Month: April 2026

Will 2026 be the “Year of the AI Ontology” for telecoms?

Overview:

For the telecommunications industry, many pundits say 2026 will be the year of “AI Ontology [1.],” primarily because a standardized knowledge plane is now seen as the “ultimate driver” for reaching higher levels of network autonomy. Industry experts from companies like Telstra and Amdocs emphasize that for agentic AI to move from isolated pilots to enterprise-scale operations, it requires a structured, explainable, and typed world model—an ontology—to unify data across fragmented systems.

Note 1. An ontology in AI is a formal, machine-readable framework that defines the concepts, properties, and relationships within a specific domain to enable knowledge sharing, reasoning, and semantic understanding. It structures data into a network of “things” (classes) rather than just files, acting as a “Rosetta stone” that allows AI systems to understand context, infer conclusions, and act on data.

…………………………………………………………………………………………………

Several network providers are adopting a “standardized, ontology-driven knowledge plane” to enable agentic AI to operate across traditionally siloed network systems. This shift in 2026, is driven by the need for Level 4 and 5 network autonomy, where agents require a common language to reason about network states and business intents.

1. Mark Sanders, Telstra’s chief architect, talked about the emergence of a structured, explainable knowledge plane that removes silo barriers between agents, freeing them up to become the workhorses of network automation. “We think for the autonomous network to reach level four or five is going to require a standardized, ontology-driven approach on the knowledge plane,” said Sanders at a recent Ericsson conference, touting this approach as the ultimate driver in next-level autonomous networks.

2. For BT, agentic AI is already yielding tangible results in IT service desks, especially as organizations shift from assistance to execution, according to Girish Mahajan, senior leader for mobile AI data/automation. In particular, AI agents have reduced trouble ticket resolution times. “It has reduced the time of the manual effort, and it has also increased efficiency of the service desk,” he said. However, same autonomy that drives value also introduces unpredictability.

“The outcome of agentic AI is something unpredictable because it’s continuously adapting during execution,” he said, adding a call for better design principles. “We need reflection-based architecture, and we need better AI/human collaboration. AI agents should learn from their actions and should work along with humans in their day-to-day.”

3. For Vodafone, work has revolved around lighthouse projects: small-scale efforts to demonstrate the value of a larger business use case.

“It’s quite a mundane use case around energy cost recovery. So obviously, energy is a huge operational expense for our industry,” said Simon Norton, digital/OSS engineering director, Vodafone Group. “It’s very complex, especially when you’re working in that multi-market environment, to manually compare line by line with energy bills against your own data sets.”

Vodafone’s AI agents, therefore, have been automatically ingesting bills and comparing them to identify any tariff anomalies.

“It’s mundane but actually super valuable,” said Norton, who stressed operators should find a project with a clear value proposition and get it out into production quickly. “You build the credibility, you start to get the funding into the system, and it buys you the time to work on that longer-term strategy.”

………………………………………………………………………………………..

- From Assistant to Doer: AI is evolving from a “helper” that provides insights to a “doer” that autonomously observes, decides, and executes actions within governed boundaries.

- Multi-Agent Orchestration: 2026 will see the rise of coordinated multi-agent ecosystems. These systems require an ontology to ensure that a “planner agent” can accurately break down goals for specialized “worker agents” without semantic confusion.

- Intent-Based Orchestration: To ensure network stability, telcos are adopting intent-based orchestration layers. These layers use ontologies to provide the deterministic, model-driven framework necessary to ground agent actions in real-world business intent.

- Network Autonomy: CSPs are aiming for TM Forum Level 3 or 4 autonomy by late 2026, using agents to turn intent into outcomes in live networks.

- Operational Leverage: Rather than massive headcount cuts, agentic AI is providing “operational leverage,” allowing teams to manage growing network complexity with the same workforce.

- Measurable ROI: Investments are focusing on high-impact areas like autonomous incident handling (30-40% cost reduction) and predictive maintenance (up to 40% fewer outages).

