AT&T Exec Talks Smart Cities: Private LTE, LTE-M, NB-IoT, and 5G

AT&T’s Mike Zeto discussed the teleco and media company’s smart cities strategy as part of its 5G and IoT roll-out, saying in an interview AT&T will go beyond providing connectivity and focus on building “end-to-end solutions” for localities and enterprises. “The only way these cities are going to be move forward is with public-private partnerships,” Zeto said.

AT&T talks cities: “We wouldn’t do it if it didn’t make sense, but it’s not about money”

Trump and FCC plan to accelerate 5G rollout in U.S.; FCC fund to connect rural areas

In a press conference today in the White House’s Roosevelt Room, President Trump laid out a number of initiatives focused on helping accelerate the U.S. role in the 5G race.

“This is, to me, the future,” Trump said, opening the press conference flanked by FCC Chairman Ajit Pai, Ivanka Trump and a room full of communications representatives in cowboy and hard hats.

“It’s all about 5G now,” Trump told the audience. “We were 4G and everyone was saying we had to get 4G, and then they said before that, ‘we have to get 3G,’ and now we have to get 5G. And 5G’s a big deal and that’s going to be there for a while. And at some point we’ll be talking about number six (6G).”

“5G will be as much as 100 times faster than the current 4G cellular networks. The race to 5G is on and America must win, It’s a race our great companies are now involved in,” Trump added.

Trump said a secure 5G network will transform how everyone communicates and create astonishing new opportunities in America. “It will make American farms more productive, American manufacturing more competitive and American health care better and more accessible,” he said.

The apparently off-script moment echoed Trump’s recent call on Twitter for the U.S. to get 6G technology “as soon as possible.” There’s something to be said for the spirit, perhaps, but it’s probably a little soon to be jumping the gun on a technology that doesn’t really exist just yet.

Trump used the opportunity to downplay earlier rumors that the government might be building its own 5G network, instead promoting a free-market method, while taking a shot at the government’s capabilities. “In the United States, our approach is private sector-driven and private sector-led,” he added. “The government doesn’t have to spend lots of money.”

“We cannot allowed any other country to out compete the United States in this power industry of the future,” Trump said. It’s important to note that China and the U.S. are fiercely competing in 5G adding to the tensions among the #1 and #2 global economies.

In recent months both the administration and the FCC have been discussing ways to make America more competitive in the race to the soon-to-be-ubiquitous cellular technology. Earlier today, the FCC announced plans to hold the largest spectrum auction in U.S. history, offering up the bands to wireless carriers. The planned auction is set to commence on December 10th. As much as 3.4 gigahertz of “millimeter-wave” spectrum could be sold by the FCC to wireless carriers such as AT&T and Verizon in the spectrum sale, according to Pai.

“Forward-thinking spectrum policy, modern infrastructure policy, and market-based network regulation form the heart of our strategy for realizing the promise of the 5G future.” – FCC Chairman Pai

………………………………………………………………………………………………………………………………………………………………………..

The focus is understandable, of course (AJW: really???). 5G’s value will go far beyond faster smartphones, providing connections for a wide range of IoT and smart technologies and potentially helping power things like robotics and autonomous vehicles. The technology will undeniably be a key economic driver, touching as of yet unseen portions of the U.S. workforce.

“To accelerate and incentivize these investments, my administration is freeing up as much wireless spectrum as needed,” Trump added, echoing Pai’s plans.

Earlier today Pai and the FCC also proposed a $20.4 billion fund design to help connect rural areas. The chairman said the commission believes the fund could connect as many as four million small businesses and residences to high-speed Internet over the course of the next decade. The “Rural Digital Opportunity Fund” could launch later this year, after a period of public notice and comment.

The focus is understandable, of course. 5G’s value will go far beyond faster smartphones, providing connections for a wide range of IoT and smart technologies and potentially helping power things like robotics and autonomous vehicles. The technology will undeniably be a key economic driver, touching as of yet unseen portions of the U.S. workforce.

…………………………………………………………………………………………………………………………………………………

References:

https://www.foxbusiness.com/politics/trump-says-securing-5g-will-create-astonishing-us-opportunities

IHS Markit: 5G Market Set to Boom, but clarity needed; Japanese Telcos: $14.4B in 5G spending

IHS Markit: 5G Market Set to Boom, but clarity needed

As global 5G capabilities expand, alignment of what 5G is, what end users should expect and how it should be measured will be critical to adoption

As the first commercial deployments of (pre-standard) 5G start to appear, the stage is set for consumers finally to find out what the powerful next-generation mobile standard promises can bring: an ambitious and far-reaching technological advance that transforms virtually all aspects of human activity—how we experience life, conduct business, create goods, and build societies. In its latest complimentary white paper, “The Promise and Potential of 5G,” business information provider IHS Markit explores the opportunities and challenges surrounding the upcoming global rollout of new 5G wireless networks.

Without question, 5G is helping set the stage for incredible change, but it remains a confusing landscape, with varied and sometimes conflicting interpretations of what 5G is and what to expect from it. This confusion is impacting not just consumers but also complicating the industry’s ability to measure itself against a standard set of 5G expectations and requirements.

