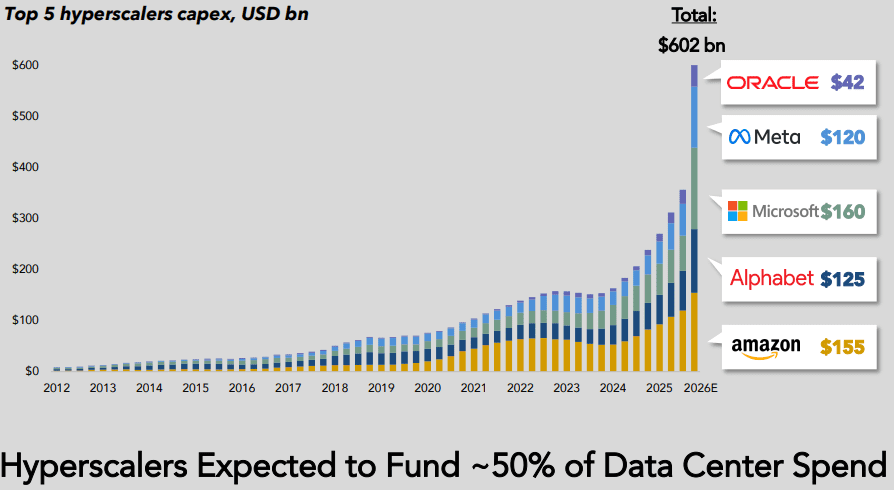

Hyperscaler capex > $600 bn in 2026 a 36% increase over 2025 while global spending on cloud infrastructure services skyrockets

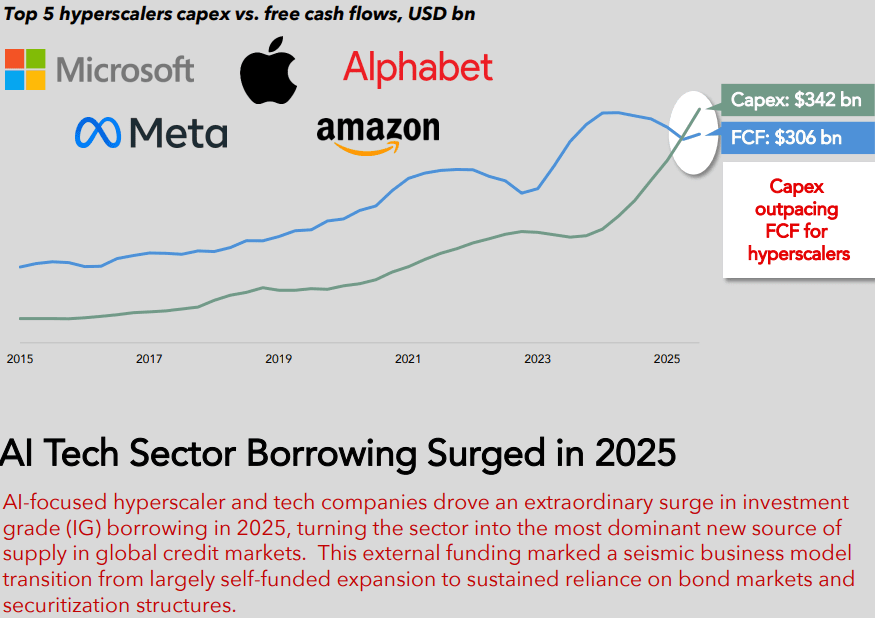

Hyperscaler capex for the “big five” (Amazon, Alphabet/Google, Microsoft, Meta/Facebook, Oracle) is now widely forecast to exceed $600 bn in 2026, a 36% increase over 2025. Roughly 75%, or $450 bn, of that spend is directly tied to AI infrastructure (i.e., servers, GPUs, datacenters, equipment), rather than traditional cloud. Hyperscalers are increasingly leaning on debt markets to bridge the gap between rapidly rising AI capex budgets and internal free cash flow, transforming historically cash-funded business models into ones utilizing leverage, albeit with still very strong balance sheets. Aggregate capex for “the big five”, after buybacks and dividends are included, are now above projected cash flows, thereby necessitating external funding needs.

