Ericsson

AT&T/Ericsson Demonstrate 5G-Based ISAC for Drone Detection at World Cup Stadium

AT&T and Ericsson recently demonstrated the potential of 5G as a platform for integrated sensing and communications (ISAC) [1.] in support of critical infrastructure protection and public safety. The demonstration, conducted at a World Cup stadium near Dallas, TX highlights how cellular networks can evolve into dual-function systems that provide both connectivity and environmental sensing.

Note 1. Integrated Sensing and Communication (ISAC) is a flagship 6G/IMT 2030 capability that unifies mobile communication and environmental sensing into a single network. By using the same infrastructure, spectrum, and waveforms, 6G systems will act as spatially aware platforms. It allows networks to detect, track, and image objects while transmitting data. ITU-R officially designated ISAC as one of the six core usage scenarios in the IMT-2030 (6G) framework.

………………………………………………………………………………………………………………………………………………………………..

In this trial, AT&T and Ericsson (its primary RAN equipment supplier) employed 5G-based network sensing to detect and track unmanned aerial vehicles (UAVs) operating at altitudes between 300 and 400 feet in authorized airspace as they approached AT&T Stadium in Arlington, Texas. The approach reflects a joint communication and sensing (JCAS) paradigm, in which existing radio access network (RAN) infrastructure is leveraged for situational awareness without the need for dedicated radar or sensing overlays.

Ericsson deployed Massive MIMO radios across multiple sites to establish a “multi-static sensing configuration,” enabling spatial diversity and improved detection performance. By combining “sensing-enabled radio transmissions with advanced signal processing and AI-enabled sensing algorithms,” the system detected, localized, and tracked drones in real time. This capability exploits the propagation characteristics of RF signals used for communication, enabling object detection and tracking within the coverage footprint of the network.

Although no match was scheduled during the demonstration, AT&T Stadium has been a primary venue during the tournament and will host the semi-final between France and Spain later this week, providing a representative high-density and security-sensitive deployment context.

Cellular Sensing for Drone Mitigation:

Image Credit: AT&T

Unauthorized UAV activity has posed ongoing challenges for public safety authorities during the tournament. On match days, drone operations are prohibited within a one-nautical-mile radius of stadiums and up to 1,000 feet above ground level, according to the Federal Aviation Administration.

Reporting from the tech demo in Arlington, NBC 5 DFW indicated that U.S. authorities have detected approximately 1,500 drones and confiscated more than 700 across World Cup venues, including 53 in the vicinity of AT&T Stadium.

AT&T and Ericsson position cellular-based sensing as a complementary capability to existing counter-UAV systems deployed by law enforcement. While the Arlington Police Department indicated it was not directly involved in the demonstration, it acknowledged ongoing evaluation of emerging technologies that could enhance future operational capabilities, according to NBC 5 DFW.

Quotes:

Ildefonso de la Cruz, senior principal analyst at Omdia (owned by Informa-UK), characterized the demonstration as strategically timed and situated, noting its alignment with global attention on the World Cup and upcoming large-scale events such as the 2028 Summer Olympic Games in Los Angeles. “This demonstration shows that robust cellular infrastructure is the foundation to build reliable next-generation critical services for public safety and other critical infrastructure verticals,” he stated.

“As networks evolve, the opportunity is not just to prepare for 6G someday, but to begin introducing important building blocks now,” said Dyon Agnew, SVP and Head of Customer Unit AT&T, Ericsson Americas. “This demonstration with AT&T shows a product roadmap in action: using advanced 5G capabilities today to explore how sensing and connectivity can work together, then evolving those capabilities over time as the path to 6G becomes clearer.”

“Integrated sensing is an important part of the road to 6G, and this work helps show how we can start bringing that future to life right now,” said Yigal Elbaz, SVP and Network CTO, AT&T. “By working with Ericsson, we are exploring how advanced wireless networks can add sensing capabilities to connectivity in ways that could support safer operations, smarter venues, and stronger customer experiences, while creating a path to evolve these capabilities responsibly over time.”

………………………………………………………………………………………………………………………………………………….

Technical Takeaways:

-

Demonstrates early-stage ISAC/JCAS capabilities using commercial 5G Massive MIMO infrastructure, with implications for 6G-native sensing architectures.

-

Validates multi-static sensing configurations in cellular deployments, improving detection accuracy through spatial diversity.

-

Highlights the role of AI-driven signal processing in extracting sensing information from communication waveforms.

-

Suggests a pathway to cost-efficient sensing by reusing existing RAN assets, avoiding dedicated radar infrastructure.

-

Reinforces the potential for cellular networks to support public safety and critical infrastructure monitoring as a value-added service layer.

…………………………………………………………………………………………………………………………………………………

“Integrated sensing is an important part of the road to 6G, and this work helps show how we can start bringing that future to life right now,” said Yigal Elbaz, SVP and Network CTO, AT&T. “By working with Ericsson, we are exploring how advanced wireless networks can add sensing capabilities to connectivity in ways that could support safer operations, smarter venues, and stronger customer experiences, while creating a path to evolve these capabilities responsibly over time.”

What this roadmap will enable over time:

- Help event and facility teams improve planning and staffing by providing broader visibility into how vehicles move through large environments.

- Enhance coordination around temporary event infrastructure and logistics by adding network-based environmental awareness alongside connectivity.

- Support a wide-area drone awareness system for public-sector stakeholders, improving visibility into low-altitude drone activity as the low-altitude economy develops across cities and regions.

- Inform the evolution of future 5G and 6G capabilities as sensing and communications mature together for large venues, enterprises, governments, and public-sector environments.

Conclusions:

AT&T and Ericsson will continue exploring how sensing capabilities can be introduced pragmatically using existing network foundations, then advanced over time as standards, ecosystems, and market needs develop.

The goal is to help shape a practical path where future 6G/IMT 2030 capabilities are not treated as a distant leap, but as an evolution that can begin delivering value well before full 6G/IMT 2030 commercialization.

………………………………………………………………………………………………………………………………………………..

References:

https://about.att.com/story/2026/att-ericsson-drone-detection.html

https://www.lightreading.com/5g/att-and-ericsson-demo-5g-sensing-for-drone-detection

https://www.linkedin.com/feed/update/urn:li:activity:7481460850159943680/ by Yigal Elbaz, of AT&T

https://www.itu.int/en/ITU-R/study-groups/rsg5/rwp5d/imt-2030/pages/default.aspx

Analysis: Cohere’s $28M U.S. DoD FutureG ISAC contract; OTFS vs OFDM; 6G-NR/IMT 2030 RIT standards outlook

Analysis & Implications of the Communications Cybersecurity Information Sharing and Analysis Center (C2 ISAC)

Network X Americas: AT&T and Comcast reveal huge AI impact on network operations

Analysis: AT&T’s $250B network investment to advance U.S. connectivity

AI-RAN and Agentic AI get real: Ericsson, Nokia, Verizon & other operators enter into a new network automation era

Analysis: Ericsson’s leading role in French INTENTION 6G project

Ericsson’s R&D center in France is leading INTENTION-6G, a project worth more than €12 million over four years. It’s backed by the France 2030 plan to embed AI into RAN control for energy efficiency and intent-based operation. Partners include Orange, BubbleRAN and CentraleSupélec.

INTENTION 6G aims to optimize energy consumption of the Radio Access Network (RAN) while meeting 5G/6G traffic requirements. At the heart of the project is the integration of artificial intelligence into network control, particularly at RAN level, to improve both performance and energy efficiency. The project has now reached its mid development phase, enabling the first technology building blocks to be defined.

INTENTION 6G is based on a public private partnership approach that combines industrial, academic and entrepreneurial expertise. The project makes it possible to design, test and validate new solutions through demonstrators and experimental platforms, with a view to their gradual integration into tomorrow’s networks.

Several key areas structure the work: advanced automation of network functions, dynamic optimization of energy consumption, and the development of so called “intent based” networks, capable of automatically adjusting their performance to usage and needs thanks to artificial intelligence.

Christian Leon, Head of Ericsson Western Europe, says:

“Mobile networks are evolving to meet ever increasing requirements in terms of performance, energy efficiency and resource optimization. With INTENTION 6G, Ericsson France’s R&D center is actively contributing, alongside leading French partners, to laying today the foundations for the networks that will support tomorrow’s critical use cases and digital transformations.”

-

- Intent-Based Networking (IBN): The project designs networks capable of automatically adjusting performance. Operators issue high-level business goals (intents) via language models, which the system automatically translates into exact technical configurations.

- Advanced Automation: AI takes over network control loops at the Radio Access Network (RAN) level. This shifts management from rigid, manual rules to real-time, zero-touch autonomous domain operations.

- Dynamic Energy Optimization: Mitigating the heavy carbon footprint of next-gen hardware is a priority. AI dynamically monitors traffic demands to initiate micro-sleep and scale down RAN energy use without dropping service quality.

- Standalone Native AI Architecture: It avoids complex legacy radio splitting by prioritizing a standalone architecture. AI components function pervasively across the edge-cloud continuum through a dedicated “AI interconnect”.

- Integrated Sensing and Communication (ISAC): Turning the network into a radar grid to track real-time physical environments.

- Mass-Market Immersive Experiences: Assuring low-latency and continuous data throughput for holographic communications and mixed reality (XR).

- Industry 5.0: Powering dynamic workgroup creation and traffic handling for mobile robot swarms, autonomous delivery drones, and smart factories.

……………………………………………………………………………………………………………………………..

Building on its R&D center in France, opened in 2020, Ericsson says it’s leveraging its expertise in next generation network technologies. The teams involved are particularly specialized in 6G research, AI native networks, critical networks and cybersecurity. The center has already contributed to a portfolio of more than 180 patents in mobile technologies and is part of a strong ecosystem of academic and industrial partners in France.

