for Verizon. “Think about how many devices are connected to data centers, the amount of data generated, and then multiply that when 5G becomes ubiquitous. Enabling enterprises to virtually connect to Verizon’s private IP services by coupling our technology with the proven ECX Fabric makes it easy to provision and manage data-intensive network traffic in real time, lifting a key barrier to digital transformation.”

Verizon’s private IP – MPLS network is seeing high double-digit traffic growth year-over-year, and the adoption of colocation services continues to proliferate as more businesses grapple with complex cloud deployments to achieve greater efficiency, flexibility and additional functionality in data management.

“Verizon’s new Software Defined Interconnect addresses one of the leading issues for organizations by improving colocation access. This offer facilitates a reduction in network and connectivity costs for accessing colocation data centers, while promoting agility and innovation for enterprises. This represents a competitive advantage for Verizon as it applies SDN technology to improve interconnecting its Private IP MPLS network globally,” said Courtney Munroe, group vice president at IDC.

“With Software-Defined Interconnect, a key barrier to digital transformation has been lifted. By allowing enterprises to virtually connect to Verizon’s private IP services using the proven ECX Fabric, SDI makes secure colocation and interconnection easier – and more financially viable – to implement than ever before,” said Bill Long, vice president, interconnection services at Equinix [2].

Note 2. Equinix Internet Exchange™ enables networks, content providers and large enterprises to exchange internet traffic through the largest global peering solution across 52 markets.

………………………………………………………………………………………………………

Expert Opinion:

SDI is an incremental addition to Verizon’s overall strategy of interconnecting with other service providers to meet customer needs, as well as virtualizing its network, says Brian Washburn, an analyst at Ovum (owned by Informa as is LightReading and many other market research firms).

“Everything can be dynamic, everything can be made pay-as-you-go, everything can be controlled as a series of virtual resources to push them around the network as you need it, when you need it,” Washburn says.

For Equinix, the Verizon deal builds its gravitational pull. “It pulls in assets and just connects as many things to other things as possible. It is a virtuous circle. The more things they get into their data centers, the more resources they have there, that pulls in more companies to connect to the resources,” Washburn says. Equinix is standardizing its APIs to make interconnections easily.

SDI is similar to CenturyLink Dynamic Connections, which connects enterprises directly to public cloud services. And telcos are building interconnects with each other; for example, AT&T with Colt. “I expect we’ll see more of this sort of automation taking advantage of Equinix APIs,” Washburn says.

Microsoft also provides a virtual WAN service to connect enterprises to Azure. “It’s a different story, but it falls into the broader category of automation between network operators and cloud services,” Washburn said.

…………………………………………………………………………………………………………..

Verizon manages 500,000+ network, hosting, and security devices and 4,000+ networks in 150+ countries. To find out more about how Verizon’s global IP network, managed network services and Software-Defined Interconnect work please visit:

https://enterprise.verizon.com/products/network/connectivity/private-ip/