To optimize short-term and long-term 5G adoption, it is imperative that clarity regarding what 5G is and when each capability will be available is established for both consumers and the ecosystem. To that end, IHS Markit follows the official 3GPP definition of 5G [1]but also believes that this description needs to be understood within the context of everyday experience and concepts.

[1.] ITU considers 5G to be based on its forthcoming IMT 2020 recommendations. Those are the only official standards for 5G.

https://news.itu.int/5g-fifth-generation-mobile-technologies/

…………………………………………………………………………………………………………………………………………………………………………………………….

According to the previously referenced IHS Markit 5G white paper, 5G will improve existing services and enable new use cases, such as driverless cars, immersive entertainment, zero-delay virtual reality, uninterrupted video and no-latency gaming. On the industrial front, 5G will be key to expanding and realizing the full promise of the internet of things (IoT), with the technology’s impact to be felt in smart homes, smart cities and smart industries.

“The marketplace implicitly understands 5G represents an unprecedented growth opportunity, with the initial smartphone rollout set to generate record shipment volumes,” said Francis Sideco, vice president, technology at IHS Markit. “However, fewer people understand the iterative nature of major technology rollouts such as the one we are going through now with 5G—a process involving multiple major updates that will add new capabilities in the coming years. With each of these updates having the potential to significantly disrupt the market’s competitive dynamics, it’s critical for companies to clearly understand the implications of each rollout or risk falling behind the competition.”

Following initial sales of 37 million first-generation 5G smartphones this year, with initial shipments only now commencing, worldwide shipments will surge to 120 million devices in 2020, IHS Markit forecasts. This rollout will be the fastest ever for a new wireless generation, generating six times more unit shipments than previous record-holder LTE, over a similar timeframe. Benefitting from strong industry momentum and alignment, global 5G smartphone shipments will continue to rise in the coming years, reaching over 525 million devices in 2023. “Despite strong growth, the level of success among individual competitors in the smartphone and infrastructure market will hinge on their ability to shift their business strategies in parallel with the evolution of 5G,” Sideco said.

New 5G technical standards (i.e. IMT 2020 from ITU) will eventually enable the creation of applications that could open new opportunities, inform new business models and transform everyday life for multiple industries and billions of users throughout the world. However, many of these capabilities won’t be available in initial 5G rollouts, but instead will arrive in subsequent releases of the standard to be implemented over the next few years. Each of the releases will deliver new challenges and opportunities not only for the wireless industry but also every industry for which the new use cases are envisioned. To fully realize the potential of these opportunities, competitors will need to understand and capitalize on new capabilities even before they are fully introduced.

The 5G standard’s next release is already on the horizon, with the expected introduction of Release 16 in late 2019. The upcoming release will deliver highly desirable enhancements, including far greater reliability and peak data rates of 20 gigabits-per-second (Gbps) downlink and 10 Gbps uplink. “This next phase of implementation and rollout will trigger a race among mobile network operators to meet and take advantage of these performance enhancements,” Sideco said. “The winners of this race are likely to gain a competitive advantage as they gear up for the next wave of growth.”

Future revisions will spur similar competitive battles, as 5G adds major new capabilities and expands into other markets beyond mobile communications, such as mission-critical applications and massive internet of things (IoT) deployments. “For companies throughout the technology supply chain—from network operators, to smartphone brands, to industrial and automotive device manufacturers and electronics suppliers—it will become increasingly important to understand the changes brought by each phase of the 5G deployment and to be ready to capitalize on the latest capabilities to gain a competitive advantage,” Sideco said.

To learn more about managing the complexities of the 5G era, download the free white paper, “The Promise and Potential of 5G.”

…………………………………………………………………………………………………………………………………………………………………………………………………….

In other 5G related news today….

Japan’s carriers plan $14.4bn spending blitz for nationwide 5G:

The Ministry of Internal Affairs and Communications has approved the allocation of spectrum after determining that the companies’ applications met the conditions of the allocation, the Nikkei Asian Review reported. Japan’s telecom ministry has allocated 5G mobile spectrum to incumbent operators NTT Docomo, KDDI, and Softbank, as well as local e-commerce giant Rakuten.

The four companies plan to invest heavily in 5G, spending a combined 1.6 trillion yen ($14.4 billion) over the next five years. Docomo is planning the largest spend, with goals to invest at least 795 billion yen in 5G over this time.

Japan’s mobile operators have set aside $14 billion to invest in 5G networks over five years. (Photo by Ken Kobayashi)

…………………………………………………………………………………………………………………………………………………………………………………………………………………….

The four Japanese wireless carriers plan to commence commercial 5G services in 2020, with KDDI and SoftBank planning to commence advertising for its services in March. Rakuten Mobile, Japan’s upcoming newest market entrant, plans to commence 4G services in October 2019 and 5G services in June 2020.

The conditions for the allocation of spectrum included commitments to commence services in every prefecture of the nation within two years, and set up 5G base stations in at least half the country within five years.

According to the report, Docomo and KDDI are each targeting more than 90% 5G population coverage by the end of the five years, while SoftBank is targeting 64% coverage while Rakuten is aiming for 56%.

The Japanese government wants industry to build out 5G infrastructure widely, from big metropolitan areas to rural regions. It expects the technology, which offers speeds up to 100 times as fast as 4G, to enable self-driving buses and telemedicine, and to help Japan combat its worker shortage.