By mobilizing its innovation capabilities and drawing on a rich and committed ecosystem, Ericsson is helping to prepare a new generation of networks that are smarter, more flexible and more sustainable.

References:

https://www.ericsson.com/en/press-releases/3/2026/intention-6g

https://ieeexplore.ieee.org/document/10942858/

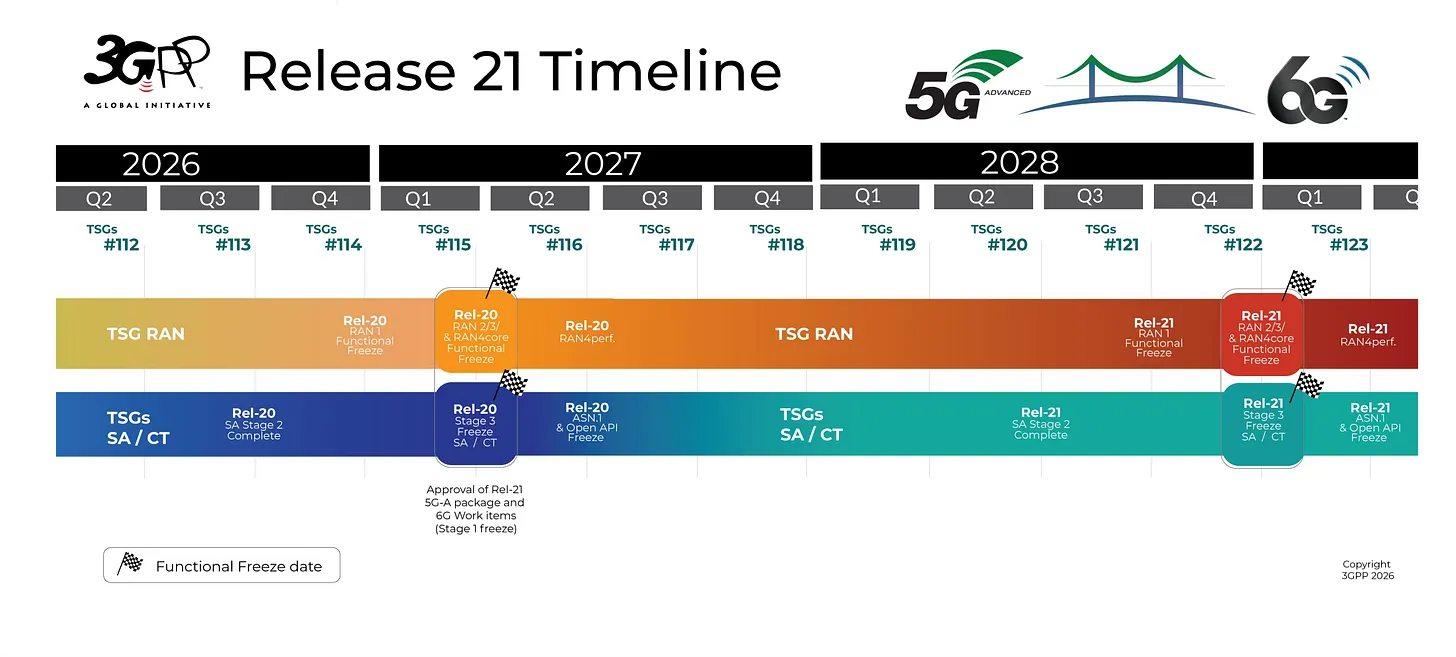

3GPP approves timelines for Release 21 which will specify 6G RAN, Core and 5G Advanced

At 3GPPs meeting last week in Singapore, Technical Specification Group (TSG) RAN #112 approved the full Release-21 timeline jointly proposed by the three TSG Chairs. On June 12th, more than 150 participants from the regions ICT community attended ‘3GPP 6G Standardization: From Study to Specification,’ featuring the combined technical leadership of 3GPP. Topics covered in the summit included the 3GPP Chairs’ analysis of progress this week on 5G Advanced work items and 6G studies across the TSGs. There were also expert overviews on some key topics: AI/ML, ISAC (integrated sensing and communications), Massive MIMO evolution, NTN standards cooperation and security considerations for the 3GPP 6G System.

This formally completes the first 6G study item in 3GPP and sets the stage for the third quarter this year in which 3GPP working groups must settle numerous questions, including the migration architecture that network operators have wanted a decision on for over a year. 3GPP TSG RAN Chairman Younsun Kim, PhD, Samsung, said during a joint session with the other two TSGs (SA and CT) that “no decisions were possible” on migration options, with input now hoped for at TSG RAN#113, scheduled for September 14–17, 2026 in Madrid, Spain. Vodafone warned in a 3GPP contribution titled, “Good migration option decisions in September need hardware impacting decisions now!” that the September decision point only works if the plenary stopped deferring decisions.

Some achievements at this 3GPP Singapore meeting:

- Over 590 standards delegates welcomed by our Hosts to Singapore.

- Social events and a Singapore Industry summit on 3GPP held.

- Singapore Ministry and Government visitors welcomed as guests.

- All Work Items and Study Items for 5G‑Advanced on schedule in Release‑

- 14 Study Items for 6G progressing.

- The TSG RAN Study on 6G Scenarios and requirements (TR 38.914) approved this week.

- First timeline for early 6G specifications approved (Rel-21).

3GPP’s Release 21 will comprise the first 6G specs as well as 5G-Advanced. Release 21 work items for 6G and 5G-Advanced are scheduled to be approved with a first functional freeze in March 2027 and a second freeze in June 2028, with a “checkpoint” in March 2028 for 80% of the work to be done. The stage 3 final freeze is set for December 2028. The full and final code freeze is scheduled for March 2029.

Guy Daniels wrote in a blog post titled, “Analysis of 3GPP RAN #112: Timeline locked but the migration question unanswered“:

There is a 3GPP structural oddity in the details. The March 2027 6G “package approval” is the approval of a placeholder whose RAN2/3/4 content is finalized three months later. This is deliberate concurrency, not an oversight, it’s how the 3GPP works. The normative engineering windows are equally tight: RAN1 runs Q2 2027 to Q3 2028; RAN2/3/4 run Q3 2027 to Q4 2028; six quarters each to specify a new radio generation.”

“The Scenarios and Requirements study is finished, but the political questions it deferred are not. The requirements now say what 6G must do. September begins the fight over what it will be.”

……………………………………………………………………………………………………………………………………………………………………………………………………………………………….

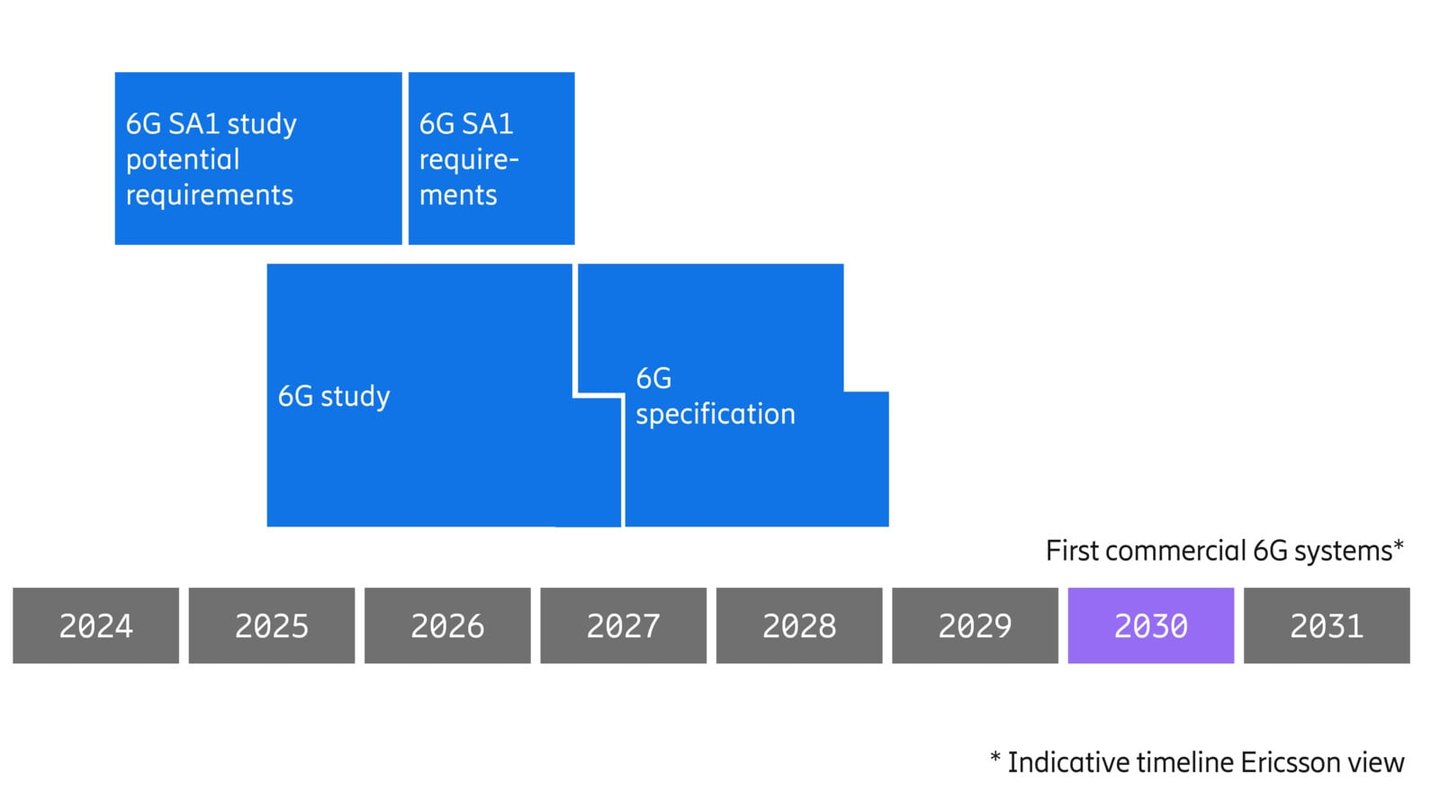

In a blog post summarizing last week’s plenary meeting, Ericsson said 6G standardization “is in full swing” and highlighted some of the early 6G decisions, including choices for waveform, modulation, channel coding, a basic security framework and supported bandwidths. The agreed 6G waveform is to use cyclic-prefix orthogonal frequency-division multiplexing (CP-OFDM) in the downlink. There are two options for uplink: CP-OFDM and discrete Fourier transform spread OFDM (DFT-s-OFDM). Supported bandwidths will range from 3MHz to 400MHz. 3GPP also agreed that 5G channel codes “will be largely reused” in 6G.

