Will “AI at the Edge” transform telecom or be yet another telco monetization failure?

New Telco Opportunity – AI at the Edge:

At MWC 2026 last week, there were a flurry of claims that “AI at the Edge” would transform the telecom industry. One of many examples is an article titled, “The AI edge boom is giving telecom a new strategic role.” In that piece, Jeff Aaron, vice president of product and solutions marketing at Hewlett Packard Enterprise (HPE) spoke with theCUBE’s John Furrier at MWC Barcelona, during an exclusive broadcast on theCUBE, SiliconANGLE Media’s livestreaming studio. They discussed telecom edge AI and why networking is becoming a strategic foundation for data-centric services. Aaron said:

“A big reason for [reignited interest in routing] is AI workloads. They’re moving everywhere now. They have to move to the edge. For them to move to the edge, you’ve got to get them outside of the factory and to all the locations. We’re right in the core of that, and it’s super exciting.”

As AI expands to the edge, data will need to move not only to local compute, but also between many distributed edge sites, making routing paramount. There are four ways AI infrastructure is scaling — inside data centers and across distributed edge locations, according to Aaron.

“There’s scale-out, scale-across, scale-up, and on-ramp. Two are within the data center — scale-out and scale-up — but scale-across and edge on-ramp basically mean you got to figure out how to connect to those areas, and those are just networking,” he added.

Scale-across refers to connecting distributed data centers and edge locations, while edge on-ramp brings remote sites such as factories or branch locations into the network to access AI services. Supporting those distributed environments creates an opportunity for HPE to bring networking and compute together into a more integrated infrastructure stack. At MWC 2026 Barcelona, those trends are clearly coming into focus, according to Aaron.

“Data is moving everywhere right now, and the network is back. The network isn’t just plumbing. The network is how you build a value-added service using an AI workload as a telco infrastructure,” he added.

Telecom carriers are now urgently trying to move from being “dumb data pipes” to becoming “AI performance platforms” by leveraging their geographically distributed infrastructure to host AI closer to the end user. They urgently want to pivot from selling just bandwidth and connectivity to selling outcomes and intelligence with a heavy focus on industrial and enterprise-specific edge deployments. They are considering the following services and business models:

- Infrastructure as a Service (IaaS) & GPUaaS: Offering raw computing power, specifically GPUs, from edge data centers to enterprises that need low-latency processing without building their own facilities.

- Sovereign AI Clouds: Providing AI services that guarantee data remains within national borders, appealing to government and highly regulated sectors like finance and healthcare.

- API Monetization: Exposing real-time network data (e.g., location intelligence, predictive network quality, fraud risk scoring) via APIs that enterprises pay to integrate into their own applications.

- Outcome-Based Pricing: Charging for specific business results, such as a “guaranteed video call quality” or “fraud loss reduction share,” rather than just data usage.

- AI-as-a-Service (AIaaS): Bundling pre-trained models or specialized AI agents (e.g., for customer service or industrial monitoring) with connectivity

Major Carrier AI Edge Deployment Plans:

- AT&T:

- Launched Connected AI for Manufacturing in March 2026, which unifies 5G, IoT, and generative AI to provide real-time fault detection (claiming a 70% reduction in waste).

- Deploying “Edge Zones” in major U.S. cities (Detroit, LA, Dallas) to allow developers to run low-latency, cloud-based software locally.

- Partnering with AWS to link fiber and 5G directly into AWS environments for distributed AI workloads.

- Verizon:

- Unveiled Verizon AI Connect, a suite of products designed to manage resource-intensive AI workloads for hyperscalers like Google Cloud and Meta.

- Trialing V2X (Vehicle-to-Everything) platforms to provide carmakers with standardized APIs for low-latency edge processing in autonomous driving.

- Collaborating with NVIDIA to integrate GPUs into private 5G networks for on-premise AI inferencing in robotics and AR.

