Fiber to the building

S&P Global Market Intelligence Surveys: Fiber Deployments in U.S. and Europe + AI Infrastructure Causes Market Shift

S&P’s Global Market Intelligence most recent survey showed that 87% of telecom providers in North America and Europe were deploying fiber optics last year, about the same as 2024. That’s according to the firm’s Erik Keith during a webinar hosted June 17th by the Fiber Broadband Association and its president, Gary Bolton. Among the 104 telecom operators surveyed globally, nearly nine out of ten are already using fiber as part of their broadband strategy. On the cable side, more than two-thirds of operators have either deployed fiber-to-the-home or plan to do so.

The Fiber Broadband Association says, “FTTH technology is clearly the “end game” solution for wireline broadband access services, however, the speed and scope of operator migration to full-fiber networks varies widely, depending on factors such as operator roadmaps and competitive landscape conditions.”

- Pervasive Adoption: Among the 104 telecom operators surveyed globally, 87% in North America and Europe utilize or are actively deploying fiber.

- FTTH Dominance: Fiber-to-the-home (FTTH) is widely regarded as the ultimate end-game for wireline broadband, though legacy copper and fixed wireless networks remain a part of some operators’ transition strategies.

- Cable Operator Progress: On the cable side, more than two-thirds of providers have already deployed FTTH or plan to do so as competition intensifies. More than two-thirds of surveyed cable operators have either deployed FTTH or plan to do so in the near future.

- Growing Cable Competition: Fiber overlap now extends across an estimated 75% of the U.S. cable footprint. Because of this, traditional cable operators are experiencing continued broadband subscriber losses and are actively revising their pricing and bundling strategies.

- High Consumer Satisfaction: Consumer surveys show that gigabit-tier fiber subscribers report the highest overall satisfaction rates, while fiber providers—including Verizon, Breezeline, and Frontier—claim the three lowest monthly churn rates in the U.S.

- AI as a Fiber Catalyst: Fiber is increasingly viewed as a dual-use asset capable of supporting both residential users and hyperscalers, as surging artificial intelligence (AI) demands require advanced, high-capacity infrastructure.

……………………………………………………………………………………………………………….

A different S&P Global Market Intelligence report argues that AI infrastructure demand is becoming linked to a larger market shift: constrained energy supply, higher expected earnings for producers and a growing premium for companies that control scarce capacity. For telecom and technology markets, the report adds another layer to the AI infrastructure conversation. The AI buildout is often discussed in terms of chips, models, cloud platforms and data centers. S&P Global Market Intelligence’s analysis suggests the conversation also needs to include energy supply, regional exposure, capex efficiency and the market value of scarce capacity.

……………………………………………………………………………………………………………….

References:

https://www.benton.org/headlines/fiber-breakfast-week-24-fiber-technology-trends

2026 Fiber Connect Keynote: “The Future of Fiber Optics: AI and the Quantum”

Analysis: Fiber Broadband Association (FBA) whitepaper: Upgrading MSO Networks to Fiber to the Home (FTTH): A Technical Perspective

Fiber Broadband Association Middle Mile WG: how to use “Digital Infrastructure Networks” for coordinated fiber backbone investments

Analysis: AT&T 1Q-2026 results: increased fiber penetration, FWA momentum, D2D deals, and mobile/home internet bundles

Fiber Optic Boost: Corning and Meta in multiyear $6 billion deal to accelerate U.S data center buildout

Fiber Optic Networks & Subsea Cable Systems as the foundation for AI and Cloud services

How will fiber and equipment vendors meet the increased demand for fiber optics in 2026 due to AI data center buildouts?

Automating Fiber Testing in the Last Mile: An Experiment from the Field

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

EdgeCore Digital Infrastructure and Zayo bring fiber connectivity to Santa Clara data center

Fiber Connect 2023: Telcos vs Cablecos; fiber symmetric speeds vs. DOCSIS 4.0?

Big Fiber’s $250M financing deal to buildout dark fiber routes for AI Data Center expansion

Executive Summary:

Big Fiber [1.] has secured $250 million in financing from Stonepeak and Caisse de dépôt et placement du Québec (CDPQ) to expand its dark fiber footprint and increase network capacity in response to accelerating hyperscaler and large-scale data center investments in AI-driven workloads.

Note 1. Sunnyvale, CA headquartered Big Fiber was previously known as Bandwidth IG, which was originally established in 2019 as a telecom and dark-fiber infrastructure company. The rebrand to BIG Fiber was announced on May 1, 2025 when the company described it as a shift to better reflect its focus on privately owned, newly constructed dark fiber networks. The company has built privately owned metro dark fiber networks from its inception, primarily in the SF Bay Area and the Greater Portland, OR and Atlanta, GA areas.

BIG Fiber structures its dark fiber portfolio around high‑strand‑count, single‑mode, low‑loss fiber deployed in purpose‑built, underground metro and regional routes, rather than a carrier‑specific “technology” stack of its own. The company’s public materials emphasize:

-

Single‑mode fiber (SMF) for metro and long‑haul connectivity, consistent with standard dark‑fiber infrastructure designed for multi‑wavelength and DWDM‑based upgrades.

-

High‑density, high‑fiber‑count cables in metro corridors (often hundreds of strands) to support dense data‑center and interconnect demand, which is typical of “new‑build” dark‑fiber operators entering AI‑and‑cloud‑centric markets.

-

Point‑to‑point and ring‑style topologies engineered for extreme route diversity (tri‑/quad‑versity) and low latency, rather than a legacy long‑haul backbone that relies on older fiber types or managed wavelengths.

To complement Big Fiber’s dark‑fiber infrastructure; the customer provides the optical PHY layer (e.g., coherent DWDM, 400ZR/ZR+, or other high‑speed optics), which is how dark‑fiber providers typically position their offerings.

–>More about Big Fiber at the end of this article from the company itself.

……………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Proceeds of the facility will be used to refinance existing debt, provide new capital and facilitate the necessary headroom for major fiber optic network expansions already underway. This includes a significant multi-market buildout in Greater Atlanta, adding over 205 route miles and 165,000 fiber miles to BIG Fiber’s existing market-leading footprint.

“Our partnership with Stonepeak Credit and La Caisse marks a pivotal moment in our mission to empower our customers with highly scalable and purpose-built dark fiber solutions,” said Bruce Garrison, CEO of BIG Fiber. “This financing ensures we have the scale to stay ahead of the escalating demand for modernized infrastructure enabling the AI ecosystem and the necessary digital highways for decades to come.”

“BIG Fiber’s infrastructure delivers critical bandwidth to meet the insatiable demand for both data and compute capacity across its key markets,” said Arun Varanasi, Managing Director at Stonepeak Credit. “We are proud to partner with Columbia Capital, SDC Capital Partners, and La Caisse to support the company’s next leg of growth as it positions itself as one of the preeminent dark fiber operators in the country.”

“BIG Fiber is well positioned to meet the growing connectivity needs of enterprises and data centers seeking new, high-quality infrastructure options,” said Jérôme Marquis, Managing Director and Head of Private Credit at La Caisse. “Its resilient business model, underpinned by long-term contracts and strong structural demand, positions the company well for growth. Together with Stonepeak Credit, we’re providing a tailored financing solution that supports the continued buildout of essential digital infrastructure.”

The latest expansion will bring BIG Fiber’s Atlanta and San Francisco Bay Area network capacity to 850 route miles and over 3 million fiber miles. Projects are currently under construction or contract, with phased Ready for Service (RFS) dates expected in early 2027.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………

According to Big Fiber Chief Commercial Officer Patton Lochridge, demand signals are particularly strong in key U.S. metros including the San Francisco Bay Area, Hillsboro, and Atlanta, where new fiber routes are being deployed to support AI-centric data center expansion. “We’re seeing customers require extreme route diversity, often moving toward triversity or quadversity networks to connect metro assets and long-haul routes,” Lochridge said. He added that inference workloads are increasing the demand for dense metro connectivity: “Traditional telecommunications networks are often too congested or lack the latency and loss tolerances required for stringent AI workloads, making purpose-built metro fiber essential.” Lochridge indicated that the majority of the new capital will be directed toward greenfield build-outs and targeted overbuilds of “exhausted legacy telecommunications corridors that need more scale.”