- Structured Knowledge Plane: Operators are shifting toward a standardized, ontology-driven knowledge plane to remove silo barriers between agents. This allows multiple specialized agents to collaborate on “broader, bigger outcomes” like root cause analysis across billing, CRM, and network systems.

- Enabling Agentic Autonomy: While 2025 focused on “agentic AI” as a buzzword, 2026 is about the foundational infrastructure—specifically graph-based data systems and digital twins—that gives agents the “executable semantics” they need to plan and act safely.

- Unified Truth for Agents: Without a central ontology, horizontal AI platforms often suffer from “agent drift,” where different agents interpret the same business logic (e.g., “unlimited plan”) differently, leading to billing and provisioning errors.

Ericsson’s View:

Hassan Iftikhar, Ericsson’s head of product domain data & analytics, called for better hyperscaler collaboration on scale, foundational cloud, and AI capabilities.

“The AI tooling, the security framework, we use those to industrialize and put agents into production… It’s pretty much an ecosystem that works together,” he said. At the panel, the data head revealed the vendor’s role in the agentic ecosystem through the use case of one operator needing help with catalog management, as well as scarce developer skills.

“They wanted to take the pain out of product configuration. So we designed a multi-agentic system where it basically helps product managers and marketers to configure and publish new instances through an actual language. So very complex catalog engineering, which can take weeks, is reduced to hours where you can search for reuse and launch.”

Iftikhar also revealed an OSS tool to help one operator’s engineers to diagnose and resolve issues within their operational instances – resulting in an agent that was seemingly too autonomous for the client.

“We put this use case together, basically taking an intent from an operations engineer, such as data diagnostics, and into it, we built the ability to take remediation actions automatically. What we sort of decided from that was a bit of a step too far to just throw that to an operations department for it to autonomously take steps. So we actually had to go in and build guardrails to limit that capability to a human oversight capability.”

“I think what we learned is that we have to sort of build that confidence in the team step by step before we can actually go to fully autonomous operation. Our learning from adjusting that use case was to be practical and adapt very quickly to what the business really needs.”

…………………………………………………………………………………

References:

https://www.sdxcentral.com/analysis/has-telco-already-faced-the-year-of-ai-agents/

The Financial Trap of Autonomous Networks: Scaling Agentic AI in the Telecom Core

Telecom operators investing in Agentic AI while Self Organizing Network AI market set for rapid growth

Nokia to showcase agentic AI network slicing; Ericsson partners with Ookla to measure 5G network slicing performance

T-Mobile US announces new broadband wireless and fiber targets, 5G-A with agentic AI and live voice call translation

Ericsson integrates Agentic AI into its NetCloud platform for self healing and autonomous 5G private networks

Agentic AI and the Future of Communications for Autonomous Vehicles (V2X)

AWS to deploy AI inference chips from Cerebras in its data centers; Anapurna Labs/Amazon in-house AI silicon products

Using AI, DeepSig Advances Open, Intelligent Baseband RAN Architectures

Using advanced AI techniques, DeepSig has reportedly managed to eliminate a mobile network’s pilot signal, thereby removing signaling overhead without degrading overall performance. Founded in 2016, the U.S.-based startup occupies a leading position at the intersection of artificial intelligence (AI) and the radio access network (RAN), developing data-driven models that could supplant traditional, human-engineered signal processing algorithms.

This work has become especially relevant as the telecom industry moves toward open and software-defined RAN architectures. DeepSig is now a visible contributor to OCUDU (Open Centralized Unit Distributed Unit), an open-source initiative announced by the Linux Foundation in collaboration with the U.S. Department of Defense and its FutureG ecosystem partners to accelerate open CU/DU development for 5G and early 6G systems. OCUDU is intended to establish a carrier-grade reference platform for baseband software, with support for AI-based algorithms and solutions embedded in the RAN compute stack.