Here’s Ericsson’s timeline for 6G:

“6G is coming into focus…We are at a point now where a lot of pieces of the puzzle are starting to come together,” Gabriel Brown, senior principal analyst at Omdia, explained in a recent podcast with colleague and analyst Ruth Brown (no relation). The analysts also presented the 6G state of play at the 6G Summit hosted by ATIS’s Next G Alliance ahead of Network X Americas last month. Gabriel noted there has been a mindset shift among telcos about 6G from being “cautious” to “embracing it.” He said that the World Radiocommunication Conference next year (WRC-27) and the Summer Olympic Games in Los Angeles in 2028 will be important “checkpoints” for the anticipated early 2029 arrival of the 6G standards.

“[The LA Summer Olympics] is going to be an amazing opportunity for the U.S. ecosystem to showcase the potential of next-generation connectivity…It’s a chance to show how wireless can serve all the other industries there,” he added.

It will be important to watch for 3GPP’s September 2026 Madrid meeting output deliverables to get a sense of what functions and features might be in 6G RANs.

……………………………………………………………………………………………………………………………………………………………………………………….

6G Core Network:

The 6G core network architecture (such as signaling, network management, security, 6G specific features, and AI-native core architecture) will be defined in Release 21 Stage-2 (System & Architecture) scheduled to be completed in June 2028. Stage-3 (Protocol Specifications) is slated for December 2028 with ASN.1 & OpenAPI Freeze to be completed in March 2029.

3GPP decided NOT to liaise/contribute their 5G SA core network architecture specs to ITU-T, but ETSI rubber stamped them. Just as they did with IMT-2020 (5G), 3GPP will likely maintain exclusive development and control over all non-radio specifications for IMT-2030 (6G). Instead of formalizing them through ITU-T. 3GPP relies on its own Organizational Partners, e.g. ETSI and ATIS, to adopt the core network framework in their standards. 3GPP decided to bypass ITU-T for the 5G mobile core network, opting to develop 5G SA core network specs directly to ensure rapid, market-driven deployment.

……………………………………………………………………………………………………………………………………………………………………………………………

Addendum – 3GPP specs are NOT standards and have no legal standing:

What most, if not all, telecom trade publications (like this one) get completely wrong is that 3GPP does not produce standards, but specifications via their Releases. Those must be contributed, discussed, debated and approved by official SDOs like ITU-R and ETSI or other 3GPP members.

In the case of 5G/IMT 2020, ATIS presented all 3GPP RIT/SRIT specifications as contributions to ITU-R WP5D, which is 100% responsible for all IMT terrestrial radio interface standards (ITU-R recommendations). It should also be noted that ITU-R WP 5D has sole responsibility for IMT 2030/6G Frequency Arrangements which will be done after 6G frequencies are agreed at the ITU World Radiocommunication Conference (WRC-27),which is scheduled to take place from October 18 to November 12, 2027, in Shanghai, China.

“The 3GPP Technical Specifications and Technical Reports have, in themselves, no legal standing. They only become “official” when transposed into corresponding publications of the Partner Organizations (or the national / regional standards body acting as publisher for the Partner). At this point, the specifications are referred to as UMTS within ETSI and FOMA within ARIB/TTC.”

https://portal.etsi.org/new3g/specs/publications_partners.htm

From Qualcomm:

“3GPP Organization – Fixing three common misconceptions: 3GPP develops technical specifications, not standards. This is a subtle, but important organizational clarification. 3GPP is an engineering organization that develops technical specifications. These technical specifications are then transposed into standards by the seven regional Standards Setting Organizations (SSOs) that form the 3GPP partnership.”

https://www.qualcomm.com/news/onq/2017/08/understanding-3gpp-starting-basics

The Partnership Project is not a legal entity but is a collaborative activity between the following recognized Standards Development Organizations (SDO):

- The Association of Radio Industries and Businesses (ARIB) – Japan

- The Alliance for Telecommunications Industry Solutions (ATIS) – US

- China Communications Standards Association (CCSA) – China

- The European Telecommunications Standards Institute (ETSI) – Europe

- Telecommunications Standards Development Society (TSDSI) – India

- Telecommunications Technology Association (TTA) – South Korea

- Telecommunication Technology Committee (TTC) – Japan

The Partnership Project is entitled the “THIRD GENERATION PARTNERSHIP PROJECT” and may be known by the acronym “3GPP.”

………………………………………………………………………………………………………………………………………………………………………………………………

References:

https://www.3gpp.org/news-events/3gpp-news/tsg112#:~:text=3GPP%20plenaries

https://www.3gpp.org/news-events/3gpp-news/rel21-timeline

https://6gfutures.substack.com/p/analysis-of-3gpp-ran-112-timeline

https://www.ericsson.com/en/blog/2026/6/6g-standardization-key-milestones-and-ran-decisions

https://www.3gpp.org/about-us/legal-matters

https://portal.etsi.org/new3g/specs/publications_partners.htm

https://www.lightreading.com/6g/it-s-official-6g-specs-are-set-for-early-2029

https://www.itu.int/en/ITU-R/study-groups/rsg5/rwp5d/imt-2030/Pages/default.aspx

Roles of 3GPP and ITU-R WP 5D in the IMT 2030/6G standards process

ITU-R M.[IMT-2030.EVAL] & ITU-R M.[IMT-2030.SUBMISSION] reports: Evaluation & Submission Guidelines for 6G RIT/SRITs (6G)

IMT-2030 (“6G”) Minimum Technology Performance Requirements for Radio Interface Technologies

Comparing AI Native mode in 6G (IMT 2030) vs AI Overlay/Add-On status in 5G (IMT 2020)

Analysis: Nvidia’s rumored new 6G AI-RAN – likely features/functions and industry impact

ITU-R WP 5D Timeline for submission, evaluation process & consensus building for IMT-2030 (6G) RITs/SRITs

ITU-R WP 5D reports on: IMT-2030 (“6G”) Minimum Technology Performance Requirements; Evaluation Criteria & Methodology

AI wireless and fiber optic network technologies; IMT 2030 “native AI” concept

Highlights of 3GPP Stage 1 Workshop on IMT 2030 (6G) Use Cases

Should Peak Data Rates be specified for 5G (IMT 2020) and 6G (IMT 2030) networks?

GSMA Vision 2040 study identifies spectrum needs during the peak 6G era of 2035–2040

Highlights and Summary of the 2025 Brooklyn 6G Summit

NGMN: 6G Key Messages from a network operator point of view

Nokia and Rohde & Schwarz collaborate on AI-powered 6G receiver years before IMT 2030 RIT submissions to ITU-R WP5D

Verizon’s 6G Innovation Forum joins a crowded list of 6G efforts that may conflict with 3GPP and ITU-R IMT-2030 work

Nokia Bell Labs and KDDI Research partner for 6G energy efficiency and network resiliency

Deutsche Telekom: successful completion of the 6G-TakeOff project with “3D networks”

Market research firms Omdia and Dell’Oro: impact of 6G and AI investments on telcos

Qualcomm CEO: expect “pre-commercial” 6G devices by 2028

Ericsson and e& (UAE) sign MoU for 6G collaboration vs ITU-R IMT-2030 framework

Virtualization’s role in 5G Advanced (3GPP Release 18) and a proposed new hardware architecture

Ericsson’s June 2026 Mobility Report Highlights + AI impact on network traffic

Ericsson’s June 2026 Mobility report states that:

- 5G global subscriptions have now passed the 3 billion mark with the addition of 162 million in the first quarter of 2026.

- Half of the world’s mobile data traffic is now carried over 5G vs 48% at the end of 2025. It’s forecast to rise to 85% by the end of 2031.

- Mobile network data traffic growth exceeded expectations, at 22% between Q1 2025 and Q1 2026.

- Fixed Wireless Access (FWA) adoption is also growing, with around 70% of FWA service providers now offering the service over 5G.

- The number of commercial 5G SA network slicing offerings has increased from 65 to 84 in just 6 months.

- Cellular IoT connections are expected to approach 8 billion by the end of 2031

“With the upcoming transition to physical AI, traffic patterns will fundamentally shift as we move from centralized models in data centers to distributed, autonomous AI agents embedded across our device vehicles and cities, commonly connected by 5G,” said Ericsson CTO Erik Ekudden, in a statement accompanying the report.

“Mobile networks are no longer only about providing best-effort connectivity, they are becoming critical, intelligent infrastructure that meets diverse application needs, Reflecting part of this shift is the continued rise in new commercial service offerings based on 5G standalone network slicing and the number of communications service providers deploying 5G SA,” Ekudden said.

Image Credit: Ericsson

……………………………………………………………………………………………………………………………………………………………………….

Impact of Agentic AI workloads on network traffic:

The most critical engineering takeaway from the report is a profound asymmetry in data traffic growth, heavily driven by agentic AI workloads and user-generated content.