Industry analysts highlight a parallel geographic shift in AI infrastructure deployment. Sterling Perrin, senior principal analyst for optical networks and transport at Omdia, noted that AI campuses are expanding beyond traditional connectivity hubs such as Ashburn, Dallas, and Northern California into power-advantaged regions including West Texas, Ohio, Tennessee, Louisiana, and Georgia. “They all require massive fiber optic connectivity,” Perrin said.

Power availability is emerging as a primary constraint shaping network topology. Ron Westfall, vice president and analyst at HyperFrame Research, emphasized that grid limitations are driving hyperscalers toward distributed AI campus architectures interconnected via metro and long-haul dark fiber. “Power grid constraints have forced a material shift toward metro and long-haul dark fiber infrastructure to stitch together distributed regional data center campuses,” Westfall said. “Because this relentless GPU-to-GPU communication demands near-zero latency and unprecedented bandwidth, infrastructure planners are prioritizing the deployment of ultra-high-strand dark fiber corridors that directly link distributed, power-rich data centers.”

AI Workloads Reshape Optical Demand:

AI-driven traffic growth is now materially impacting the optical supply chain. In its April 2026 post-OFC analysis, CRU Group reported that AI-related data center demand “has overtaken traditional telecom as the primary growth engine for optical [fiber] and cable,” contributing to tightening supply conditions for high-fiber-count cables and upstream preform materials.

Despite this surge, the majority of AI traffic remains intra-data-center. Omdia estimates indicate that up to 90% of AI traffic does not exit the facility during GPU cluster operations. However, the emergence of distributed AI architectures is beginning to increase requirements for high-capacity inter-data-center interconnect (DCI).

At the Optica Executive Forum, Cisco SVP and Fellow Rakesh Chopra highlighted the scale differential between AI and conventional traffic profiles. As cited by Perrin, AI “scale-up” traffic within data centers can generate 504 times more traffic than traditional DCI flows, while “scale-out” traffic can produce 56 times DCI bandwidth requirements. “With AI training models at the limits of what can be processed within a data center, distributed AI clusters are inevitable,” Perrin said.

This architectural transition is reflected in NVIDIA’s AI factory designs, which decouple east-west GPU compute traffic from traditional north-south enterprise flows, leveraging low-latency leaf-spine topologies optimized for continuous GPU synchronization.

Westfall further noted that these evolving traffic patterns are fundamentally altering network design assumptions. Operators are increasingly optimizing for persistent machine-to-machine synchronization rather than burst-oriented enterprise traffic models.

Fiber as a Core AI Infrastructure Asset:

The Big Fiber’s latest financing aligns with broader trends in AI infrastructure investment, where capital is being deployed across integrated stacks including energy, land, connectivity, and compute infrastructure. Utilities are expanding transmission capacity, while developers are co-locating generation resources near emerging AI hubs.

Within this context, fiber infrastructure is being revalued based on its strategic proximity to power-rich data center clusters. “Infrastructure monetization is shifting away from historical metrics such as per-megabit pricing toward asset-level valuations built around proximity to power-rich data centers,” Westfall said.

If current deployment trajectories persist, the resulting topology will consist of a dense, high-capacity mesh of metro and long-haul fiber routes interconnecting geographically distributed, power-optimized AI campuses with hyperscale cloud and interconnection ecosystems.

………………………………………………………………………………………………………………………………

About BIG Fiber:

BIG Fiber is a metro dark fiber provider that offers high capacity, strategically placed, dark fiber networks to mission critical data centers, Hyperscalers and enterprises throughout the San Francisco Bay Area, Greater Portland and Greater Atlanta areas. BIG Fiber’s 100% underground network meets critical data needs for enterprises and data centers that require new, quality infrastructure options. BIG Fiber’s San Francisco Bay Area network offers more than 320 route miles and 65 data centers. The Greater Portland network has more than 20 route miles and 15 data centers, and the Greater Atlanta network has more than 550 route miles and 30 data centers. BIG Fiber was founded in 2019 and is headquartered in Sunnyvale, California. Visit www.bigfiber.com to learn more.

………………………………………………………………………………………………………………………………

References:

BIG Fiber Secures $250 Million Financing Led by Stonepeak Credit and La Caisse

Analysis: Fiber Broadband Association (FBA) whitepaper: Upgrading MSO Networks to Fiber to the Home (FTTH): A Technical Perspective

Fiber Broadband Association Middle Mile WG: how to use “Digital Infrastructure Networks” for coordinated fiber backbone investments

Analysis: AT&T 1Q-2026 results: increased fiber penetration, FWA momentum, D2D deals, and mobile/home internet bundles

Fiber Optic Boost: Corning and Meta in multiyear $6 billion deal to accelerate U.S data center buildout

Fiber Optic Networks & Subsea Cable Systems as the foundation for AI and Cloud services

How will fiber and equipment vendors meet the increased demand for fiber optics in 2026 due to AI data center buildouts?

Automating Fiber Testing in the Last Mile: An Experiment from the Field

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

Analysis: Fiber Broadband Association (FBA) whitepaper: Upgrading MSO Networks to Fiber to the Home (FTTH): A Technical Perspective

Executive Summary:

The Fiber Broadband Association (FBA) has published an economic and structural framework for Hybrid Fiber Coax (HFC)-to-Fiber to the Premises (FTTP) [1.] upgrades, viewing that as a ‘strategic imperative’ for cable network operators (MSOs). FBA’s The whitepaper white paper, “Upgrading MSO Networks to Fiber to the Home (FTTH): A Technical Perspective,“ positions fiber as the long-term architectural solution for cable access networks.

The whitepaper evaluates multiple migration paths—including full overbuilds, targeted deployments, and HFC/FTTP coexistence—alongside passive optical network (PON) options and operating models. Economically, the report estimates FTTP operating expenses to be approximately 50% lower than HFC, driven by the elimination of active outside plant components. It outlines deployment options ranging from incremental overlays to full HFC replacement, each with distinct cost-performance trade-offs.

Note 1. Fiber optic access networks (sometimes referred to as fiber-to-the-home—FTTH—or fiber-to-the-premises—FTTP) are built to connect homes and businesses to lightning fast Internet connections. The fiber optic cables that make up these networks are the fastest and most reliable broadband technology and are capable of delivering vastly higher bandwidth than traditional copper wires or wireless. All-fiber networks are directly connected from the central office all the way to a subscriber’s building. There is no other technology along the path except fiber optics.

Fiber optic cables are made up of thin strands of glass that carry information by transmitting pulses of light, which are usually created by lasers. The vibrations are turned on and off very quickly. A single fiber can carry multiple streams of information simultaneously over different wavelengths, or colors, of light, enabling more robust video, Internet, and voice services. Fiber cables are capable of transmitting multi-gigabit Internet speeds compared to the mere megabytes typical of copper connections.

Image Credit: Panther Media GmbH/Alamy Stock Photo

…………………………………………………………………………………………………………………………..

Divergent Cable Operator (MSO) Strategies:

In practice, MSO upgrade strategies remain highly variable, shaped by market competition, plant condition, density, and capital constraints. Most large operators now manage hybrid access portfolios spanning HFC, FTTP, and, in some cases, fixed wireless access (FWA).

Optimum Communications, for example, is deploying FTTP overlays in dense Northeastern markets while relying on DOCSIS 3.1 in rural areas where fiber economics are less favorable.