As AI becomes a central theme across the telecom ecosystem, DeepSig has rapidly moved from relative obscurity to prominence through collaborations with major industry and government stakeholders. Most recently, the company emerged as a key contributor to OCUDU—the Open Central Unit Distributed Unit initiative announced by the Linux Foundation and the U.S. Department of Defense (DoD) ahead of MWC Barcelona 2026. The program’s goal is to introduce open-source software elements into the RAN baseband domain, an area historically dominated by proprietary offerings from Ericsson, Nokia, and Samsung. By lowering barriers to entry, OCUDU aims to foster innovation and enable smaller players like DeepSig to participate more freely in the U.S. baseband ecosystem.

Image Credit: DeepSig

DeepSig was identified, alongside Ireland-based Software Radio Systems (SRS), as one of two startups selected to deliver OCUDU’s initial software stack. “The National Spectrum Consortium had an RFQ for developing an open-source stack,” explained Jim Shea, DeepSig’s CEO. “SRS already had a capable baseline, but it needed to be elevated to carrier-grade—adding new features and strengthening reliability,” he added.

Meanwhile, major vendors Ericsson and Nokia were named “premier members” of the new OCUDU Ecosystem Foundation. While both could, in principle, leverage the platform to integrate third-party components into their baseband systems, industry observers remain skeptical that these incumbents will fully embrace open-source alternatives over their established proprietary stacks. In comments at MWC, Nokia CEO Justin Hotard characterized OCUDU as a welcome ecosystem evolution to accelerate innovation but clarified that “not everything necessarily needs to be open source.”

Driven in part by DoD interests, OCUDU reflects broader U.S. government ambitions to ensure that 5G and future 6G networks remain open to domestic innovation, particularly for defense and mission-critical use cases. For vendors like Ericsson and Nokia—who view defense markets as increasingly strategic—this alignment could bring both opportunity and complexity.

DeepSig’s trajectory extends beyond OCUDU. The company’s technology originated from research by Tim O’Shea, now CTO, during his tenure at Virginia Tech, where he explored deep learning’s application to wireless signal processing. “You can apply deep learning to enhance the way communication systems operate by replacing many of the traditional algorithms,” said Jim Shea. While these methods do not circumvent theoretical limits such as Shannon’s Law, small efficiency gains can yield substantial operational and economic benefits for cost-sensitive mobile operators.

As DeepSig and peers continue to redefine how intelligence is integrated into the RAN, their work signals a shift toward AI-native architectures—where machine learning, rather than handcrafted algorithms, becomes the foundation for next-generation network optimization.

References:

https://www.lightreading.com/5g/small-deepsig-is-at-heart-of-ai-ran-challenge-to-ericsson-nokia

Accelerating 5G vRAN, AI-RAN, and 6G on OCUDU, “the Linux of RAN”

AI-RAN Reality Check: hype vs hesitation, shaky business case, no specific definition, no standards?

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

InterDigital led consortium to advance wireless spectrum coexistence & sharing

Telecom sessions at Nvidia’s 2025 AI developers GTC: March 17–21 in San Jose, CA

Sources: AI is Getting Smarter, but Hallucinations Are Getting Worse

Huawei FY2025: 2.2% YoY revenue increase; strategic pivot to AI and intelligent automotive solutions

Overview:

Huawei has released its 2025 audited financial results, reporting total revenue of CNY 880.9bn ($127.6bn) — a 2.2% YoY increase. The report highlights a significant expansion in profitability, with operating profit surging 22.1% to CNY 96.9bn ($14bn). That translated to an operating profit margin of 11%, up 180 bps from the 9.2% recorded in 2024.

Image Credit: Imago/Alamy Stock Photo

……………………………………………………………………………………………….

“In 2025, Huawei’s overall performance remained steady,” said Sabrina Meng, Huawei’s Rotating Chairwoman. “I would like to thank our customers for your ongoing trust and support. Thanks also to consumers for choosing Huawei, as well as suppliers, partners, and developers around the world for working with us. “Of course, we couldn’t do any of this without the support of every Huawei employee. Thank you for your hard work, and also your families for their steadfast support.”