……………………………………………………………………………………………………………………………………………………………………………………………………………………..

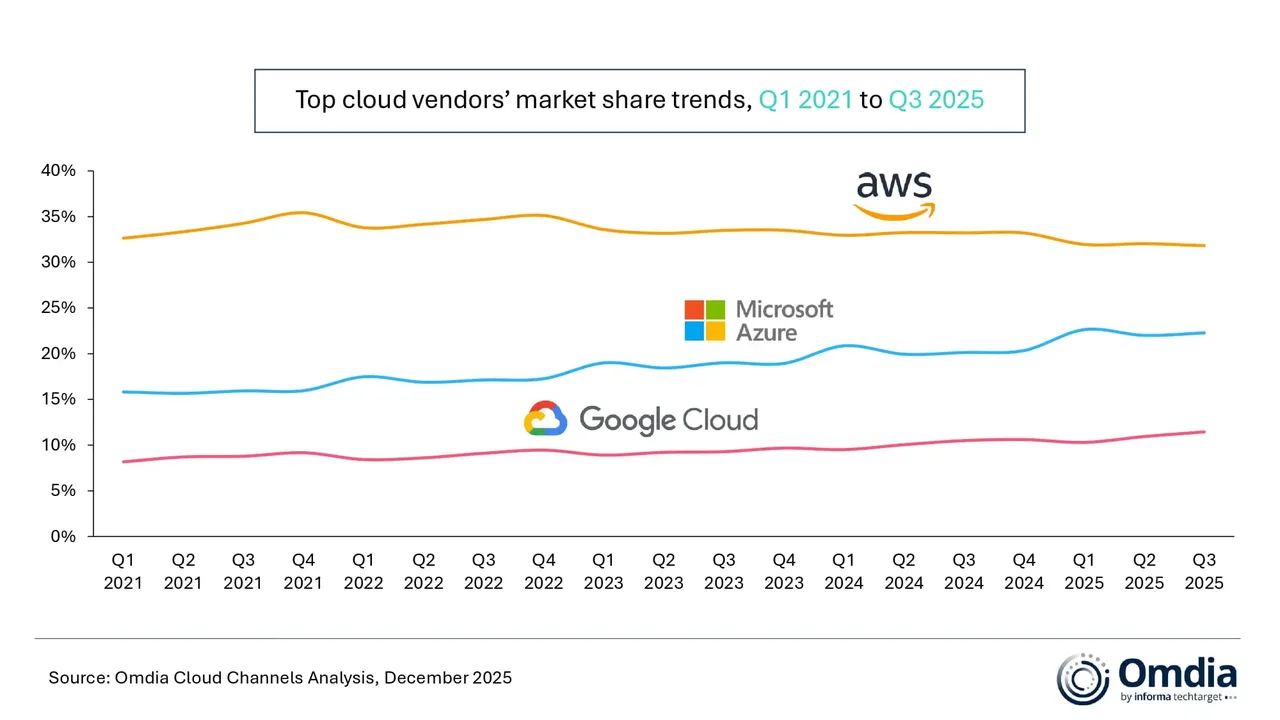

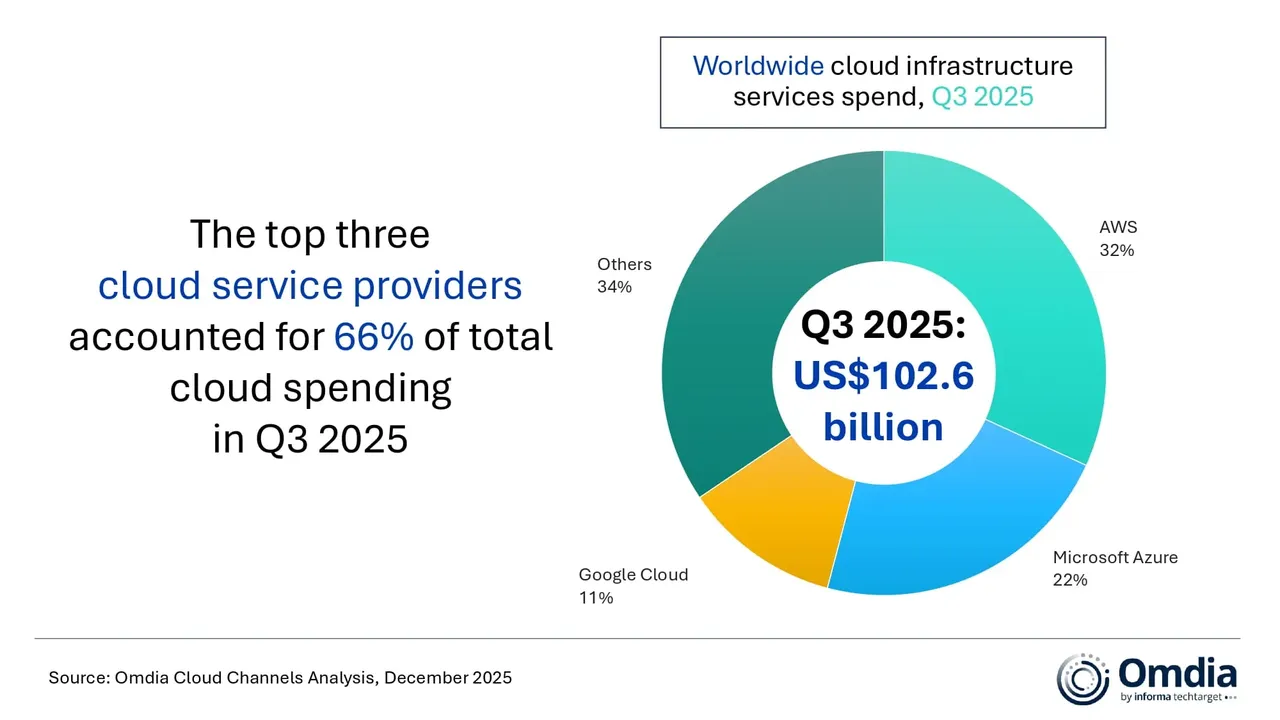

According to market research from Omdia (owned by Informa) global spending on cloud infrastructure services reached $102.6 billion in Q3 2025 — a 25% year-on-year increase. It was the fifth consecutive quarter in which cloud spending growth remained above 20%. Omdia says it “reflects a significant shift in the technology landscape as enterprise demand for AI moves beyond early experimentation toward scaled production deployment.” AWS, Microsoft Azure, and Google Cloud – maintained their market rankings from the previous quarter, and collectively accounted for 66% of global cloud infrastructure spending. Together, the three firms had 29% year-on-year growth in their cloud spending.

Hyperscaler AI strategies are shifting from a focus on incremental model performance to platform-driven, production-ready approaches. Enterprises are now evaluating AI platforms based not solely on model capabilities, but also on their support for multi-model strategies and agent-based applications. This evolution is accelerating hyperscalers’ move toward platform-level AI capabilities. According to the report, Amazon Web Services (AWS), Microsoft Azure, and Google Cloud are integrating proprietary foundation models with a growing range of third-party and open-weight models to meet these new demands.

“Collaboration across the ecosystem remains critical,” said Rachel Brindley, Senior Director at Omdia. “Multi-model support is increasingly viewed as a production requirement rather than a feature, as enterprises seek resilience, cost control, and deployment flexibility across generative AI workloads.”

Facing challenges with practical application, major cloud providers are boosting resources for AI agent lifecycle management, including creation and operationalization, as enterprise-level deployment proves more intricate than anticipated.

Yi Zhang, Senior Analyst at Omdia, said, “Many enterprises still lack standardized building blocks that can support business continuity, customer experience, and compliance at the same time, which is slowing the real-world deployment of AI agents. This is where hyperscalers are increasingly stepping in, using platform-led approaches to make it easier for enterprises to build and run agents in production environments.”