The conditions required for receiving 5G spectrum included starting services in every prefecture within two years. The communications ministry also divided Japan into 4,500 blocks, requiring operators to set up base stations in at least half of them within five years. Docomo and KDDI each plan to achieve coverage of more than 90% in that time. SoftBank and Rakuten set less ambitious goals, at 64% and 56%, respectively. The requirement will force mobile operators to balance making heavy investments with attaining profits.

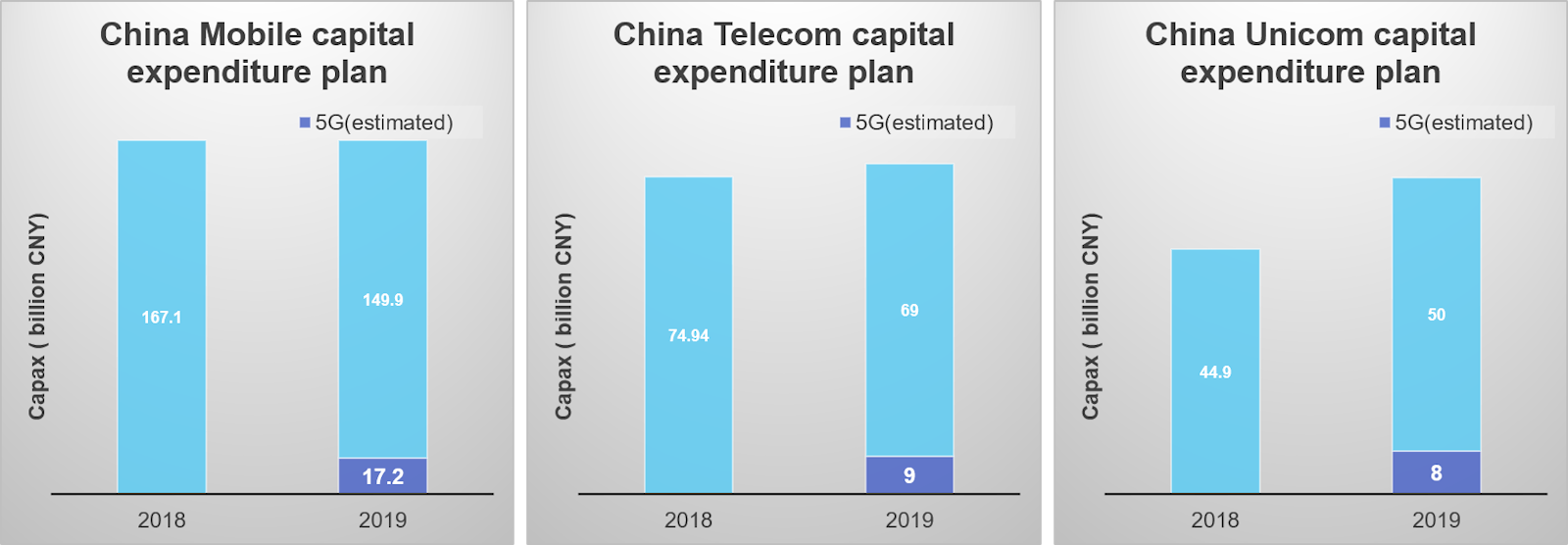

IDTechEx: China’s 5G investments may be slowing, but it’s still the 5G market to watch

China is certain to be one of the world’s largest 5G markets and has been spending heavily to gain an early lead in 5G adoption, yet there are signs that 5G momentum is slowing down in the market. That was one of the conclusions of a new report from IDTechEx Research on the 5G technology market forecast for the next 10 years.

The report found that China’s big three operators China Mobile, China Telecom and China Unicom have all announced 5G capex budgets that are lower than expected.

China Unicom plans to spend between 6 billion yuan ($893.3 million) and 8 billion yuan on 5G in 2019, while China Telecom has allocated 9 billion yuan. While market leader China Mobile has not disclosed its projected 5G spending, the report forecasts that its spending will be in the region of 17 billion yuan. The total 5G capex budget allocated in China (34 billion yuan) for 2019 is therefore significantly lower than the projected 50 billion to 100 billion yuan.

Factors behind the lower than expected spending include: greater activity to upgrade 3G networks to 4G, falling per-subscriber revenue and the uncertainty over whether 5G investments will generate returns, the market research firm said. The CEO from Huawei, the top one telecom infrastructure supplier and number two smartphone provider in the world, has publicly expressed a similar concern on the payback from 5G.

Based on slower than expected 5G deployment schedules, the total contribution of 5G for the telecoms sector could be reduced from the projected $200 billion by 2029 to $160 billion. Network operators are forecast to invest around $200 billion to $350 billion for 5G development from 2020 to 2030.

Source: IDTechEx Research

……………………………………………………………………………………………………………………………………………………………………………………………………………………….

IDTechEx Research predicts that by 2030 the direct 5G revenue in China will be 6.3 trillion CNY (about $930 bn) and the Compound Annual Growth Rate (CAGR) in the coming ten years will be 29%. 5G will create 8 million jobs and contribute around 5.8% GDP growth in China by 2030. The indirect revenue generated by 5G will be 10.6 trillion CNY (about $1,579 bn), with CAGR of 24%. Among them, the direct revenue for telecoms will be over $200 bn by 2029.

