Tutorial: LEO Satellite Internet connectivity, D2D, and major providers

Satellite Orbits:

Satellite connectivity operates across three orbital tiers:

- Geostationary (GEO) satellites have been the dominant platform for decades, powering telecommunications, TV broadcasting, weather forecasting, military surveillance, rural internet, and satellite phones. Positioned 36,000 kilometres above the equator, a single GEO satellite covers nearly a third of the planet, but the distance creates a 500–700 millisecond signal delay that makes video calls and real-time services impractical. Each satellite is roughly the size of a school bus and requires its own rocket launch.

- Medium Earth Orbit (MEO) satellites sit between 2,000 and 36,000 kilometres above Earth’s surface, with a latency of 70–120 milliseconds. The satellites range from car-sized to van-sized, with a few deployable per launch. MEO satellites are used for GPS and other global navigation systems but have never played a significant role in consumer connectivity.

- Low Earth Orbit (LEO) satellites sit at just 300 to 2,000 kilometres above Earth’s surface, bringing latency down to 20–50 milliseconds — on par with home broadband. Their small, flat-panel design, roughly the size of a dining table, allows dozens to be stacked into a single rocket, significantly lowering the cost per satellite. Modern LEO constellations also link satellites directly via laser, forming a mesh network in space. Instead of every signal bouncing through a fixed ground gateway, data travels between satellites and descends at the nearest point, allowing LEO signals to reach oceans, disaster zones, and remote communities that no ground infrastructure will ever serve.

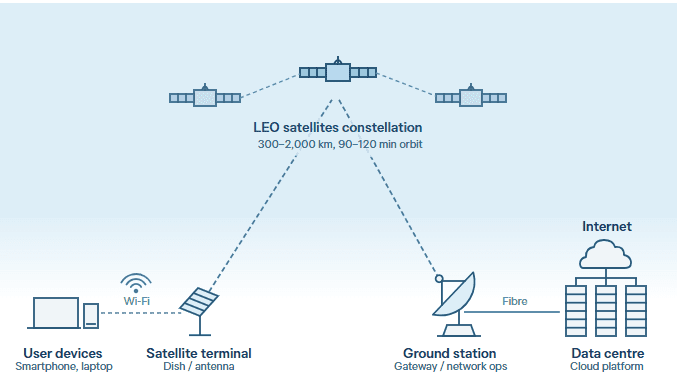

LEO satellites sit between 300 and 2,000 kilometres above Earth, completing an orbit every 90 to 120 minutes and covering different parts of the globe as they move. They communicate with ground stations or through inter-satellite links that relay data between satellites. Supporting infrastructure includes gateway stations, network operation centers, and data centers that manage satellite movements, route traffic, and maintain service reliability. For users, accessing LEO services requires a small satellite terminal — typically a dish — with power and a subscription plan. As shown in the figure below, users connect to a local Wi-Fi network linked to the dish. Data is transmitted to LEO satellites, relayed to a ground station, and then routed through fiber-optic networks to data centers or cloud platforms. The process is reversed for the return signal, completing the connection in milliseconds.

Importantly, LEO satellites are revolutionizing Direct-to-Device (D2D) communications by acting as cell towers in space, allowing standard, unmodified smartphones and IoT sensors to connect seamlessly without terrestrial infrastructure. By utilizing standard mobile-carrier spectrums or dedicated satellite bands, these fast-moving satellites bypass localized coverage gaps to provide ubiquitous, text, voice, and data services in remote, rural, and maritime areas, as well as critical backup during disasters.

LEO satellite internet functional block diagram:

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Regulatory approval is central to LEO satellite deployment. Providers must typically obtain spectrum licenses, comply with national rules for ground infrastructure, and secure approval for service provision. Requirements vary widely across jurisdictions — from registration to multi-stage authorization processes. Competition from incumbent internet service providers may constrain market entry and expansion. As a result, services may be restricted or delayed even where technical coverage exists.

LEO connectivity also has practical limitations. Terminals require an unobstructed view of the sky, making installation easier in open areas but more difficult in dense urban environments where buildings or trees block the signal. Tropical downpours, heavy rain, or storms can cause signal attenuation and reduce throughput. Compared with terrestrial systems such as fibre-optic or mobile networks, LEO services may deliver less consistent performance, particularly in urban areas, and speeds can drop during peak demand.

Providers of LEO satellite connectivity:

The global space economy is projected to reach US$1.8 trillion by 2035, driven largely by LEO constellations. However, value creation is likely to be concentrated among a small number of providers controlling key parts of the value chain, Financial barriers to entry remain significant, varying depending on mission scope and technical ambition. Amazon Leo (formerly Project Kuiper) will cost more than US$10 billion, while full deployment of SpaceX’s Starlink is estimated at US $20–30 billion.

A mix of private and state-backed operators is developing LEO constellations with different strategies in satellite numbers, coverage, and target markets. Chinese-backed LEO operators GuoWang and Qianfan represent a strategic shift, both advancing rapidly towards full operation with a dual mandate of serving domestic communications and extending broadband connectivity across the Indo-Pacific and beyond. Their emergence could reshape strategic choices for governments in the region.

Where LEO satellite delivers:

LEO satellites are not a universal solution to connectivity gaps, nor a replacement for terrestrial networks. In most countries, fibre-optic and mobile infrastructure will remain the primary source of broadband connectivity. Their value lies in specific contexts: serving remote communities beyond the economic reach of terrestrial investment; providing resilient backup when ground networks fail; and supporting connectivity where no viable alternative exists.

LEO satellites are increasingly used to enhance resilience in countries with extensive fiber-optic networks or high exposure to natural disasters. They can provide automatic failover — near instantaneous transition to a standby system — during submarine cable outages, power failures, or other disruptions, maintaining communications and supporting emergency response. In December 2024, earthquakes in Vanuatu disrupted contact with national disaster authorities until Starlink was activated. In April 2025, a blackout in Spain and Portugal cut power to thousands of mobile towers, halving terrestrial network capacity — Starlink maintained connectivity via ground stations in Italy.

The main advantage is network independence: LEO satellites operate separately from terrestrial infrastructure and continue functioning when ground systems fail. Integrating LEO satellites into national disaster frameworks, rather than relying on ad hoc deployment, would maximize resilience.

………………………………………………………………………………………………………………………………………………………………………………………………………………….

References:

https://www.telecoms.com/satellite/satellite-disruption-how-leo-and-d2d-are-impacting-telecoms

Analyst firms wide forecasts for the LEO satellite direct-to-device (D2D) market

Analysis: SpaceX FCC filing to launch up to 1M LEO satellites for solar powered AI data centers in space

Blue Origin announces TeraWave – satellite internet rival for Starlink and Amazon Leo

Open Cosmos introduces global space-based LEO satellite service for IoT monitoring

China ITU filing to put ~200K satellites in low earth orbit while FCC authorizes 7.5K additional Starlink LEO satellites

Amazon Leo (formerly Project Kuiper) unveils satellite broadband for enterprises; Competitive analysis with Starlink

GEO satellite internet from HughesNet and Viasat can’t compete with LEO Starlink in speed or latency