In 2025, Huawei’s connectivity business weathered the impact of industry investment cycles, while its computing business continued to seize opportunities in AI. The consumer business worked to overcome formidable challenges, driving the HarmonyOS ecosystem to cross a new threshold in user experience. Huawei’s digital power business continued to place quality before all else. Huawei Cloud honed its competitiveness with a focus on core services, and the company’s intelligent automotive solutions grew rapidly.

………………………………………………………………………………………….

Pivot to Intelligent Automotive Solutions:

Huawei is aggressively diversifying and placing a massive strategic bet on the automotive sector to drive future growth. Its Intelligent Automotive Solutions business is experiencing explosive growth, with revenue increasing by over 400% in 2024 to 26.35 billion yuan ($3.62bn).

In 2025, the unit surged another 72% to CNY 45 billion (approx. $6.2bn). Huawei does not manufacture its own cars directly but operates as a top-tier supplier and technology partner (similar to “Bosch”) via its Harmony Intelligent Mobility Alliance (HIMA). Huawei continues to invest heavily in its “future-oriented” auto and AI businesses.

Revenue Breakdown by Segment & Geography:

- Infrastructure & Solutions: Remains the primary anchor, contributing 42.6% of total revenue (up 2.6% YoY).

- Consumer Business: Accounted for 39.1% of revenue, maintaining a steady recovery with 1.6% YoY growth.

- Intelligent Automotive Solutions (IAS): The high-growth outlier, with revenues spiking 72.1% YoY to CNY 45bn, now representing 5.1% of the total portfolio.

- Geographic Mix: Domestic China operations generated ~70% of revenue. International footprints were led by EMEA (18.3%), followed by Asia-Pacific (5.7%) and the Americas (4.2%).

R&D Intensity and Ecosystem Strategy:

Huawei continues to maintain one of the industry’s highest reinvestment rates, allocating CNY 192.3bn ($27.9bn) to R&D—a massive 21.8% of annual revenue. Huawei’s R&D expenditure rose 7% last year to an impressive RMB 192.3 billion (approximately $28 billion), representing nearly 22% of annual revenue.