As the current 5G deployment plan is slower than expected, these numbers might be overestimated. The new IDTechEx Research report 5G Technology, Market and Forecast 2019-2029 forecasts a moderated revenue of $160 bn for telecoms in China by 2029. Nonetheless, China is still the main market to watch. It is likely that the telecoms in China will invest at least $200-350 bn from 2020-2030 for 5G development, with the key focus on automotive, industry, healthcare and energy.

References:

https://www.idtechex.com/research/articles/is-5g-slowing-down-in-china-00016958.asp

More information can be found from 5G Technology, Market and Forecast 2019-2029 – contact [email protected] or visit www.IDTechEx.com/5g.

China Broadcasting Network Corp. to launch mobile network; already provides cable TV, Internet and Telecom services in China

As China state-owned telecom carriers (Unicom, China Mobile, China Telecom) prepeare for launch of 5G services, Beijing is supporting the creation of a new full-service telco by upgrading the nation’s cable network giant, China Broadcasting Network Corp. This is evident from the flurry of initiatives from the state-owned cable TV network operator to enhance its infrastructure and emerge as a stronger entity that can join the Big Three telecom firms in their own game.

Last month, China Broadcasting, an entity set up to run the nation’s cable TV system before being awarded, in 2016, a license to operate internet and telecom services, announced strategic partnerships with CITIC Group and Alibaba Group to help speed up efforts for network upgrades.

Under the cooperation agreements, China Broadcasting, which was founded by what is currently known as the National Radio and Television Administration (NRTA), will receive assistance from CITIC and Alibaba “for integrated development and upgrading of the nation’s cable TV networks as well as related product development and management,” state news agency Xinhua reported.

China aims to make its national cable TV networks smarter and create new generation radio and TV technology infrastructure by integrating cable TV networks and letting 4K, 5G, IPv6, big data, artificial intelligence and quantum communications technologies play their roles, Nie Chenxi, the head of the NRTA, said at the signing ceremony.

China Broadcasting’s plans comes as the traditional cable TV business faces a tough challenge in the era of internet TV and streaming services, throwing up the need for operators to upgrade themselves and expand their services via two-way interactive high speed broadband infrastructure.

Currently, telecom operators like China Telecom and China Mobile are offering fiber-to-the-home or fiber-to-the-building broadband networks to provide dedicated bandwidth for each broadband line, while cable network can only adopt a share-bandwidth approach. That has made it difficult for cable networks to compete with the fiber broadband operators.

China has seen cable TV subscribers falling in number after hitting a peak in 2016. Last year, subscribers were estimated at 223 million, down 8.75 percent from a year ago. The industry has seen its profitability get constrained and profit margins decline amid the weak subscriber figures. Meanwhile, IPTV and OTT video platforms had around 150 million users in 2018.

As the industry gets reshaped, CITIC is emerging as a key player in the reform of China’s cable network. The group, as a matter of fact, is not new to telecom network deployment. It owns CITIC Guoan network in Beijing, which is expanding its cable network operation across the nation. The conglomerate is also exploring new business models by teaming up with local cable operators to operate smart community service platforms for citizens.

Such experience puts CITIC in a good position to help integrate China’s state-owned nationwide cable network into a single valuable backbone network to deliver high definition content to TV as well as mobile devices.

CITIC Group can also help ease the financial burden of the government on network capital expenditure. Though there isn’t an equity deal, CITIC’s partnership with China Broadcasting can help the latter catch up with the three big state-owned telecom carriers through a market-driven approach.

In November last year, mainland media quoted Chinese authorities as saying that they have allowed China Broadcasting to build 5G networks, a move that will allow the market to transform into a four-player battleground. China Daily cited sources close to the Ministry of Industry and Information Technology as saying that China Broadcasting, which was formed in 2014 by combining several regional cable TV operators, was officially applying for a 5G license. That will help boost competition in the industry that has long been dominated by three players — China Mobile, China Unicom and China Telecom.

In China, traditional cable TV service has been facing keen competition from online media services such as IPTV, OTT video as well as Internet video. Telecom operators are using fiber broadband to provide IPTV services to their broadband users, while OTT players like Youku and Tencent also dominate the screen time of Chinese users.

Amid this situation, cable TV network operators need to invest not only on the content but also the network technology to provide triple or even quad play in the market to catch up with the telecom carriers.

China Broadcasting is preparing to launch a mobile network using the 700MHz spectrum band. The spectrum is currently being used for domestic analogue television broadcasting. Now, China Broadcasting and CITIC have formed a joint venture, China Broadcasting Network Mobile, to operate a mobile business on 700Mhz band. The joint venture is expected to receive a mobile license from the Chinese government so that they can build a network across the nation to challenge the dominance of the Big Three operators.

As the low-band 700MHz spectrum can have better network coverage compared with other frequency bands, the joint venture will be in a good position to provide better coverage for high speed mobile internet using 5G technology. Once the 5G war kicks off, apart from China Broadcasting, CITIC Group could also effectively become a major player in the China telecom market.