Comcast and Charter similarly pursue selective FTTP in greenfield and edge-out scenarios but continue to prioritize HFC evolution via DOCSIS 4.0. Both assert that upgraded HFC can deliver symmetrical multi-gigabit services at lower cost. Charter estimates upgrade costs at approximately $100 per home passed (excluding CPE), versus roughly $200 for Comcast. Both operators utilize virtualized CMTS platforms and distributed access architectures (DAA) to support converged HFC/FTTP operations and targeted fiber extensions.

Operational cost differences remain contested. Charter CEO Chris Winfrey characterized the delta as minimal—on the order of one to two dollars per passing—stating, “We’ll take that tradeoff any day.” This reinforces the view that large-scale HFC-to-FTTP overbuilds are unlikely among major incumbents in the near term.

HFC investment also continues. Comcast and Charter are deploying low-latency capabilities based on the IETF Low Latency Low Loss Scalable Throughput (L4S) standard, with Charter already launching in multiple U.S. markets.

Fiber-First Deployments:

Smaller operators are, in some cases, moving more decisively toward FTTP. MCTV, serving approximately 57,000 customers in Ohio and West Virginia, determined that FTTP and DOCSIS 3.1 were cost-comparable and opted for full fiber rebuilds. The operator now passes more than 80% of its footprint with FTTP and has decommissioned roughly two-thirds of its HFC power supplies.

Competitive and Technology Outlook:

The FBA identifies FTTP as the “primary driver” of recent cable subscriber losses, citing “structural limitations” of HFC in symmetry, latency, and scalability “that DOCSIS upgrades can partially address but not fully overcome.” Cable proponents dispute this, pointing to DOCSIS 4.0 and future enhancements.

However, competitive pressure is multi-dimensional. In addition to fiber, FWA is gaining traction, particularly in lower-speed tiers. As a result, operators are increasingly focused on pricing, service bundling, and customer experience, including converged broadband-mobile offerings, rather than peak speeds alone.

On the technology roadmap, CableLabs continues to extend DOCSIS, including exploration of an “operational annex” supporting spectrum up to 3 GHz and downstream rates around 25 Gbit/s, with longer-term targets of 6 GHz and 50 Gbit/s. At the same time, it is expanding work on PON, including coherent PON, reflecting a more access-technology-agnostic posture.

Migration Trajectory:

Some industry veterans align with the FBA’s long-term view. John Chapman has advocated a “fiber-first” strategy, citing projections that access networks may need to support up to 1 Tbit/s by 2040. Rather than abrupt transitions, this approach emphasizes phased migration from HFC to FTTP while leveraging existing infrastructure.

Quotes:

John Chapman, a DOCSIS pioneer and former long-time Cisco Systems engineering exec, suggested last year that the cable industry should adjust its thinking and take a “fiber-first” approach as historical trends indicate that broadband access networks will need to be capable of supporting speeds of 1 Tbit/s by 2040. Rather than doing a quick cutover, he thinks MSO’s should migrate from HFC to FTTP over an extended period. But they should get started now.

“The industry has reached an inflection point between the maturity of DOCSIS and the inevitability of fiber. It’s about coming up with a graceful, pragmatic solution to migrate, to transition from DOCSIS to fiber. And that migration’s going to take 20 years. But we need a strategy that accommodates the two,” he said. “It’s a cultural change.”

Jay Rolls, a former Charter CTO and current CTO of BSP, a company that conducts due diligence on various types of broadband network transactions, also believes that cable operators should be weighing whether FTTP is the right move. His recent analysis suggests that the capital spend on a DOCSIS 4.0 overhaul is comparable to an FTTP rebuild.

“Every network and market is different, but the tipping point is fast arriving where overbuilding fiber makes as much financial sense as upgrading HFC, especially when you consider what comes next,” he said on a Light Reading podcast.

References:

Upgrading MSO Networks to Fiber to the Home (FTTH): A Technical Perspective

https://fiberconnect.fiberbroadband.org/

Fiber Broadband Association Middle Mile WG: how to use “Digital Infrastructure Networks” for coordinated fiber backbone investments

Analysis: AT&T 1Q-2026 results: increased fiber penetration, FWA momentum, D2D deals, and mobile/home internet bundles

Fiber Optic Boost: Corning and Meta in multiyear $6 billion deal to accelerate U.S data center buildout

Fiber Optic Networks & Subsea Cable Systems as the foundation for AI and Cloud services

How will fiber and equipment vendors meet the increased demand for fiber optics in 2026 due to AI data center buildouts?

Automating Fiber Testing in the Last Mile: An Experiment from the Field

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

Analysis: AT&T 1Q-2026 results: increased fiber penetration, FWA momentum, D2D deals, and mobile/home internet bundles

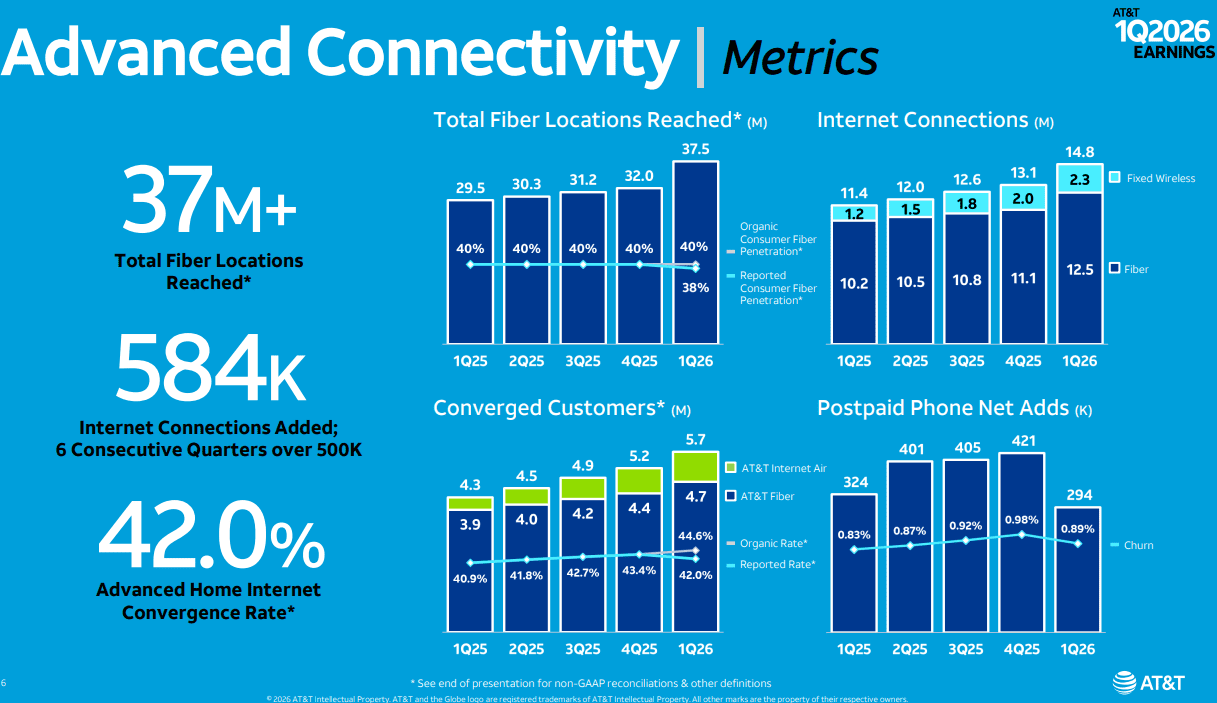

AT&T reported first-quarter results today, achieving its fastest-ever year-over-year organic growth in its advanced connectivity convergence rate, with nearly 45% of advanced home internet subscribers also choosing AT&T wireless. Customers are increasingly purchasing their internet and wireless together from AT&T, highlighting the strength of the company’s differentiated, investment-led strategy to drive converged advanced connectivity at scale.