This past October, Omdia released a report forecasting that growth of cloud adoption among communications service providers (CSPs) will double this year. It also forecasted a compound annual growth rate (CAGR) of 7.3% to 2030, resulting in the telco cloud market being worth $24.8 billion.

………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Editor’s Note: Does anyone remember the stupendous increase in fiber optic spending from 1998-2001 till that bubble burst? Caveat Emptor!

………………………………………………………………………………………………………………………………………………………………………………………………………………………..

References:

https://www.telecoms.com/public-cloud/global-cloud-infrastructure-spend-up-25-in-q3

https://www.telecoms.com/public-cloud/telco-investment-in-cloud-infrastructure-is-accelerating-omdia

AI infrastructure spending boom: a path towards AGI or speculative bubble?

Expose: AI is more than a bubble; it’s a data center debt bomb

Can the debt fueling the new wave of AI infrastructure buildouts ever be repaid?

AI spending boom accelerates: Big tech to invest an aggregate of $400 billion in 2025; much more in 2026!

Gartner: AI spending >$2 trillion in 2026 driven by hyperscalers data center investments

AI spending is surging; companies accelerate AI adoption, but job cuts loom large

Will billions of dollars big tech is spending on Gen AI data centers produce a decent ROI?

Big tech spending on AI data centers and infrastructure vs the fiber optic buildout during the dot-com boom (& bust)

Canalys & Gartner: AI investments drive growth in cloud infrastructure spending

Sovereign AI infrastructure for telecom companies: implementation and challenges

AI Echo Chamber: “Upstream AI” companies huge spending fuels profit growth for “Downstream AI” firms

Custom AI Chips: Powering the next wave of Intelligent Computing

7 thoughts on “Hyperscaler capex > $600 bn in 2026 a 36% increase over 2025 while global spending on cloud infrastructure services skyrockets”

Leave a Reply

KobeissiLetter tweet – US technology CapEx spend has been massive:

In 2025, tech CapEx as a % of GDP nearly matched the COMBINED scale of the largest capital projects of the 20th century. This comes as Big Tech CapEx rose to ~1.9% of GDP last year. By comparison, nationwide broadband development at the beginning of the century made up ~1.2% of GDP.

The rapid expansion of electricity in 1949, the Apollo Moon Landing project, and the Interstate Highway system in the 1960s each represented ~0.6% of GDP. The Manhattan Project to develop the first atomic weapons in the 1940s totaled ~0.4% of GDP.

https://x.com/KobeissiLetter/status/2009429665421885480

In 2025, investment in tech equipment and software had reached 4.4% of GDP, nearly as high as at the peak of the dotcom bubble (Chart 1). The five hyperscalers – Amazon, Google, Meta, Microsoft, and Oracle – had plans to add about $2 trillion of AI-related assets to their balance sheets by 2030. Given that AI assets typically depreciate at a rate of around 20% per year, this implied that the hyperscalers were facing an annual depreciation expense of $400 billion – more than their combined profits in 2025.

These capex plans still do not capture the full extent of the AI build-out. OpenAI alone had intended to spend $1.4 trillion on data centers, alongside the billions that Anthropic and xAI planned to undertake, and the additional billions in AI-related assets targeted by the emerging “neoclouds” – CoreWeave, Nebius, IREN, Lambda, and Crusoe.

https://www.bcaresearch.com/sites/default/files/2026-01/GIS_SO_2025_12_11_Sample_Report.pdf

Yann LeCun left his role as Meta’s chief AI scientist in late 2025, arguing that the capabilities of LLMs were limited. In his estimation, LLMs were great at regurgitating old knowledge but not so great at coming up with new knowledge. Supporting LeCun’s perspective, a study by METR found that experienced programmers who had access to AI took 19% longer to finish their tasks than those who did not

Hyperscalers CAPEX budgets have been aggressively increased for the coming year, and are now set to make up 2.2% of GDP. Google co-founder Larry Page was quoted saying “I’m willing to go bankrupt rather than lose this race.” In case it wasn’t already clear, this is not AI hype; it’s a capital war.

Capex spending is only good when it can generate a profit. Investors push back on spending when ROI is questionable, and not enough to justify growth ambitions.