References:

http://www.ejinsight.com/20190409-china-cable-network-reform-what-it-means-for-telecom-industry/

https://en.wikipedia.org/wiki/Telecommunications_industry_in_China

http://english.cctv.com/2016/05/06/VIDElPgPCFpnb3m4hk1XC3Gq160506.shtml

San Diego and Verizon in deal to deploy small cells for 4G-LTE to be upgraded to 5G

Verizon and the city of San Diego, CA have announced a partnership under which the U.S.’ #1 wireless telco will invest upward of $100 million to deploy as many as 200 energy-efficient light poles that host small cells for 5G wireless, as well as providing the police with 500 smartphones and the fire and rescue department with 50 tablets. The city, in exchange, will ensure a streamlined process for approval of small cells and fiber optic links.

San Diego has pledged to streamline the permitting process for rolling out mobile network “small cells” in a deal with Verizon that could help lay the foundation for bringing 5G technology to the city. Mayor Kevin Faulconer announced the deal in a news conference Monday on Harbor Island. Verizon will spend more than $100 million to install up to 200 power efficient light poles with small cell wireless network gear to improve cellular coverage.

“Verizon is a partner in our effort to enhance wireless capability and lay the groundwork for the future of 5G wireless,” said Faulconer. “This agreement is going to increase services and expand our smart cities capabilities, at no additional costs to taxpayers.”

Small cells — about the size of a pizza box — contain lower power radios and antennas. They add density to the cellular network to boost range and increase the number of smartphone/ endpoint users who can then gain high speed connections to the Internet. This is done via frequency reuse– small cells in one area of town may use the same frequency bands as other small cells in a different part of the city. Small cells are expected to be a key component of high speed 5G mobile networks, which have just begun rolling out in a few cities in the U.S. and South Korea. They have to be mounted on city owned polls or like infrastructure. “Most of these small cells essentially they are on poles, and they blend into the areas to provide that coverage, as well as capacity,” said Ed Chan, Verizon’s senior vice president of engineering.

Verizon plans to install 4G LTE small cells in San Diego under the new program, said Chan. These small cells can be upgraded to 5G technology — either through software updates or the addition of 5G radio equipment. 5G networks aim to deliver speeds 10 times faster than current 4G technologies, with imperceptible transmission delays. They are expected to help power ubiquitous mobile video, self-driving cars, smart cities infrastructure and connected health care devices.

Verizon deployed its first pre-standard mobile 5G networks last week in neighborhoods in Chicago and Minneapolis. It expects to expand to 30 additional cities U.S. by year end. The telco hasn’t named the next 30 cities to get 5G. Chan said to stay tuned. “This will definitely create the foundation to get to 5G” in San Diego, he said.

The city and Verizon have been talking for several months about ways to speed up the permitting process for small cells and fiber optic links. Plans include updating some building codes and allowing “master permits” where the installation of several, similarly designed small cell street-light poles in a neighborhood would fall under one permit, said Ron Villa, assistant chief operating officer with the city.

“We are doing a pilot in Mission Valley where they can permit a whole area all at once, and they don’t have to go through individual permits,” said Villa. “It will be to the advantage of other carriers as well. If we can get this to work, there will be other carriers that will be welcome” to use the streamlined permitting process.

Verizon is providing poles with street lights and will cover installation costs, said Villa. The company will own the poles. In the future, it will provide analysis of traffic patterns and other data to bolster San Diego’s smart cities capabilities.

“From smart streetlights on Mira Mesa Boulevard to weather-based irrigation controllers in Clairemont, innovation is shaping how we are living and working in District 6,” said Council member Chris Cate. “San Diego’s partnership with Verizon will not only benefit San Diegans today, it will help all future generations.”

References:

2019 Open Network Summit: AT&T Virtualizes its Network; Deploys White Boxes in Toronto and London; 400G and Open ROADM

Last week at the 2019 Open Network Summit, AT&T announced that its white box switch/routers, which interconnect compute servers in the network cloud, are live and carrying 5G traffic. This is part of the company’s push to virtualize its network, which at the end of 2018 had 65% virtualized network functions. AT&T’s goal is to virtualize 75 percent of its core network functions by 2020. “This year (2019) our goal is to get to 70 percent,” Fuetsch said in his Thursday morning keynote. “Why not faster progress this year? We left all the hard stuff for last.”

AT&T CTO Andre Fuetsch during his keynote address at 2019 Open Network Summit

………………………………………………………………………………………………………………………………………………………………………………………………………………

Sidebar: AT&T 5G White Boxes

The radio access network (RAN) includes radios on towers, small cells and other types of equipment that traditionally “were specialized, expensive devices sold by a small number of (wireless network equipment) vendors,” said Fuetsch in a blog post. Those vendors “dictated costs, technical capabilities and upgrade schedules. They controlled the hardware and the software.”

This status quo no longer makes sense, now that carriers are deploying 5G wireless, which will support higher speeds and lower latency, Fuetsch argues. Wireless network traffic is expected to skyrocket, but carriers cannot afford to increase the price of service commensurately.

AT&T previously released specifications for a white box router for use in its 5G network and invited vendors to submit proposals to build the router. Feutsch’s blog post notes that the company is working on additional hardware specs with the O-RAN Alliance, an industry group focused on defining 5G white box requirements.