“We saw our best first quarter ever for Advanced Connectivity internet customer net additions, demonstrating the solid foundation of assets we have built,” said John Stankey, AT&T Chairman and CEO. “We’re uniquely positioned to deliver more of what customers want — fiber and 5G all from one provider on the nation’s largest advanced converged network, backed by the AT&T Guarantee. The actions we’ve taken this quarter are evidence of how we are improving the customer value proposition, scaling faster, and accelerating growth.”

AT&T reported $31.5 billion in consolidated operating revenues, representing a 2.9% year-over-year (YoY) increase and outperforming Street estimates of $31.22 billion. This growth was largely driven by the Advanced Connectivity segment, which generated $22.15 billion in consumer revenues, up from $20.97 billion in the prior-year period.

- Wireless Performance: Mobility services posted mostly flat $16.94 billion in revenue, compared to $16.65 billion in Q1 2025.

- Legacy Decommissioning: Legacy revenues fell 25.3% YoY to $1.8 billion. The aggressive copper-to-fiber migration continues, with 85% of wire centers now approved for legacy service cessation.

- Strategic Sunsetting: 30% of these wire centers are slated for total decommissioning by late 2026, coinciding with the loss of 270,000 DSL subscribers this quarter.

The shift toward high-speed, durable connectivity is evidenced by the growth of AT&T’s Fiber and Fixed Wireless Access (FWA) portfolios.

- Fiber Penetration: AT&T recorded 292,000 fiber net additions, bringing the total subscriber base to 12.5 million. The current passings stand at 37.5 million locations, with 32.7 million owned/operated and 4.8 million via joint ventures (JVs).

- FWA Momentum: AT&T Internet Air added 239,000 customers in the quarter (up from 181,000 in Q1 2025), reaching a total of 1.73 million subscribers.

- Roadmap to 60 Million: AT&T remains on track to reach 60 million fiber locations by 2030 through organic expansion, the Gigapower JV, and open-access agreements.

AT&T is evolving its “NetworkCo” model to optimize capital intensity and market reach.

- Lumen Asset Integration: Recently acquired fiber assets from Lumen will be transferred into a JV structure. CFO Pascal Desroches expects to finalize an agreement with an equity partner for these assets in 2H 2026.

- Convergence and “One Connect”: The “One Connect” platform is the cornerstone of AT&T’s converged strategy.

- Bundle Adoption: 42% of advanced home internet customers (5.68 million) also subscribe to mobile services.

- Fiber-Mobile Synergy: Among fiber-specific customers, the mobility bundle penetration rate is 40.2% (4.74 million).

- The “One Connect” Roadmap: CEO John Stankey views the platform as an iterative engine, beginning with BYOD (Bring Your Own Device) and eventually expanding into tailored family plans.

“We made further progress at positioning AT&T as the preferred provider for connecting consumers and businesses to the internet. We closed our transaction with Lumen, ahead of schedule, adding 1.1 million fiber customers, and over 4 million fiber locations. We’re pleased with the progress we’re making as we integrate these assets in several major metro areas and position the business for faster growth. Early indicators are positive. We now offer fiber services throughout our distribution channels in these areas, which has driven sales activity well above pre-transaction trends. We’re executing the steps to scale engineering, construction and service delivery in the acquired geographies, expected as we move into the back half of the year, will achieve steady improvement in fiber and wireless customer growth in these areas. When we focus on customers needs and invest in the experience and products they want, we find success, and in the first quarter, we gave customers more reasons to choose AT&T. We expanded the AT&T guarantee to cover internet Air and launched a new flagship app to deliver a simple digital-first experience to customers.

We also launched AT&T OneConnect, which enables customers to easily connect all their eligible devices at home and on the go, and eliminates the need to buy internet access twice. We refreshed our Unlimited Your Way plans to deliver more value. All these moves are based on a consistent set of principles that drive our approach to serving customers the way they want to be served, with offers that deliver simplicity, value and choice and converged connectivity.

After years of industry-leading investments in our fiber and wireless network, we believe that we have now established a structural advantage that others will not catch. We reached more than 90 million customer locations across the country with our advanced internet services, over either fiber or 5G. We believe this provides us with more scalable reach and converged connectivity than any of our peers, including a meaningful scale and performance advantage in fiber. This is an advantage we’re growing as we ramp our deployment at a faster pace than anyone else. Today, we reach over 37 million customer locations with fiber, and we’re on track to reach 60 million plus locations by the end of the decade.”

NTNs and D2D:

Regarding its choice of AST SpaceMobile for direct-to-device (D2D) connectivity for its smartphones, Stankey said, “I think it’s natural that we work with LEO partners that have the capabilities to solve that problem, to integrate those offerings into our services,” Stankey said Tuesday on AT&T’s Q1 2026 earnings call. “My goal would be that I have a good, strong wholesale relationship, and it may not just be with one of them. It may be with more than one of them.”

Besides AST SpaceMobile, Stankey said he expects SpaceX/Starlink to have a “robust direct-to-device capability,” as well as Amazon Leo and potentially a fourth NTN satellite internet company. SpaceX is developing a next-generation D2D offering with spectrum it’s acquiring from EchoStar, and Amazon plans to introduce a new D2D offering in 2028 amid its recent deal to acquire Globalstar. AT&T has a deal with Amazon Leo to connect business customers that are out of reach of terrestrial wireless and wireline networks, but it has not yet signed a D2D-specific deal with Amazon’s satellite and services unit.

Market Analysis – The Fiber Coverage Gap:

Despite strong growth, analysts remain cautious regarding AT&T’s convergence ceiling. With fiber currently available in only about 20% of the U.S., the primary concern is whether AT&T can maintain competitive parity in non-fiber regions.

- Potential Underperformance Risk: In markets where AT&T relies on legacy copper or wholesale third-party access, it may struggle to match the churn reduction and ARPU (Average Revenue Per User) lift seen in its “Fiber + Wireless” footprint.

- Mitigation Strategy: The success of the “60-million-locations fiber by 2030” roadmap which is the primary driver of AT&Ts increased spending. Also, the scaling of Internet Air as a “bridge” technology will be critical in preventing regional underperformance.

- 2026 Milestone: AT&T expects to exceed 40 million total fiber locations by the end of 2026.

- Build Cadence: The company is targeting an organic deployment pace of 4 million new locations per year by the end of 2026. After 2026, this rate is projected to increase to approximately 5 million additional spots annually.

- Funding Mechanism: To support this acceleration, AT&T plans to reinvest $3.5 billion in cost savings specifically into the fiber build-out over the 2026–2027 period.

- “There’s no path for AT&T to have a fiber footprint that will cover more than a third of the country. Will AT&T be consigned to losing share in the other two thirds?” MoffettNathanson analyst Craig Moffett asked in a research note to clients posted after AT&T’s earnings call.

Despite the high CapEx, AT&T CFO Pascal Desroches reaffirmed that the company remains on track to deliver $18 billion+ in free cash flow (FCF) for 2026.

………………………………………………………………………………………………………………………………………………………………………

References:

https://www.lightreading.com/satellite/at-t-might-look-beyond-ast-spacemobile-for-d2d

Analysis: AT&T’s $250B network investment to advance U.S. connectivity

AT&T and AWS to deliver last mile connectivity for AI workloads; AT&T Geo Modeler™ AI simulation tool

AT&T and Ericsson boost Cloud RAN performance with AI-native software running on Intel Xeon 6 SoC

AT&T’s convergence strategy is working as per its 3Q 2025 earnings report

AT&T deploys nationwide 5G SA while Verizon lags and T-Mobile leads

AT&T to buy spectrum licenses from EchoStar for $23 billion

AT&T grows fiber revenue 19%, 261K net fiber adds and 29.5M locations passed by its fiber optic network

How will fiber and equipment vendors meet the increased demand for fiber optics in 2026 due to AI data center buildouts?