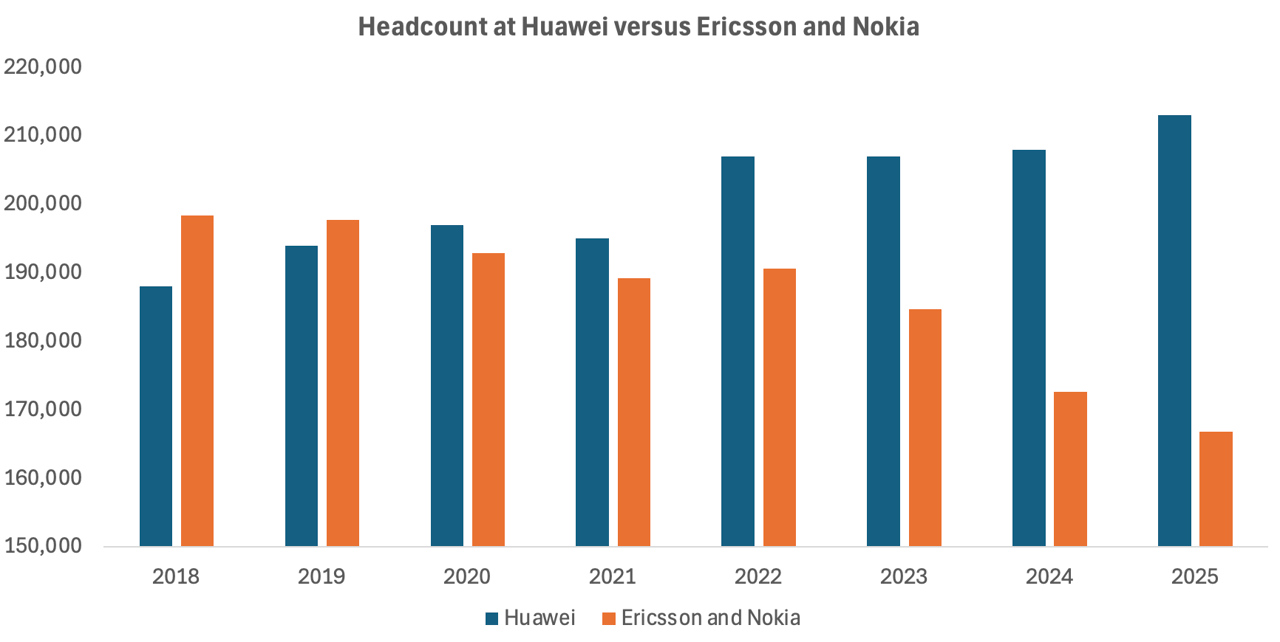

In sharp contrast, Ericsson—whose portfolio remains heavily centered on 5G—reduced its R&D outlay by 9% to SEK 48.9 billion (about $5.2 billion). At 21% of sales, Ericsson’s R&D intensity was largely in line with Huawei’s. Nokia, meanwhile, outpaced both rivals in relative terms, allocating 23% of revenue—roughly €4.6 billion ($5.3 billion)—to R&D, up 7% year over year. Most of that increase stemmed from the February 2025 acquisition of optical systems vendor Infinera, which expanded Nokia’s technology base and R&D footprint.

The huge divergence lies in workforce trends. As reported by Light Reading, Ericsson and Nokia have collectively shed nearly 28,000 positions since 2022, equivalent to about 15% of their combined headcount that year. While growing automation and AI integration have arguably improved operational efficiency, the scale of these reductions also reflects a cooling investment climate among operators. With telco spending on 5G deployments tapering off, Europe’s two large network equipment vendors are continuing layoffs.

In contrast, Huawei’s workforce has continued to increase as it has pushed into new industrial sectors. Since 2021, when Huawei suffered its worst-ever sales decline, the Chinese behemoth has added about 18,000 employees to its payroll, according to annual reports. Around 5,000 of them were recruited last year, including 1,000 in R&D alone. That resulted in 213,000 employees Huawei employees in 2025.

The increased hiring boosted overall operating costs, including R&D expenditure, by 7.2%, to about RMB334 billion ($48.5 billion).

Source & Graph Credit: Light Reading

………………………………………………………………………………………………………………….

Moving forward, China’s largest IT vendor’s roadmap prioritizes:

- Full-Stack AI Integration: Embedding AI and carrier-grade security across the entire product lifecycle and network architecture.

- Strategic Domain Expansion: Increasing CapEx and R&D in connectivity, cloud, and autonomous driving.

- Ecosystem Sovereignty: Scaling the Ascend (AI), Kunpeng (Computing), and HarmonyOS ecosystems to drive vendor-agnostic collaboration and industry-wide adoption

Meng stressed, “We are moving toward a future that is full of uncertainty, so we have to remain true to our strategy and maintain strategic focus. We will translate strategy to execution, keep cultivating the developer ecosystem, and pursue high-quality development.”

………………………………………………………………………………………………………………….

References:

https://www.huawei.com/en/news/2026/3/annual-report-2025

https://www.lightreading.com/5g/huawei-sales-growth-plummeted-in-2025-as-it-gained-5-000-workers

Huawei unveils AI Centric Network roadmap, U6 GHz products, 5G Advanced strategy and SuperPoD cluster computing platforms

Huawei, Qualcomm, Samsung, and Ericsson Leading Patent Race in $15 Billion 5G Licensing Market

Huawei Cloud Review and Global Sales Partner Policies for 2026

Huawei’s Electric Vehicle Charging Technology & Top 10 Charging Trends

Huawei to Double Output of Ascend AI chips in 2026; OpenAI orders HBM chips from SK Hynix & Samsung for Stargate UAE project

Omdia on resurgence of Huawei: #1 RAN vendor in 3 out of 5 regions; RAN market has bottomed

Huawei launches CloudMatrix 384 AI System to rival Nvidia’s most advanced AI system

U.S. export controls on Nvidia H20 AI chips enables Huawei’s 910C GPU to be favored by AI tech giants in China