The other AT&T 5G white box initiative highlighted in Fuetsch’s blog post is something he calls the “network cloud white box,” which he said is now live in the AT&T network and carrying 5G traffic. This device would be a switch that would interconnect servers in the edge data centers that AT&T is establishing to support low-latency 5G wireless applications. Some of these applications need more processing power than end-user devices can support, which dictates a cloud approach. But the cloud resources must be located near the end-user to provide low latency.

The servers in the edge data centers are powered by the ONAP open source network operating system that AT&T played a key role in developing. The white box deployment uses a software stack that will be part of the open source Disaggregated Network Operating System (DANOS) Project, and AT&T plans to introduce its code contribution to the community soon

Also in the blog post, Fuetsch noted that AT&T has deployed white boxes in Toronto and London to support internet service for business customers and that the company plans to offer the devices in 76 countries by the end of the year. In addition, he said AT&T is working on technology that would enable a single fiber optic wavelength to carry 400 Gbps. For its 400G deployment, AT&T expects to use Open ROADM optical networking for interoperability, to achieve more competition, mix and match between vendors, and lower the barrier to entry for startup vendors, Fuetsch said.

“These white boxes and open source routing software that we’re deploying, the cell site router initiative that we’re putting in is going to 65,000 (domestic) cell sites over the coming years,” Fuetsch said.

AT&T contributed its white box specs to the Open Compute Project last year, which led to the development of the cell site router gateway that it’s showing at ONS this week. AT&T is demonstrating a white box router gateway from UfiSpace that was developed via the OCP specifications.

Fuetsch said AT&T planned to update 65,000 cell tower sites with the UfiSpace white boxes. While he didn’t provide a timeline, he said those efforts were ramping up this year.

“This is a hardware box that is based on Broadcom’s Qumran chipset, and it’s basically a cell site router that is a hardened for extreme environmental conditions,” Fuetsch said. “So think like negative 40 Celsius up to 65 degrees Celsius operating ranges. It’s also a box that basically can support interfaces from as low as 100 megs all the way up to 100 gig for both supporting our radio based RAN units as well as our backhaul needs.”

While AT&T hasn’t said which vendors it’s using for the internet white boxes, AT&T is running its Vyatta software stack on them, which Fuetsch said AT&T still planned to contribute into the Linux Foundation’s DANOS community at some point this year. These open, white box systems allow AT&T to run 10 times as much traffic as the proprietary routers it previously bought at the same price. Fuetsch declined to give a time frame for when a majority of AT&T’s network might operate on open source-based hardware, but said certain aspects of it will in the coming years.

………………………………………………………………………………………………………………………………………………………………………………………………………………

Regarding AT&T’s motivations for open source, Fuetsch identified security, freedom of choice, flexibility, and interoperability. “As we shift from a hardware-centric network to a more software-centric network we needed a way to get our software to become more open, more flexible. We also were looking for software that’s more secure. Open source is inherently more secure because you have more eyeballs on it,” he said.

“We believe that not only having more open reference designs on the hardware level but also having more open source based projects in that ecosystem will drive more innovation, more economic solutions, more competition, thus a better experience and products and services for our customers,” he said. “Open source has really become a major foundation to a lot of our major network initiatives.”

………………………………………………………………………………………………………………………………………………………………………………………………………………..

AT&T’s Network by the Numbers:

• 214 Countries & territories

• 1.1M+ Global fiber route miles

• 253 Petabytes per day

“5G” Deployment:

• 12 5G US cities launched (with pre-IMT 2020 standard, 3GPP Release 15 NR, NSA implementation)

• 9 additional 5G US cities coming soon

• Nationwide 5G early 2020 (IMT 2020 won’t be completed by then)

In the next 5 years [Source: Cisco Visual Networking Index Forecast & Trends 2/27/19]:

• 3x Increase global IP traffic

• 7x Increase mobile IP Traffic

• 71% Traffic from wireless devices

………………………………………………………………………………………………………………………………………………………………………………………………………………..

References:

https://about.att.com/story/2019/open_networking_summit_2019.html

https://about.att.com/innovationblog/2019/04/open_source_and_white_box.html

https://events.linuxfoundation.org/wp-content/uploads/2018/07/Fuetsch-ONS-2019-keynote-FINAL.pdf

IHS Markit: Enterprise Data Center SDN savings yet to be realized

by Josh Bancroft, IHS Markit Analyst

IHS Markit recently surveyed 100 North American enterprises that are evaluating or implementing software-defined networking (SDN) for the data center by 2020. Respondents currently evaluating SDN expect that it will drive operational- and capital-expenditure decreases at a faster pace than what has been experienced by those already deploying SDN.

“Migrating to SDN means deploying new equipment, upgrading existing equipment, and training IT staff, which requires investment,” said Josh Bancroft, senior analyst, cloud and data center research, IHS Markit. “Those evaluating SDN need to adjust their expectations that savings might not be felt immediately, but instead might happen over a longer period of time.”

The 2018 “Data Center SDN Strategies North American Enterprise Survey” indicated that the transition to live SDN deployment is well underway. By the end of 2019, 74 percent of respondents will be in production trials, and 36 percent will be in live production, up from 38 percent and 20 percent, respectively, in 2018. Enhancements have been made by vendors, including integrating network analytics to improve application performance and security. Doing so will encourage enterprises to deploy SDN, since improved application performance and improved security were two of the top drivers for deploying SDN. Other top deployment drivers for SDN included; decreased operating costs, simplified network provisioning and improved management capability.