- SK Telecom (SKT):

- Announced an “AI Native” strategy at MWC 2026, including a roadmap for AI-RAN (Radio Access Network) that uses GPUs to optimize network performance and host user AI apps simultaneously.

- Building a Manufacturing AI Cloud powered by over 2,000 NVIDIA RTX GPUs to support digital twin simulations and robotics.

- Expanding AI Data Centers (AIDC) across South Korea and Southeast Asia (Vietnam, Malaysia) using energy-optimized LNG-powered facilities.

- Orange & Deutsche Telekom:

- Deploying AI-powered planning tools to cut fiber rollout costs and optimize site power consumption by up to 33% using AI “Deep Sleep” modes.

- Focusing on Sovereign AI strategies to ensure data governance for European enterprise customers.

- Vodafone:

- Utilizing AI/ML applications for daily power reduction at 5G sites and testing autonomous network healing via AI agents

- BT:

- Offers 5G-connected VR for manufacturing design teams (e.g., Hyperbat) to collaborate on 3D models in real-time.

| Product Category | Primary Target | Key Value Proposition |

|---|---|---|

| AI-RAN | Industry 4.0 | Seamless, ultra-low latency for robotics and sensing. |

| Connected AI Platforms | Manufacturing | Real-time predictive maintenance and waste reduction. |

| AI-as-a-Service (AIaaS) | Developers/SMBs | Access to GPU power and pre-trained models via telco edge nodes. |

| Network Slicing APIs | App Developers | Programmatic control over bandwidth for AR/VR and gaming. |

…………………………………………………………………………………………………………………………………………………………………………………………..

A Dissenting View of “AI at the Edge”:

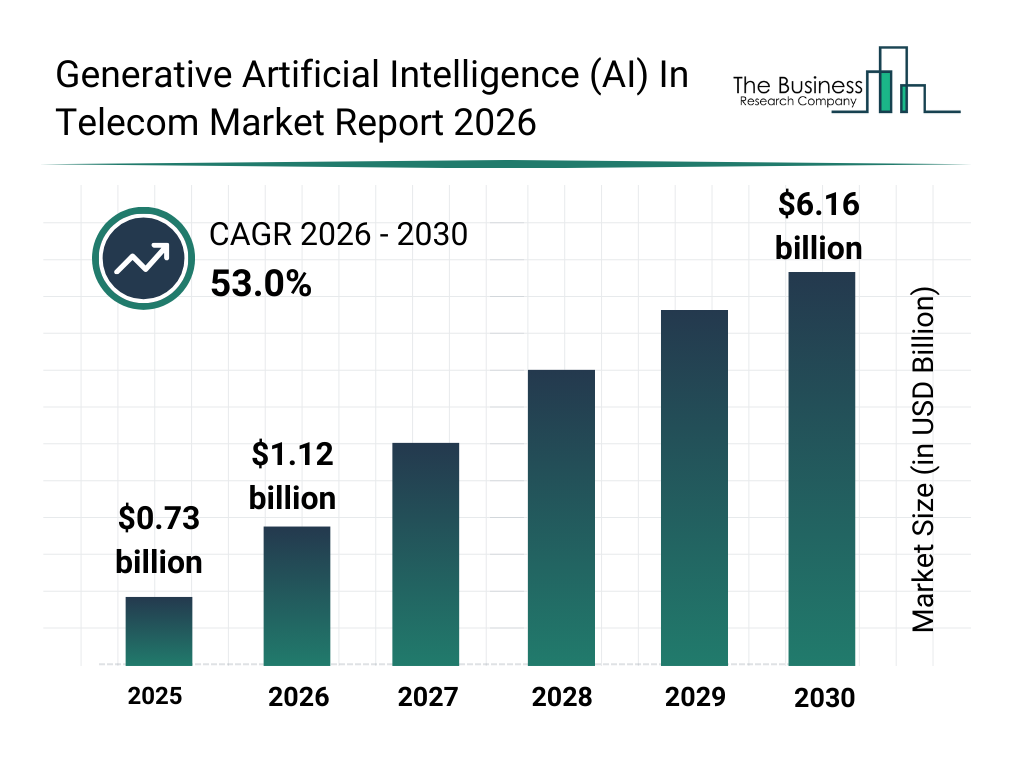

The global market for AI within the global telecommunications sector is valued at $6.69 billion in 2026, growing at a compound annual rate (CAGR) of 41.9% from 2025. The broader edge AI market—including hardware, software, and services—is forecast to reach $29.98 billion in 2026, according to The Business Research Company. We think those estimates are way too high.

The market research firm states:

………………………………………………………………………………………………………

Author’s Opinion:

Unless telcos change their corporate culture along with slowing the footprint growth of cloud service providers/hyperscalers, we think that AI at the Edge will be yet another telco monetization failure. Just like their failure to monetize: 4G LTE apps, the telco cloud, 5G, multi-access edge computing (MEC), OpenRAN, LPWANs and other telecom technologies that never lived up to their promise and potential.

That’s largely because telcos are very weak: developing IT platforms, compute services, killer applications, and rapid execution of new services (e.g. 5G services require a 5G SA core network which telcos were very slow to deploy). Telecom execs themselves cite cultural and speed‑of‑change issues: the industry is not organized like a software company, so it struggles to iterate products at AI/cloud pace. Also, telcos historically struggle with software. Managing distributed GPU clusters is vastly different from managing cell towers.

After spending billions on 5G with very little or no ROI, investors are skeptical of the increased capex required for AI-grade edge servers which must be maintained by telcos. Those servers will be expensive (especially if they contain clusters of Nvidia GPUs) and consume a lot of power, which is a critical issue at the edge of the carrier’s network.

Many network operators frame AI/edge as “network optimization” or “utilizing underused sites,” not as building monetizable AI platforms with APIs, SDKs, and ecosystems. This mirrors 5G, where huge RAN/core builds were not matched by a clear product and platform strategy, leaving value to OTTs and hyperscalers which are extending their control planes and protocol stacks to the network edge (local zones, operator co‑lo, on‑premises stacks).

Telcos risk becoming “dumb pipes” for AI traffic if they can’t provide a superior developer ecosystem. If they only sell space/power/connectivity, the cloud service providers will continue to own the developer and AI value chain. Analysts warn that edge is a “right to participate, not a right to win.” As such, value accrues to whoever owns the AI platform, tools, marketplace, and pricing power, not the entity that provides connectivity, PoP or cell towers.

Data fragmentation and weak “intelligence” layer:

-

AI monetization depends on high‑quality, cross‑domain data, but telco data is fragmented across OSS, BSS, probes, and partner systems; without unification, it is hard to expose compelling network/edge intelligence services.

-

Analysts emphasize that failure here reduces telcos to generic GPU landlords, while higher‑margin offers (real‑time quality, fraud, identity, mobility/context APIs) remain unrealized.

Narrow internal focus on cost savings:

-

Many operators’ early AI focus is inward (Opex reduction in assurance, planning, customer care) rather than building external, revenue‑generating products, echoing how early 5G was justified mainly on cost/efficiency.

-

Commentators warn that if AI/edge remains a “network efficiency” play, the commercial upside will go to cloud/AI natives that turn similar capabilities into products sold to enterprises.

What analysts say telcos must do differently:

-

Build “Sovereign AI factories” and edge AI clouds: GPU‑enabled sites with cloud‑like developer experience (APIs, self‑service portals, metering, SLAs) and clear sovereign/regional guarantees.

-

Combine differentiated connectivity with AI services (latency‑backed SLAs, AI‑on‑RAN, domain‑specific models for verticals) and use modern, flexible commercial models instead of just selling bandwidth or colocation.