Key Insights:

- AI-driven applications – spanning smartphones, AI/AR smart glasses and autonomous vehicles – are inherently uplink heavy, generating continuous data streams that challenge traditional downlink-dominated traffic patterns.

- Uplink traffic growth is already outpacing downlink for many service providers, with field measurements indicating capacity constraints under peak load. Scenario modeling suggests that additional AI traffic will result in uplink traffic being three times higher in 2031 compared to 2025.

- Current networks are not dimensioned for sustained uplink demand, calling for a step change in design – from 5G software and hardware enhancements in the near term to 6G-native uplink innovations over the longer horizon.

- Traffic Inversion: Traditionally, cellular networks are architected and provisioned to handle heavily downlink-centric (DL) traffic patterns. However, the proliferation of multimodal generative AI and uplink-heavy applications is radically flipping this paradigm.

- Field Measurement Data: Out of 55 global operators analyzed, 43 experienced uplink (UL) growth rates outpaces DL growth. Crucially, 17 of those service providers reported UL expansion exceeding DL by a factor of 1.5x or higher.

- Projections: Ericsson’s scenario modeling suggests that cumulative AI-driven traffic could cause UL demands to spike threefold by 2031 compared to 2025 baselines.

- Near-Term: Immediate deployment of 5G RAN software optimizations and hardware refreshes. This includes pushing for 5G Standalone (SA) core migrations, leveraging AI-optimized Massive MIMO beamforming, and utilizing network slicing to guarantee bounded latency for critical UL channels.

- Long-Term: Transitioning to 6G-native uplink innovations. Early 6G standardization, targeted for finalization around 2028–2029, will focus deeply on AI-native architectures, Integrated Sensing and Communication (ISAC), and asymmetric air-interface designs natively optimized for continuous data streams.

Market Outlook:

Resolving these capacity constraints requires immediate, targeted infrastructure capital expenditure. While macro RAN spending has faced recent headwinds, the urgent necessity to re-dimension the air interface for an AI-centric world represents a powerful pipeline catalyst for Ericsson and its infrastructure rivals. Telco spending on RAN products has slumped from $45 billion in 2022 to $35 billion last year, according to analysts at Omdia, while Ericsson’s annual sales have dropped from SEK271.5 billion ($28.8 billion) to SEK236.7 billion ($25.1 billion) over this same period.

References:

https://www.ericsson.com/en/reports-and-papers/mobility-report/reports/june-2026

GSA: Global private mobile networks exceed 2,000 worldwide; Ericsson Private 5G from Verizon Business extends beyond U.S.

Ericsson reports 10% drop in 1st quarter sales; targets network growth

AT&T and Ericsson boost Cloud RAN performance with AI-native software running on Intel Xeon 6 SoC

Ericsson and Intel collaborate to accelerate AI-Native 6G; other AI-Native 6G advancements at MWC 2026

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Nokia to showcase agentic AI network slicing; Ericsson partners with Ookla to measure 5G network slicing performance

China’s telecom industry rapid growth in 2025 eludes Nokia and Ericsson as sales collapse

Latest Ericsson Mobility Report talks up 5G SA networks and FWA

Ericsson Mobility Report touts “5G SA opportunities”

Optus and Ericsson achieve 180MHz across 2.3GHz and 3.5GHz bands using carrier aggregation on a live 5G SA network

Australian telco Optus has demonstrated advanced 5G NR carrier aggregation (5G NR-CA) performance on its 5G standalone (SA) network by implementing four-component carrier aggregation (4CC CA) across low-, mid-, and upper-mid-band spectrum. Using Ericsson 5G SA network equipment and software, the configuration aggregates FDD bands at 900 MHz (Band n8) and 2.1 GHz (Band n1) with TDD bands at 2.3 GHz (Band n40) and 3.5 GHz (Band n78). Two-Component Carrier (2CC CA) uplink aggregation

This combined Optus’ unique two mid-band TDD spectrum holdings across 2.3GHz and 3.5GHz, achieving a record 180MHz TDD spectrum aggregation. In particular:

- Four-Component Carrier aggregation enabled 220MHz downlink bandwidth, leveraging spectrum across four different bands of 900MHz, 2.1GHz, 2.3GHz and 3.5GHz

- Two-Component Carrier uplink aggregation combined one Frequency Division Duplex (FDD) band from 900MHz and 2.1GHz with one TDD band from 2.3GHz and 3.5GHz

- Achieved peak speeds of 3.4Gbps (downlink) and 200Mbps (uplink) in a live network site with commercial devices, including the Samsung Galaxy S26 Ultra

The demonstration aligns with 3GPP Release 16 and Release 17 5G NR-CA enhancements (TS 38.300, TS 38.101-1/2), which extend carrier aggregation capabilities across heterogeneous duplex modes (FDD+TDD) and multiple frequency ranges within FR1. The downlink configuration leverages cross-band scheduling and advanced MIMO layers (likely up to 4×4 or higher per component carrier, depending on band support) to maximize spectral efficiency across aggregated carriers.

On the uplink, Optus and Ericsson reported 200 Mbps throughput using two-component carrier aggregation (2CC CA), combining FDD (n8/n1) and TDD (n40/n78) spectrum. This implementation is consistent with 3GPP Release 16 uplink enhancements, including uplink carrier aggregation and transmit (Tx) switching (TS 38.213), which enables efficient utilization of UE power resources across multiple uplink carriers, particularly in mixed duplex scenarios.

All results were achieved on a live commercial 5G SA network at Optus’ Sydney campus using commercial off-the-shelf (COTS) user equipment, including the Samsung Galaxy S26 Ultra. This indicates full compliance with 3GPP-defined UE capability signaling (TS 38.306) and the availability of device-side support for complex NR-CA band combinations, including inter-band and cross-duplex aggregation.

“This achievement demonstrates how we are translating cutting-edge 5G technology into meaningful benefits for customers in real-world environments. Through our ongoing collaboration with Ericsson, we are unlocking greater capacity and performance across our 5G network, enabling faster speeds and more reliable connectivity,” said Optus CTO Sri Amirthalingam. “This milestone marks an important step in our network evolution towards 5G Advanced, reinforcing our commitment to remain at the forefront of innovation and to deliver tangible value for our customers.”

Ludvig Landgren, head of Ericsson Australia and New Zealand operations said: “Optus continues to demonstrate strong leadership in adopting advanced 5G capabilities, and this milestone highlights the strength of our partnership. By expanding and combining multiple spectrum assets with Ericsson technology, we are helping Optus deliver meaningful performance improvements that translate directly into better everyday experiences for their customers.”

………………………………………………………………………………………………………………………………………………..

From a broader industry perspective, these results build on ongoing 5G NR-CA advancements. T-Mobile US has demonstrated approximately 6 Gbps downlink throughput using six aggregated carriers in FR1, as well as 550 Mbps uplink throughput leveraging uplink Tx switching across sub-6 GHz bands. In Europe, Vodafone and MediaTek achieved 277 Mbps uplink throughput using NR uplink CA, while Elisa, Ericsson, and MediaTek demonstrated 12CC aggregation reaching 8 Gbps downlink—highlighting the scalability of NR-CA as defined in 3GPP Release 17 and evolving into Release 18 (5G-Advanced).

Within Australia, Telstra has deployed Ericsson’s automated carrier aggregation (CA) optimization solution across more than 50 live 5G Advanced sites, leveraging dynamic CA configuration and traffic-aware scheduling—capabilities aligned with 3GPP Release 18 objectives for AI-assisted RAN optimization.

A notable aspect of the Optus/Ericsson demonstration is the aggregation of 180 MHz of mid-band spectrum across n40 (2.3 GHz) and n78 (3.5 GHz). While not a headline peak-rate milestone, this represents a first in terms of contiguous mid-band NR-CA deployment at this bandwidth scale. Mid-band aggregation is particularly significant within the 3.3–4.2 GHz “golden band” range defined in global 5G spectrum harmonization efforts, as it offers an optimal balance between coverage and capacity.

Operationally, this configuration is expected to deliver immediate gains in high-traffic scenarios—such as dense urban environments, transport hubs, and large venues—by increasing available cell throughput and improving user-level quality of service (QoS). Furthermore, the expanded mid-band capacity directly benefits fixed wireless access (FWA) deployments, where sustained throughput and cell-edge performance are critical. Because the demonstrated CA combinations are already supported by commercial UE categories, deployment can proceed without requiring new device classes, accelerating time-to-impact.

Ericsson was recently selected to modernize and expand SoftBank’s core networks, as well as accelerate the Japanese giant’s 5G SA adoption. Expanding on a previous 5G SA deal centered around its radio access network (RAN) products, Ericsson is providing SoftBank with its Core Networks’ portfolio, including a dual-mode 5G Core solution running on Ericsson’s Cloud Native Infrastructure Solution (CNIS).

……………………………………………………………………………………………………………………………..

References:

https://www.sdxcentral.com/news/ericsson-and-optus-claim-5g-sa-world-first/

https://www.ericsson.com/en/press-releases/7/2026/optus-and-ericsson-trial-ai-to-boost-5g-downlink

https://www.nokia.com/mobile-networks/ran/carrier-aggregation/5g-carrier-aggregation-explained/

China Unicom-Beijing and Huawei build “5.5G network” using 3 component carrier aggregation (3CC)

Nokia, BT Group & Qualcomm achieve enhanced 5G SA downlink speeds using 5G Carrier Aggregation with 5 Component Carriers

Finland’s Elisa, Ericsson and Qualcomm test uplink carrier aggregation on 5G SA network

T-Mobile US, Ericsson, and Qualcomm test 5G carrier aggregation with 6 component carriers

Ericsson and MediaTek set new 5G uplink speed record using Uplink Carrier Aggregation

BT tests 4CC Carrier Aggregation over a standalone 5G network using Nokia equipment

T-Mobile US achieves speeds over 3 Gbps using 5G Carrier Aggregation on its 5G SA network

Ericsson reports 10% drop in 1st quarter sales; targets network growth

Executive Summary:

Ericsson reported mixed first-quarter 2026 results, characterized by continued resilience in its Networks segment despite regional demand variability and emerging supply-side cost pressures. The Swedish company recorded 7% year-over-year organic growth in its Networks business, supported by sustained network modernization programs and ongoing 5G deployments across Europe, the Middle East, and Africa (EMEA), as well as increased delivery volumes in India and Japan. This growth offset a decline in North American sales, which followed a period of elevated operator investment in 2025 and reflects a near-term reallocation of capital expenditure by key customers. However, Ericsson reported a 10% total sales drop to 49.33 billion kronor in the first quarter, with EBITA falling to 1.44 billion kronor.