Big tech companies issued $100B of bonds so far in 2026 to fund their AI CAPEX and investors demanded record protection against it via Credit Default Swaps (CDS) which are insurance policies against bond defaults.

At some point, the market maxes out of capacity to absorb any further debt, creating refinancing troubles down the road. As technology progresses and Chinese competition remains ever-present, the capex becomes ever-harder to justify. Moore’s law says that things should be getting cheaper, not more expensive. It is likely that big tech companies will soon start walking back their capex plans in light of investor reactions.

Will AI CAPEX Boom go Bust?

GMO notes that higher corporate investment is associated with lower stock returns. What’s more, periods of higher investment also seem to occur just before economic recessions. “Clearly, this is extremely topical for today,” the firm notes. Could the bursting of the AI bubble soon put the “stag” in “stagflation”?

https://www.gmo.com/americas/research-library/sink-or-swim_insights/

The bar for tech companies to make AI profitable was already high. Then came a surge in memory-chip prices that has sent costs through the roof, adding fresh urgency to questions about who’s going to pay for it all and how. The tech companies that are largely funding the AI boom have been avoiding that riddle. They need to invest in chips and data centers as fast as they can to capitalize on the world-changing potential of AI, they argue. This isn’t the time for prudence.

Now, though, the cost of AI isn’t growing just because they are adding to data-center footprints. It is rising because the stuff they need to buy to make it all work is a lot more expensive.

Memory has become a big issue of late. The most advanced AI computing setups require more of the most advanced kind of memory chips available. This is called high-bandwidth memory. Tech companies are competing to secure supplies, giving memory manufacturers the upper hand on pricing.

The impact has been dramatic. Microsoft last week said about $25 billion of its annual capital expenditures of around $190 billion were down to “higher component pricing.” That’s code for more expensive memory. Google parent Alphabet and Meta Platforms also cited higher component costs in raising their capital-spending plans.

The impact of the memory crunch has already been far-reaching in consumer electronics. It is hitting PCs and smartphones as memory makers divert production to more profitable AI-related products. Surging prices will have an impact on AI itself, too. Tech companies are already under pressure to show their AI investments are paying off as depreciation accelerates and eats into reported profit. And returns on AI ultimately must come from people who use it. That may be in the form of subscription fees, time spent watching advertisements, software licenses or some other novel way tech companies devise to get money out of customers’ pockets. Making that financial model work is suddenly a lot harder.

“We stand on the walls, sentinels of the inner sanctum, against the assault of AI slop. The Ontology is based firmly in reality—there is, here, a dialectic between ground truth, tribal knowledge, and enhancements.”

— Alex Karp, Palantir Technologies chief executive, on the advantages of his company’s approach to AI

Hyperscalers’ earnings growth this quarter was boosted by an unusually large contribution from equity stakes in private companies.

Microsoft reported “only” $942mn of other income in the first three months of the year, but this line item has now made $7.2bn over the past nine months.

Alphabet and Amazon generated “other income” totaling $53 billion in Q1 2026, which accounted for nearly 60% of those two companies’ income in Q1 and 34% of the total $155 billion in income this quarter across the five largest hyperscalers. This represents the group’s largest collective share of earnings attributable to “other income” in at least a decade. Of this $53 billion in “other income,” $49 billion was explicitly due to equity stakes in private companies.

This is another sign of just how comically codependent the AI tech industry has become.

Not only have private investments and increasingly engorged funding rounds become a meaningful driver of the hyperscalers’ aggregate earnings, but the money the hyperscalers have pumped into the likes of Anthropic and OpenAI has allowed the AI companies to sign huge computing deals with Alphabet’s Google Cloud, Microsoft’s Azure and Amazon Web Services.

OpenAI and Anthropic now make up about half of the entire cloud computing order books at Oracle, Alphabet, Amazon and Microsoft.

References:

https://www.ft.com/content/be97df0a-76b1-4cb0-9ba4-d1117d8d1450

https://fortune.com/2026/04/30/google-amazon-ai-profits-anthropic-stake-bubble-earnings-2026/