Fiber optic vendors are employing a mix of manufacturing expansion, technological innovation in high-density and next-generation fibers, and strategic supply chain alignment to meet the anticipated surge in demand from AI and data centers in 2026. The demand is so high that at least one major fiber manufacturer, whose name was not explicitly disclosed in news reports, has already sold all its fiber inventory through 2026. Major fiber optic vendors by category are:

- Fiber & Cable Manufacturing: Corning, Prysmian Group, Sumitomo Electric, Fujikura, CommScope, Sterlite Technologies (STL), Yangtze Optical Fibre & Cable (YOFC)

- Optical Transport/Networking: Nokia, Ciena (gaining share), Cisco, Fujitsu, Huawei, Infinera (now part of Nokia)

- Optical Components/Transceivers: Coherent Corporation, Lumentum, Broadcom, Innolight, Accelink

Major focus areas of selected vendors:

- Corning: Leading in fiber cable quality and innovation

- Nokia & Ciena: Strong in optical transport and network solutions, gaining market share

- Cisco & Huawei: Significant players in optical transceivers, catching up to leaders

- CommScope, Clearfield, STL: Preparing for huge demand surges

John McGirr, SVP and general manager for Corning Optical Fiber & Cable, said, “The surge in hyperscale and AI network loads has significantly increased our expectations for fiber demand. Enterprise sales grew 58% year-over-year in Q3 2025, driven by continued strong adoption of Corning’s Gen AI products, largely due to AI network growth demands. The 72-GPU nodes, such as (Nvidia’s) Blackwell, require 16 times more fiber than traditional cloud switch racks. We see no signs of AI network growth slowing down especially as operators scale up (increase computational power by adding more resources within the existing backend AI network node) and scale out (increase the number of nodes to accommodate increasing demand) their networks.”

Rahul Puri, CEO of the Optical Networking Business at STL, said, “AI-focused data centers require significantly more fiber — about 36x more fiber than traditional CPU-based racks — to handle the massive data volumes and high-speed connectivity required by GPU clusters.” Puri predicts that cumulative hyperscale data capacity will increase by three times in the next few years alone. “The U.S. will need to add 213.3 million more fiber miles by 2029, more than doubling its current amount from 159.6 million fiber miles to 372.9 million miles. Our roadmap is shaped directly with the world’s leading cloud, AI and data center operators,”” Puri added.

CommScope’s VP of Technology John Chamberlain and VP of Hyperscale Cloud Erik Gronvall noted that the company has expanded its fiber manufacturing capacity in recent years to meet increased demand. “We are also innovating to reduce the amount of time it takes to deploy AI clusters,” said Chamberlain and Grovall.

………………………………………………………………………………………………………………………………………………………

Fiber Vendor Strategies:

Capacity Increase: Vendors like Corning and CommScope are investing in increasing their production capacity for fiber optic cables and the necessary preforms (raw material for fiber). This includes expanding existing facilities to help alleviate the current supply chain tightness and long lead times.

Technological Innovation in Fiber Design: To support the extreme bandwidth and low-latency needs of AI, vendors are focusing on advanced fiber technologies.

-

- Higher Fiber Counts: Companies are launching cables with extremely high fiber counts (e.g., 1,728+ strands) and higher density options to pack more capacity into existing infrastructure.

- Next-Generation Fibers: Research is ongoing in areas like hollow-core fiber (which uses air or a vacuum to transmit light faster and with less loss) and multicore fiber (multiple cores in one strand to increase capacity). These technologies, while not yet mainstream for 2026, are part of the long-term strategy.

- Bend-Insensitive Fiber: Innovations in bend-insensitive and ultra-high fiber count cables are improving durability and easing deployment in complex data center environments.

Pre-connectorized and Modular Solutions: To counter a persistent skilled labor shortage and speed up deployment, vendors are pushing factory-terminated, plug-and-play fiber systems and modular platforms (like Siemon’s LightStack). These solutions require less on-site expertise and reduce installation time.

Strategic Partnerships and Supply Chain Alignment: Vendors are forming strategic collaborations with hyperscalers and network operators (like the agreement between Corning and Lumen) to align manufacturing platforms with future demand and ensure supply. They are also working to optimize supply chains and, in some cases, regionalize manufacturing to reduce lead times.

Structured Cabling and Photonics: There is a renewed focus on structured cabling architectures, as recommended by some AI platform providers, to ensure predictable, low-latency performance and simpler long-term management. The industry is also exploring integrated photonics to address the power and thermal challenges of future systems.

Focus on AI-Specific Demands: Vendors recognize that AI data centers require up to five times more connectivity than traditional hyperscaler topologies and network architectures. Their strategies are specifically tailored to high-volume, intra-bay, inter-bay, and middle-mile fiber connections to link distributed data center clusters into a single, unified AI computing environment.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

Ciena and Nokia:

- Ramping up Production: Ciena is accelerating the production of 800G ZR+ optical pluggables, with plans to ship a large volume in 2026 to major cloud providers who are currently testing the technology.

- New Architectures: The company is developing new interconnect solutions under the “Scaleacross” architecture designed to support growing AI workloads by significantly increasing capacity and density within the data center.

- Increased Forecasts: Driven by record orders from hyperscalers, Ciena has raised its revenue guidance for fiscal 2026 to a range of $5.7 billion to $6.1 billion, a significant increase that analysts tie directly to AI-driven demand.

- Strategic Positioning: Ciena emphasizes that the network will be the primary limiter of AI performance by 2026, positioning its high-speed fiber solutions as critical for moving massive amounts of data between compute nodes efficiently.

- Major U.S. Investment: Nokia announced a $4 billion investment in U.S. R&D and manufacturing capabilities for “AI-ready” network technologies, including optical and data center networking, to ensure robust domestic supply.

- Strategic Reorganization: Effective at the start of 2026, Nokia will reorganize into two primary segments, one of which is “Network Infrastructure” (including optical networks), which it sees as the center of the “AI supercycle.”

- Industry Collaboration: Nokia has deepened its commitment to the Open Compute Project (OCP) at the Platinum level, aiming to collaborate on open, interoperable AI networking innovations that optimize space, cost, and power efficiency with standards-driven technology.

- Advocacy for Network Modernization: Nokia’s research highlights that current networks are insufficient for future AI growth, advocating for substantial investment and cross-industry collaboration to modernize digital infrastructure to handle the uplink-heavy, distributed data flows generated by AI.

…………………………………………………………………………………………………………………………………………………………….

References:

https://www.fierce-network.com/broadband/major-fiber-vendors-strategize-huge-demand-ai-2026

https://www.fierce-network.com/premium/research/1410126?pk=FN-Research-Commscope-111925-listing

NTT to launch 25 Gps FTTH service in Tokyo starting March 2026

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

AI infrastructure investments drive demand for Ciena’s products including 800G coherent optics

AT&T sets 1.6 Tbps long distance speed record on its white box based fiber optic network

China Telecom with ZTE demo single-wavelength 1.2T bps hollow-core fiber transmission system over 100T bps

Lumen and Ciena Transmit 1.2 Tbps Wavelength Service Across 3,050 Kilometers

Co-Packaged Optics to play an important role in data center switches

Coherent Optics: Synergistic for telecom, Data Center Interconnect (DCI) and inter-satellite Networks

Hyper Scale Mega Data Centers: Time is NOW for Fiber Optics to the Compute Server

Microsoft acquires Lumenisity – hollow core fiber high speed/low latency leader

China Mobile to deploy 400G QPSK by the end of 2023

NTT to launch 25 Gps FTTH service in Tokyo starting March 2026

NTT East plans to launch a 25 Gbps Fiber-to-the-Home (FTTH) service in Tokyo starting March 2026, according to Telecompaper, The service will offer significantly faster residential broadband, building on their existing fiber services and recent developments in higher-speed business options. Currently, the highest speed Fiber-to-the-Home (FTTH) access plan commercially available in Japan is 10 Gbps offered by multiple fiber optic network providers, including NTT East/West and Sony-backed NURO Hikari.