Ericsson reiterated its expectation of a broadly flat global RAN market in 2026 but expressed confidence in its ability to outperform the overall sector. The Networks segment maintained a robust adjusted gross margin of 50.4%, within its guided 49–51% range, with similar margin performance anticipated in the second quarter. Sequential revenue growth is projected to align with typical seasonal trends, approximating a 4% increase.

Despite these operational strengths, Ericsson highlighted increasing uncertainty in the macroeconomic and geopolitical environment. Of particular concern is the rising cost of components—especially semiconductors—driven in part by global AI-related demand. The company indicated that while semiconductors represent a relatively limited portion of its total cost base, sustained price increases are expected to create headwinds.

To mitigate these pressures, Ericsson is pursuing a combination of supply chain optimization, product substitution strategies, operational efficiencies, and selective cost-sharing mechanisms with customers. The company emphasized that its prior investments in supply chain diversification have enhanced resilience, although it acknowledged that it remains exposed to broader market disruptions affecting pricing and component availability.

Geopolitical factors have also introduced operational challenges. Ongoing conflict in the Middle East has necessitated adjustments to logistics and transportation routes, resulting in incremental costs. Ericsson noted that its regional distribution infrastructure has been impacted but that supply continuity has been maintained through flexible supply chain management.

From a financial perspective, Ericsson reported first-quarter EBIT of SEK 1.44 billion, a significant decline from SEK 5.93 billion in the prior year, reflecting restructuring charges and adverse currency movements. Group revenue decreased 10% year-over-year to SEK 49.33 billion, below market expectations, while gross margin contracted to 47.2% from 48.2%.

Image Credit: lars schroder/Agence France-Presse/Getty Images

…………………………………………………………………………………………………………………………………………

Börje Ekholm, Ericsson President and CEO, said:

“Our Q1 results demonstrate continued resilience in a dynamic environment, with organic sales growth of 6%. Our healthy gross margins and strong cash flow reflect the progress we have made in recent years, reducing reliance on geographic mix and strengthening our foundations globally. Our multi-year investments in building a resilient, diversified, supply chain have enabled us to deliver consistently for customers amidst geopolitical and macroeconomic uncertainties. We are facing increasing input costs, especially in semiconductors, caused in part by AI demand. Our ambition is to offset these challenges, by working closely with customers and suppliers, and through product substitution and efficiency actions. Looking ahead, while we continue to expect a flattish RAN market, our focused strategy, leading portfolio, and strengthened positions in mission critical and Enterprise give us confidence in our ability to grow faster than the mobile networks market and drive long-term success.”

Overall, the results underscore a transitional phase for Ericsson, with strong execution in global 5G and modernization programs partially offset by cyclical demand softness in North America and emerging cost inflation in critical technology inputs. The company recorded 7% year-over-year organic growth in its Networks business, supported by sustained network modernization programs and ongoing 5G deployments across Europe, the Middle East, and Africa (EMEA), as well as increased delivery volumes in India and Japan. This growth offset a decline in North American sales, which followed a period of elevated operator investment in 2025 and reflects a near-term reallocation of capital expenditure by key customers.

Ericsson’s quarter reinforces a broader industry pattern: the global RAN market is stabilizing after the 5G deployment peak, but not re-entering a meaningful growth phase. Until 6G capex begins to scale later in the decade, vendor performance will depend more on regional share gains, modernization cycles, and margin discipline than on total market expansion. After the 5G buildout peak, network operators are largely shifting from coverage expansion to optimization, monetization, and cost efficiency, which limits near-term revenue upside for vendors even when unit shipments remain healthy.

………………………………………………………………………………………………………………………………………………

RAN Market dynamics:

The key issue is that RAN demand is no longer being driven by broad-based new macro rollouts. Instead, spending is being concentrated on targeted modernization, selective capacity adds, and feature upgrades, while legacy LTE revenue continues to decline and offsets much of the remaining 5G activity.

That helps explain why vendors can still post pockets of growth in regions like EMEA, India, and Japan while North America softens after a prior wave of heavy investment. In other words, regional growth is becoming more cyclical and more dependent on operators’ capex timing than on a sustained global upgrade super-cycle.

Why RAN growth stays muted:

The structural problem is that RAN is maturing into a low-growth infrastructure market. Dell’Oro’s latest forecast points to only about 1% CAGR over the next five years, with the broader market remaining largely flat until 6G-related capex begins to ramp late in the decade.

That means the industry is effectively living through a long gap between the end of the 5G peak and the start of the 6G investment cycle. During that gap, vendors compete less on market expansion and more on mix, efficiency, software attach, and share gains, which is why financial performance can diverge from headline market growth.

What this means for Ericsson:

For Ericsson, the implication is that beating the market may matter more than the market itself. If the underlying RAN market is flat to low-single-digit growth, then Ericsson’s ability to sustain margin through supply-chain discipline, pricing, and product mix becomes more important than chasing top-line expansion alone.

This is also why component inflation matters now. When market growth is weak, cost pressure from semiconductors, logistics, and geopolitics has a larger effect on earnings quality, because vendors have fewer natural volume tailwinds to absorb it.

6G/IMT 2030 timing risk:

The big strategic uncertainty is timing. If meaningful telco 6G capex does not begin until around 2030–2031 (which seems highly likely), then the wireless telecom industry faces several years of subdued RAN revenue. That creates pressure on vendors to extract value from 5G Advanced, automation, private networks, and software-led differentiation before the next technology cycle arrives.

This is why “no real growth till 6G in 2031” is a reasonable framing. It captures the reality that the market can remain technically active while still being economically stagnant, with limited aggregate revenue growth even as networks become more capable and more software-defined.

From Sebastian Barros:

“Ericsson’s Q1 results are a masterclass in structural paradox. Pulling a 6% organic growth rate in a dead-flat global RAN market is a massive operational flex for a 150-year-old heavyweight. But look under the hood. Reported sales took a 10% hit due to brutal FX headwinds, and their supply chain is under intense pressure as global AI data centers hoard 3nm semiconductor capacity. Their historic dominance in custom ASIC silicon and radio frequency is exactly what makes them structurally vulnerable today. Being functionally addicted to a $35 billion RAN market that accounts for over 60% of their portfolio is a massive liability, as that profit pool is being actively dismantled by x86/GPU disaggregation, open architectures, and geopolitical hardware wars…”

………………………………………………………………………………………………………………………………………………………………….

References:

Ericsson and Forschungszentrum Jülich MoU for neuromorphic computing use in 5G and 6G

AT&T and Ericsson boost Cloud RAN performance with AI-native software running on Intel Xeon 6 SoC

Ericsson and Intel collaborate to accelerate AI-Native 6G; other AI-Native 6G advancements at MWC 2026

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

China’s telecom industry rapid growth in 2025 eludes Nokia and Ericsson as sales collapse

SoftBank and Ericsson-Japan achieve 24% 5G throughput improvement using AI-optimized Massive MIMO

Huawei, Qualcomm, Samsung, and Ericsson Leading Patent Race in $15 Billion 5G Licensing Market

Ericsson announces capability for 5G Advanced location based services in Q1-2026

Highlights of Ericsson’s Mobility Report – November 2025

Ericsson’s revenue drops, profits soar; deal with Vodafone and partnership with Export Development Canada look promising

Huawei FY2025: 2.2% YoY revenue increase; strategic pivot to AI and intelligent automotive solutions

Overview:

Huawei has released its 2025 audited financial results, reporting total revenue of CNY 880.9bn ($127.6bn) — a 2.2% YoY increase. The report highlights a significant expansion in profitability, with operating profit surging 22.1% to CNY 96.9bn ($14bn). That translated to an operating profit margin of 11%, up 180 bps from the 9.2% recorded in 2024.

Image Credit: Imago/Alamy Stock Photo

……………………………………………………………………………………………….

“In 2025, Huawei’s overall performance remained steady,” said Sabrina Meng, Huawei’s Rotating Chairwoman. “I would like to thank our customers for your ongoing trust and support. Thanks also to consumers for choosing Huawei, as well as suppliers, partners, and developers around the world for working with us. “Of course, we couldn’t do any of this without the support of every Huawei employee. Thank you for your hard work, and also your families for their steadfast support.”

In 2025, Huawei’s connectivity business weathered the impact of industry investment cycles, while its computing business continued to seize opportunities in AI. The consumer business worked to overcome formidable challenges, driving the HarmonyOS ecosystem to cross a new threshold in user experience. Huawei’s digital power business continued to place quality before all else. Huawei Cloud honed its competitiveness with a focus on core services, and the company’s intelligent automotive solutions grew rapidly.

………………………………………………………………………………………….

Pivot to Intelligent Automotive Solutions:

Huawei is aggressively diversifying and placing a massive strategic bet on the automotive sector to drive future growth. Its Intelligent Automotive Solutions business is experiencing explosive growth, with revenue increasing by over 400% in 2024 to 26.35 billion yuan ($3.62bn).