In the IHS Markit survey, Cisco, VMware, and Dell EMC were identified as the SDN hardware and software manufacturers with which respondents were most familiar.

Following are some additional highlights from the survey:

- Top deployment barriers among the respondents were the interruption of critical network operations (30 percent), interoperability with existing network equipment (29 percent) and lack of trained staff (29 percent)

- Less than half (48 percent) of respondents expect capital expenditures (capex) to increase again in the second year of deployment. However, capex increased in the second year for 61 percent of those who have deployed SDN, which suggests those evaluating deployment should adjust their expectations.

- Nearly one-third (31 percent) of respondents chose automated disaster recovery as the top use case for capex reduction, while 35 percent selected automated provisioning as the top use case for operating expenditure (opex) reduction, and 30 percent chose automation for application deployment as the top use case for employee productivity.

- By 2020, 83 percent of respondents will be in live production with data center SDN.

Data Center SDN Strategies North American Enterprise Survey

This IHS Markit survey analyzes the trends and assesses the needs of enterprises deploying SDN in their data centers. The study probes issues defining how the enterprise market will evolve with data center SDN, including deployment drivers and barriers, rollout plans, applications, use cases, vendors installed and under evaluation, top rated vendors, and more.

IHS Markit: Huawei Led Global 4G LTE Infrastructure Market which totalled $22.9B in 2018; China CAPEX bottoms out

By Stéphane Téral, director, IHS Markit

Key information from China released over the past two weeks indicate that China’s 4G LTE capital expenditures (capex) totaled $17.3 billion in 2018, which is 8.5 percent above the initial plan. Among the three Chinese service providers – China Mobile, China Telecom and China Unicom – China Mobile was responsible for much of the increase in plan, spending $1.5 billion more than its initial plan released in March 2018.

With this hike in China’s capex, along with solid sustained infrastructure spending in Europe, Middle East, Africa and various countries in Asia, global 4G LTE infrastructure revenue was $22.9 billion in 2018.

Huawei finished 2018 with 31 percent market share in the global mobile infrastructure market, which includes 2G, 3G and 4G hardware macrocell networks. Huawei was followed by Ericsson with 27 percent and Nokia with 22 percent.

As always, March is an important month in China, as it is punctuated by full-year financial results and the release of guidance for the full calendar year from China Mobile, China Unicom and China Telecom. Given the magnitude of telecom capex in China, everyone involved in the telecom ecosystem pays attention to what the three service providers say, particularly their plans for the year.

……………………………………………………………………………………………………………………………………………………………………………………………………………..

On April 1, 2019 Mr Teral wrote: Capex in China has bottomed out; 5G produces a 3% YoY increase!

O-RAN Alliance and Linux Foundation form O-RAN Open Source Community; Open Networking Assessment and Telcos

On April 2nd, the O-RAN Alliance and the Linux Foundation jointly announced the creation of the O-RAN Software Community (O-RAN SC). The O-RAN SC will provide open software aligned with the O-RAN Alliance’s open architecture. As a new open source community under the Linux Foundation, the O-RAN SC is sponsored by the O-RAN Alliance, and together they will develop open source software enabling modular, open, intelligent, efficient, and agile disaggregated radio access networks. The initial set of software projects may include: near-real-time RAN intelligent controller (nRT RIC), non-real-time RAN intelligent controller (NRT RIC), cloudification and virtualization platforms, open central unit (O-CU), open distributed unit (O-DU), and a test and integration effort to provide a working reference implementation. Working with other adjacent open source networking communities, the O-RAN SC will enable collaborative development across the full operator network stack.

Background: The telecom industry is experiencing a profound transformation and 5G is expected to radically change how we live, work, and play. This means it’s critical to make network infrastructure commercially available as quickly as possible to ensure business success for operators. It’s time to turn to open source, as it is one of the most efficient ways to accelerate product development in a collaborative and cost-efficient way.

“This collaboration between the O-RAN Alliance and the Linux Foundation is a tremendous accomplishment that represents the culmination of years of thoughtful innovation around the next generation of networks,” said Andre Fuetsch, Chairman of the O-RAN Alliance, and President of AT&T Labs and Chief Technology Officer at AT&T. “The launch of the O-RAN SC marks the next phase of that innovation, where the benefits of disaggregated and software-centric platforms will move out to the edge of the network. This new open source community will be critical if 5G is to reach its full potential.”

“We are really excited to see the establishment of the O-RAN Open Source Community,” said Chih-Lin I, chief scientist of China Mobile, co-chair of the O-RAN Technical Steering Committee and member of the Executive Committee of the O-RAN Alliance. “The O-RAN Alliance is aiming at building an ‘Open’ and ‘Smart’ Radio Access Network for future wireless systems. From day one, the Alliance has embraced open source as one of the most powerful means to achieve its vision. The O-RAN Open Source Community is the fruit of a yearlong extensive deliberation between the O-RAN Alliance and the Linux Foundation. We believe that the power of open source will further the momentum and accelerate the development, test, commercialization and deployment of O-RAN solutions.”