NTT’s forthcoming Flet Hikari 25G service will be a best-effort FTTH access product, utilizing shared subscriber fiber to connect customers to their chosen Internet Service Providers (ISPs).

The launch is part of NTT’s broader initiative to develop next-generation digital infrastructure, which also includes the development of key devices for an ultrafast optical network under its “Innovative Optical and Wireless Network” (IOWN) project in 2026.

Source: NTT Access Service Systems Laboratories

Separately, researchers in Japan have set world records for internet transmission speeds using experimental fiber optic technology, reaching speeds of over 1 petabit per second (which is over a million gigabits per second) in laboratory settings. These are research achievements and not a commercially available service for everyday use.

References:

https://www.ntt-review.jp/archive/ntttechnical.php?contents=ntr201604fa6.html

https://www.telecompaper.com/news/ntt-east-and-west-launch-10-gbps-service–1538339

NTT’s IOWN provides ultra low latency and energy efficiency in Japan and Hong Kong

NTT Data and Google Cloud partner to offer industry-specific cloud and AI solutions

Sony and NTT (with IOWN) collaborate on remote broadcast production platform

NTT & Yomiuri: ‘Social Order Could Collapse’ in AI Era

UK’s CityFibre launches 5.5Gbit/s wholesale broadband service- 3 times faster than BT Openreach

CityFibre, the UK’s largest independent full fiber optic platform, has unveiled a new 5.5Gbit/s wholesale broadband internet service based on 10Gbit/s XGS-PON technology that has already been rolled out across 85% of the company’s network. CityFibre claims its new product is more than three times faster than the highest rate available service from its much larger rival, Openreach (the network access arm of BT). and available at a much lower wholesale cost, CityFibre’s 5.5Gb symmetrical product will enable partners to offer a range of Multi-Gig speed tiers to customers, improving margins whilst providing a valuable customer retention tool for the long term.

Highlights:

- CityFibre’s new 5500/5500Mbps service offers >3x faster downloads, >45x faster uploads than BT Openreach’s fastest full fibre service which is 1800/120Mbps and is delivered over its GPON network.

- CityFibre’s upgraded XGS-PON network provides numerous benefits over GPON technology, including network cost savings, reduced power consumption, improved performance, and enhanced efficiency.

- CityFibre’s launch of its new Multi-Gig products enables the UK to keep pace with countries including France, the Netherlands, New Zealand and the United States of America where consumers are already making the most of affordable Multi-Gig services.

Photo Credit: CityFibre

Greg Mesch, CEO of CityFibre, said: “The UK’s full fibre future is here, thanks to CityFibre’s powerful, 10Gb XGS-PON network. Our ISP partners are already connecting customers with speeds over 2Gb and exceeding expectations when it comes to quality and reliability, but our next generation of full fibre will set a new standard for what’s possible.

“CityFibre started out to challenge the incumbents and bring choice and competition to the UK market. This is another huge step-forward, giving ISPs more power and flexibility than ever before and bringing affordable Multi-Gig speeds and an unrivalled experience to millions of UK consumers.”

Even faster multi-gig services will be launched in 2026 the company promises.

CityFibre’s network now passes more than 4.3 million premises, which the company says means it is more than halfway along its journey towards its “rollout milestone” of 8 million premises. Actual service take-up, however, has reached just 518,000, an increase of around 181,000 customers on its previous total. During the year covered by the earnings statement, CityFibre announced a partnership with Sky that will see the UK’s second-largest broadband provider launch services on CityFibre’s network later this year.

References:

https://cityfibre.com/news/cityfibre-unveils-new-5-5gb-wholesale-product-its-fastest-ever

Nokia and CityFibre sign 10 year agreement to build 10Gb/second UK broadband network

Dell’Oro: Broadband access equipment sales to increase in 2025 led by XGS-PON deployments

Frontier Communications offers first network-wide symmetrical 5 Gig fiber internet service

Frontier Communications fiber growth accelerates in Q1 2025

AT&T grows fiber revenue 19%, 261K net fiber adds and 29.5M locations passed by its fiber optic network

Google Fiber planning 20 Gig symmetrical service via Nokia’s 25G-PON system

STELLAR Broadband offers 10 Gigabit Symmetrical Fiber Internet Access in Hudsonville, Michigan

Verizon to buy Frontier Communications

Wall Street Journal reported today that Verizon is on the verge of buying Frontier Communications for as much as $7 billion in a deal that would bolster the company’s fiber network to compete with rivals notably AT&T. With a market value of over $7 billion, Dallas, TX based Frontier provides broadband (mostly fiber optic) connections to about three million locations across 25 states. Frontier is in the midst of upgrading its legacy copper landline network to cutting-edge fiber. Rising interest rates sparked fears among investors, however, that the business would run out of cash and not be able to raise more before completing those upgrades. Frontier has a 25-state footprint and serves largely rural areas. It reported sales of $5.8 billion in 2023, with about 52% of total revenue from activities related to its fiber-optic products and bills itself as “largest pure-play fiber internet company in the US.”

An all-cash deal between the two companies could be announced as soon as Thursday, a person familiar with the negotiations told Bloomberg.

Fiber M&A has heated up as telecom companies and financial firms pour capital into neighborhoods that lack high-speed broadband or offer only one internet provider, usually from a cable-TV company. New fiber-optic construction is expensive and time-consuming, making existing broadband providers attractive takeover targets.

Verizon, with a market valuation of around $175 billion, will be under pressure from shareholders to justify any big purchase after the company paid more than $45 billion to secure C-band 5G wireless spectrum licenses and spent billions more to use them. Executives have said they are focused on trimming the telecom giant’s leverage to put it on a firmer financial footing.

Verizon, the top cellphone carrier by subscribers, has faced increased pressure from competitors and from cable-TV companies that offer discounted wireless service backed by Verizon’s own cellular network. Faced with slowing wireless revenue growth and an expensive dividend, Verizon has invested in expanding its home-internet footprint. It has both 5G fixed wireless access (FWA) and its Fios-branded fiber to the premises network.

T-Mobile is the only major U.S. cellphone carrier that lacks a large landline business. Since its 2020 takeover of rival carrier Sprint, the company has focused on 5G dominance and succeeded in growing its cellphone business faster than rivals. That network has also linked millions of customers to its fixed 5G broadband service, which offers cablelike service over the air. T-Mobile’s strategy has shifted in recent months, however, as the company dabbles in partnerships and wholesale leasing agreements with companies that build fiber lines to homes and businesses. The wireless “un-carrier” in July agreed to spend about $4.9 billion through a joint venture with private-equity giant KKR to buy Metronet, a Midwestern broadband provider.

Photo Credit: Jeenah Moon/Bloomberg News

…………………………………………………………………………………………………………………………………………………………

A deal for Frontier would be a round trip of sorts for some of the network infrastructure that Frontier bought from Verizon in 2016 for $10.54 billion in cash. Frontier later filed for Chapter 11 bankruptcy in April 2020 as it burned through cash and was burdened by a heavy debt load. It emerged as a leaner business in 2021 with about $11 billion less debt and focused on building a next-generation fiber optic network.

Frontier’s biggest investors today include private-equity firms Ares Management and Cerberus Capital Management. The company drew the attention of activist Jana Partners last year, which built a stake in the business. Jana delivered a letter to Frontier’s board late last year asking the company to take steps immediately to help reverse its sinking share price, including a possible outright sale.