In 2025, the unit surged another 72% to CNY 45 billion (approx. $6.2bn). Huawei does not manufacture its own cars directly but operates as a top-tier supplier and technology partner (similar to “Bosch”) via its Harmony Intelligent Mobility Alliance (HIMA). Huawei continues to invest heavily in its “future-oriented” auto and AI businesses.

Revenue Breakdown by Segment & Geography:

- Infrastructure & Solutions: Remains the primary anchor, contributing 42.6% of total revenue (up 2.6% YoY).

- Consumer Business: Accounted for 39.1% of revenue, maintaining a steady recovery with 1.6% YoY growth.

- Intelligent Automotive Solutions (IAS): The high-growth outlier, with revenues spiking 72.1% YoY to CNY 45bn, now representing 5.1% of the total portfolio.

- Geographic Mix: Domestic China operations generated ~70% of revenue. International footprints were led by EMEA (18.3%), followed by Asia-Pacific (5.7%) and the Americas (4.2%).

R&D Intensity and Ecosystem Strategy:

Huawei continues to maintain one of the industry’s highest reinvestment rates, allocating CNY 192.3bn ($27.9bn) to R&D—a massive 21.8% of annual revenue. Huawei’s R&D expenditure rose 7% last year to an impressive RMB 192.3 billion (approximately $28 billion), representing nearly 22% of annual revenue.

In sharp contrast, Ericsson—whose portfolio remains heavily centered on 5G—reduced its R&D outlay by 9% to SEK 48.9 billion (about $5.2 billion). At 21% of sales, Ericsson’s R&D intensity was largely in line with Huawei’s. Nokia, meanwhile, outpaced both rivals in relative terms, allocating 23% of revenue—roughly €4.6 billion ($5.3 billion)—to R&D, up 7% year over year. Most of that increase stemmed from the February 2025 acquisition of optical systems vendor Infinera, which expanded Nokia’s technology base and R&D footprint.

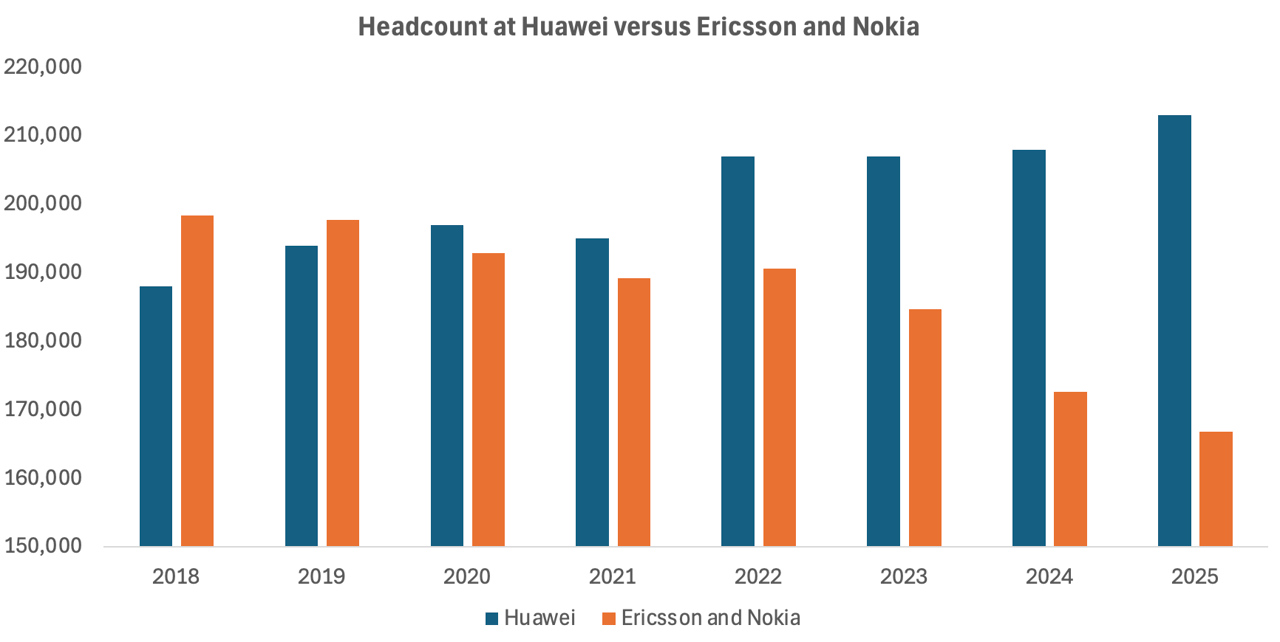

The huge divergence lies in workforce trends. As reported by Light Reading, Ericsson and Nokia have collectively shed nearly 28,000 positions since 2022, equivalent to about 15% of their combined headcount that year. While growing automation and AI integration have arguably improved operational efficiency, the scale of these reductions also reflects a cooling investment climate among operators. With telco spending on 5G deployments tapering off, Europe’s two large network equipment vendors are continuing layoffs.

In contrast, Huawei’s workforce has continued to increase as it has pushed into new industrial sectors. Since 2021, when Huawei suffered its worst-ever sales decline, the Chinese behemoth has added about 18,000 employees to its payroll, according to annual reports. Around 5,000 of them were recruited last year, including 1,000 in R&D alone. That resulted in 213,000 employees Huawei employees in 2025.

The increased hiring boosted overall operating costs, including R&D expenditure, by 7.2%, to about RMB334 billion ($48.5 billion).

Source & Graph Credit: Light Reading

………………………………………………………………………………………………………………….

Moving forward, China’s largest IT vendor’s roadmap prioritizes:

- Full-Stack AI Integration: Embedding AI and carrier-grade security across the entire product lifecycle and network architecture.

- Strategic Domain Expansion: Increasing CapEx and R&D in connectivity, cloud, and autonomous driving.

- Ecosystem Sovereignty: Scaling the Ascend (AI), Kunpeng (Computing), and HarmonyOS ecosystems to drive vendor-agnostic collaboration and industry-wide adoption

Meng stressed, “We are moving toward a future that is full of uncertainty, so we have to remain true to our strategy and maintain strategic focus. We will translate strategy to execution, keep cultivating the developer ecosystem, and pursue high-quality development.”

………………………………………………………………………………………………………………….

References:

https://www.huawei.com/en/news/2026/3/annual-report-2025

https://www.lightreading.com/5g/huawei-sales-growth-plummeted-in-2025-as-it-gained-5-000-workers

Huawei unveils AI Centric Network roadmap, U6 GHz products, 5G Advanced strategy and SuperPoD cluster computing platforms

Huawei, Qualcomm, Samsung, and Ericsson Leading Patent Race in $15 Billion 5G Licensing Market

Huawei Cloud Review and Global Sales Partner Policies for 2026

Huawei’s Electric Vehicle Charging Technology & Top 10 Charging Trends

Huawei to Double Output of Ascend AI chips in 2026; OpenAI orders HBM chips from SK Hynix & Samsung for Stargate UAE project

Omdia on resurgence of Huawei: #1 RAN vendor in 3 out of 5 regions; RAN market has bottomed

Huawei launches CloudMatrix 384 AI System to rival Nvidia’s most advanced AI system

U.S. export controls on Nvidia H20 AI chips enables Huawei’s 910C GPU to be favored by AI tech giants in China

AI-RAN Reality Check: hype vs hesitation, shaky business case, no specific definition, no standards?

Introduction:

The narrative surrounding “AI-RAN” — a term thrust into the spotlight by Nvidia — may have left many believing that boatloads of GPUs are already powering baseband compute in RAN equipment across the world’s seven million mobile sites. In truth, the reality is far more nascent.

Among major RAN vendors, Nokia stands alone in adapting baseband software for GPU acceleration. Yet even Nokia does not anticipate commercial readiness until late 2026, as confirmed by its Chief Technology Officer, Pallavi Mahajan, during the company’s MWC press conference earlier this year. For now, no operator has announced a commercial deployment — despite the buzz around trials.

Early Movers, Limited Momentum:

Much of the current AI-RAN activity centers on two operators: T-Mobile US and Japan’s SoftBank. At MWC, T-Mobile’s Executive Vice President of Innovation and ex-CTO, John Saw, acknowledged the limited availability of deployable solutions, quipping that he hoped Nokia would deliver an AI-RAN product within the year. Nokia CEO Justin Hotard quickly assured him that such a milestone was indeed on track.

Still, the debut of a GPU-based RAN stack does not imply an imminent large-scale rollout. Without tangible network performance or cost advantages over existing virtualized or disaggregated RAN approaches, operators are unlikely to move past controlled trials.

SoftBank, while often positioned as an AI-RAN pioneer, remains cautious. As Ryuji Wakikawa, Vice President of its Advanced Technology Division, outlined last year, the operator aims to deploy only a handful of AI-RAN sites over the next fiscal cycle. Transitioning from testing to carrying live commercial traffic, he emphasized, demands a significant maturity leap in quality and feature completeness.

Beyond Hype: Limited Commercial Engagement:

Elsewhere, Indonesia’s Indosat Ooredoo Hutchison (IOH) was heralded in 2025 as the first operator in Southeast Asia pursuing AI-RAN. More than a year later, authoritative sources indicate IOH’s work remains confined to its research facility in Surabaya, with no near-term plans for GPU investment at cell sites until measurable value is demonstrated.

The challenge for Nokia — and for GPU-backed AI-RAN broadly — is convincing operators that general-purpose accelerators offer sufficient performance or efficiency gains for most RAN workloads. T-Mobile and SoftBank continue evaluating both Nokia and Ericsson, whose AI-RAN philosophies diverge sharply. Nokia is developing GPU-based baseband software, while Ericsson maintains its focus on custom silicon and CPU architectures.