Conclusions:

In summary, the main risk for telcos is to successfully transition from owning and maintaining network infrastructure to owning and operating AI platforms and products at software industry speed. AI at the edge is less of a new service or product and more an architectural upgrade. The two ways telcos can benefit are from:

- Internal cost reduction: If telcos use it to lower their own costs (fraud prevention, risk management, predictive maintenance, fault isolation, self-healing networks, etc.), it’s an automatic win but won’t increase the top line.

- Revenue from new AI -Edge services, e.g. Verizon uses edge-based video analytics in warehouses to improve inventory turnover by up to 40%. If they expect to charge a massive premium for “AI-enabled 5G,” they face the same monetization wall that has doomed them for the past 20 years!

References:

https://siliconangle.com/2026/03/04/telecom-edge-ai-makes-networking-strategic-mwc26/

https://www.nvidia.com/en-us/lp/ai/the-blueprint-for-ai-success-ebook/

AT&T and AWS to deliver last mile connectivity for AI workloads; AT&T Geo Modeler™ AI simulation tool

Analysis: Edge AI and Qualcomm’s AI Program for Innovators 2026 – APAC for startups to lead in AI innovation

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Private 5G networks move to include automation, autonomous systems, edge computing & AI operations

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Dell’Oro: RAN revenue growth in 1Q2025; AI RAN is a conundrum

Nvidia AI-RAN survey results; AI inferencing as a reinvention of edge computing?

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

CES 2025: Intel announces edge compute processors with AI inferencing capabilities

4 thoughts on “Will “AI at the Edge” transform telecom or be yet another telco monetization failure?”

Leave a Reply to Ken Pyle Cancel Reply

The Broadband Forum has ongoing standards work regarding far-edge computing and the implementation of AI in the network to improve efficiency and quality of experience. Broadband Forum Service Requirements provides a high-level overview in this brief video:

https://www.broadband-forum.org/video-insights/quality-on-demand-ai-and-edge-computing-a-service-requirements-update/

It’s doubtful the telcos can compete against the hyperscalers in deploying edge AI, but we don’t know for sure.

Some pundits use the phrase “AI will eat itself,” which refers to the potential for AI models to experience a phenomenon known as “model collapse,” where they learn from their own outputs, leading to a decline in performance and accuracy.

This occurs when AI-generated content is used to train subsequent models, causing them to rely on increasingly less varied and less accurate data.

As a result, the quality of the AI’s outputs diminishes, and the models may produce nonsensical or repetitive content. This situation raises concerns about the reliability and ethical implications of AI technologies, as they may become increasingly dependent on their own outputs for training, ultimately leading to a degradation in their capabilities.

https://techcrunch.com/2024/07/24/model-collapse-scientists-warn-against-letting-ai-eat-its-own-tail/

Roughly $1 for every $5,000 created by the AI economy went to telcos:

AI generated $1.5 trillion revenue in 2025. At best, telecom operators captured about $300 million in direct AI revenue. Even if the definition is stretched to include connectivity and other indirect services, the most optimistic estimates reach around $4 billion. The sense of déjà vu is hard to ignore.

https://sebastianbarros.substack.com/p/for-every-5000-spent-on-ai-telcos

SoftBank Corp. Announces Telco AI Cloud

Telco AI Cloud is an AI infrastructure vision that integrates a large-scale AI data center platform powered by a GPU (Graphics Processing Unit) cloud, an AI-RAN-based MEC (Multi-access Edge Computing) platform, and a software stack for AI data centers*1 called “Infrinia AI Cloud OS.” By optimizing AI processing from training to inference and utilizing its nationwide telecommunications infrastructure, SoftBank will build a distributed AI infrastructure that delivers low latency, high reliability, and sovereign capability (data sovereignty). Through its Telco AI Cloud vision, SoftBank aims to evolve beyond the traditional role of a telecommunications operator and become an AI infrastructure provider.

https://www.softbank.jp/en/corp/technology/research/topics/202/