“We are excited to collaborate with O-RAN Alliance in bringing communities together to create software for this important access area of Telecommunications,” said Arpit Joshipura, general manager, Networking, Edge & IOT, the Linux Foundation. “This step towards execution marks another major milestone in networking partnerships across standards and open source organizations.”

About O-RAN Alliance

The O-RAN Alliance is a world-wide, carrier-led effort to drive new levels of openness in the radio access network of next generation wireless systems. Future RANs will be built on a foundation of virtualized network elements, white-box hardware and standardized interfaces that fully embrace O-RAN’s core principles of intelligence and openness. An ecosystem of innovative new products is already emerging that will form the underpinnings of the multi-vendor, interoperable, autonomous RAN, envisioned by many in the past, but only now enabled by the global industry-wide vision, commitment and leadership of O-RAN Alliance members and contributors.

More information about O-RAN can be found at www.o-ran.org.

About the Linux Foundation

Founded in 2000, the Linux Foundation is supported by more than 1,000 members and is the world’s leading home for collaboration on open source software, open standards, open data, and open hardware. Linux Foundation’s projects are critical to the world’s infrastructure including Linux, Kubernetes, Node.js, and more. The Linux Foundation’s methodology focuses on leveraging best practices and addressing the needs of contributors, users and solution providers to create sustainable models for open collaboration. For more information please visit us at www.linuxfoundation.org.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Assessment of Open Networking:

While Open Source Software (e.g. ONAP from ONF, Sonic from OCP) and Hardware (from OCP, TIP, Open RAN consortiums, ONF, etc) for networking is advancing rapidly, Open Networking via SDN, NFV, SD-WAN is really a euphemism for closed networking. That’s because almost all such “Open Networks” are proprietary to either the service provider (e.g. Amazon, Google, AT&T, etc) or SD-WAN vendor (many).

Some hyper-scale cloud providers (e.g. Microsoft) use a mix of open source software and purpose built proprietary software. Others (like Amazon and Google) use only their own (proprietary) software. Open Networking hasn’t much of an impact on the enterprise network yet, because of complex support and training issues. It seems like the main beneficiary of open networking will be Facebook (which started the OCP and TIP) and global telcos/ISPs (e.g. Yahoo Japan).

Telco Focused Open Source Projects:

Telcos such as AT&T, Verizon, China Mobile, DTK, and others have embraced open source technologies to move faster into the future. And LF Networking is at the heart of this transformation. AT&T seems to be the leading open source software telco. The company contributed their own software on virtual networks as ONAP to the Linux Foundation. The project is now being used by in production by other companies, and AT&T in return is benefiting from the work the competitors are doing to improve the code base.

AT&T also led the effort on Project CORD (Central Office Rearchitected as a Data center). CORD combines NFV, SDN, and the elasticity of commodity clouds to bring data center economics and cloud agility to the Telco Central Office. CORD lets the network operator manage their Central Offices using declarative modeling languages for agile, real-time configuration of new customer services. Major service providers like AT&T, SK Telecom, Verizon, China Unicom and NTT Communications are already supporting CORD.

AT&T contributed to the Open Networking Foundation (ONF) work on multi-gigabit PON virtual optical line termination hardware abstraction (VOLTHA), which is an open source software stack for PON networks. ONF is now working on integrating the ONAP operating system with multi-gigabit passive optical networks. ONAP was created by the merger of the Open ECOMP platform created by AT&T Labs with a similar, preexisting open source development project.

AT&T and the ONF will build on ongoing field trials of XGS-PON technology designed to support speeds up to 10 Gbps. The current XGS-PON trial is testing multi-gigabit high-speed internet traffic and providing AT&T DirecTV NOW video to trial participants. “Collaboration and openness across AT&T, the ONF and VOLTHA teams will be key to bringing this 10 Gbps broadband network to customers faster,” said Igal Elbaz, AT&T senior vice president of wireless network architecture and design, in the press release. “Now that we’ve proven the viability of open access technology in our trials, we can start the integration with our operations and management automation platform – ONAP.

ONF also provides a variety of Reference Designs, which are are “blueprints” developed by ONF’s Operator members to address specific use cases for the emerging edge cloud. Each Reference Design is backed by specific network operator partner(s) who plan to deploy these designs into their production networks and will include participation from invited supply chain partners sharing the vision and demonstrating active investment in building open source solutions.

The Telecom Infra Project aims to collaborate on building new technologies, examining new business approaches, and spurring investment in the telecom space. TIP Project Groups are divided into three strategic networks areas that collectively make up an end-to-end network: Access, Backhaul, and Core and Management. TIP members include operators, suppliers, developers, systems integrators, startups, and other entities that have joined TIP to build new technologies and develop innovative approaches for deploying telecom network infrastructure. Most telco members are outside the U.S. However, Century Link, Cox Communications, Sprint, and Windstream are U.S. based members. Representatives from Deutsche Telekom, BT, Vodafone, and Telefonica are on the TIP Board of Directors.

———————————————————————————————————————————————————————————–

References:

https://techblog.comsoc.org/category/open-source-telecom-software/

AT&T, ONF Collaborate on Virtualized Multi-Gigabit PON Service Automation