Divergent Architectures and Use Cases:

Ericsson contends that no core RAN performance enhancements intrinsically require GPUs. Its ongoing collaboration with Nvidia leverages the latter’s Grace CPU technology rather than its GPU portfolio, reserving GPU acceleration only for compute-intensive functions like forward error correction (FEC).

If Ericsson’s premise holds, GPUs in the RAN become justifiable only when supporting AI inference workloads. Even then, inference at every radio site remains improbable. A more incremental strategy — deploying GPUs selectively at edge locations where AI workloads justify their cost — may prove more practical.

This modular approach aligns with existing virtual RAN deployments based on Intel CPUs, which already include native FEC acceleration. “It is an off-the-shelf card that you can slide right into an HPE or Dell or Supermicro server,” said Alok Shah, the vice president of network strategy for Samsung Networks. “That gets you the edge functionality you are looking for.”

Rethinking the Economic Case for AI RAN:

Initially, Nvidia positioned GPUs for AI-RAN as viable only if broadly utilized for AI inference across the RAN. Following its strategic alignment with Nokia, however, the company has softened its stance — now suggesting that appropriately sized, power-efficient GPUs could make sense even when dedicated solely to baseband computation.

For now, the global RAN landscape remains far from GPU-saturated. AI-RAN remains an exploratory frontier — one testing not only the technical feasibility of GPUs at the edge, but also the economic/business case rationale for re-architecting a trillion-dollar telecom infrastructure around them.

The AI models suitable for RAN environments must be compact and efficient, far slimmer than those that drive data center-scale AI. There’s no room for the massive, parameter-heavy neural networks that justify a GPU’s cost or energy appetite. In that light, a GPU looks less like a breakthrough and more like a mismatch — a chainsaw brought to a task better handled with a sharp pair of scissors.

Evaluating the Case for AI-RAN Acceleration:

The central question is whether GPUs can deliver meaningful benefits over custom silicon or conventional CPUs for RAN compute. Ericsson’s engineers argue that AI models deployed at the RAN must remain relatively lightweight, with far fewer parameters than those used in large-scale data centers. Excessive model complexity could introduce signaling delays unacceptable in real-time radio environments. In this context, deploying a GPU for such workloads might seem disproportionate — a high-powered tool for a low-demand task.

The most compelling defense of GPU-based RAN acceleration came from Ronnie Vasishta, Nvidia’s Senior Vice President for Telecom, who told Light Reading last summer, “The world is developing on Nvidia.” His point underscores a shift in semiconductor economics: the cost and risk of building dedicated silicon for a mature and shrinking RAN market make general-purpose processors — supported by large-volume ecosystems — increasingly attractive alternatives.

Intel’s difficulties further illustrate this dynamic. Despite $53 billion in revenue during 2025, the former microprocessor king barely broke even despite $53 billion in revenue, following a $19 billion loss the previous year. A major restructuring cut its headcount by nearly 24,000, and its planned spinoff of the Network and Edge division — serving telecom infrastructure customers — was ultimately abandoned in December. Nvidia, the world’s most valuable company, may be eager to step into that space — but the economic logic seems upside down. Wireless network operators are looking to reduce costs, not import data center economics into the RAN.

Ecosystem or Echo Chamber?

Nvidia’s Aerial platform and CUDA-based software ecosystem do present a compelling story: open infrastructure, modular APIs, and space for smaller developers to innovate alongside giants like Nokia. On paper, it’s an alluring image of democratized RAN software. In practice, it ties the industry even more tightly to a vertically integrated, proprietary ecosystem.

Nokia appears comfortable with that trade-off. Nokia CTO Pallavi Mahajan’s recent blog post framed AI-RAN as a vehicle for “software speed and innovation.” He added, “Nokia’s AI-RAN initiative begins with a simple observation: AI is changing not only how networks are operated, but also the nature of the traffic they carry. AI workloads have already reached massive scale, with mobile devices accounting for more than half of AI interactions. Large language model interactions introduce richer uplink flows and burstier patterns as devices continuously send context to models.”

Indeed, that me be true someday. But for now, most wireless network operators need stable, cost-efficient networks, not AI-driven complexity or GPU-level power draw.

Image Credit: Nokia

Conclusions:

The uncomfortable truth is that AI-RAN feels more like a vendor-driven experiment than an operator-driven demand. Until someone proves that GPUs in the RAN deliver a measurable payoff — in performance, cost, or operational simplicity — the whole concept risks joining the long list of telecom “game-changers” that never made it past the trial stage. The hype cycle is predictable; the economics are not. Unless that equation changes, the real intelligence may be knowing when not to deploy AI RAN.

………………………………………………………………………………………………………………

In a Substack post today, Sebastian Barros writes: What Does AI-RAN Even Mean?

Despite the crazy hype, there is no definition for AI-RAN. Today it is at best a vibe, a dangerous reality for an industry that moves on strict standards that are currently completely absent.

The AI RAN hype is crazy right now. But despite the endless talk and vendor announcements, there is no actual technical definition of what it even means. As wild as it sounds for an industry built on strict 3GPP and O-RAN standards (those are specs- not standards), AI RAN is currently just a vendor interpretation designed to move hardware. Moreover, telecom has been using AI in the RAN before it was even cool. In fact, we were among the first industries to use neural networks in signal processing back in the 80s.

The problem is that treating AI-RAN as a marketing narrative rather than a rigid standard actively stalls progress. When the definition of AI-RAN is as different as night and day depending on which OEM you ask, it becomes impossible for any Telco to accurately model TCO or make solid CAPEX decisions.

Editor Notes:

- ITU-R’s IMT-2030 framework (ITU-R Recommendation M.2160-0 for IMT-2030) calls for an AI-native new air interface and AI-enhanced radio networks, but does not mention Nokia’s AI RAN.

- 3GPP Release 18 and later have study/work items on AI/ML for RAN functions such as energy saving, load balancing, mobility optimization, and AI/ML on the RAN air interface, but again no specifics have been discussed let alone agreed upon.

- 3GPP Release 19 continues and expands this work, with reporting that it builds on Release 18’s normative work and adds new AI/ML-based use cases for NG-RAN. In other words, 3GPP does have AI-RAN-related specs in progress and some normative features, but they are distributed across multiple RAN work items rather than packaged as one standalone “AI RAN” specification.

- AI RAN Alliance “is dedicated to driving the enhancement of RAN performance and capability with AI.” However, they’ve not yet produced any implementable specifications for AI RAN. Yet there are only four carriers that are “executive members“: Vodafone, T-Mobile, and SK Telecom, and Softbank (which is a conglomerate).

In Japan, NTT Docomo holds the largest cellular market share, with KDDI second, followed by SoftBank and the rapidly expanding Rakuten Mobile.

References:

https://www.lightreading.com/5g/ai-ran-lots-of-talk-little-action-no-guarantees

https://www.nokia.com/blog/ai-ran-bringing-software-speed-innovation-into-the-radio-network/

Ericsson goes with custom silicon (rather than Nvidia GPUs) for AI RAN

Dell’Oro: RAN Market Stabilized in 2025 with 1% CAG forecast over next 5 years; Opinion on AI RAN, 5G Advanced, 6G RAN/Core risks

Dell’Oro: Analysis of the Nokia-NVIDIA-partnership on AI RAN

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

Dell’Oro: AI RAN to account for 1/3 of RAN market by 2029; AI RAN Alliance membership increases but few telcos have joined

AT&T and Ericsson boost Cloud RAN performance with AI-native software running on Intel Xeon 6 SoC

Overview:

AT&T and Ericsson have completed a milestone Cloud RAN test by successfully demonstrating Ericsson’s AI-native Link Adaptation [1.] on a Cloud RAN stack powered by Intel Xeon 6 SoC. The test showed how artificial intelligence (AI) can improve spectral efficiency and network responsiveness in real-world conditions. Conducted over AT&T’s licensed frequency bands, the experiment was the first to use portable Ericsson RAN software running on Intel’s new Xeon 6 system-on-chip (SoC) platform—an architecture designed for high-performance, cloud-native processing of RAN workloads. Engineered specifically for network and edge deployments, Intel Xeon 6 SoC delivers breakthrough AI RAN performance with built-in acceleration. Integrated Intel Advanced Vector Extensions (AVX) and Intel Advanced Matrix Extension (AMX) technologies eliminate the need for discrete accelerators while maximizing capacity, efficiency, and TCO optimization.

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Note 1. AI-native Link Adaptation dynamically adjusts to changes in signal quality and interference, boosting RAN performance on purpose-built and cloud-based infrastructure alike.

Other Notes:

-

vRAN: A radio access network (RAN) in which the baseband processing functions run as software on general-purpose processors (mostly from Intel) instead of on dedicated hardware at the cell site. In vRAN, the functional split defines how baseband processing is divided between centralized processors and the radio unit at the site, and that split drives fronthaul bandwidth, latency, and cost.

- Cloud RAN: An evolution of vRAN where those same RAN functions are re-architected as cloud‑native microservices/containers with CI/CD (Continuous Integration and either Continuous Delivery or Continuous Deployment), automation, and orchestrators, optimized for elastic scaling across distributed cloud infrastructure.

- Ericsson Cloud RAN is a cloud native software solution that handles compute functionality in the RAN. It virtualizes RAN functions on Commercial Off The Shelf (COTS) hardware, decoupling software from hardware to enable more flexible, scalable, and efficient network deployments.

- According to Dell’Oro Group, Cloud RAN (often encompassing vRAN) accounted for approximately 5% to 10% of the total global Radio Access Network (RAN) market revenues in 2025. In early 2026, Dell’Oro revised Cloud RAN projections downward. While virtualization remains a “key pillar” for the long term, short-term adoption is being slowed by performance, power, and cost-parity challenges when compared to purpose-built hardware.