…………………………………………………………………………………………………………………………………………………………..

AT&T has focused on expanding its fiber network since spinning off its WarnerMedia assets in 2022 to Warner Brothers Discovery. AT&T has 27.8 million fiber homes/businesses passed, growing at ~2.4 million per year, plus more locations passed via its Gigapower joint venture. AT&T’s fiber internet business is expected to contribute to an increase in consumer broadband and wireline revenue. AT&T expects broadband revenue to increase by at least 7% in 2024, which is more than double the rate of growth for wireless service revenue. In contrast, Verizon only has about 18 million fiber locations, growing at about 500,000 per year.

Other recent deals in the fiber transport market sector include the $3.1 billion acquisition, including debt, of fiber provider Consolidated Communications in late 2023 by Searchlight Capital Partners and British Columbia Investment Management.

………………………………………………………………………………………………………………………………………………………….

It’s All About Convergence (fiber based home internet combined with mobile service):

Speaking at a Bank of America investors conference today, Verizon’s CEO for the Consumer Group Sowmyanarayan Sampath said when Verizon bundles Fios with wireless, it sees a 50% reduction in mobile churn and a 40% reduction in broadband churn. He said they don’t see the same benefits with FWA. Sampath was scheduled to speak at the Mobile Future Forward conference tomorrow, but he canceled at the last minute, which may be a sign that this deal for Frontier is imminent.

The analysts at New Street Research led by Jonathan Chaplin said Verizon’s rationale for the purchase is “convergence baby.” They wrote, wrote, “Verizon seemed complacent. No longer.” Indeed, Verizon CEO Hans Vestberg was challenged on the company’s second quarter 2024 earnings call by analysts who questioned whether Verizon had a big enough fiber footprint to compete in the future. The New Street analysts said Sampath’s comments today “marked a shift in rhetoric from: ‘convergence is important, but we can do it with FWA.”

The analysts at New Street wrote today, “We have been arguing for a couple of years that all the fiber assets would eventually be rolled up into the three big national carriers (AT&T, Verizon, T-Mobile). We always knew that if one carrier started the process, others would have to follow swiftly because there are three wireless carriers and only one fiber asset in every market with a fiber asset.”

Other potential fiber companies that the big three national carriers might be eyeing include Google Fiber, Windstream, Stealth Communications and TDS Telecom.

After its annual summer conference in August in Boulder, Colorado, the analysts at TD Cowen, led by Michael Elias, said there was a lot of conversation about the wireline-wireless “convergence” frenzy. “We believe convergence is a race to the bottom, but if one player is going in with a slight advantage (AT&T), the others must reluctantly follow,” wrote TD Cowen. In the mid-term they speculated that T-Mobile might look at fiber roll-ups with Ziply or Lumen (formerly or other regional players.

References:

https://www.wsj.com/business/deals/verizon-nearing-deal-for-frontier-communications-9e402bb4

https://www.fierce-network.com/broadband/verizon-rumored-buy-frontier-its-convergence-game

https://finance.yahoo.com/news/verizon-talks-buy-frontier-communications-180419091.html

https://videos.frontier.com/detail/videos/internet/video/6322692427112/why-fiber

Building out Frontier Communications fiber network via $1.05 B securitized debt offering

Fiber builds propels Frontier Communication’s record 4th Quarter; unveils Fiber Innovation Labs

Frontier Communications fiber build-out boom continues: record number of fiber subscribers added in the 1st quarter of 2023

Frontier’s Big Fiber Build-Out Continued in Q3-2022 with 351,000 fiber optic premises added

AT&T and BlackRock’s Gigapower fiber JV may alter the U.S. broadband landscape

AT&T Highlights: 5G mid-band spectrum, AT&T Fiber, Gigapower joint venture with BlackRock/disaggregation traffic milestone

AT&T to use Frontier’s fiber infrastructure for 4G/5G backhaul in 25 states

Frontier Communications offers first network-wide symmetrical 5 Gig fiber internet service

Frontier Communications adds record fiber broadband customers in Q4 2022

Verizon Q2-2024: strong wireless service revenue and broadband subscriber growth, but consumer FWA lags

Summary of Verizon Consumer, FWA & Business Segment 1Q-2024 results

U.S. fiber rollouts now pass ~52% of homes and businesses but are still far behind HFC

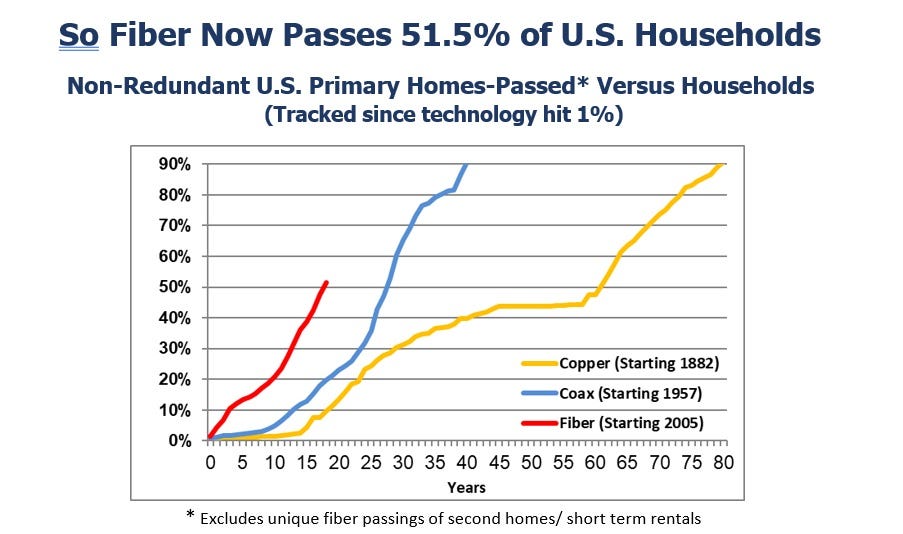

Fiber optic network deployments have reached a milestone as they now pass more than 50% of U.S. households, according to recent report from the Fiber Broadband Association (FBA) [1.] and RVA Market Research and Consulting. Fiber broadband deployment set a new historical record in 2023, passing nine million new homes at a growth rate of 13% year-over-year. The 2023 North America Fiber Provider Survey, sponsored by the FBA, concluded that 77.9 million U.S. homes were passed with fiber, with nearly 52% of all the nation’s unique homes and businesses passed.

Note 1. The FBA is an all-fiber trade association that provides resources, education, and advocacy for companies, organizations, and communities that want to deploy fiber networks. The FBA’s goal is to raise awareness and provide education about the fiber deployment process, safe worksites, and effective fiber installs.

Image Credit: The Fiber Broadband Association (FBA)

………………………………………………………………………………………………………………………………………………………………………………………….

The last $10 billion U.S. Treasury American Rescue Plan (ARP) funding for infrastructure projects such as broadband networks is being distributed this year. The $42.5 billion in NTIA BEAD funding available over the next few years will significantly contribute to enabling and upgrading communities across America with the high-speed, low-latency broadband necessary for participation in today’s 21st-century society. We are seeing a steady stream of NTIA approvals and expect the first states to make BEAD awards in the second half of 2024.

Here’s how the growth of fiber has risen in recent years compared to coax cable (or hybrid fiber/coax, HFC) and the long history of copper.

“Thanks to this latest surge, fiber lines now pass nearly 78 million U.S. homes, up 13% from a year ago,” Alan Breznick, Heavy Reading analyst and the cable/video practice leader at Light Reading, explained in recorded opening remarks here at Light Reading’s 17th’s annual Cable Next-Gen event. Almost 69 million of those locations are “unique” fiber homes, meaning that about 9 million are passed by more than one fiber provider, Breznick added.

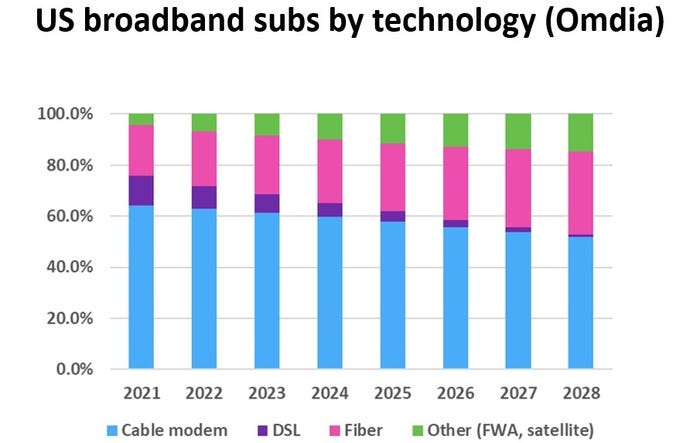

The share of broadband technology is also evolving. While HFC remains the primary way of delivering broadband, fiber-to-the-premises (FTTP) and fixed wireless access (FWA) will continue to make their presence felt in the coming years. Omdia (owned by Informa) expects cable’s share of that mix to drop over the next four years, hitting about 55% by 2028, while fiber’s share is expected to rise to 30% by that time, Breznick explained.

For the cable industry, fiber and FWA are not solely about competition. Many operators are also using FTTP extensively in greenfield deployments and subsidized rural buildouts. They are deploying it on a targeted basis via a new generation of nodes that can support multiple access technologies, including HFC and wireless.

CableLabs has put fiber-to-the-premises on the front burner via a pair of new working groups. A recent survey from Omdia shows that more than one-third of cable operators have already deployed passive optical networking (PON) in some form. That number will “undoubtedly keep rising” thanks to initiatives such as the Broadband Equity Access and Deployment (BEAD) program, Breznick said. Omdia expects spending on next-gen cable technologies to tick up in 2024 and 2025 and then reach a relatively steady annual state through 2029.

Meanwhile, operators such as Mediacom Communications have tapped into FWA to extend the reach of broadband in rural areas. Combined, they demonstrate some of the reasons why the industry has been shedding the “cable” label via rebranding efforts and name changes in recent years.

Cable’s broadband challenge is to grow broadband subscribers as it faces more broadband competition combined with historically low churn and a slow housing move market. “If it feels like an uphill battle for cable, maybe that’s because it is. But that doesn’t mean it has to be a losing battle,” Breznick said. “That’s because the cable industry still has plenty of tricks left up its sleeve.”

Those tricks include the use of next-generation DOCSIS 3.1 (sometimes called DOCSIS 3.1+ or extended DOCSIS 3.1) that can bump up speeds as high as 8 Gbit/s by opening up new orthogonal frequency division multiplexing (OFDM) channels. Some operators, including Comcast, Charter Communications, Rogers Communications, Cox Communications and Cable One, have begun to deploy DOCSIS 4.0 or have put it squarely on their network upgrade roadmaps.

And though cable operators’ network spending is expected to be down in the first half of 2024, vendors are optimistic that the spigots will start to open up again in the second half of the year as operators pick up the pace.

References:

https://www.lightreading.com/fttx/us-fiber-rollouts-reach-tipping-point-but-are-still-far-behind-hfc

Fiber Connect 2023: Telcos vs Cablecos; fiber symmetric speeds vs. DOCSIS 4.0?

Dell’Oro: Broadband access equipment sales to increase in 2025 led by XGS-PON deployments

Nokia’s launches symmetrical 25G PON modem

Fiber and Fixed Wireless Access are the fastest growing fixed broadband technologies in the OECD

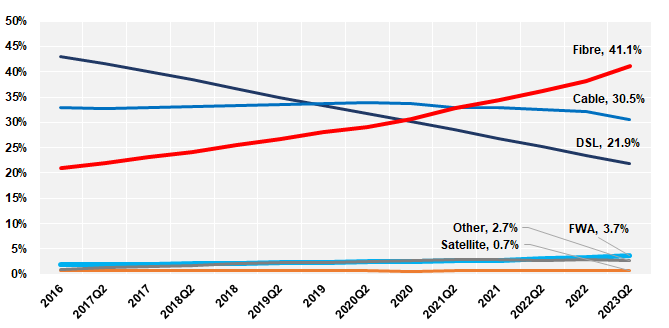

The latest OECD statistics show that Fiber and Fixed Wireless Access (FWA) have seen the strongest growth in fixed broadband technologies in three years. Fibre subscriptions have increased by 56% between June 2020 to June 2023, and FWA subscriptions have increased by 64%. The United States (252%), Estonia (153%), Norway (139%) and Spain (118%) led this FWA growth. The dynamism of fiber and FWA stands in stark contrasts to the decline in DSL (-24%).

Nine OECD countries have more than 70% of fibre connections over total broadband, with Korea, Japan, Iceland, Spain leading the way with the highest fibre penetration rates of 89%, 86%, 85% , and 84%, respectively. The highest fibre growth rates are in Europe, with Austria and Belgium having growth rates of 75% and 73% over the last year, closely followed by Mexico with a growth in fibre of 68%. Two other Latin American countries are in the top 7: Costa Rica and Colombia with fibre growth rates of 42% and 34%, respectively.

Mobile data usage per subscription grew substantially by 28% in one year passing from 10.2 GB to 13 GB per subscription per month in OECD countries as of June 2023. The amount of data consumed in countries vary greatly from 6 GB to 46 GB, with Latvia being the OECD leader.

Despite an already very high mobile broadband penetration in the OECD area, overall mobile subscriptions continue to grow by 4.6% over the last year, which totalled 1.8 billion as of June 2023, up from 1.74 billion a year earlier. Mobile broadband penetration is highest in Japan, Estonia, the United States and Finland, with subscriptions per 100 inhabitants at 200%, 192%, 183% and 161%, respectively.

Eighteen countries were able to provide the number of their 5G subscriptions separately from mobile broadband subscriptions. The share of 5G in total mobile broadband subscriptions is 23% on average for the OECD countries that provided this data.

Machine-to-machine (M2M) SIM cards grew 14% increase in one year. The two leading countries are Sweden with 238 M2M SIM cards per 100 inhabitants and Iceland (203), followed by Austria (179), the Netherlands (93) and Norway (76). Both Sweden and Iceland issue M2M SIM cards for international use.

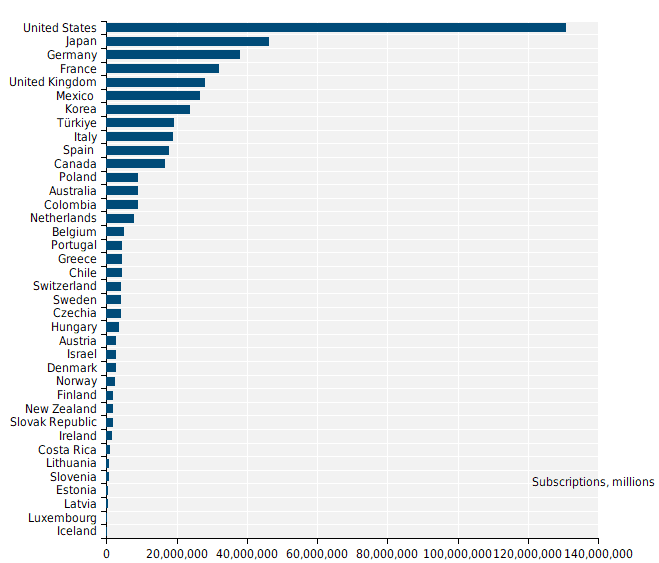

Total number of fixed broadband subscriptions, by country, millions, June 2023:

……………………………………………………………………………………………………………………….