- The total RAN market stabilized in late 2025 after losing approximately 20% of its value between 2022 and 2024. Market concentration reached a 10-year high in 2025, with the top five vendors (Huawei, Ericsson, Nokia, ZTE, and Samsung) capturing 96% of the revenue.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Image Credit: Ericsson

In this proof-of-concept setup, Ericsson’s disaggregated and containerized RAN software operated within AT&T’s target Cloud RAN configuration, built on open, commercial off-the-shelf hardware. The test advanced from basic call functionality to validation of feature-rich network behavior in a cloud computing environment. Ericsson’s AI-native Link Adaptation is a learning algorithm that continuously assesses channel state and interference to determine the optimal modulation and coding scheme for each transmission interval. By generating real-time predictions of link quality, the AI model dynamically adjusts data rates to maximize throughput and spectral efficiency.

Early results were promising. Throughput gains reached up to 20% compared with conventional rule-based link adaptation approaches, alongside measurable improvements in spectral efficiency. Ericsson and Intel also used the trial to benchmark various AI inference models, demonstrating performance scalability and energy efficiency on general-purpose compute nodes rather than proprietary hardware accelerators. This suggests a more pragmatic path for deploying AI workloads across distributed RAN architectures.

AI-native Link Adaptation dynamically adjusts to changes in signal quality and interference, boosting RAN performance on purpose-built and cloud-based infrastructure alike.

Ericsson Cloud RAN is a cloud native software solution that handles compute functionality in the RAN. It virtualizes RAN functions on Commercial Off The Shelf (COTS) hardware, decoupling software from hardware to enable more flexible, scalable, and efficient network deployments.

Engineered specifically for network and edge deployments, Intel Xeon 6 SoC delivers breakthrough AI RAN performance with built-in acceleration. Integrated Intel Advanced Vector Extensions (AVX) and Intel Advanced Matrix Extension (AMX) technologies eliminate the need for discrete accelerators while maximizing capacity, efficiency, and TCO optimization.

Beyond the immediate performance improvements, the trial illustrates how open RAN architectures can accelerate innovation. By decoupling RAN software from vendor-specific hardware, AT&T can integrate AI capabilities and update network functions more quickly, avoiding the constraints of lock-in. The portability demonstrated here—running production-grade Ericsson RAN software on Intel Xeon 6 silicon—marks an industry first.

For AT&T, the achievement represents more than a lab milestone. It provides a technical template for scaling AI-native RAN functions into its cloud infrastructure, pointing to a future where machine learning operates natively within radio environments to fine-tune performance in real time. As operators continue balancing cost, flexibility, and efficiency, AI-optimized Cloud RAN deployments could become the next competitive frontier in 5G—and eventually, 6G—network evolution.

………………………………………………………………………………………………………………………………………………………………………………………………………………………..

Quotes:

Rob Soni, Vice President, RAN Technology at AT&T, says: “AT&T is leading the charge toward an open, intelligent, and scalable network future by advancing Open RAN and Cloud RAN with AI-native capabilities at their core. This demo highlights how AI capabilities, powered by our next-generation Cloud RAN platform, can be deployed seamlessly to drive innovation and deliver superior customer experiences.”

Mårten Lerner, Head of Networks Strategy and Product Management, Business Area Networks at Ericsson, says: “Together with AT&T and Intel, Ericsson is demonstrating how our domain expertise combined with AI-native RAN software can drive transformative advancements in both Cloud RAN and purpose-built deployments. Our industry-leading AI-native Link Adaptation serves as the first proof point on this journey. With a hardware-agnostic RAN software stack, Ericsson is committed to offering maximum flexibility and enabling all our customers to benefit from future innovations – regardless of their chosen underlying hardware. This milestone underscores Ericsson’s commitment to helping operators advance their networks by deploying AI functionality across the RAN stack.”

Cristina Rodriguez, VP and GM, Network and Edge at Intel, says: “This successful collaboration with AT&T and Ericsson showcases the power of Intel Xeon 6 SoC to enable and accelerate AI workloads in Cloud RAN environments. Xeon 6 SoC is architected to handle the demanding compute requirements of AI-native network functions, delivering the performance and efficiency operators need to unlock the full potential of intelligent networks. By providing a flexible, standards-based platform, Intel Xeon 6 enables service providers like AT&T to deploy innovative AI capabilities while maintaining the openness and choice that drive industry innovation.”

………………………………………………………………………………………………………………………………………………………………………………………………………………………….

AI-Native Link Adaptation vs. Traditional Methods:

Traditional link adaptation in RAN relies on deterministic, rule-based algorithms that select the Modulation and Coding Scheme (MCS) from predefined lookup tables. These methods primarily use instantaneous Channel Quality Indicator (CQI) reports or estimated Signal-to-Interference-plus-Noise Ratio (SINR) thresholds, often adjusted via Outer Loop Link Adaptation (OLLA) based on ACK/NACK feedback from the UE. This reactive approach applies conservative margins to account for channel estimation errors, prediction lag, and varying interference, which can lead to suboptimal throughput—either underutilizing the link with low MCS or triggering excess HARQ retransmissions with overly aggressive selections.

AI-native Link Adaptation shifts to a predictive, model-driven paradigm using machine learning (typically lightweight neural networks or time-series models) trained on historical channel data. Rather than static thresholds, the AI processes sequences of CQI, beam metrics, mobility patterns, and interference traces to forecast the probable channel state for the next transmission time interval (TTI). This enables precise MCS selection that hugs the Shannon capacity limit more closely, minimizing BLER while maximizing spectral efficiency in dynamic scenarios like high-mobility NLOS or bursty interference.

Key differences include:

| Aspect | Traditional (Rule-Based) | AI-Native (ML-Based) |

|---|---|---|

| Decision Mechanism | Lookup tables, SINR thresholds, OLLA offsets | Real-time inference from ML models |

| Channel Handling | Reactive (past CQI/SINR) | Predictive (time-series forecasting) |

| Adaptation Speed | Step-wise, with feedback lag | Continuous, sub-TTI granularity |

| Performance Gains | Baseline (0% reference) | Up to 20% throughput, 10% spectral efficiency |

| Compute Needs | Low (fixed arithmetic) | Moderate (edge inference on COTS like Xeon 6) |

| Limitations | Struggles with non-stationary channels | Requires training data, retraining overhead |

Analysis: Rakuten Mobile and Intel partnership to embed AI directly into vRAN

RAN silicon rethink – from purpose built products & ASICs to general purpose processors or GPUs for vRAN & AI RAN

vRAN market disappoints – just like OpenRAN and mobile 5G

Nokia and Eolo deploy 5G SA mmWave “Cloud RAN” network

Ericsson and Google Cloud expand partnership with Cloud RAN solution

Ericsson and O2 Telefónica demo Europe’s 1st Cloud RAN 5G mmWave FWA use case

Cloud RAN with Google Distributed Cloud Edge; Strategy: host network functions of other vendors on Google Cloud

vRAN market disappoints – just like OpenRAN and mobile 5G

Ericsson and Intel collaborate to accelerate AI-Native 6G; other AI-Native 6G advancements at MWC 2026

Ericsson and Intel at MWC 2026:

Building on milestones in Cloud RAN, 5G Core, and open network innovation, Ericsson and Intel are showcasing joint technology advancements at the Mobile World Congress (MWC) 2026 in Barcelona this week. Demonstrations can be experienced at the Ericsson Pavilion (Hall 2), Intel Booth (Hall 3, Stand 3E31), and across partner event spaces, highlighting the companies’ shared progress in enabling the next era of AI-driven networks.

The two companies are strengthening their long-standing technology partnership to accelerate ecosystem readiness for AI-native 6G networks and use cases. The expanded collaboration spans next-generation mobile connectivity, cloud infrastructure, and compute acceleration — with a focus on AI-driven RAN and packet core evolution, platform-level security, and scalable cloud-native architectures designed to shorten time-to-market for advanced network solutions.

“6G is not merely an iteration of mobile technology; it will serve as the foundational infrastructure distributing AI across devices, the edge, and the cloud,” said Börje Ekholm, President and CEO of Ericsson. “With our deep history in network innovation and global-scale operator deployments, Ericsson is uniquely positioned to drive practical 6G integration from research to commercialization.”

Lip-Bu Tan, CEO of Intel, added: “Intel’s vision is to lead the industry in unifying RAN, Core, and edge AI to enable seamless deployment of AI-native 6G environments. Together with Ericsson, we are proving that next-generation connectivity can be open, energy-efficient, secure, and intelligent. With future Ericsson Silicon built on Intel’s most advanced process technologies, coupled with Intel Xeon-powered AI-RAN ready Cloud RAN and collaborative multi-year research efforts, we are delivering the performance, efficiency, and supply assurance demanded by leading operators worldwide.”

As 6G transitions from research to commercialization, the industry must align around a mature, standards-based ecosystem. The Ericsson–Intel collaboration aims to accelerate development of high-performance, energy-efficient compute architectures optimized for both AI for Networks and Networks for AI.

AI-native 6G will fuse intelligent, programmable network functions with distributed compute and real-time sensing, bringing processing power closer to the network edge and enabling ultra-responsive, adaptive services. This convergence will enhance network efficiency, agility, and service intelligence across future deployments.

About Ericsson:

Ericsson‘s high-performing networks provide connectivity for billions of people every day. For 150 years, we’ve been pioneers in creating technology for communication. We offer mobile communication and connectivity solutions for service providers and enterprises. Together with our customers and partners, we make the digital world of tomorrow a reality.

About Intel:

Intel is an industry leader, creating world-changing technology that enables global progress and enriches lives. Inspired by Moore’s Law, we continuously work to advance the design and manufacturing of semiconductors to help address our customers’ greatest challenges. By embedding intelligence in the cloud, network, edge and every kind of computing device, we unleash the potential of data to transform business and society for the better.

…………………………………………………………………………………………………………………………………………………………

Related AI-Native 6G Announcements at MWC 2026: